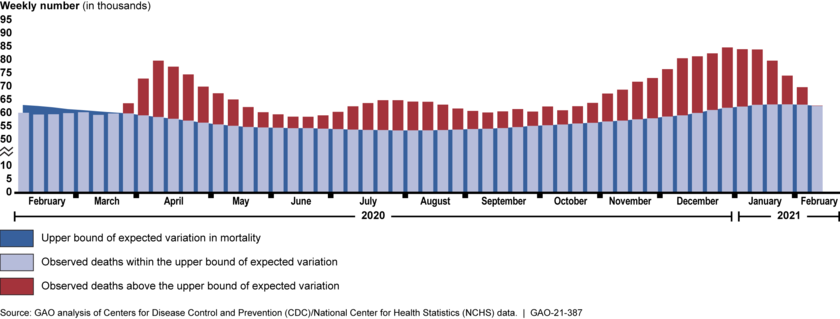

More than a year after the U.S. declared COVID-19 a public health emergency, the pandemic continues to result in catastrophic loss of life and substantial damage to the global economy, stability, and security. According to data from the Centers for Disease Control and Prevention’s (CDC) National Center for Health Statistics, about 520,000 more deaths occurred from all causes (COVID-19 and other causes) than would be normally expected from February 2020 through mid-February 2021, highlighting the effect of the pandemic on U.S. mortality (see figure). The pandemic also continues to cause economic challenges, particularly for the labor market. As of February 2021, there were about 10 million unemployed individuals, compared to nearly 5.8 million at the beginning of 2020.

Higher-Than-Expected Weekly Mortality in the U.S., February 2020 through Mid-February 2021

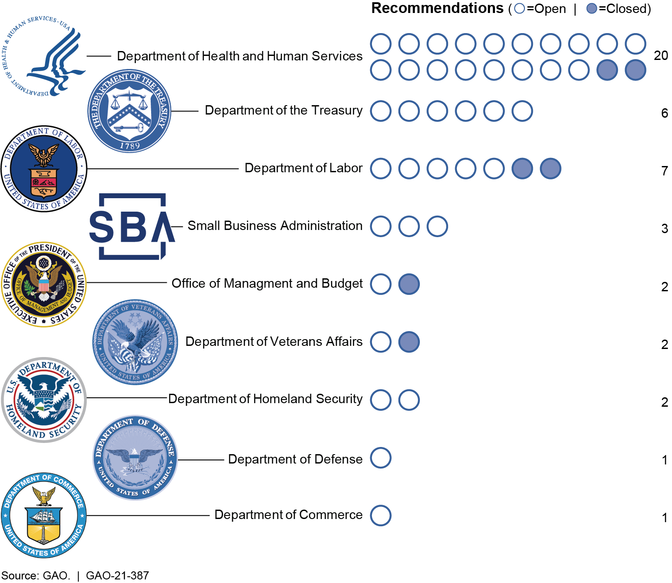

In the past year, GAO has made 44 recommendations for agency actions, 6 of which have been implemented. Since taking office, the new administration has taken some action consistent with GAO’s recommendations, such as issuing the National Strategy for the COVID-19 Response and Pandemic Preparedness and issuing executive orders calling for the development of a pandemic supply chain resilience strategy and providing emergency economic relief. GAO will continue to monitor the administration’s actions toward addressing GAO’s recommendations in future reporting.

In this report GAO is making 28 new recommendations in the areas of public health, the economy, and program integrity. Implementing these 28 recommendations, as well as 38 of GAO’s 44 prior recommendations that have not been fully implemented from CARES Act reports issued since June 2020, would improve the ongoing federal response to COVID-19.

GAO’s new recommendations are discussed below.

Hospital and Pharmacy Perspectives on COVID-19 Vaccine Administration and Medical Supply Availability

In February 2021, GAO surveyed hospitals and interviewed large retail pharmacy chains and an association of independent pharmacies to gain their perspectives on vaccine administration and medical supply availability. Providers expressed concerns about COVID-19 vaccine availability and limitations in the availability of certain key medical supplies for administering the vaccines—notably syringes and needles. For example, representatives from one retail pharmacy chain stated that the chain has the capacity to administer 25 million doses per month at 9,900 locations, but the chain’s initial allocation of vaccines from the federal government was expected to be only 230,000 doses at 250 locations. Several retail pharmacy chain representatives also indicated that limited vaccine availability has led to uncertainty regarding the amount of vaccines their pharmacies can expect to receive each week. The new administration has taken steps to increase certainty and vaccine availability. For example, the White House announced at the end of January 2021 that the federal government would begin notifying states earlier about availability and shipments of vaccines, to give greater certainty for planning vaccination efforts.

Of the 146 surveyed hospitals that plan to or have begun administering COVID-19 vaccines, 40 hospitals reported at the time of GAO’s survey being greatly concerned about having a sufficient quantity of syringes in the next 30 days for vaccine administration following the survey, and 43 hospitals were greatly concerned about having a sufficient quantity of needles. Additionally, shortages of personal protective equipment (PPE) and COVID-19 testing supplies also remain a challenge for some providers. GAO and other entities have documented persistent and evolving supply chain challenges throughout the pandemic, such as shortages of key supplies used for COVID-19 testing. GAO will continue to examine the medical supply chain, including the role of the Strategic National Stockpile, in future reporting, including actions to respond to GAO’s previous recommendations.

Emergency Use Authorizations

Emergency use authorizations (EUA)—which allow for the temporary use of unapproved medical products—have been instrumental in increasing needed supply of certain devices, such as PPE, during the COVID-19 pandemic response (see figure). However, there have been instances of inconsistencies between EUAs issued by the Food and Drug Administration (FDA) and device guidance from CDC and the Department of Labor (DOL), which led to confusion and hesitancy among providers about using such devices, according to provider associations. GAO recommends that FDA, CDC, and DOL work together to develop a process for sharing information to facilitate decision-making and guidance consistency related to devices with EUAs. The Department of Health and Human Services (HHS)—which includes FDA and CDC—and DOL agreed with this recommendation.

Examples of Medical Devices Other Than Tests with Emergency Use Authorizations for COVID-19

In addition, stakeholders—including associations representing manufacturers, distributors, and users of authorized devices, such as health care providers—raised concerns about what will happen to devices with EUAs after the declarations permitting their use for COVID-19 end. HHS has indicated that it intends to develop draft guidance for a transition plan for medical devices distributed under EUAs for COVID-19 by the end of fiscal year 2021. A plan for devices with EUAs that specifies a reasonable timeline and process for transitioning away from their use, taking into account stakeholder input, would help ensure a smooth transition. As HHS develops a transition plan for devices with EUAs, GAO recommends that the agencyspecify a reasonable timeline and process for transitioning authorized devices to clearance, approval, or appropriate disposition that takes into account input from stakeholders. HHS agreed with this recommendation.

COVID-19 Data for Health Care Indicators

Since June 2020, GAO has identified concerns with federal COVID-19 data and underscored that in the midst of a nationwide public health emergency, clear and consistent communication between the federal government and the public is critical given that effective response requires the public’s participation. As part of its efforts to communicate with the public and stakeholders about the pandemic, several experts suggested that the federal government should improve the accessibility of its COVID-19 data by making these data available from a central location on the internet. HHS publishes its data on COVID-19 health indicators across several websites. However, the data it makes publicly available are not all located on, or available from website links on, one online location. As a result, the public, including stakeholders, may not be able to fully understand the extent of the pandemic and use the data to best inform their decision-making.

To make the data more easily accessible, GAO recommends that HHS make its different sources of publicly available COVID-19 data accessible from a centralized location on the internet. HHS neither agreed nor disagreed with this recommendation, but agreed that COVID-19 data should be made accessible to support communication with the public about the pandemic.

COVID-19 Health Disparities

GAO previously reported that communities of color have been disproportionately affected by the pandemic. According to HHS, as of February 8, 2021, data collected from states and jurisdictions on COVID-19 vaccine recipients were missing data on race and ethnicity for almost half of recipients. Without complete information on the race and ethnicity of those vaccinated, HHS may have difficulty determining whether vaccines are distributed equitably to communities of color. GAO recommends that HHS take steps to ensure the complete reporting of race and ethnicity information for recipients of COVID-19 vaccinations. HHS neither agreed nor disagreed with this recommendation.

HHS’s July 2020 COVID-19 Response Health Equity Strategy has a goal to reduce health disparities by using data-driven approaches to attain the highest level of health possible for all individuals, including communities of color. However, the strategy lacks important elements of an effective national strategy. For example, HHS’s strategy does not provide specific actions that the agency will take to determine whether or where it needs to increase access to testing for populations at increased risk for COVID-19—an essential first step before taking steps to increase testing access. GAO recommends that HHS incorporate key elements of a national strategy to implement the agency’s COVID-19 Response Health Equity Strategy, including determining how intermediate outcomes should be prioritized. HHS agreed with this recommendation.

Nursing Homes

Collecting detailed information on vaccinations for nursing home populations is important for tracking and transparency, particularly because nursing homes have been an epicenter of the COVID-19 pandemic and HHS has recommended priority vaccinations for this group. HHS established a pharmacy partnership program for vaccinating staff and residents of long-term care facilities, and publicly reports the number of vaccination doses, by state, provided to residents and staff of all long-term care facilities participating in the program. However, HHS does not report data showing vaccination rates specifically for nursing homes and does not collect or report data for nursing homes not participating in the program. To improve the monitoring and transparency of nursing home vaccination efforts,GAO recommends that HHS collect data specific to COVID-19 vaccination rates in nursing homes and make these data publicly available. HHS neither agreed nor disagreed with this recommendation.

In addition, as of January 2021, HHS had not specified whether nursing homes would be required to offer COVID-19 vaccinations as they have with other vaccines and how these vaccinations would be incorporated into the agency’s nursing home quality strategy. Data on COVID-19 vaccinations in nursing homes will also be important for HHS’s ongoing efforts to monitor nursing home quality. GAO recommends that HHS require nursing homes to offer COVID-19 vaccinations to residents and staff and design and implement associated quality measures. HHS neither agreed nor disagreed with this recommendation.

Veterans Health Care

According to the Department of Veterans Affairs (VA), many veterans enrolled in VA’s health care system are at a higher risk of infection or severe disease from COVID-19 due to their age or underlying health conditions. GAO identified several areas where VA can improve its vaccination efforts:

VA does not have metrics related to staff and veterans who do not show (no-shows) for their vaccination appointments. Without data on no-shows, VA may be at risk for not being able to determine the extent to which staff and veterans are not showing up for appointments for their second vaccinations, and may miss opportunities to better target outreach to individuals not showing up for appointments.

VA lacks targets for when it will move from one vaccination phase to another or within one phase for when the agency will move from one group of veterans to another, making it difficult for the department to assess progress.

VA is utilizing a phased vaccine rollout; however, VA’s current metrics do not capture vaccine data by phases. As a result, VA is not able to determine which facilities may be at an earlier phase than others and direct resources or assistance to those facilities.

GAO recommends that VA (1) collect data on the number of staff and veterans who do not show up for a vaccination appointment to better monitor for completion of the second dose of the vaccine; (2) develop preliminary vaccination targets for when it will move from one vaccination phase to another; or within one phase, from one group of veterans to another; and (3) develop metrics to assess the number of vaccines administered by vaccine rollout phase to better assess progress and make any necessary adjustments. VA agreed with the first and third recommendations and agreed in principle with the second recommendation.

Nutrition Assistance

The U.S. Department of Agriculture (USDA) administers a number of federal nutrition assistance programs to vulnerable populations. Recent legislative and executive actions made several changes to these programs as the negative economic effects of the COVID-19 pandemic have continued. However, until recently, USDA had released minimal data about participation in these programs during the pandemic, and when the department released data in late January 2021, it did not publicly share sufficient information about data quality. In August 2020, USDA announced it had identified significant issues with the quality of state-reported data on two programs. As it worked to identify the root causes of the issues, USDA opted not to release participation data for any of its other nutrition assistance programs from July 2020 until late January 2021. When USDA released the data, the department did not explain how it resolved the data quality issues it previously disclosed, nor did it share necessary context to help stakeholders and the public understand and interpret the data.

As a result, stakeholders and the public lack sufficient information and appropriate context to interpret key program data and understand the effects of the pandemic on the programs. GAO recommends that USDA (1) provide sufficient context to help stakeholders and the public understand and interpret data on federal nutrition assistance programs during the pandemic and (2) disclose potential sources of error that may affect data quality during the pandemic, such as manual processing. USDA generally agreed with these recommendations.

Disaster Relief Fund and Assistance to Tribal Governments

Available data from HHS indicate that tribes are among communities of color bearing a disproportionate burden of COVID-19 positive tests, cases, hospitalizations, and deaths. The Federal Emergency Management Agency (FEMA), within the Department of Homeland Security (DHS), plays a key role in the ongoing COVID-19 pandemic response effort, including using the Disaster Relief Fund to provide Public Assistance grants to reimburse tribal governments, among others, for pandemic costs, such as testing supplies, PPE, and vaccine distribution.

Several tribal organizations reported challenges related to completing administrative requirements to request and receive Public Assistance. For example, two tribal officials told GAO that when requesting technical assistance from FEMA to help with disaster activities such as developing a Public Assistance Administrative Plan, FEMA did not have staff to assist. FEMA’s initial assessment report of its response to the pandemic noted challenges and recommended that FEMA develop a tribal nation engagement strategy that includes providing the resources and personnel throughout each region required to support program delivery for all tribal nations. However, as of March 2021, FEMA had not developed this strategy.

GAO recommends that FEMA provide timely and consistent technical assistance to support tribal governments’ efforts to request and receive Public Assistance as direct recipients, including providing additional personnel, if necessary, to ensure that tribal nations are able to effectively respond to COVID-19. DHS agreed with this recommendation.

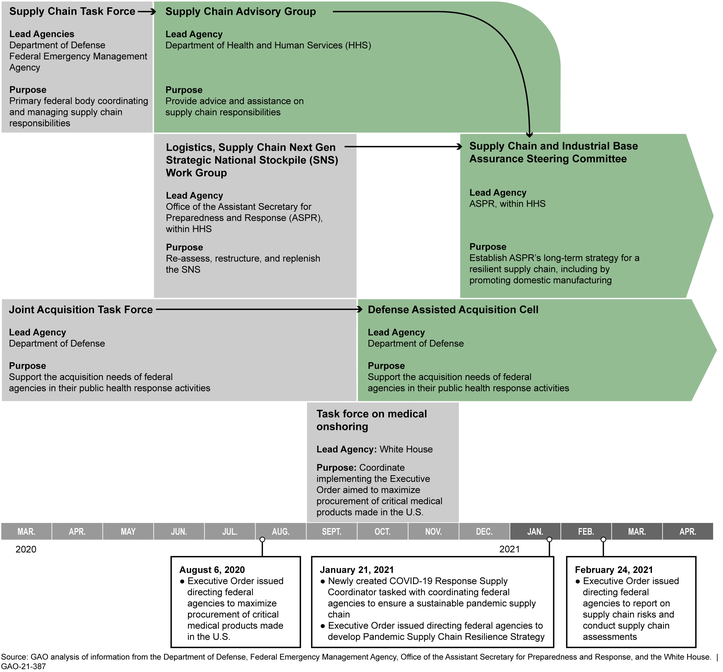

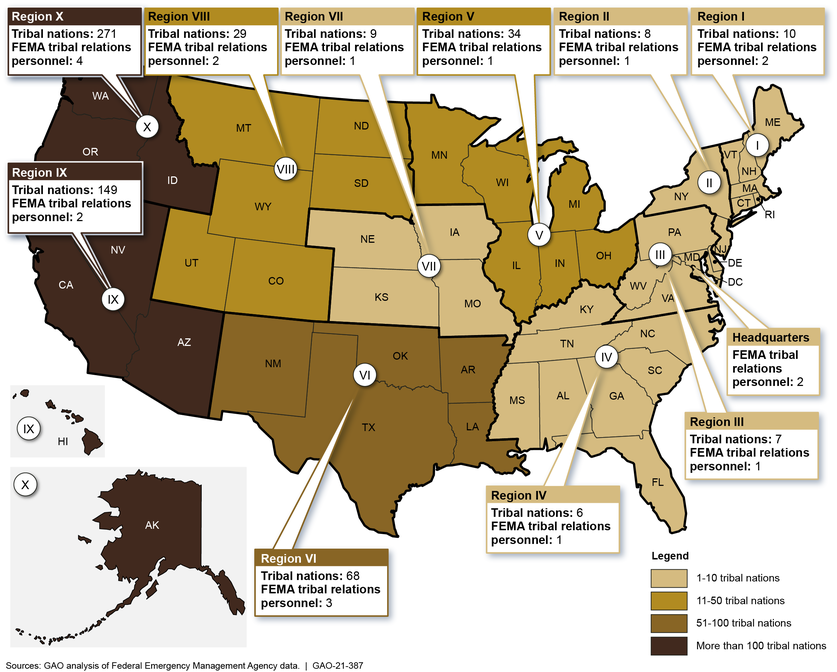

FEMA’s 2019 Tribal Consultation Policy specifies the process for consulting with tribes throughout the four phases that guide the agency in how to conduct regular and meaningful collaboration with tribes (see figure). However, GAO found that FEMA did not follow the tribal consultation process while developing an interim policy detailing eligible items for reimbursement under the Public Assistance program. If tribes had been formally consulted earlier in the process, they could have been in a better position to provide meaningful input to FEMA on how its policy might impact tribes. Further, there may have been less confusion on which items were considered eligible for reimbursement during the early months of the pandemic, and tribes could have made more informed decisions. GAO recommends that FEMA adhere to the agency’s protocols listed in the updated 2019 Tribal Consultation Policy by obtaining tribal input via the four phases of the tribal consultation process when developing new policies and procedures related to COVID-19 assistance. DHS agreed with this recommendation.

Overview of FEMA’s Tribal Consultation Policy Process

K-12 Education

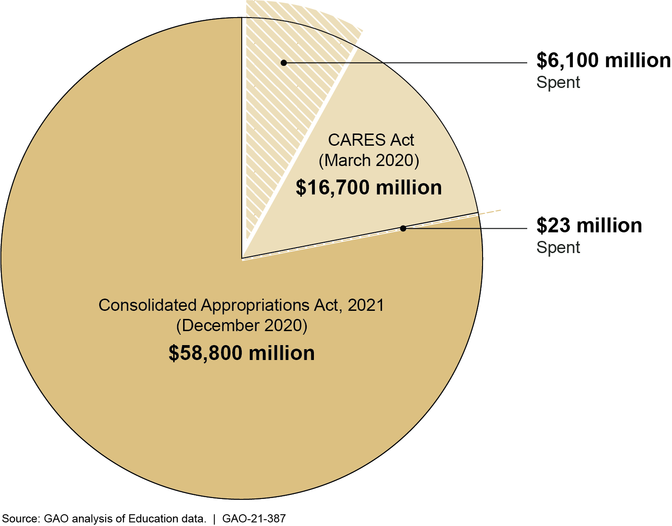

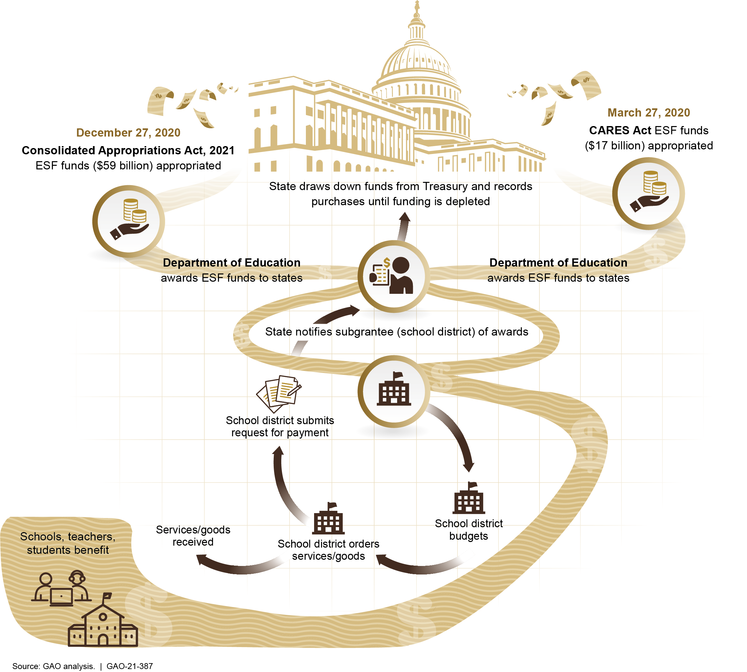

The Department of Education (Education) has taken steps to track state and school district spending of certain COVID-19 relief funds, but the data give an incomplete picture of the status of funds and understate the rate at which funds are being used. According to data collected by Education, as of February 28, 2021, states and territories have spent about $6.1 billion of the approximately $75 billion appropriated through the Education Stabilization Fund for states’ and territories’ education needs. However, federal spending data alone provide an incomplete picture of states’ and school districts’ spending, as there are several factors that influence the rate at which funds appear to be spent. For example, there is often a significant gap between when a district “uses” the funds (i.e., orders, contracts for, installs, and pays for goods or services, such as information technology equipment) and when those funds are reported as “spent” in state and federal reporting systems, as is common in federal grants management processes.

According to Education officials, states award applicable funds to school districts so that the school districts can obligate those funds for specific purposes. The state does not transfer funds to the district until the district requests payment for services or deliverables received. Education officials do not consider the funds spent until the state requests payment for expenses. Given this gap between when a district uses funds and funds are recorded as spent, absent information on obligations, policymakers will not have complete information on how these funds are being used to address the pandemic-related education needs of America’s schoolchildren. GAO recommends that Education regularly collect and publicly report information on school districts’ financial commitments (obligations), as well as outlays (expenditures) in order to more completely reflect the status of their use of federal COVID-19 relief funds. For example, Education could modify its annual report on state and school district spending data to include obligations data in subsequent reporting cycles. Education agreed with this recommendation.

Small Business Assistance Programs

The Consolidated Appropriations Act, 2021, appropriated additional funding for the creation of the Targeted Economic Injury Disaster Loan (EIDL) Advance program and authorized additional Paycheck Protection Program (PPP) loans, among other things, highlighting the continued need for ensuring program integrity. Since March 2020, the Department of Justice has publicly announced charges in numerous fraud-related cases associated with loans made through these programs. As a result of concerns about program integrity, GAO has added Small Business Administration (SBA) loans to GAO’s High Risk List. SBA has taken some steps to mitigate fraud risks to EIDL and PPP, but it has not taken a strategic approach to managing fraud risks to both programs. GAO recommends that SBA (1) implement a comprehensive oversight plan to identify and respond to risk in the EIDL program to ensure program integrity, achieve program effectiveness, and address potential fraud; (2) conduct and document a fraud risk assessment for the EIDL program and PPP; (3) develop a strategy that outlines specific actions to address assessed fraud risks in the EIDL program; and (4) outline specific actions to monitor and manage fraud risks in PPP on a continuous basis. SBA agreed with these recommendations.

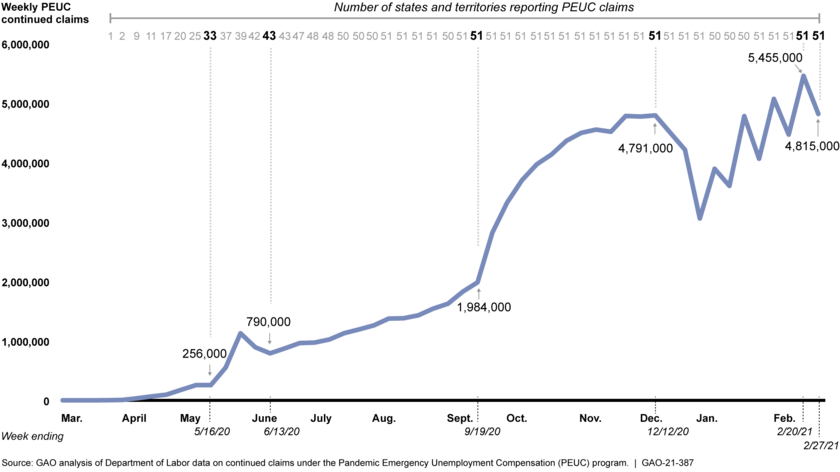

Unemployment Insurance Programs

GAO continues to have concerns about overpayments and potential fraud in the unemployment insurance (UI) system, including the federally funded Pandemic Unemployment Assistance (PUA) program, which authorizes UI benefits to certain individuals not otherwise eligible for these benefits, such as self-employed and certain gig economy workers. As of March 15, 2021, DOL reported that states had identified more than $3.6 billion in PUA overpayments from March 2020 through February 2021. In response to a recommendation in GAO’s January 2021 report, DOL has taken steps to collect data on states’ recovery of PUA overpayments. However, the Consolidated Appropriations Act, 2021, enacted in December 2020, provided states with authority to waive certain PUA overpayments. Thus, additional data on the amounts of PUA overpayments states have waived are also needed to effectively monitor the recovery of overpayments. GAO recommends that DOL collect data from states on the amount of overpayments waived in the PUA program, similar to the regular UI program. DOL agreed with this recommendation.

This report contains additional recommendations related to transparency and accountability in the following areas: relief for health care providers, economic impact payments, federal contracts and agreements, audits of nonfederal entities receiving federal pandemic assistance, and employer tax relief and payroll tax deferrals.

GAO is also examining the federal government’s COVID-19 vaccine efforts, which will be the focus of an upcoming report. Finally, GAO will review actions federal agencies have taken in response to the American Rescue Plan of 2021 in future reporting.

Why GAO Did This Study

As of March 15, 2021, the U.S. had over 29 million reported cases of COVID-19 and more than 523,000 reported deaths, according to CDC. The country also continues to experience serious economic repercussions.

Five relief laws, including the CARES Act, were enacted as of January 31, 2021, to provide appropriations to address the public health and economic threats posed by COVID-19. As of January 31, 2021, of the $3.1 trillion appropriated by these five laws for COVID-19 relief, the federal government had obligated a total of $2.2 trillion and expended $1.9 trillion, as reported by federal agencies.

Most recently, in March 2021, a sixth relief law, the American Rescue Plan of 2021, was enacted and provides additional federal assistance for the ongoing response and recovery.

The CARES Act includes a provision for GAO to report on its ongoing monitoring and oversight efforts related to the COVID-19 pandemic. This report examines the federal government’s continued efforts to respond to and recover from the COVID-19 pandemic.

GAO reviewed data, documents, and guidance from federal agencies about their activities and interviewed federal and state officials, experts, and other stakeholders, including health care professionals.

What GAO Recommends

GAO is making 28 new recommendations for agencies that are detailed in this Highlights and in the report.

Recommendations

Recommendations for Executive Action

Recommendations for Executive Actions

We are making a total of 28 recommendations to federal agencies:

Number

Agency

Recommendation

1

Department of Health and Human Services

The Secretary of Health and Human Services should make the Department’s different sources of publicly available COVID-19 data accessible from a centralized location on the internet. This could improve the federal government’s communication with the public about the ongoing pandemic. See Health Care Indicators enclosure. (Recommendation 1)

2

Department of Health and Human Services

The Secretary of Health and Human Services should finalize and implement a post-payment review process to validate COVID-19 Uninsured Program claims and to help ensure timely identification of improper payments, including those resulting from potential fraudulent activity, and recovery of overpayments. See Relief for Health Care Providers enclosure. (Recommendation 2)

3

Department of Health and Human Services

The Secretary of Health and Human Services should ensure that the Director of the Centers for Disease Control and Prevention collects data specific to the COVID-19 vaccination rates in nursing homes and makes these data publicly available to better ensure transparency and that the necessary information is available to improve ongoing and future vaccination efforts for nursing home residents and staff. See Nursing Homes enclosure. (Recommendation 3)

4

Department of Health and Human Services

The Secretary of Health and Human Services should ensure that the Administrator of the Centers for Medicare & Medicaid Services, in consultation with the Centers for Disease Control and Prevention, requires nursing homes to offer COVID-19 vaccinations to residents and staff and design and implement associated quality measures. See Nursing Homes enclosure. (Recommendation 4)

5

Department of Veterans Affairs : Office of the Under Secretary for Health

The Department of Veterans Affairs Under Secretary for Health should develop metrics to assess the number of vaccines administered by vaccine rollout phase to better assess progress and make any necessary adjustments as needed. See Veterans Health Care enclosure. (Recommendation 5)

6

Department of Veterans Affairs : Office of the Under Secretary for Health

The Department of Veterans Affairs Under Secretary for Health should develop preliminary vaccination targets for when it will move from one vaccination phase to another; or within one phase, from one group of veterans to another. See Veterans Health Care enclosure. (Recommendation 6)

7

Department of Veterans Affairs : Office of the Under Secretary for Health

The Department of Veterans Affairs Under Secretary for Health should collect data on the number of staff and veterans who do not show up for a vaccination appointment to better monitor for completion of the second dose of the vaccine. See Veterans Health Care enclosure. (Recommendation 7)

8

Department of Health and Human Services

The Secretary of Health and Human Services should ensure that the Food and Drug Administration and the Centers for Disease Control and Prevention work with the Assistant Secretary of Labor for Occupational Safety and Health to develop a process for sharing information to facilitate decision-making and guidance consistency related to devices with emergency use authorization. See Emergency Use Authorizations for Medical Devices enclosure. (Recommendation 8)

9

Department of Labor : Occupational Safety and Health Administration

The Assistant Secretary of Labor for Occupational Safety and Health should work with the Food and Drug Administration and the Centers for Disease Control and Prevention to develop a process for sharing information to facilitate decision-making and guidance consistency related to devices with emergency use authorization. See Emergency Use Authorizations for Medical Devices enclosure. (Recommendation 9)

10

Department of Health and Human Services : Food and Drug Administration

As the Food and Drug Administration develops a transition plan for devices with emergency use authorizations, the Commissioner should specify a reasonable timeline and process for transitioning authorized devices to clearance, approval, or appropriate disposition that takes into account input from stakeholders. See Emergency Use Authorizations for Medical Devices enclosure. (Recommendation 10)

11

Department of Health and Human Services : Public Health Service : Centers for Disease Control and Prevention

The Director of the Centers for Disease Control and Prevention should incorporate key elements of a national strategy in the agency’s COVID-19 Response Health Equity Strategy. These elements include (1) specific actions to achieve intermediate outcomes, such as increased access to testing; (2) how intermediate outcomes should be prioritized within its four broad priority areas; (3) who will implement actions to achieve intermediate outcomes; and (4) how the strategy relates to other relevant strategies. See Health Disparities enclosure. (Recommendation 11)

12

Department of Health and Human Services : Public Health Service : Centers for Disease Control and Prevention

The Director of the Centers for Disease Control and Prevention should take steps to ensure more complete reporting of race and ethnicity information for recipients of COVID-19 vaccinations, such as working with states and jurisdictions to facilitate consistent collecting and reporting of this information. See Health Disparities enclosure. (Recommendation 12)

13

Department of Agriculture : Office of the Secretary

The Secretary of Agriculture should direct the Administrator of the Agricultural Marketing Service to issue guidance—such as an acquisition alert or a reminder to contracting officials—on the use of the COVID-19 National Interest Action code for the Farmers to Families Food Box Program or successor food distribution program to ensure it accurately captures COVID-19-related contract obligations in support of the program. See Federal Contracts and Agreements for COVID-19 enclosure. (Recommendation 13)

14

Department of Agriculture : Office of the Secretary

The Secretary of Agriculture should direct the Administrator of the Agricultural Marketing Service to assess the contracting personnel needed to fully execute the award and administration of existing contracts in support of the Farmers to Families Food Box Program or successor future food distribution program, and take the necessary steps to ensure it has adequate contracting staff in place to award and administer any future contracts for the program. See Federal Contracts and Agreements for COVID-19 enclosure. (Recommendation 14)

15

Department of Labor

The Secretary of Labor should ensure the Office of Unemployment Insurance collects data from states on the amount of overpayments waived in the Pandemic Unemployment Assistance program, similar to the regular unemployment insurance program. See Unemployment Insurance Programs enclosure. (Recommendation 15)

16

Department of the Treasury : Internal Revenue Service

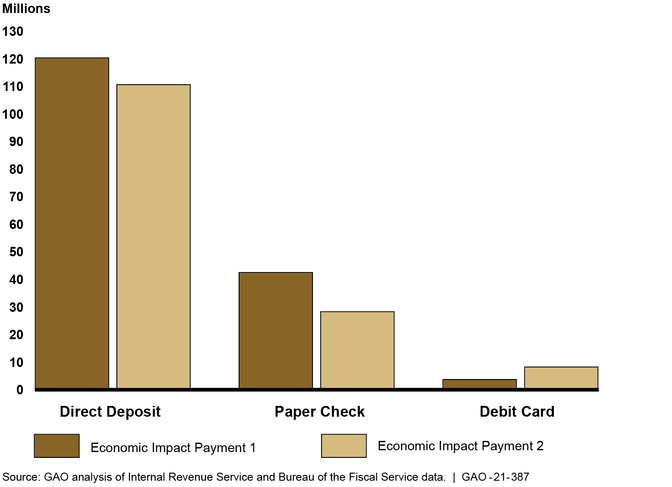

The Commissioner of Internal Revenue should periodically review control activities for issuing direct payments to individuals to determine that the activities are designed and implemented appropriately as IRS disburses a third round of Economic Impact Payments and prepares for advance payments on the Child Tax Credit. These control activities should include appropriate testing procedures, quality assurance reviews, and processes that ensure payments distributed by tax partners reach the intended recipients. See Economic Impact Payments enclosure. (Recommendation 16)

17

Department of Agriculture : Office of the Secretary

The Secretary of Agriculture should ensure that the Administrator of the Food and Nutrition Service (1) provides sufficient context to help stakeholders and the public understand and interpret data on federal nutrition assistance programs during the pandemic and (2) discloses potential sources of error that may affect data quality during the pandemic, such as manual processing. For example, the agency could publish key information from its internal communications plan that it developed for the January 2021 data release and include additional table notes in subsequent data releases to help explain these issues. See Nutrition Assistance enclosure. (Recommendation 17)

18

Department of the Treasury : Internal Revenue Service

The Commissioner of Internal Revenue should leverage employee counts from Form 941, Employer’s Quarterly Federal Tax Return, and Form 943, Employer’s Annual Federal Tax Return for Agricultural Employees, to identify potentially ineligible COVID-19 related sick and family leave credit claims, and address discrepancies the Internal Revenue Service deems significant. See Employer Tax Relief and Payroll Tax Deferrals enclosure. (Recommendation 18)

19

Department of the Treasury : Internal Revenue Service

The Commissioner of Internal Revenue should conduct outreach to employment tax return filers to educate and promote accurate reporting of employee counts on Form 941, Employer’s Quarterly Federal Tax Return, and Form 943, Employer’s Annual Federal Tax Return for Agricultural Employees. See See Employer Tax Relief and Payroll Tax Deferrals enclosure. (Recommendation 19)

20

Small Business Administration

The Administrator of the Small Business Administration should conduct and document a fraud risk assessment for the Economic Injury Disaster Loan program. See Economic Injury Disaster Loan Program enclosure. (Recommendation 20)

21

Small Business Administration

The Administrator of the Small Business Administration should develop a strategy that outlines specific actions to address assessed fraud risks in the Economic Injury Disaster Loan program on a continuous basis. See Economic Injury Disaster Loan Program enclosure. (Recommendation 21)

22

Small Business Administration

The Administrator of the Small Business Administration should implement a comprehensive oversight plan to identify and respond to risks in the Economic Injury Disaster Loan program to help ensure program integrity, achieve program effectiveness, and address potential fraud. See Economic Injury Disaster Loan Program enclosure. (Recommendation 22)

23

Small Business Administration

The Administrator of the Small Business Administration should conduct and document a fraud risk assessment for the Paycheck Protection Program. See Paycheck Protection Program enclosure. (Recommendation 23)

24

Small Business Administration

The Administrator of the Small Business Administration should develop a strategy that outlines specific actions to monitor and manage fraud risks in the Paycheck Protection Program on a continuous basis. See Paycheck Protection Program enclosure. (Recommendation 24)

25

Department of Homeland Security : Directorate of Emergency Preparedness and Response : Federal Emergency Management Agency

The Federal Emergency Management Agency Administrator should adhere to the agency’s protocols listed in its updated 2019 Tribal Consultation Policy by obtaining tribal input via the four phases of the tribal consultation process when developing new policies and procedures related to COVID-19 assistance. See FEMA’s Disaster Relief Fund and Assistance to Tribal Governments enclosure. (Recommendation 25)

26

Department of Homeland Security : Directorate of Emergency Preparedness and Response : Federal Emergency Management Agency

The Federal Emergency Management Agency Administrator should provide timely and consistent technical assistance to support tribal governments’ efforts to request and receive Public Assistance as direct recipients, including providing additional personnel, if necessary, to ensure that tribal nations are able to effectively respond to COVID-19. See FEMA’s Disaster Relief Fund and Assistance to Tribal Governments enclosure. (Recommendation 26)

27

Department of Education : Office of the Secretary

The Secretary of Education should regularly collect and publicly report information on school districts’ financial commitments (obligations), as well as outlays (expenditures) in order to more completely reflect the status of their use of federal COVID-19 relief funds. For example, Education could modify its annual report on state and school district spending data to include obligations data in subsequent reporting cycles. See K-12 Education enclosure. (Recommendation 27)

28

Executive Office of the President : Office of Management and Budget

The Director of the Office of Management and Budget should work in consultation with federal agencies and the audit community (e.g., agency Offices of Inspector General; National Association of State Auditors, Comptrollers, and Treasurers; and American Institute of Certified Public Accountants), to the extent practicable, to incorporate appropriate measures in the Office of Management and Budget’s process for preparing single audit guidance, including the annual Single Audit Compliance Supplement, to better ensure that such guidance is issued in a timely manner and is responsive to users’ input and needs. See Single Audits enclosure. (Recommendation 28)

More than a year after the Secretary of Health and Human Services first declared a public health emergency for the U.S. and the World Health Organization characterized the Coronavirus Disease 2019 (COVID-19) as a pandemic, COVID-19 continues to result in catastrophic loss of life and substantial damage to the global economy, stability, and security.[1] Worldwide, as of March 15, 2021, there were more than 119,452,000 reported cases and about 2,648,000 reported deaths due to COVID-19; within the U.S., there were about 29,270,000 reported cases and more than 523,000 reported deaths.[2]

The country also continues to experience serious economic repercussions and turmoil as a result of the pandemic. As of February 2021, there were about 10 million unemployed individuals, compared to nearly 5.8 million individuals at the beginning of 2020.[3]

In March 2020, Congress took action in response to this unprecedented global crisis to protect the health and well-being of Americans. Notably, Congress passed, and the President signed into law, the CARES Act, which provided over $2 trillion in emergency assistance and health care response for individuals, families, and businesses affected by COVID-19.[4] Over the past year, agencies from across the federal government have demonstrated extraordinary dedication and commitment to responding to the unprecedented COVID-19 pandemic, including those serving on the front lines to establish and sustain services for those infected with the virus.

Since the enactment of the CARES Act—which includes a provision for GAO to report bimonthly on its ongoing efforts related to the pandemic—we have continued to monitor and oversee the federal government’s efforts to prepare for, respond to, and recover from the COVID-19 pandemic.[5] To date, we have issued six reports in response to this provision, made 44 recommendations to federal agencies, and raised four matters for congressional consideration to improve the federal government’s response efforts.[6]

Since taking office, the new administration has taken some action consistent with our recommendations, such as issuing the National Strategy for the COVID-19 Response and Pandemic Preparedness and issuing executive orders calling for the development of a pandemic supply chain resilience strategy and providing emergency economic relief. We will continue to monitor the administration’s actions towards addressing our recommendations in future reporting. Agencies should swiftly take action on the 38 prior recommendations that have not been fully implemented from our CARES Act reports issued since June 2020, including those on topics such as addressing potential fraud, developing national testing and vaccine strategies, and providing clear and consistent communication.

We are also examining the federal government’s COVID-19 vaccine efforts, which will be the focus of an upcoming report. In addition, we have issued other targeted COVID-19-related report in areas such as Federal Reserve lending programs supported by CARES Act funds, the Defense Production Act, and the CARES Act loan program for aviation and other eligible businesses, and we have reviews ongoing in these and other areas.[7] Additionally, we will review actions federal agencies have taken in response to the American Rescue Plan of 2021 in future reporting.

This report examines the federal government’s continued efforts to respond to and recover from the COVID-19 pandemic. We make 28 new recommendations to federal agencies in areas including relief for health care providers, veterans’ health care, nursing homes, federal contracts and agreements for the COVID-19 response, the Paycheck Protection Program, and unemployment insurance programs.

This report also includes 46 enclosures about a range of federal programs and activities across the government concerning public health and the economy. (See Appendix I) Figure 1 lists these enclosures by topic area and highlights those with new recommendations.

Figure 1: Report Enclosures by Topic Area

Given the government-wide scope of this report, we undertook a variety of methodologies to complete our work, including examining a wide range of data sources and conducting interviews with federal and state officials and representatives from stakeholder groups including health care professionals and other entities. Among other things, we examined federal laws, agency documents, and guidance. In each enclosure, we include a summary of the methodology specific to the work conducted.

See Appendix II for a list of ongoing GAO work related to COVID-19 and Appendix III for the status of matters for congressional consideration and recommendations for executive action made in our June, September, November 2020, and January 2021 CARES Act reports and in our November 2020 report on vaccines and therapeutics.

We conducted this performance audit from October 2020 to March 2021 in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

The number of new reported COVID-19 cases reached a high in January 2021 and decreased considerably in February. Between February 25 and March 10, 2021, new reported COVID-19 cases averaged about 65,000 per day, which was about a quarter of the peak that occurred during the winter of 2021 and similar to the peak that occurred during the summer of 2020 (see fig. 2).[8] During this same 2-week period, reported new COVID-19 cases per day, on average, increased in 5 jurisdictions, held steady in 18 jurisdictions, and decreased in 28 jurisdictions.[9]

The need to remain vigilant in efforts to contain the spread of the virus is underscored by the emergence of new variants of the virus, the fragmented nature of our public health sector, the fragility of our medical supply chain, and longstanding disparities in health care access, treatment, and outcomes. The virus also continues to be an obstacle to a more robust economic recovery.

Figure 2: Reported COVID-19 Cases per Day in the U.S., through March 10, 2021

Note: Reported COVID-19 cases include confirmed and probable cases. Beginning April 14, 2020, states could include probable as well as confirmed COVID-19 cases in their reports to CDC. Prior to that time, counts only included confirmed cases. According to CDC, the actual number of cases is unknown for a variety of reasons, including that people who have been infected may not have been tested or may have not sought medical care. The data were accessed on March 15, 2021.

According to data from the Centers for Disease Control and Prevention’s (CDC) National Center for Health Statistics, about 520,000 more deaths occurred from all causes (COVID-19 and other causes) than would be normally expected from February 2020 through mid-February 2021, highlighting the effect of the pandemic on U.S. mortality (see fig. 3).

Figure 3: Higher-Than-Expected Weekly Mortality, February 2020 through mid-February 2021

Note: The figure shows the number of deaths from all causes in a given week through February 13, 2021, reported in the U.S. that exceeded the upper bound threshold of expected deaths calculated by CDC’s National Center for Health Statistics on the basis of variation in mortality experienced in prior years. See CDC’s National Center for Health Statistics webpage on excess deaths for further details on how CDC estimates this upper bound threshold: https://www.cdc.gov/nchs/nvss/vsrr/covid19/excess_deaths.htm, accessed on March 15, 2021. The number of deaths in recent weeks should be interpreted cautiously as this figure relies on provisional data that are generally less complete.

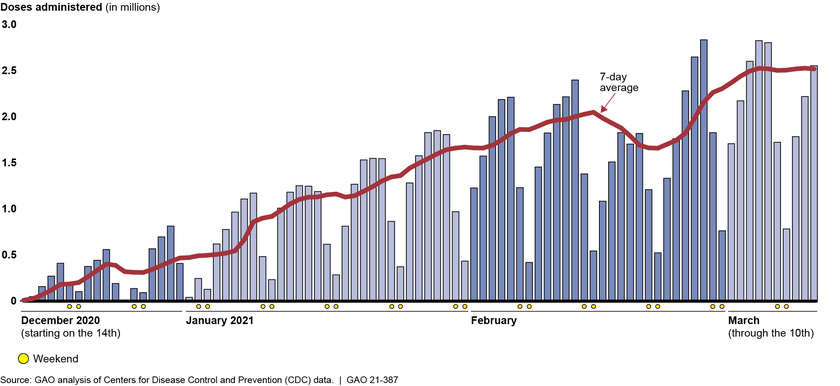

Providing the public with safe and effective vaccines to protect people from getting sick with COVID-19 is crucial to mitigating the public health and economic impacts of the virus and ending the pandemic. It is also a time-sensitive undertaking, with over 6 million cases of COVID-19 and 95,704 deaths reported in the United States in the month of January 2021 alone. Two, two-dose COVID-19 vaccines were authorized for emergency use in December 2020 and a third, one-dose vaccine was authorized in February 2021.[10] Doses of COVID-19 vaccine administered each day have steadily increased from December 14, 2020 through March 10, 2021, with a temporary dip in February due to severe weather across the country (see fig. 4). As of March 15, 2021, about 109,082,000 doses had been administered, according to CDC.

Figure 4: Daily Count of Doses of COVID-19 Vaccine Administered and Reported to CDC, through March 10 2021

Note: Data show the number of COVID-19 vaccine doses administered in the U.S. as reported to CDC by state, territorial, and local public health agencies, and federal entities, since the national vaccine program began on December 14, 2020, and include doses administered through all vaccine partners including jurisdictional partner clinics, retail pharmacies, long-term care facilities, Federal Emergency Management Agency and Health Resources and Services Administration partner sites, and federal entity facilities. The data were accessed on March 15, 2021. As of March 15, 2021, three COVID-19 vaccines were authorized for emergency use; two of these vaccines are two-dose regimens and the third vaccine requires one dose. The number of doses administered on a given day may be affected by several factors, such as weekend days, holidays, weather, and vaccine availability. On February 19, 2021, officials from the White House COVID-19 Response Team said in a press briefing that severe weather across the country impacted vaccine distribution and administration in all 50 states. Further, officials said the shipment of 3 days’ worth—about 6 million doses—of vaccines was delayed due to weather.

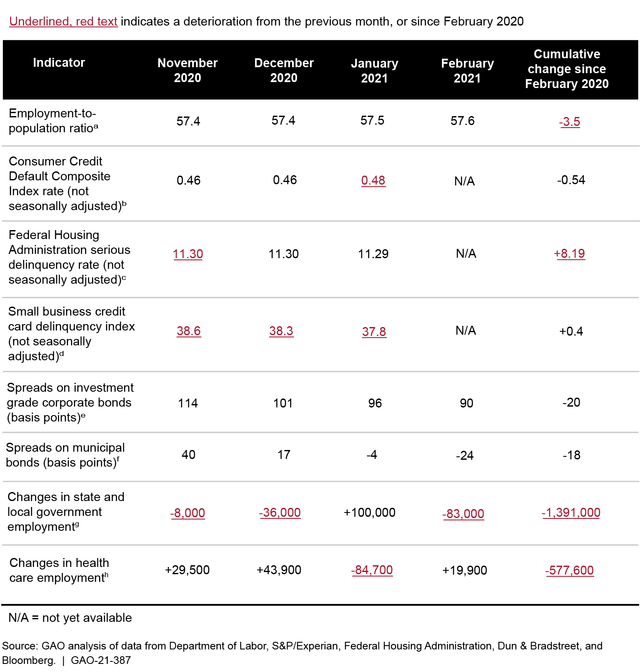

In addition to the public health effects, the pandemic continues to cause economic challenges, particularly for the labor market. For example, in February 2021, the employment-to-population ratio, which measures the share of the population employed, was 3.5 percentage points lower than in February 2020, indicating that labor market conditions remain worse than in the pre-pandemic period (see fig. 5).[11]

Figure 5: Employment Remains below Its Pre-pandemic Level, as of February 2021

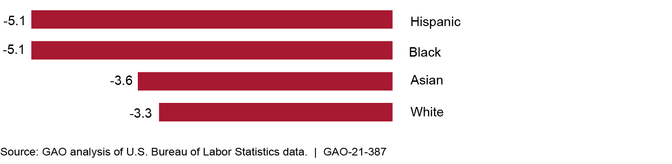

The pandemic has affected some sectors of the economy much more than others. In particular, sectors like leisure and hospitality, mining and logging, and education have seen the largest losses in employment during the pandemic. Importantly, individuals working in the leisure and hospitality sector historically have had the lowest average earnings among sectors and, moreover, during the pandemic have seen the most significant job losses, and many low-wage workers remained out of work as of February 2021 (see fig. 6).

Figure 6: Percentage Change in Employment by Sector, February 2020–February 2021

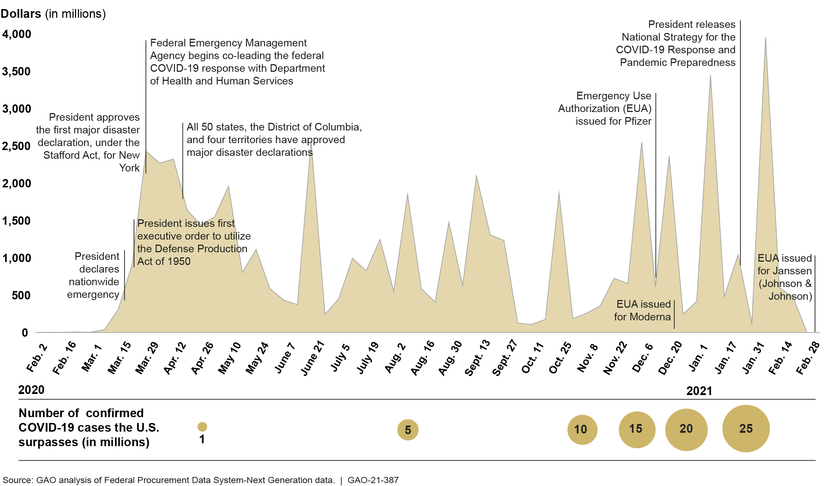

In response to the far-reaching public health and economic crises, Congress has passed, and the President has signed, legislation to fund recovery efforts for COVID-19 (COVID-19 relief laws). Figure 7 shows the COVID-19 relief laws enacted from March 2020 through March 11, 2021.

Figure 7: COVID-19 Relief Laws Enacted, as of March 11, 2021

Note: The figure shows selected COVID-19-related federal legislation. It does not show all of the COVID-19-related actions taken by Congress and the administration. Additional federal actions, such as the enactment of legislation providing limited and targeted relief to certain individuals and presidential actions authorizing federal support for states and individuals, also occurred during this time frame. Amounts for the first five COVID-19 relief laws are based on appropriation warrant information provided by the Department of the Treasury (Treasury) as of January 31, 2021. These amounts have increased over time and could increase in the future for programs with indefinite appropriations, which are appropriations that, at the time of enactment, are for an unspecified amount. The amount for the American Rescue Plan Act of 2021 is based on estimates made by the Congressional Budget Office.aThe Coronavirus Preparedness and Response Supplemental Appropriations Act, 2020, provided $7.8 billion to agencies for health emergency prevention, preparedness, and response activities related to COVID-19, with the Department of Health and Human Services receiving a majority of the funds. Pub. L. No. 116-123, 134 Stat. 146.bThe Families First Coronavirus Response Act provided supplemental appropriations for nutrition assistance programs and public health services and authorized the Internal Revenue Service to provide tax credits for paid emergency sick leave and expanded family medical leave that the act required certain employers to provide. In addition, the act provided states with flexibility to temporarily modify provisions of their unemployment insurance laws and policies related to certain eligibility requirements and provided additional federal financial support to the states. Pub. L. No. 116-127, 134 Stat. 178 (2020).cThe CARES Act provided supplemental appropriations for federal agencies to respond to COVID-19. In addition, it also funded various loans, grants, and other forms of assistance for businesses, industries, states, local governments, and hospitals; provided tax rebates for certain individuals; temporarily expanded unemployment benefits; and suspended payments and interest on federal student loans. Pub. L. No. 116-136, 134 Stat. 281 (2020). dThe Paycheck Protection Program and Health Care Enhancement Act provided additional appropriations for small business loans, grants to health care providers, and COVID-19 testing. Pub. L. No. 116-139, 134 Stat. 620 (2020).eThe Consolidated Appropriations Act, 2021, expanded or extended several CARES Act programs, including unemployment insurance programs, economic impact payments, and Paycheck Protection Program loans, and rescinded unobligated funds for certain programs. Pub. L. No. 116-260, 134 Stat. 1182 (2020). As of January 31, 2021, Treasury issued about $948.0 billion in warrants for appropriations for COVID-19 relief. In addition, approximately $478.8 billion from Treasury’s Economic Stabilization and Assistance to Distressed Sectors programs and $146.5 billion from the Small Business Administration’s Business Loans Program was rescinded, in response to the Consolidated Appropriations Act, 2021.fThe American Rescue Plan Act of 2021 provided additional relief to address the continued impact of COVID-19 on the economy, public health, state and local governments, individuals, and businesses. The Congressional Budget Office estimates the budgetary effects of the law to be $1.9 trillion. Pub. L. No. 117-2, 135 Stat. 4.

As of January 31, 2021, about $3.1 trillion had been appropriated to fund response and recovery efforts for—as well as to mitigate the public health, economic, and homeland security effects of—COVID-19.[12] As of January 31, 2021, the most recent date for which government-wide information was available at the time of our analysis, the federal government had obligated a total of $2.2 trillion and expended $1.9 trillion of the COVID-19 relief funds as reported by federal agencies to the Department of the Treasury’s (Treasury) Governmentwide Treasury Account Symbol Adjusted Trial Balance System (GTAS).[13]

Eight spending areas—the Business Loan Programs, unemployment insurance, economic impact payments, Public Health and Social Services Emergency Fund, Coronavirus Relief Fund, Education Stabilization Fund, Disaster Loans Programs, and Economic Stabilization and Assistance to Distressed Sectors programs—represent $2.6 trillion, or 84 percent, of the total amounts appropriated.[14] For these eight largest spending areas, agencies reported obligations totaling $2.0 trillion and expenditures totaling $1.7 trillion as of January 31, 2021. Table 1 provides additional details on appropriations, obligations, and expenditures of government-wide COVID-19 relief funds, including the eight largest spending areas.

Table 1: COVID-19 Relief Appropriations, Obligations, and Expenditures, as of January 31, 2021

Major spending area

Total appropriationsa ($ billions)

Total obligationsb ($ billions)

Total expendituresb ($ billions)

Business Loan Programs (Small Business Administration)

830.7c

611.3

538.1d

Unemployment Insurance (Department of Labor)

651.8

437.8

424.1

Economic Impact Payments (Department of the Treasury)

455.3

415.0

415.0

Public Health and Social Services Emergency Fund (Department of Health and Human Services)

280.0

195.0

133.9

Coronavirus Relief Fund (Department of the Treasury)

150.0

150.0

149.5

Education Stabilization Fund (Department of Education)

112.6

100.0

16.6

Disaster Loans Programs (Small Business Administration)

50.6

26.4

24.7d

Economic Stabilization and Assistance to Distressed Sectors (Department of the Treasury)

21.2e

21.1

19.5d

Other Areas

504.3

216.4

194.9

Totalf

3,056.6

2,172.9

1,916.2

Source: GAO analysis of data from the Department of the Treasury and applicable agencies. | GAO-21-387

aCOVID-19 relief appropriations reflect amounts appropriated under the Consolidated Appropriations Act, 2021, Pub. L. No. 116-260, 134 Stat. 1182 (2020); Paycheck Protection Program and Health Care Enhancement Act, Pub. L. No. 116-139, 134 Stat. 620 (2020); CARES Act, Pub. L. No. 116-136, 134 Stat. 281 (2020); Families First Coronavirus Response Act, Pub. L. No. 116-127, 134 Stat. 178 (2020); and Coronavirus Preparedness and Response Supplemental Appropriations Act, 2020, Pub. L. No. 116-123, 134 Stat. 146. These amounts are based on appropriation warrant information provided by the Department of the Treasury as of January 31, 2021. These amounts have increased over time and could increase in the future for programs with indefinite appropriations, which are appropriations that, at the time of enactment, are for an unspecified amount. In addition, this table does not represent transfers of funds that federal agencies may make between appropriation accounts or transfers of funds they may make to other agencies. bObligation and expenditure data are based on data reported by applicable agencies. cThe Consolidated Appropriations Act, 2021, rescinded $146.5 billion from the Small Business Administration’s Business Loans Programs. dThese expenditures relate mostly to the loan subsidy costs (the loan’s estimated long-term costs to the U.S. government). eEconomic Stabilization and Assistance to Distressed Sectors programs received $500 billion in appropriations from the CARES Act, approximately $478.8 billion was rescinded in response to the Consolidated Appropriations Act, 2021. fThe sum of amounts may not agree due to rounding.

Throughout our reporting in response to the CARES Act, we have identified and continued to reinforce the importance of key principles that are essential for an effective federal response based on our prior work examining responses to public health and fiscal emergencies. Specifically, federal agencies should

coordinate, establish, and define roles and responsibilities among those responding to the crisis;

provide clear, consistent communication;

collect and analyze data to inform decision-making and future preparedness;

establish clear goals; and

establish mechanisms for accountability and transparency to help ensure program integrity and address fraud risks.

As the nation enters the second year of the COVID-19 pandemic, these principles remain important factors in the federal response to the crisis and a focus of our oversight. In our 2021 High-Risk report, we added Small Business Administration (SBA) loans to our High-Risk List because of concerns about program integrity.[15] In addition, in that report, we discuss other important challenges facing our nation that merit continuing close attention as emerging issues of concern, including Department of Health and Human Services’ (HHS) leadership and coordination of public health emergencies. We will determine whether the leadership and coordination issue should be added to the High-Risk List once we have completed ongoing and planned work in this area.

In this report we are making 28 new recommendations across the federal government in the areas of public health and the economy. As Congress and the administration carry out plans for the federal government’s ongoing COVID-19 response, we urge action on these 28 recommendations, as well as 38 of our 44 prior recommendations that have not been fully implemented from six CARES Act reports. For a summary and the status of all prior recommendations from these reports, see Appendix III.

Hospital and Pharmacy Perspectives on COVID-19 Vaccine Administration and Medical Supply Availability

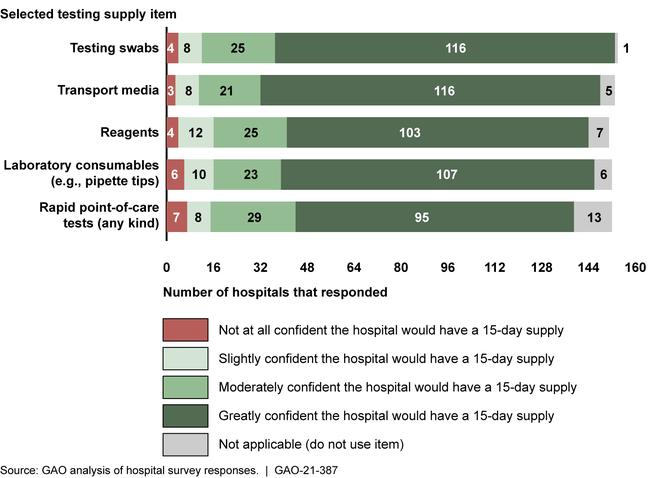

In February 2021, we surveyed 383 hospitals and interviewed nine large retail pharmacy chains and an association of independent pharmacies to gain their perspectives on vaccine administration and medical supply availability. Providers expressed concerns about COVID-19 vaccine availability and limitations in certain key medical supplies for administering the vaccines—notably syringes and needles. Reported concerns included the following.

Vaccine availability. Of the 166 total hospitals that responded to our survey, 102 (61 percent) reported not having sufficient information to respond to questions from their staff, the public, and others about vaccine availability. In addition, 35 hospitals (21 percent) described concerns with general vaccine availability in open-ended survey responses. Similarly, our interviews with officials representing retail pharmacy chains and an association of independent pharmacies also revealed concerns about vaccine availability. For example, representatives from one retail pharmacy chain stated that the chain has the capacity to administer 25 million doses per month at 9,900 locations, but the chain’s initial allocation of vaccines from the federal government was expected to be only 230,000 doses at 250 locations.

Several retail pharmacy chain representatives also indicated that limited vaccine availability has led to uncertainty regarding the amount of vaccines their pharmacies can expect to receive each week. The new administration has taken steps to increase certainty and vaccine availability. For example, the White House announced at the end of January 2021 that the federal government would begin notifying states earlier about availability and shipments of vaccines, to give greater certainty for planning vaccination efforts.

Availability of syringes and needles. Out of the 146 hospitals that reported they have either begun administering COVID-19 vaccines or plan to do so, 40 hospitals (27 percent) reported being greatly concerned about having a sufficient quantity of syringes in the next 30 days, and 43 hospitals (29 percent) were greatly concerned about having a sufficient quantity of needles.

Capacity to administer COVID-19 vaccines. In addition to supplies, administering vaccines requires managing vaccine orders as well as having additional storage, staff, and information technology system capacity. Some of the most commonly cited concerns include having the ability to track the expected arrival of vaccine orders, having a sufficient number of trained providers to administer vaccines, and storing vaccines in ultra-cold storage.

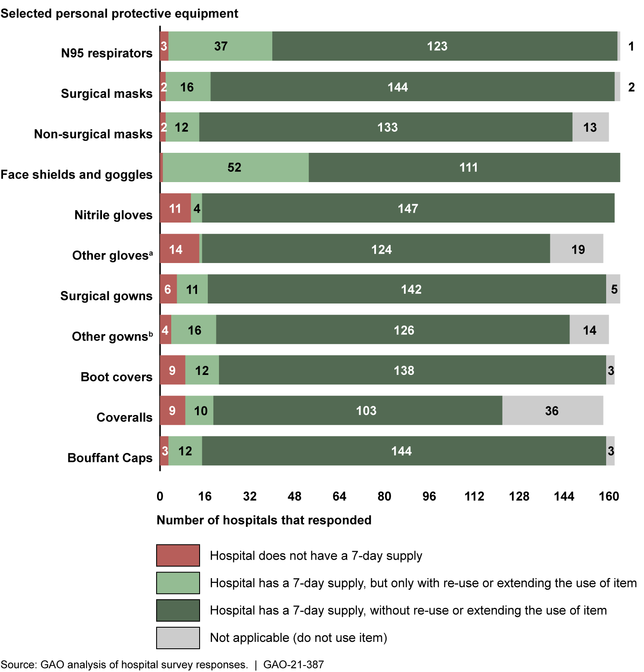

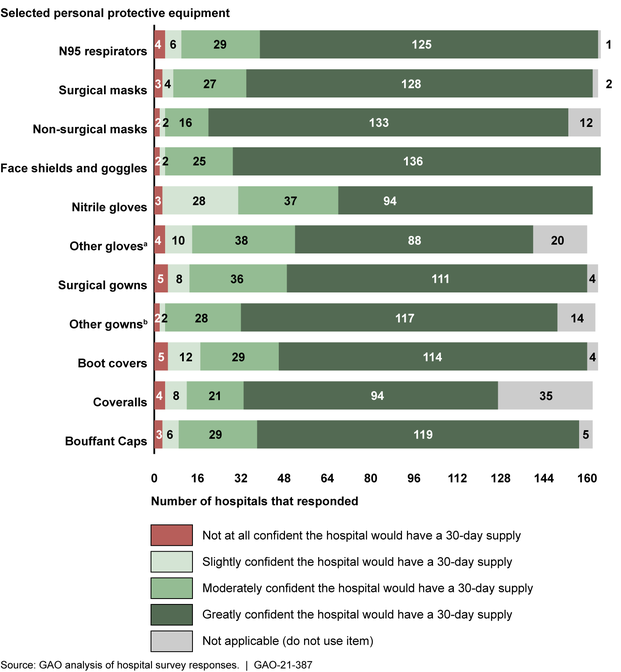

Shortages of personal protective equipment (PPE) and COVID-19 testing supplies also remain a challenge for some providers.

PPE supply. Most of the 166 hospitals that responded to our survey reported having an adequate 7-day supply of the 11 types of PPE we asked about in our survey. However, in some cases, hospitals reported avoiding shortages only with reuse or extending the use of the items. For example, 37 hospitals (23 percent) reported needing to reuse or extend the use of N95 respirators in order to have a 7-day supply. Representatives from all nine retail pharmacy chains reported being confident or very confident their pharmacies could access 30 days or more of PPE, and independent pharmacies generally reported sufficient access. See our enclosure on the Strategic National Stockpile and the Medical Supply Chain in appendix I for additional information and recommendations related to the medical supply chain.

Testing supplies. Most of the surveyed hospitals conducting COVID-19 diagnostic testing reported having at least a 7-day supply of testing supplies we asked about in our survey. However, hospitals were somewhat less confident about levels of those same supplies over the next 15 days. Representatives of the retail pharmacy chains and independent pharmacies that conduct COVID-19 testing did not report current problems accessing testing supplies. See our enclosure on Funding for COVID-19 Testing in appendix I for more information on testing issues.

Along with other entities, we have documented persistent and evolving supply chain challenges throughout the pandemic, such as shortages of key supplies used for COVID-19 testing. We will continue to examine the medical supply chain, including the role of the Strategic National Stockpile, in future reporting.

The Strategic National Stockpile (SNS), overseen by HHS, is a federal stockpile of vaccines, pharmaceuticals, and medical supplies and devices designed to be deployed to support the response to a public health emergency.[16] The near depletion of the SNS early in the COVID-19 response raised questions among the state officials and experts we interviewed about the role and expectations of the SNS during a nationwide pandemic. However, HHS officials told us that the SNS was not designed to provide states with supplies for a prolonged nationwide event such as the COVID-19 pandemic; it is primarily designed to respond to discrete and localized events.

Over the course of our CARES Act work, we have reported on efforts to modernize and restructure the SNS, including progress toward building a 90-day supply of certain key types of PPE, including eye protection or face shields, gowns, gloves, and N95 respirators, in order to respond to future surges in COVID-19 cases. According to HHS officials, they were aiming to meet their 90-day targets of certain PPE by the end of 2020; however, they also noted that they had to balance replenishing the stockpile with ensuring adequate commercial availability. As such, HHS reported delayed delivery of some items to the SNS to enable manufacturers to make them available in the commercial market to alleviate supply constraints. According to HHS data from February 2021, the SNS has reached, or almost reached, its 90-day targets for N95 respirators, surgical or procedural masks, and eye protection or face shields. However, supplies of gloves and gowns or coveralls remain far from their 90-day targets.

As we reported in January 2021, reexamining the role of the SNS in the U.S. response to pandemics will require difficult policy decisions and trade-offs about systems, budgets, and authorities. Stockpiling the SNS for the near term could help address the challenges faced at the beginning of the pandemic response, including the quality and quantity of supplies provided, and allow for more targeted allocation strategies. However, HHS officials were uncertain whether they would maintain the current 90-day target supply levels beyond the COVID-19 response.

In January 2021, the President signed an Executive Order calling for the development of a pandemic supply chain resilience strategy to design, build, and sustain a long-term capability to manufacture medical supplies for future pandemics and biological threats.[17] Per the order, this strategy is to include the role of the SNS in (1) providing and allocating supplies across state, local, tribal, and territorial governments, (2) sustaining supplies during a pandemic, and (3) contingency planning, among other things, within 180 days.[18] As we previously recommended, a process for regularly engaging with Congress and stakeholders in the development and implementation of a medical supply chain strategy to enhance pandemic response capabilities—to include the role of the SNS—would help guide this complex transformation.

Additionally, the Consolidated Appropriations Act, 2021, included a provision requiring the President to make publicly available a report containing a whole-of-government plan for effective response to subsequent COVID-19 outbreaks and for future global pandemic diseases.[19] The act stipulates that this pandemic plan should address how to improve the role of the federal government with respect to the regulation, acquisition, and disbursement of medical supplies necessary to respond to COVID-19 as well as the procurement and distribution of PPE, among other things. See the Strategic National Stockpile and the Medical Supply Chain enclosure in appendix I for additional information.

Funding for COVID-19 Testing

Diagnostic testing for COVID-19 is critical to controlling and understanding the spread of the virus, according to HHS. Overall, HHS reported total testing-specific obligations of about $42.9 billion as of February 28, 2021. A majority of this funding was obligated to states, localities, territories, and tribal organizations, but funding was also used by HHS agencies for testing-related activities, such as procurement of testing supplies and funding for testing for the uninsured.

Officials from all nine selected jurisdictions we spoke with in January 2021 told us that they had sufficient funding to meet their immediate testing goals.[20] While it appears as though a relatively small percentage (about 7 percent) of the federal testing funding obligated for state, local, and territorial jurisdictions has been expended, we found this is due, in part, to funding availability time frames. For example, officials from six of nine selected jurisdictions told us they or their members prioritized spending federal funds whose availability ended earliest. However, more than half of selected jurisdictions told us they had concerns about maintaining testing capacity and preparedness in the longer term. While the supplemental funding has helped jurisdictions address needs to respond to the pandemic in the short term, most jurisdictions interviewed for this report had concerns about future testing and related preparedness. The American Rescue Plan of 2021, enacted on March 11, 2021, includes funding for implementation of a national testing strategy, manufacturing and procurement of tests, and assistance to state, local, and territorial health departments.[21] The additional assistance may help ameliorate concerns about the sufficiency of funding for COVID-19 testing in the longer term. See the Funding for COVID-19 Testingenclosure in appendix I for additional information.

Emergency Use Authorizations

Generally, medical devices must be cleared or approved by the Food and Drug Administration (FDA) to be marketed in the U.S.; however, the Secretary of Health and Human Services may declare that circumstances exist justifying the authorization of emergency use of certain medical products, including devices.[22] Such emergency use authorizations (EUA) allow for the temporary use of unapproved medical products or unapproved uses of approved medical products, provided certain statutory criteria are met.[23] EUAs have been instrumental in increasing needed supply of certain devices, such as PPE, during the COVID-19 pandemic response. However, there have been instances of inconsistencies between EUAs issued by FDA and device guidance from CDC and the Department of Labor (DOL)—agencies that also have a role in ensuring proper use of respirators and other devices.[24] Such inconsistencies led to confusion and hesitancy among health care providers about using devices with EUAs, according to health care provider association officials, and may have undermined the use of these critical medical products early in the pandemic. We recommend that FDA, CDC, and DOL work together to develop a process for sharing information to facilitate decision-making and guidance consistency related to devices with EUAs. HHS—which includes FDA and CDC—and DOL agreed with this recommendation.

Additionally, officials representing health care providers, device manufacturers, and distributors raised a number of concerns about what will happen to authorized devices after the declarations permitting their use for COVID-19 end.[25] The Secretary of Health and Human Services is required to provide advance notice prior to the termination of the EUA declarations and consult with manufacturers about proper disposition of authorized devices. HHS has indicated that it intends to develop draft guidance for a transition plan for medical devices distributed under EUAs for COVID-19 by the end of the fiscal year 2021. As of March 15, 2021, the agency had not released a draft plan to provide a transition for the use of these devices. Specifying a reasonable timeline and process for transitioning away from use of authorized devices before the EUA declarations end, taking into account stakeholder input, would help ensure a smooth transition.

We also recommend that as HHS develops a transition plan for devices with EUAs, it should specify a reasonable timeline and process for transitioning authorized devices to clearance, approval, or appropriate disposition that takes into account input from stakeholders. HHS agreed with this recommendation. See the Emergency Use Authorizations for Medical Devices enclosure in appendix I for additional information.

COVID-19 Data for Health Care Indicators

Since June 2020, we have identified concerns with federal COVID-19 data, and we have underscored that in the midst of a nationwide public health emergency, clear and consistent communication between the federal government and the public is critical given that effective response requires the public’s participation.

As part of its efforts to communicate with the public and stakeholders about the pandemic, several experts suggested to us that the federal government should make federal COVID-19 data more accessible, such as by making them available from a central online location. HHS publishes its data on COVID-19 health indicators across several websites, but does not make all of the data accessible from a central online location. That is, all of its publicly available data are not located on, or available from website links on, one online location. As a result, the public, including stakeholders, may not be able to fully understand the extent of the pandemic and use the data to best inform their decision-making.

We are recommending that HHS make its different sources of publicly available COVID-19 data accessible from a centralized location on the internet. This could improve the federal government’s communication with the public about the ongoing pandemic. HHS neither agreed nor disagreed with our recommendation, but it agreed that COVID-19 data should be made accessible to support communication with the public about the pandemic.

We have previously reported that communities of color have been disproportionately affected by the pandemic. We continue to emphasize the need for HHS to implement our recommendation to improve data collection and work with stakeholders to identify and address COVID-19-related racial and ethnic disparities.

HHS released its COVID-19 Response Health Equity Strategy in July 2020 with a goal to reduce health disparities by using data-driven approaches to attain the highest level of health possible for all individuals, including communities of color. We found that HHS’s equity strategy does not include important elements of an effective national strategy, as defined by our prior work. For example, HHS’s strategy includes an intermediate outcome to increase access to testing for populations at increased risk for COVID-19. However, HHS’s strategy does not provide specific actions that the agency will take to determine whether or where it needs to increase access to testing for populations at increased risk for COVID-19—an essential first step before taking steps to increase testing access. By including these elements, HHS can better ensure the effective implementation of its equity strategy to help improve the health outcomes of populations disproportionately affected by COVID-19, including communities of color.

Improving completeness of race and ethnicity data for COVID-19 vaccinations is critical to federal efforts to advance equity. HHS plans to reach disproportionately affected communities through vaccination strategies, including plans to collect and report timely, complete, and representative data on COVID-19 vaccinations. However, according to HHS, as of February 8, 2021, data from states and jurisdictions on race and ethnicity were missing for almost half (45.6 percent) of COVID-19 vaccine recipients. HHS stated that this information is missing for a variety of reasons, including a lack of consistent data collection and reporting by physicians and pharmacists and challenges with transmitting data to HHS. Without complete information on the race and ethnicity of persons who have received COVID-19 vaccines, HHS may have difficulty determining whether vaccines are distributed equitably to communities of color who have been disproportionately affected by COVID-19.

We are recommending that HHS incorporate key elements of a national strategy in its COVID-19 Response Health Equity Strategy, including specific actions to achieve intermediate outcomes and determining how they should be prioritized. HHS agreed with this recommendation. In addition, we are recommending that HHS take steps to ensure more complete reporting of race and ethnicity information for recipients of COVID-19 vaccinations. HHS neither agreed nor disagreed with this recommendation. See the Health Disparities enclosure in appendix I for more information.

Relief for Health Care Providers

The Provider Relief Fund, which reimburses eligible providers for health-care-related expenses or lost revenues attributable to COVID-19, includes an allocation for the COVID-19 Uninsured Program.[26] Although HHS officials have not yet determined the total amount to be used for this program, as of March 1, 2021, approximately $2.2 billion from the Provider Relief Fund had been disbursed for COVID-19 treatment, testing, and vaccine administration of uninsured individuals. Providers who choose to participate in this program must attest to its terms and conditions, which include that the individual treated, tested, or administered a vaccine is uninsured, that the provider will accept reimbursement as payment in full, and that the provider will not bill the individual for the balance of the bill.

HHS’s risk assessment identified the potential for providers to falsify patients as being uninsured as a risk for the COVID-19 Uninsured Program.[27] HHS officials told us that HHS intends to perform post-payment reviews of claims to validate certain provider attestations. However, HHS did not have documentation describing how it plans to conduct these reviews. Without documented post-payment review policies and procedures and timely implementation of related control activities, HHS’s ability to consistently identify and recover improper payments will be limited, and the agency’s efforts to recover the payments identified as overpayments will be delayed, or the payments may not be recovered.

We are recommending that HHS finalize and implement a post-payment review process to validate COVID-19 Uninsured Program claims and to help ensure timely identification of improper payments, including those resulting from potential fraudulent activity, and recovery of overpayments. HHS agreed with the recommendation. See the Relief for Health Care Providers enclosure in appendix I for more information.

Nursing Homes

The health and safety of the 1.4 million elderly or disabled residents in the nation’s more than 15,000 Medicare- and Medicaid-certified nursing homes—who are often in frail health and living in close proximity to one another—has been of particular concern during the COVID-19 pandemic. According to HHS case-reporting data, as of February 7, 2021, more than 99 percent of Medicare- and Medicaid-certified U.S. nursing homes had reported at least one confirmed resident or staff case, and more than 80 percent had reported at least one resident or staff COVID-19 death.

Collecting detailed information on vaccinations for nursing home populations is important for tracking and transparency, particularly because nursing homes have been an epicenter of the pandemic and because HHS has recommended priority vaccinations for this group. The National Strategy for the COVID-19 Response and Pandemic Preparedness notes that agencies should share data on COVID-19 response and recovery efforts and that these data should be publicly available to support performance tracking and ensure transparency.