As the nation continues to respond to, and recover from, the COVID-19 pandemic, increases in COVID-19 cases in July, August, and September 2021, primarily due to the Delta variant of the virus, have hampered these efforts. From the end of July 2021 to September 23, 2021, the number of new cases reported each day generally exceeded 100,000, according to Centers for Disease Control and Prevention (CDC) data. This was a daily case count not seen since February 2021 (see figure).

Reported COVID-19 Cases per Day in the U.S., Mar. 1, 2020–Sept. 23, 2021

Meanwhile, COVID-19 vaccination efforts continue. As of September 23, 2021, about 64 percent of the U.S. population eligible for vaccination (those 12 years and older), or almost 183 million individuals, had been fully vaccinated, according to CDC.

The government must remain vigilant and agile to address the evolving COVID-19 pandemic and its cascading impacts. Furthermore, as the administration implements the provisions in the COVID-19 relief laws, the size and scope of these efforts—from distributing funding to implementing new programs—demand strong accountability and oversight. In that vein, GAO has made 209 recommendations across its body of COVID-19 reports issued since June 2020. As of September 30, 2021, agencies had addressed 33 of these recommendations, resulting in improvements including increased oversight of relief payments to individuals and improved transparency of decision-making for emergency use authorizations for vaccines and therapeutics. Agencies partially addressed another 48 recommendations. GAO also raised four matters for congressional consideration, three of which remain open.

In this report, GAO is making 16 new recommendations, including recommendations related to fiscal relief funds for health care providers, recovery funds for states and localities, worker safety and health, and assessing fraud risks to unemployment insurance programs. GAO’s recommendations, if swiftly and effectively implemented, can help improve the government’s ongoing response and recovery efforts as well as help it to prepare for future public health emergencies. GAO’s new findings and recommendations, where applicable, are discussed below.

Relief for Health Care Providers

A total of $178 billion has been appropriated to the Provider Relief Fund (PRF) to reimburse eligible providers for health care–related expenses or lost revenues attributable to COVID-19. As of August 31, 2021, the Department of Health and Human Services (HHS) had allocated and disbursed about $132.5 billion of this amount and had allocated but not yet disbursed about $21.5 billion; the remaining $24.1 billion was unallocated and undisbursed. On September 10, 2021, HHS announced that $17 billion of the previously unallocated $24.1 billion would be allocated for a general distribution to a broad range of providers who could document COVID-related revenue loss and expenses. HHS expected to begin disbursing the funds in December 2021.

As of September 2021, HHS’s Health Resources and Services Administration (HRSA) had not established time frames for implementing and completing post payment reviews for all PRF payments. In addition, the agency had not finalized procedures for recovery of overpayments or recovered the bulk of the overpayments that it had already identified.

Without post-payment oversight to help ensure that relief payments are made only to eligible providers in correct amounts and to identify unused payments or payments not properly used, HHS cannot fully address stated payment integrity risks for the PRF and seek to recover overpayments, unused payments, or payments not properly used. GAO recommends that HRSA take steps to finalize and implement post-payment oversight. Specifically, HRSA should establish time frames for completing post-payment reviews to promptly address identified risks and identify overpayments made from the PRF, such as payments made in incorrect amounts or payments to ineligible providers; and it should finalize procedures and implement post-payment recovery of any PRF overpayments, unused payments, or payments not properly used. HHS—which includes HRSA—partially agreed with these recommendations.

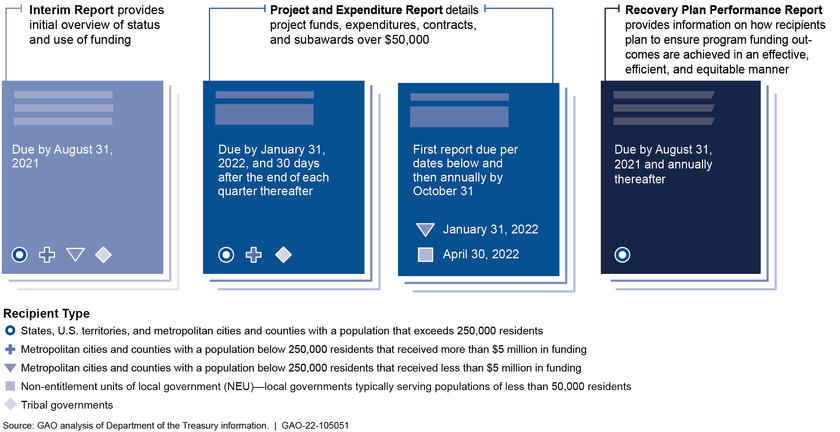

Coronavirus State and Local Fiscal Recovery Funds

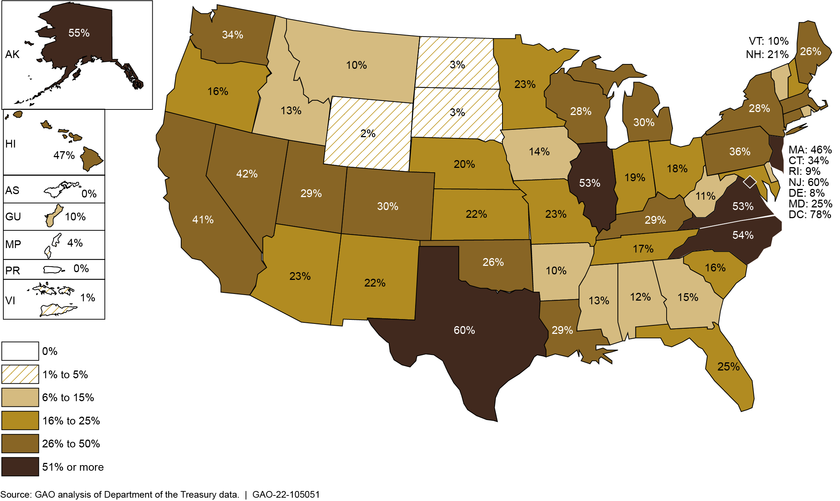

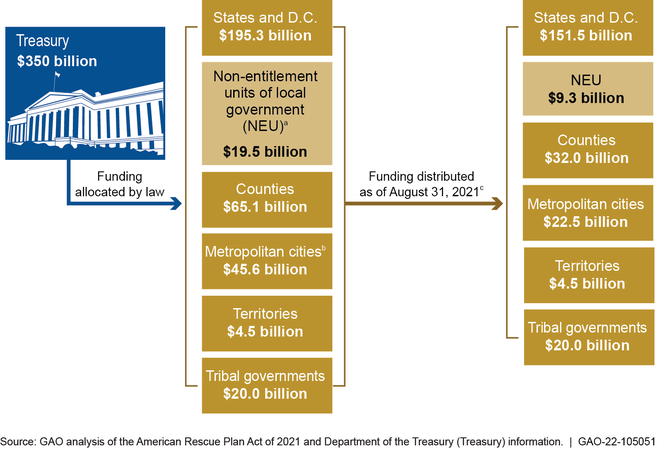

In March 2021, the American Rescue Plan Act of 2021 (ARPA) appropriated $350 billion to the Department of the Treasury (Treasury) to provide payments from the Coronavirus State and Local Fiscal Recovery Funds (CSLFRF). The CSLFRF allocates funds to states, the District of Columbia, localities, tribal governments, and U.S. territories to cover a broad range of costs stemming from the COVID-19 pandemic’s fiscal effects. According to Treasury data, it had distributed approximately $240 billion from the CSLFRF to recipients as of August 31, 2021 (see figure).

Coronavirus State and Local Fiscal Recovery Funds Allocations and Treasury Distributions as of Aug. 31, 2021, by Recipient Type

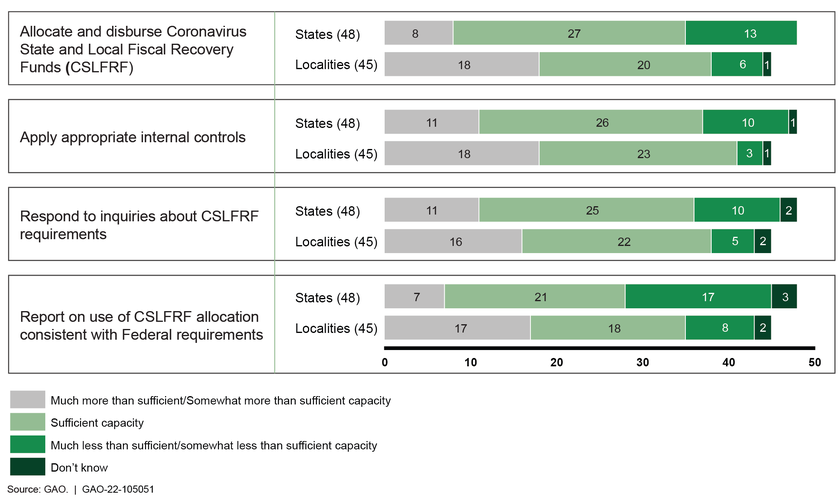

As of July 2021, some of the 48 states that responded to GAO’s survey reported that they had somewhat less than or much less than sufficient capacity to report on their use of CSLFRF allocation consistent with federal requirements (17 of 48 states), capacity to disburse the funds (13 of 48 states), and apply appropriate internal controls and respond to inquiries about requirements (10 of 48 states). In addition, most states (44 of 48) reported that they had taken or planned to take additional steps—such as hiring new staff or reassigning existing staff—to help them manage their CSLFRF allocations.

As of August 2021, Treasury was developing—but had not finalized or documented—key internal processes and control activities to monitor recipients’ use of their CSLFRF allocations for allowable purposes and to respond to internal control and compliance findings. According to officials, these internal processes and control activities were in the development stage, partly because of the short time frame since ARPA’s enactment and because Treasury’s Office of Recovery Programs, established in April 2021, continues to work to recruit and onboard key team members.

Until Treasury properly designs and documents policies and procedures to guide CSLFRF program officials and other responsible oversight parties in the Office of Recovery Programs, there is a risk that key control activities needed to help ensure program management fulfills its recipient monitoring and oversight responsibilities may not be established or applied effectively and consistently. This risk may be particularly acute with respect to monitoring state and local recipients that face capacity challenges in managing their CSLFRF allocations in accordance with federal requirements, as some survey respondents noted. GAO recommends that Treasury design and document timely and sufficient policies and procedures for monitoring CSLFRF recipients to provide assurance that recipients are managing their allocations in compliance with laws, regulations, agency guidance, and award terms and conditions. Treasury agreed with the recommendation.

Unemployment Insurance Fraud Risk Management

GAO continues to have concerns about potential fraud in the unemployment insurance (UI) program, including concerns about Department of Labor (DOL) efforts to assess and manage program fraud risks. During the pandemic, fraudulent and potentially fraudulent activity has increased substantially and new types of fraud have emerged, according to DOL officials. For example, in June 2021, DOL’s Office of Inspector General reported that it had identified nearly $8 billion in potentially fraudulent UI benefits paid from March 2020 through October 2020. Improper payments have also been a long-standing concern in the regular unemployment insurance program, suggesting that the program may be vulnerable to fraud. While DOL continues to identify and implement strategies to address potential fraud and has some ongoing program integrity activities, it has not comprehensively assessed fraud risks in alignment with leading practices identified in GAO’s Fraud Risk Framework, which by law must be incorporated in guidelines established by the Office of Management and Budget for agencies.

DOL has not clearly assigned defined responsibilities to a dedicated entity for designing and overseeing fraud risk management activities. Without a dedicated entity with defined responsibilities to lead antifraud initiatives, including the process of assessing fraud risks to UI programs, DOL may not be strategically managing UI fraud risks. GAO recommends that DOL designate a dedicated entity and document its responsibilities for managing the process of assessing fraud risks to the unemployment insurance program, consistent with leading practices as provided in GAO’s Fraud Risk Framework. This entity should have, among other things, clearly defined and documented responsibilities and authority for managing fraud risk assessments and for facilitating communication among stakeholders regarding fraud-related issues. DOL neither agreed nor disagreed with this recommendation.

DOL also has not comprehensively assessed UI fraud risks in alignment with leading practices identified in GAO’s Fraud Risk Framework. These leading practices call for federal managers to plan regular fraud risk assessments and determine their fraud risk profile, among other things. Such assessments would provide reasonable assurance that DOL has identified the most significant fraud risks for the regular UI program that will exist after the pandemic. For example, some fraud risks identified in the CARES Act UI programs may continue to exist in the regular UI program after the temporary UI programs expire. GAO recommends that DOL (1) identify inherent fraud risks facing the unemployment insurance program, (2) assess the likelihood and impact of inherent fraud risks facing the program, (3) determine fraud risk tolerance for the program, (4) examine the suitability of existing fraud controls in the program and prioritize residual fraud risks, and (5) document the fraud risk profile for the program. DOL neither agreed nor disagreed with these recommendations.

FEMA’s Disaster Relief Fund and Assistance to State, Local, Tribal, and Territorial Governments

The Federal Emergency Management Agency (FEMA) has used the Disaster Relief Fund to respond to the COVID-19 pandemic—the first time the fund has been used during a nationwide public health emergency. For example, from September 1, 2020 to August 31, 2021, FEMA obligated a total of approximately $26.8 billion through one type of disaster assistance, Public Assistance, for emergency protective measures, such as eligible medical care, the purchase and distribution of food, and distribution of personal protective equipment.

GAO found that FEMA inconsistently interpreted and applied its policies for expenses eligible for COVID-19 Public Assistance within and across its 10 regions. For example, officials in one state said that FEMA at one point had deemed the provision of personal protective equipment at correctional facilities as ineligible for reimbursement in their region but that states in other regions had received reimbursement for the same expense. These inconsistencies were due to, among other things, changes in policies as FEMA used the Public Assistance program for the first time to respond to a nationwide emergency. FEMA officials stated that it was difficult to ensure consistency in policies as different states and regions are not experiencing the same things at the same time.

FEMA is likely to receive applications for reimbursement for a larger number of projects than it estimated earlier in 2021, given the surge in COVID-19 cases this summer. To improve the consistency of the agency’s interpretation and application of the COVID-19 Public Assistance policy, GAO recommends that FEMA further clarify and communicate eligibility requirements nationwide. GAO also recommends that FEMA require the agency’s Public Assistance employees in the regions and at its Consolidated Resource Centers to attend training on changes to COVID-19 Public Assistance policy. The Department of Homeland Security—which includes FEMA— agreed with both of these recommendations.

Loans for Aviation and Other Eligible Businesses

Treasury has executed 35 loan agreements with certain aviation businesses and other businesses deemed critical to maintaining national security. These loans have totaled about $22 billion of the $46 billion authorized by the CARES Act for loans and loan guarantees to such businesses. As directed by the CARES Act, Treasury required certain loan recipients to provide financial assets, such as warrants that give the federal government an option to buy shares of stock at a predetermined price before a specified date, to protect taxpayer interests.

According to Treasury officials, it is likely that, if the airline industry continues to recover and borrowers do not default, the warrants could have higher values than the predetermined price Treasury would have to pay to act on them. Treasury has not exercised any of the warrants for stock it received from nine businesses, nor has it developed policies and procedures for determining when to act on the warrants to benefit the taxpayer. GAO recommends that Treasury develop policies and procedures to determine when to act on warrants obtained as part of the loan program for aviation and other eligible businesses to benefit the taxpayers. Treasury agreed with this recommendation.

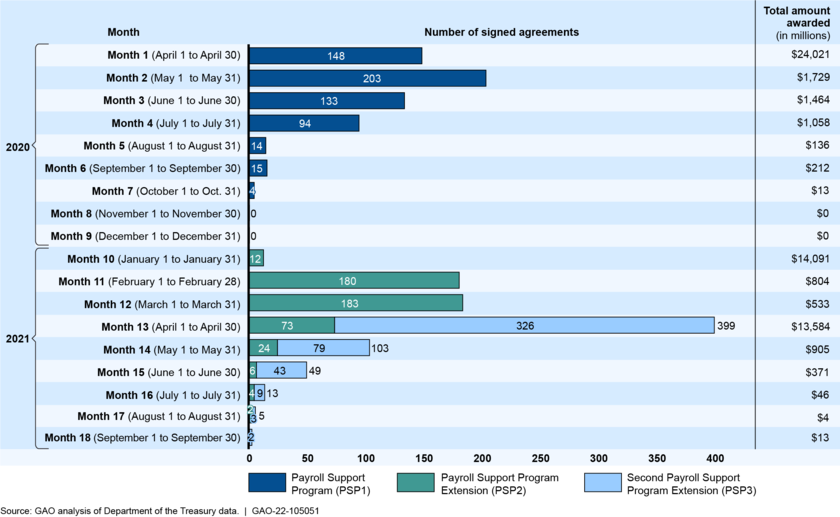

Payroll Support Assistance to Aviation Businesses

As of September 2021, Treasury had made payments totaling $59 billion of $63 billion provided for the Payroll Support Programs to support aviation business. These payments were to be used exclusively for the continuation of wages, salaries, and benefits.

Similar to Treasury’s requirement for loans for aviation and other eligible businesses, Treasury required certain Payroll Support Program recipients to provide warrants, as allowed by the CARES Act. As of September 2021, 14 recipients had provided a total of 58 million warrants.

As Treasury continues to hold these warrants for stock purchases, the warrants may increase in value as the airline industry recovers. Treasury has not exercised any of the warrants for stock it holds in the 14 businesses, nor has it documented policies and procedures to guide when to act on the warrants to fulfill the statutory purpose to provide appropriate compensation to the federal government. GAO recommends that Treasury develop policies and procedures to determine when to act on warrants obtained as part of the Payroll Support Program to provide appropriate compensation to the federal government. Treasury agreed with this recommendation.

COVID-19 Testing

Use is increasing for antigen tests, one of two types of COVID-19 diagnostic and screening tests for which HHS’s Food and Drug Administration has issued emergency use authorizations. These “rapid” antigen tests typically have a turnaround time of about 30 minutes or less for results, compared with 1 to 3 days for molecular tests, the second type of test HHS authorized. Antigen tests can be conducted at doctors’ offices or in homes or other settings; some antigen tests can be conducted without a prescription.

Since June 2020, HHS has worked to encourage and improve the reporting of antigen testing data to local, state, and federal health officials. However, HHS officials told GAO reporting of antigen test results is incomplete, which prevents HHS from using antigen testing data for COVID-19 surveillance. HHS is taking additional steps aimed at improving reporting of antigen test data. For example, officials told GAO that HHS will continue to make enhancements to data reporting by building reporting methods into the testing process, such as for testing in schools and workplaces.

HHS is also considering surveillance approaches to supplement or enhance current surveillance efforts. For example, HHS is exploring wastewater surveillance approaches, which provide data that can complement and confirm other forms of surveillance for COVID-19 and an efficient pooled community sample that is particularly useful in areas where timely COVID-19 clinical testing is underutilized or unavailable, according to HHS officials.

Worker Safety and Health

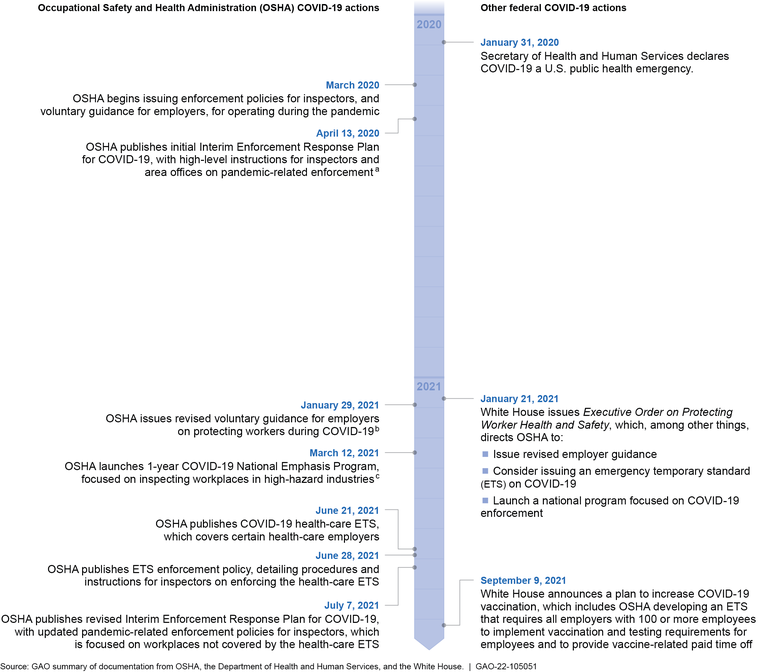

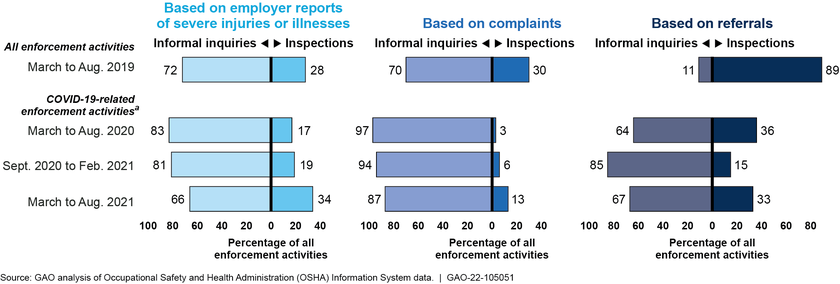

The Occupational Safety and Health Administration (OSHA) faced challenges in enforcing workplace safety and health standards during the COVID-19 pandemic, but the agency has not assessed lessons learned or promising practices. According to inspectors from area offices, they faced challenges related to resources and to communication and guidance, such as a lack of timely guidance from OSHA headquarters. GAO recommends that OSHA assess—as soon as feasible and, as appropriate, periodically thereafter—various challenges related to resources and to communication and guidance that the agency has faced in its response to the COVID-19 pandemic and take related actions as warranted. The Department of Labor—which includes OSHA—partially agreed with this recommendation.

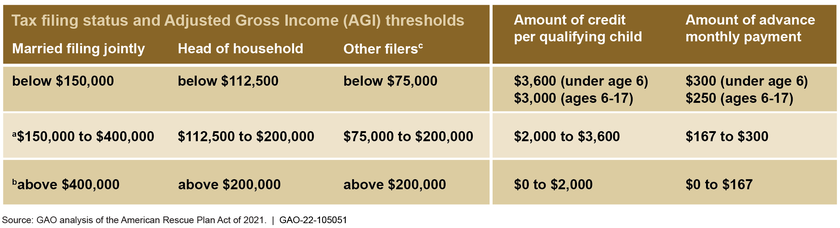

Advance Child Tax Credit Payments

ARPA temporarily expanded eligibility for the child tax credit (CTC) to additional qualified individuals by eliminating a requirement that individuals must earn a minimum amount annually to be eligible. ARPA also temporarily increased the maximum amount of the CTC from $2,000 per qualifying child to $3,000 or $3,600, depending on the child’s age. As required by ARPA, the Internal Revenue Service (IRS) and Treasury are responsible for issuing half of the CTC through periodic advance payments, known as advance CTC payments.

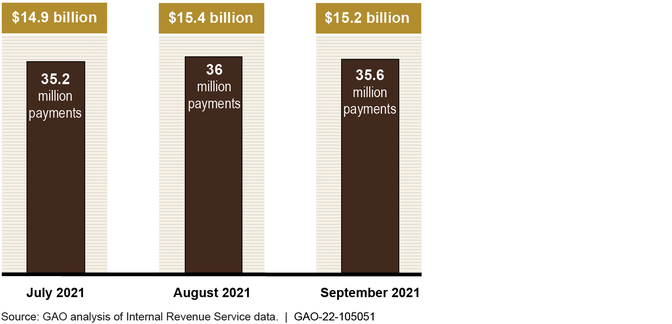

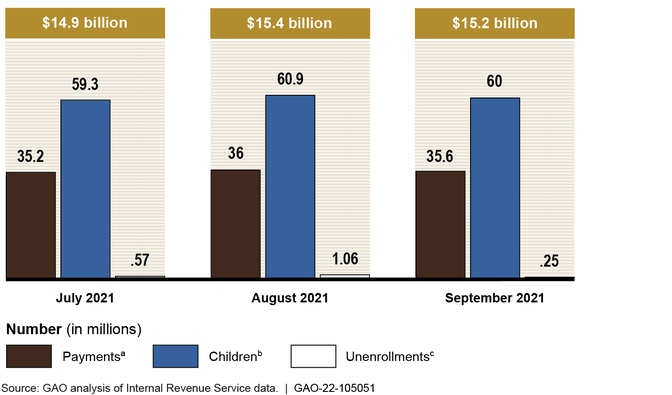

IRS reported disbursing more than 106 million advance payments totaling over $45.5 billion as of September 25, 2021 (see figure).

Dollar Amount and Count of Advance Child Tax Credit Payments, by Month, as of Sept. 25, 2021

IRS is conducting and planning several outreach efforts to increase the public’s awareness of advance CTC payments. However, IRS and Treasury have not developed a comprehensive estimate of individuals who are potentially eligible for advance CTC payments and the agencies have not set a participation goal. Such an estimate would enable Treasury and IRS to measure the tax credit’s participation rate, providing greater clarity regarding populations at risk of not receiving the payments. GAO recommends that Treasury, in coordination with IRS, estimate the number of individuals, including nonfilers, who are eligible for advance CTC payments, measure the 2021 participation rate based on that estimate, and use that estimate to develop targeted outreach and communications efforts for the 2022 filing season; the participation rate could include individuals who opt in and out of the advance payments. Treasury neither agreed nor disagreed with this recommendation.

Child Nutrition

Child nutrition programs administered by the Department of Agriculture’s Food and Nutrition Service (FNS) supply cash reimbursements to schools or other programs for meals and snacks provided to eligible children nationwide. In fiscal year 2019, before the pandemic, the four largest programs—the National School Lunch Program, School Breakfast Program, Summer Food Service Program, and Child and Adult Care Food Program—along with other child nutrition programs, received $23.1 billion in federal funds. During a typical year, two of these programs—the National School Lunch Program and the School Breakfast Program—subsidize meals for nearly 30 million children in approximately 95,000 elementary and secondary schools nationwide.

As of July 2021, FNS officials were unable to provide a plan showing how FNS intends to comprehensively analyze lessons learned during the pandemic, such as from operational and financial challenges. Further, according to FNS officials, while the School Meals Operations study—launched in spring 2021—is surveying school districts and state agencies that administer the federal child nutrition programs, the study is not gathering local perspectives directly from child care centers and day care homes or other local program sponsors that are not school districts. As a result, FNS may miss opportunities to identify lessons learned and will lack comprehensive information to aid its future planning. GAO recommends that the Department of Agriculture document its plan to analyze lessons learned from operating child nutrition programs during the COVID-19 pandemic. This plan should include a description of how the department will gather perspectives of key stakeholders, such as Child and Adult Care Food Program institutions and nonschool Summer Food Service Program sponsors. The Department of Agriculture—which includes FNS—agreed with this recommendation.

Why GAO Did This Study

As of September 23, 2021, the U.S. had about 43 million reported cases of COVID-19 and about 699,000 reported deaths, according to CDC. The country also continues to experience economic repercussions from the pandemic.

Six relief laws, including the CARES Act, had been enacted as of August 31, 2021, to address the public health and economic threats posed by COVID-19. As of that same date (the most recent for which government-wide data was available), the federal government had obligated a total of $3.9 trillion and expended $3.4 trillion of the $4.8 trillion in COVID-19 relief funds that had been appropriated by these six laws, as reported by federal agencies.

The CARES Act includes a provision for GAO to report on its ongoing monitoring and oversight efforts related to the COVID-19 pandemic. This report examines the federal government’s continued efforts to respond to, and recover from, the COVID-19 pandemic.

GAO reviewed data, documents, and guidance from federal agencies about their activities. GAO also interviewed federal and state officials, stakeholders from organizations for localities, and other stakeholders.

What GAO Recommends

GAO is making 16 new recommendations for agencies that are detailed in this Highlights and in the report.

Recommendations

Recommendations for Executive Action

Recommendations for Executive Action

We are making a total of 16 recommendations to federal agencies:

Number

Agency

Recommendation

1

Department of Health and Human Services : Public Health Service : Health Resources and Services Administration

The Administrator of the Health Resources and Services Administration should establish time frames for completing post-payment reviews to promptly address identified risks and identify overpayments made from the Provider Relief Fund, such as payments made in incorrect amounts or payments to ineligible providers. See the Relief for Health Care Providers enclosure. (Recommendation 1)

2

Department of Health and Human Services : Public Health Service : Health Resources and Services Administration

The Administrator of the Health Resources and Services Administration should finalize procedures and implement post-payment recovery of any Provider Relief Fund overpayments, unused payments, or payments not properly used. See the Relief for Health Care Providers enclosure. (Recommendation 2)

3

Department of the Treasury

The Secretary of the Treasury should design and document timely and sufficient policies and procedures for monitoring recipients of Coronavirus State and Local Fiscal Recovery Funds to provide assurance that recipients are managing their allocations in compliance with laws, regulations, agency guidance, and award terms and conditions, including ensuring that expenditures are made for allowable purposes. See the Coronavirus State and Local Fiscal Recovery Funds enclosure. (Recommendation 3)

4

Department of Labor

The Secretary of Labor should designate a dedicated entity and document its responsibilities for managing the process of assessing fraud risks to the unemployment insurance program, consistent with leading practices as provided in our Fraud Risk Framework. This entity should have, among other things, clearly defined and documented responsibilities and authority for managing fraud risk assessments and for facilitating communication among stakeholders regarding fraud-related issues. See the Unemployment Insurance Fraud Risk Management enclosure. (Recommendation 4)

The Secretary of Labor should examine the suitability of existing fraud controls in the unemployment insurance program and prioritize residual fraud risks. See the Unemployment Insurance Fraud Risk Management enclosure. (Recommendation 8)

Department of Homeland Security : Directorate of Emergency Preparedness and Response : Federal Emergency Management Agency

The Federal Emergency Management Agency Administrator should require the agency’s Public Assistance Program employees in the regions and at its Consolidated Resource Centers to attend training on changes to COVID-19 Public Assistance policy to help ensure it is interpreted and applied consistently nationwide. See the FEMA’s Disaster Relief Fund and Assistance to State, Local, Tribal, and Territorial Governments enclosure. (Recommendation 11)

12

Department of the Treasury

The Secretary of the Treasury should develop policies and procedures to determine when to act on warrants obtained as part of the loan program for aviation and other eligible businesses to benefit the taxpayers. See the Loans for Aviation and Other Eligible Businesses enclosure. (Recommendation 12)

13

Department of the Treasury

The Secretary of the Treasury should develop policies and procedures to determine when to act on warrants obtained as part of the Payroll Support Program to provide appropriate compensation to the federal government. See the Payroll Support Assistance to Aviation Businesses enclosure. (Recommendation 13)

14

Department of Labor : Occupational Safety and Health Administration

The Assistant Secretary of Labor for Occupational Safety and Health should assess—as soon as feasible and, as appropriate, periodically thereafter—various challenges related to resources and to communication and guidance that the Occupational Safety and Health Administration has faced in its response to the COVID-19 pandemic and should take related actions as warranted. See the Worker Safety and Health enclosure. (Recommendation 14)

15

Department of the Treasury

The Secretary of the Treasury, in coordination with the Commissioner of Internal Revenue, should estimate the number of individuals, including nonfilers, who are eligible for advance child tax credit payments, measure the 2021 participation rate based on that estimate, and use that estimate to develop targeted outreach and communications efforts for the 2022 filing season; the participation rate could include individuals who opt in and out of the advance payments. See the Advance Child Tax Credit and Economic Impact Payments enclosure. (Recommendation 15)

16

Department of Agriculture

The Secretary of Agriculture should document the Department of Agriculture’s plan to analyze lessons learned from operating child nutrition programs during the COVID-19 pandemic. This plan should include a description of how the department will gather perspectives of key stakeholders, such as Child and Adult Care Food Program institutions and nonschool Summer Food Service Program sponsors. See the Child Nutrition enclosure. (Recommendation 16)

As the nation continues to respond to the Coronavirus Disease 2019 (COVID-19) pandemic, response and recovery efforts have been hampered by increases in COVID-19 cases, due primarily to the Delta variant of the virus.[1] Although the daily number of new cases had begun to decline earlier in the summer, the number of new cases reported each day from the end of July 2021, to September 23, 2021, generally exceeded 100,000, according to the Centers for Disease Control and Prevention (CDC)—a daily case count not seen since February 2021 and substantially higher than the approximately 8,000 new cases reported per day in mid-June. As a result of the rise in cases, CDC, state and local governments, and private businesses revised their mask guidance or requirements.[2]

While vaccination efforts continue, vaccination rates across the U.S. vary. As of September 23, 2021, about 64 percent of the U.S population eligible for vaccination (those 12 years and older)—about 183 million individuals—had been fully vaccinated, according to CDC.

Hospitals reported an average of more than 9,000 individuals hospitalized daily for the 7-day period from September 17 to September 23, 2021, a decrease from more than 12,000 individuals hospitalized daily during a 7-day period in August 2021.[3] According to CDC, at the end of August 2021, new admissions of patients with confirmed COVID-19 were at their highest levels since the beginning of the pandemic for all age groups under 50 years old.[4] As of the end of September 2021, CDC reported that weekly hospitalization rates for children aged 11 and younger due to COVID-19 were at their highest since the beginning of the pandemic, although hospitalizations due to COVID-19 are lower in children than they are in adults. As the pandemic continues, the U.S. and the world may continue to see fluctuating increases in new cases, making an agile federal response to the pandemic even more important.

Ongoing demand for medical supplies for the COVID-19 response, including testing materials and personal protective equipment, has resulted in fluctuating shortages. For example, on September 2, 2021, CDC announced a temporary shortage of point-of-care and over-the-counter COVID-19 testing supplies. In addition, the federal government continues to provide personal protective equipment—N95 respirators, surgical masks, surgical and isolation gowns, and nitrile and other gloves—to states, with gloves accounting for the largest number of shipments. For example, during the 7-day period from September 18 to September 24, 2021, the federal government and its commercial partners shipped close to 700 million units of gloves, over 44 million surgical masks, over 13 million surgical gowns, and close to 5 million N95 respirators to all 50 states, the District of Columbia, and Puerto Rico.

To help prevent medical supply shortages for future public health emergencies, the Department of Health and Human Services (HHS) released its pandemic supply chain resilience strategy, as called for in Executive Order 14001, in September 2021.[5] The strategy outlines the goals and objectives for a resilient public health supply chain and the “path for implementation” of the strategy.[6]

Since March 2020, Congress has provided about $4.8 trillion through the CARES Act and other laws that were enacted to fund efforts to help the nation respond to and recover from the COVID-19 pandemic (COVID-19 relief laws).[7]

Ongoing implementation of the provisions in the COVID-19 relief laws and the size and scope of these efforts—from distributing funding to implementing new programs—continue to demand strong accountability and oversight. Furthermore, the government must remain vigilant and agile to address the evolving COVID-19 pandemic well into its second year. The current annual hurricane and flu seasons could place further burdens on the already overtaxed health care, medical supply, and emergency management sectors.[8]

The CARES Act includes a provision for us to report regularly on the federal response to the pandemic. Specifically, the act requires us to monitor and oversee the federal government’s efforts to prepare for, respond to, and recover from the COVID-19 pandemic.[9] To date, we have issued seven recurring oversight reports in response to this provision.[10]

This report examines the federal government’s continued efforts to respond to and recover from the COVID-19 pandemic. We are making 16 new recommendations to federal agencies in areas including fiscal relief funds for health care providers, worker safety and health, assessing fraud risks to unemployment insurance programs, and state and local recovery funds.

This report also includes 37 enclosures addressing a range of federal programs and activities across the government concerning public health and the economy (see app. I). Figure 1 lists these enclosures by topic area and highlights those with new recommendations.

Figure 1: Report Enclosures by Topic Area

In addition to the seven recurring oversight reports, we have issued over 100 targeted COVID-19-related reports, testimonies, and science and technology spotlights in areas such as housing protections, Medicare and Medicaid program flexibilities, and digital vaccine credentials. We also have reviews ongoing in other areas. See appendix II for highlights pages from our recently issued work on COVID-19 and appendix III for a list of our ongoing work related to COVID-19.

Across our body of COVID-19-related reports, we have made 209 recommendations to federal agencies and have raised four matters for congressional consideration to improve the federal government’s response efforts. As of September 30, 2021, agencies had addressed 33 of these recommendations and partially addressed 48.[11]

See figure 2 for an overview of the status of our COVID-19-related recommendations by department. For a complete list of our COVID-related products, see https://www.gao.gov/coronavirus.

Figure 2: Status of Prior GAO Recommendations from COVID-19-Related Work, by Federal Department or Agency, as of Sept. 30, 2021

Note: For this figure, recommendations made to the Internal Revenue Service are counted toward the total of recommendations made to the Department of the Treasury.

Given the government-wide scope of this report, we undertook a variety of methodologies to complete our work, including examining a wide range of data sources and conducting interviews with federal and state officials and stakeholders, such as those from four antihunger organizations and organizations that represent landlords and lower-income households. We also examined federal laws, agency documents, and guidance, among other things. In each enclosure, we include a summary of the methodology specific to the work conducted.

We conducted this performance audit from March 2021 to October 2021 in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

The COVID-19 pandemic continues to have devastating effects on public health and the economy. As of September 23, 2021, the U.S. had about 43 million reported cases of COVID-19, according to CDC.[12] As of the week ending September 25, 2021, the U.S. had about 699,000 reported deaths attributed to COVID-19.[13] In addition, the country continues to experience high unemployment. As of September 2021, about 7.7 million individuals were unemployed, compared with nearly 5.8 million at the beginning of 2020.[14]

The number of newly reported COVID-19 cases began increasing at the end of July 2021, following a decrease in daily cases since the January 2021 peak. Between September 10 and September 23, 2021, new reported COVID-19 cases averaged about 138,000 per day—close to 60 percent of the peak that occurred during January 2021.[15] See figure 3 for 7-day case averages. During this same period, reported new COVID-19 cases per day, on average, increased in 14 jurisdictions, held steady in 20 jurisdictions, and decreased in 18 jurisdictions.[16]

Figure 3: Reported COVID-19 Cases per Day in the U.S., Mar. 1, 2020–Sept. 23, 2021

Note: Reported COVID-19 cases include confirmed and probable cases. Beginning April 14, 2020, states could include probable as well as confirmed COVID-19 cases in their reports to CDC. Previously, counts included only confirmed cases. According to CDC, the actual number of cases is unknown for a variety of reasons, including that people who have been infected may not have been tested or may not have sought medical care. See CDC, “COVID Data Tracker: Trends in Number of COVID-19 Cases and Deaths in the U.S. Reported to CDC, by State/Territory,” accessed September 30, 2021, https://covid.cdc.gov/covid-data-tracker/#trends_dailytrendscases.

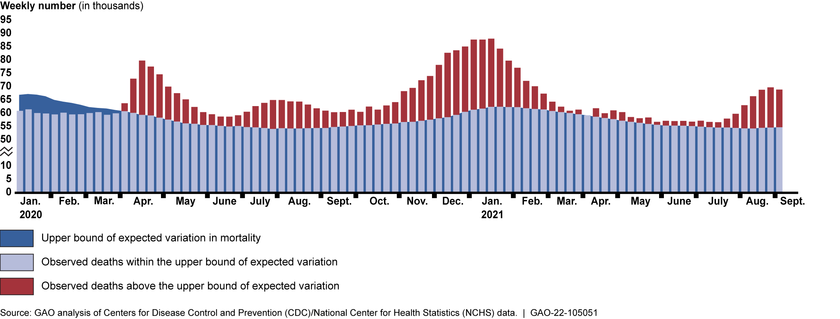

According to data from CDC’s National Center for Health Statistics, the number of deaths in the U.S. has been higher during the pandemic than the expected number of deaths based on previous years’ data. For example, from January 1, 2020, through September 4, 2021, about 687,000 more deaths occurred from COVID-19 and other causes than would be normally expected (see fig. 4).

Figure 4: Higher-Than-Expected Weekly Mortality in the U.S., Jan. 2020 to Sept. 2021

Note: The data shown represent the number of deaths from all causes reported in the U.S.in a given week through September 4, 2021, that exceeded the upper-bound threshold of expected deaths calculated by CDC’s NCHS on the basis of variation in mortality in prior years. For further details of CDC’s methodology for estimating this upper-bound threshold, see CDC, National Center for Health Statistics, “Excess Deaths Associated with COVID-19,” accessed October 4, 2021, https://www.cdc.gov/nchs/nvss/vsrr/covid19/excess_deaths.htm. The number of deaths in recent weeks should be interpreted cautiously, as this figure relies on provisional data that are generally less complete.

Providing the public with safe and effective vaccines to protect people from getting critically ill with COVID-19 is crucial to mitigating the public health and economic impacts of the virus and ending the pandemic. Two COVID-19 vaccines requiring two doses were authorized by the Food and Drug Administration (FDA) for emergency use in December 2020 and a third vaccine, requiring one dose, was authorized in February 2021.[17] On August 23, 2021, FDA approved Pfizer’s biologics license application for its two-dose vaccine for individuals aged 16 years and older.[18]

On August 18, 2021, the administration recommended that individuals who received the two-dose vaccines should get a third “booster” shot 8 months after the second dose, pending FDA authorization and a recommendation from CDC’s immunization advisory committee.[19] On September 22, 2021, FDA amended the authorization for the Pfizer vaccine to allow for a booster shot to be administered to individuals aged 65 years and older, individuals aged 18 to 64 years who are at high risk of developing severe illness from COVID-19, and individuals aged 18 to 64 years whose frequent institutional or occupational exposure to COVID-19 puts them at high risk of serious complications from COVID-19, including severe illness. Boosters for these individuals are to be administered at least 6 months after completion of the first series of shots.[20] In mid-October, FDA’s vaccine advisory panel recommended boosters of the Moderna and Johnson & Johnson vaccines.[21]

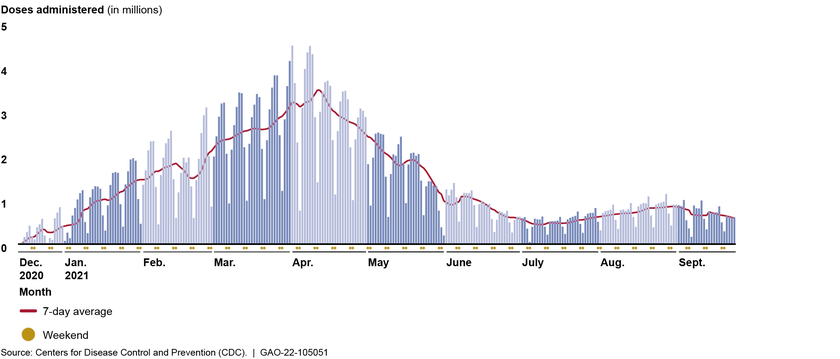

As of September 23, 2021, almost 390 million doses of COVID-19 vaccine had been administered, according to CDC. Since the vaccination peak in early April 2021, the number of doses of COVID-19 vaccine administered each day have generally declined. As of September 23, 2021, the number of daily administered doses was less than one-fifth of those administered in the April peak (see fig. 5).

Figure 5: Daily Count of COVID-19 Vaccine Doses Administered in the U.S. and Reported to CDC, Dec. 14, 2020–Sept. 23, 2021

Notes: The data shown reflect COVID-19 vaccine doses administered in the U.S. as reported to CDC by state, territorial, and local public health agencies and by federal entities since the national vaccine program began on December 14, 2020. The data include doses administered through all vaccine partners, including jurisdictional partner clinics, retail pharmacies, long-term care facilities, Federal Emergency Management Agency and Health Resources and Services Administration partner sites, and federal entity facilities. See CDC, “COVID Data Tracker: COVID-19 Vaccinations in the United States,” accessed on September 30, 2021, https://covid.cdc.gov/covid-data-tracker/#vaccinations.As of September 30, 2021, one COVID-19 vaccine had been licensed by the Food and Drug Administration for individuals aged 16 years and older and was authorized for emergency use for individuals aged 12 to 15 years. Two additional COVID-19 vaccines were authorized for emergency use for individuals aged 18 years and older. The approved vaccine and one of the vaccines authorized for emergency use are two-dose regimens; the other vaccine with emergency authorization requires one dose. The number of doses administered on a given day may be affected by several factors, such as weekend days, holidays, weather, and vaccine availability. The most recent days of reporting may be more impacted by reporting delays, and all reported numbers may change over time as historical data are reported to CDC.

In addition to the impact on public health, the pandemic continues to present economic challenges, particularly for the labor market, though the economy has improved in recent months. According to data from the Department of Labor, labor market conditions improved in June, July, August, and September 2021 but remained worse relative to the prepandemic period. For example, although initial unemployment insurance claims generally declined through September 2021, initial claims remain high compared to the prepandemic period.

Moreover, in September 2021, the employment-to-population ratio, which measures the share of the population employed, was 58.7 percent—a slight increase from the previous month. However, this ratio was 2.4 percentage points lower than in the prepandemic period, indicating that labor market conditions remain worse than in the prepandemic period (see fig. 6).[22] See the Economic Indicators enclosure in appendix I for more information.

As of August 31, 2021, the most recent date for which government-wide information was available at the time of our analysis, the federal government had obligated a total of $3.9 trillion and expended $3.4 trillion of the $4.8 trillion in appropriated COVID-19 relief funds as reported by federal agencies to the Department of the Treasury’s Governmentwide Treasury Account Symbol Adjusted Trial Balance System.[23] Obligations and expenditures relative to the amounts appropriated through COVID-19 relief laws have varied over time, as new relief laws have appropriated additional relief funds and as the federal government has obligated and expended those funds (see fig. 7).

Figure 7: Percentage of COVID-19 Relief Appropriations Obligated and Expended, July 31, 2020–Aug. 31, 2021

Notes: The percentages shown represent the portions of appropriated funds available as of each date shown that had been obligated and expended. An appropriation provides legal authority for federal agencies to incur obligations and make payments out of the U.S. Treasury for specified purposes. Appropriation amounts are based on appropriation warrant information provided by the Department of the Treasury as of July 31, 2020; September 30, 2020; November 30, 2020; January 31, 2021; May 31, 2021; June 30, 2021; July 31, 2021; and August 31, 2021, for the six COVID-19 relief laws, four of which were enacted before July 2020. These amounts have increased over time and could increase in the future for programs with indefinite appropriations (i.e., appropriations that, at the time of enactment, are for an unspecified amount).An obligation is a definite commitment that creates a legal liability of the U.S. government for the payment of goods and services ordered or received, or a legal duty on the part of the U.S. government that could mature into a legal liability by virtue of actions on the part of another party that are beyond the control of the U.S. government. An expenditure is the actual spending of money, or an outlay. Expenditures reflected in the percentages shown include some estimates, such as estimated subsidy costs for direct loans and loan guarantees. Increased spending in Medicaid and Medicare is not accounted for in the appropriations provided by the COVID-19 relief laws. Under Office of Management and Budget guidance, federal agencies were not directed to report COVID-19 related obligations and expenditures until July 2020.

The nine major spending areas shown in table 1 represent $3.9 trillion, or 81 percent, of the total amounts appropriated. For these nine spending areas, agencies reported obligations totaling $3.3 trillion and expenditures totaling $3.0 trillion as of August 31, 2021. Table 1 provides additional details on appropriations, obligations, and expenditures of government-wide COVID-19 relief funds, including the nine major spending areas as of August 31, 2021.

Table 1: COVID-19 Relief Appropriations, Obligations, and Expenditures, as of Aug. 31, 2021

Major spending areaa

Total appropriationsb ($ in billions)

Total obligationsc ($ in billions)

Total expendituresc ($ in billions)

Unemployment Insurance (Department of Labor)

858.6

660.3

650.2

Economic Impact Payments (Department of the Treasury)

855.3

841.6

841.6

Business Loan Programs (Small Business Administration)

838.0

829.2

827.6d

Public Health and Social Services Emergency Fund (Department of Health and Human Services)

350.1

240.0

172.1

Coronavirus State and Local Fiscal Recovery Funds (Department of the Treasury)

350.0

239.8

239.8

Education Stabilization Fund (Department of Education)

278.6

257.0

51.7

Coronavirus Relief Fund (Department of the Treasury)

150.0

149.9

149.9

Disaster Relief Fund (Department of Homeland Security)e

97.0

63.8

9.9

Supplemental Nutrition Assistance Programs (Department of Agriculture)

91.7

66.1

64.6

Other areasf

881.6

532.4

391.9

Totalg

4,750.9

3,880.1

3,399.3

Source: GAO analysis of data from the Department of the Treasury and applicable agencies. | GAO-22-105051

aMajor spending areas shown are based on federal accounts in Treasury’s Governmentwide Treasury Account Symbol Adjusted Trial Balance System. Each spending area may include multiple programs. bCOVID-19 relief appropriations shown reflect amounts appropriated under the American Rescue Plan Act of 2021 (ARPA), Pub. L. No. 117-2, 135 Stat. 4; Consolidated Appropriations Act, 2021, Pub. L. No. 116-260, 134 Stat. 1182 (2020); Paycheck Protection Program and Health Care Enhancement Act, Pub. L. No. 116-139, 134 Stat. 620 (2020); CARES Act, Pub. L. No. 116-136, 134 Stat. 281 (2020); Families First Coronavirus Response Act, Pub. L. No. 116-127, 134 Stat. 178 (2020); and Coronavirus Preparedness and Response Supplemental Appropriations Act, 2020, Pub. L. No. 116-123, 134 Stat. 146. These amounts are based on appropriation warrant information provided by Treasury as of August 31, 2021. These amounts have increased over time and could increase in the future for programs with indefinite appropriations, which are appropriations that, at the time of enactment, are for an unspecified amount. The amounts shown do not include transfers of funds that federal agencies may make between appropriation accounts or transfers of funds they may make to other agencies. cObligation and expenditure data shown are based on data reported by applicable agencies. An obligation is a definite commitment that creates a legal liability of the U.S. government for the payment of goods and services ordered or received, or a legal duty on the part of the U.S. government that could mature into a legal liability by virtue of actions on the part of another party that are beyond the control of the U.S. government. An expenditure is the actual spending of money, or an outlay. Expenditures shown include some estimates, such as estimated subsidy costs for direct loans and loan guarantees. dThe Small Business Administration’s Business Loan Program account includes activity for the Paycheck Protection Program loan guarantees and certain other loan subsidies. These expenditures relate mostly to the loan subsidy costs (i.e., the loan’s estimated long-term costs to the U.S. government). eAppropriations to the Disaster Relief Fund are generally not specific to individual disasters. Therefore, Treasury’s methodology for determining COVID-19-related obligations and expenditures does not capture obligations and expenditures for the COVID-19 response based on appropriations other than those in the COVID-19 relief laws. Further, Treasury’s methodology includes all obligations and expenditures based on appropriations in the COVID-19 relief laws, including those for other disasters. In its Disaster Relief Fund Monthly Report dated September 9, 2021, the Department of Homeland Security reported COVID-19-related obligations totaling $80.0 billion and expenditures totaling $60.6 billion as of August 31, 2021. fSeveral provisions in the Families First Coronavirus Response Act and ARPA authorized increases in Medicaid payments to states and U.S. territories. The Congressional Budget Office estimated that federal expenditures from these provisions would be approximately $76.9 billion through fiscal year 2030. The largest increase to federal Medicaid spending is based on a temporary formula change rather than a specific appropriated amount. Some of the estimated costs in this total are for the Children’s Health Insurance Program, permanent changes to Medicaid, and changes not specifically related to COVID-19. This increased spending is not accounted for in the appropriations provided by the COVID-19 relief laws and therefore not included in this table. gBecause of rounding, amounts shown in columns may not sum to the totals.

The COVID-19 relief laws provided more than $1 trillion to federal agencies to provide assistance related to the COVID-19 pandemic to states, the District of Columbia, localities, U.S. territories, and tribes through existing and newly created programs and funds.[24] Table 2 lists programs and funds that each received $10 billion or more—exclusively or primarily for states, the District of Columbia, localities, U.S. territories, and tribes—in at least one of the six laws. It also provides obligations and expenditures for these programs and funds as of August 31, 2021.

Table 2: Appropriations, Obligations, and Expenditures for Federal Programs and Funds Receiving $10 Billion or More in COVID-19-Related Aid for States, the District of Columbia, Localities, U.S. Territories, and Tribes, as of Aug. 31, 2021

Program fund/description

Appropriations ($ in billions)

Obligations ($ in billions)

Expenditures ($ in billions)

Coronavirus State and Local Fiscal Recovery Funds Administered by the Department of the Treasury, these funds provide payments to states, the District of Columbia (D.C.), U.S. territories, tribal governments, and localities to mitigate the fiscal effects stemming from the COVID-19 pandemic, among other things.

350

239.8

239.8

Elementary and Secondary School Emergency Relief Fund Administered by the Department of Education, this fund generally provides formula grants to states (including D.C. and Puerto Rico) for education-related needs to address the impact of the COVID-19 pandemic.

190.3

172.3

17.3

Coronavirus Relief Fund Administered by Treasury, this fund provides payments to states, D.C., localities, U.S. territories, and tribal governments to help offset costs of their response to the COVID-19 pandemic.

150

149.9

149.9

Disaster Relief Fund Administered by the Federal Emergency Management Agency, this fund provides federal disaster recovery assistance for state, local, tribal, and territorial governments when a major disaster occurs.

95a

31.3b

19.6b

Medicaid Administered by states and U.S. territories according to plans approved by the Centers for Medicare & Medicaid Services, which oversees Medicaid at the federal level. This program finances health care for certain low-income and medically needy individuals through federal matching of states’ and U.S. territories’ health care expenditures. The Families First Coronavirus Response Act and American Rescue Plan Act of 2021 temporarily increased federal Medicaid matching rates under specified circumstances, among other changes.

76.9c

50.9d

50.9d

Transit grants Administered by the Federal Transit Administration, these funds are distributed through existing grant programs to provide assistance to states, localities, U.S. territories, and tribes to prevent, prepare for, and respond to the COVID-19 pandemic.

69.5

37.0

22.8

Child Care and Development Fund Administered by the Department of Health and Human Services (HHS), this program provides funds to states, D.C., territories, and tribes to subsidize the cost of child care for low-income families. COVID relief funds have supported assistance to health care and other essential workers without regard to income eligibility requirements. Additional child care stabilization funding was provided for subgrants to eligible child care providers to support the stability of the child care sector during and after the COVID-19 pandemic.e

52.5

52.4

7.0

Emergency Rental Assistance Administered by Treasury, this program provides grants to states, D.C., U.S. territories, localities, and tribes to provide assistance to eligible households for rent and utility payments.

46.6

33.2

33.2f

Public Health and Social Services Emergency Fund Administered by HHS, this fund provides for grants to states, U.S. territories, localities, and tribal governments to support COVID-19 testing, surveillance, and contact tracing, among other uses.

33.4

30.3

7.7

Airport grants Administered by the Federal Aviation Administration, these grants provide funds for eligible airports to prevent, prepare for, and respond to the effects of the COVID-19 pandemic.g

20

15.8h

7.7h

Highway infrastructure programs Administered by the Federal Highway Administration, these programs provide funds to states, D.C., U.S. territories, and tribes for highway construction and authorize the use of these funds for maintenance, personnel, and other purposes to prevent, prepare for, and respond to the COVID-19 pandemic.

10

3.9h

1.5h

Coronavirus Capital Projects Fund Administered by Treasury, this fund provides payments to states, D.C., U.S. territories, and tribal governments for critical capital projects that directly enable work, education, and health monitoring in response to the COVID-19 pandemic.i

10

0

0

State Small Business Credit Initiative Administered by Treasury, this program provides funds to states, D.C., U.S. territories, tribal governments, and eligible localities to fund small business credit support and investment programs.j

10

0

0

Source: GAO analysis of federal laws, data from the Congressional Budget Office, and obligations and expenditures data from Treasury and applicable agencies. | GAO-22-105051

Notes: The COVID-19 relief laws providing the appropriations shown are the American Rescue Plan Act of 2021 (ARPA), Pub. L. No. 117-2, 135 Stat. 4 (2021), the Consolidated Appropriations Act, 2021, Pub. L. No. 116-260, div. M and N, 134 Stat. 1182 (2020), the Paycheck Protection Program and Health Care Enhancement Act, Pub. L. No. 116-139, 134 Stat. 620 (2020), the CARES Act, Pub. L. No. 116-136, 134 Stat. 281 (2020), and the Families First Coronavirus Response Act, Pub. L. No. 116-127, 134 Stat. 178 (2020). The Coronavirus Preparedness and Response Supplemental Appropriations Act, 2020 did not provide any specified amounts for these programs or funds for states, D.C., localities, territories, or tribes. The amounts shown are the cumulative amounts for each program or fund under the other five laws. Some appropriation amounts include an amount available for administration expenses or for the relevant inspectors general. Numbers are rounded to the nearest hundred million. We did not independently verify obligations and expenditures amounts. aAppropriations for the Disaster Relief Fund generally are not specific to individual disasters and may be used for various disaster assistance programs, including the Public Assistance program, which provides assistance to state, local, territorial, and tribal governments. bThe obligations and expenditures listed in the table are for the Public Assistance program for the COVID-19 response. cSeveral provisions in the Families First Coronavirus Response Act and ARPA authorized increases in Medicaid payments to states and U.S. territories. The Congressional Budget Office estimated that federal expenditures from these provisions would be approximately $76.9 billion through fiscal year 2030. The largest increase to federal Medicaid spending is based on a temporary funding formula change rather than a specific appropriated amount. Some of the estimated costs in this total are for the Children’s Health Insurance Program, permanent changes to Medicaid, and changes not specifically related to COVID-19. dMedicaid obligations and expenditures are as of June 30, 2021. COVID-19 related obligation and expenditure amounts for Medicaid only reflect provisions in the Families First Coronavirus Response Act. Obligation and expenditure amounts for COVID-19 related Medicaid provisions in the American Rescue Plan Act are not currently available from the Centers for Medicare & Medicaid Services. eThe Child Care and Development Fund is made up of two funding streams: mandatory and matching funding authorized under section 418 of the Social Security Act, and discretionary funding authorized under the Child Care and Development Block Grant Act of 1990, as amended. See 42 U.S.C. §§ 618 and 9858m. fExpenditures represent funding disbursed to grantees by Treasury for distribution to renters, landlords, and utility providers. As of August 31, 2021, grantees had spent about $7.7 billion of these amounts. For additional information on grantee spending, see the enclosure on the Emergency Rental Assistance program in appendix I. gFunds are available to eligible sponsors of airports. Nearly all of these airports are under city, state, county, or public-authority ownership. hObligations and expenditures for these funds are as of August 30, 2021. iTreasury issued implementing guidance in September 2021 that provides that the application deadline for requesting allocations of the Coronavirus Capital Projects Fund from Treasury is (1) December 27, 2021, for states, D.C., and U.S. territories; and (2) June 1, 2022, for tribal governments. jStates, the District of Columbia, territories, and tribal governments must initiate applications for the State Small Business Credit Initiative program with Treasury by December 11, 2021. Eligible jurisdictions must submit completed applications by February 11, 2022.

As the nation continues to respond to the pandemic and significant increases in COVID-19 cases from the Delta variant, this report provides key updates on the government’s pandemic response and makes 16 new recommendations aimed at improving the accountability and program effectiveness of the federal response.

In our prior CARES Act reports and other targeted COVID-19-related reports, we have made a total of 209 recommendations to federal agencies.[25] As of September 30, 2021, agencies had fully addressed 33 of these recommendations, resulting in improvements including increased oversight of relief payments to individuals and improved transparency of decision making for emergency use authorizations for vaccines and therapeutics. Agencies have also partially addressed an additional 48 recommendations. Fully addressing our previous recommendations as well as the new recommendations we are making will enhance the transparency and accountability of the federal government’s response to and recovery from the COVID-19 pandemic.

Relief for Health Care Providers

To respond to the pandemic, $178 billion has been appropriated to the Provider Relief Fund (PRF) to reimburse eligible providers for health care-related expenses or lost revenues attributable to COVID-19. As of August 31, 2021, HHS had allocated about $153.9 billion. Of the $153.9 billion allocated, HHS had disbursed about $132.5 billion and about $21.5 billion remained to be disbursed. Approximately $24.1 billion of PRF funds remained unallocated and undisbursed as of August 31, 2021. On September 10, 2021, HHS announced that $17 billion of the previously unallocated $24.1 billion would be allocated for a general distribution to a broad range of providers who could document COVID-related revenue loss and expenses. HHS expected to begin disbursing these funds in December 2021.

The Health Resources and Services Administration (HRSA) has taken some oversight actions regarding post-payment reviews of PRF payments and recovery of identified overpayments; however, it has not established key next steps. While the agency has conducted post-payment reviews for certain priority types of provider payments, it has not established time frames for implementing and completing all remaining post-payment reviews or set review schedules beyond the first quarter of calendar year 2022. In regards to recovery of identified overpayments, the agency has yet to recover most of the overpayments that had been identified as of September 2021. HRSA officials stated they had plans for recovering overpayments, but had not finalized procedures for doing so.

Without timely post-payment oversight that includes time frames for conducting reviews to help ensure that relief payments are made only to eligible providers in correct amounts and to identify unused payments or payments not properly used, HHS cannot fully address its stated payment integrity risks for the PRF and seek to recover overpayments, unused payments, or payments not properly used. Moreover, setting time frames for completion of these oversight efforts can help the agency achieve its objectives and increase the likelihood of recovering funds.

We are recommending that the Administrator of the Health Resources and Services Administration take several steps to finalize and implement post-payment oversight. Specifically, the Administrator should establish time frames for completing post-payment reviews to promptly address identified risks and identify overpayments made from the Provider Relief Fund, such as payments made in incorrect amounts or payments to ineligible providers. The Administrator should also finalize procedures and implement post-payment recovery of any Provider Relief Fund overpayments, unused payments, or payments not properly used. HHS, which includes HRSA, partially agreed with both recommendations. HRSA stated that it has a schedule for reviewing the payment types it initially prioritized, and that reviews for the remaining types and payment recovery efforts will occur in the future. We maintain that establishing time frames for completing reviews and finalizing procedures and implementing recovery efforts expeditiously will help the agency succeed in recovering overpayments.

In March 2021, the American Rescue Plan Act of 2021 (ARPA) appropriated $350 billion to Treasury for the Coronavirus State and Local Fiscal Recovery Funds (CSLFRF).[26] The CSLFRF allocates funds to states, the District of Columbia, localities, tribal governments, and U.S. territories to cover a broad range of costs stemming from the fiscal effects of the COVID-19 pandemic.[27] According to Treasury data, it had distributed approximately $240 billion in CSLFRF funds to recipients as of August 31, 2021.

As of July 2021, some of the 48 states that responded to a GAO survey reported that they had somewhat less than or much less than sufficient capacity to report on use of CSLFRF allocation consistent with federal requirements (17 of 48), to disburse the funds (13 of 48), and to apply appropriate internal controls and respond to inquiries about requirements (10 of 48). In addition, most states (44 of 48) reported that they had taken or planned to take additional steps—such as hiring new staff or reassigning existing staff—to help them manage their CSLFRF allocations.

As of August 2021, Treasury was developing its key internal processes and control activities for the timely monitoring of recipients’ use of their CSLFRF allocations for allowable purposes and for responding, as appropriate, to internal control and compliance findings. According to Treasury officials, the key internal processes and control activities had not been finalized or documented. The officials noted that program development has occurred within a short time frame since the enactment of ARPA in March 2021, and that finalizing and documenting internal processes and control activities for this new program requires time and resources. Further, vacancies in top-level leadership positions in the Office of Recovery Programs, which Treasury established in April 2021, have contributed to uncertainty about how the final program policies and procedures will be implemented.

Until Treasury properly designs and documents policies and procedures to guide CSLFRF program officials and other responsible oversight parties in the Office of Recovery Programs, there is a risk that key control activities needed to help ensure program management fulfills its recipient monitoring and oversight responsibilities may not be established or applied effectively and consistently. This risk may be particularly acute with monitoring state and local recipients that face capacity challenges in managing their CSLFRF allocations in accordance with federal requirements, as some noted in our survey.

We are recommending that the Secretary of the Treasury design and document timely and sufficient policies and procedures for monitoring CSLFRF recipients to provide assurance that recipients are managing their allocations in compliance with laws, regulations, agency guidance, and award terms and conditions, including ensuring that expenditures are made for allowable purposes. Treasury agreed with the recommendation and stated that it is in the process of designing, documenting, and implementing a risk-based compliance program to monitor recipient use of CSLFRF program funds.

Federal and state entities continue to investigate and report on high levels of fraud, potential fraud, and fraud risks in the unemployment insurance (UI) programs overseen at the federal level by the Department of Labor (DOL). For example, in June 2021, DOL’s Office of Inspector General reported that it had identified nearly $8 billion in potentially fraudulent UI benefits paid from March 2020 through October 2020. In addition, from March 2020 through July 2021, 71 individuals pleaded guilty to federal charges of defrauding UI programs, and federal charges were pending against 192 individuals.

In addition to a substantial increase in fraudulent and potentially fraudulent activity in UI programs, DOL officials stated that the types of fraud observed during the pandemic differed from historical UI fraud risks and schemes observed before the pandemic. While DOL continues to identify and implement strategies to address potential unemployment insurance fraud and has ongoing program integrity activities to identify risks, it has not comprehensively assessed fraud risks in alignment with leading practices identified in our Fraud Risk Framework, which by law must be incorporated into guidelines established by the Office of Management and Budget for agencies.

First, DOL has not clearly assigned defined responsibilities to a dedicated entity for designing and overseeing fraud risk management activities such as managing the fraud risk assessment process. Without a dedicated entity with defined responsibilities to lead antifraud initiatives, including the process of assessing fraud risks to UI programs, DOL may not be strategically managing UI fraud risks. For example, a dedicated antifraud entity could, among other activities, manage the fraud risk assessment process and coordinate antifraud initiatives across an agency’s various programs to assure that agency activities called for by the Fraud Risk Framework are conducted.

We are recommending that the Secretary of Labor designate a dedicated entity and document its responsibilities for managing the process of assessing fraud risks to the unemployment insurance program, consistent with leading practices as provided in our Fraud Risk Framework. This entity should have, among other things, clearly defined and documented responsibilities and authority for managing fraud risk assessments and for facilitating communication among stakeholders regarding fraud-related issues. DOL neither agreed nor disagreed with this recommendation. DOL stated that the department’s Chief Financial Officer and the Employment and Training Administration’s Assistant Secretary are the designated senior executive officials responsible for risk assessment and management of the UI program. While this approach may incorporate the roles and responsibilities of a dedicated antifraud entity, it is important that, consistent with our Fraud Risk Framework, DOL clearly document this designation and these senior staff members’ antifraud responsibilities.

Second, DOL has not comprehensively assessed UI fraud risks in alignment with leading practices or documented a prioritized approach to managing fraud risks. Our Fraud Risk Framework calls for federal managers to plan regular fraud risk assessments and determine a fraud risk profile. Specifically, the fraud risk assessment should be tailored to the program and conducted at regular intervals as well as when there are changes to the program or operating environment, such as for program operations and expansions during emergencies.

Without comprehensively assessing UI fraud risks, DOL lacks reasonable assurance that it has identified the most significant fraud risks for the regular UI program that will exist after the pandemic. For example, some fraud risks identified in the CARES Act UI programs may continue to exist in the regular UI program after the temporary UI programs expire. An analysis of fraud risks across all UI programs would also help DOL determine whether additional fraud controls are needed for the regular UI program and could position DOL to deal more effectively with any future emergency UI programs.

We are also recommending that the Secretary of Labor (1) identify inherent fraud risks facing the unemployment insurance program; (2) assess the likelihood and impact of inherent fraud risks facing the program; (3) determine fraud risk tolerance for the program; (4) examine the suitability of existing fraud controls in the program and prioritize residual fraud risks; and (5) document the fraud risk profile for the program. DOL neither agreed nor disagreed with this recommendation. DOL said its current process allows it to identify, evaluate, and manage risks. However, DOL also said it will incorporate the recommended practices and approaches moving forward.

FEMA’s Disaster Relief Fund and Assistance to State, Local, Tribal, and Territorial Governments

The Federal Emergency Management Agency (FEMA) is using the Disaster Relief Fund to respond to the COVID-19 pandemic, which is the first time the fund has been used during a nationwide public health emergency.[28] For example, FEMA’s Public Assistance Program helps state, local, tribal, and territorial governments, and certain types of private nonprofit organizations respond to and recover from major disasters or emergencies. From September 1, 2020, to August 31, 2021, FEMA obligated a total of approximately $26.8 billion to Public Assistance projects for emergency protective measures, such as eligible medical care, the purchase and distribution of food, and distribution of personal protective equipment.

We found that FEMA inconsistently interpreted and applied its policies for expenses eligible for COVID-19 Public Assistance within and across its 10 regions. For example, officials in one state said that, at one point, FEMA had deemed the provision of personal protective equipment at correctional facilities as ineligible for reimbursement in their region but that states in other regions had received reimbursement for the same expense.

We identified four key areas that contributed to the inconsistent interpretation and application of COVID-19 policies for Public Assistance based on our discussions with FEMA headquarters officials and state emergency managers. These four areas are (1) changes in policy that were interpreted and applied differently by FEMA personnel as FEMA used the Public Assistance Program for the first time to respond to a nationwide emergency; (2) delegation of authority to FEMA regions for making final application eligibility determinations; (3) lack of required training on COVID-19 policies for staff handling Public Assistance applications; and (4) variation in the experience level of staff making eligibility determinations for applications. FEMA officials stated that it has been difficult to ensure consistency in policies as different states and regions are not experiencing the same things at the same time.

FEMA officials have acknowledged that in spite of efforts to ensure consistency in interpretation and application of its Public Assistance COVID-19 policy, inconsistent interpretation and application of its policy continue to occur within and across regions. Given the current rise in the COVID-19 Delta variant across the nation, FEMA is likely to receive applications for reimbursement for a larger number of projects than it estimated earlier in 2021.

We are recommending that the Federal Emergency Management Agency Administrator improve the consistency of the agency’s interpretation and application of the COVID-19 Public Assistance policy within and across regions by further clarifying and communicating eligibility requirements nationwide.

We are also recommending that the Federal Emergency Management Agency Administrator require the agency’s Public Assistance program employees in the regions and at its Consolidated Resource Centers to attend training on changes to COVID-19 Public Assistance policy to help ensure it is interpreted and applied consistently nationwide.

The Department of Homeland Security agreed with both recommendations and outlined actions it has taken to improve the consistency of its interpretation and application of COVID-19 Public Assistance policy and to train employees in the regions and at its Consolidated Resource Centers.

Treasury has executed 35 loan agreements with certain aviation businesses and other businesses deemed critical to maintaining national security (national security businesses).[29] These loans have totaled about $22 billion of the $46 billion authorized by the CARES Act for loans and loan guarantees. Of these 35 loans, as of October 1, 2021, 10 loans had been fully repaid and the total value of outstanding loans was about $1.1 billion.

As directed by the CARES Act, Treasury required certain loan recipients to provide financial assets, such as warrants—an option to buy shares of stock at a predetermined price before a specified date—which give the federal government the ability to protect taxpayer interests. In addition, the CARES Act provided that for the primary benefit of taxpayers Treasury may sell, exercise, or surrender financial instruments it obtained. Treasury received warrants from nine businesses equal to 10 percent of the total loan amount drawn. Treasury has not exercised any of the warrants for stock it holds in these nine businesses.

According to Treasury officials, it is likely that—if the airline industry continues to recover and borrowers do not default—the warrants could have higher values than the predetermined price Treasury would have to pay to act on them. For example, based on the stock price at market close on October 1, 2021, its warrants from one borrower would be valued at 159 percent above the initial value at which Treasury received them. However, Treasury has not developed policies and procedures to guide when to act on the warrants to benefit the taxpayer.

We are recommending that the Secretary of the Treasury develop policies and procedures to determine when to act on warrants obtained as part of the loan program for aviation and other eligible businesses to benefit the taxpayers. Treasury agreed with our recommendation and said it is in the process of creating a policy that will allow it to evaluate when and how to act to dispose of the warrants obtained as part of the loan program.

As of September 2021, Treasury had made $59 billion in payments out of $63 billion provided to the Payroll Support Program to support aviation business.[30] These payments, made to air carriers and aviation contractors, were to be used exclusively for the continuation of wages, salaries, and benefits.

Similar to Treasury’s loan program for aviation and other businesses described above, the CARES Act allowed the department to receive financial instruments from these businesses to provide appropriate compensation to the federal government for providing the financial assistance, and Treasury required 14 recipients to provide warrants. These 14 recipients provided a total of 58 million warrants.

As Treasury continues to hold these warrants for stock purchases—and as the airline industry recovers—these warrants may increase in value. Treasury has not exercised any of the warrants for stock it holds in the 14 businesses, nor has the agency documented policies and procedures to guide when to act on the warrants to provide appropriate compensation to the federal government.

We are recommending that the Secretary of the Treasury develop policies and procedures to determine when to act on warrants obtained as part of the Payroll Support Program to provide appropriate compensation to the federal government. Treasury agreed with our recommendation and said it is in the process of creating a policy that will allow it to evaluate when and how to act to dispose of the warrants obtained as part of the Payroll Support Program.