TECHNOLOGY BUSINESS MANAGEMENT

Critical Go or No Go Action Required on Federal Agency Adoption of IT Spending Framework

Report to Congressional Requesters

United States Government Accountability Office

View GAO‑25‑106488. For more information, contact Carol C. Harris at harriscc@gao.gov.

Highlights of GAO‑25‑106488, a report to congressional requesters

Technology Business Management

Critical Go or No Go Action Required on Federal Agency Adoption of IT Spending Framework

Why GAO Did This Study

In 2017, OMB announced its intention to improve insights into IT spending through government-wide adoption of the Technology Business Management framework. This framework provides a standard taxonomy that is organized into four layers (cost pools, IT resources, solutions, and business units and capabilities). It is intended to show an organization’s total IT spending from financial, technology, and business perspectives.

GAO was asked to review federal agencies’ TBM implementation. GAO’s objectives were to (1) summarize its 2022 TBM report and the implementation status of recommendations it made, (2) evaluate the extent to which agencies have implemented selected leading TBM practices, and (3) identify agency costs and benefits attributed to TBM.

GAO reviewed its prior report on TBM and assessed actions taken to implement its seven recommendations. GAO also evaluated the extent to which 26 federal agencies implemented two leading TBM practices. Further, GAO interviewed agency officials regarding selected practices and reporting of TBM implementation costs and benefits.

What GAO Recommends

GAO is making one recommendation to OMB to either (1) terminate the stalled government-wide TBM effort or (2) deem TBM an Administration priority. OMB neither agreed nor disagreed with the recommendation.

What GAO Found

The Technology Business Management (TBM) framework focuses on organizations using a standard taxonomy to describe and report IT costs, resources, and solutions. GAO previously reported in 2022 that the Office of Management and Budget (OMB) and General Services Administration (GSA) took steps in 2017 to lead government-wide TBM adoption, but progress and results were limited. Specifically, OMB’s initial 2017 plans required agencies to report IT spending in layer one’s nine categories (e.g., facilities and power, hardware, and software) and layer two’s 11 categories (e.g., applications, data centers, and networks). However, as GAO previously reported, 5 years after its initial plans, OMB had not expanded requirements to include the rest of the taxonomy.

In its 2022 report, GAO made seven recommendations to OMB and GSA to establish requirements for completing the taxonomy and to address other concerns central to demonstrating that TBM is an Administration priority. However, as of March 2025, one of the seven recommendations has been partially implemented while five have not been implemented, including requiring taxonomy completion.

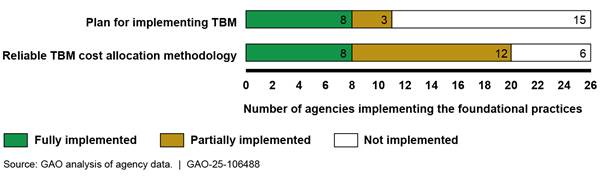

Given OMB’s lack of guidance, most agencies had not developed a plan for implementing TBM and had not fully established a reliable cost allocation methodology. Specifically, 15 of 26 agencies GAO reviewed did not have a plan for implementing TBM while 18 agencies had either partially implemented or not implemented a reliable cost allocation methodology (see fig.).

Regarding costs to implement TBM and any resulting benefits, 12 of 26 agencies provided GAO with their total reported costs. These individual agency costs ranged from approximately $1.5 million to $28.9 million. According to these agencies, the costs were associated with government labor, contractors, tools/licenses, or training for all or part of the time spanning fiscal years 2017 through 2023. Further, agencies reported some benefits, such as increased transparency into IT spending, but did not identify any cost savings.

OMB’s lack of action and guidance over the last 8 years has led to substantial TBM delays. While costs continue to mount, full TBM implementation is stalled. Action is required now to determine the future of TBM in the federal government.

Abbreviations

|

CIO |

Chief Information Officer |

|

DHS |

Department of Homeland Security |

|

DOD |

Department of Defense |

|

EPA |

Environmental Protection Agency |

|

GSA |

General Services Administration |

|

HHS |

Department of Health and Human Services |

|

HUD |

Department of Housing and Urban Development |

|

IT |

information technology |

|

NARA |

National Archives and Records Administration |

|

NASA |

National Aeronautics and Space Administration |

|

NRC |

Nuclear Regulatory Commission |

|

NSF |

National Science Foundation |

|

OMB |

Office of Management and Budget |

|

OPM |

Office of Personnel Management |

|

SBA |

Small Business Administration |

|

SSA |

Social Security Administration |

|

TBM |

Technology Business Management |

|

USACE |

U.S. Army Corps of Engineers |

|

USAID |

U.S. Agency for International Development |

|

VA |

Department of Veterans Affairs |

This is a work of the U.S. government and is not subject to copyright protection in the United States. The published product may be reproduced and distributed in its entirety without further permission from GAO. However, because this work may contain copyrighted images or other material, permission from the copyright holder may be necessary if you wish to reproduce this material separately.

July 17, 2025

The Honorable James Comer

Chairman

The Honorable Robert Garcia

Ranking Member

Committee on Oversight and Government Reform

House of Representatives

The Honorable Jamie Raskin

House of Representatives

The federal government spends more than $100 billion annually on IT. However, the government has faced longstanding challenges in IT management and spending transparency. For example, we have previously reported on issues with Chief Information Officers’ (CIO) authority over and visibility into IT in their agencies’ acquisition and budgeting processes across the government.[1] Accordingly, since 2015 we have included improving the management of IT acquisitions and operations on our High-Risk List.[2]

In August 2017, the Office of Management and Budget (OMB) announced its intention to improve insights into IT spending through the government-wide adoption of Technology Business Management (TBM).[3] According to OMB’s guidance, it planned to modernize the federal IT budgeting process into a TBM-based approach that would require agencies to use the TBM Council’s taxonomy to categorize and report spending on IT investments as part of their annual budget requests.[4]

In addition, OMB designated itself and the General Services Administration (GSA) as responsible for leading the government-wide adoption of TBM. In September 2022, we reported that OMB and GSA had taken steps to lead government-wide TBM adoption. However, we found that progress and results were limited.[5] As a result, we concluded that the continuing absence of OMB direction could cloud agency efforts and prevent the federal government from fully achieving intended benefits from TBM. Accordingly, we made seven recommendations to the agencies. As of March 2025, one of the seven recommendations has been fully implemented.

You requested that we review federal agencies’ implementation of TBM. Our objectives were to (1) summarize GAO’s 2022 TBM report and the implementation status of recommendations it made, (2) evaluate the extent to which agencies have implemented selected leading TBM practices, and (3) identify agency costs and benefits attributed to TBM.

To address the first objective, we reviewed OMB and GSA documentation, including IT capital planning guidance and artifacts on benchmarking functionality, to determine what actions, if any, OMB and GSA had taken to address prior recommendations made in our 2022 TBM report.[6] We also interviewed OMB and GSA officials responsible for TBM about the status of their efforts to address our prior recommendations.

To address the second objective, we focused on the 26 federal agencies that must adhere to TBM reporting requirements.[7] We analyzed guidance developed by the TBM Council, GSA, and OMB.[8] The guidance includes leading practices for implementing TBM. We identified two practices that were of particular importance for federal agencies that are implementing TBM regardless of their level of maturity or organizational structure, size, and resources. These two practices are: (1) develop a plan for implementing TBM and (2) establish a reliable cost allocation methodology. We then collected relevant documentation from the 26 agencies, such as plans and roadmaps for implementing TBM and documentation regarding procedures and guidance for allocating costs to the taxonomy. We analyzed the documentation and compared it against the selected leading practices and their associated criteria elements. We also interviewed cognizant agency officials from each of the 26 agencies to discuss their implementation of selected leading practices and causes for any gaps.

Based on our assessment of the documentation and discussion with agency officials, we assessed each agency’s implementation of the two leading practices as:

· fully implemented—the agency provided evidence that showed it had fully or largely addressed the elements of the practice;

· partially implemented—the agency provided evidence that showed it had addressed at least part of the practice; and

· not implemented—the agency did not provide evidence that it had addressed any part of the practice.

To address the third objective, we obtained and reviewed written responses from the 26 agencies on the total costs and benefits they attributed to implementing TBM. We also asked agencies to provide any cost savings they may have realized from their implementations. We did not receive any cost savings estimates from agencies. Additional details about our objectives, scope, and methodology are discussed in appendix I.

We conducted this performance audit from January 2023 to July 2025 in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

Background

Established by the TBM Council, TBM is a framework focused on providing technology, finance, and business leaders with standards for managing the value that IT brings to their organizations. The TBM Council is a nonprofit professional organization established in 2012 that is dedicated to advancing the discipline of TBM.[9]

According to the council, organizational leaders can leverage TBM to understand trade-offs between specific IT investment decisions, such as the extent to which consuming more of a particular technology will increase cost or reduce performance. Additionally, the council stated that organizations could use these insights to accelerate initiatives such as consolidating storage, servers, data centers, and vendors; transitioning applications to cloud services; and retiring legacy applications.

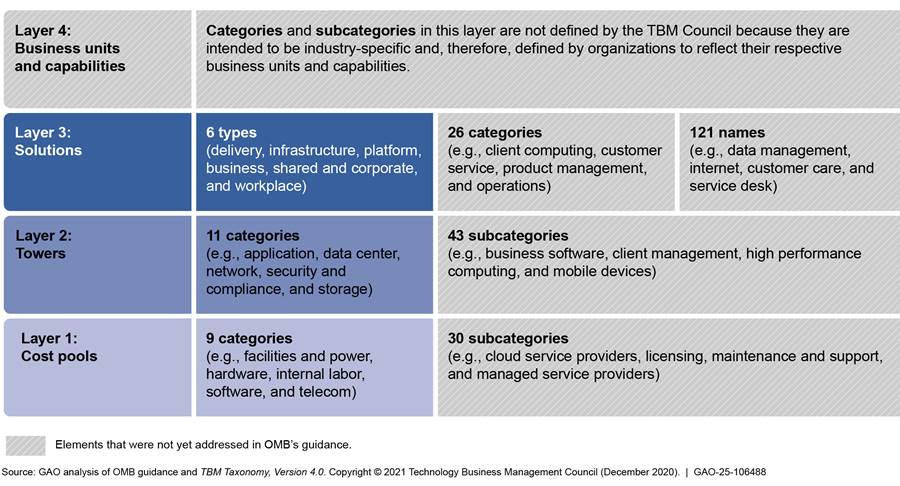

The TBM framework includes a taxonomy that, according to the council, provides a common language for categorizing, comparing, and reporting IT spending. The taxonomy is organized into four layers that are intended to show an organization’s total IT spending from different perspectives. Each of the four layers of the taxonomy is comprised of higher-level IT spending categories, which are then decomposed into more specific subcategories.

· Layer 1 (cost pools). Describe IT spending using terms that are often closely aligned to an organization’s general ledger accounts, which capture expenditures and expenses for financial reporting.

· Layer 2 (towers). Describe IT spending in terms of the IT resources (i.e., assets and technologies) that an organization typically uses to develop and support products and services.

· Layer 3 (solutions). Describe IT spending in terms of the technology solutions that the organization provides to its internal and external users (e.g., computing devices and software, infrastructure services such as facilities and networks, and shared services for core operating capabilities).

· Layer 4 (business units and capabilities). Describe IT spending in terms of how products and services support the organization’s business units, customers, and business partners. This layer also describes IT spending in terms of the capabilities and processes that enable business outcomes.

According to the TBM Council, to establish each layer, organizations need to allocate their IT cost and consumption data up through the taxonomy, layer by layer, beginning with layer 1 (cost pools). To accurately allocate their cost and consumption data to the taxonomy, organizations may need to collect different types of data across functional areas and systems (e.g., general ledger, human resources, projects, services, service desk, and vendors).

The TBM Council stated that when organizations allocate their cost and consumption data to the taxonomy, they are ideally able to capture the same amount of total IT spending in each layer. According to the council, instances in which an organization’s IT spending totals are inconsistent among layers of the taxonomy can be useful for identifying data gaps and irregularities. For example, because financial systems are intended to capture all IT spending, data inconsistencies could help organizations to uncover spending on “shadow IT” (i.e., technologies that were purchased or built without the knowledge of the organization’s CIO). According to the council, unsanctioned technologies not only represent compliance and security risks to the enterprise, but they also make it difficult to understand actual investment and spending on technologies.

The council also stated that, as organizations begin to adopt the TBM framework, they are often challenged to obtain the quality cost and consumption data that they need to accurately allocate their IT spending to the taxonomy. The council stated that low-quality data (e.g., data that are inaccurate, incomplete, or not current) can result in inaccurate allocations and reporting and, ultimately, impede organizations’ abilities to make data-driven decisions. However, the council stressed that organizations will never have perfect data and, therefore, they should start with what is available and work toward obtaining better data over time. Thus, the council recognized that successful TBM programs often take an iterative approach to adopting the framework, with an emphasis on maturing over time.

Further, the council stated that organizations typically rely on software to support their TBM processes. For example, software tools could automate the collection of cost data from a variety of sources, identify and fix errors, and allocate data to the taxonomy’s categories and subcategories using defined rules. The council stated that automated tools, as opposed to manual approaches, could allow organizations to create interactive dashboards and regularly produce meaningful reports that facilitate detailed analyses of their TBM data. Because organizations cannot predict all of their reporting needs, automated tools could also provide users with the ability to access and manipulate TBM data and create their own reports more quickly.[10]

OMB Guidance Called for Agencies to Implement TBM

In August 2017, OMB announced its intention to improve insights into IT spending through the government-wide adoption of TBM.[11] According to OMB’s guidance, it planned to modernize the federal IT budgeting process into a TBM-based approach that would require agencies to use the TBM Council’s taxonomy to categorize and report spending on IT investments as part of their annual budget requests. By integrating TBM into the IT budgeting process, OMB expected to increase transparency into federal IT spending, enable benchmarking, and enhance investment decision making.

OMB also stated in August 2017 that it planned to use a phased, multi-year approach to make the shift to TBM. OMB’s guidance recognized that each agency had a different level of maturity, capability, and resources to address the changes needed for TBM. OMB expected that the gradual approach would provide agencies with an extended period of time to understand and implement the new requirements, and to ease the eventual transition to incorporating the entire TBM taxonomy into the IT budgeting process.

OMB’s guidance included high-level time frames for when agencies need to begin reporting, such as identifying which fiscal year agencies need to report a certain set of TBM taxonomy elements. OMB’s initial plans required agencies to begin incrementally reporting categories using layer 1 (cost pools) and layer 2 (towers) over a 3-year period, as part of their annual IT budget requests for fiscal years 2019 through 2021. OMB continued to require the reporting of these layers over the next 3 years (fiscal years 2022 through 2024).[12]

In subsequent guidance, OMB required agencies to begin incrementally reporting elements in layer 3 (solutions) over a 4-year period (fiscal years 2025 through 2028).[13] Specifically, for fiscal year 2025, OMB required agencies to submit spending data on standard IT investments using three of six types in the solutions layer.[14] For fiscal year 2026, OMB expanded the requirements to include reporting on all IT investments using the same three types. For fiscal years 2027 and 2028, OMB called for agencies to build toward reporting on all IT investments using the six types in the solutions layer and ensuring alignment of those costs with reported costs under layers 1 and 2 (cost pools and towers).[15] Figure 1 shows the elements of the TBM taxonomy (e.g., layers, categories, and subcategories) and identifies which elements are required by OMB.

Figure 1: Overview of the Technology Business Management (TBM) Taxonomy Version 4.0 and Elements Required by the Office of Management and Budget (OMB)

Note: The TBM Council’s most current version of the taxonomy is version 4.1. We used version 4.0 because OMB’s requirements for TBM referenced version 4.0.

As previously mentioned, OMB designated itself and GSA as responsible for leading the government-wide adoption of TBM. Specifically, OMB’s Office of the Federal CIO is to provide leadership for the policy, planning, and budgeting aspects of TBM adoption in order to ensure success; and develop strong data standards and implementation guidance. In addition, GSA’s Office of Government-wide Policy is to serve as a central program management office to integrate TBM efforts, coordinate acquisition efforts with GSA’s Federal Acquisition Service, assist with OMB’s strategy and implementation efforts for all agencies, and support a TBM community of practice.[16]

The TBM community of practice is referred to as the Federal Technology Investment Management Community of Practice. According to its charter, this group was intended to create a cross-agency community of federal partners that provide feedback to OMB’s Office of the Federal CIO and mature the integration of TBM, IT capital planning and investment control, and portfolio management practices in the federal government through the sharing of best practices and lessons learned.[17] Further, federal agencies are responsible for implementing and maturing TBM within their agencies and serving on the TBM community of practice to provide ongoing input into capital planning and investment control reform as well as strategy development and implementation efforts.

Status of Federal Agencies’ Implementation of the TBM Taxonomy

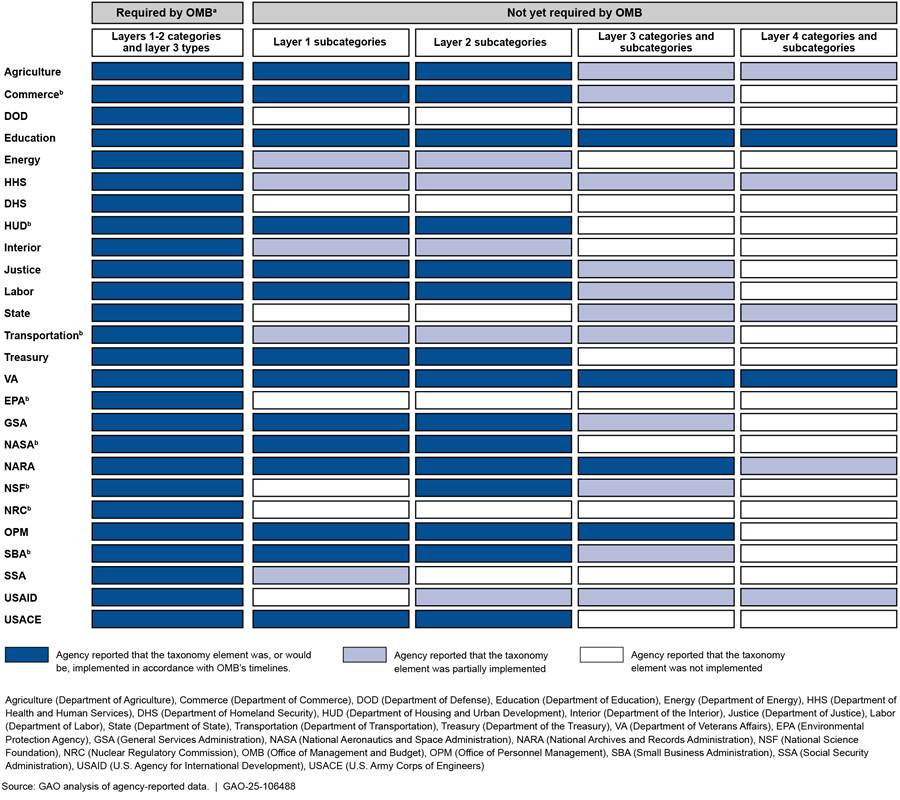

While OMB does not yet require agencies to implement the entire TBM taxonomy, it encourages them to implement additional elements that are not yet required. All 26 agencies reported that they had implemented the TBM taxonomy elements that were required by OMB. In addition, they reported they were at various stages of implementing the elements not yet required by OMB. For example,

· Two agencies (the Departments of Education and Veterans Affairs (VA)) reported they have implemented all elements of the TBM taxonomy not yet required by OMB.

· Twenty agencies (the Departments of Agriculture, Commerce, Energy, Health and Human Services (HHS), Housing and Urban Development (HUD), the Interior, Justice, Labor, State, Transportation, and the Treasury; GSA, National Aeronautics and Space Administration (NASA), National Archives and Records Administration (NARA), National Science Foundation (NSF), Office of Personnel Management (OPM), Small Business Administration (SBA), Social Security Administration (SSA), U.S. Agency for International Development (USAID), and U.S. Army Corps of Engineers (USACE)) reported they have implemented some, but not all, elements of the TBM taxonomy not yet required by OMB.

· Four agencies (the Departments of Defense (DOD) and Homeland Security (DHS), Environmental Protection Agency (EPA), and Nuclear Regulatory Commission (NRC)) reported they have only implemented the elements that were required by OMB.

Figure 2 summarizes the reported status of implementing the TBM taxonomy for each of the 26 agencies, as of December 2024.

Figure 2: Implementation Status of Technology Business Management (TBM) Taxonomy Version 4.0 Elements Reported by 26 Federal Agencies, as of December 2024

aThe TBM taxonomy elements required by OMB included all nine categories in layer 1 (cost pools), all 11 categories in layer 2 (towers), and all six types in layer 3 (solutions).

bThe agency discussed future plans to implement some additional elements that it had not yet implemented.

Agencies that have not implemented all elements of the TBM taxonomy that were not yet required by OMB offered various explanations. Specifically, many of the agencies said they intended to wait for OMB to issue additional TBM requirements because it takes significant resources to implement taxonomy elements, they faced competing priorities, or they wanted to focus on improving the quality of the data that is currently required.

Additional explanations provided by agencies include the following:

· EPA officials stated that the agency maps the TBM taxonomy onto the existing financial account code structure and any changes to the account code structure would take significant resources and time to implement.

· NASA officials stated that implementing additional taxonomy elements could lead to future rework and incur additional costs if the agency’s implementation did not align with OMB’s future requirements.

· Interior officials stated that their current focus is on implementing the required data elements and improving data quality to support decision making. They also stated that implementation of the additional elements would likely require stakeholders across the department to dedicate a significant number of resources to implement new processes for mapping IT portfolio data to the additional TBM elements.

OMB Progress on Implementing GAO Recommendations to Improve Federal TBM Adoption Continues to Be Stalled

In September 2022, we reported that OMB and GSA had taken steps to lead government-wide TBM adoption, but progress and results were limited.[18] For example, we found that OMB had not expanded on its requirements for agencies to report additional TBM taxonomy elements. Specifically, OMB’s initial 2017 plans required agencies to report IT spending in layer one’s nine categories (e.g., facilities and power, hardware, and software) and layer two’s 11 categories (e.g., applications, data centers, and networks). However, OMB had not expanded requirements to include the rest of the taxonomy—the categories in layers three and four and layer one’s 30 subcategories and layer two’s 41 subcategories.

OMB staff from the Office of the Federal CIO stated that they planned to begin adopting the third layer and intended to incorporate the fourth layer and subcategories in the future, but OMB had not documented its intention in relevant plans or had time frames for doing so. OMB staff said they were considering how to implement the remaining elements in light of resource constraints facing agencies (e.g., ongoing issues with the quality of agencies’ data). They also stated that it would be more difficult for agencies to implement the fourth layer because of the complex and diverse missions across the federal enterprise.

We also found that OMB and GSA had not assessed agencies’ maturity in their implementation of TBM government-wide. OMB staff and GSA officials stated that the maturity of data can vary among agencies, and they did not know which agencies had better quality data. They also said agencies were encouraged to mature their TBM implementations beyond what is required. However, they could not identify the extent to which agencies had taken such additional steps.

Further, when asked about agency progress and next steps, OMB staff and GSA officials referred to the TBM maturity model assessment as a tool that could be leveraged to help agencies measure and improve their implementations.[19] However, the model was an optional tool for agencies to use, and OMB and GSA were not collecting completed assessments from agencies or tracking which agencies were using the tool. According to OMB staff and GSA officials, they were taking a consensus-driven approach to encouraging government-wide TBM maturity. We noted that the use of an existing tool like the TBM maturity model assessment could provide a consistent method for measuring progress across agencies.

We concluded that progress on the TBM taxonomy had stalled because 5 years after establishing initial plans, OMB had not provided additional guidance on implementing most of the taxonomy. Although OMB staff maintained that TBM continued to be a priority, the lack of accompanying action on the taxonomy increased uncertainty about agency TBM efforts. We further stated that the continuing absence of OMB direction could prevent the federal government from fully achieving intended benefits such as optimizing IT spending. We also noted that, by not assessing agency maturity, OMB and GSA had limited insights into government-wide progress and the extent that it is providing benefits to agencies that implement TBM.

Accordingly, we made seven recommendations—six to OMB and one to GSA—to help strengthen efforts to lead federal adoption of TBM. OMB neither agreed nor disagreed with our recommendations and GSA agreed with our recommendation. However, limited progress has been made on implementing these recommendations, with only one recommendation fully implemented, one partially implemented, and five not yet implemented, as of March 2025. Specifically,

· GSA implemented our recommendation to develop TBM benchmarking functionality for the IT Dashboard. The functionality was released on the dashboard in February 2023 and allows users to compare their TBM data to other agencies that share similar characteristics, such as the agency’s IT budget range or business function. It also allows users to download their benchmarking comparison data.

· OMB has partially implemented our recommendation to establish plans and time frames for government-wide TBM adoption that addresses the remaining elements of the taxonomy. Specifically, OMB’s plans have addressed some portions of layer 3 (solutions); however, several additional elements of the taxonomy remain to be addressed (as shown in figure 1).

· OMB has not yet implemented the other five recommendations related to (1) establishing an approach for assessing the maturity of agencies’ TBM implementation, (2) requiring all agencies to complete and submit the TBM maturity model assessment tool to OMB and GSA, (3) updating budget object classification codes to better align agencies’ financial management systems with the TBM taxonomy, (4) ensuring that known limitations in the TBM data for fiscal year 2021 are publicly disclosed on the IT Dashboard, and (5) analyzing inconsistencies in agency-reported TBM data to determine why agencies are reporting differences between their TBM and IT portfolio spending data.

For each of these six open recommendations, OMB reported in March 2024 that it had actions planned to address them that were not yet underway. However, OMB did not provide additional information such as what specific actions were planned and associated time frames. As of March 2025, we have not received additional information on OMB’s plans.

Few Agencies Have Fully Implemented Selected Leading TBM Practices

According to the TBM Council and federal guidance, implementing TBM is an iterative approach and having a clear plan to execute priorities and find ways to keep maturing data over time can increase the likelihood that the TBM implementation will be successful.[20] In addition, the guidance emphasizes the importance of ensuring consistent application of the taxonomy by having reliable processes for allocating the data across the TBM taxonomy elements. According to the guidance, doing so can increase the accuracy and timeliness of the data and ultimately improve an organization’s decision-making abilities. Two leading practices include:

1. Develop a plan for implementing TBM. The agency has developed an implementation plan that identifies key milestones and time frames, including steps needed to improve the quality of its TBM data.

2. Establish a reliable TBM cost allocation methodology. The agency has established consistent, repeatable processes for allocating costs to the TBM taxonomy (e.g., automation, documents describing the processes and any assumptions or rules that are in place, and data validation).

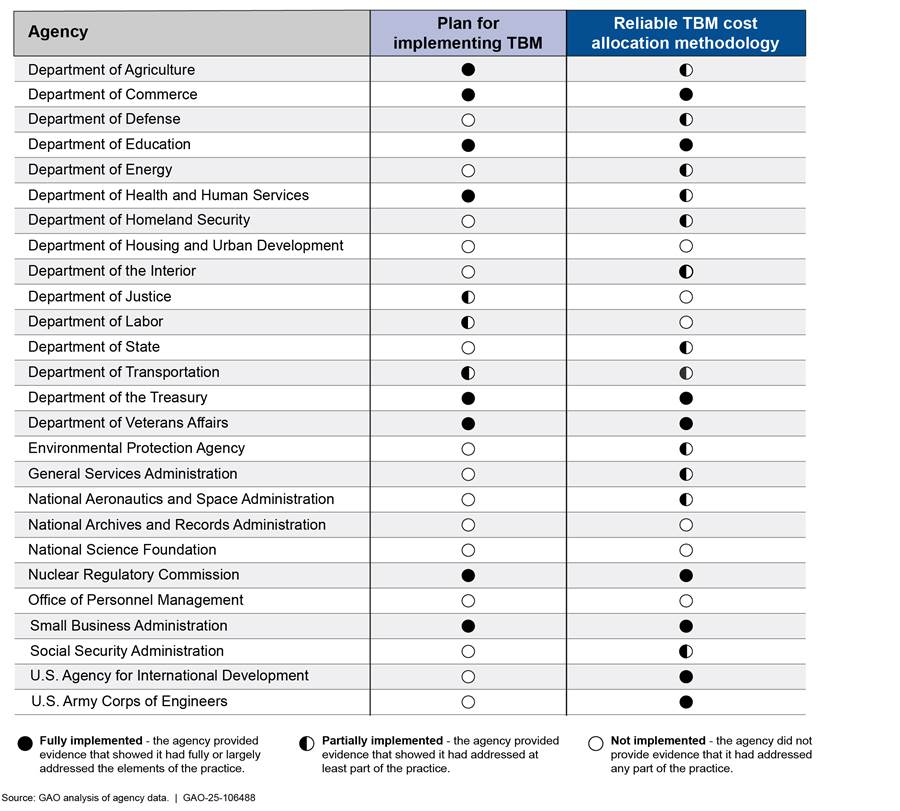

Six of the 26 agencies have fully implemented both of the selected leading practices and four of the agencies have not implemented either of the practices. The remaining 16 agencies had mixed progress implementing the practices. Figure 3 and the narrative that follows summarize the extent to which the agencies implemented the practices. A detailed discussion of agencies’ implementation of the practices is provided in appendix II.

Figure 3: Extent to Which 26 Federal Agencies Implemented Selected Leading Technology Business Management (TBM) Practices

Develop a plan for implementing TBM. Most of the 26 agencies did not fully implement this practice. Specifically,

· eight agencies fully implemented this practice (Agriculture, Commerce, Education, HHS, the Treasury, VA, NRC, and SBA),

· three agencies partially implemented this practice (Justice, Labor, and Transportation), and

· fifteen agencies did not implement this practice (DOD, Energy, DHS, HUD, Interior, State, EPA, GSA, NASA, NARA, NSF, OPM, SSA, USAID, and USACE).

For example:

· Commerce fully implemented this practice. Commerce developed roadmaps that identified key milestones and time frames for implementing TBM across its bureaus. For example, the agency had milestones planned for fiscal years 2020 through 2024, such as completing TBM maturity assessments, developing a business case for a TBM tool, and developing guidance and benchmarking standards. In addition, the roadmaps included steps needed to improve TBM data quality such as creating a standardized TBM data repository and reports, linking data to authoritative sources, and identifying data anomalies.

· Labor partially implemented this practice. Labor developed a plan that identified key milestones and time frames for implementing TBM and improving data quality for fiscal year 2022. However, the plan had not been updated since August 2022 to reflect the agency’s current plans for TBM.

· HUD did not implement this practice. HUD did not develop plans for implementing TBM that identified key milestones and time frames, including steps needed to improve the quality of the agency’s TBM data. HUD officials stated that the agency developed a draft TBM roadmap for fiscal years 2024 through 2026 that was undergoing internal review but did not provide a date by which they expected to complete this effort.

Establish a reliable TBM cost allocation methodology. Most of the 26 agencies did not fully implement this practice. Specifically,

· eight agencies fully implemented this practice (Commerce, Education, Treasury, VA, NRC, SBA, USAID, and USACE),

· twelve agencies partially implemented this practice (Agriculture, DOD, DHS, Energy, HHS, Interior, State, Transportation, EPA, GSA, NASA, and SSA), and

· six agencies did not implement this practice (HUD, Justice, Labor, NARA, NSF, and OPM).

For example:

· SBA fully implemented this practice. SBA established a reliable methodology for allocating costs to the TBM taxonomy that included documented instructions. In addition, SBA established a consistent, repeatable process for validating the accuracy of the agency’s cost allocations. Specifically, SBA developed a validation checklist with steps to identify and resolve incorrect allocations to taxonomy elements.

· DHS partially implemented this practice. DHS established a methodology for allocating costs to layer 1 (cost pools) and layer 2 (towers) of the TBM taxonomy and validating the results. However, DHS’s approach did not address all elements of the taxonomy it had implemented. Specifically, the approach did not address the portions of layer 3 (solutions) that had been required by OMB.

· NSF did not implement this practice. Officials described manual steps for allocating costs, such as analyzing each line of budget data and coding them manually to TBM taxonomy elements but did not provide documentation of its processes. According to officials, the agency is currently developing documentation of its approach for allocating and validating TBM costs and plans to complete this effort in early 2025.

Agency officials pointed to various factors that limited their implementation of the selected leading TBM practices. The most common factor, cited by nine agencies (DOD, Energy, DHS, Interior, Justice, GSA, SSA, USAID, and USACE), was that they had not fully developed agency-specific plans because they were following the implementation time frames outlined in OMB guidance. As we discussed earlier in this report, OMB guidance has only included high-level time frames for when agencies need to begin reporting, such as identifying which fiscal year agencies need to report a certain set of TBM taxonomy elements.

Further, OMB stated that the multi-year approach was intended to give agencies sufficient time to determine how to implement TBM within their organizations because OMB recognized that agencies were at different levels of maturity, capability, and resources to address the changes needed.

Agency officials also cited other factors that limited their implementation of the leading practices:

· Three agencies (DOD, Justice, and State) reported that they had not fully developed an agency-wide methodology because their components were responsible for determining how to appropriately allocate costs to the TBM taxonomy and validate the results. Nevertheless, TBM Council and federal guidance call for TBM to be implemented agency-wide and emphasize the importance of establishing a cost allocation methodology that ensures consistent application of the taxonomy.

· Two agencies (HHS and the Interior) reported that they operated in complex and federated environments with large portfolios of IT investments and systems, which impeded their abilities to fully implement agency-wide cost allocation methodologies. However, without an agency-wide approach, agencies may lack consistent and effective implementation and oversight of TBM activities. In addition, other federated agencies, such as Commerce, have shown that an agency-wide approach is possible.

· Labor officials from the Office of the CIO stated that documenting TBM processes takes time and has been challenging due to the number and variety of stakeholders involved, many of which do not reside within their office. While we agree that TBM can be a complex, agency-wide effort, establishing reliable TBM processes is important for increasing data quality and improving an organization’s decision-making abilities.

· NASA officials from the Office of the CIO stated that their office had undergone a significant reorganization that has taken priority over many activities in order to achieve the transformation’s purpose to better serve the agency and improve the delivery of IT services. These officials also stated that TBM maturity is still a goal, and the agency continues to collaborate with customers and stakeholders to improve data quality and to determine the best approach and timing for further TBM implementation.

Agency-Reported Costs and Benefits from Implementing TBM

Of the 26 agencies, 20 agencies provided information on their costs from implementing TBM. Of those 20 agencies, 12 agencies reported their total TBM implementation costs, ranging from approximately $1.5 million to $28.9 million. According to these agencies, their costs were associated with government labor, contractors, tools/licenses, or training in fiscal years 2017 through 2023. Table 1 shows the total TBM implementation costs reported by agencies.

Table 1: Total Technology Business Management (TBM) Implementation Costs for Fiscal Years 2017 Through 2023, as Reported by 12 Federal Agencies

|

Agency |

Total approximate TBM implementation costs |

Time period, in fiscal years |

|

Department of Agriculture |

$2.0 million |

2018 – 2023 |

|

Department of Commerce |

$7.9 million |

2018 – 2023 |

|

Department of Education |

$5.5 million |

2017 – 2023 |

|

Department of Health and Human Servicesa |

$1.5 million |

2017 – 2022 |

|

Department of State |

$6.8 million |

2017 – 2023 |

|

Department of the Treasury |

$5.6 million |

2021 – 2023 |

|

Department of Veterans Affairs |

$28.9 million |

2018 – 2022 |

|

General Services Administration |

$7.0 million |

2017 – 2023 |

|

National Aeronautics and Space Administration |

$15.2 million |

2017 – 2023 |

|

Nuclear Regulatory Commission |

$3.0 million |

2017 – 2023 |

|

Office of Personnel Management |

$2.2 million |

2022 – 2023 |

|

U.S. Army Corps of Engineers |

$5.7 million |

2018 – 2023 |

Source: GAO analysis of agency-reported data. | GAO‑25‑106488

aThe agency noted that the costs were high-level estimates for headquarters only and did not include costs for the agency’s bureaus.

In addition, the remaining eight agencies provided partial TBM implementation costs, such as a one-time cost for training or a current annual cost for contractor support.[21] These agencies reported costs ranging from about $1,000 to $1.3 million on government labor, contractors, software/tools/licenses, or training in fiscal years 2017 through 2023. Table 2 shows partial TBM implementation costs reported by agencies.

Table 2: Partial Technology Business Management (TBM) Implementation Costs for Fiscal Years 2017 Through 2023, as Reported by Eight Federal Agencies

|

Agency |

Partial TBM implementation costs |

|

Department of Energy |

The agency said it spends about $1.3 million annually on government labor, contractor support, tools, and training for TBM. |

|

Department of Housing and Urban Development |

The agency said it estimated spending roughly $100,000 annually on contractor support for TBM. |

|

Department of Homeland Security |

The agency said it did not separately track total costs for implementing TBM but cited about $100,000 spent annually on contractual support and system licenses for TBM. |

|

Environmental Protection Agency |

The agency stated that TBM costs are inherently connected to the IT budget program and cannot be broken out separately. However, it estimated about $50,000 in contractor support in fiscal year 2022 to develop and implement the current data model used to transform raw data from the financial system to the TBM taxonomy for external reporting and analysis. |

|

National Archives and Records Administration |

The agency said it spent about $1,000 in 2017 on TBM Executive Foundation training and certification, and that it has not spent any other funding specifically on TBM implementation or tools. |

|

Small Business Administration |

The agency said it spent about $820,000 in fiscal year 2023 on government labor, contractor support, and training. |

|

Social Security Administration |

The agency said it does not track separate time or costs for TBM because the costs are included in its overall budget. However, it cited about $20,000 in fiscal year 2017 on a TBM Council Executive Foundation Course. |

|

U.S. Agency for International Development |

The agency said it spent about $450,000 annually for contract support (based on a rough level of effort estimate, as of fiscal year 2023), and $35,700 in fiscal year 2019 on TBM training. |

Source: GAO analysis of agency-reported data. | GAO‑25‑106488

Of the 26 agencies, 20 agencies described benefits they had realized from implementing TBM. The majority of these agencies cited increased transparency into IT spending. Many of them also cited more consistent or structured IT budget formulation processes. Some agencies also identified additional benefits, such as improved collaboration within their organizations, automation of manual processes, improved data, and the ability to analyze IT spend data for decision making.

None of the agencies provided actual cost savings estimates. Specifically, 19 agencies stated they have not yet achieved any cost savings from implementing TBM. Some of these agencies indicated that they did not expect to see cost savings until after TBM is fully implemented. Although a few agencies described actions related to potential cost savings, such as cost avoidance through vendor and license management and efficiency gains in the budget formulation process, they did not have actual cost savings estimates.

Conclusions

OMB intended for TBM to improve insights into IT spending and address longstanding challenges with transparency. However, as costs continue to mount, OMB’s lack of action and guidance over the last 8 years has led to substantial TBM delays. Most concerning is that OMB has not completed its expansion of requirements for agencies to fully implement the taxonomy, which we recommended in 2022. We also made five additional recommendations to OMB to address other concerns that are central to demonstrating that TBM is an Administration priority; however, none of those recommendations have been implemented.

In the absence of OMB guidance, most agencies had not developed a plan for implementing TBM and had not fully established a reliable cost allocation methodology. Nevertheless, the agencies in our review continue to direct resources toward TBM. Given the protracted time frames of the initiative and the resources that have been aimed at it, OMB must act now to determine the future of TBM in the federal government.

Recommendation for Executive Action

The Director of OMB should direct the Federal CIO to either (1) terminate the stalled government-wide TBM effort and direct agencies to not incur further related costs or (2) deem TBM an Administration priority, expeditiously implement GAO’s prior recommendations, and take immediate action to fully implement TBM government-wide, including tracking costs and benefits (Recommendation 1).

Agency Comments and Our Evaluation

We requested comments on a draft of this report from OMB and the other 26 agencies included in our review. OMB, the one agency to which we made a recommendation, did not provide comments on the report. Of the 26 agencies to which we did not make recommendations, two agencies concurred with the information presented in our report, one agency commented on our report but neither agreed nor disagreed with our findings, and 23 agencies did not have comments on our report. In addition, three agencies provided technical comments, which we incorporated as appropriate.

The following two agencies concurred with the information presented in the report:

· In comments provided via email, a Management Analyst from the Audit Management Division stated that DOD appreciated the opportunity to review the draft report and concurred without comment.

· In comments provided via email, an Audit Coordinator from the Office of the Chief Information Officer stated that Energy concurred with the report and agreed with making TBM an administrative priority.

The following agency did not state whether it agreed or disagreed with our report:

· In written comments, reprinted in appendix III, VA provided general comments regarding its adoption of TBM and the resulting benefits. Specifically, VA stated that OMB’s requirement to report TBM elements in agency budget submissions was the catalyst for the agency’s TBM implementation. It stated that without the OMB mandate as a forcing function, as well as the Federal Technology Investment Management Community of Practice as an enabler, there would be little incentive for transparency into IT spending within a common framework across the federal government. We agree that OMB’s role is critical to the government-wide adoption of TBM.

VA also stated that it had purchased TBM cost modeling software that supports activities beyond the current OMB mandate, such as producing reliable financial data and generating customer statements for cloud cost optimization. VA stated that, in addition to investing in software, it has invested time and money to conduct data analysis and detailed monitoring of data accuracy. VA’s comments also discussed benefits associated with its TBM implementation related to improvements in the agency’s IT budget structure, cost transparency, data quality, and IT investment decision making, among other things.

We recognize there are many potential benefits from fully implementing the TBM framework. However, as discussed in our report, VA was only one of two agencies that had fully implemented the TBM taxonomy. The majority of agencies (24 of 26) had not implemented the entire taxonomy, and many of them stated they intended to wait for OMB to issue additional requirements. Further, the majority of agencies (20 of 26) had not fully developed plans for implementing TBM and established reliable cost allocation methodologies. Given the lack of progress government-wide, we concluded that OMB’s lack of action and guidance over the last 8 years have led to substantial TBM delays across the federal government. As a result, we maintain our recommendation to OMB to either terminate the stalled government-wide effort or deem TBM an Administration priority is valid.

In addition, 23 agencies did not provide comments on our report (Agriculture, Commerce, Education, HHS, DHS, HUD, the Interior, Justice, Labor, State, Transportation, the Treasury, EPA, GSA, NASA, NARA, NSF, NRC, OPM, SBA, SSA, USAID, and USACE). In addition, we received technical comments from three agencies (HUD, Labor, and GSA), which we have incorporated into the report as appropriate.

As agreed with your offices, unless you publicly announce the contents of this report earlier, we plan no further distribution until 30 days from the report date. At that time, we will send copies to the appropriate congressional committees, the heads of the agencies in our review, and other interested parties. In addition, the report will be available at no charge on the GAO website at http://www.gao.gov.

If you or your staff have any questions about this report, please contact Carol Harris at HarrisCC@gao.gov. Contact points for our Offices of Congressional Relations and Public Affairs may be found on the last page of this report. GAO staff who made key contributions to this report are listed in appendix IV.

Carol C. Harris

Director, Information Technology Acquisition Management Issues

Our objectives for this review were to (1) summarize GAO’s 2022 Technology Business Management (TBM) report and the implementation status of recommendations it made, (2) evaluate the extent to which agencies have implemented selected leading TBM practices, and (3) identify agency costs and benefits attributed to TBM.

To address the first objective, we reviewed Office of Management and Budget (OMB) and General Services Administration (GSA) documentation, including IT capital planning guidance and artifacts on benchmarking functionality, to determine what actions, if any, OMB and GSA had taken to address prior recommendations made in our 2022 TBM report.[22] We also interviewed OMB and GSA officials responsible for TBM about the status of their efforts to address our prior recommendations.

To address the second objective, we focused on the 26 federal agencies that must adhere to TBM reporting requirements.[23] We analyzed guidance developed by the TBM Council, GSA, and OMB.[24] The guidance includes leading practices for implementing TBM. We identified two practices that were of particular importance for federal agencies that are implementing TBM regardless of their level of maturity or organizational structure, size, and resources. These two practices are:

1. Develop a plan for implementing TBM. The agency has developed an implementation plan that identifies key milestones and time frames, including steps needed to improve the quality of its TBM data.

2. Establish a reliable TBM cost allocation methodology. The agency has established consistent, repeatable processes for allocating costs to the TBM taxonomy (e.g., automation, documents describing the processes and any assumptions or rules that are in place, and data validation).

We reviewed relevant documentation for each of the 26 agencies, such as plans and roadmaps for implementing TBM and documentation regarding procedures and guidance for allocating costs to the taxonomy. We then compared the information to our evaluation criteria and analyzed the documentation against the selected leading practices to identify gaps and their causes. We also interviewed cognizant officials from each of the 26 agencies to discuss their implementation of the selected leading practices and causes for any gaps. Based on our assessment of the documentation and discussion with agency officials, we assessed each agency’s implementation of the leading practices as:

· fully implemented—the agency provided evidence that showed it had fully or largely addressed the elements of the practice;

· partially implemented—the agency provided evidence that showed it had addressed at least part of the practice; and

· not implemented—the agency did not provide evidence that it had addressed any part of the practice.

To address the third objective, we obtained written responses from the 26 agencies on the total costs and benefits they attributed to implementing TBM. We also asked agencies to provide any cost savings they may have realized from their implementations. We did not receive any cost savings estimates from agencies. Twenty agencies provided cost information—either total costs from implementing TBM or partial costs. We presented these separately when summarizing agency-reported costs.

To assess the reliability of the agency-reported TBM costs, we discussed with agency officials the source of their estimates, clarified any obvious inconsistencies in the information they had provided, and any limitations in the accuracy or completeness of the data. We reviewed the agencies’ responses and determined that the data were sufficiently reliable for the purposes of this report, which was to describe TBM implementation costs as provided by agencies. We also rounded the estimates to approximate figures and included any notes regarding limitations in the data that were provided by agencies.

We conducted this performance audit from January 2023 to July 2025 in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

This appendix contains assessments of the extent to which the 26 federal agencies that report technology business management (TBM) data have implemented selected leading TBM practices.[25]

Department of Agriculture

Table 3: The Department of Agriculture’s Implementation of Selected Leading Technology Business Management (TBM) Practices

|

Leading practices |

Rating |

Description |

|

Develop a plan for implementing TBM |

Fully implemented |

Agriculture developed roadmaps that identified key milestones and time frames for implementing TBM. For example, the agency had milestones planned for fiscal years 2020 through 2024, such as enhancing TBM reporting, allocating data to additional taxonomy elements, and developing a communications plan. In addition, the roadmaps included steps needed to improve TBM data quality such as creating a standardized repository, using authentic sources, and identifying anomalies. |

|

Establish a reliable TBM cost allocation methodology |

Partially implemented |

Agriculture established a methodology with consistent, repeatable processes for allocating costs to layer 1 (cost pools) and layer 2 (towers) of the TBM taxonomy. However, the agency’s methodology did not address all elements of the taxonomy it had implemented—specifically, portions of layer 3 (solutions) and layer 4 (business units and capabilities). |

Source: GAO analysis of Agriculture data. | GAO‑25‑106488

Department of Commerce

Table 4: The Department of Commerce’s Implementation of Selected Leading Technology Business Management (TBM) Practices

|

Leading practices |

Rating |

Description |

|

Develop a plan for implementing TBM |

Fully implemented |

Commerce developed roadmaps that identified key milestones and time frames for implementing TBM across its bureaus. For example, the agency had milestones planned for fiscal years 2020 through 2024, such as completing TBM maturity assessments, developing a business case for a TBM tool, and developing guidance and benchmarking standards. In addition, the roadmaps included steps needed to improve TBM data quality such as creating a standardized TBM data repository and reports, linking data to authoritative sources, and identifying data anomalies. |

|

Establish a reliable TBM cost allocation methodology |

Fully implemented |

Commerce established consistent, repeatable processes for allocating costs to the TBM taxonomy. For example, Commerce documented and automated its processes for allocating source data to all the TBM taxonomy elements it had implemented. In addition, Commerce established a process for validating the agency’s allocations that included quarterly reporting and reviews of accuracy. |

Source: GAO analysis of Commerce data. | GAO‑25‑106488

Department of Defense

Table 5: The Department of Defense’s (DOD) Implementation of Selected Leading Technology Business Management (TBM) Practices

|

Leading practices |

Rating |

Description |

|

Develop a plan for implementing TBM |

Not implemented |

DOD had not developed plans that identify key milestones and time frames for implementing TBM, including steps needed to improve data quality. According to officials, the agency collects TBM data based on and in accordance with the Office of Management and Budget (OMB) guidance. However, as we stated earlier in our report, OMB guidance only included high-level time frames for implementing TBM taxonomy elements and did not address specifics on improving data quality because agencies were at different levels of maturity. |

|

Establish a reliable TBM cost allocation methodology |

Partially implemented |

Although DOD established guidance with business rules for allocating costs to layer 1 (cost pools) and layer 2 (towers) of the TBM taxonomy, it did not do so for layer 3 (solutions). The agency decided to leverage its own taxonomy, referred to as the Enterprise Information Environment Mission Area Definition, that appears to be consistent with TBM taxonomy elements. Components are to use the taxonomy to align their common IT assets (e.g., cybersecurity, data storage, and networking). However, DOD did not establish processes for validating the accuracy of its allocations to the TBM taxonomy elements it had implemented. Agency officials stated that the components are to determine how they allocate TBM costs and validate their allocations. However, in June 2022 we reported that DOD’s reliance on components’ quality control processes was not sufficient to ensure quality TBM data and, consequently, made a recommendation to update department-wide guidance to components regarding TBM implementation to address, among other things, how components should allocate spending for cloud services to specific cost pools and towers, and identify what control process should be in place to ensure the TBM data is reliable.a As of January 2025, DOD has only partially implemented this recommendation. |

Source: GAO analysis of DOD data. | GAO‑25‑106488

aGAO, Cloud Computing: DOD Needs to Improve Workforce Planning and Software Application Modernization, GAO‑22‑104070 (Washington, D.C.: June 29, 2022). We recommended, among other things, that DOD update department-wide guidance regarding TBM implementation.

Department of Education

Table 6: The Department of Education’s Implementation of Selected Leading Technology Business Management (TBM) Practices

|

Leading practices |

Rating |

Description |

|

Develop a plan for implementing TBM |

Fully implemented |

Education developed plans that identified key milestones and time frames for implementing TBM. For example, the agency had milestones planned for fiscal years 2020 through 2023, such as developing monthly reports using TBM data, providing training, and collecting and implementing lessons learned. The plans also included steps needed to improve TBM data quality, such as using authoritative financial and operational data sources, adopting a tool that provides real time cost and IT data, and automating data collection. |

|

Establish a reliable TBM cost allocation methodology |

Fully implemented |

Education established consistent, repeatable processes for allocating costs to the TBM taxonomy. For example, Education documented and automated its processes for collecting and allocating source data to all the TBM taxonomy elements it had implemented. In addition, Education established a process for validating TBM allocations that included confirming that allocations to taxonomy elements are accurate and, if anomalies exist, ensuring there is a valid explanation. |

Source: GAO analysis of Education data. | GAO‑25‑106488

Department of Energy

Table 7: The Department of Energy’s Implementation of Selected Leading Technology Business Management (TBM) Practices

|

Leading practices |

Rating |

Description |

|

Develop a plan for implementing TBM |

Not implemented |

Energy did not develop a plan for implementing TBM that identified key milestones and time frames, including steps needed to improve data quality. According to officials, the agency has fully met the Office of Management and Budget’s (OMB) requirements for implementing TBM. However, as we stated earlier in our report, OMB guidance only included high-level time frames for implementing TBM taxonomy elements and did not address specifics on improving data quality because agencies were at different levels of maturity. |

|

Establish a reliable TBM cost allocation methodology |

Partially implemented |

Energy established a consistent, repeatable methodology for allocating costs to layer 1 (cost pools) and layer 2 (towers) of the TBM taxonomy. However, the agency’s methodology did not address all elements of the taxonomy it had implemented—specifically, the portions of layer 3 (solutions) that had been required by OMB. Agency officials stated that Energy was in the process of developing and instituting a solutions layer cost methodology but did not provide a date by which they expected to complete this effort. |

Source: GAO analysis of Energy data. | GAO‑25‑106488

Department of Health and Human Services

Table 8: The Department of Health and Human Services’s (HHS) Implementation of Selected Leading Technology Business Management (TBM) Practices

|

Leading practices |

Rating |

Description |

|

Develop a plan for implementing TBM |

Fully implemented |

HHS developed roadmaps that identified key milestones and time frames for implementing TBM. For example, the agency had milestones planned for fiscal years 2022 through 2026, such as conducting a TBM maturity assessment, developing benchmarking guidance, and conducting TBM training. In addition, the roadmaps included steps needed to improve TBM data quality such as conducting analysis to identify gaps and maturing TBM data collection and reporting. |

|

Establish a reliable TBM cost allocation methodology |

Partially implemented |

HHS developed guidance and templates for collecting and allocating data to layer 1 (cost pools) and layer 2 (towers) of the TBM taxonomy. However, while HHS reported that it had also partially implemented layer 3 (solutions) and layer 4 (business units and capabilities), the agency’s templates did not address these layers. HHS also did not establish a process for validating the accuracy of the agency’s allocations. HHS officials stated that the agency has begun efforts to mature its approach to cost allocations that they expect will be completed by the end of fiscal year 2026. |

Source: GAO analysis of HHS data. | GAO‑25‑106488

Department of Homeland Security

Table 9: The Department of Homeland Security’s (DHS) Implementation of Selected Leading Technology Business Management (TBM) Practices

|

Leading practices |

Rating |

Description |

|

Develop a plan for implementing TBM |

Not implemented |

DHS had not developed plans that identify key milestones and time frames for implementing TBM, including steps needed to improve data quality. DHS officials stated that the agency is not implementing TBM beyond requirements set forth by the Office of Management and Budget (OMB), does not intend to establish any plans, and is satisfied with the agency’s current approach. However, as we stated earlier in our report, OMB guidance only included high-level time frames for implementing TBM taxonomy elements and did not address specifics on improving data quality because agencies were at different levels of maturity. |

|

Establish a reliable TBM cost allocation methodology |

Partially implemented |

DHS established a methodology for allocating costs to layer 1 (cost pools) and layer 2 (towers) of the TBM taxonomy and validating the results. However, DHS’s approach did not address all elements of the taxonomy it had implemented—specifically, the portions of layer 3 (solutions) that had been required by OMB. Agency officials stated that they expect to revise policies and procedures as needed to align with any future TBM requirements from OMB. |

Source: GAO analysis of DHS data. | GAO‑25‑106488

Department of Housing and Urban Development

Table 10: The Department of Housing and Urban Development’s (HUD) Implementation of Selected Leading Technology Business Management (TBM) Practices

|

Leading practices |

Rating |

Description |

|

Develop a plan for implementing TBM |

Not implemented |

HUD had not developed plans that identify key milestones and time frames for implementing TBM, including steps needed to improve data quality. HUD officials stated that the agency developed a draft TBM roadmap for fiscal years 2024 through 2026 that was undergoing internal review but did not provide a date by which they expected to complete this effort. |

|

Establish a reliable TBM cost allocation methodology |

Not implemented |

HUD did not establish consistent, repeatable processes for allocating costs to the TBM taxonomy. For example, agency officials stated that they use formulas embedded in worksheets for assigning TBM allocations; however, the worksheet did not appear to include any embedded allocation formulas. In addition, officials stated there was no other documentation, besides the workbook, on their processes for ensuring consistent allocation methods. Officials further stated that the agency expects to establish more detailed documentation on its cost allocation processes in the future but did not provide a date by which they expected to complete this effort. |

Source: GAO analysis of HUD data. | GAO‑25‑106488

Department of the Interior

Table 11: The Department of the Interior’s Implementation of Selected Leading Technology Business Management (TBM) Practices

|

Leading practices |

Rating |

Description |

|

Develop a plan for implementing TBM |

Not implemented |

Interior had not developed plans that identify key milestones and time frames for implementing TBM, including steps needed to improve data quality. Interior officials stated that the agency has met all Office of Management and Budget (OMB) reporting requirements to date and plans to continue implementing layer 3 (solutions) as outlined in OMB guidance. Interior officials also stated that improvements to the quality of the agency’s TBM data is a continuous process. However, as we stated earlier in our report, OMB guidance only included high-level time frames for implementing TBM taxonomy elements and did not address specifics on improving data quality because agencies were at different levels of maturity. |

|

Establish a reliable TBM cost allocation methodology |

Partially implemented |

Interior established consistent, repeatable processes for collecting and allocating source data to all the TBM taxonomy elements it had implemented. However, Interior did not establish processes for validating the accuracy of the agency’s allocations. According to officials, Interior’s bureaus and offices are responsible for allocating their IT investments to TBM, and due to their varied budget structures and processes, there is not a standardized process across the agency. Officials also stated that most bureaus and offices use largely manual processes because the agency’s authoritative sources (e.g., finance, budget, and acquisition systems) do not capture IT investment or TBM data elements. |

Source: GAO analysis of Interior data. | GAO‑25‑106488

Department of Justice

Table 12: The Department of Justice’s Implementation of Selected Leading Technology Business Management (TBM) Practices

|

Leading practices |

Rating |

Description |

|

Develop a plan for implementing TBM |

Partially implemented |

Justice developed a plan that identified key milestones and time frames for implementing TBM for fiscal year 2025. For example, the plan identified key milestones such as developing recommendations for allocation methodologies and validation processes to ensure that TBM reporting for layer 1 (cost pools) and layer 2 (towers) is consistent and accurate. However, while Justice’s plan identified time frames for implementing layer 3 (solutions), it did not include steps needed to improve data quality for this layer. Justice officials stated that the agency’s plan for improving data quality is pending further guidance from the Office of Management and Budget (OMB). However, as we stated earlier in our report, OMB guidance only included high-level time frames for implementing TBM taxonomy elements and did not address specifics on improving data quality because agencies were at different levels of maturity. |

|

Establish a reliable TBM cost allocation methodology |

Not implemented |

Justice did not establish consistent, repeatable processes for allocating data to the TBM taxonomy. Justice officials stated that the agency delegates the responsibility of allocating IT budget data to its components and that it does not have an enterprise-wide automation tool or process. Officials also stated that the components’ processes are largely manual and very labor intensive. Thus, the agency has focused on larger scale data integrity for items where mapping may have been incomplete. According to Justice documentation, the agency expects to develop recommendations for allocating and validating TBM data in fiscal year 2025. |

Source: GAO analysis of Justice data. | GAO‑25‑106488

Department of Labor

Table 13: The Department of Labor’s Implementation of Selected Leading Technology Business Management (TBM) Practices

|

Leading practices |

Rating |

Description |

|

Develop a plan for implementing TBM |

Partially implemented |

Labor developed a plan that identified key milestones and time frames for implementing TBM for fiscal year 2022. The plan identified key activities such as facilitation training, leveraging organizational change management best practices, and publishing standard operating procedures. The plan also included steps needed to improve data quality such as establishing expectations and next steps for improvement. However, Labor’s plan was dated August 2022 and had not been updated to reflect the agency’s current plans for TBM. Labor officials stated that they were developing a roadmap for improved TBM adoption and implementation, but did not provide a date by which they expected to complete these efforts. |

|

Establish a reliable TBM cost allocation methodology |

Not implemented |

Labor did not establish consistent, repeatable processes for allocating costs to the TBM taxonomy. Labor officials stated that the agency’s processes for allocating costs to the TBM taxonomy and validating the data were largely manual and that these processes had not been formally documented. Officials also stated that they planned to develop formal documentation in the future but did not provide a date by which they expected to complete this effort. |

Source: GAO analysis of Labor data. | GAO‑25‑106488

Department of State

Table 14: The Department of State’s Implementation of Selected Leading Technology Business Management (TBM) Practices

|

Leading practices |

Rating |

Description |

|

Develop a plan for implementing TBM |

Not implemented |

State had not developed plans for implementing TBM that identify key milestones and time frames, including steps needed to improve data quality. In January 2024, officials stated that the agency was not furnishing plans to implement TBM because it had already implemented TBM. In April 2024, State officials described some milestones the agency had planned for implementing TBM in fiscal years 2022 through 2025, but did not provide any documentation of its plans. |

|

Establish a reliable TBM cost allocation methodology |

Partially implemented |

State established consistent, repeatable processes for allocating costs to layer 1 (cost pools) of the TBM taxonomy. However, State’s methodology did not address all elements of the taxonomy it had implemented—specifically, portions of layer 2 (towers), layer 3 (solutions), and layer 4 (business units and capabilities). Although State officials described some automated validation checks, they also stated that TBM cost allocations are completed manually by its bureaus and each bureau is responsible for validating their IT portfolio details, including TBM cost allocations. Officials further stated that the responsibility for developing and maintaining a centralized cost allocation methodology does not fall under the purview of the Bureau of Information Resource Management. |

Source: GAO analysis of State data. | GAO‑25‑106488

Department of Transportation

Table 15: The Department of Transportation’s Implementation of Selected Leading Technology Business Management (TBM) Practices

|

Leading practices |

Rating |

Description |

|

Develop a plan for implementing TBM |

Partially implemented |

Transportation developed plans that identify key milestones and time frames for implementing layer 1 (cost pools) and layer 2 (towers) of the TBM taxonomy. However, the agency’s plans did not include key milestones and time frames for implementing layer 3 (solutions) of the taxonomy and taking steps to improve data quality. Officials stated that they expect to develop agency guidance with milestones for maturing TBM, but did not provide a date by which they expected to complete this effort. |

|

Establish a reliable TBM cost allocation methodology |

Partially implemented |

Transportation established reliable processes for submitting TBM data to the agency’s Office of the Chief Information Office for approval. However, the agency did not establish consistent, repeatable processes for the steps leading up to submission. Instead, officials stated that the agency relies on its Operating Administrations to make allocation decisions and manually enter the data into worksheets. Transportation officials stated that the agency expects to include an allocation methodology in future guidance, but did not provide a date by which they expected to complete this effort. |

Source: GAO analysis of Transportation data. | GAO‑25‑106488

Department of the Treasury

Table 16: The Department of the Treasury’s Implementation of Selected Leading Technology Business Management (TBM) Practices

|

Leading practices |

Rating |

Description |

|

Develop a plan for implementing TBM |

Fully implemented |

Treasury developed roadmaps that identified key milestones and time frames for implementing TBM. For example, the agency had milestones planned for fiscal years 2020 through 2028, such as increasing the reporting of cloud costs, improving TBM dashboards, and gaining insight into the efficiency and effectiveness of the agency’s IT investments. The roadmaps also included steps needed to improve TBM data quality such as expanding data sets, increasing automation, and exploring artificial intelligence capabilities. |

|

Establish a reliable TBM cost allocation methodology |

Fully implemented |

Treasury established consistent, repeatable processes for allocating costs to the TBM taxonomy. For example, Treasury documented and automated its processes for allocating costs to all the TBM taxonomy elements it had implemented. In addition, Treasury established a process for validating the accuracy of the agency’s allocations to the TBM taxonomy. |

Source: GAO analysis of Treasury data. | GAO‑25‑106488

Department of Veterans Affairs

Table 17: The Department of Veterans Affairs’ (VA) Implementation of Selected Leading Technology Business Management (TBM) Practices

|

Leading practices |

Rating |

Description |

|

Develop a plan for implementing TBM |

Fully implemented |

VA developed a roadmap that identified key milestones and time frames for implementing TBM, including determining the total cost of ownership for products and services. The roadmap also included steps needed to improve data quality, such as increasing automation for the collection and allocation of TBM data, ongoing financial and operational data analysis, and improving the accuracy and completeness of the agency’s systems inventory. |

|

Establish a reliable TBM cost allocation methodology |

Fully implemented |

VA established consistent, repeatable processes for allocating costs to the TBM taxonomy. For example, VA documented and automated its processes for allocating costs to all the TBM taxonomy elements it had implemented. In addition, VA established an approach for validating the accuracy of the agency’s allocations to the TBM taxonomy. |

Source: GAO analysis of VA data. | GAO‑25‑106488

Environmental Protection Agency

Table 18: The Environmental Protection Agency’s (EPA) Implementation of Selected Leading Technology Business Management (TBM) Practices

|

Leading practices |

Rating |

Description |

|

Develop a plan for implementing TBM |

Not implemented |

EPA had not developed plans that identify key milestones and time frames for implementing TBM, including steps needed to improve data quality. EPA officials stated that they were reviewing the Office of Management and Budget’s (OMB) TBM requirements for fiscal years 2025 through 2026 and expected to develop a plan and identify key milestones for inclusion in the agency’s budget planning process. However, officials did not identify when the agency expected to complete this effort. |

|

Establish a reliable TBM cost allocation methodology |

Partially implemented |