NATIONAL NUCLEAR SECURITY ADMINISTRATION

Progress Made Toward Fully Addressing Recommendations on Common Financial Reporting

Report to Congressional Committees

United States Government Accountability Office

For more information, contact Allison Bawden at bawdena@gao.gov.

Highlights of GAO-25-107696, a report to congressional committees

National Nuclear Security Administration

Progress Made Toward Fully Addressing Recommendations on Common Financial Reporting

Why GAO Did This Study

NNSA has long faced challenges identifying the total costs of its programs and comparing costs across its M&O contractors. Congress needs this information to provide oversight and make budgetary decisions. The National Defense Authorization Act for Fiscal Year 2017 required NNSA to implement a common financial reporting system, to the extent practicable.

Two Senate committee reports accompanying National Defense Authorization Act bills include provisions for GAO to review NNSA’s progress in implementing common financial reporting. This is GAO’s fifth report on this issue. This report assesses the extent to which DOE and NNSA have addressed GAO’s prior recommendations on common financial reporting since GAO’s June 2023 report on the topic.

GAO compared DOE’s and NNSA’s actions to implement common financial reporting since June 2023 against the 19 outstanding recommendations from prior GAO reports on this topic. To do so, GAO reviewed DOE and NNSA documents related to implementing common financial reporting. Lastly, GAO interviewed officials from DOE’s Office of the Chief Financial Officer and Office of Science, as well as NNSA’s Financial Integration Team and program offices.

What GAO Recommends

Seventeen recommendations remain outstanding and still warrant action as of July 2025. DOE and NNSA generally agreed with the prior recommendations.

What GAO Found

The National Nuclear Security Administration (NNSA) is a separately organized agency within the Department of Energy (DOE). NNSA is responsible for enhancing national security through the military application of nuclear energy, maintaining and modernizing infrastructure for the U.S. nuclear weapons stockpile, and supporting the nation’s nuclear nonproliferation efforts, among other things. NNSA relies on management and operating (M&O) contracts to carry out its missions at eight government-owned, contractor-operated national laboratories and nuclear weapons production facilities, collectively known as the nuclear security enterprise.

NNSA and Congress have had difficulty understanding the total costs of NNSA’s programs and comparing constituent costs between contractors because the M&O contractors use different methods of accounting and tracking costs. GAO has issued four prior reports on NNSA’s progress in implementing common financial reporting since fiscal year 2019 and made 28 recommendations to DOE and NNSA on this topic. As of June 2023, 19 of GAO's recommendations were outstanding.

GAO now assesses that DOE and NNSA have fully implemented two of the 19 outstanding recommendations and partially implemented nine. Eight of the recommendations have not yet been addressed. NNSA needs to take additional actions to fully implement the remaining 17 outstanding recommendations.

NNSA addressing and fully implementing the remaining outstanding recommendations would provide better assurance to NNSA, M&O contractors, and other stakeholders that the data collected for common financial reporting are accurate, consistent, and standardized. Implementing GAO’s recommendations would also help NNSA to reduce duplicative data requests across its offices and minimize the cost and reporting burdens on M&O contractors, while ensuring that common financial reporting provides the data needed to understand the total costs of NNSA’s programs and compare costs across its M&O contractors.

GAO will continue to review NNSA’s efforts to address and fully implement the remaining 17 outstanding recommendations on common financial reporting.

|

|

Number of recommendations by rating |

||

|

Closed – fully implemented |

Open – partially implemented |

Open – not addressed |

|

|

Prior rating, as of June 2023 |

— |

— |

19 |

|

Updated rating, as of July 2025 |

2 |

9 |

8 |

Source: GAO analysis of DOE and NNSA documents and interviews with DOE and NNSA officials. | GAO-25-107696

|

Abbreviations |

|

|

|

|

|

|

|

B&R |

budget and reporting |

|

|

DOE |

Department of Energy |

|

|

M&O |

management and operating |

|

|

NAP |

National Nuclear Security Administration Policy Document |

|

|

NDAA |

National Defense Authorization Act |

|

|

NNSA |

National Nuclear Security Administration |

|

|

STARS |

Standard Accounting and Reporting System |

|

This is a work of the U.S. government and is not subject to copyright protection in the United States. The published product may be reproduced and distributed in its entirety without further permission from GAO. However, because this work may contain copyrighted images or other material, permission from the copyright holder may be necessary if you wish to reproduce this material separately.

July 23, 2025

Congressional Committees,

The National Nuclear Security Administration (NNSA)—a separately organized agency within the Department of Energy (DOE)—is responsible for enhancing national security through the military application of nuclear energy; maintaining and modernizing infrastructure for the U.S. nuclear weapons stockpile; and supporting the nation’s nuclear nonproliferation efforts, among other things. NNSA relies on management and operating (M&O) contracts to carry out its missions at eight government-owned, contractor-operated national laboratories and nuclear weapons production facilities, collectively known as the nuclear security enterprise.[1]

NNSA and Congress have had difficulty understanding the total costs of NNSA’s programs—especially program work conducted at multiple sites—and comparing constituent costs across its contractors because M&O contractors use different methods of accounting and tracking costs. DOE’s management of contracts and projects, including those executed by NNSA, has been on our list of areas at high risk for fraud, waste, abuse, and mismanagement since 1990.[2] As we have emphasized through our prior work, effective management and oversight of the contracts, projects, and programs that support NNSA’s missions are dependent upon the availability of enterprise-wide cost information that is detailed, accurate, and reliable. Agency officials and Congress need this information to identify the costs of ongoing activities and ensure the validity of NNSA’s cost estimates for such activities.

The National Defense Authorization Act (NDAA) for Fiscal Year 2017 required NNSA to implement common financial reporting, to the extent practicable, for the nuclear security enterprise by December 23, 2020.[3] The act requires the common financial reporting system to include:

1. common data reporting requirements for work performed using NNSA funds, including reporting of financial data by standardized labor categories, labor hours, functional elements, and cost elements;[4]

2. a common work breakdown structure that aligns contractor work breakdown structures with NNSA’s budget structure;[5] and

3. definitions and methodologies for identifying and reporting costs for programs of record and base capabilities.[6]

NNSA’s Office of Management and Budget leads the common financial reporting effort through its Financial Integration Team, headed by the Program Director for Financial Integration. The effort includes the eight NNSA nuclear security enterprise sites, each managed and operated by an M&O contractor, and the NNSA program offices whose activities are executed by these contractors. The six NNSA program offices that participate in common financial reporting are the Offices of Defense Programs, Defense Nuclear Nonproliferation, Emergency Operations, Defense Nuclear Security, Counterterrorism and Counterproliferation, and Infrastructure.[7] In addition, some M&O contractors at DOE sites perform NNSA-funded work. We refer to them as “non-NNSA M&O contractors.” DOE’s Offices of Energy Efficiency and Renewable Energy, Environmental Management, Nuclear Energy, and Science oversee non-NNSA M&O contractors at 13 DOE sites that receive funding from NNSA.

Two Senate committee reports accompanying NDAA bills include provisions for us to review NNSA’s progress in implementing common financial reporting.[8] This report, our fifth review, assesses the extent to which DOE and NNSA have addressed our 19 recommendations on this topic that were outstanding as of June 2023.

We have issued four prior reports on NNSA’s progress in implementing common financial reporting since fiscal year 2019.[9] We made 28 recommendations to DOE and NNSA in our prior reports on this topic, nine of which NNSA had implemented by June 2023. With respect to the 19 outstanding recommendations, one is directed to DOE and 18 are directed to NNSA. As of June 2023, DOE and NNSA had not yet addressed any of these 19 recommendations.

To assess the extent to which DOE and NNSA have addressed the recommendations that were outstanding as of June 2023, we compared the information we gathered on DOE’s and NNSA’s progress against the 19 outstanding recommendations from our four prior reports. We also reviewed additional documents produced by NNSA’s Financial Integration Team in implementing common financial reporting, including summary reports from verification meetings and dashboard reports produced using common financial data.

To review NNSA’s progress in implementing common financial reporting since June 2023, we reviewed DOE and NNSA documents related to the implementation of the common financial reporting effort, including NNSA’s financial integration policy and DOE’s relevant financial management guidance.[10] We interviewed officials from NNSA’s Financial Integration Team, including the Program Director for Financial Integration, about NNSA’s progress in implementing common financial reporting and any challenges they may have encountered. We also interviewed officials from NNSA’s program offices and DOE’s Office of the Chief Financial Officer and Office of Science about actions they have taken to implement our prior recommendations and reviewed documents related to those actions.[11]

We compared the evidence against the actions called for in our recommendations. Two GAO analysts independently assessed the evidence against the outstanding recommendations. The analysts subsequently reached agreement on all assessments of whether the evidence indicates DOE and NNSA have partially or fully implemented the recommendations, or have not yet addressed the recommendations.[12]

We conducted this performance audit from July 2024 through July 2025 in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

Background

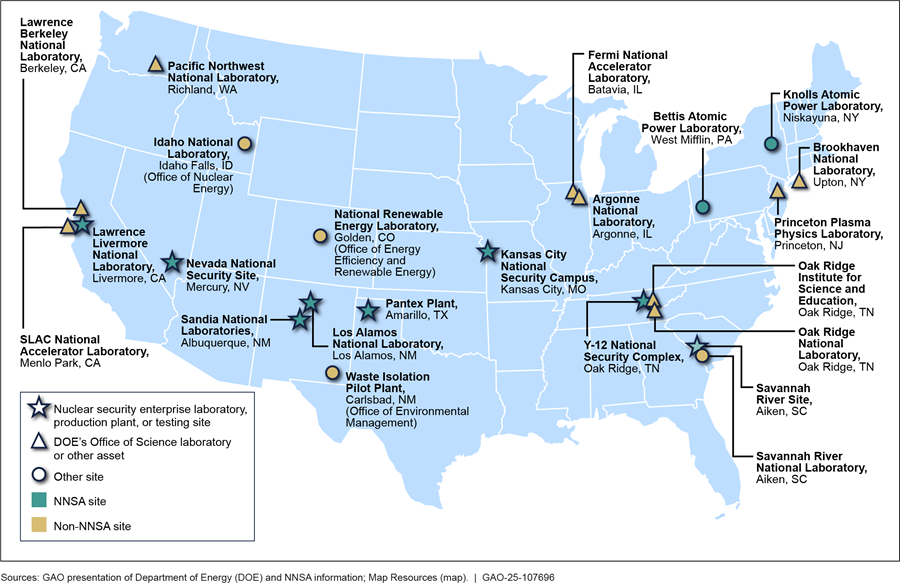

Sites Participating in NNSA’s Common Financial Reporting Effort

NNSA largely executes its mission at eight sites that constitute the nuclear security enterprise, and the M&O contractors that manage and operate these sites report common financial data to NNSA (see fig. 1). NNSA also collects common financial data from non-NNSA M&O contractors at other DOE sites that perform work funded by NNSA. DOE’s Offices of Energy Efficiency and Renewable Energy, Environmental Management, Nuclear Energy, and Science oversee non-NNSA M&O contractors at 13 sites that receive funding from NNSA, as also shown in figure 1.

Figure 1: National Nuclear Security Administration (NNSA) and Non-NNSA Sites Participating in NNSA’s Common Financial Reporting Effort

NNSA’s Approach to Implementing Common Financial Reporting

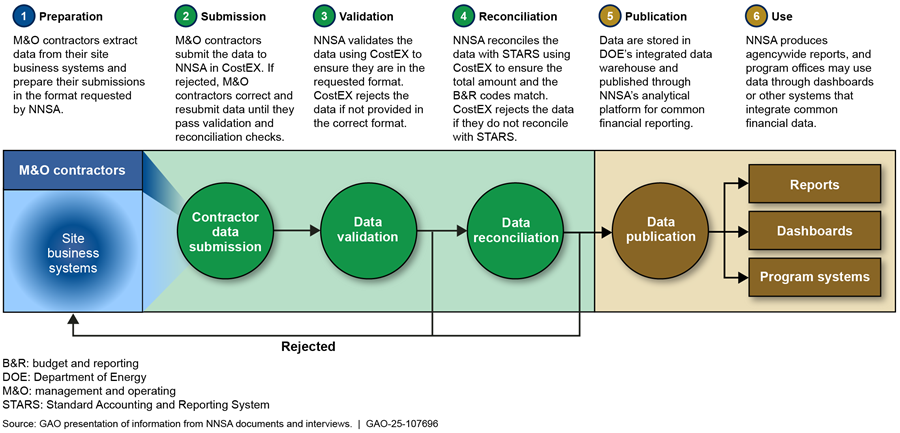

To implement common financial reporting across programs and sites, NNSA collects M&O contractors’ financial data in a common framework, using an agencywide data reporting tool called CostEX (see fig. 2).[13] The framework that NNSA established for common financial reporting relies on an agreed-upon work breakdown structure and common cost elements and definitions.

Figure 2: The National Nuclear Security Administration (NNSA) Common Financial Reporting Data Management Process

Notes: NNSA collects data for the common financial reporting effort using a data and analysis tool known as CostEX. NNSA establishes B&R codes that correlate with activities and that are used for reporting obligations, costs, and revenues; formulating budgets; and controlling and measuring actual (rather than budgeted) performance. DOE and NNSA use STARS for budget execution, financial accounting, and financial reporting capabilities.

M&O contractors prepare their data for submission to NNSA by crosswalking financial data from their sites’ business systems into NNSA’s work breakdown structure, using common cost elements and definitions. The M&O contractors’ business systems capture their financial data at a more detailed level than is needed for common financial reporting. This is because each M&O contractor tracks financial data for its site based on how it manages the work, using projects, tasks, and expenditure types as allowed by federal Cost Accounting Standards.[14] When the M&O contractors prepare their data for common financial reporting, site program managers identify the segments of the applicable work breakdown structure with which the project aligns. They crosswalk the financial data to the NNSA structure using professional judgment.

M&O contractors also crosswalk their financial data to NNSA’s cost elements. Cost elements capture discrete costs of a particular work activity and include direct and indirect costs. Direct costs are assigned to the benefitting program or programs. Indirect costs—costs that cannot be assigned to a single program—are to be accumulated, or grouped, into indirect cost pools.[15] M&O contractors manage their sites’ financial data, using expenditure types to track the costs of their projects. These expenditure types capture similar costs as the cost elements, but at a more detailed level, and are specific to each individual M&O contractor based on how the contractor manages its expenses. M&O contractors have flexibility to determine how they structure their work and the expenditures they track in their financial systems consistent with Cost Accounting Standards.

M&O contractors may each structure their work differently from one another, but each does so consistent with Cost Accounting Standards. However, these differences may make it difficult for NNSA to meet Managerial Cost Accounting Standards (Statement of Federal Financial Accounting Standards No. 4), a general standard for federal agencies to provide reliable and timely information on the full cost of federal programs. NNSA’s common financial reporting effort seeks to bridge this issue through crosswalking M&O contractors’ costs to the common work breakdown structure.

NNSA uses CostEX to collect common financial data from contractors. M&O contractors submit data each month as an electronic file. These data include costs and encumbrances, the unpaid balance of an awarded subcontract. The data submitted to CostEX are in addition to the cost information that M&O contractors report into the Standard Accounting and Reporting System (STARS), DOE’s and NNSA’s financial management and accounting system.[16]

NNSA publishes the cost data through an analytical platform for common financial reporting. Using this platform, NNSA offices can access the data through “dashboards,” data visualizations used to view multiple aspects of a program’s costs and that can be customized to meet each office’s needs. For example, the platform can provide dashboards to track obligations and a variety of cost data and to view detailed costs associated with the work breakdown structure for a program. According to NNSA Financial Integration Team officials, the dashboards also display spend rates for an office’s programs. This information can be used to compare programs and sites and to monitor a program’s financial performance. The Financial Integration Team also uses the analytical platform to produce reports summarizing agencywide financial data.

Roles and Responsibilities for Common Financial Reporting

Both the NNSA Financial Integration Team and NNSA program offices play important roles related to data collection for common financial reporting, including the development and management of the work breakdown structure. For example, the Financial Integration Team developed the initial common work breakdown structure. The Financial Integration Team also makes updates to the work breakdown structure in CostEX, documents and tracks these changes, and communicates the changes to the M&O contractors. NNSA program offices are responsible for establishing a work breakdown structure for their program activities, consistent with the agencywide common structure, and managing changes to the structure over time. Specifically, NNSA program offices have the ability to customize the relevant segments of the common work breakdown structure to reflect how they manage their work, which may change over time.

Both the Financial Integration Team and NNSA program offices also have roles related to common financial data use. The Financial Integration Team manages NNSA’s analytical platform for common financial reporting, including providing training to users and developing dashboards for NNSA’s offices to view the data. NNSA program offices may use common financial data through the dashboards and can provide feedback to the Financial Integration Team on the most useful content for those dashboards. Program offices may also work with the Financial Integration Team to integrate common financial data into the systems that they use for program management.

DOE and NNSA Fully or Partially Implemented 11 of 19 Recommendations on Common Financial Reporting, but Additional Action Is Needed on 17 Recommendations

DOE and NNSA fully or partially implemented 11 of 19 outstanding recommendations on common financial reporting since our June 2023 report. Of these 11, DOE and NNSA each fully implemented one recommendation and NNSA took actions to partially implement another nine recommendations. However, NNSA needs to take additional actions to fully implement the nine recommendations.[17] Additionally, the agency has not yet taken action to address the eight other recommendations that were outstanding as of June 2023. In total, NNSA needs to take additional actions for 17 of the 19 recommendations. NNSA addressing and fully implementing these outstanding recommendations would provide better assurance to NNSA, M&O contractors, and other stakeholders that the data collected for common financial reporting are accurate, consistent, and standardized. It would also help ensure that common financial reporting provides the data needed by Congress, NNSA, and other stakeholders to understand the total costs of NNSA’s programs and compare costs across M&O contractors. For a listing of all 19 recommendations and our assessment of their implementation status, see appendix I.

DOE Fully Implemented One Recommendation on Common Financial Reporting

Since June 2023, DOE fully implemented the one outstanding recommendation that we had directed to the department in our prior reports on common financial reporting. We recommended that DOE’s Chief Financial Officer facilitate NNSA and the DOE Office of Science—and other stakeholders, as appropriate—in coming to an agreement on the indirect cost elements the Office of Science should report to NNSA.[18] Similarly, the James M. Inhofe National Defense Authorization Act for Fiscal Year 2023 required that DOE’s Deputy Chief Financial Officer, in consultation with the Administrator for NNSA and the Director of the DOE Office of Science, determine by March 31, 2025 standardized indirect cost elements to be reported to NNSA by DOE M&O contractors doing work funded by NNSA.[19]

Officials previously told us that obtaining standardized cost data from all M&O contractors, including non-NNSA M&O contractors, through a common financial reporting process would benefit DOE by providing greater insight on costs at a more detailed level, leading to better decision-making. It would also help ensure that NNSA can collect standardized data from all M&O contractors to which it obligates funds.

In response to our recommendation and the NDAA for Fiscal Year 2023, DOE’s Office of the Chief Financial Officer updated DOE’s Financial Management Handbook in January 2025. The handbook now requires all DOE M&O contractors to report cost information monthly in CostEX. The handbook further states that all DOE M&O contractors must report indirect costs consistent with the data elements and structures defined in the CostEX system. These new requirements in DOE’s Financial Management Handbook are effective as of the start of fiscal year 2026, or October 1, 2025.

We now assess this recommendation as closed and fully implemented based on the revisions to DOE’s Financial Management Handbook and the new requirements it contains.

NNSA Fully Implemented One Recommendation on Common Financial Reporting

Since June 2023, NNSA fully implemented one of 19 recommendations on common financial reporting that we had directed to the agency. Specifically, we recommended the Program Director for Financial Integration should collect and document requirements to define the common financial reporting effort’s scope and meet project objectives and update such requirements periodically. NNSA revised its policy 412.1A on financial integration and, according to NNSA officials, the policy includes requirements for NNSA’s common financial reporting efforts, as called for by our recommendation.[20]

We reviewed the revised policy 412.1A and found it states that its purpose is to define, among other things, requirements for NNSA’s implementation of enterprise-wide financial integration. Further, we found that the policy identifies as a requirement for NNSA’s financial integration efforts the need to consistently and transparently report accurate cost information for NNSA and non-NNSA M&O contractors. The policy also includes contractor requirements for cost reporting to NNSA by reference and as an attachment to the policy. Lastly, we found the policy identifies a responsibility for NNSA elements, in coordination with the NNSA Director of Business Systems and Integration, to identify and define necessary enhancements to common financial reporting requirements.[21]

We now assess this recommendation as closed and fully implemented based on the revisions to NNSA’s policy on financial integration; specifically, the requirements it contains and the responsibilities it identifies. NNSA’s circulation of the revised policy and its requirements for stakeholder comment and concurrence review address the recommendation’s call for periodic updates. By collecting, documenting, and periodically updating stakeholder requirements, NNSA will have better assurance that common financial reporting data will meet stakeholder needs.

NNSA Took Actions to Implement Nine of 17 Other Recommendations on Common Financial Reporting, but Additional Actions Are Needed

NNSA took additional actions to implement nine recommendations on common financial reporting since June 2023, but we assess that more needs to be done to fully address these recommendations.[22] For example, we recommended that NNSA’s Program Director for Financial Integration should develop and implement internal processes for NNSA to verify how M&O contractors crosswalk financial data from their systems to the appropriate NNSA work breakdown structure. Doing so would help to ensure the reported data are accurate and consistent. We also recommended that the Program Director should develop and implement internal processes for NNSA to verify that M&O contractors are consistently applying common cost element definitions at their sites and across the nuclear security enterprise. By developing, institutionalizing, and implementing such internal processes, NNSA will have better assurance that the data collected for common financial reporting are accurate and consistent across M&O contractors. Further, such processes would help address long-term issues with NNSA’s ability to report the total costs of its programs.

NNSA agreed with our recommendations and, in response, NNSA officials we interviewed told us the agency has conducted and is continuing to schedule verification meetings with all M&O contractors for NNSA sites. The purposes of these verification meetings are for NNSA to review (1) how the contractors crosswalk their financial data into the appropriate segments and activities in the NNSA work breakdown structure to ensure the reported amounts are correct, and (2) that the contractors are consistently applying common cost element definitions. In addition, NNSA officials told us that they are using the same verification meetings to also (3) collect information from the M&O contractors on the recurring financial data requests they receive from NNSA program offices outside of common financial reporting, in response to another of our recommendations.

As of April 2025, NNSA had conducted verification and information collection meetings with six M&O contractors at five sites (the individual contractors at Kansas City National Security Campus, Los Alamos National Laboratory, Nevada National Security Site, and Sandia National Laboratory, and the two contractors at Savannah River). At Savannah River, the verification and information collection process had been completed for NNSA M&O contractor Savannah River Nuclear Solutions. Verification and information collection was ongoing for non-NNSA M&O contractor Battelle Savannah River Alliance at the Savannah River National Laboratory.[23] As of April 2025, NNSA had scheduled meetings with an additional two of eight NNSA M&O contractors through July 2025. NNSA has yet to schedule the meeting with NNSA contractor PanTeXas Deterrence at the Pantex site.[24]

NNSA officials we interviewed said that they will generally schedule the verification and information collection meetings with the remaining M&O contractors for non-NNSA sites after the meetings for the remaining NNSA sites are completed. The one exception was that NNSA conducted the verification meeting with the non-NNSA M&O contractor at Savannah River (Battelle Savannah River Alliance), but the verification process had not yet been finalized for this contractor as of April 2025. NNSA has yet to schedule verification meetings for the other 12 non-NNSA M&O contractors and does not plan to start holding such meetings until at least October 2025, according to officials. It remains uncertain when NNSA will complete the verification process and information collection for all M&O contractors at all sites, including non-NNSA sites.

According to agency officials, NNSA has not yet fully implemented these recommendations because of the personnel resource demands and logistics associated with scheduling verification meetings with all M&O contractors for both NNSA and non-NNSA sites. Officials stated they conducted the meetings during in-person site visits through February 2025. However, the meetings were conducted virtually starting in March 2025 and will be virtual going forward due to a moratorium on most travel by agency officials for the rest of fiscal year 2025.[25] We will continue to monitor NNSA’s implementation of the M&O contractor verification and information collection meetings until all such meetings have been completed for both NNSA and non-NNSA contractors.

In addition, NNSA revised its policy 412.1A on financial integration and, according to NNSA officials, it includes recurring verification meetings as a requirement, as called for by our recommendations. We reviewed the updated policy and found it identifies the responsibility for NNSA’s Financial Integration Team to conduct an annual assessment of NNSA and non-NNSA M&O contractors’ financial data for consistency and accuracy with the associated work breakdown structure. We also found that it identifies the responsibility for NNSA’s Director of Business Systems and Integration to assess NNSA and non-NNSA M&O contractor crosswalks of financial data to NNSA’s cost elements. In addition, the policy identifies the responsibility for NNSA’s Financial Integration Team to conduct initial assessments, follow-up crosswalk assessments, and common cost element assessments during NNSA and non-NNSA M&O contractor transitions. This policy revision is a positive commitment toward ensuring that consistent and accurate reporting of common financial data continues over time. However, our recommendations will not be fully addressed until the M&O contractor verification and information collection meetings have been completed for all NNSA and non-NNSA contractors.

NNSA Has Not Taken Action to Address Eight of 17 Outstanding Recommendations on Common Financial Reporting

Since June 2023, NNSA has not yet taken action to address eight of the 19 outstanding recommendations on common financial reporting that we had directed to DOE and NNSA. For a listing of all 19 recommendations and our assessment of their implementation status—including two recommendations that have been implemented since June 2023—see appendix I. Specifically, we assessed NNSA as having not yet taken actions to address the following eight outstanding recommendations on common financial reporting from our prior reports on the topic:

· NNSA’s Deputy Associate Administrator for Management and Budget, as chair of NNSA’s Financial Integration Executive Committee, should define and communicate goals and expectations for using the common financial reporting data (recommendation 2 from GAO‑22‑104810). According to NNSA officials, the agency has not yet done so, in part because they consider the NDAA for Fiscal Year 2017 to be the source of such goals and expectations.[26] We reviewed the law, and while it includes four required elements for NNSA’s common financial reporting effort, the law does not itself communicate goals or expectations for the use of such data by agency officials once the data are made available.[27]

· NNSA’s Program Director for Financial Integration should coordinate with program offices to develop an approach, such as through changes to the work breakdown structure or analytical tools, to ensure all program elements, including crosscutting and multi-programmatic costs, are included in total program costs (recommendation 3 from GAO‑22‑104810). According to NNSA officials, some internal conversations occurred within NNSA’s Office of Management and Budget exploring how the agency could potentially implement this recommendation, but officials subsequently determined that implementing it would be infeasible. The officials told us developing crosscutting and multi-programmatic costs is infeasible because of the personnel resource demands and logistics associated with developing, tracking, and annually updating such costs across all NNSA programs and among all M&O contractors. We continue to consider our recommendation appropriate and necessary for determining crosscutting and multi-programmatic costs within the nuclear security enterprise.

· Six NNSA program offices should develop, document, and implement plans to (1) regularly assess whether the office is making recurring financial data requests to M&O contractors that are duplicative of data that are or could be collected through common financial reporting, and (2) reduce or eliminate data requests where possible. In conducting the assessments, the offices should coordinate with NNSA’s Program Director for Financial Integration and incorporate information from M&O contractors (recommendations 8–13 from GAO‑23‑106069). According to NNSA’s Program Director for Financial Integration, the office has not yet coordinated with the program offices to implement these six recommendations because the office is prioritizing the implementation of recommendation 7 from GAO‑23‑106069, which is partially implemented.[28] The official told us that the recommendations are related and should therefore be implemented sequentially.[29]

We will continue to review NNSA’s efforts to address and fully implement the remaining 17 outstanding recommendations on common financial reporting.

Agency Comments

We provided a draft of this report to DOE and NNSA for review and comment. NNSA provided technical comments, which we incorporated as appropriate.

We are sending copies of this report to the appropriate congressional committees, the Secretary of Energy, and the Administrator of NNSA. In addition, this report is available at no charge on the GAO website at https://www.gao.gov.

If you or your staff have any questions about this report, please contact me at bawdena@gao.gov. Contact points for our Offices of Congressional Relations and Public Affairs may be found on the last page of this report. GAO staff who made key contributions to this report are listed in appendix II.

Allison Bawden

Director, Natural Resources and Environment

List of Committees

The Honorable Roger F. Wicker

Chairman

The Honorable Jack Reed

Ranking Member

Committee on Armed Services

United States Senate

The Honorable John Kennedy

Chair

The Honorable Patty Murray

Ranking Member

Subcommittee on Energy and Water Development

Committee on Appropriations

United States Senate

The Honorable Mike Rogers

Chairman

The Honorable Adam Smith

Ranking Member

Committee on Armed Services

House of Representatives

The Honorable Chuck Fleischmann

Chairman

The Honorable Marcy Kaptur

Ranking Member

Subcommittee on Energy and Water Development,

and Related Agencies

Committee on Appropriations

House of Representatives

Appendix I: Status of Outstanding Recommendations from Prior GAO Reports on Common Financial Reporting

DOE and NNSA fully or partially implemented 11 of 19 outstanding recommendations on common financial reporting since our June 2023 report.[30] Of these 11, DOE and NNSA each fully implemented one recommendation and NNSA took actions to partially implement another nine recommendations. However, NNSA needs to take additional actions to fully implement the nine recommendations. Additionally, the agency has not yet taken action to address the eight other recommendations that were outstanding as of June 2023. In total, NNSA needs to take additional actions for 17 of the 19 recommendations. For a list of all 19 recommendations and our assessment of their implementation status, see table 1.

Table 1: Status of Outstanding Recommendations from Prior GAO Reports on Department of Energy (DOE) and National Nuclear Security Administration (NNSA) Common Financial Reporting Efforts and Actions Taken Since June 2023

|

Outstanding recommendation |

Prior GAO rating as of June 2023, updated rating

as of July 2025, |

|

|

The NNSA Program Director for Financial Integration should collect and document requirements to define project scope and meet project objectives. These requirements should be updated periodically throughout the life of the project. recommendation 2 |

Prior rating: Open – not addressed ○ |

Updated rating: Closed – fully implemented ● |

|

We now assess this recommendation as closed and fully implemented. NNSA’s revised policy 412.1A on financial integration, according to NNSA officials, includes requirements for NNSA’s common financial reporting efforts, as called for by our recommendation. We reviewed the updated policy and found that it states that its purpose is to define, among other things, requirements for NNSA’s implementation of enterprise-wide financial integration. We found that NNSA’s policy 412.1A identifies as a requirement for NNSA’s common financial reporting efforts the need to consistently report costs across NNSA and non-NNSA management and operating (M&O) contractors. The policy also includes contractor requirements for cost reporting to NNSA by reference and as an attachment to the policy. Lastly, we found that the policy requires NNSA elements—including NNSA program, operation, and field offices—to coordinate with the NNSA Director of Business Systems and Integration to identify and define necessary enhancements to the common financial reporting requirements. NNSA circulated the updated policy within the agency for stakeholder comment and concurrence review prior to finalization in December 2024. We now assess this recommendation as closed and fully implemented based on the revisions to NNSA’s policy on financial integration and the requirements it contains, as well as the responsibilities it identifies. NNSA’s circulation of the revised policy and its requirements for stakeholder comment and concurrence review address the recommendation’s call for periodic updates. By collecting, documenting, and periodically updating stakeholder requirements, NNSA will have better assurance that common financial reporting data will meet stakeholder needs. |

||

|

The NNSA Program Director for Financial Integration should develop and implement an internal process for NNSA to verify how the M&O contractors crosswalk financial data from their systems to the appropriate NNSA work breakdown structure to ensure the reported data are accurate and consistent. GAO‑20‑180, recommendation 3 |

Prior rating: Open – not addressed ○ |

Updated rating: Open – partially implemented ◑ |

|

We now assess this recommendation as partially implemented. According to NNSA officials, the agency has conducted and is continuing to schedule crosswalk verification meetings with all M&O contractors for NNSA sites and non-NNSA sites that perform work for NNSA. The meetings are for, among other things, reviewing how the contractors crosswalk their financial data into the appropriate segments and activities in the NNSA work breakdown structure to validate the crosswalks.a As of April 2025, NNSA had conducted verification meetings with six M&O contractors at five sites: (1) Kansas City National Security Campus, (2) Los Alamos National Laboratory, (3) Nevada National Security Site, (4) Sandia National Laboratories, and (5) Savannah River. At Savannah River, the verification process had been completed for NNSA M&O contractor Savannah River Nuclear Solutions at the Savannah River Site, and it is ongoing for non-NNSA M&O contractor Battelle Savannah River Alliance at the Savannah River National Laboratory. As of April 2025, NNSA had scheduled verification meetings with an additional two of eight NNSA M&O contractors through July 2025. NNSA has yet to schedule the verification meeting with NNSA contractor PanTeXas Deterrence at the Pantex site. According to NNSA officials, they will generally schedule the verification meetings with the remaining M&O contractors for non-NNSA sites after the meetings for the remaining NNSA sites are completed. The one exception was that NNSA conducted the verification meeting with the non-NNSA M&O contractor at Savannah River, Battelle Savannah River Alliance. However, the verification process had not yet been finalized for this contractor as of April 2025. NNSA has yet to schedule verification meetings for the other 12 non-NNSA M&O contractors and does not plan to start holding such meetings until at least October 2025, according to officials. NNSA’s policy 412.1A on financial integration has been revised and, according to NNSA officials, includes recurring crosswalk verification meetings as a requirement, as called for by our recommendation. We reviewed the updated policy and found it identified a responsibility for NNSA’s Financial Integration Team to conduct an annual assessment of NNSA and non-NNSA M&O contractors’ financial data for consistency and accuracy with the associated work breakdown structure. According to agency officials, NNSA has not yet fully implemented this recommendation because of the personnel resource demands and logistics associated with scheduling and conducting the verification meetings with all M&O contractors for both NNSA and non-NNSA sites. Officials stated the meetings were conducted during in-person site visits through February 2025. However, the meetings were conducted virtually starting in March 2025 and will be virtual going forward due to a moratorium on most travel by agency officials for the rest of fiscal year 2025.b By developing, institutionalizing, and implementing an internal process for NNSA to verify how the M&O contractors crosswalk their financial data to the work breakdown structures, NNSA will have better assurance that the data collected for common financial reporting are accurate and consistent across the M&O contractors. |

||

|

|

|

|

|

The NNSA Program Director for Financial Integration should develop and implement an internal process for NNSA to verify that the M&O contractors are consistently applying common cost element definitions at their sites and across the nuclear security enterprise. GAO‑20‑180, recommendation 4 |

Prior rating: Open – not addressed ○ |

Updated rating: Open – partially implemented ◑ |

|

We now assess this recommendation as partially implemented. According to NNSA officials, the agency has conducted and is continuing to schedule common cost element definition verification meetings with all M&O contractors for NNSA sites and non-NNSA sites that perform work for NNSA. The meetings are for, among other things, verifying that the M&O contractors are consistently applying common cost element definitions at their sites and across the nuclear security enterprise.c As of April 2025, NNSA had conducted verification meetings with six M&O contractors at five sites: (1) Kansas City National Security Campus, (2) Los Alamos National Laboratory, (3) Nevada National Security Site, (4) Sandia National Laboratories, and (5) Savannah River. At Savannah River, the verification process had been completed for NNSA M&O contractor Savannah River Nuclear Solutions at the Savannah River Site, and it is ongoing for non-NNSA M&O contractor Battelle Savannah River Alliance at the Savannah River National Laboratory. As of April 2025, NNSA had scheduled verification meetings with an additional two of eight NNSA M&O contractors through July 2025. NNSA has yet to schedule the verification meeting with NNSA contractor PanTeXas Deterrence at the Pantex site. According to NNSA officials, they will generally schedule the common cost element definition verification meetings with the remaining M&O contractors for non-NNSA sites after the verifications for the remaining NNSA sites are completed. The one exception was that NNSA conducted the common cost element definition verification meeting with the non-NNSA M&O contractor at Savannah River, Battelle Savannah River Alliance. However, the verification process had not yet been finalized for this contractor as of April 2025. NNSA has yet to schedule definition verification meetings for the other 12 non-NNSA M&O contractors and does not plan to start holding such meetings until at least October 2025, according to officials. NNSA’s policy 412.1A on financial integration has been revised and, according to NNSA officials, includes recurring common cost element definition verification meetings as a requirement, as called for by our recommendation. We reviewed the updated policy and found it identified a responsibility for NNSA’s Director of Business Systems and Integration to assess NNSA and non-NNSA M&O contractor crosswalks of financial data to NNSA’s cost elements. In addition, the policy identified a responsibility for NNSA’s Financial Integration Team to conduct initial assessments, follow-up crosswalk assessments, and common cost element assessments during NNSA and non-NNSA M&O contractor transitions. In addition, according to NNSA officials, NNSA program managers and M&O contractor representatives should review the reported costs to identify any inconsistencies in the common financial reporting data produced by NNSA’s Financial Integration Team based on M&O contractor reported financial data. One of the responsibilities of the NNSA Financial Integration Team, according to the revised policy 412.1A, is to share common financial reporting data with NNSA program offices for their review. According to agency officials, NNSA has not yet fully implemented this recommendation because of the personnel resource demands and logistics associated with scheduling and conducting the common cost element definition verification meetings with all M&O contractors for both NNSA and non-NNSA sites. Officials stated the meetings were conducted during in-person site visits through February 2025. However, the meetings were conducted virtually starting in March 2025 and will be virtual going forward due to a moratorium on most travel by agency officials for the rest of fiscal year 2025.d By developing, institutionalizing, and implementing an internal process for NNSA to verify that the M&O contractors are consistently applying common cost element definitions, NNSA will have better assurance that the data collected for common financial reporting are accurate and consistent across the M&O contractors. |

||

|

The DOE Chief Financial Officer should facilitate NNSA and the Office of Science—and other stakeholders, as appropriate—in coming to an agreement on the indirect cost elements the Office of Science should report to achieve NNSA’s common cost reporting objectives. GAO‑22‑104810, recommendation 1 |

Prior rating: Open – not addressed ○ |

Updated rating: Closed – fully implemented ● |

|

In addition to our recommendation, the James M. Inhofe National Defense Authorization Act (NDAA) for Fiscal Year 2023 required that DOE’s Deputy Chief Financial Officer, in consultation with the Administrator for Nuclear Security and the Director of the Office of Science, determine by March 31, 2025 standardized indirect cost elements to be reported by contractors to the Administrator of NNSA.e We now assess this recommendation as closed and fully implemented. In response to our recommendation and the NDAA for Fiscal Year 2023, DOE’s Office of the Chief Financial Officer updated DOE’s Financial Management Handbook in January 2025. The handbook now includes, among other things, the following new requirement: “Not later than October 1, 2025, all DOE management and operating contractors performing work for NNSA must report cost information on a monthly basis in the cost execution financial integration system known as CostEX. Cost reporting must be provided for all NNSA-funded activities... “Specific data reporting requirements are specified in the CostEX system, consistent with the objectives defined in NNSA Policy (NAP) 412.1A, Financial Integration. Indirect cost reporting must conform to the data elements and structures defined in the CostEX system. Conformity does not require a modification to the management and operating contractor’s disclosed indirect cost model (i.e., conformity can be achieved by the contractor performing a crosswalk between its disclosed indirect cost model and the data elements and structures in the CostEX system).” The handbook applies to all DOE entities, including the DOE Office of Science. The requirement for DOE entities to report costs consistent with NNSA’s standardized cost elements is effective starting in October 2025. Officials previously told us that obtaining standardized cost data from all M&O contractors, including non-NNSA M&O contractors, through a common financial reporting process would benefit DOE. They said it would provide greater insight on costs at a more detailed level and lead to better decision-making. It would also help to ensure that NNSA can collect standardized data from all M&O contractors to which it obligates funds. DOE also continues to consider the benefits of implementing a department-wide common financial reporting process as part of a longer-term effort to achieve an integrated approach to financial management, according to officials from DOE’s Office of the Chief Financial Officer. However, DOE has not committed to adopting such a process. |

||

|

|

|

|

|

NNSA’s Deputy Associate Administrator for Management and Budget, as chair of NNSA’s Financial Integration Executive Committee, should define and communicate goals and expectations for using the common financial reporting data. GAO‑22‑104810, recommendation 2 |

Prior rating: Open – not addressed ○ |

Updated rating: Open – not addressed ○ |

|

We continue to assess this recommendation as not yet addressed by NNSA. According to NNSA officials, NNSA does not have current plans for the Deputy Associate Administrator for Management and Budget to further define and communicate goals and expectations for using common financial reporting data. We reviewed the revised policy 412.1A and found that the policy does not itself define or communicate the goals or expectations for using the common financial reporting data. According to NNSA officials, the agency has not yet defined and communicated goals and expectations for using common financial reporting data in part because NNSA’s Financial Integration Executive Committee was discontinued due to personnel turnover and associated vacancies. Agency officials told us the committee was discontinued as of May 2018. Further, the revised policy 412.1A reassigned the roles and responsibilities of the Financial Integration Executive Committee to the agency’s Program Director for Financial Integration (i.e., NNSA’s Director of Business Systems and Integration). NNSA officials also stated that they consider the NDAA for Fiscal Year 2017 to be the source of goals and expectations for the agency’s development and adoption of common financial reporting.f We reviewed the law, and while it includes four required elements for NNSA’s common financial reporting effort, the law does not itself communicate goals or expectations for the use of such data by agency officials once the data are made available. By establishing goals or expectations for using the data, NNSA offices would better understand how data are expected to be used, as well as various options for how the data could be used. NNSA offices could also better achieve the benefits of common financial reporting, such as providing total program costs and transparency. |

||

|

NNSA’s Program Director for Financial Integration should coordinate with program offices to develop an approach, such as through changes to the work breakdown structure or analytical tools, to ensure that all program elements, including crosscutting and multi-programmatic costs, are included in total program costs. GAO‑22‑104810, recommendation 3 |

Prior rating: Open – not addressed ○ |

Updated rating: Open – not addressed ○ |

|

We continue to assess this recommendation as not yet addressed by NNSA. According to NNSA officials, NNSA’s Program Director for Financial Integration does not currently have plans to coordinate with program offices to implement this recommendation. NNSA officials told us that the agency is able to use common financial reporting to identify most program costs, but crosscutting or multi-programmatic costs have not been developed and are therefore not currently available to officials. Some internal conversations occurred within NNSA’s Office of Management and Budget exploring how the agency could potentially implement this recommendation prior to a determination that implementing it would be infeasible, according to NNSA officials. The officials told us that developing crosscutting and multi-programmatic costs is infeasible because of the personnel resource demands and logistics associated with developing, tracking, and annually updating such costs across all NNSA programs and among all M&O contractors. We continue to consider our recommendation appropriate and necessary for determining crosscutting and multi-programmatic costs within the nuclear security enterprise. By updating the work breakdown structure or using analytical tools to capture all work activities, including those that are crosscutting and multi-programmatic, NNSA (1) can be better positioned to report total program costs, regardless of budget structure, and (2) would better ensure the data are reported at a sufficient level of detail to support program management. |

||

|

(Rec. 1) The NNSA Deputy Administrator for Defense Programs… (Rec. 2) The NNSA Deputy Administrator for Defense Nuclear Nonproliferation… (Rec. 3) The NNSA Associate Administrator for Emergency Operations… (Rec. 4) The NNSA Associate Administrator and Chief for Defense Nuclear Security… (Rec. 5) The NNSA Associate Administrator for Counterterrorism and Counter-proliferation… (Rec. 6) The NNSA Associate Administrator for Infrastructure… …should work with NNSA’s Program Director for Financial Integration to (1) assess the actions the office has taken to collect and use common financial data and (2) develop and document a plan to fully participate in the effort, including meeting the office’s responsibilities in the financial integration policy and ensuring that common financial data meet their program needs to the extent possible. GAO‑23‑106069, recommendations 1-6 |

Prior rating: Open – not addressed ○ |

Updated rating: Open – partially implemented ◑ |

|

We now assess these six related recommendations as partially implemented. NNSA officials from the six program offices to which these recommendations were directed have had some internal conversations about the recommendation since June 2023. They informally assessed the actions their offices had taken to collect and use common financial data.g We now assess these six recommendations as partially implemented because of these internal conversations. While the program offices have informally assessed the actions their offices have taken to collect and use common financial reporting, according to officials, the offices have not worked directly with NNSA’s Program Director for Financial Integration to assess their actions, as recommended. In addition, the offices have not yet worked with NNSA’s Program Director for Financial Integration to develop and document a plan for each program office to fully participate in the common financial reporting effort, also as recommended. According to NNSA’s Program Director for Financial Integration, the office has not yet worked with the program offices to implement these six recommendations because the office is prioritizing the implementation of recommendation 7 from GAO‑23‑106069 (see next row in this table). The official told us that the recommendations are related and should be implemented sequentially. Specifically, the Program Director said his office would work to implement recommendation 7 and related recommendations 8–13 from GAO‑23‑106069 before implementing recommendations 1–6. These recommendations are dependent on the collection of information and development of plans resulting from the implementation of recommendations 7–13. By assessing the actions that they have taken to collect and use common financial data and developing a plan to fully participate in the effort, the six program offices could help ensure that NNSA effectively implements the common financial reporting effort and realizes its intended benefits. |

||

|

NNSA’s Program Director for Financial Integration should collect information from M&O contractors participating in common financial reporting on the recurring financial data requests they receive from NNSA program offices outside of common financial reporting and provide this information to the program offices for use in their assessments of such requests. GAO‑23‑106069, recommendation 7 |

Prior rating: Open – not addressed ○ |

Updated rating: Open – partially implemented ◑ |

|

We now assess this recommendation as partially implemented. According to NNSA officials, the agency has conducted and is continuing to schedule information collection meetings with all M&O contractors for NNSA sites and non-NNSA sites that perform work for NNSA. The meetings are for, among other things, collecting information from M&O contractors participating in common financial reporting on the recurring financial data requests they receive from NNSA program offices outside of common financial reporting.h As of April 2025, NNSA had conducted information collection meetings with six M&O contractors at five sites: (1) Kansas City National Security Campus, (2) Los Alamos National Laboratory, (3) Nevada National Security Site, (4) Sandia National Laboratories, and (5) Savannah River. At Savannah River, the information collection had been completed for NNSA M&O contractor Savannah River Nuclear Solutions at the Savannah River Site, and it is ongoing for non-NNSA M&O contactor Battelle Savannah River Alliance at the Savannah River National Laboratory. As of April 2025, NNSA had scheduled meetings with an additional two of eight NNSA M&O contractors through July 2025. NNSA has yet to schedule the information collection meeting with NNSA contractor PanTeXas Deterrence at the Pantex site. According to NNSA officials, they will generally schedule the information collection meetings with the remaining M&O contractors for non-NNSA sites after the meetings for the remaining NNSA sites are completed. The one exception was that NNSA conducted the meeting with the non-NNSA M&O contractor at Savannah River (Battelle Savannah River Alliance). NNSA has yet to schedule information collection meetings for the other 12 non-NNSA M&O contractors and does not plan to start holding such meetings until at least October 2025, according to officials. According to agency officials, NNSA has not yet fully implemented this recommendation because of the personnel resource demands and logistics associated with scheduling and conducting the information collection meetings with all M&O contractors for both NNSA and non-NNSA sites. Officials stated the meetings were conducted during in-person site visits through February 2025. However, the meetings were conducted virtually starting in March 2025 and will be virtual going forward due to a moratorium on most travel by agency officials for the rest of fiscal year 2025.i By collecting information from M&O contractors on the additional financial data requests they receive from NNSA program offices, NNSA’s Financial Integration Team could better understand the broader effects of the common financial reporting effort. This includes whether NNSA is meeting the intended purpose of the effort by providing efficiencies and minimizing cost and burden on contractors. In addition, the Financial Integration Team could use this information to help the program offices understand the extent of their additional financial data requests. By assessing their additional data requests and reducing or eliminating them where possible, program offices could decrease duplication of effort and help ensure the accuracy of the agency’s financial data. |

||

|

(Rec. 8) The NNSA Deputy Administrator for Defense Programs… (Rec. 9) The NNSA Deputy Administrator for Defense Nuclear Nonproliferation… (Rec. 10) The NNSA Associate Administrator for Emergency Operations… (Rec. 11) The NNSA Associate Administrator and Chief for Defense Nuclear Security… (Rec. 12) The NNSA Associate Administrator for Counterterrorism and Counter-proliferation… (Rec. 13) The NNSA Associate Administrator for Infrastructure… …should develop, document, and implement a plan to (1) regularly assess whether the office is making recurring financial data requests to M&O contractors that are duplicative of data that are or could be collected through common financial reporting and (2) reduce or eliminate data requests where possible. In conducting the assessment, the office should coordinate with NNSA’s Program Director for Financial Integration and incorporate information from M&O contractors. GAO‑23‑106069, recommendations 8-13 |

Prior rating: Open – not addressed ○ |

Updated rating: Open – not addressed ○ |

|

We continue to assess these six related recommendations as not yet addressed. NNSA officials from five of the six program offices these recommendations were directed to said their offices have had some internal conversations about the recommendation since June 2023. They informally assessed their efforts to reduce recurring financial data requests to M&O contractors that duplicate data collected through common financial reporting.j However, we continue to assess these six recommendations as not yet addressed because, according to NNSA’s Program Director for Financial Integration, his office has not yet completed the collection of information from M&O contractors to share with the program offices as called for in this recommendation. The program offices have informally assessed the actions their offices have taken to reduce recurring financial data requests to M&O contractors. However, the offices have not yet coordinated directly with NNSA’s Program Director for Financial Integration to assess their actions, nor have the program offices yet developed and implemented the associated plans, as recommended. According to NNSA’s Program Director for Financial Integration, the office has not yet coordinated with the program offices to implement these six recommendations because the office is prioritizing the implementation of recommendation 7 from GAO‑23‑106069 (see prior row in this table). The official told us the recommendations are related and should therefore be implemented sequentially. Specifically, the Program Director said the office would work to implement recommendation 7 before related recommendations 8–13 from GAO‑23‑106069 as these recommendations are dependent on information collected through the implementation of recommendation 7. By regularly assessing whether they could fulfill their additional financial data requests using information collected through common financial reporting and doing so where possible, program offices could reduce duplication of effort across NNSA offices and minimize M&O contractors’ reporting of financial data to NNSA outside of common financial reporting. In addition, program offices could better ensure the accuracy of the financial data that program offices use for decision-making. |

||

Legend:

● DOE/NNSA took actions that fully implemented the recommendation.

◑ DOE/NNSA took actions that partially implemented the recommendation.

○ DOE/NNSA has not yet taken actions to implement the recommendation.

DOE = Department of Energy

NNSA = National Nuclear Security Administration

Source: GAO analysis of DOE and NNSA documents and interviews with DOE and NNSA officials. | GAO‑25‑107696

aThe meetings are held for multiple purposes. Specifically, NNSA officials are conducting the crosswalk verification meetings for this recommendation concurrently with the common cost element definition verification meetings discussed in the update for recommendation 4 from GAO‑20‑180 and the information collection meetings discussed in the update for recommendation 7 from GAO‑23‑106069. NNSA is conducting a single meeting with each M&O contractor to address all three recommendations.

bNNSA curtailed most employee travel in early March 2025 as part of its efforts to implement Executive Order 14222, Implementing the President’s Department of Government Efficiency Cost Efficiency Initiative. Exec. Order No. 14222 (Feb. 26, 2025), reprinted at 90 Fed. Reg. 11095 (Mar. 3, 2025).

cThe meetings are held for multiple purposes. Specifically, NNSA officials are conducting the common cost element definition verification meetings for this recommendation concurrently with the crosswalk verification meetings discussed in the update for recommendation 3 from GAO‑20‑180 and the information collection meetings discussed in the update for recommendation 7 from GAO‑23‑106069. NNSA is conducting a single meeting with each M&O contractor to address all three recommendations.

dNNSA curtailed most employee travel in early March 2025 as part of its efforts to implement Executive Order 14222, Implementing the President’s Department of Government Efficiency Cost Efficiency Initiative. Exec. Order No. 14222 (Feb. 26, 2025), reprinted at 90 Fed. Reg. 11095 (Mar. 3, 2025).

ePub. L. No. 117-263, § 3123, 136 Stat. 2395, 3057 (2022).

fThe NDAA for Fiscal Year 2017 required NNSA to implement common financial reporting for the nuclear security enterprise by December 23, 2020. The law requires four elements: (1) common data reporting requirements for work performed using NNSA funds, including reporting of financial data by standardized labor categories, labor hours, functional elements, and cost elements; (2) a common work breakdown structure for the Administration that aligns contractor work breakdown structures with the budget structure of the Administration; (3) definitions and methodologies for identifying and reporting costs for programs of records and base capabilities within the Administration; (4) a capability to leverage, where appropriate, the Defense Cost Analysis Resource Center of the Office of Cost Assessment and Program Evaluation of the Department of Defense using historical costing data by the Administration. NDAA for Fiscal Year 2017, Pub. L. No. 114-328, § 3113, 130 Stat. 2000, 2757 (2016).

gWe requested documentation of the program offices’ assessments and were told by officials that the assessment conversations were not documented.

hThe meetings are held for multiple purposes. Specifically, NNSA officials are conducting the information collection meetings for this recommendation concurrently with the crosswalk verification meetings discussed in the update for recommendation 3 from GAO‑20‑180 and the common cost element definition verification meetings discussed in the update for recommendation 4 from GAO‑20‑180. NNSA is conducting a single meeting with each M&O contractor to address all three recommendations.

iNNSA curtailed most employee travel in early March 2025 as part of its efforts to implement Executive Order 14222, Implementing the President’s Department of Government Efficiency Cost Efficiency Initiative. Exec. Order No. 14222 (Feb. 26, 2025), reprinted at 90 Fed. Reg. 11095 (Mar. 3, 2025).

jWe requested documentation of the program offices’ assessments and were told by officials that the assessment conversations were not documented.

GAO Contact

Allison Bawden, bawdena@gao.gov

Staff Acknowledgments

In addition to the contact named above, the following staff members made key contributions to this report: Ned H. Woodward (Assistant Director), Bill Hoehn (Assistant Director), David Lysy (Analyst in Charge), Kevin Bray, Elizabeth Dretsch, Kathryn Fledderman, Frank Garro, Cindy Gilbert, Heather Keister, Jeanette Soares, and Sara Sullivan.

The Government Accountability Office, the audit, evaluation, and investigative arm of Congress, exists to support Congress in meeting its constitutional responsibilities and to help improve the performance and accountability of the federal government for the American people. GAO examines the use of public funds; evaluates federal programs and policies; and provides analyses, recommendations, and other assistance to help Congress make informed oversight, policy, and funding decisions. GAO’s commitment to good government is reflected in its core values of accountability, integrity, and reliability.

Obtaining Copies of GAO Reports and Testimony

The fastest and easiest way to obtain copies of GAO documents at no cost is through our website. Each weekday afternoon, GAO posts on its website newly released reports, testimony, and correspondence. You can also subscribe to GAO’s email updates to receive notification of newly posted products.

Order by Phone

The price of each GAO publication reflects GAO’s actual cost of production and distribution and depends on the number of pages in the publication and whether the publication is printed in color or black and white. Pricing and ordering information is posted on GAO’s website, https://www.gao.gov/ordering.htm.

Place orders by calling (202) 512-6000, toll free (866) 801-7077,

or

TDD (202) 512-2537.

Orders may be paid for using American Express, Discover Card, MasterCard, Visa, check, or money order. Call for additional information.

Connect with GAO

Connect with GAO on X,

LinkedIn, Instagram, and YouTube.

Subscribe to our Email Updates. Listen to our Podcasts.

Visit GAO on the web at https://www.gao.gov.

To Report Fraud, Waste, and Abuse in Federal Programs

Contact FraudNet:

Website: https://www.gao.gov/about/what-gao-does/fraudnet

Automated answering system: (800) 424-5454

Media Relations

Sarah Kaczmarek, Managing Director, Media@gao.gov

Congressional Relations

A. Nicole Clowers, Managing Director, CongRel@gao.gov

General Inquiries

[1]50 U.S.C. § 2501(6). M&O contracts are agreements under which the government contracts for the operation, maintenance, or support, on its behalf, of a government-owned or government-controlled research, development, special production, or testing establishment wholly or principally devoted to one or more of the major programs of the contracting agency. 48 C.F.R. § 17.601.

[2]GAO, High-Risk Series: Heightened Attention Could Save Billions More and Improve Government Efficiency and Effectiveness, GAO‑25‑107743 (Washington, D.C.: Feb. 25, 2025).

[3]National Defense Authorization Act for Fiscal Year 2017, Pub. L. No. 114-328, § 3113,130 Stat. 2000, 2757 (2016). We have described NNSA’s actions and another statutory requirement related to common financial reporting prior to the enactment of this act in our previous reports. For example, see GAO, National Nuclear Security Administration: Additional Actions Needed to Collect Common Financial Data, GAO‑19‑101 (Washington, D.C.: Jan. 31, 2019).

[4]Cost elements capture discrete costs of a particular work activity and include direct costs, such as labor and equipment, and indirect costs, such as general and administrative costs.

[5]A work breakdown structure is a method of deconstructing a program’s end product into successive levels of detail with smaller specific elements until the work is subdivided to a level suitable for management control. Project Management Institute, Inc., A Guide to the Project Management Body of Knowledge (PMBOK® Guide), Seventh Edition (2021). PMBOK is a trademark of Project Management Institute, Inc. The Project Management Institute is a not-for-profit association that, among other things, provides standards for managing various aspects of projects, programs, and portfolios.

[6]According to an NNSA official, NNSA establishes its programs of record in its congressional budget justification and other documents to align with agency appropriations, which include weapons activities, defense nuclear nonproliferation, and federal salaries and expenses. A base capability captures an increment of discipline, or skill that serves a variety of functions, depending on the desired product.

[7]The statutory definition of the nuclear security enterprise does not include the Office of Naval Reactors; therefore, NNSA is not required to implement common financial reporting for this office.

[8]The Senate report accompanying S.1519, a bill for the NDAA for Fiscal Year 2018, included a provision for GAO to periodically review and report, through fiscal year 2022, on the progress of NNSA’s efforts to implement common financial reporting. S. Rep. No. 115-125, at 355 (2017). The Senate report accompanying S.4543, a bill for the NDAA for Fiscal Year 2023, included a provision for GAO to continue the periodic reviews of NNSA’s financial integration efforts through fiscal year 2025. S. Rep. No. 117-130, at 367 (2022).

[9]GAO‑19‑101; GAO, National Nuclear Security Administration: Additional Verification Checks Could Improve the Accuracy and Consistency of Reported Financial Data, GAO‑20‑180 (Washington, D.C.: Jan. 16, 2020); GAO, National Nuclear Security Administration: Actions Needed to Improve Usefulness of Common Financial Data, GAO‑22‑104810 (Washington, D.C.: Feb. 17, 2022); and GAO, National Nuclear Security Administration: Additional Actions Could Improve Efficiency of Common Financial Reporting, GAO‑23‑106069 (Washington, D.C.: June 20, 2023).

[10]National Nuclear Security Administration, Financial Integration, NNSA Policy Document (NAP) 412.1A (Washington, D.C.: Dec.16, 2024). Department of Energy, Financial Management Handbook (Washington, D.C.: Jan. 2025).

[11]Appendix I describes the current status, as of July 2025, for each of 19 outstanding recommendations from our previous four reports on NNSA’s common financial reporting effort.

[12]Fully implemented means that DOE or NNSA took actions that fully implemented the recommendation. Partially implemented means that DOE or NNSA took actions that partially implemented the recommendation, but additional actions are needed to fully implement the recommendation. Not yet addressed means that DOE or NNSA have not taken actions to implement the recommendation.

[13]Prior to the implementation of common financial reporting, NNSA’s program offices separately collected cost information from M&O contractors under their own cost structures. We have described NNSA’s legacy approach to collecting financial information in our previous reports. For additional details on the timeline for NNSA’s implementation of common financial reporting from fiscal years 2014–2021, see appendix II of GAO‑23‑106069.

[14]Federal Cost Accounting Standards govern how M&O contractors structure and account for their costs. They are a set of 19 standards promulgated by the U.S. Cost Accounting Standards Board, an independent, statutorily established board that is administratively part of the White House Office of Management and Budget’s Office of Federal Procurement Policy. See 41 U.S.C. § 1501. For current applicability, see 48 C.F.R. pt. 9904.

[15]The contractor is to estimate the amount of indirect costs to distribute to each program and make adjustments by the end of the fiscal year to reflect actual costs. The final program cost is the sum of the total direct costs plus the indirect costs distributed to the program. NNSA’s direct cost elements include labor, travel, materials and supplies, subcontracts, staff augmentation, and recovery of service center costs. NNSA’s indirect cost elements include site support; program office support; general and administrative; fees; and laboratory-, plant-, and site-directed research and development.

[16]Financial data collected through STARS represent DOE’s official financial data. However, we have previously found that STARS data are not detailed and may not satisfy the informational needs of NNSA’s program offices. See GAO‑19‑101.

[18]In February 2022, we found that the Office of Science had decided that its sites should not provide certain indirect cost data to NNSA. Office of Science officials told us at that time that they were hesitant to adopt the indirect cost reporting method used by another part of DOE, in this case NNSA, without having a consistent policy in place department-wide. In contrast, the M&O contractors at Office of Environmental Management and Office of Nuclear Energy sites reported indirect costs using the standardized cost elements specified by NNSA. See GAO‑22‑104810.

[19]Pub. L. No. 117-263, § 3123, 136 Stat. 2395, 3057 (2022).

[20]NNSA circulated the updated policy within the agency for stakeholder comment and concurrence review prior to finalization in December 2024.

[21]NNSA elements include program, operation, and field offices.

[22]In addition to the examples cited here, see appendix I for a listing of all 19 recommendations and our assessment of their implementation status.

[23]DOE’s Office of Environmental Management administered the contract for the management and operation of the Savannah River Site until 2024. NNSA assumed the administrator role for the Savannah River Site in fiscal year 2025. DOE’s Office of Environmental Management continues to administer the Savannah River National Laboratory.

[24]PanTeXas Deterrence was awarded the M&O contract for the Pantex site in June 2024. From March 2014 to June 2024, the Pantex site was operated under the same M&O contract as the Y-12 National Security Complex, managed by Consolidated Nuclear Security. According to NNSA officials, Pantex and Y-12 reported combined financial data under the Consolidated Nuclear Security M&O contract. The Pantex site began participating individually in common financial reporting in November 2024 under the PanTeXas Deterrence M&O contract.

[25]NNSA curtailed most employee travel in early March 2025 as part of its efforts to implement Executive Order 14222, Implementing the President’s Department of Government Efficiency Cost Efficiency Initiative. Exec. Order No. 14222 (Feb. 26, 2025), reprinted at 90 Fed. Reg. 11095 (Mar. 3, 2025).

[26]According to NNSA officials, NNSA’s Financial Integration Executive Committee was discontinued as of May 2018. The revised policy 412.1A reassigned the roles and responsibilities of the Financial Integration Executive Committee to the agency’s Program Director for Financial Integration (i.e., NNSA’s Director of Business Systems and Integration).