Report to Congressional Committees

United States Government Accountability Office

A report to congressional committees

Contact: Vijay A. D'Souza at dsouzav@gao.gov or Asif Khan at khana@gao.gov

What GAO Found

In response to its December 2020 acknowledgment that it had wasted billions of dollars sustaining redundant and obsolete IT systems, the Department of the Navy initiated an effort to modernize, consolidate, and retire its systems. The Navy reports that this initiative has resulted in terminating at least 11 legacy systems and saved more than $100 million. In addition, the Navy announced in January 2026 that it had completed its effort to migrate remaining Navy commands to Navy Enterprise Resource Planning, its financial system of record.

Fully adhering to leading practices for strategic and migration planning could strengthen the Navy’s systems modernization. Regarding strategic planning, the Navy met two of three leading practices and partially met one. For example, the Navy demonstrated that the portion of its Navy Financial Management Strategy associated with financial management systems aligned with relevant Navy and DOD-level strategic plans. However, the Navy did not fully implement performance measurement approaches for seven of the nine fiscal year 2025 metrics that it identified for this portion of its financial management strategy.

GAO’s Assessment of Navy Financial Management Systems Modernization Strategic Planning

|

Leading practices |

GAO assessment |

|

Align with the overall strategic plan |

● |

|

Identify results-oriented goals and performance metrics |

● |

|

Identify and implement performance measurement approaches |

◐ |

● Met = The Navy addressed all elements of the corresponding leading practice.

◐ Partially met = The Navy addressed some, but not all, elements of the corresponding leading practice.

Source: GAO analysis of Navy documentation. | GAO-26-107119

Regarding migration planning, the Navy met one and partially met three of four leading practices. For example, the Navy’s executive management uses Systems Consolidation Action Plans to obtain status reports and monitor system consolidations. Navy actions to fully comply with the remaining migration leading practices could further reduce modernization risks.

GAO’s Assessment of Navy Financial Management Systems Modernization Migration Planning

|

Leading practices |

GAO assessment |

|

Develop an enterprise roadmap |

◐ |

|

Provide a mechanism for executive management to monitor the migration effort |

●

|

|

Schedule periodic reviews |

◐ |

|

Establish a tracking system for executive management to manage progress, issues, and other action items |

◐ |

● Met = The Navy addressed all elements of the corresponding leading practice.

◐ Partially met = The Navy addressed some, but not all, elements of the corresponding leading practice.

Source: GAO analysis of Navy documentation. | GAO-26-107119

In reviewing the extent to which the Navy established a tracking system to manage progress, issues, and action items, GAO identified at least 111 changes to Navy consolidation plans, including at least 49 system schedule delays. These slippages may limit the Navy’s ability to fully support DOD’s auditability goals.

Why GAO Did This Study

The Department of Defense (DOD) remains the only major federal agency to not achieve an unmodified (clean) audit opinion. Modernizing and consolidating the Department of the Navy’s financial management systems is critical to its ability to support DOD’s goal of a clean opinion by the end of 2028. Attaining that goal would enable informed department officials to be accountable stewards of scarce federal resources needed for readiness and the warfighter.

This report was developed in connection with GAO’s audit of the U.S. government’s consolidated financial statements. It examines the extent to which the Navy’s consolidation and modernization of its financial management systems (1) are consistent with strategic planning leading practices and (2) align with migration planning leading practices.

GAO compared key Navy strategic planning documentation and associated evidence to leading practices in strategic planning. In addition, GAO compared Navy transition plans to migration planning leading practices and agency guidance. GAO also interviewed key Navy program officials.

What GAO Recommends

GAO is making five recommendations to the Navy: four on strategic and migration planning and one on the magnitude of schedule delays and their impact on the critical path to achieving a clean opinion. The Navy concurred with one recommendation; partially concurred with two; and did not concur with two. As discussed in the report, GAO maintains that all five recommendations are warranted.

Abbreviations

|

AFR |

agency financial report |

|

BSO |

budget submitting office |

|

DAI |

Defense Agencies Initiative |

|

DOD |

Department of Defense |

|

DOD IG |

Department of Defense Office of Inspector General |

|

ERP |

Enterprise Resource Planning |

|

FMO |

Office of Financial Operations |

|

FMS |

Financial Management Systems |

|

FY |

fiscal year |

|

I-Plan |

Implementation Plan |

|

NFR |

notice of findings and recommendations |

|

OMB |

Office of Management and Budget |

|

SABRS |

Standard Accounting Budgeting and Reporting System |

|

SCAP |

Systems Consolidation Action Plan |

This is a work of the U.S. government and is not subject to copyright protection in the United States. The published product may be reproduced and distributed in its entirety without further permission from GAO. However, because this work may contain copyrighted images or other material, permission from the copyright holder may be necessary if you wish to reproduce this material separately.

April 14, 2026

Congressional Committees

The Department of Defense (DOD) spends billions each year to acquire and modernize financial management and other business systems. For Fiscal Year (FY) 2025 the department requested $47.8 billion for its unclassified IT investments, including its financial management systems.[1] Sound financial management and financial information are critical to DOD’s ability to ensure accountability for its extensive resources.[2] However, DOD remains the only federal agency to not achieve an unmodified (clean) audit opinion. DOD’s financial management and business systems modernization efforts have been on GAO’s list of high-risk programs since 1995.[3]

According to the DOD Office of Inspector General (DOD IG), the Department of the Navy accounts for 51 percent of all DOD assets and it also remains unable to achieve a clean audit opinion.[4] Deficiencies in its financial management systems are a key reason the Navy is unable to achieve a clean opinion. Of note, the Marine Corps, which accounts for 2 percent of DOD assets, achieved a clean audit opinion in FY 2025, for the third straight year.[5] A key reason for this was its implementation of a new financial management system, the Defense Agencies Initiative (DAI). DAI is an enterprise resource planning platform that uses and is based on standard end-to-end business processes delivered by commercial off-the-shelf software.

The Navy’s financial management systems modernization efforts currently include migrating selected Navy and Marine Corps legacy systems to DAI and another financial management system, Navy Enterprise Resource Planning (Navy ERP). Navy ERP is intended to streamline the Navy’s business operations and is focused on financial and supply chain management.[6] As of March 2026, Navy ERP is the Navy’s financial system of record.

We performed this audit in connection with our audit of the U.S. government’s consolidated financial statements, which cover the financial status and activities related to the operation of the federal government.[7] This report examines the extent to which the Navy’s efforts to modernize its financial management systems (1) are consistent with strategic planning leading practices and (2) align with migration planning leading practices.

To address our first objective, we reviewed prior GAO reports and guidance from the Office of Management and Budget (OMB) to identify leading practices for strategic planning. We selected three practices that were most relevant to our evaluation of the Navy’s financial management systems modernization strategic planning efforts: (1) aligning with the agency’s overall strategic plan; (2) identifying results-oriented goals and performance metrics; and (3) identifying and implementing performance measurement approaches to measure actual results. We reviewed the Navy’s overarching strategic guidance for FY 2020 through FY 2025 and DOD financial management strategic guidance. We then compared the goals and priorities in each to the Navy’s financial management strategic planning documents, including its annual FY 2024 and 2025 implementation plans.[8] We focused our analysis of the Navy’s financial management strategic planning and related implementation plans on the portions of these documents associated with consolidating financial management systems. We evaluated these documents against the selected strategic planning leading practices.[9] We considered a practice to be fully met if the Navy addressed or substantially addressed all elements of the leading practice, partially met if the Navy provided evidence satisfying some, but not all, elements of the leading practice, and not met if the Navy did not address any elements of the leading practice.

To address our second objective, we reviewed OMB, Software Engineering Institute, and GAO guidance to identify leading practices for migration planning.[10] We selected four leading practices that were most relevant to the Navy’s efforts: (1) develop an enterprise roadmap, (2) provide a mechanism for executive management to monitor the migration effort, (3) schedule periodic reviews, and (4) establish a tracking system for executive management to manage progress, issues, and other action items. We evaluated the Navy’s key transition planning documents—such as the Systems Consolidation Action Plans (SCAP)—against the selected migration planning practices.[11] We considered a practice to be fully met if the Navy addressed or substantially addressed all elements of the leading practice, partially met if the Navy provided evidence satisfying some, but not all, elements of the leading practice, and not met if the Navy did not address any elements of the leading practice.

For both objectives, we met with cognizant Navy officials from the offices of the Financial Management and Comptroller, Financial Operations (FMO), Financial Management Systems (FMS), and Chief Information Officer. Appendix I provides additional details on our objectives, scope, and methodology.

We conducted this performance audit from October 2023 to April 2026 in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

Background

Financial statements provide information about an organization’s financial position—such as assets (what it owns) and liabilities (what it owes)—as of a certain point in time. They also provide information about the results of the organization’s operations—such as revenue (what came in) and expenses (what went out)—over a period of time, such as a fiscal year. DOD prepares an annual agency-wide financial statement to describe and communicate its financial position and the results of DOD operations. In addition, DOD’s military services—the Air Force, Army, Navy, and Marine Corps—and several other DOD subsidiary components also prepare separate, or stand-alone, financial statements.[12]

DOD collects financial information from its subsidiary organizations’ accounting systems to produce summarized, or consolidated, financial statements. If this information is not accurate, the reliability of DOD’s financial reporting and the department’s ability to manage operations can be adversely affected.

Pervasive weaknesses have adversely affected DOD’s ability to prepare auditable financial statements. Since 1997, the inspectors general of 24 executive agencies, including DOD, have been responsible for annual audits of agency-wide financial statements.[13] Since that time, auditors have been unable to express an opinion on the financial statements for DOD and its subsidiary military services, making DOD the only major federal agency to not achieve an unmodified (clean) audit opinion.[14] The impact of these pervasive weaknesses on DOD’s ability to prepare auditable financial statements is one of three major impediments preventing GAO from expressing an audit opinion on the U.S. government’s consolidated financial statements.[15]

According to DOD’s FY 2025 Agency Financial Report (AFR), published in December 2025, of the 28 DOD reporting entities, 11—including the Army and Air Force general funds and working capital funds and the Navy general fund—received disclaimers of opinion.[16] In February 2026, for the third consecutive year, the FY 2025 audit of the Marine Corps general fund financial statements resulted in a clean audit opinion.[17] However, the audit continued to identify seven material weaknesses related to internal controls over financial reporting within the Marine Corps general fund. This included three material weaknesses associated with IT.[18] In addition, in December 2025, the Navy’s AFR identified that the Navy general fund had six material weaknesses, including one associated with IT. The FY 2024 Navy AFR identified that the Navy working capital fund had nine material weaknesses, including three associated with IT.[19]

GAO has designated DOD financial management as a high-risk area since 1995 because of pervasive weaknesses in its financial management systems, business processes, internal controls, corrective action plans, financial monitoring and reporting, and fraud risk management.[20] DOD business systems, which include financial systems and systems that support other business functions (e.g., logistics and health care), have also been on GAO’s High-Risk List since 1995. This high-risk area addresses the department’s critical challenges in improving its business system acquisitions and investment management.

The DOD IG has similarly reported on DOD’s challenges in fully implementing the needed corrective actions to improve how it accounts for and reports its spending and assets. DOD’s longstanding IT challenges prevent it from implementing efficient and effective financial management and inhibit the department’s progress toward receiving a clean audit opinion.

For example, the DOD IG reported that during DOD’s FY 2024 audits, auditors issued or reissued 2,848 notices of findings and recommendations (NFR) and closed 930 prior-year NFRs.[21] Of these 2,848 NFRs, 1,119 were related to IT. Additionally, according to DOD’s FY 2025 AFR, the DOD IG identified 26 DOD-wide material weaknesses.[22] Of the 26 DOD-wide material weaknesses identified in the FY 2025 AFR, six were related to financial management systems and IT.[23]

In January 2024, the DOD IG reported that the department’s list of systems relevant to its internal controls over financial reporting was not complete or accurate.[24] The IG added that DOD’s plans to modernize or replace relevant systems that do not comply with the Federal Financial Management Improvement Act of 1996 were not complete. It also reported that these plans were not aggressive enough to ensure that the systems will comply in time to meet DOD’s FY 2028 goal for achieving a clean audit opinion on its financial statements.[25] This goal is consistent with a requirement in the FY 2024 National Defense Authorization Act for the Secretary of Defense to ensure that the department receives a clean audit opinion no later than December 31, 2028.[26]

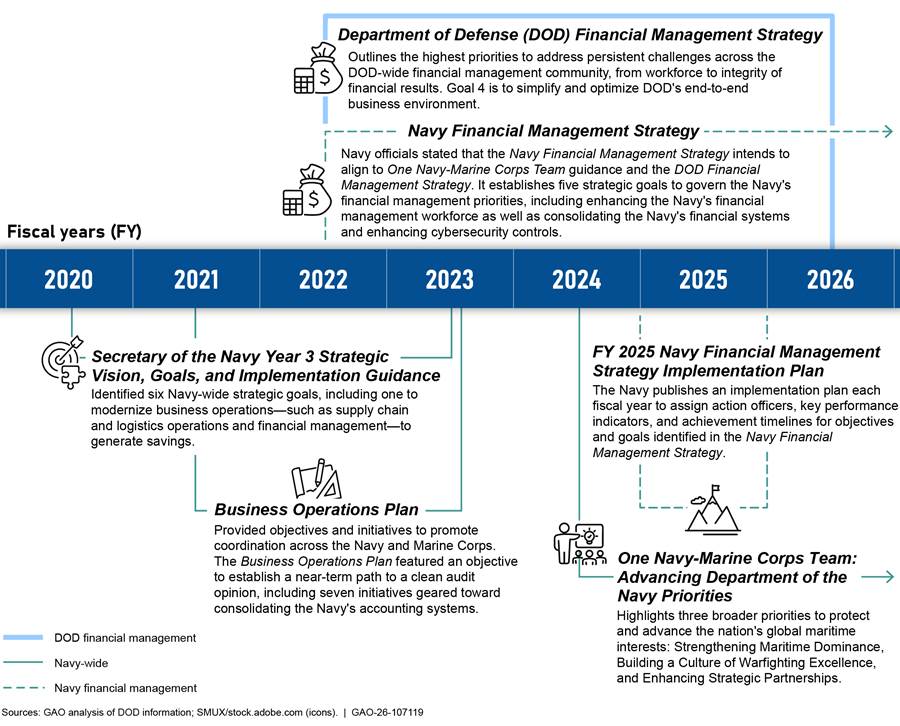

Strategic and Implementation Plans Guide Navy’s Financial Management Modernization

DOD has developed the Department of Defense Financial Management Strategy (DOD Financial Management Strategy) for FY 2022–2026.[27] This strategy is intended to guide department-wide priorities for the financial management community with input from across DOD, including the Navy. One of five strategic goals outlined in the DOD Financial Management Strategy is to simplify and optimize DOD’s end-to-end business environment. Within this goal, DOD has identified strategic objectives to optimize a secure systems environment, including by retiring legacy systems, leveraging innovative digital and automation solutions, and simplifying financial management regulation and policy.

The Navy has also developed several strategic documents to guide its financial systems modernization efforts. These documents include the Department of the Navy Financial Management Strategy (Navy Financial Management Strategy)[28] and annual implementation plans, including the Department of the Navy Financial Management Strategy Fiscal Year 2025 Implementation Plan (I-Plan).[29] Specifically,

· The Navy Financial Management Strategy document is intended to define the Navy’s priorities, mission, and vision as well as outline strategic goals and objectives for its business and financial operations. The strategy highlights the consolidation of the Navy’s financial systems and the enhancement of cybersecurity controls to improve data integrity as one of five strategic goals. Within this goal are objectives to (1) optimize the Department of the Navy’s financial management systems architecture via consolidation and system reduction and (2) enable the delivery of this portfolio of systems through improved governance.

· The I-Plan documents are intended to advance the Navy’s goals to achieve the larger vision for the financial management community across DOD. The FY 2025 I-Plan, for example, breaks down each objective from the wider Financial Management Strategy into annual goals, performance metrics, and timelines for action and completion. The FY 2025 I-Plan associates current FY goals—such as the completion of pre-migration data cleansing activities for select system go-lives—as well as performance metrics and timelines with each objective in the Navy Financial Management Strategy.[30]

Navy-wide strategic guidance also includes the Navy’s current strategic plan, called the One Navy-Marine Corps Team: Advancing Department of the Navy Priorities (One Navy-Marine Corps Team).[31] Previously, the Navy used strategic guidance such as the Secretary of the Navy Year 3 Strategic Vision, Goals, and Implementation Guidance Fiscal Years 2020–2023 (Year 3 Strategic Vision);[32] and the Business Operations Plan Fiscal Years 2021–2023, which included a strategic goal regarding modernizing business operations and a focus area on accounting systems consolidation, respectively.[33]

Figure 1 shows the departmental level, purpose, and time frame for each of these Navy and DOD strategic documents.

Two Initiatives Drive System Modernization and Consolidation

The Navy initiated two efforts to drive and track progress related to its system modernization and consolidation efforts:

· Operation Cattle Drive is an initiative intended to identify, assess, and eliminate redundant systems, and

· Quarterly Systems Consolidation Action Plans (SCAP) are a tool Navy executives use to obtain status reports and monitor system consolidations.

Operation Cattle Drive. On December 2, 2020, the Navy issued a memorandum stating that it maintains an excessive number of IT systems, networks, and applications and wastes billions of dollars to sustain them. As a result, it launched Operation Cattle Drive, which is led by the Navy’s FMS office and the office of the Navy Chief Information Officer. It involves a multiphase approach to enable either the retirement or rationalization of obsolete, insecure, and unauditable IT systems.[34] Further, as part of each phase of Operation Cattle Drive, the Navy has identified and projected cost savings associated with decommissioning legacy systems. For instance, over the first two phases, the Navy reported more than $100 million in potential savings from the shutdown of 11 legacy systems covering FY 2020 to 2026. Table 1 summarizes the Navy’s reported cost savings for the first three phases of Operation Cattle Drive.[35]

Table 1: Navy’s Reported Cost Savings and Avoidance for the First Three Phases of Operation Cattle Drive

|

Phase |

End date |

Focus |

Reported potential cost savings |

Reported date range for potential savings |

|

1 |

Sept. 1, 2021 |

Navy general ledger systems |

$69.7 million |

FY 2020-2026 |

|

2 |

July 19, 2022 |

Navy audit-relevant systems identified in the System Consolidation Action Plana |

$30.48 million |

FY 2022-2026 |

|

3 |

Aug. 9, 2024 |

Remaining Navy financial management systems and applications |

$13.31 million |

FY 2022-2029b |

Source: GAO analysis of Navy information. | GAO‑26‑107119

aAudit-relevant systems refer to systems that currently are considered material to audit and have a significant impact on financial reporting.

bThis date range represents the range of shutdown dates for the six systems Navy identified for decommissioning as part of this phase.

As of February 2025, the Navy had reduced its general ledger IT systems to three—Navy ERP, DAI, and the Standard Accounting Budgeting and Reporting System (SABRS)—and was on track to sunset SABRS at the end of FY 2026.[36] In January 2026, the Navy announced that it had successfully migrated remaining commands to Navy ERP as part of this continuing effort to streamline general ledgers. Additionally, according to the FY 2024 Navy AFR, a total of 10 IT systems have been decommissioned since FY 2018, resulting in the reduction of the number of IT systems with open IT NFRs from 46 to 36 and the closure of 155 IT NFRs.

SCAP. The Navy publishes quarterly SCAPs to obtain status reports and monitor system consolidations. SCAPs maintain data on the migration and shutdown dates of audit-relevant financial management systems and serve as an executive-level migration plan to assist the Navy in managing its efforts to decommission and consolidate these audit-relevant systems. Navy officials stated that the SCAP was developed in response to a 2017 DOD instruction on business systems requirements and acquisition[37] and a 2017 DOD IG recommendation for the Navy to develop and implement milestones and performance metrics for a Navy-wide IT strategic plan.[38]

According to Navy FMS officials, the Navy published quarterly SCAPs from March 2019 to March 2024 along with Summary of Changes presentations that document adjustments across SCAP versions (e.g., system migration and shutdown dates) for senior leadership. In addition, the Navy published an updated SCAP in May 2025. To develop the SCAP, the Navy obtains relevant data using data calls with system owners and Functional Area Managers.

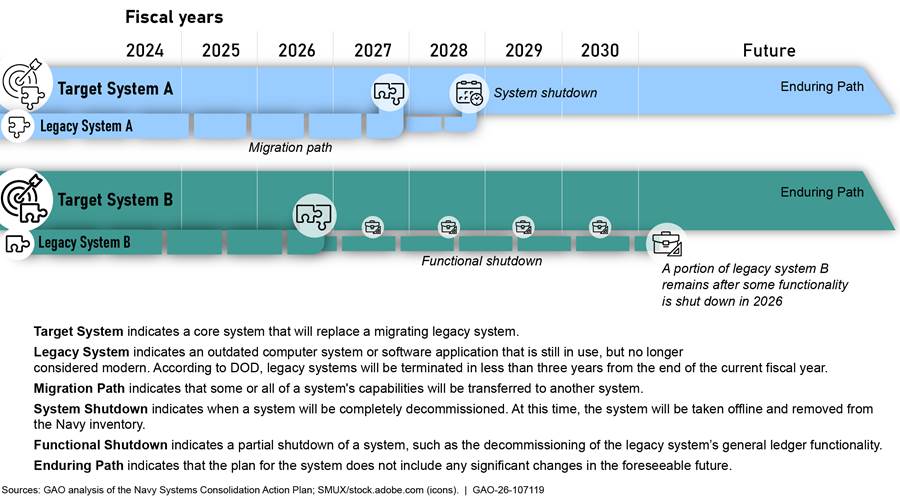

Figure 2 provides a conceptual representation of the information in the SCAPs.

Figure 2: Conceptual Representation of the Information Contained in the Navy’s Systems Consolidation Action Plans

As depicted in figure 2,

· Legacy System A is scheduled to migrate to Target System A in the fourth quarter of FY 2027 and the system shutdown will occur in the fourth quarter of FY 2028.

· Legacy System B is scheduled to migrate to Target System B in the fourth quarter of FY 2026. A portion of legacy system B’s functionality remains after some functionality is shut down in 2026.

Plans for Modernizing and Consolidating Navy Financial Management Systems

The Department of the Navy’s business and financial systems include systems intended to support financial operations at both the Navy and the Marine Corps. For example, in May 2025, the Navy identified 23 Navy, eight Marine Corps, and 14 combined use (i.e., used by both Navy and Marine Corps) systems relevant to DOD internal controls over financial reporting.[39] DOD uses information summarized from component systems to produce its consolidated financial statements.

To increase financial audit readiness, the Navy has been integrating business management systems and standardizing business operations. This included developing Navy ERP, which the Navy initiated in 2003. Navy ERP is a commercial off-the-shelf program intended to consolidate the Navy’s business operations into a single platform and address long-standing problems related to financial transparency and asset visibility.[40] It was established to standardize Navy business processes for key acquisition, financial, and logistics operations. It is intended to combine business process reengineering, use industry best practices, and integrate all facets of the Navy’s business into a single database. According to the Navy’s Program Executive Office, Manpower, Logistics, and Business Solutions, Navy ERP facilitates more than $145 billion in financial transactions each year.

As of March 2026, Navy ERP is the Navy’s financial system of record. A Navy ERP program official stated in October 2024 that the program’s planned total lifecycle cost was $10.01 billion. As of February 2025, Navy ERP was expected to cost $1.62 billion in actual and planned spending from FY 2023 through FY 2025, including $431 million in actual spending in FY 2023.[41]

The current Navy ERP program investment is expected to reach the end of its useful life in 2027, with support available through 2030. As a result, program officials stated that a system modernization will be required by 2030. According to Navy officials, this modernization project, known as Navy ERP+, received an acquisition decision memo authorizing the upgrade in June 2024 and was expected to receive authority to proceed in February 2026.[42]

In addition, the Marine Corps began operating in DAI, a financial management platform that uses commercial off-the-shelf software, and using it as its core financial system on October 1, 2021.[43] DAI replaced the legacy platform SABRS. In October 2024, a DAI program official stated that the program’s total lifecycle cost was $1.78 billion. As of November 2024, DAI supported 30 components across DOD, including the Marine Corps.[44] DAI accounted for $358.46 million in actual and planned spending from FY 2023 through FY 2025, including $104 million in actual spending in FY 2023.[45] According to a DAI program official, DAI is expected to reach the end of its useful life in 2038.

As of May 2025, the Navy continues to consolidate its 45 audit-relevant systems by moving selected legacy systems to Navy ERP and DAI. These modernization efforts also include consolidating feeder systems that provide relevant information to Navy ERP and DAI.[46]

Navy Financial Management System Roles and Responsibilities

According to Navy officials, multiple officials have responsibilities associated with overseeing or supporting the Navy’s financial management modernization efforts. For example, according to these officials:

· The Deputy Assistant Secretary of the Navy, FMS, is responsible for overseeing the Navy’s financial management transformation, including the modernization of financial systems and the reporting of complete, timely, and accurate information in Navy SCAPs.

· The Acting Assistant Secretary of the Navy, Financial Management and Comptroller, is the co-lead for Operation Cattle Drive and manages the Navy Financial Management Strategy to improve and transform Navy financial management operations.

· The Deputy Assistant Secretary of the Navy, FMO, executes accounting and financial management responsibilities related to the financial statement audit and modernization of Navy financial systems.

· The Department of the Navy Chief Information Officer is the co-lead for Operation Cattle Drive and responsible for management of the business mission area, to include all Navy defense business systems. Additionally, the Navy Chief Information Officer works with Financial Management and Comptroller and Navy leadership to provide recommendations and support to the Assistant Secretary of the Navy (Financial Management and Comptroller) on the transition and modernization of systems and plans supporting the Navy’s financial management transformation.

These and other roles and responsibilities are summarized in Appendix II.

GAO Has Previously Made Recommendations to Improve Selected Navy Financial Systems

We have issued a variety of reports and made recommendations regarding Navy ERP and DAI.

Navy ERP. Previously, we reported that the Navy ERP program effectively managed some, but did not effectively manage other, key aspects of its business system investment. For example:

· In 2009, we reported that the Navy had largely implemented effective controls on Navy ERP associated with system testing and change control but had not fully implemented important aspects of test management and change control.[47] As a result, we recommended that the Secretary of Defense direct the Secretary of the Navy to improve the program’s system change request review and approval process and its independent verification and validation activities. The Navy has implemented our recommendations.

· In 2008, we reported that Navy ERP program management weaknesses[48] had contributed to a 2-year schedule delay and about $570 million in cost overruns.[49] We recommended that the Secretary of Defense direct the Secretary of the Navy to improve cost and schedule estimating and earned value management practices and address risk management weaknesses. The Navy subsequently implemented three of our four recommendations.

DAI. In June 2024, we reported on the Marine Corps’ transition to DAI.[50] We found that DOD used selected leading practices in estimating cost and schedule and in measuring progress of the Marine Corps’ migration to DAI but did not implement all practices. In addition, regarding data migration and conversion, the Marine Corps followed five leading practices and partially followed five others. Further, we found that the Marine Corps followed four change management leading practices and partially followed three others. We made 14 recommendations on cost, schedule, performance metrics, data migration, and change management. As of January 2025, DOD and the Marine Corps have implemented all of the 14 recommendations.

Leading Practices for Strategic and Migration Planning

Prior GAO reports and other agencies’ and organizations’ guidance have identified leading practices for strategic planning and migration planning.

Leading practices for strategic planning. We have previously reported that planning for results—such as by defining goals, identifying strategies and resources needed to achieve goals, and identifying internal and external factors that might impact goal achievement—can help federal organizations identify what they intend to achieve, how they will achieve it, and any obstacles to mitigate.[51]

Selected strategic planning leading practices derived from OMB guidance and prior GAO reports include:

· Align with the overall strategic plan: The goals and objectives should align with those in broader agency strategic plans to ensure efforts at lower levels are supporting the agency’s mission, and the contributions of these actions can be linked to broader outcomes.

· Identify results-oriented goals and performance metrics: The strategic plan should define goals and metrics that map to the agency’s mission and should be specific, verifiable, and measurable so that progress can be tracked. Results-oriented goals should, for example, identify levels of performance to be accomplished within a timeframe and provide a target, or a measurable characteristic—often expressed as a number—that indicates how well an agency or component aspires to perform.

· Identify and implement performance measurement approaches: Performance evaluation approaches should be identified and implemented to assess progress towards goals and to develop an understanding of why actual results were or were not achieved.

Leading practices for migration planning. OMB calls for agencies to develop an enterprise roadmap that documents the current and future states of a systems environment at a high level and presents a migration plan for moving from the current to the future in an efficient, effective manner.[52]

In addition, the Software Engineering Institute’s migration planning leading practices call for management to provide a mechanism for executive management to monitor the effort; schedule periodic reviews; and establish a system to track progress, issues, and other action items.[53] Further, GAO’s IT investment management framework calls for executive-level oversight and monitoring into the performance of IT portfolios. This includes overseeing and monitoring the performance of systems (e.g., performance against schedule expectations) to identify issues and take actions to address underperformance.[54] This approach is consistent with GAO’s guidance on internal controls, which calls for management to monitor ongoing activities, evaluate the results, and timely remediate identified deficiencies.[55]

Selected migration planning leading practices are described below:

· Develop an enterprise roadmap: An enterprise roadmap should document a migration plan for moving from the current to the future systems environment in an efficient and effective manner. The roadmap should contain a system inventory and discuss performance gaps, resource requirements, and planned solutions, and it should map the strategy to projects and budget. The roadmap should also document the tasks, time frames, and milestones for implementing solutions.

· Provide a mechanism for executive management to monitor the migration effort: The organization should provide a mechanism for management to monitor and report on its migration efforts.

· Schedule periodic reviews: The organization should schedule periodic reviews commensurate with the risks involved, organizational policies and regulations, stakeholder interests, and assurances sought by the sponsor and project manager.

· Establish a tracking system for executive management to manage progress, issues, and other action items: The organization should have mechanisms in place to track progress on milestones, identify and monitor open issues, and identify and mitigate risks.

Navy’s Strategic Planning Partially Addressed Leading Practices

As previously stated, OMB and GAO guidance call for organizations to engage in strategic planning efforts that (1) align with the agency’s overall strategic plan, (2) identify results-oriented goals and performance metrics that permit the agency to determine whether implementation of the plan is succeeding, and (3) identify and implement performance measurement approaches to measure actual results. The Navy’s financial management strategic planning efforts met two and partially met one of these leading practices for effective strategic planning.[56] Table 2 summarizes our evaluation of the Navy’s financial systems modernization strategic planning efforts against these leading practices. Our evaluation of each practice is summarized after the table and discussed in more detail in Appendix III.

|

Leading practice |

GAO evaluation |

|

Align with the overall strategic plan |

● |

|

Identify results-oriented goals and performance metrics |

● |

|

Identify and implement performance measurement approaches |

◐ |

● Met = Navy evidence or documentation addressed or substantially addressed all elements of the corresponding leading practice.

◐ Partially met = Navy evidence or documentation addressed some, but not all, elements of the corresponding leading practice.

Sources: Office of Management and Budget and GAO guidance; GAO analysis of Navy documentation and practices. | GAO‑26‑107119

Align with the overall strategic plan—met. The Navy’s strategic goal for consolidation of financial management systems, issued in March 2022, aligned with related goals and priorities in DOD financial management guidance, the Navy’s current and prior strategic plans, and more detailed underlying plans.

Specifically, Strategic Goal 4 of the Navy Financial Management Strategy—the Navy’s current strategic guidance for its business and financial operations—is to consolidate Navy financial systems and enhance cybersecurity controls to improve data integrity. This goal aligned with a DOD Financial Management Strategy goal to simplify and optimize DOD’s end-to-end business environment. Additionally, the Navy provided documentation of an internal analysis linking this Navy Financial Management Strategy consolidation goal and its objectives to the One Navy-Marine Corps Team priority to Strengthen Maritime Dominance. Further, the Navy Financial Management Strategy goal aligned with elements of documents that previously served as overarching Navy strategic guidance but are now obsolete—namely, the “accounting systems consolidation” focus area in the Navy Business Operations Plan, published in FY 2021, and the “modernize business operations” strategic goal of the Year 3 Strategic Vision, which was effective as of FY 2020.[57]

Identify results-oriented goals and performance metrics—met. As previously stated, leading practices for strategic planning include identifying results-oriented goals and performance metrics that are specific and measurable to permit the agency to track its progress and determine how well it is performing. The Navy substantially identified results-oriented goals and performance metrics. Specifically, the Navy Financial Management Strategy and its associated annual I-Plan both included results-oriented goals associated with financial systems modernization. For example, Goal 4 of the Navy Financial Management Strategy includes an objective to consolidate Navy financial management systems. Annual I-Plan documents further assigned annual goals to this objective and included related tasks, performance metrics, and targets.

Additionally, eight of nine metrics associated with Goal 4 in the FY 2025 I-Plan—the most recent I-Plan we reviewed—were measurable and contained specific timeframes. This included seven metrics in the FY 2025 I-Plan document and one additional FY 2025 I-Plan metric. For the additional metric, the Navy demonstrated that it had developed a precise, measurable data cleansing target for three planned migrations to Navy ERP subsequent to the FY 2025 I-Plan’s publication. Conversely, the Navy did not provide evidence documenting one FY 2025 I-Plan performance metric’s measurability. Specifically, the Navy did not describe how the identification of gaps against ERP process models to inform requirements for ERP+ could be measured prior to the completion of our fieldwork. Nevertheless, because eight of the nine FY 2025 I-Plan metrics relevant to our review were specific, verifiable, and measurable, we determined that the Navy substantially met this leading practice.

Identify and implement performance measurement approaches—partially met. As previously stated, leading practices for strategic planning include identifying and implementing approaches to measure the actual results of the efforts using performance metrics. The Navy identified and partially implemented performance measurement approaches for performance metrics related to Goal 4.

To its credit, the Navy identified approaches for how it either collected or planned to collect and present information related to all nine performance metrics to measure its progress across the four FY 2025 I-Plan goals related to Goal 4 of the Navy Financial Management Strategy. In addition, the Navy provided evidence that it had fully implemented its designated performance measurement approach for two of nine performance metrics related to Goal 4 in the FY 2025 I-Plan prior to the completion of our fieldwork. For example, the Navy demonstrated regular internal communication documenting point-in-time totals for one metric measuring a Navy command’s progress toward reconciling and closing all open contracts in SABRS by the fourth quarter of FY 2025. Additionally, the Navy documented its completion of several milestones to measure progress for a metric to decommission a Navy command out of SABRS by the fourth quarter of FY 2025. This included a checklist marking the completion of several criteria needed to achieve full operational tempo, such as migration of legacy data and provisioning end user accounts. The Navy also produced a report to document the command’s transition from cutover to stabilization.[58]

However, the Navy did not fully implement five approaches and did not provide evidence demonstrating that it had implemented the remaining two approaches. Specifically, the Navy did not provide evidence that it had fully collected performance information to measure progress toward all elements of related performance metrics and FY 2025 I-Plan goals prior to the completion of our fieldwork.

For example, officials stated that they measured progress toward a metric for a command to achieve full operational tempo in Navy ERP by holding weekly situation summary meetings, completing a checklist, and internally communicating completion of the milestone. The Navy provided evidence of the latter two elements, including the checklist as previously noted, but did not provide evidence of weekly situation summary meetings to measure progress as this command approached full operational tempo. Additionally, for a FY 2025 I-Plan goal to deliver requirements for ERP+ and a related metric to capture gaps against standard process models to inform requirements, officials stated that the Navy identified gaps in weekly integrated product team sessions and escalated them to ERP+ leadership. However, the Navy did not provide evidence that it conducted these requirements-gathering efforts for teams that had begun work prior to the conclusion of our fieldwork. Further, the Navy did not document these and other performance measurement approaches in the Navy Financial Management Strategy or the annual I-Plan documents.

Navy officials stated that they believed they provided evidence of having carried out performance measurement approaches for FY 2025 I-Plan goals and metrics and that additional mechanisms they had in place to assess progress toward strategic goals—such as forums to track performance metrics and timelines—were sufficient. However, the Navy did not provide evidence that it held these forums or, as noted, that it had performance evaluation approaches in place to fully assess progress toward all elements of its financial management systems modernization goals.

We have previously reported on DOD’s challenges in identifying and reporting performance metrics and their potential to limit program accountability and inhibit performance oversight.[59] Identifying clear and complete approaches to measure the success of its financial system goals would help the Navy ensure it is fully measuring the extent to which it is achieving intended financial systems modernization outcomes. This would enable the Navy to more effectively identify deficiencies and inefficiencies and take corrective action, as appropriate.

Navy’s Migration Planning Did Not Fully Address Leading Practices

As previously stated, OMB, Software Engineering Institute, and GAO guidance call for organizations to follow relevant leading practices in their migration planning efforts. These leading practices are (1) developing an enterprise roadmap, (2) providing a mechanism for executive management to monitor the migration effort, (3) scheduling periodic reviews, and (4) establishing a tracking system for executive management to manage progress, issues, and other action items.

Table 3 provides a summary of our evaluation of the Navy’s financial management modernization efforts against relevant leading practices. Our evaluation of each practice is discussed in further detail below the table.

|

Leading practice |

GAO evaluation |

|

Develop an enterprise roadmap |

◐ |

|

Provide a mechanism for executive management to monitor the migration effort |

● |

|

Schedule periodic reviews |

◐ |

|

Establish a tracking system for executive management to manage progress, issues, and other action items |

◐ |

● Met = Navy evidence or documentation addressed or substantially addressed all elements of the corresponding leading practice.

◐ Partially met = Navy evidence or documentation addressed some, but not all, elements of the corresponding leading practice.

Sources: Office of Management and Budget, Software Engineering Institute, and GAO guidance; GAO analysis of Navy documentation. | GAO‑26‑107119

Develop an enterprise roadmap—partially met. The Navy addressed some elements of this leading practice. However, it has not developed an enterprise roadmap. In April 2024, officials stated that the Navy has identified key IT systems and shared service provider systems that support its business process areas and generate, process, store, record, or report transactions with a material impact on its financial statements. In addition, Navy officials stated that they maintain an audit roadmap and I-Plan.[60] Officials also provided an example of a portion of their audit roadmap as well as their FY 2024 and 2025 I-Plans. The audit roadmap and I-Plans, among other things, document interdependencies between business processes and system improvements needed to help achieve a clean audit opinion.[61] Further, the Navy documents the status of these systems in the quarterly SCAPs that it provides to leadership and stakeholders. As noted, the SCAPs include an inventory of audit-relevant systems as well as key migration milestones and time frames.

However, the SCAPs and other associated documentation do not constitute an enterprise roadmap, which would need to include information such as performance gaps and resource requirements. Further, Navy officials stated they do not have an enterprise roadmap for all system migration efforts. Navy FMO officials stated that system migrations are monitored at the system level and they believe existing mechanisms for monitoring system transitions are sufficient. Nevertheless, the Navy did not demonstrate that it maintains an enterprise roadmap to guide its financial management modernization efforts. Until the Navy develops a complete and comprehensive enterprise roadmap to help inform its audit-relevant system migration effort, it will not be well-positioned to ensure that it has the necessary resources to allow for more effective system migrations and provide measurable results.

Provide a mechanism for executive management to monitor the migration effort—met. The Navy fully addressed all elements of this leading practice. Navy executive management uses SCAPs to obtain status reports and monitor system consolidations.[62] Navy officials also provided examples of system-level briefings to leadership and stakeholders, such as briefings about progress associated with the Navy ERP system migration effort.

According to Navy officials, the SCAP is intended to provide point-in-time status updates on its system migration efforts. The Navy’s FY 2025 I-Plan also stated that the SCAP was an example of oversight related to its strategic goal to consolidate Navy financial systems. Specifically, the I-Plan cited the SCAP as an example of efforts in place to review progress, risks, and milestones of system-owning organizations and ERP modernization and migration activities. The Navy provided six quarterly SCAPs and associated SCAP Summaries of Changes. The SCAP’s point-in-time status updates provide executive-level insight to help facilitate leadership’s monitoring of the Navy’s overall migration effort.

Schedule periodic reviews—partially met. The Navy demonstrated that it addressed some elements of this practice. For example, Navy officials stated that they use SCAP quarterly reviews and the Navy’s audit roadmap to inform periodic reviews with leadership and stakeholders about its systems migration efforts. They also provided five signed SCAPs and associated summaries of quarterly updates from March 2023 through March 2024, a signed SCAP from May 2025, and an example of an audit roadmap dashboard. Navy officials also provided examples of system-level migration updates. For example, officials provided a briefing from a December 2023 integrated status weekly review meeting that discussed Navy ERP migration progress by functional task area and documented potential problem items, risks, and action items.

However, the Navy did not publish an updated SCAP between March 2024 and May 2025. Navy officials stated that the Navy had been unable to develop quarterly SCAP updates since March 2024 due to limited resources. In February 2025, Navy officials stated that they had obtained additional resources and planned to resume publishing quarterly updates on April 30, 2025. Further, these officials stated that they were planning to update the SCAP based on a new list of systems derived by FMO and FMS leadership. The Navy provided its May 2025 SCAP in June 2025. Nevertheless, without regular quarterly SCAP updates, the Navy risks being unable to monitor the progress systems are making to meet their intended migration dates.

Establish a tracking system to manage progress, issues, and other action items—partially met. The Navy partially addressed elements of this leading practice. Navy officials stated that risks and issues are monitored during weekly meetings with system owners where officials discuss progress by functional area and identify potential issues and action items. Officials also provided examples of briefings to leadership and stakeholders, such as briefings about progress associated with the Navy ERP system migration effort. In addition, the Navy SCAPs and the associated Summaries of Changes provide a mechanism for leadership to monitor progress and changes to planned system transition dates. However, they do not document issues and other action items.

Documenting issues and action items is particularly important given the number of changes that occurred across the SCAPs we evaluated. For example, the SCAPs contained delays and unanticipated changes to systems and dates that may indicate other issues associated with system transitions. In particular, they contained at least 111 changes to systems and system migration, functional shutdown, and system shutdown dates. Some of these changes were due to systems being descoped or consolidated and reflected progress towards the Navy’s efforts to streamline its financial management systems environment.[63]

However, the changes also included at least 49 delays to planned system transition dates, including 20 delays to functional shutdown and system shutdown dates. These changes are inconsistent with the Navy’s December 2020 Cattle Drive memorandum from the Under Secretary of the Navy. The memorandum called for portfolio managers and IT capability owners to develop transition plans with clear system and application sunset dates with no extensions.[64]

Navy officials provided various reasons for the changes in the SCAPs. With respect to the changes to transition dates, Navy FMS officials stated that modernization is a moving target and changes are to be expected. Navy FMS officials further stated that they are not aware of any underlying issues associated with the numerous extensions and changes to system transition dates. These officials stated that changes are made on a case-by-case basis and outside forces or possible mandates may contribute to delays and changes. However, the Navy did not document the underlying reasons for changes to system transition dates or associated issues to determine if underlying issues exist that Navy leadership can take action to address.

Navy officials stated that the SCAP was not intended to be a tool to manage progress, issues, and other action items related to migration planning at the Navy level. Officials stated that the SCAP was only intended to report on the status of system migrations. As noted, they stated that risks and issues are reviewed during system owner-level weekly meetings where officials discuss progress by functional area and identify potential risks and action items, as required by the Navy’s ERP Command Implementation Guide.

Nevertheless, the documentation provided about the Navy’s approach to monitoring system migrations did not demonstrate that it collected the information needed to identify and manage issues and other action items at the executive level. Further, while the Summaries of Changes that accompanied the updated SCAPs indicated that changes to key system transition dates occurred, this document was not sufficiently detailed to provide an executive-level means to monitor progress, issues, and other action items.

Without a comprehensive executive-level tracking system to manage issues and other action items, Navy leadership risks lacking key information about potential underlying issues that may contribute to changes to systems transition dates or action items that might help address these underlying issues. Further, without this critical information, the Navy risks being unable to identify actions that might limit changes to system transition dates in support of DOD’s goal of achieving a clean audit opinion by the end of 2028.

Conclusions

The Department of the Navy’s financial management system modernization and consolidation efforts are critical to both the Navy and DOD’s ability to achieve a clean audit opinion by the end of 2028. Attaining that goal would enable informed department officials to be accountable stewards of scarce federal resources needed for readiness and the warfighter. Further, it would strengthen the reliability of information needed by DOD decision-makers. To the Navy’s credit, the Navy announced in January 2026 that it had successfully migrated its remaining commands to Navy ERP as part of its effort to streamline general ledger systems. However, the Navy’s strategic planning efforts did not fully address leading practices to measure the results of its financial management systems modernization and consolidation goals.

In addition, the Navy did not fully implement leading practices to monitor and manage its audit-relevant financial management systems migration efforts in a comprehensive, enterprise-wide manner. Rather, the Navy’s system-focused approach places it at risk of taking a piecemeal approach to monitoring its progress. Moreover, Navy officials lack key information about potential underlying issues that may be impacting its progress for multiple audit-relevant system migrations. This includes maintaining information about issues that might be contributing to changes in system transition dates, which limits the Navy’s ability to identify actions to address these underlying issues. By not maintaining this critical information, the Navy risks not expeditiously reducing its excessive number of audit-relevant systems.

Further, without fully addressing leading practices for strategic and migration planning and taking steps to identify the magnitude and impact of schedule delays for systems on the critical path to achieving a clean audit opinion, the Navy risks not achieving its remaining systems modernization and consolidation goals in a timely manner. This in turn could result in the Navy not being able to fully support DOD’s auditability goals. In addition, lessons learned from the Navy’s migration efforts could provide helpful insights to other DOD components’ financial systems initiatives to better position DOD to achieve its goal of a clean audit opinion by the end of 2028.

Recommendations for Executive Action

We are making the following five recommendations to the Secretary of the Navy:

The Secretary of the Navy should direct the Office of the Assistant Secretary of the Navy (Financial Management and Comptroller) and other Navy entities, as appropriate, to ensure that it identifies and follows through on an approach to collect actual performance results for its financial systems goals. (Recommendation 1)

The Secretary of the Navy should direct the Office of the Assistant Secretary of the Navy (Financial Management and Comptroller) and other Navy entities, as appropriate, to ensure that the Navy develops an enterprise roadmap to guide its audit-relevant financial system migration efforts and ensure that it develops and uses an enterprise roadmap that fully addresses leading practices. (Recommendation 2)

The Secretary of the Navy should direct the Office of the Assistant Secretary of the Navy (Financial Management and Comptroller) and other Navy entities, as appropriate, to ensure that the Navy prioritizes its efforts to more closely monitor its audit-relevant system migrations by resuming more frequent Systems Consolidation Action Plan updates and ensuring these updates are provided to senior leadership and stakeholders. (Recommendation 3)

The Secretary of the Navy should direct the Office of the Assistant Secretary of the Navy (Financial Management and Comptroller) and other Navy entities, as appropriate, to ensure that the Navy develops and follows through with a process to track and manage issues and other action items associated with its audit-relevant system migration efforts. This process should include a mechanism to monitor identified issues and action items, evaluate the results, and remediate identified deficiencies on a timely basis. (Recommendation 4)

The Secretary of the Navy should direct the Office of the Assistant Secretary of the Navy (Financial Management and Comptroller) and other Navy entities, as appropriate, to ensure that the Navy takes steps to identify the magnitude of schedule delays to audit-relevant systems and their impact to systems that are on the critical path for achieving a clean audit opinion by the end of 2028. (Recommendation 5)

Agency Comments and Our Evaluation

We provided a draft of this report to the Department of the Navy (Navy) for review and comment.

In its written comments, reproduced in appendix IV and addressed below, the Navy concurred with one recommendation, partially concurred with two recommendations, and did not concur with two recommendations. The Navy also described actions it has taken and plans to take associated with our recommendations. In addition, the Navy provided technical comments, which we incorporated as appropriate.

After the completion of our fieldwork in February 2025, the Navy provided additional information between June and November 2025 that included evidence of actions taken before and after we concluded our fieldwork. Given the importance of the Navy’s efforts to modernize its financial management systems environment to DOD’s goal of achieving a clean audit opinion by the end of 2028, we revised this report to reflect actions that occurred prior to the conclusion of our fieldwork. In what follows, we also provide examples of actions the Navy took after the conclusion of our fieldwork.

The Navy concurred with recommendation 2 and stated that it is committed to developing and implementing a comprehensive enterprise roadmap to guide audit-relevant financial system migration efforts consistent with leading practices. Further, the Navy stated that its goal is to have the SCAP become an enterprise-wide document and basis for future system consolidations.

The Navy partially concurred with recommendation 3, but described plans consistent with the recommendation. More specifically, the Navy stated that it will immediately resume quarterly SCAP updates for audit relevant systems, beginning in Quarter 1 of Fiscal Year 2026.

The Navy partially concurred with recommendation 4. Specifically, the Navy stated that it has already established a robust process to track, manage, and remediate issues and action items associated with audit-relevant system migration efforts. The department also stated that this process includes recurring meetings to ensure swift notification, communication, and the implementation of mitigation strategies to eliminate or minimize any associated impacts.

We acknowledge that Navy officials provided examples of briefings to leadership and stakeholders, such as briefings about progress associated with the Navy ERP system migration effort. We also acknowledge the successes referred to elsewhere in the Navy’s response, such as reducing the number of its general ledger systems.

However, the documentation provided about the Navy’s approach to monitoring system migrations did not demonstrate that it had a robust process in place to collect the information needed to identify and manage issues and other action items at the executive level. Therefore, we maintain that the Navy should develop and follow through with a process to track and manage issues and other action items associated with its audit-relevant system migration efforts.

The Navy did not concur with recommendation 1 and stated that it continuously monitors and tracks performance metrics for each strategic goal in the Department of the Navy Financial Management Strategy’s annual I-Plan. For example, officials described weekly status reporting meetings throughout migration efforts conducted by Navy FMS, the Navy ERP program office, and Navy commands to track and manage risks, progress, and metrics, such as those related to data cleansing, change management, and user acceptance testing. Nevertheless, Navy officials stated the Navy remains committed to continuously improving how it communicates results to leadership and measures achievement of intended financial systems modernization outcomes.

As noted, after the completion of our fieldwork in February 2025, the Navy provided additional information that included evidence of actions taken before and after we concluded our fieldwork. We updated this report to reflect additional actions that occurred prior to the conclusion of our fieldwork.

However, the information the Navy provided to demonstrate actions that occurred after we concluded our fieldwork did not fully address this recommendation. To the Navy’s credit, it provided evidence to demonstrate that it has further implemented the performance measurement approaches it identified. For example, Navy officials previously described the use of situation summaries to monitor the status of data cleansing activities and related risks and, more broadly, the achievement of go-live for three commands that were scheduled to migrate to Navy ERP in FY 2025. In September 2025, officials provided evidence to demonstrate that each of the three commands developed weekly situation summary briefings in the leadup to Navy ERP migration documenting, among other things, data cleansing and other metrics, risks, and a schedule for the command’s migration to Navy ERP. Further, Navy officials demonstrated that meetings included a discussion of data cleansing and other targets and migration progress with FMS leadership.

However, the Navy still did not demonstrate full alignment with the strategic planning leading practice referenced in this report and associated with this recommendation. For example, regarding a portion of a FY 2025 I-Plan goal and related performance metric for a Navy command to achieve full operational tempo—the milestone after production cutover—in Navy ERP by the second quarter of FY 2025, officials stated that they measured progress by holding weekly situation summary meetings, completing a checklist, and internally communicating completion of the milestone. As previously noted, prior to the completion of our fieldwork, the Navy provided evidence of the latter two elements, including a signed full operational tempo checklist and email communication from FMS leadership to various Navy and DOD officials noting achievement of the milestone. However, both before and after the completion of our fieldwork, the Navy did not provide evidence of weekly situation summary meetings or related presentations to measure progress as the command approached full operational tempo in Navy ERP. While we recognize that the Navy has made important progress, we maintain that the Navy should fully follow through with its defined approaches to collect performance data and assess results associated with its financial systems goals.

The Navy also did not concur with recommendation 5 but described actions that may be consistent with this recommendation. With respect to its nonconcurrence, Navy officials described actions the department has taken to improve its financial management systems. For example, Navy officials stated they have continuously improved their IT controls environment through closing IT notices of findings and recommendations to show measurable progress towards achieving audit goals. Navy officials also described decommissioning one audit relevant system and migrating audit-relevant functionality out of an additional system in FY 2025. We recognize that the Navy has made progress in addressing its IT notices of findings and recommendations and decommissioning audit-relevant systems.

Nevertheless, the Navy also stated that it is developing a comprehensive critical path roadmap that includes rigorous tracking and reporting mechanisms to identify and mitigate potential delays for all other audit-relevant system migration efforts necessary to achieve a clean audit opinion by the end of 2028. We maintain that it is critical for the Navy to take steps to identify the magnitude of schedule delays to audit-relevant systems and their impact to systems that are on the critical path to achieving a clean audit opinion by the end of 2028. Developing a critical path roadmap for its audit-relevant systems can be an important step in addressing this recommendation.

We are sending copies of this report to the appropriate congressional committees, the Secretary of Defense, and the Secretary of the Navy. In addition, the report will be available at no charge on the GAO website at http://www.gao.gov.

If you or your staff members have any questions on matters discussed in this report, please contact Vijay A. D’Souza at dsouzav@gao.gov and Asif A. Khan at khana@gao.gov. Contact points for our Offices of Congressional Relations and Media Relations may be found on the last page of this report. GAO staff who made major contributions to this report are listed in appendix V.

Vijay A. D’Souza

Director

Information Technology and Cybersecurity

Asif A. Khan

Director

Financial Management and Assurance

List of Committees

The Honorable Roger Wicker

Chairman

The Honorable Jack Reed

Ranking Member

Committee on Armed Services

United States Senate

The Honorable Rand Paul, M.D.

Chairman

The Honorable Gary C. Peters

Ranking Member

Committee on Homeland Security and Governmental Affairs

United States Senate

The Honorable Mike Rogers

Chairman

The Honorable Adam Smith

Ranking Member

Committee on Armed Services

House of Representatives

The Honorable James Comer

Chairman

The Honorable Robert Garcia

Ranking Member

Committee on Oversight and Government Reform

House of Representatives

Our objectives were to determine the extent to which the Department of the Navy’s efforts to modernize its financial management systems (1) are consistent with strategic planning leading practices and (2) align with migration planning leading practices.

To address the first objective, we reviewed prior GAO reports and guidance from the Office of Management and Budget (OMB) to identify leading practices for strategic planning.[65] Specifically, we used each of these documents to identify strategic planning leading practices, which we grouped based on similarities. We then used these grouped statements to identify three strategic planning leading practices and related descriptions. According to OMB and GAO guidance, leading practices for strategic planning include: (1) aligning with the agency’s overall strategic plan; (2) identifying results-oriented goals and performance metrics; and (3) identifying and implementing performance measurement approaches to measure actual results.

We then used these leading practices to assess the Navy’s financial management systems strategic planning efforts. To conduct this assessment, we reviewed two prior Navy strategic plans—the Secretary of the Navy Year 3 Strategic Vision, Goals, and Implementation Guidance Fiscal Years 2020–2023 and the Navy’s Business Operations Plan Fiscal Years 2021–2023—as well as its current strategic plan, the One Navy-Marine Corps Team: Advancing the Department of the Navy Priorities strategy.[66] We also reviewed the Department of Defense Financial Management Strategy FY22-26. In addition, we reviewed the Department of the Navy Financial Management Strategy and the Department of the Navy Financial Management Strategy Fiscal Year 2024 Implementation Plan and Fiscal Year 2025 Implementation Plan.[67] We limited our analysis of the Navy Financial Management Strategy and associated Implementation Plan documents to portions associated with consolidating financial management systems. Specifically, our analysis focused on Goal 4 of the Navy Financial Management Strategy, which is associated with consolidating Navy financial systems and enhancing cybersecurity controls.

For the first leading practice, we compared the strategic goals and guiding principles in the Navy and Department of Defense (DOD) strategic plans to the goals and metrics contained in the three Navy financial management strategic planning documents. For each leading practice, we assessed if the Navy’s strategic planning efforts for its financial management systems transition met, partially met, or did not meet each of the three leading practices. In doing so, we assessed the Navy’s control activities designed to achieve financial system modernization strategic planning objectives; identify, analyze, and respond to risks to financial management systems transition efforts; implement policies in support of its strategic planning efforts; and use and communicate quality information to achieve the objectives of the financial management systems transition. Our assessment was based on the following decision rules:

· Met: the Navy provided sufficient evidence and documentation related to strategic planning that addressed or substantially addressed all elements of the leading practice.

· Partially met: the Navy provided evidence satisfying some, but not all, elements of the leading practice.

· Not met: the Navy’s evidence or documentation did not address any elements of the leading practice.

In addition, we met with Navy officials in the Office of the Assistant Secretary of the Navy (Financial Management and Comptroller), Office of Financial Operations (FMO), Financial Management Systems (FMS), and Chief Information Officer to understand the rationale behind decisions made when developing and implementing the strategic planning documents and the reasons for any differences between Navy financial management systems strategic planning efforts and selected leading practices. We also followed up with Navy officials in writing to, among other things, clarify details documented within and linkages between Navy strategic planning documents.

To address the second objective, we reviewed prior GAO reports and other relevant federal and nonfederal guidance to identify leading practices for migration planning. For example, OMB calls for agencies to develop an enterprise roadmap that documents the current and future states of a systems environment at a high level and present a transition plan for moving from the current to the future in an efficient, effective manner.[68] Such a roadmap should discuss performance gaps, resource requirements, and planned solutions, and it should map the strategy to projects and budget. The roadmap should also document the tasks, time frames, and milestones for implementing new solutions. In addition, it should contain an inventory of systems.

Further, we reviewed Software Engineering Institute guidance on migration planning, which includes practices such as providing a mechanism for executive management to monitor the effort; scheduling periodic reviews; and establishing a tracking system to manage progress, issues, and other action items.[69] We also reviewed GAO’s guidance for IT investment management, which calls for executive-level oversight and monitoring of IT system portfolios. This includes oversight and monitoring of system performance (e.g., performance against schedule expectations) and identifying and addressing identified issues.[70] Further, we reviewed GAO’s guidance on internal controls, which calls for management to establish and operate monitoring activities, evaluate the results, and remediate identified deficiencies on a timely basis.[71] This approach is consistent with the above Software Engineering Institute guidance.

We used each of these documents to identify migration planning leading practices, which we grouped based on similarities. We then used these grouped statements to identify four migration planning leading practices and related descriptions. Specifically, we identified (1) developing an enterprise roadmap; (2) providing a mechanism for executive management to monitor the migration effort; (3) scheduling periodic reviews; and (4) establishing a tracking system for executive management to manage progress, issues, and other action items.

To assess the Navy’s migration planning effort, we reviewed the Navy’s key financial management systems transition planning documents, such as quarterly Systems Consolidation Action Plans (SCAP) for March 2023, September 2023, December 2023, and March 2024 and associated quarterly SCAP Summaries of Changes. We then evaluated these documents against the selected system migration planning leading practices.[72] We also used information obtained from officials to further supplement our understanding of Navy’s migration planning process and our analysis of the extent to which Navy followed relevant leading practices. In addition, we reviewed information provided by Navy officials regarding how the Navy manages and monitors financial system migrations at the system level.

We also compared the SCAPs and the Summaries of Changes to determine the amount of changes over time regarding key transition dates, including migration dates, functional shutdown dates, and system shutdown/retirement dates.[73] In addition, we met with and obtained written responses from cognizant officials from the Office of the Assistant Secretary of the Navy (Financial Management and Comptroller), FMS, FMO, and the Chief Information Officer to discuss, among other things, the changes that we identified across the plans (e.g., different systems, different system transition dates, and changes to transition dates over time) and reasons for those differences.

Using an approach consistent with our assessment of Navy’s strategic planning leading practices, we assessed whether the Navy met, partially met, or did not meet each of the leading practices for migration planning.

We conducted this performance audit from October 2023 to April 2026 in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

According to Navy officials, multiple officials have responsibilities associated with overseeing or supporting the Navy’s financial management modernization efforts. Table 4 summarizes their respective roles and responsibilities.

Table 4: Roles and Responsibilities Associated with the Navy’s Financial Management Modernization, According to Navy Officials

|

Role |

Navy financial management modernization-related responsibilities |

|

Deputy Assistant Secretary of the Navy, Financial Management Systems |

Overseeing the Navy’s financial management transformation, including the financial statement audit and modernization of financial systems; ensuring complete, reliable, consistent, timely, and accurate information on the Navy audit-relevant Systems Consolidation Action Plans (SCAP), which maintain data on the migration and shutdown dates of audit-relevant financial management systems; and monitoring and reviewing the implementation of audit recommendations. |

|

Principal Deputy Assistant Secretary of the Navy, Financial Management and Comptroller |

Overseeing strategy and working closely with the leadership throughout the Navy to provide recommendations and support to the Assistant Secretary of the Navy (Financial Management and Comptroller) on efforts related to the Navy’s financial management transformation, including the financial statement audit and modernization of financial systems. |

|

Acting Assistant Secretary of the Navy, Financial Management and Comptroller |

Co-leading Operation Cattle Drive and managing the Navy Financial Management Strategy to improve and transform Navy financial management operations, in support of the Navy SCAP. |

|

Deputy Assistant Secretary of the Navy, Financial Operations |

Executing the responsibilities for the Navy in accounting and financial management matters related to the financial statement audit and modernization of financial systems. |

|

Assistant General Counsel-Fiscal, Financial Management and Comptroller |

Assisting the Assistant Secretary of the Navy (Financial Management and Comptroller) with implementing the Navy’s financial management transformation, including the financial statement audit and modernization of financial systems. |

|

Deputy Assistant Secretary of the Navy, Office of Budget |