Report to Congressional Committees

United States Government Accountability Office

A report to congressional committees.

For more information, contact: Kristen Kociolek at kociolekk@gao.gov

What GAO Found

GAO found that the Air Force accurately accounted for general equipment that contractors hold, at selected locations, in two of its accountable property systems of record. Specifically, GAO was able to verify all 187 records that Reliability, Availability, and Maintainability for Pods & Integrated Systems reported as being maintained at the Raytheon Missile Systems facility. That system had accurate records for the pods that are normally affixed to a variety of aircraft the Air Force operates. In addition, GAO was able to verify all sample items tested from the Defense Property Accountability System, which had accurate records for items such as trucks and other vehicles used by Air Force contractors.

However, GAO found that the Air Force has not accurately accounted for general equipment that contractors hold, at selected locations, in its Stock Control System (D035) accountable property systems. Specifically, GAO could not locate 18 of the 96 sampled items at the Reliance Test & Technology facility at Eglin Air Force Base in Valparaiso, Florida. In addition, GAO could not locate 58 of the104 sampled items at the Standard Aero facility in San Antonio, Texas, such as a torque adapter, an electric synthesizer, and a gear assembly adapter.

In addition, the D035 system lacks item descriptions and serial numbers, making it impossible to track and distinguish between items that share the same national stock number. Specifically, if a contractor has multiple of the same general equipment item provided to it, the Air Force cannot determine when one of the items is returned, or which item should be updated in the D035 system. The Air Force could see a significant improvement in the accuracy of general equipment information in the D035 system by ensuring that all equipment records have item descriptions and serial numbers.

GAO also found that the Air Force’s D035 system did not accurately record equipment that contractors returned when no longer needed for contract performance. This is because the Air Force Program Office did not establish an integrated product team to create proper disposition instructions and system updates as required by policy. As a result, the Air Force may be unaware of general equipment it has in stock and risks purchasing items unnecessarily.

Why GAO Did This Study

In fiscal year 2024, the Air Force reported $118.4 billion of the Department of Defense (DOD) consolidated $443.5 billion of general equipment, a portion of which is in the possession of a contractor. DOD has long-standing issues with tracking and reporting equipment for financial reporting purposes. GAO performed this audit related to its statutory requirement to audit the U.S. government’s consolidated financial statements. This report examines the extent to which the Air Force has properly recorded general equipment contractors hold in its accountable property systems of record.

GAO reviewed relevant annual financial reports and DOD and Air Force guidance, regulations, manuals, and instructions. In addition, GAO visited five locations to test samples of general equipment contractors hold. GAO’s testing focused on locating items at the contractor location and selecting a sample of general equipment that was physically observed at the location to trace back to the Air Force accountable property system of record. GAO also interviewed Air Force and contractor officials.

What GAO Recommends

GAO is making two recommendations to the Air Force to (1) ensure that all general equipment contractors hold that is tracked in the D035 system has item descriptions and serial numbers and (2) ensure that officials adhere to policies requiring program offices to establish integrated product teams to plan for and manage the receipt of returned general equipment that is maintained in the D035 system. The Air Force partially concurred with the first recommendation and concurred with the second. The actions that the Air Force plans to take address the intent of both recommendations.

|

Abbreviations |

|

|

|

|

|

AFB |

Air Force Base |

|

APSR |

accountable property system of record |

|

D035 |

Stock Control System |

|

DOD |

Department of Defense |

|

DPAS |

Defense Property Accountability System |

|

GFP |

government-furnished property |

|

LCO |

Loan Control Officer |

|

RAMPOD |

Reliability, Availability, Maintainability for Pods & Integrated Systems |

This is a work of the U.S. government and is not subject to copyright protection in the United States. The published product may be reproduced and distributed in its entirety without further permission from GAO. However, because this work may contain copyrighted images or other material, permission from the copyright holder may be necessary if you wish to reproduce this material separately.

February 4, 2026

Congressional Committees

The Department of Defense (DOD) is the only major federal agency that has never received a clean audit opinion on its department-wide financial statements. This is one of the three major impediments preventing GAO from expressing an opinion on the accrual-based consolidated financial statements of the U.S. government.[1] In addition, GAO continues to report DOD financial management as a high-risk area in its biennial High-Risk List.[2]

DOD’s financial statement auditors have reported a DOD-wide material weakness related to government property in the possession of contractors since fiscal year 2001.[3] In DOD’s fiscal year 2024 agency financial report, auditors reported that DOD components did not have the policies, procedures, and internal controls in place to effectively oversee and report on government property in the possession of contractors. As a result, DOD has been unable to accurately and completely account for the total amount of government property possessed by its contractors. Proper oversight and accounting for these assets are key to DOD’s ability to address the material weakness, mitigate the risks the weakness creates, and help produce auditable financial statements.

The Department of the Air Force comprises a significant amount of the general property, plant and equipment in DOD’s consolidated financial statements. Specifically, for fiscal year 2024, the Air Force had $118.4 billion of the $443.5 billion of general equipment that DOD reported. A portion of this equipment is possessed by contractors, referred as general equipment that contractors hold.

We performed this audit in connection with the statutory requirement for GAO to audit the U.S. government’s consolidated financial statements, which cover all accounts and associated activities of executive branch agencies, including DOD.[4] This report examines the extent to which the Air Force has properly recorded general equipment that contractors hold in its accountable property systems of record (APSR).

To address our objective, we reviewed DOD’s and the Air Force’s fiscal year 2024 annual financial reports and relevant DOD and Air Force guidance, regulations, manuals, and instructions. In addition, we interviewed Air Force officials as well as contractors and observed key processes to record and report general equipment in the Air Force’s APSRs.[5] According to the Air Force, the APSRs we selected for review were those that the Air Force uses to record general equipment that contractors hold.

To assess the existence of general equipment recorded in the Air Force’s APSRs,[6] we reviewed the total population of Air Force-owned general equipment that is in contractor possession and selected a generalizable sample of records for general equipment that contractors hold at five locations.[7] We selected the five locations based on a variety of factors, including the number of inventory items at the site, the APSR used to account for the inventory at the location, and the geographic location. We analyzed the data from each of the systems to determine the locations to conduct existence and completeness testing. For the selected records, we reviewed supporting documentation to determine if the Air Force had recorded transactions consistent with relevant policies and procedures. We also performed observations of the selected recorded items to validate the existence of recorded assets. While on-site, we also selected a nongeneralizable sample of Air Force-owned general equipment found at the contractor facility, to assess the completeness of transactions recorded for general equipment that contractors hold. This was to determine whether Air Force personnel properly recorded the items in the Air Force APSRs in accordance with relevant policies and procedures.

We conducted this performance audit from March 2024 to February 2026 in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

Background

DOD defines government-furnished property (GFP) as property in the possession of, or directly acquired by, the government and subsequently furnished to a contractor, including subcontractors and alternate locations, for performance of a contract. GFP includes equipment, special tools, and special test equipment. It does not include consumables, material items, or items held as inventory.

The Air Force uses an APSR as a system to control and manage accountable property records, including those for GFP. Entities establish accountability property records when they must control and manage items to protect against unauthorized use, disclosure, or loss, even if an entity does not report an item within its financial statements.

The Air Force reports general equipment (including GFP) in its financial statements under property, plant, and equipment. Within the notes to the financial statement, equipment is broken out as general equipment and military equipment. According to officials, the Air Force uses the Defense Property Accountability System (DPAS) as the APSR to generate general equipment information and the Reliability and Maintainability Information System, and Reliability, Availability, and Maintainability for Pods & Integrated Systems (RAMPOD) to generate military equipment information. In addition, it uses the Stock Control System (D035) to manage general equipment held at contractor facilities. However, according to the Air Force, it does not use general equipment information tracked in D035 for financial reporting purposes.

DOD and Air Force policy requires all accountable property and respective data elements to be tracked in an APSR.[8] Officials are to establish accountable property records in an APSR for property of any value provided to a contractor as GFP. Certain data elements are also required in an accountable property record and APSR, including item descriptions, serial numbers, and national stock numbers. In addition, officials must keep accountable property records current and reflect the status, location, financial information, and condition until authorized disposition of the property occurs.

The Air Force policy manual also requires specific actions when contractors no longer require general equipment that they hold for contract performance, including when (1) the program office identifies the general equipment as such, (2) the contract’s period of performance or loan of the equipment to the contractor reaches its end, or (3) the contractor sends the program office a request for disposition.[9] When any of these events occur, the manual requires the program office to form an integrated product team to develop disposition instructions for the general equipment that contractors hold. The team must include, at a minimum, the contracting officer, resource manager, product support manager, loan control officer (LCO), and a representative from the Air Force Material Command. The integrated product team is to provide disposition instructions to the contracting office, which is then to provide them to the contractor, modifying the contract as needed. Upon the receipt of the returned general equipment to the government, the LCO is then to update the D035 system and clear the loaned item from the system.

The Air Force Has Not Accurately Recorded General Equipment That Contractors Hold in All of Its Accountable Property Systems

The Air Force Accurately Accounted for General Equipment That Contractors Hold in Two of Its Accountable Property Systems

Through existence and completeness testing we performed, we found that the Air Force accounted for general equipment that contractors hold, at the selected locations, in two of its APSRs.[10] Specifically, at Raytheon Missile Systems facility in Tucson, Arizona, we found no errors in the total population of 187 equipment items recorded in RAMPOD. That system had accurate records for the pods that are normally affixed to a variety of aircraft the Air Force operates. We were able to verify the existence of all 53 equipment items that we sampled from RAMPOD. In addition, through completeness testing, we were able to trace 56 equipment items that we observed at the contractor location back to RAMPOD and verify the remaining 78 items through Air Force inventory testing or shipping documentation.

In addition, we found that the Air Force generally accounted for its equipment accurately in DPAS at two locations, that included such items as trucks and other vehicles used by Air Force contractors. At both Sheppard Air Force Base (AFB) in Wichita Falls, Texas, and Eglin AFB in Valparaiso, Florida, we were able to verify the existence of all sampled items from DPAS.[11] However, at Sheppard AFB, we were not able to trace two of the 17 equipment items that we physically observed for completeness testing back to DPAS. The Air Force has corrected one of the two errors, which was related to an inaccurate item label. The second item was not found in DPAS. We were able to trace all items we physically observed as part of our completeness testing at Eglin AFB back to DPAS records.

The Air Force Has Not Accurately Accounted for General Equipment That Contractors Hold in One of Its Accountable Property Systems

We performed existence and completeness testing for the Air Force’s D035 system at (1) Reliance Test & Technology at Eglin AFB, Florida, in April 2025 and (2) Standard Aero in San Antonio, Texas, in March 2025. We found that the Air Force did not accurately account for general equipment that contractors hold in its D035 system at the two contractor facilities we visited. In addition, the Air Force’s D035 system lacks item descriptions and serial numbers, making it impossible to track and distinguish between items that share the same national stock number.[12] As a result, to perform our sample testing, we used the contractor-created serial numbers identified for each of the sample items to trace the items back to the contractor system. Once found there, we determined the national stock number and the quantity the contractor has recorded in its possession and cross-referenced these identifiers to the national stock number in the Air Force D035 system.

Based on the results of our generalizable sample, we found that about 24 percent of the items recorded in the D035 system could not be located at the Reliance Test & Technology facility at Eglin AFB.[13] Specifically, we could not locate 14 equipment items out of a sample size of 58 recorded in the D035 system at the facility. Examples of missing items included an oscilloscope, heater, and signal generator. According to D035, the facility had a total of 140 general equipment items during the time of our visit. Table 1 presents the errors we identified.

Table 1: Existence Testing Errors in Sampled Air Force Stock Control System (D035) Accountable Property System at Reliance Test & Technology at Eglin Air Force Base as of April 2025

|

Description of error |

Number of

errors found in sample of |

|

Items listed as being held by the contractor in the Air Force D035 system that were returned to the Air Force |

14 |

Source: GAO analysis of Air Force data. | GAO‑26‑107442

While on-site at the Reliance Test & Technology facility, we also selected a nongeneralizable sample of 38 general equipment items that we physically observed for completeness testing. We identified four items that were not properly recorded in the D035 system. Table 2 presents the errors we identified.

Table 2: Completeness Testing Errors in Sampled Air Force Stock Control System (D035) Accountable Property System at Reliance Test & Technology at Eglin Air Force Base as of April 2025

|

Description of error |

Number of

errors found in sample of |

|

National stock numbers of items not found in the Air Force D035 system |

3 |

|

Air Force D035 system had fewer items recorded than what was physically observed |

1 |

|

Total |

4 |

Source: GAO analysis of Air Force data. | GAO‑26‑107442

Based on the results of our generalizable sample, we found the rate of error is about 46 percent of the items in the D035 system at the Standard Aero facility in San Antonio, Texas.[14] Specifically, we identified 31 equipment items out of a sample size of 68 recorded in the D035 system with errors. Examples of missing items included a torque adapter, an electric synthesizer, and a gear assembly adapter. According to D035, the facility had a total of 1,085 general equipment items during the time of our visit. Table 3 presents the errors we identified.

Table 3: Existence Testing Errors in Sampled Air Force Stock Control System (D035) Accountable Property System at Standard Aero Facility in San Antonio, Texas, as of March 2025

|

Description of error |

Number of

errors found in sample of |

|

Air Force D035 system did not match the quantity in the contractor system or number we observed |

17 |

|

Items that are missing |

11 |

|

Items misclassified as equipment not materials |

3 |

|

Total |

31 |

Source: GAO analysis of Air Force data. | GAO‑26‑107442

While onsite at the Standard Aero facility, we selected a nongeneralizable sample of 36 general equipment items for completeness testing. We identified 27 items that we could not trace to the D035 system. Table 4 presents the errors we identified.

Table 4: Completeness Testing Errors in Sampled Air Force Stock Control System (D035) Accountable Property System at Standard Aero Facility in San Antonio, Texas, as of March 2025

|

Description of error |

Number of

errors found in sample of |

|

Items that could not be found in the Air Force records or contractor system |

21 |

|

Instances where the item could be one of multiple listings with the same national stock number in the Air Force D035 system |

6 |

|

Total |

27 |

Source: GAO analysis of Air Force data. | GAO‑26‑107442

Air Force policy requires all accountable property and respective data elements to be tracked in an APSR, including item descriptions, serial numbers, and national stock numbers. Also, accountable property records must be kept current and reflect status, location, and condition until authorized disposition of the property occurs. However, we found that the Air Force’s D035 system lacks item descriptions and serial numbers as required. The system, as it was originally designed, did not contain those fields. As a result, it was impossible to track and distinguish between items that share the same national stock number without the assistance of contractor systems and records. Specifically, if a contractor has multiple of the same general equipment item provided to it, the Air Force cannot determine when one of the items is returned or which item should be updated in the D035 system. An Air Force official stated that there are plans to migrate equipment tracked in the D035 system to DPAS, which does contain item description and serial number fields, but that transition has not been finalized.

As stated earlier, Air Force policy also requires that the Air Force Program Office form an integrated product team to develop disposition instructions for GFP that is no longer needed for contract performance. However, we found that the Air Force’s D035 system does not accurately record returned equipment from contractors because the Program Office did not establish an integrated product team to create proper disposition instructions. Air Force officials instead stated that contractors interacted directly with logistics personnel to facilitate the return of the item. As a result, the LCO may be unaware of returned general equipment that need to be updated in the system, and the Air Force may be unaware of general equipment items it has on hand and thus risks purchasing additional items unnecessarily.

Conclusions

The Air Force has worked for years to produce auditable financial statements, which need to include accurate accounting for general equipment that contractors hold. While two of its APSRs had accurate records at selected sites, the D035 APSR continues to include errors. The Air Force could see a significant improvement in the accuracy and reliability of general equipment information in the D035 system by ensuring that all equipment has item descriptions and serial numbers in the system. Serial numbers will make it easier to differentiate between items, reducing the risk of inventory errors and mismanagement. Additionally, by ensuring program offices adhere to existing requirements for establishing integrated product teams when contractors no longer require general equipment, the Air Force will strengthen its ability to oversee equipment transitions. These measures will enhance accountability, minimize inventory discrepancies, and improve the overall effectiveness of the Air Force’s asset management.

Recommendations for Executive Action

We are making the following two recommendations to the Air Force:

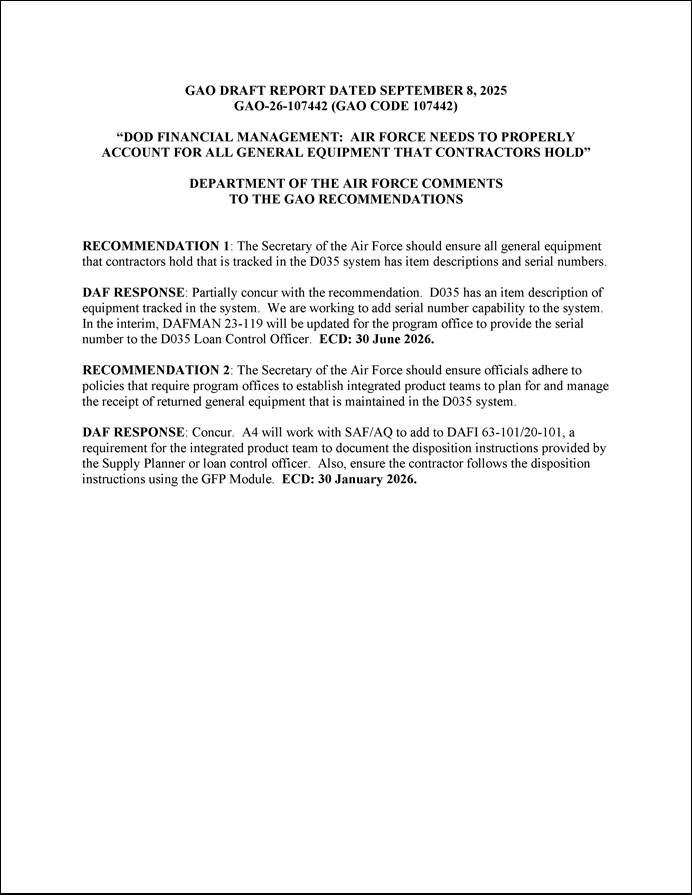

The Secretary of the Air Force should ensure that all general equipment that contractors hold that is tracked in the D035 system has item descriptions and serial numbers. (Recommendation 1)

The Secretary of the Air Force should ensure that officials adhere to policies requiring program offices to establish integrated product teams to plan for and manage the receipt of returned general equipment that is maintained in the D035 system. (Recommendation 2)

Agency Comments and Our Evaluation

We provided a draft of this report to the Air Force for review and comment. We received written comments from the Air Force, which are reproduced in appendix I and summarized below.

The Air Force partially agreed with the first recommendation, agreed with the second recommendation, and discussed planned implementation steps. For our first recommendation, the Air Force stated that the D035 system has an item description of equipment tracked in the system. However, the data we obtained from the Air Force did not have item descriptions. The Air Force further stated that it is working to add serial number capability to the D035 system and will update program office policy to provide each serial number to the D035 Loan Control Officer. If implemented effectively, these actions should address the intent of our recommendation.

For our second recommendation, the Air Force said that it will update its policy to require the integrated product team to document the disposition instructions that the Supply Planner or Loan Control Officer provide and ensure that the contractor follows them. If implemented effectively, this action should also address the intent of our recommendation.

We are sending copies of this report to the appropriate congressional committees and the Secretary of the Air Force. In addition, the report is available at no charge on the GAO website at https://www.gao.gov.

If you or your staff have any questions about this report, please contact me at kociolekk@gao.gov. Contact points for our Offices of Congressional Relations and Public Affairs may be found on the last page of this report. GAO staff who made key contributions to this report are listed in appendix II.

Kristen A. Kociolek

Managing Director, Financial Management and Assurance

List of Committees

The Honorable Roger Wicker

Chairman

The Honorable Jack Reed

Ranking Member

Committee on Armed Services

United States Senate

The Honorable Rand Paul, M.D.

Chairman

The Honorable Gary C. Peters

Ranking Member

Committee on Homeland Security and Governmental Affairs

United States Senate

The Honorable Mike Rogers

Chairman

The Honorable Adam Smith

Ranking Member

Committee on Armed Services

House of Representatives

The Honorable James Comer

Chairman

The Honorable Robert Garcia

Ranking Member

Committee on Oversight and Government Reform

House of Representatives

Appendix I: Comments from the Department of the Air Force

Kristen Kociolek, kociolekk@gao.gov

In addition to the contact named above, Jonathan Meyer (Assistant Director), Kevin Scott (Auditor in Charge), and Michael Zalenski made major contributions to this report. Other key contributors include James Ashley, Julie Ann Clark, Anne Rhodes-Kline, Diana Lee, and Matthew Valenta.

The Government Accountability Office, the audit, evaluation, and investigative arm of Congress, exists to support Congress in meeting its constitutional responsibilities and to help improve the performance and accountability of the federal government for the American people. GAO examines the use of public funds; evaluates federal programs and policies; and provides analyses, recommendations, and other assistance to help Congress make informed oversight, policy, and funding decisions. GAO’s commitment to good government is reflected in its core values of accountability, integrity, and reliability.

Obtaining Copies of GAO Reports and Testimony

The fastest and easiest way to obtain copies of GAO documents at no cost is through our website. Each weekday afternoon, GAO posts on its website newly released reports, testimony, and correspondence. You can also subscribe to GAO’s email updates to receive notification of newly posted products.

Order by Phone

The price of each GAO publication reflects GAO’s actual cost of production and distribution and depends on the number of pages in the publication and whether the publication is printed in color or black and white. Pricing and ordering information is posted on GAO’s website, https://www.gao.gov/ordering.htm.

Place orders by calling (202) 512-6000, toll free (866) 801-7077,

or

TDD (202) 512-2537.

Orders may be paid for using American Express, Discover Card, MasterCard, Visa, check, or money order. Call for additional information.

Connect with GAO

Connect with GAO on X,

LinkedIn, Instagram, and YouTube.

Subscribe to our Email Updates. Listen to our Podcasts.

Visit GAO on the web at https://www.gao.gov.

To Report Fraud, Waste, and Abuse in Federal Programs

Contact FraudNet:

Website: https://www.gao.gov/about/what-gao-does/fraudnet

Automated answering system: (800) 424-5454

Media Relations

Sarah Kaczmarek, Managing Director, Media@gao.gov

Congressional Relations

David A. Powner, Acting Managing Director, CongRel@gao.gov

General Inquiries

[1]GAO, Financial Audit: FY 2024 and FY 2023 Consolidated Financial Statements of the U.S. Government, GAO‑25‑107421 (Washington, D.C.: Jan. 16, 2025). The other two major impediments are (1) the federal government’s inability to adequately account for intragovernmental activity and balances between federal entities and (2) weaknesses in the federal government’s process for preparing the consolidated financial statements.

[2]GAO’s High-Risk List is a biennial report that identifies government operations with vulnerabilities to fraud, waste, abuse, and mismanagement or in need of transformation. Each biennial update describes the status of high-risk areas, outlines actions that are needed to assure further progress, and identifies new high-risk areas needing attention by the executive branch and Congress. GAO, High-Risk Series: Heightened Attention Could Save Billions More and Improve Government Efficiency and Effectiveness, GAO‑25‑107743 (Washington, D.C.: Feb. 25, 2025).

[3]A material weakness is a deficiency, or combination of deficiencies, in internal control over financial reporting, such that there is a reasonable possibility that a material misstatement of the entity’s financial statements will not be prevented, or detected and corrected, on a timely basis. A deficiency in internal control exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, misstatements on a timely basis.

[4]31 U.S.C. § 331(e) requires the Secretary of the Treasury, in coordination with the Director of the Office of Management and Budget, to annually prepare and submit audited financial statements for the executive branch of the U.S. government to the President and Congress and requires GAO to audit these statements.

[5]We observed key processes at (1) The Boeing Guidance Repair Center in Heath, Ohio; (2) an Air Force facility in Dayton, Ohio; (3) Tinker Air Force Base in Oklahoma City, Oklahoma; and (4) Joint-base Langley-Eustis in Hampton, Virginia.

[6]The Air Force accountable property systems of record within the scope of our review included the Reliability, Availability, Maintainability for Pods & Integrated Systems (RAMPOD); the Stock Control System (D035); and the Defense Property Accountability System (DPAS), including its use by the Vehicle Support Chain Operations Squadron.

[7]We took samples from the following systems and locations: RAMPOD Raytheon Missile Systems in Tucson, Arizona; DPAS multiple on-site contractor facilities at Sheppard Air Force Base (AFB) in Wichita Falls, Texas, and Eglin AFB, Valparaiso, Florida; and D035 Standard Aero in San Antonio, Texas, and Reliance Test & Technology at Eglin AFB, Valparaiso, Florida.

[8]Department of the Air Force, Accountability and Management of DOD Equipment and Other Accountable Property, DODI 5000.64_DAFI 23-111 (Dec. 6, 2021).

[9]Department of the Air Force Manual 23-119, Government Furnished Property (Apr. 6, 2022).

[10]For our audit, we performed existence testing by selecting a sample of general equipment records from the accountable property system that we determined contractors hold and physically locating the items at the contractor location. In addition, we performed completeness testing by selecting a sample of general equipment items that we physically observed at the contractor location and tracing it back to the accountable property system.

[11]We completed testing with a sample size of 73 out of a population of 1,851 at Sheppard AFB in Wichita Falls, Texas, and a sample size of 61 out of a population of 324 at Eglin AFB in Valparaiso, Florida.

[12]The national stock number is a term used for the 13-digit stock number consisting of the four-digit Federal Supply Class and the nine-digit National Item Identification Number. Each national stock number is assigned to identify an item of supply and equipment within the material management functions. Only one national stock number is assigned to an item.

[13]The 95 percent confidence interval for this estimate ranges from 16 to 34 percent.

[14]The 95 percent confidence interval for this estimate ranges from 32 to 57 percent.