Report to Congressional Requesters

United States Government Accountability Office

A report to congressional requesters

Contact: Paula M. Rascona at rasconap@gao.gov

What GAO Found

Agencies can use more than 100 federal data sources—or a combination of them—to verify if recipients meet the eligibility criteria for federal programs throughout the award life cycle (which includes pre-award screening, post-award monitoring, and payment validation). As of September 2025, these included 28 data sources in the Do Not Pay working system (DNP) or designated for inclusion in DNP. However, weaknesses in data interoperability may hinder agencies’ ability to efficiently determine award and payment eligibility.

Data interoperability is the ability to share and disseminate standardized data in a way that is efficient, consistent, and accessible across different systems and users, for which high-quality data are essential. Without it, the risk of improper awards or payments increases, and the potential use of artificial intelligence and advanced analytics to assist agencies in making eligibility determinations is limited.

GAO found that, for more than 30 years, several laws and guidance have established general requirements related to data interoperability but have not established specific requirements for enforcing interoperability, such as for recipient eligibility data, throughout the federal government. Many of the data sources GAO identified, including those in DNP, were created to comply with legal requirements or to manage specific federal programs—not to support eligibility determinations for other agencies.

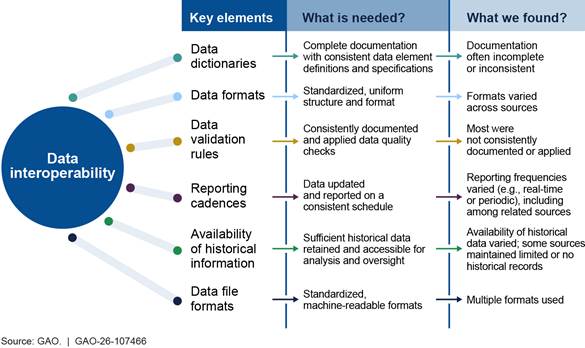

GAO also found a variety of obstacles and challenges that can affect the interoperability of the nine selected data sources that agencies may use for eligibility determinations (see figure).

Summary Comparison of Key Elements GAO Assessed to Eligibility Data Interoperability Needs and Observations

GAO also found that insufficient or improperly documented validation rules contributed to data quality issues. All nine selected data sources had data quality

Why GAO Did This Study

Government agencies are responsible for ensuring that data, including those needed to determine whether entities are eligible to receive federal awards and funds, are interoperable and reliable. Having interoperable data among agencies and data sources is crucial to improving the federal government’s efforts to detect and prevent improper payments. The Payment Integrity Information Act of 2019 requires executive agencies to take actions to reduce improper payments, such as using DNP to ensure that they make awards and payments only to eligible recipients.

GAO was asked to review how the government can better leverage USAspending.gov and other data sources to help enhance monitoring of federal spending and potential fraud, waste, and abuse. This report describes (1) federal data sources agencies may use to verify award recipient’s eligibility, (2) the extent to which selected eligibility data sources are interoperable, and (3) the extent to which eligibility data can be matched with USAspending.gov post-award information to analyze potentially ineligible recipients.

To conduct this review, GAO

· reviewed laws, regulations, OMB guidance, and relevant federal agencies’ websites and documentation to identify federal data sources that agencies can use to determine award recipients’ eligibility;

· reviewed laws, regulations, policies, and OMB guidance related to data interoperability to identify requirements;

· judgmentally selected nine eligibility data sources that were publicly available, in DNP or designated for inclusion in DNP, and included information about entities;

issues (e.g., missing, invalid, and duplicate data), and seven data sources had inconsistences between them, such as overlap in mutually exclusive data. These data quality issues undermine data reliability and interoperability for agencies seeking to make eligibility determinations.

To determine the extent to which eligibility and award data could be linked to help agencies identify whether potentially ineligible entities had received federal awards, GAO partially linked two data sources—System for Award Management (SAM) entity information and SAM Exclusion records—with USAspending.gov awards based on the unique entity identifiers (UEI). Most USAspending.gov award recipient UEIs could be linked to SAM entity information. However, most SAM Exclusion records, which identify parties excluded from receiving federal benefits and awards, such as contracts, did not have a UEI because this data source does not always require them. For the SAM Exclusion records with a UEI, GAO identified 2,074 awards to recipients that were listed in the data source at the time of the transaction. However, these matches by themselves do not indicate that the awards were improper or involved fraud, waste, or abuse. Making this determination requires specific evaluation of each case.

The inability to fully analyze SAM Exclusions and USAspending.gov data is an example of government-wide issues with data matching for recipient eligibility determinations. While analysis based on unique identifiers can support eligibility determinations, such identifiers might not always be required or available. Improved data interoperability—including standardized data elements and increased interoperability of data elements, such as names and addresses across data sources and agencies—could enable more comprehensive and efficient data matching. This would improve the government’s ability to identify potentially ineligible recipients.

In addition, several federal agencies and cross-agency groups support best practices for data management and interoperability. However, there is no data governance agency designated to establish and enforce mandatory data interoperability requirements to support recipient eligibility determinations. This has led to fragmented and inconsistent data management efforts that rely on agencies’ voluntary adoption.

Congress could help improve government-wide data interoperability for recipient eligibility data by assigning a single agency a lead role in establishing and implementing data interoperability requirements for recipient eligibility data sources. Based on its role supporting agencies in their efforts to prevent and detect improper payments and operating systems that collect, validate, and use financial, award, spending, and payment data, the Department of the Treasury could be assigned the explicit authority to establish and implement mandatory government-wide data standards and interoperability requirements for recipient eligibility data sources. Treasury could then work with the Chief Data Officer (CDO) Council and the Office of Management and Budget (OMB) to implement the requirements. Not having a data governance agency will contribute to unreliable reporting and inefficiencies as agencies attempt to determine recipient eligibility, and it will limit the government’s ability to leverage artificial intelligence and advanced analytics to identify and prevent improper awards and payments.

· reviewed agencies’ data dictionaries and documentation of validation processes about the selected eligibility data sources for consistency with interoperability practices GAO identified;

· tested data for fiscal years 2023 and 2024 for data quality issues, such as missing and invalid values, consistency, and comparability based on specifications established by the data owners and GAO’s professional judgment;

· interviewed officials at Treasury, the General Services Administration, and the Department of Health and Human Services’ Office of Inspector General because they own the selected data sources; and

· linked SAM data sources with USAspending.gov award information using UEI.

What GAO Recommends

GAO recommends that Congress consider assigning a single agency, such as Treasury, explicit authority to lead, in coordination with the CDO Council and in consultation with the OMB—and others, as needed—the development and implementation of government-wide data standards and interoperability requirements for recipient eligibility data sources. These sources include relevant financial, award, spending, and payment data needed to support eligibility determinations throughout the award life cycle. In its comments, the Bureau of the Fiscal Service agreed with the findings of GAO’s report and stated that, to be successful in setting government-wide data standards, Treasury would require clear authority to lead standardization related to eligibility data that are designated for use in DNP. OMB did not provide comments.

|

Abbreviations |

|

|

|

|

|

API |

application programming interface |

|

ARL |

Automatic Revocation of Exemption List |

|

CDO |

Chief Data Officer |

|

CFO Act |

Chief Financial Officers Act of 1990 |

|

CSV |

Comma-Separated Values |

|

DATA Act |

Digital Accountability and Transparency Act of 2014 |

|

DNP |

Do Not Pay working system |

|

EIN |

employer identification number |

|

FAC |

Federal Audit Clearinghouse |

|

FAR |

Federal Acquisition Regulation |

|

FFATA |

Federal Funding Accountability and Transparency Act of 2006 |

|

GREAT Act |

Grant Reporting Efficiency and Agreements Transparency Act of 2019 |

|

GSA |

General Services Administration |

|

HHS |

Department of Health and Human Services |

|

IRS |

Internal Revenue Service |

|

JSON |

JavaScript Object Notation |

|

LEIE |

List of Excluded Individuals and Entities |

|

NIEM |

National Information Exchange Model |

|

NPI |

National Provider Identifier |

|

OFAC |

Office of Foreign Assets Control |

|

OIG |

Office of Inspector General |

|

OMB |

Office of Management and Budget |

|

|

Portable Document Format |

|

PIIA |

Payment Integrity Information Act of 2019 |

|

SAM |

System for Award Management |

|

SDN |

Specially Designated Nationals and Blocked Persons |

|

SSA |

Social Security Administration |

|

UEI |

unique entity identifier |

|

Uniform Guidance |

Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards |

|

UTC |

Coordinated Universal Time |

|

XML |

Extensible Markup Language |

This is a work of the U.S. government and is not subject to copyright protection in the United States. The published product may be reproduced and distributed in its entirety without further permission from GAO. However, because this work may contain copyrighted images or other material, permission from the copyright holder may be necessary if you wish to reproduce this material separately.

June 16, 2026

Congressional Requesters

Accurate and timely eligibility data are essential for ensuring that agencies only award and pay federal funds to entities that meet applicable legal and regulatory criteria. This is especially critical in preventing the misuse of funds, including fraud, waste, and abuse. Inaccurate eligibility data, such as incomplete records, can lead to improper payments, including payments to ineligible recipients or to recipients that cannot be verified.

Quality eligibility data also enables greater transparency, accountability, and effective government operations, including the potential use of artificial intelligence to analyze large datasets, identify risks and anomalies, and support more efficient oversight. The use of eligibility information to prevent improper federal awards and payments and the role of USAspending.gov in detecting potentially improper awards are vital to safeguarding taxpayer dollars.

The Payment Integrity Information Act of 2019 (PIIA) requires executive agencies to take specific actions to identify and reduce improper payments.[1] This includes mandatory use of the Do Not Pay working system (DNP) to ensure that they make awards and payments only to eligible recipients.[2] DNP includes information from certain databases, such as those that track debarred, suspended, or excluded parties, that executive agencies may use to help prevent ineligible entities from receiving federal awards or funds.

The use of eligibility data is fundamental to maintaining the integrity of the federal procurement and grants processes. In our prior work evaluating agencies’ use of DNP, we emphasized the need for better integration of eligibility checks into award decision-making processes.[3] When agencies do not effectively use eligibility data, it increases the risk of improper federal awards and payments, undermining PIIA’s goals. This highlights the urgent need for agencies to prioritize the quality, accuracy, and accessibility of eligibility data, ensuring that they consistently apply the data to verify recipients’ eligibility before they award and pay funds.

USAspending.gov—the government’s official public source for federal spending information, including federal awards, recipients, obligations, and outlays—plays a critical role in providing transparent, accessible information on federal spending. Making this information publicly available helps enhance oversight, enabling federal agencies, including their Offices of Inspector General (OIG), and the public to detect potentially improper awards and payments.

Accurate and compatible eligibility data—data that are standardized and aligned across systems to enable consistent comparison and use—help agencies support these award decisions, perform automated and systemic eligibility checks, and capture relevant spending information. As such, ensuring that agencies can effectively match eligibility data and award spending information, to validate that only eligible entities receive federal funds, is crucial to improving the success of efforts aimed at detecting and preventing improper payments.

This report is part of a series of reports in response to your request for us to study how the government can better leverage USAspending.gov and other data sources to enhance monitoring of federal spending and to help identify and prevent fraud, waste, and abuse.[4] This report (1) describes the federal data sources that agencies may use to verify entities’ eligibility to receive federal awards, (2) determines the extent to which data in the selected federal eligibility data sources are interoperable, and (3) determines the extent to which eligibility data can be matched with post-award data from USAspending.gov to help agencies identify potentially ineligible recipients of federal awards.

For objective one, we reviewed laws, regulations, Office of Management and Budget (OMB) guidance, and relevant federal agencies’ websites and documentation to identify federal data sources agencies may use to determine recipients’ eligibility for federal awards. We obtained an understanding of the Department of the Treasury’s DNP by reviewing related web pages, documentation, and information on integrated data sources and federal agency participation, and by interviewing agency officials. We also interviewed OMB staff and officials from federal agencies that own and manage eligibility data sources or administer DNP, such as the General Service Administration (GSA), the Department of Health and Human Services’ (HHS) OIG, and Treasury, to identify and better understand federal data sources available to agencies.

To address objective two, we judgmentally selected nine data sources to assess data interoperability. We selected eligibility data sources that were publicly available, in DNP or designated for inclusion in DNP, and included information about entities. We also considered whether the data sources contained information to support eligibility determinations. We selected (1) GSA’s Federal Audit Clearinghouse (FAC) Single Audit Reports, (2) GSA’s System for Award Management (SAM) Entity Registrations, (3) GSA’s SAM Exclusions, (4) HHS OIG’s List of Excluded Individuals and Entities (LEIE), (5) the Internal Revenue Service’s (IRS) Automatic Revocation of Exemption List, (6) IRS’s Form 990-N list, (7) IRS’s Publication 78 list, (8) the Office of Foreign Assets Control’s (OFAC) Specially Designated Nationals and Blocked Persons (SDN) List, and (9) OFAC’s Non-SDN Lists.[5]

For the selected data sources, we reviewed data dictionaries and documentation of validation processes for consistency with OMB guidance and other interoperability practices we identified. These practices included the U.S. Geological Survey’s guidance on data dictionaries and metadata and Treasury’s Governmentwide Spending Data Model documentation and validation rules. We interviewed agency officials responsible for the selected sources to understand how they collected, validated, maintained, and monitored their data. In addition, we performed electronic testing of data for fiscal years 2023 and 2024 (the latest available at the time of our analyses) for apparent errors in accuracy and completeness, such as duplicate records, missing or invalid values, data formatting, and conflicting data relationships. To determine consistency across data sources, we performed electronic comparison procedures, where applicable, using exact matching.

For objective three, we narrowed our selection to the data sources that Treasury’s DNP categorized as debarment data sources and had the unique entity identifier (UEI) data element, which USAspending.gov uses.[6] We selected GSA’s SAM entity information and SAM Exclusions. We matched selected data from these data sources with relevant USAspending.gov award data for fiscal years 2023 and 2024 based on the UEI to identify awards to potentially ineligible recipients. To the extent possible, we also quantified the number and obligation amounts of awards that matched. As discussed later in the report, data limitations prevented us from analyzing the full data set to identify awards to potentially ineligible recipients using UEIs.

Because we made a nongeneralizable selection of data sources, our findings for objectives two and three cannot be used to make inferences about other data sources nor the full population of awards. However, we determined that the selection of these data sources was appropriate for our design and objectives, and that the selection would generate valid and reliable evidence to support our work. We provide additional details regarding our objectives, scope, and methodology in appendix I.

We conducted this performance audit from March 2024 to June 2026 in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

Background

Legal Framework and Guidance for Federal Award Eligibility and Payment Integrity

The Federal Funding Accountability and Transparency Act of 2006 (FFATA) requires federal awards of more than $25,000 and subawards of more than $30,000 to be displayed on a publicly accessible and searchable website, which is USAspending.gov.[7] Federal awards displayed on the website include the following:

· Contracts. Agreements between the federal government and a prime recipient to provide goods and services for a fee, such as purchasing equipment or supplies. They include contracts, subcontracts, purchase orders, task orders, and delivery orders.

· Financial assistance. Federal program, service, or activity that directly aids organizations; individuals; or state, local, or tribal governments, such as funding for a lower-income housing program. It includes grants, subgrants, loans, cooperative agreements, and insurance.

For purposes of this report, we refer to both contracts and federal financial assistance collectively as “federal awards.” A variety of laws, regulations, and guidance establish a framework for ensuring the integrity of award-related funds, with specific legal requirements varying based on the type of agreement used.

The Federal Acquisition Regulation (FAR), which codifies uniform policies for executive agencies to acquire supplies and services, governs most contracts. The FAR, together with individual agencies’ regulations implementing or supplementing it, provides rules for contractors’ qualifications, monitoring, and oversight. For example, prospective contractors must meet standards of responsibility in areas such as financial resources and past performance.[8] It also requires agencies and contractors to check SAM Exclusions to prevent awarding contracts and subcontracts to contractors with active exclusion records, such as contractors that have been debarred or suspended.[9]

OMB has issued Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (Uniform Guidance), reprinted in 2 C.F.R. part 200, which provides government-wide policy for executive agencies and nonfederal entities carrying out federal financial assistance programs. Among other things, it requires agencies and entities to review eligibility and to monitor activities and reports to ensure compliance.[10] OMB also provides guidance in part 170 of 2 C.F.R. to agencies on reporting awards and establishes requirements for recipients’ reporting on subawards to SAM.gov, which is then published on USAspending.gov.

PIIA requires agencies to manage improper payments by identifying risks, taking corrective actions, and estimating and reporting on improper payments in programs they administer.[11] As discussed, PIIA mandates that agencies use, at a minimum, DNP to ensure that they make awards and payments only to eligible recipients.

Treasury has a central role in managing payments for the federal government, with broad authority to disburse funds on behalf of other agencies and to maintain the financial reporting and accounting system of the federal government.[12] A 2025 executive order entitled Protecting America’s Bank Account Against Fraud, Waste, and Abuse instructed agencies to make greater use of Treasury’s centralized disbursement system.[13] It also enhanced the requirement for agencies to use DNP as part of a precertification and pre-award process. Further, the executive order directed Treasury to minimize administrative barriers to accessing and using data to prevent fraud and improper payments, such as by using existing authority to waive requirements for computer matching agreements.[14]

Do Not Pay and Federal Efforts

The Do Not Pay initiative, which PIIA statutorily authorized, provides centralized access to certain databases to verify a recipient’s payment or award eligibility before issuance.[15] DNP, which Treasury operates and OMB oversees, provides data matching, data-analytics services, and support to executive agencies in their efforts to prevent and detect improper payments. State agencies that administer federal programs may also use DNP, which is free for all authorized users.

DNP Products and Services

Treasury’s Office of Financial Integrity manages DNP and offers a variety of services and solutions, such as account and entity verification and data analytics. It provides the following services.

· Do Not Pay Connect. Allows users to connect through a secure application programming interface for real-time, system-to-system eligibility screening by conducting single or batch queries. It also provides users with risk and confidence levels for identifying and making eligibility determinations.

· Do Not Pay Web Portal. Provides users on-demand access through a web-based portal to conduct single eligibility searches and review batch matching results and continuous monitoring alerts. This option can also generate and export detailed reports.

· Treasury Payment Verification. Automatically screens federal agencies’ disbursements against authoritative data to confirm identity and eligibility, helping flag ineligible payments and reduce improper payments. While this provides a critical safeguard, agencies must still conduct prepayment eligibility checks through DNP Connect and Web Portal. This service is only available to federal agencies that use Treasury for payment disbursement.

Participating states can also securely access DNP through program integrity hubs, such as the HHS’s Administration for Children & Families’ Public Assistance Reporting Information System and the Department of Labor’s Unemployment Insurance Integrity Center Integrity Data Hub. These hubs can be used, as applicable, to detect and prevent duplicate public assistance benefits, verify eligibility, identify deceased payees, confirm bank account ownership, and prevent unemployment insurance fraud, among other things.

Data Sources Used by DNP

PIIA requires that, at a minimum, agencies must review the following six databases via DNP before issuing payments and awards: (1) the Social Security Administration’s (SSA) Death Master File; (2) GSA’s SAM Exclusions; (3) Treasury Debt Check; (4) the Department of Housing and Urban Development’s Credit Alert System, also known as the Credit Alert Interactive Voice Response System; (5) HHS OIG’s LEIE; and (6) SSA’s incarcerated individuals list.[16]

As of September 2025, OMB had designated 22 additional databases for inclusion in DNP. Treasury evaluates and integrates the databases into DNP based on multiple factors, including technical feasibility; whether a database addresses a relevant root cause of improper payments; data quality and reliability; the program’s authorities; and data compatibility with the tool’s matching capabilities, such as presence of a unique identifier—for example, employer identification number (EIN) or UEI—of a potential recipient. In June 2025, OMB delegated the authority to designate data sources for inclusion in DNP to Treasury. Many of the data sources included, or designated for inclusion, in DNP were originally created to comply with legal requirements or manage specific federal programs. OMB and Treasury have since repurposed them to support more widespread payment and eligibility determinations.

The nine DNP data sources we selected for analysis, from the broader set of 28 data sources, and a brief description of each are listed in table 1.

|

Owner Data source |

Description |

|

General Services Administration |

|

|

Federal Audit Clearinghouse (FAC) |

Contains single audit reports and indicates whether a significant deficiency or material weakness was found and addressed. The Single Audit Act and related guidance require certain nonfederal entities to undergo a single audit or, in select cases, a program-specific audit. This audit evaluates an entity’s financial statements and compliance with federal awards, and entities must submit the results to FAC. |

|

System for Award Management (SAM) Entity Registrations |

Contains publicly available entity registration data for those entities that are registered in SAM to conduct business with the federal government in accordance with the Federal Acquisition Regulation and 2 C.F.R. Part 200 (2026). |

|

SAM Exclusions |

Identifies parties excluded from receiving federal benefits and awards such as contracts and federal financial assistance. |

|

Department of Health and Human Services - Office of Inspector General |

|

|

List of Excluded Individuals and Entities |

Contains current information about individuals and entities excluded from participation in Medicare, Medicaid, and all other federal health care programs. |

|

Department of the Treasury - Internal Revenue Service (IRS) |

|

|

Automatic Revocation of Exemption List |

Contains information about nonprofit entities whose tax-exempt status was automatically revoked because they did not file Form 990 for 3 consecutive years. Tax-exempt organizations must file an annual information return or notice with the IRS, unless an exception applies. Annual information returns include Form 990, Form 990-EZ, and Form 990-PF. |

|

Form 990-N list |

Contains Form 990-N data. Form 990-N is an annual electronic notice that most small tax-exempt organizations (i.e., organizations with annual gross receipts normally $50,000 or less) are eligible to file instead of Form 990 or Form 990-EZ. |

|

Publication 78 list |

Lists organizations that are eligible to receive tax-deductible charitable contributions. |

|

Treasury - Office of Foreign Assets Control (OFAC) |

|

|

Specially Designated Nationals and Blocked Persons (SDN) List |

Contains a list of individuals, groups, and entities owned or controlled by, or acting for or on behalf of, sanctioned countries. It also lists individuals, groups, and entities, such as terrorists and narcotics traffickers, designated under programs that are not country specific. Such persons’ assets are blocked, and U.S. persons are generally prohibited from transacting or dealing with them. |

|

Non-SDN Consolidated Sanctions List |

Includes parties subject to specific, limited prohibitions, rather than full blocking. It consolidates individuals, groups, and entities from various OFAC lists, such as the Sectoral Sanctions Identifications, Foreign Sanctions Evaders, and others with targeted restrictions. |

Source: GAO analysis of agency information. | GAO‑26‑107466

Note: While OFAC’s Non-SDN Consolidated List has not specifically been designated for inclusion in DNP, it is included in the SAM Exclusions, which were designated and are part of DNP. Therefore, we included it in our selection of data sources.

Users of DNP

As of July 2025, more than 60 federal government agencies use DNP. According to Treasury, DNP has demonstrated its ability to prevent improper payments. For example, Treasury officials told us that in fiscal year 2025, DNP yielded almost $5 billion in prevention and recovery of improper payments and fraud (compared to more than $2 billion in fiscal year 2024). In addition, officials said that almost $7 billion was identified in fiscal year 2025 using other tools to detect check fraud and conduct additional screenings (compared to more than $5 billion in fiscal year 2024).

OIGs’ and Our Work on Award Processes, Payment Integrity, and Use of Federal Data

Agency OIGs and we have frequently examined federal award processes; payment integrity; and agencies’ use of data-matching tools, such as DNP. We have also reported on opportunities to leverage existing tools, such as USAspending.gov, to identify potential fraud, waste, and abuse and to inform enforcement of recipient compliance. These reports have highlighted the importance of standardized data and effective internal controls to minimize fraud, waste, and abuse.[17]

For example, we have previously reported on agencies’ implementation of PIIA, including requirements and challenges with managing and reducing improper payments.[18] We have also reported on challenges agencies face regarding data matching due to a lack of government-wide data standards, adherence to existing standards, or system interoperability.[19] We and the OIGs have also reported on improving the quality of data available through USAspending.gov.[20]

While USAspending.gov can be helpful in identifying potential improper payments and fraud, its current data quality issues limit its usefulness. Our work has shown that clarifying data standards, enhancing agency practices, and reinstating OIG oversight could significantly help improve the website’s effectiveness and usefulness.[21] Our and the OIGs’ work has also emphasized that stopping improper payments before they happen through preventive controls, such as DNP, is more efficient than recovering them later (“pay and chase”).[22]

Agencies May Use Many Federal Data Sources to Verify Entities’ Eligibility Throughout the Award Life Cycle

What federal data sources may agencies use?

Agencies may use more than 100 federal data sources, including the 28 data sources in DNP or designated for inclusion in DNP, to help determine if entities, as well as individuals, qualify to receive federal awards and payments. Some of these sources include information on identity verification, financial delinquency, criminal records, and prior audit findings.[23] Agencies may use a combination of data sources to verify eligibility of recipients.[24] However, many of the data sources we identified were created to comply with legal requirements or manage specific federal programs. These data sources were not originally created to support eligibility determinations for other agencies.

Examples include the following:

· SSA maintains data on identity, disability, U.S. citizenship, incarceration, and death to administer its own programs. Other agencies may also use these data to verify identity or eligibility for other federal programs (e.g., the Department of Housing and Urban Development uses SSA information to help verify applicant identity or eligibility for subsidized housing programs).

· The Department of Veterans Affairs maintains data on veterans’ health, education, and compensation benefits to manage and deliver personalized benefits and services to veterans. Other agencies may also use this information when veteran status affects program eligibility (e.g., the Small Business Administration uses veterans’ information to help verify eligibility for contracting opportunities).

· IRS publishes the tax-exempt organizations lists to make available the status of such organizations.[25] Other agencies may also use these data to verify eligibility to receive federal funding (e.g., the National Institutes of Health use IRS tax-exempt status information to monitor whether tax-exempt hospitals meet federal requirements).

How may agencies access federal data sources?

Agencies may access relevant data through public websites, by direct access to source systems, and through centralized access. For example:

· Public website. Agencies may obtain sanctions-related data from OFAC’s website. Agencies may also obtain the list of individuals and entities that are excluded from participation in federal health care programs, such as Medicare, from the HHS OIG’s website.

· Direct access. Agencies may verify Social Security numbers directly from the SSA State Verification and Exchange System. Agencies may also verify institutions, day care home providers, and individuals that have been terminated or otherwise disqualified from Child and Adult Care Food Program participation through the Department of Agriculture’s National Disqualified List.

· Centralized access. Agencies may use the Federal Data Services Hub, which the Centers for Medicare & Medicaid Services primarily maintains. It is a single point of access to a variety of federal data sources, including those from SSA, the Department of Homeland Security, and IRS, to verify income, citizenship, and other eligibility factors. Similarly, the DNP Connect and Web Portal provides access to multiple federal databases, including those from IRS, OFAC, and GSA.

Depending on the type and nature of the data, statutory authorities, and privacy and security protections involved, access to certain federal data sources may be limited or require a memorandum of understanding or computer matching agreement that dictates how agencies may use, share, and protect the data.[26] For sensitive or restricted data, such as Social Security numbers or financial records, agencies must meet additional legal and technical requirements and may only access the data through secure federal systems that require proper authentication.

Laws such as the Privacy Act of 1974 and the Computer Matching and Privacy Protection Act of 1988 govern how agencies may access and use personal data.[27] These laws require agencies to establish safeguards, document formal agreements, and ensure that they use data only for authorized purposes. Congress established these protections to balance efficiency and the government’s need to verify eligibility by protecting the public’s trust and reducing misuse of personal information.

How do federal data sources help agencies verify eligibility?

Agencies may use federal data sources to improve program efficiency and verify if entities, as well as individuals, meet the eligibility criteria for federal programs throughout the award life cycle, including pre-award screening, post-award monitoring, and payment validation. These data sources support more informed decision-making, help reduce the risk of improper awards and payments, identify potential fraud, and ensure compliance with legal and policy requirements.[28]

For example, agency officials, including auditors, may use these data sources throughout the award life cycle to

· verify identity or status, such as confirming that an individual is not deceased or that a business is properly registered in SAM;

· check for suspensions, debarments, or other prohibitions that would disqualify an applicant from receiving federal funds, such as contracts or payments from federal programs;[29]

· confirm compliance and assess eligibility by identifying disqualifying conditions or risks based on past performance or financial history by considering factors such as prior audit findings, failure to meet reporting requirements, or delinquent debt; and

· identify potential fraud risks, such as duplicate or conflicting information and other inconsistencies or irregularities, that may indicate potentially fraudulent activity.

Our prior work has shown that these data sources can help corroborate self-reported information from applicants and enable more accurate and efficient eligibility determinations.[30] Having access to timely, standardized federal information also helps reduce the administrative burden on agencies and improve coordination, among other things.

Data Interoperability Weaknesses May Hinder Agencies’ Ability to Efficiently Determine Award and Payment Eligibility

What is data interoperability, and why does it matter to the federal government?

Data interoperability refers to the ability to share and disseminate standardized data in a way that is efficient, consistent, and accessible across different systems and users, for which high-quality data are essential.[31] OMB guidance directs agencies to promote open, interoperable data by building or modernizing information systems using machine-readable formats, data standards, and consistent metadata to support downstream data processing. Agencies are also required to ensure that the information is reliable by implementing rigorous pre-dissemination practices that evaluate accuracy and coherence.[32]

This approach to data interoperability is critical to support federal government efforts emphasizing the use of existing data. It requires high-quality program data to accurately evaluate the effectiveness of government programs and policies. To increase the integrity of analyses based on such data, the National Academies of Sciences, Engineering, and Medicine recommend a comprehensive quality framework that includes evaluating and documenting data interoperability concerns, including timeliness, accuracy, accessibility, coherence, interpretability, and granularity.[33] Because data interoperability depends on quality and consistency, maintaining strong data standards is essential. This includes ensuring that formats are standardized, data validation checks are effective, and agencies address inaccuracy issues, such as missing or invalid values, and duplicates.

Data interoperability allows federal data systems to exchange information and collaborate seamlessly, enabling more timely, informed, and evidence-based decision-making and increasing the efficiency and effectiveness of federal operations. In contrast, poor data quality or inconsistent data structures break down interoperability, preventing accurate or efficient record matching and data integration, which undermines the usefulness of the data. Consequently, relying on poorly matched or poorly integrated data limits agencies’ ability to inform decision-making and to implement efficient and reliable processes, including the potential use of artificial intelligence to assist users in making eligibility determinations.

Within the context of eligibility determinations, the lack of data interoperability across systems may limit agencies’ ability to efficiently and reliably determine whether a recipient is identified as ineligible in the relevant data sources. For the same reasons, officials might also be unable to determine whether previous payments were improperly made to ineligible recipients, thereby increasing the risks of improper awards or payments going undetected.

What are the requirements for federal data interoperability?

For more than 30 years, several laws and OMB and Treasury guidance have established general requirements related to data interoperability and standardization, but they have not established specific requirements for enforcing data interoperability, such as for recipient eligibility data, throughout the federal government.

Legal Requirements Related to Data Interoperability

We identified 12 laws and one executive order that promote federal data interoperability. For example, the Digital Accountability and Transparency Act of 2014 (DATA Act) and the Grant Reporting Efficiency and Agreements Transparency Act of 2019 (GREAT Act) include requirements to establish data standards and definitions for spending and grant data, respectively. In contrast, laws such as the Paperwork Reduction Act of 1995, E-Government Act of 2002, and the Foundations for Evidence-Based Policymaking Act of 2018 promote key principles, such as data standardization, sharing, reuse, and transparency. These are important aspects of data interoperability, but they do not address the establishment of government-wide data governance to establish specific requirements and help enforce interoperable data across the federal government. We summarize relevant laws and one executive order related to data interoperability in table 2.

Table 2: Laws and an Executive Order with Requirements Relevant to Data Interoperability for Federal Agencies

|

Law or executive order |

Requirements relevant to data interoperability |

|

Federal Managers’ Financial Integrity Act of 1982, Pub. L. No. 97-255, 96 Stat. 814, codified at 31 U.S.C. § 3512(c), (d) |

Requires executive branch entities to establish systems of internal control in accordance with Comptroller General standards to ensure accurate accounting, safeguarding of assets, and reliable financial reporting. |

|

Paperwork Reduction Act of 1995, Pub. L. No. 104-13, 109 Stat. 163, codified as amended at 44 U.S.C. § 3501 et seq. |

Assigns the Office of Management and Budget (OMB) responsibility for federal information dissemination and mandates the development of common standards for federal information, including interoperability. Directs OMB to develop and oversee the implementation of uniform information resources management policies, principles, standards, and guidelines. |

|

Information Technology Management Reform Act of 1996 (also known as the Clinger-Cohen Act of 1996), Pub. L. No. 104-106, div. E, 110 Stat. 186, 679, codified at 40 U.S.C. § 11101 et seq. |

Establishes agency chief information officers and tasks them with developing and implementing integrated IT architectures. |

|

Federal Financial Management Improvement Act of 1996, Pub. L. No. 104‑208, title VIII, §§ 801 et seq., 110 Stat. 3001, 300-389-394, codified at 31 U.S.C. § 3512 note |

Requires Chief Financial Officers Act of 1990 (CFO Act) agencies—24 major executive departments and large independent agencies—to implement and maintain financial management systems that comply with federal requirements, applicable accounting standards, and the U.S. Standard General Ledger at the transaction level. It promotes consistency in agency accounting practices across fiscal years and the use of uniform accounting standards. |

|

Information Quality Act of 2000, Pub. L. No. 106-554, app. C, title V, § 515, 114 Stat. 2763, 2763A-153-155 |

Requires OMB to issue guidance to federal agencies for ensuring and maximizing the quality, objectivity, utility, and integrity of disseminated information. |

|

E-Government Act of 2002, Pub. L. No. 107-347, 116 Stat. 2899, codified at 44 U.S.C. § 3601 et seq. |

Establishes the Chief Information Officer Council and the Interagency Committee on Government Information to promote government information interoperability and IT standards. |

|

Federal Funding Accountability and Transparency Act of 2006 (FFATA), Pub. L. No. 109-282, 120 Stat. 1186, codified at 31 U.S.C. § 6101 note |

Establishes USAspending.gov and requires federal agencies to report information on federal awards to entities over $25,000, including unique identifiers for the award recipient and, if applicable, the parent entity (the organization that owns another entity). |

|

Digital Accountability and Transparency Act of 2014, Pub. L. No. 113-101, 128 Stat. 1146, codified at 31 U.S.C. § 6101 notea |

Expands FFATA and requires the Department of the Treasury and OMB to establish government-wide financial data standards for federal funds, including the use of common data elements and unique identifiers, to submit data on USAspending.gov. It also aimed to hold federal agencies accountable for the completeness, timeliness, quality, and accuracy of the data they submitted through reviews by their Offices of Inspector General and GAO, but that requirement sunset in 2021. |

|

21st Century Integrated Digital Experience Act, Pub. L. No. 115-336, 132 Stat. 5025, codified at 44 U.S.C. § 3501 note |

Requires agencies to standardize and modernize public-facing websites and digital services by avoiding duplicative legacy sites, ensuring searchable content, and maintaining common standards that support future shared service interoperability. |

|

Foundations for Evidence-Based Policymaking Act, Pub. L. No. 115-435, title II, 132 Stat. 5529, 5534-5544, codified in scattered sections of 44 U.S.C. ch. 35, subch. I (2019) |

Establishes a Chief Data Officer Council within OMB required to set government-wide best practices for the use, protection, dissemination, and generation of data. While the council’s statutory authorization expired on December 15, 2024, the act continues to mandate that agencies develop and maintain comprehensive data inventories, among other requirements. |

|

Grant Reporting Efficiency and Agreements Transparency Act of 2019, Pub. L. No. 116-103, 133 Stat. 3266, codified at 31 U.S.C. § 6401 et seq. |

Requires OMB and a standard-setting agency to establish government-wide data standards for information that recipients of federal grants and other financial assistance report, including standardized definitions for data elements and unique identifiers. |

|

Payment Integrity Information Act of 2019, Pub. L. No. 116-117, 134 Stat. 113, codified at 31 U.S.C. § 3351-3358 (2020) |

Encourages executive agencies to enter into computer matching agreements with other executive agencies to allow ongoing data matching (e.g., automated data matching) to detect and prevent improper payments. |

|

Protecting America’s Bank Account Against Fraud, Waste, and Abuse, Exec. Order No. 14249, 90 Fed. Reg. 14,011, (Mar. 28, 2025) |

Directs Treasury and OMB to strengthen fraud prevention and improper payment verification by expanding data access, enabling precertification checks for all Treasury-disbursed payments, and guiding agencies on data sharing for payment verification. It also requires CFO Act agencies to consolidate, standardize, and integrate their core financial systems with Treasury platforms. |

Source: GAO analysis of the laws and executive order. | GAO‑26‑107466

aIn March 2022, we recommended that Congress consider extending requirements for the Offices of Inspector General to periodically report on USAspending.gov data, among other things. As of February 2026, Congress had not enacted legislation to address these matters. See GAO‑22‑105715.

Data Interoperability Provisions from Guidance

We identified several guidance documents for agencies that relate to federal data interoperability. For example, Treasury and OMB guidance for USAspending.gov reporting outline specific standards, definitions, and requirements for data submitted under the DATA Act. In contrast, other OMB guidance about federal data broadly requires agencies to leverage data standards to promote alignment, comparability, and reuse of data but does not provide specific data standards, definitions, or requirements. We summarize relevant guidance in table 3.

|

Guidance |

Relevant data interoperability guidance |

|

Office of Management and Budget (OMB) M-15-12, Increasing Transparency of Federal Spending by Making Federal Spending Data Accessible, Searchable, and Reliable (May 8, 2015) |

Provides guidance to federal agencies on reporting requirements under the Federal Financial Accountability and Transparency Act of 2006 (FFATA), as amended by the Digital Accountability and Transparency Act of 2014 (DATA Act). It directs the use of standardized data definitions published in a virtual repository and requires Treasury to publish spending data on USAspending.gov. |

|

OMB Circular A-130, Managing Information as a Strategic Resource (July 27, 2016) |

Establishes government-wide policy for managing federal information and IT resources, directing agencies to use open data standards, application programming interfaces (API), and machine-readable formats to support interoperability. It also requires agencies to implement policies, procedures, and standards that enable data governance. |

|

OMB M-19-15, Improving Implementation of the Information Quality Act (Apr. 24, 2019) |

Provides agencies with additional guidelines for their responsibilities under the Information Quality Act, including requirements for pre-dissemination quality reviews and updates to agency information quality assurance procedures. It also reinforces that agencies are required to create information that supports public transparency and enables third-party use, ensuring that data are accessible and usable. Additionally, it emphasizes that agencies must provide potential users with sufficient information about data quality, strengths, weaknesses, and analytical limitations when disseminating it publicly. |

|

OMB M-19-18, Federal Data Strategy – A Framework for Consistency (June 4, 2019) |

Establishes the Federal Data Strategy as a government-wide framework to guide federal agencies in managing and using data as a strategic asset, requiring agencies to prioritize data governance and leverage data standards to maximize data quality and facilitate access, sharing, and interoperability. |

|

OMB M-19-23, Phase 1 Implementation of the Foundations for Evidence-Based Policymaking Act of 2018 (July 10, 2019) |

Provides implementation guidance of the Foundations for Evidence-Based Policymaking Act, Pub. L. No. 115-435, title II, 132 Stat. 5529, 5534-5544, codified in scattered sections of 44 U.S.C. ch. 35, subch. I (2019), in support of statutory establishment of agency data governance roles and responsibilities for key personnel, including the newly designated Chief Data Officer (CDO) position. It also directs the CDO Council to develop government-wide best practices, promote data sharing agreements, and identify ways to improve the collection, access, and use of data. |

|

OMB M-20-12, Phase 4 Implementation of the Foundations for Evidence-Based Policymaking Act of 2018: Program Evaluation Standards and Practices (Mar. 10, 2020) |

Requires agencies to support the secondary use and dissemination of information. Notes that one effective approach is to enable reuse of evaluation data by providing clear data dictionaries or other documentation describing data sources, defining data elements, and outlining any limitations in completeness or accuracy of the data. |

|

OMB M-21-19, Transmittal of Appendix C to OMB Circular A-123, Payment Integrity Improvement (Mar. 5, 2021) |

Provides a payment integrity framework to guide agencies authorized to enter into ongoing computer matching agreements to detect and prevent improper payments. |

|

OMB M-21-27, Evidence-Based Policymaking: Learning Agendas and Annual Evaluation Plans (June 30, 2021) |

Reaffirms and expands on previous OMB guidance on learning agendas and annual evaluation plans, including OMB M-19-23 and OMB M-20-12. It provides additional guidance for implementing the Foundations for Evidence-Based Policymaking Act to support data-sharing efforts as part of evidence-based government. |

|

OMB M-23-22, Delivering a Digital-First Public Experience (Sept. 22, 2023) |

Directs agencies to deliver digital services using structured, machine-readable content and standardized interfaces, such as web APIs, to enable data exchange and promote interoperability across different systems. |

|

Treasury Governmentwide Spending Data Model, GSDM 1.2 (Dec. 2025) |

Provides government-wide data definition standards and technical guidance for federal agencies on what to report to USAspending.gov. The Department of the Treasury and OMB first released it as the DATA Act Information Model Schema in 2016, and Treasury continually updates it to reflect new legislation and policies. It includes data-reporting submission specifications, such as data elements, character limits and valid values, and validation rules. |

|

OMB M-25-05, Phase 2 Implementation of the Foundations for Evidence-Based Policymaking Act of 2018: Open Government Data Access and Management Guidance (Jan. 15, 2025) |

Requires agencies to develop and maintain a comprehensive data inventory of their data assets that uses the OMB-approved standard metadata schema, is published in open and machine-readable formats, and is interoperable with the Federal Data Catalog that the General Services Administration maintains. |

|

OMB M-25-06, Re-establishing the Chief Data Officer Council (Jan. 15, 2025) |

Reestablishes the CDO Council to establish government-wide best practices for federal data, promote interagency data-sharing agreements, and identify new technology solutions for improving the collection and use of data. |

Source: GAO analysis of guidance. | GAO‑26‑107466

Who is responsible for data interoperability across the federal government?

While several agencies and cross-agency groups support coordination of best practices for data management and interoperability, there is no data governance agency designated to establish and enforce interoperability requirements across the federal government. Based on our research, these agencies and cross-agency groups identify shared needs and challenges, provide technical and policy guidance, and develop frameworks to enable more consistent data use and exchange. We found that none of them issue mandatory directives and some of them have limited technical and operational enforcement capacity. As a result, interoperability efforts—including those related to eligibility data sources—remain fragmented and depend on agencies’ voluntary adoption. Table 4 includes the stakeholders and a summary of their roles and responsibilities that we identified based on our research and interviews with agency officials regarding data interoperability.

Table 4: Stakeholders of Federal Data Interoperability That GAO Identified and Their Management Areas, Roles, and Responsibilities

|

Stakeholder |

Management area |

Roles or responsibilities |

|

Office of Management and Budget (OMB) |

Government-wide data policy |

Encourages agencies to adopt data standardization and interoperability practices through the Federal Data Strategy and implementation guidance for the Foundations for Evidence-Based Policymaking Act. It also co-leads implementation of the Digital Accountability and Transparency Act of 2014 (DATA Act), ensuring transparent, accessible financial data. Further, it collaborates with the Federal Committee on Statistical Methodology—an interagency committee that OMB founded in 1975 comprising career federal employees that OMB selected based on their expertise in statistical methods—to promote consistent statistical standards and methods for federal data collection and use. |

|

Department of the Treasury |

Financial and award data reporting and disbursements |

Co-leads implementation of the DATA Act, requiring agencies to report financial and award data in standardized formats in systems such as USAspending.gov and the Financial Assistance Broker Submission—a system through which federal agencies report detailed financial assistance award data—to enforce data uniformity across agencies. It also manages several government-wide financial data systems, including the Governmentwide Treasury Account Symbol Adjusted Trial Balance and other systems that support the preparation of the consolidated financial statements of the U.S. government. Furthermore, Treasury operates the Do Not Pay working system and various federal payment systems that disburse funds on behalf of agencies. |

|

General Services Administration (GSA) |

Data platforms and technology |

Supports interoperability through modernizing and centralizing data systems through Integrated Award Environment systems, such as SAM.gov, which is part of the federal awards life cycle, and Data.gov, which is a central repository for federal open data. |

|

National Information Exchange Model (NIEM) Opena |

Data sharing framework and data model |

Provides a framework developed through interagency and intergovernmental collaboration to support consistent data exchange and interoperability. It includes a standardized data vocabulary model for use in community-specific business areas, such as emergency management, human services, and forensic data sharing. Agencies may choose to adopt its standards but are not required to do so. |

|

Chief Data Officer Council |

Cross-agency data strategy |

Coordinates data-sharing efforts and promotes best practices for the management, use, protection, dissemination, and generation of data between federal agencies. Established under the Foundations for Evidence-Based Policymaking Act, the council comprises chief data officers from the 24 major executive departments and large independent agencies (i.e., the 24 Chief Financial Officer Act of 1990 (CFO Act) agencies), other designated federal agencies, and officials from OMB. It engages with stakeholders to help improve access to federal data. It also publishes guides, playbooks, and reports, such as recommendations related to data sharing. Further, the council shares responsibilities with other interagency councils that conduct and affect data-related activities, including those focused on IT, statistics, information security, evaluation, and privacy. |

|

Interagency Council on Statistical Policy |

Statistical data integration |

Advises OMB and coordinates statistical methods and systems to support interoperability of survey, census, and administrative data, and to help ensure secure, shared access to data throughout the Federal Statistical Research Data Centers. The council comprises 30 unique members, including the Chief Statistician, designated statistical officials from the 24 CFO Act agencies, as well as all heads of OMB recognized statistical agencies and units. |

|

Shared Services Governance Board |

Cross-functional steering committee |

Coordinates agency inputs, recommends changes to service offerings, and supports government-wide efforts to improve service delivery efficiency. GSA manages it under OMB guidance, and it is part of the governance structure for shared IT and service delivery initiatives, including those that support data interoperability. The board operates in an advisory and coordinating capacity. Its membership includes representation across federal interagency councils, including the Chief Acquisition Officer Council, Performance Improvement Council, and Chief Data Officer Council, among others. |

|

Chief Information Officer Council |

Cross-agency federal information management |

Advises OMB and the Office of Personnel Management and promotes collaboration across the federal government to improve IT practices related to cybersecurity, cloud adoption, using data, and IT workforce development. The council also shares best practices, ideas, experiences, and innovative approaches to enhance government efficiency and effectiveness and delivery of services. It comprises OMB officials and the chief information officers from the 24 CFO Act agencies, among others. |

|

Council on Federal Financial Assistance |

Financial assistance |

Supports coordination of data standards and practices to help improve coordination, transparency, and accountability related to federal financial assistance awards. This interagency forum also promotes consistent application and interpretation of government-wide financial assistance policies, management practices, and business data standards, among other requirements. The Council on Federal Financial Assistance comprises OMB officials, senior financial assistance officers from the 24 CFO Act agencies, and a representative from the Small Agency Council. |

Source: GAO analysis of policies and guidance. | GAO‑26‑107466

Note: This list may not be comprehensive. We listed the agencies and groups and a summary of their roles and responsibilities that we identified based on our research and interviews with regards to eligibility data sources, including Treasury’s Do Not Pay working system.

aWhile the Departments of Justice, Health and Human Services, and Homeland Security originally established NIEM in 2005, it is not a federal agency. It provides a collaborative partnership among governmental agencies, operational practitioners, systems developers, standards bodies, and other stakeholders across federal, state, local, tribal, territorial, international, and private organizations.

What obstacles can affect the interoperability of selected federal data sources?

We identified three obstacles that can affect the interoperability of the nine selected federal data sources: (1) lack of comprehensive data dictionaries, (2) lack of comprehensive or documented data validation rules, and (3) inconsistencies between data sources.[34] Without clear requirements for data standards, agencies have developed datasets that use inconsistent definitions and validation rules, contributing to data quality issues. These weaknesses and inconsistencies in data management reduce the accuracy and completeness of the data and increase the difficulty of sharing and integrating data across systems.

Incomplete Data Dictionaries

Data dictionaries for eight of the nine selected data sources we reviewed were incomplete. As shown in table 5, these eight selected data sources did not include all six of the following key elements that we developed from practices identified in our prior work, as well as data standards, policies, and processes that federal agencies developed or use.[35]

· Name. A word or set of words that the field is called.

· Definition. Description of what data elements represent.

· Character limit. Limit in the number of characters allowed for a field.

· Data type and format. Description of the expected value types, such as text, string, numbers, or a date in a specific order (e.g., MM/DD/YYYY).

· Mandatory or optional field indicator. Clarification of whether a field is required or optional, including conditional circumstances.

· Sensitivity indicator. Identification of data elements that contain sensitive or restricted information.

Table 5: GAO Assessment of Data Element Specifications in Data Dictionaries for the Nine Selected Data Sources

|

Owner Data source |

Name |

Definition |

Character limit |

Data type and format |

Mandatory or optional field indicator |

Sensitivity indicator |

|

General Services Administration |

||||||

|

Federal Audit Clearinghouse |

Yes |

Yes |

No |

Yes |

Yes |

NA |

|

System for Award Management (SAM) Entity Registrations |

Yes |

Yes |

Yes |

Yes |

Yes |

Yes |

|

SAM Exclusions |

Yes |

Yes |

Yes |

No |

No |

NA |

|

Department of Health and Human Services - Office of Inspector General |

||||||

|

List of Excluded Individuals and Entities |

Yes |

Yes |

Yes |

No |

Yes |

No |

|

Department of the Treasury - Internal Revenue Service (IRS) |

||||||

|

Automatic Revocation of Exemption List (ARL)a |

Yes |

Yes |

Yes |

No |

No |

NA |

|

Form 990-N list |

Yes |

Yes |

Yes |

No |

Yes |

NA |

|

Publication 78 lista |

Yes |

Yes |

Yes |

No |

No |

NA |

|

Treasury - Office of Foreign Assets Control (OFAC) |

||||||

|

Specially Designated Nationals and Blocked Persons (SDN) Listb |

Yes |

No |

No |

Yes |

No |

NA |

|

Non-SDN Consolidated Sanctions Listb |

Yes |

No |

No |

Yes |

No |

NA |

Legend: Yes = agency data dictionary documentation included the key element; No = agency data dictionary documentation did not include the key element; NA = Not applicable because all information provided in the related files is public.

Source: GAO analysis of agency documentation. | GAO‑26‑107466

aIRS did not publish and could not provide a data dictionary upon request for the ARL and the Publication 78 list. In March 2025, after our request, IRS published on its website a data dictionary for each of these data sources.

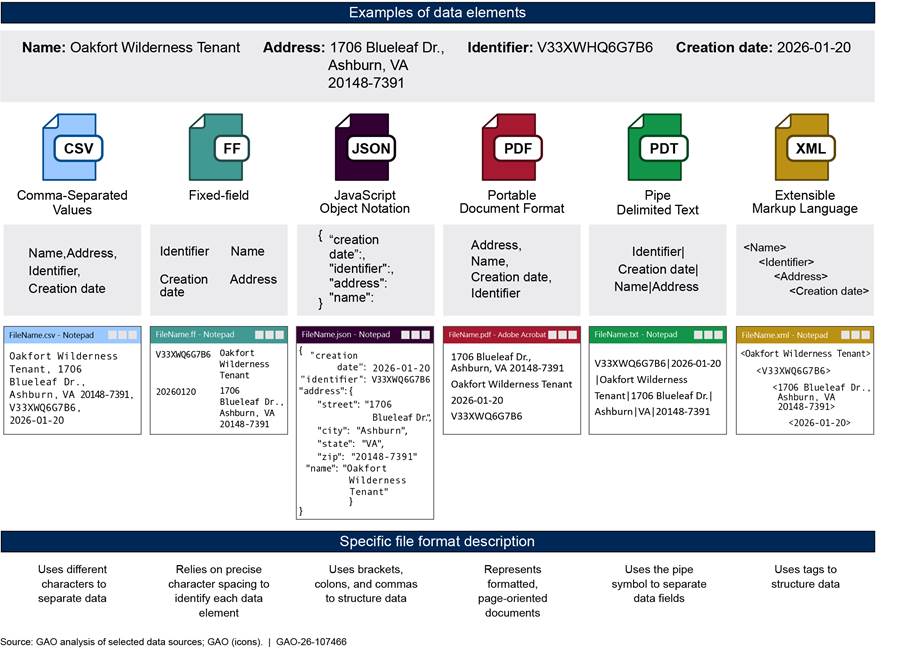

bOFAC has different data dictionaries for different file formats. We evaluated the data dictionary for the Extensible Markup Language (XML) file only. XML is a flexible, nonproprietary set of standards for tagging information so that it can be transmitted using internet protocols and other computer systems can readily interpret it.

We found no specific federal requirements that define what a data dictionary should include, which has led to variation in how agencies manage documentation for their data. As such, the lack of complete and standardized data dictionaries contributed to other interoperability challenges. For example, inconsistent data elements and formats across sources increased the level of effort required to achieve consistency across the data sources in our analyses. These types of interoperability challenges that we encountered could also affect agencies and result in them using inconsistent or incomplete information for decision-making. For example, program staff processing federal payments or awards could have unclear or inconsistent data when making eligibility determinations, which increases the risk of errors and improper payments or awards.

Inconsistent Data Elements

We found that different data sources used different data element field names, numbers of data elements, and orders of data element fields to represent the same information. For example, while Treasury and OMB collaboratively have developed specific standards for some of these elements for certain platforms, such as USAspending.gov, there is no government-wide standard for reporting name and address. Table 6 shows examples of the fields used to represent names in the selected data sources.

|

Data source |

Fields representing “Name” |

|

System for Award Management Entity Registrations |

legal business name dba name |

|

Publication 78 list |

business name |

|

List of Excluded Individuals and Entities |

lastname firstname midname busname |

|

Specially Designated Nationals and Blocked Persons List |

FormattedFirstName FormattedLastName FormattedFullName |

Legend: dba = doing business as

Source: GAO analysis of agency documentation. | GAO‑26‑107466

Our prior work has found that, without clear data elements and definitions, agencies have interpreted and applied the definitions for the same data elements differently. This resulted in the reporting of data that were not comparable as well as difficulties for users in understanding and using those data.[36]

Inconsistent data elements may also lead to additional efforts, such as extra time and resources needed to combine and compare data across different data sources, and increase the risk that management may misinterpret information when making decisions.

Inconsistent Data Formats

We also encountered formatting differences, such as different character limits, and names appearing in all capital letters in one source and mixed case in another source. For example, LEIE limited name fields to a fewer number of characters than did SAM Exclusions, resulting in a middle name being truncated. This difference caused a record to appear as a mismatch between the two sources, even though it referred to the same individual.

We also found that different data sources reported address and country information in a variety of formats. For example, entries for country information in the different data sources included United States, USA, and US. These variations could reflect the use of different standards or formatting options available (e.g., Geopolitical Entities, Names, and Codes and International Organization for Standardization). Without clear documentation that specifies the required standard and formatting, determining the reason for the mismatches can be time consuming and require additional efforts to reconcile and integrate data. It may also result in the inability to compare data elements that represent the same information across data sources.

|

Types of unique identification numbers used in the selected federal data sources Unique entity identifier is an identification number that SAM.gov assigns to entities doing business with the federal government. The General Services Administration has required it since April 4, 2022, when it replaced the Dun & Bradstreet number. Employer identification number is an identification number that the Internal Revenue Service issues to administer federal tax laws for businesses, tax-exempt organizations, and other entities. National Provider Identifier is a unique identifier that the Centers for Medicare & Medicaid Services issues to covered health care providers for use in Health Insurance Portability and Accountability Act administrative and financial transactions. Source: GAO analysis of agency information. | GAO‑26‑107466 |

Lack of Common Unique Identifiers

There was no common unique identifier across all the selected data sources, as shown in table 7. Not all entities included in the data sources we reviewed conduct business with the federal government, such as foreign entities, or are required to have a UEI. The EIN was available in certain formats, such as restricted or sensitive files or on the data source owners’ websites when known in advance.

|

|

Common unique identifiers |

||

|

Owner Data source |

Unique entity identifier (UEI) |

Employer identifier number (EIN) |

National Provider Identifier |

|

General Services Administration |

|

|

|

|

Federal Audit Clearinghouse |

✓ |

✓ |

|

|

System for Award Management (SAM) Entity Registrations |

✓ |

✓a |

✓ |

|

SAM Exclusions |

✓ |

✓b |

✓ |

|

Department of Health and Human Services - Office of Inspector General |

|||

|

List of Excluded Individuals and Entities |

|

✓c |

✓ |

|

Department of the Treasury - Internal Revenue Service |

|||

|

Automatic Revocation of Exemption List |

|

✓ |

|

|

Form 990-N list |

|

✓ |

|

|

Publication 78 list |

|

✓ |

|

|

Treasury - Office of Foreign Assets Control |

|

|

|

|

Specially Designated Nationals and Blocked Persons (SDN) List |

|

|

|

|

Non-SDN Consolidated Sanctions List |

|

|

|

Legend: ✓ = Unique identifier is present in the data source for at least some records.

Source: GAO analysis of agency data. | GAO‑26‑107466

Note: The availability of common unique identifiers may vary within each data source, and the unique identifier may not be present for all records.

aThe EIN is only available in the sensitive file.

bThe EIN is not available in the public data files but may be searched in SAM.gov if known in advance.

cThe EIN for entities (and Social Security number for individuals) is available in the restricted file, not the public file, and may be used to verify the provider in the online tool after a name match, if known in advance.

We aimed to work exclusively with publicly accessible data, which reflect the type of information agency officials would have, at a minimum, available for their decision-making. Without accessible and reliable common unique identifiers in our analyses, we sometimes relied on individual and entity names or other fields, such as country, to match records between data sources. These fields varied in name, formatting, and number of fields, further complicating exact matching. We used exact matching techniques to replicate what a human might do and to avoid making incorrect matches. We did not use “fuzzy matching”—a collection of techniques that calculate how similar the values are. Fuzzy matching without human judgment to confirm a match can reduce the accuracy and reliability of the analysis if it incorrectly identifies matches or misses true matches. For instance, it can incorrectly identify matches, such as “Global Tech Industries Inc” in one data source matching with “Global Technologies Inc” in another data source. While using common unique identifiers across databases could improve the accuracy and efficiency of data matching, we have previously reported that it may also pose challenges, such as those related to implementation and cost as well as potential security and privacy risks if identifiers were compromised.[37]

Comprehensive and required use of data dictionaries for each selected data source could have helped to mitigate these challenges by clearly documenting the structure, definitions, and formatting requirements for each data element. This information would have supported our efforts to identify and reconcile inconsistencies across sources, such as the varying data formats and field names and the lack of unique identifiers, thereby improving the reliability and efficiency of data comparisons.

Insufficient Validation Rules Contribute to Data Quality Issues

Of the nine data sources we reviewed, eight had data validation rules—quality checks that help ensure that data are valid, reliable, and accurate enough for their intended use—that were insufficient or not properly documented for the time frame we selected. In addition, the remaining data source lacked formal validation rules. For example, GSA officials stated that validation checks were built directly into SAM. However, they could not readily provide documentation to describe which rules were applied to SAM Entity Registrations and how they worked. The lack of clearly defined or documented validation rules contributed to the quality issues we found, such as incomplete, inaccurate, or duplicate data, that undermine data reliability and interoperability.

OMB guidance requires agencies to establish procedures to ensure that information is reviewed for quality before it is disseminated, but there are no specific federal requirements or guidance for what these procedures should be.[38] Therefore, we identified practices based on our prior work and policies and processes that federal agencies used.[39]

Based on the practices identified, we developed and used these five factors to assess data quality:

· Missing values. Information in data elements is missing, which could indicate incomplete records.

· Invalid values. Data do not conform to expected values or fall outside of valid time periods.

· Invalid data formats. Characters and format type for the data field do not align with the data source owners’ rules and specifications, when available.

· Conflicting data relationships. Combinations of values between data elements are illogical.

· Duplicate values. Data entries are either full duplicates (i.e., where all the values in a record are repeated) or partial duplicates (i.e., where specific values within a record appear more than once).

All nine data sources we reviewed had at least one data quality issue based on the factors we assessed, as we summarize in table 8.

|

Owner Data source |

Missing values |

Invalid values |

Invalid data formats |

Conflicting data relationships |

Duplicate data |

|

General Services Administration (GSA) |

|

||||

|

Federal Audit Clearinghouse |

Unclear |

✓ |

✓ |

✓ |

✓ |

|

System for Award Management (SAM) Entity Registrations |

✓ |

✓ |

X |

✓ |

X |

|

SAM Exclusions |

✓ |

✓ |

✓ |

X |

✓ |

|

Department of Health and Human Services (HHS) - Office of Inspector General (OIG) |

|||||

|

List of Excluded Individuals and Entities |

✓ |

✓ |

✓ |

X |

✓ |

|