RETIREMENT SECURITY

Most Defined Contribution Plans Do Not Require Spousal Consent to Remove Funds and Doing So Would Involve Trade-offs

Report to Congressional Requesters

United States Government Accountability Office

A report to congressional requesters.

For more information, contact: Tranchau (Kris) T. Nguyen at nguyentt@gao.gov.

What GAO Found

Millions of married Americans save for retirement by participating in a defined contribution plan, such as a 401(k). While most plans require spousal consent for beneficiary changes, few require it to remove funds (e.g., take a loan, withdrawal, or distribution). For example, money purchase and target benefit plans, which require spousal consent to actively remove funds (e.g., not use the plan’s default distribution option), account for less than one percent of all private sector defined contribution plans. These plans require a survivor annuity upon the participant’s death, ensuring the spouse receives regular plan payments unless the spouse previously consented to the designation of another beneficiary. The Thrift Savings Plan for federal workers generally requires spousal consent to remove funds but not for beneficiary changes. Among the married households where at least one spouse had a 401(k) or similar account, about one in 10 removed funds in 2021, according to national survey data. Those that removed funds typically took less than 10 percent of the total household retirement balance.

When a defined contribution plan participant removes funds without their spouse’s consent, their spouse may experience financial and personal hardship, according to most stakeholders GAO interviewed. For example, the funds may be irreversibly gone, or it may create marital conflict. Stakeholders said that women are more likely than men to be negatively affected, in part because fewer women have their own retirement accounts. While there are no data on how often participants remove funds without their spouses’ knowledge, stakeholders said they think it is likely not common. Of the incidences stakeholders described to GAO, however, some cases reportedly involved severe consequences for the spouse, including losses of hundreds of thousands of dollars. The severity of the economic impact on the spouse depends on the total amount of funds taken and what proportion they represented of the retirement savings. Other factors impacting severity include personal circumstances such as the spouse’s income and how much time they have to make up lost savings before retirement.

401(k)-type Account Ownership in Married Couples

Adding spousal consent requirements to all defined contribution plans could increase financial safeguards for some spouses but may delay processing or increase costs for plans and participants, according to most stakeholders. For example, spousal consent requirements could prevent participants from removing funds during a divorce without the knowledge of the spouse. Additional requirements could increase operating costs, which plans may pass on to participants. Stakeholders identified alternatives and modifications to spousal consent requirements that may reduce administrative burdens, including notifying spouses when a participant removes funds, or only requiring consent to remove funds above a certain threshold. They also said that some exceptions to spousal consent requirements may be warranted, such as in cases of domestic violence.

Why GAO Did This Study

Married individuals can spend a lifetime saving for retirement through defined contribution plans, and the federal government offers incentives to contribute to them. If a plan participant removes retirement funds from their account without their spouse’s knowledge, it can significantly reduce the future retirement income for both of them. Federal law provides protections in some retirement plans by requiring spousal consent to remove funds, but protections differ among plan types.

GAO was asked to examine these issues. This report examines (1) when married participants are required to obtain spousal consent to remove funds from or designate a beneficiary in defined contribution plans, and how often fund removal occurs; (2) what stakeholders said about the potential effects on spouses when married participants take out funds without their spouse’s consent; and (3) what stakeholders cite as the trade-offs of increasing spousal protections and potential alternatives.

GAO reviewed relevant federal laws and regulations. GAO also analyzed nationally representative survey data from the 2022 Survey of Consumer Finances, the most recent available. GAO interviewed federal government officials and stakeholders from eight national organizations. These organizations represented retirees or the retirement industry. GAO also interviewed representatives from four family or retirement law firms and five firms that sponsor or manage retirement plans, and three spouses. GAO selected interviewees based on research or referral from other interviewees.

Abbreviations

ERISA The Employee Retirement Income Security Act of 1974

CSRS Civil Service Retirement System

FERS Federal Employees’ Retirement System

ICI Investment Company Institute

IRA Individual Retirement Account

IRC Internal Revenue Code

IRS Internal Revenue Service

REA Retirement Equity Act of 1984

SCF Survey of Consumer Finances

TSP Thrift Savings Plan

This is a work of the U.S. government and is not subject to copyright protection in the United States. The published product may be reproduced and distributed in its entirety without further permission from GAO. However, because this work may contain copyrighted images or other material, permission from the copyright holder may be necessary if you wish to reproduce this material separately.

March 5, 2026

The Honorable Bill Cassidy, M.D.

Chair

Committee on Health, Education, Labor, and Pensions

United States Senate

The Honorable Bernard Sanders

Ranking Member

Committee on Health, Education, Labor, and Pensions

United States Senate

The Honorable Patty Murray

Vice Chair

Committee on Appropriations

United States Senate

The Honorable Tammy Baldwin

United States Senate

Married individuals each can spend a lifetime saving for retirement through their respective defined contribution plans, such as 401(k) plans, and the federal government offers incentives to foster savings in these plans. For many U.S. households, retirement accounts can be their biggest financial asset outside the value of their home, for those who own one. But if one spouse removes funds from their defined contribution plan without the knowledge of the other spouse, it can significantly reduce future retirement income for both of them.

Federal law requires spousal consent for certain retirement plans, for example, by requiring documented consent to actively remove funds from the plan.[1] These requirements provide spousal protections to prevent participants from taking out funds without their spouse’s knowledge.[2] Plans subject to spousal consent requirements include private sector defined benefit plans, which typically provide a lifetime annuity benefit, and the Thrift Savings Plan, a defined contribution plan for federal employees and uniformed services members. However, federal law does not require these same spousal protections for all defined contribution plans. Defined benefit plans and certain defined contribution plans are also subject to spousal consent requirements for changes in beneficiary designation.

When individuals take out funds from defined contribution accounts without the knowledge or consent of their spouse, this can disproportionately affect women’s financial security. Women are more likely than men to work in part-time jobs that do not offer retirement plans. Women are also more likely to interrupt their careers to take care of family members. Because of this and other factors, married women may be more reliant on their spouse’s retirement savings and therefore more vulnerable to financial hardship if their spouse removes savings without their consent.

Members of Congress and the public have expressed concern about the potential effects of participants removing funds from defined contribution plans without spousal consent, as well as the potential burdens of introducing additional spousal protections to defined contribution plans. You requested that we study these issues. This report examines (1) when married plan participants are required to obtain spousal consent to remove funds from and designate beneficiaries in defined contribution plans, and how often they remove funds; (2) the potential effects on spouses when married participants take out funds from defined contribution plans without their spouse’s consent, according to stakeholders; and (3) the trade-offs of increasing spousal protections in defined contribution plans and potential alternatives, according to stakeholders.

To identify when married plan participants are required to obtain spousal consent to remove funds from or to designate beneficiaries of defined contribution plans, we reviewed relevant federal laws and regulations. To determine how many defined contribution plans require spousal consent and how often married participants take out funds from plans that require spousal consent, we reviewed relevant federal agency publications.[3] These publications were the most recent available at the time of our analysis.

To provide additional context on how often married participants take funds out of their defined contribution accounts and the potential effect on spouses, we analyzed nationally representative survey data from the 2022 Survey of Consumer Finances (SCF), the most recent available at the time of our analysis.[4] The SCF is a triennial survey of about 4,600 households that includes in-depth information about household assets and income, including any funds individuals in those households removed from their defined contribution accounts. For example, the SCF includes information on the amount and type of funds removed and demographic information on married participants.

To assess the reliability of the SCF data, we reviewed related documentation and conducted electronic testing (e.g., checked for missing data, outliers, and obvious errors, and conducted logic tests). We determined that the SCF data were sufficiently reliable to report on how often married and unmarried participants took out funds from their defined contribution plans and to describe certain demographics and characteristics of participants and their spouses.[5]

To describe what stakeholders said are the potential effects on spouses when married participants remove funds from defined contribution plans without their spouse’s consent, we interviewed three current or former spouses with relevant experience, representatives of four national organizations representing a range of retirees, and representatives from four retirement or family law firms that provide support to such individuals.[6] We selected the four national organizations based on their expertise in retirement policy and procedure and their work representing the interests of current or future retirees. Similarly, we selected the four law firms based on their experience with retirement and family law and their work with spouses who had gone through or were presently engaged in divorce proceedings that required the division of assets, including funds held in retirement accounts.

To describe what stakeholders cite as the trade-offs of increasing spousal protections in defined contribution plans, we interviewed representatives from four national organizations that represent the views of the retirement industry (including a range of plan sponsors, plan administrators, and record keepers).[7] We selected these organizations based on their expertise in retirement policy and procedure and their work representing the interests of groups that sponsor or manage defined contribution plans. In addition, we interviewed representatives of three large record keepers to understand their experience and any potential challenges managing spousal consent requirements for retirement plans that they service through their platforms.[8] Together, these record keepers have served tens of millions of participants. We interviewed representatives of two plan sponsors that had increased spousal protections in place for the defined contribution plans to understand the reasons they required consent and any challenges to the consent process. We also interviewed representatives of the same four law firms and four organizations representing retirees we previously mentioned.

To inform all three objectives, we interviewed officials from the Department of Labor, the Department of the Treasury and its Internal Revenue Service (IRS), and the Federal Retirement Thrift Investment Board, which administers the Thrift Savings Plan.

We conducted this performance audit from April 2024 to March 2026 in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

Background

There are generally two forms of employer-sponsored retirement plans:

· A defined benefit (pension) plan is a retirement plan that traditionally promises to provide a lifetime annuity benefit. The benefit is based on a formula specified in the plan that typically takes into account factors such as an employee’s salary, years of service, and age at retirement.

· A defined contribution plan is an account-based retirement plan, such as a 401(k) plan, that allows individuals to accumulate tax-preferred retirement savings in an individual account. The savings are based on employee and/or employer contributions, and the investment returns (gains and losses) earned on the account. There are several types of defined contribution plans, and 401(k) plans are the most commonly held defined contribution plan.

Removing Funds from Defined Contribution Plans

Defined contribution plan participants may be able to withdraw funds from their retirement account while working for their employer or may request a distribution of funds upon retirement or separation from their employer.[9] Plan participants may actively remove funds from the plan, or they may take no action and passively choose the plan’s default distribution option.[10] The type of withdrawals and distributions available to participants are generally determined by the plan.

Plan participants can access their retirement savings early (prior to retirement, while they are still working) to help meet certain financial needs, if permitted by their plan. Typically, plans allow participants early access to their savings in one or more of the following forms:[11]

· Hardship withdrawals. Defined contribution plans may allow participants who are facing a hardship to take an early withdrawal because of an immediate and heavy financial need. As of 2022, plans can rely on participants’ self-certification regarding their hardship.[12] Employers are no longer required to collect documentation from participants when approving hardship withdrawals.[13]

· Loans. Defined contribution plans may allow participants to take loans from their accounts and they can limit the number of loans allowed.[14] If the plan allows loans, the maximum amount a participant may borrow cannot exceed the lesser of (1) 50 percent of their vested account balance or $10,000, whichever amount is greater, or (2) $50,000.[15] Generally, the employee must repay a plan loan within 5 years and must make payments at least quarterly.[16]

· Age 59½ withdrawals. Defined contribution plans may permit withdrawals when the participant reaches age 59½, even if still employed.

When plan participants separate from their employer or retire, they generally have four options for their defined contribution plan savings, depending on the terms of the plan. These options include

· leaving their savings in their former employer’s plan,

· consolidating their savings by rolling it over into a new plan sponsored by their new employer (i.e., a plan-to-plan rollover),

· rolling over their savings into an Individual Retirement Account[17], or

· taking a lump-sum distribution of their plan savings (i.e., a “cashout”[18]).

Annuities and the Evolution of Spousal Consent in Federal Law

The Employee Retirement Income Security Act of 1974 (ERISA), as amended, and the Internal Revenue Code (IRC) generally set requirements for private-sector retirement plans.[19] One such requirement applies to defined benefit plans and certain defined contribution plans that pay benefits to participants in the form of a life annuity. In the event of the participant’s death in retirement, these plans generally must provide for the accrued benefit payable to the participant to be provided to the surviving spouse as a qualified joint and survivor annuity.[20] The amount paid to the surviving spouse must be no less than 50 percent and no greater than 100 percent of the amount of the annuity paid during the participant’s life.

The Retirement Equity Act of 1984 (REA) amended ERISA’s annuity requirements for all defined benefit plans and certain defined contribution plans to require spousal consent in additional specific circumstances, and included corresponding amendments to the IRC.[21] The REA was enacted primarily in response to public concerns that retirement plan participant’s spouses and working women were not receiving their fair share of private-sector retirement benefits in some circumstances. ERISA provided some spousal protection post-retirement with its requirement that plans offer vested participants a qualified joint and survivor annuity at retirement. However, in some cases, participants were choosing to forgo a joint and survivor annuity in favor of a single life annuity, which left surviving spouses without any ongoing retirement benefit when the participant died. REA added a requirement that participants could only forgo the qualified joint and survivor annuity with spousal consent.

REA also added some pre-retirement spousal protections. In particular, REA required defined benefit plans and certain defined contribution plans to provide married participants a qualified pre-retirement survivor annuity. Participants can only waive this pre-retirement survivor coverage with written spousal consent.[22]

If a defined contribution plan offers a lifetime annuity, then the plan is generally subject to the annuity requirements for married participants and their spouses. Most defined contribution plans, such as 401(k) plans, do not offer participants the option to receive benefits in the form of a life annuity. In 2023, nearly 7 percent of profit-sharing or 401(k) plans offered an “in-plan” annuity option to their participants, according to an industry survey. About 17 percent of these types of plans are considering offering some form of annuity option in the future, according to the survey.[23]

Beneficiary Designation in Defined Contribution Plans

A beneficiary under an ERISA-covered defined contribution plan is a person who is or may become entitled to a portion of a participant’s benefit under the plan, such as in the event of the participant’s death. The beneficiary is designated by the participant or the terms of the plan. For all ERISA-covered plans, the surviving spouse is the default designated beneficiary.[24]

The Thrift Savings Plan

Federal employees and uniformed service members may participate in a defined contribution plan called the Thrift Savings Plan (TSP). Thrift Savings Plan accounts are similar to 401(k) accounts available to private-sector employees. Like some other defined contribution plans, TSP participants can make early withdrawals (while they are working for their employer) as well as receive distributions post-retirement. The TSP offers hardship withdrawals, loans, and age 59½ in-service withdrawals for working participants.[25] The TSP also allows distributions in the form of rollovers, cashouts, and non-annuity distributions, such as periodic payments or installment payments for separated or retired participants. Thrift Savings Plan participants can also elect an annuity option to distribute their post-retirement benefits.

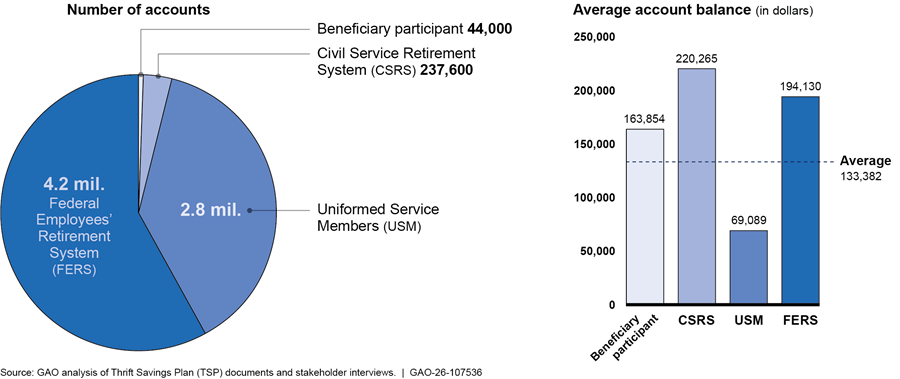

The TSP is the largest defined contribution plan in the U.S., with about $963 billion in assets and 7.2 million plan participant accounts in December 2024. The Federal Employees’ Retirement System Act of 1986 established the TSP and governs its administration. Unlike the plans we have previously discussed, the TSP is not subject to ERISA or the Retirement Equity Act. However, the TSP has its own set of spousal consent requirements.[26]

Most Defined Contribution Plans Do Not Require Spousal Consent for Participants to Take Out Funds, but a Few Plan Types, and the TSP, Do

Married participants in most defined contribution plans, such as 401(k)s, are allowed to take a loan or otherwise remove funds without obtaining consent from their spouse. There are some exceptions. A relatively small number of defined contribution plans, such as money purchase plans, and the Thrift Savings Plan, are subject to federal laws requiring documented spousal consent to actively remove funds from the plan. While spousal consent is not often required for fund removal, in most defined contribution plans, the spouse is generally the default beneficiary, and the plan must obtain spousal consent if a participant seeks to change their beneficiary designation. Nationally representative data from the Survey of Consumer Finances provides information on the prevalence of fund removal from defined contribution plans. Among the married households of any age in which at least one spouse had a 401(k) or similar account, about one in 10 households removed funds in 2021 and typically took less than 10 percent of the balance.

Few Defined Contribution Plans Require Spousal Consent to Actively Remove Funds, but Most Require It for Beneficiary Changes

Most defined contribution plans, including most 401(k)s, do not require spousal consent for participants to actively remove funds through withdrawals, loans, or distributions. Defined contribution plans that are not subject to spousal consent requirements under the REA, such as those that do not pay benefits in the form of a life annuity and meet other requirements, are not required to obtain spousal consent before married participants remove funds from the plan. The majority of defined contribution plans fall into this category. In cases where a defined contribution plan offers benefits in the form of an annuity and meets other requirements, spousal consent requirements do not apply if the participant does not elect the annuity option. Specifically, defined contribution plans are not subject to spousal consent requirements under the REA when

· the plan provides that the participant’s vested accrued benefit is payable in full upon their death to the surviving spouse or, if there is no surviving spouse or the surviving spouse consents in a manner consistent with federal requirements, to a designated beneficiary;

· the participant does not elect payment of benefits in the form of a life annuity; and

· the plan is not a direct or indirect transferee of a plan that was a defined benefit plan or was subject to the Internal Revenue Code’s funding requirements.[27]

Such plans are referred to as REA “safe harbor” plans.

|

Choosing to Remove Funds from Defined Contribution Accounts Federal law prescribes the circumstances in which retirement plans can allow participants (i.e., the eligible employees covered by the retirement plan) to remove funds through withdrawals, loans, and distributions from their plan accounts. Federal law also prescribes the applicability of spousal consent requirements to remove funds. This report focuses on active removal of funds (e.g., not on removal of funds through the plan’s default distribution option). Plans are not required to offer all distribution options to participants. For example, defined contribution plans are permitted but not required to provide distributions in the case of hardship. A plan may elect to include spousal consent requirements in its design, even if it is not required to. Spousal consent requirements impose a restriction on a plan participant’s ability to remove funds. Source: GAO analysis of federal law and agency guidance. | GAO‑26‑107536 |

Additionally, there is no requirement for spousal consent regarding a rollover of REA “safe harbor” plan funds to another retirement account.[28] Federal spousal protection and consent rules are no longer applicable after a plan participant transfers funds from a defined contribution plan account to an Individual Retirement Account (IRA). For more information about IRAs see text box.

|

Individual Retirement Accounts An Individual Retirement Account (IRA) is a tax-favored personal savings account that allows an individual to set aside money for retirement. Traditional IRAs are not defined contribution plans and are not subject to the Employee Retirement Income Security Act of 1974, as amended, or the Retirement Equity Act of 1984. Consequently, they are not subject to federal spousal consent requirements when removing funds from an IRA, but state laws may apply. IRAs play a large role in retirement savings. According to Investment Company Institute (ICI) research, IRAs held $17 trillion in assets at the end of 2024 in comparison to $12 trillion in assets for defined contribution plans. In mid-2024 ICI found that 59 percent of traditional IRA-owning households said their IRAs contained rollovers from their employer-sponsored retirement plans. |

Source: GAO analysis of retirement industry reports and federal laws and regulations. | GAO‑26‑107536

While most defined contribution plans do not have spousal consent requirements to actively remove funds (e.g., not use the plan’s default distribution option), money purchase and target benefit plans do. Together these plans made up less than 1 percent of all private sector defined contribution plans in 2022, according to the Department of Labor.

Money purchase plans. Employers are required to make annual contributions on behalf of their employees. Federal law requires the employer to decide what percentage of each employee’s salary to contribute, with a deductible limit of 25 percent (this is subject to the overall defined contribution limit, which is $72,000 in 2026). Employees determine how to invest the contributions made on their behalf. Money purchase plans generally do not permit in-service withdrawals, but loans are permitted. These plans accounted for 0.5 percent of private sector defined contribution plans in 2022, according to the Department of Labor.

Target benefit plans. A target benefit plan is a defined contribution money purchase plan where contributions to an employee’s account are determined based on the estimated amounts necessary to fund an employee’s stated target retirement benefit under the plan. The actual benefit that the participant will receive will vary from the stated target benefit based on investment performance. According to the Department of Labor, target benefit plans accounted for less than 0.1 percent of private sector defined contribution plans in 2022. See table 1 for more information on selected defined contribution plan types.

|

Type of plan |

Number of plans |

Active participants (Thousands) |

Assets (Billions of dollars) |

|

401(k) plan |

685,997 |

79,444 |

$6,786 |

|

Money purchase plan |

4,051 |

1,856 |

$199 |

|

Target benefit plan |

306 |

20 |

$2 |

Source: Department of Labor documents. | GAO 26-107536

Note: We selected 401(k) plans because they are the most commonly held private sector defined contribution plan, and we selected money purchase and target benefit plans because they are subject to spousal consent requirements under the Retirement Equity Act of 1984. Approximately 0.05% of individual account plans indicate both 401(k) and 403(b) plan characteristics. Such plans are classified as 401(k) plans in this table. The 401(k) plan counts include 287 money purchase plans and 86 target benefit plans.

The few defined contribution plans subject to the federal spousal consent rules under REA require spousal consent for participants to actively remove funds from their account. Such plans (including money purchase plans and target benefit plans) must require spousal consent for all removal of funds permitted by the plan while the participant is employed, and any post-retirement withdrawal that differs from the plan’s default distribution option.[29] These plans also must offer survivor benefits in the form of a joint and survivor annuity for account balances over $7,000. As noted earlier, the joint and survivor annuity generally provides benefits for the participant and, in the event of the participant’s death in retirement, their surviving spouse. In the event of the participant’s death before retirement, these plans must offer survivor benefits in the form of a pre-retirement survivor annuity. The plan participant may elect to waive the annuity, but their spouse must consent to the election in writing witnessed by a notary or a plan administrator.

For context across the retirement system, we reviewed the spousal consent requirements applicable to various types of retirement plans and IRAs. Spousal consent requirements differ by type of retirement plan. For example, similar to money purchase and target benefit plans, defined benefit plans also require spousal consent to change distributions. However, defined benefit plans do not allow hardship withdrawals with or without spousal consent. For additional information regarding plan spousal consent provisions for withdrawals, loans, and distributions by plan type, see table 2.

|

|

Defined benefit plansa |

Money purchase and target benefit plansb |

401(k) plansc |

Thrift Savings Pland |

Individual retirement accounts |

|

Spousal consent required to waive annuity rights |

√ |

√ |

N/A |

√ |

N/A |

|

Spousal consent required for post-retirement withdrawalse |

√ |

√ |

No |

√ |

No |

|

Spousal consent required for loans, where permitted |

√ |

√ |

No |

√ |

N/A |

|

Spousal consent required for hardship withdrawal, where permitted |

N/A |

N/A |

No |

√ |

N/A |

|

Spousal consent to be witnessed by notary or plan representative |

√ |

√ |

N/A |

Nof |

N/A |

Source: GAO analysis of federal laws and regulations. | GAO‑26‑107536

aAn employer-sponsored retirement plan that traditionally promises to provide a lifetime annuity benefit. The benefit is based on a formula specified in the plan that typically takes into account factors such as an employee’s salary, years of service, and age at retirement.

bIf a participant transfers funds from a money purchase or target benefit plan to a 401(k) plan, then spousal consent requirements in the “Money Purchase and Target Benefit Plan” column apply to those funds.

cSome 401(k) plans offer an annuity option. For these plans, if a participant chooses this option, then spousal consent requirements described in the “Money Purchase and Target Benefit Plan” column will apply.

dThe TSP provides federal civilian employees and members of the uniformed services the opportunity to save for retirement security in a similar manner as many private corporations do with 401(k) plans. This column describes requirements for Federal Employees’ Retirement System (typically hired on or after 1987) and uniformed services member participants. Spouses of Civil Service Retirement System participants (typically hired before 1987) only receive notice that a participant has taken out funds.

eThis category includes new withdrawals (e.g., not previously established, automatically recurring withdrawals) or changes to existing automatically recurring withdrawals. It does not include recurring annuity payments.

fThe TSP discontinued the notary requirement in 2022.

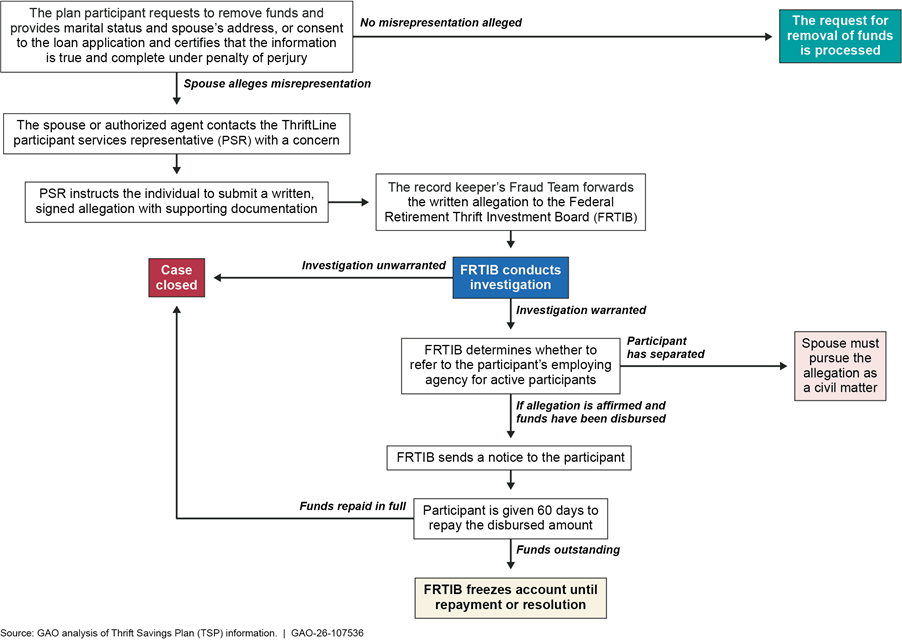

The Thrift Savings Plan Generally Requires Spousal Consent to Remove Funds

The TSP for federal employees and uniformed service members requires spousal consent for a plan participant to remove funds. Plan participants have multiple options to remove funds, including in-service withdrawals, loans, and post-employment distributions.[30] Whether spousal consent is required depends upon the type of plan participant. There are three groups of plan participants: Civil Service Retirement System (CSRS) employees (typically those hired before 1987), Federal Employees’ Retirement System (FERS) employees (typically those hired on or after 1987), and uniformed service members.[31] FERS and uniformed services member plan participants must obtain written consent from their spouse waiving any right the spouse may have to a survivor annuity to remove funds.[32]

CSRS plan participants are not required to obtain spousal consent, but their spouses are generally entitled to be notified when the participant applies for a post-employment distribution or a change to existing payments. Participants must provide a copy of their spouse’s email or physical address with their request to remove funds. CSRS plan participants made up a small share of total TSP participants and had a larger average account balance than other participant groups, as of December 2024 (see fig. 1).

Notes: FERS typically includes federal employees and uniformed service members hired on or after 1987. CSRS typically includes those hired before 1987. Beneficiary participants are the spouses of deceased participants whose TSP account balance is $200 or more.

Most Defined Contribution Plans Require Spousal Consent to Change Beneficiaries, but the TSP Does Not

Most defined contribution plans generally require that the participant’s spouse be the designated beneficiary of plan funds if the participant dies. Specifically, in ERISA-covered plans, the spouse must be the beneficiary unless the spouse consents to changing the beneficiary. Before allowing a change in beneficiary, any ERISA-covered plan is generally required to obtain written notarized spousal consent.

For context across the retirement system, we reviewed the beneficiary designation requirements of various types of retirement plans. Spousal consent requirements regarding the designation of a beneficiary differ by type of retirement plan or account. For example, the TSP and IRAs do not require spousal consent for beneficiary changes. For additional information, see table 3.

Table 3: Federal Spousal Consent Requirements for Beneficiary Designation in Different Types of Retirement Plans and Accounts

|

|

Defined benefit plansa |

Money purchase and target benefit plans |

401(k) plans |

Thrift Savings Plan |

Individual retirement accounts |

|

|

Requires spouse as default beneficiary |

√ |

√ |

√ |

√ |

No |

|

|

Spousal consent required to change beneficiary |

√ |

√ |

√ |

No |

No |

|

Source: GAO analysis of federal laws and regulations. | GAO‑26‑107536

aAn employer-sponsored retirement plan that traditionally promises to provide a lifetime annuity benefit. The benefit is based on a formula specified in the plan that typically takes into account factors such as an employee’s salary, years of service, and age at retirement.

The TSP Does Not Require Spousal Consent to Change Beneficiaries

Unlike the ERISA-covered plans discussed above, TSP participants may change their beneficiaries at any time without the knowledge or consent of their spouse.[33] When a participant dies without designating a beneficiary, the TSP follows an order of precedence established in statute where the spouse is first. While the default beneficiary is the spouse, participants who choose to may designate up to 20 beneficiaries for an account without informing their spouse or obtaining their consent. In addition to individuals, plan participants may designate firms, corporations, legal entities, and the U.S. government as beneficiaries. TSP officials said that generally when a participant names a beneficiary it is the participant’s spouse.

Among Married Households with Defined Contribution Accounts, About 11 Percent Took Out Funds in 2021, and They Typically Took Less Than 10 Percent of the Balance

Among married households of any age with one or more defined contribution retirement accounts, about 11 percent took out retirement funds in 2021, according to our analysis of Survey of Consumer Finances data.[34] For this analysis, taking out funds includes withdrawing funds before retirement (e.g., loans, hardship withdrawals) and taking disbursements in retirement, but not rollovers (see text box on leakage). The 2022 Survey of Consumer Finances generally provides a snapshot of financial activity in 2021, which may not be representative of other years.[35]

|

Leakage from Defined Contribution Retirement Accounts In its 2021 report, the Joint Committee on Taxation described “leakage” as generally occurring when more funds leave a worker’s retirement account than enter it. This captures a broader range of activity than we could observe with our analysis of Survey of Consumer Finances data. The Joint Committee on Taxation report found that the most prominent factor associated with leakage is job separation, and that roughly 22 percent of contributions made by those age 50 or younger leak out of the retirement savings system in a given year. They noted that when a worker separates from a job, employers can force workers with small defined contribution balances ($1,000 or less) to remove those funds from the account. At that point, the worker may roll the funds over to an Individual Retirement Account or move the funds outside of retirement accounts. |

Source: Joint Committee on Taxation, Estimating Leakage from Retirement Savings Accounts, JCX-20-21 (Washington, D.C.: April 26, 2021). | GAO 26 107536

Removal of Defined Contribution Funds Among Married Households

Married households that took out funds were slightly older than those that did not take out funds, with an average survey respondent age of 56 for that subgroup (see table 4).[36] However, for several characteristics we examined, the differences between households that did and did not take out funds were not statistically significant.

Table 4: Selected Characteristics of Married Households That Removed and Did Not Remove Defined Contribution Retirement Funds

|

|

Married households that took out funds from their accounts in 2021 |

Married households that did not take out funds from their accounts in 2021 |

|

Average age of respondent |

56 years |

48 years |

|

Median household retirement savings |

$149,100* |

$95,800* |

|

Median household income |

$134,900* |

$150,700* |

|

Percent of respondents with a college degree |

42% |

60% |

|

Percent of respondents who are White (non-Hispanic) |

77%* |

78%* |

Source: 2022 Survey of Consumer Finances. | GAO‑26‑107536

Notes: Accounts include defined contribution accounts (such as 401(k) accounts). They do not include defined benefit (pension) plans or Individual Retirement Accounts. Households that took out retirement funds are households in which one or more spouses took out funds from one or more retirement account. This includes loans, pre-retirement withdrawals, and post-retirement distributions. It does not include rollovers. For estimates marked with an asterisk (*), the difference between household types is not statistically significant. For the estimate of respondents’ age in households that took out funds, the 95 percent confidence interval was + / - about 3 years. It was + / - about 1 year in households that did not take out funds. For the estimate of median household retirement account savings in households that took out funds, the 95 percent confidence interval was + / - $42,800. It was + / - $21,100 in households that did not take out funds. For the estimate of median household income in households that took out funds, the 95 percent confidence interval was + / - $19,600. It was + / - $8,900 in households that did not take out funds. For the estimate of respondents with a college degree in households that took out funds, the 95 percent confidence interval was + / - 9 percentage points. It was + / - 4 percentage points in households that did not take out funds. For the estimate of respondents who are White (non-Hispanic) in households that took out funds, the 95 percent confidence interval was + / - 8 percentage points. It was + / - 2 percentage points in households that did not take out funds.

For context, a higher proportion of married households had 401(k)-type defined contribution retirement accounts when compared to non-married households, including single-person households and unmarried couples. Specifically, 49 percent of married households had one or more such accounts, compared to 28 percent of non-married households.[37] Married households with defined contribution accounts, on average, were older, had higher levels of education, income, and savings, and were more often White (non-Hispanic) than non-married households with defined contribution accounts (see table 5).

Table 5: Selected Characteristics of Married and Non-Married Households with One or More Defined Contribution Retirement Accounts

|

|

Married Households with Accounts |

Non-Married Households with Accounts |

|

Average age of respondent |

49 years |

44 years |

|

Median household retirement savings |

$100,000 |

$27,400 |

|

Median household income |

$148,500 |

$76,500 |

|

Percent of respondents with a college degree |

58 percent |

47 percent |

|

Percent of respondents who are White (non-Hispanic) |

78 percent |

68 percent |

Source: GAO analysis of 2022 Survey of Consumer Finances data. | GAO‑26‑107536

Notes: Accounts include defined contribution accounts (such as 401(k) accounts). They do not include Individual Retirement Accounts or defined benefit (pension) plans. For all estimates, the difference between household types is statistically significant. For the estimate of respondent age in married households, the 95 percent confidence interval was + / - 1 year. It was also + / - 1 year in non-married households. For the estimate of median household retirement savings in married households, the 95 percent confidence interval was + / - $11,800. It was + / - $4,900 for non-married households. For the estimate of median household income in married households, the 95 percent confidence interval was + / - $8,500. It was + / - $5,300 for non-married households. For the estimate of respondents with a college degree in married households, the 95 percent confidence interval was + / - 4 percentage points. It was + / - 4 percentage points in non-married households. For the estimate of respondents who are White (non-Hispanic) in married households, the 95 percent confidence interval was + / - 2 percentage points. It was + / - 4 percentage points in non-married households.

When one or more person of any age in a married household took out retirement funds in 2021, the median amount they took was about 7 percent of the total household’s balance.[38] Specifically, the median amount they took out during the year was $8,500.[39] This comprised about 5 percent of their annual income from all sources.[40]

Among married households that took out funds from their defined contribution accounts in 2021, many took out small amounts. Specifically, 42 percent took out $5,000 or less.[41] In contrast, removal of large shares was not typical among married households that took out funds from their defined contribution accounts. About 14 percent of married households that removed funds from their defined contribution accounts took out more than a quarter of the household savings.[42] The estimate for those that took a third or more was not statistically different from zero. For a broader discussion that includes removing funds from IRAs, see text box.

|

Removing Funds from Individual Retirement Accounts (IRA) While our analysis focused on 401(k)-type defined contribution accounts, we conducted additional analysis that included IRAs, using Survey of Consumer Finances data. About 69 percent of married households of any age had at least one IRA or defined contribution account, compared to about 49 percent of married households that had only defined contribution accounts. As individuals may generally invest in and remove funds from IRAs independent of their employer’s rules, including IRAs in our analysis also results in the more widespread removal of funds. Specifically, about 22 percent of married households with at least one IRA or defined contribution account removed funds in 2021, compared to about 11 percent for married households with at least one defined contribution account alone. Moreover, when including married households with IRAs, about 34 percent of those who removed funds took out $5,000 or less, which was not statistically different than the estimate for those with defined contribution accounts only. |

Source: GAO analysis of 2022 Survey of Consumer Finances. | GAO 26 107536

Note: The 95 percent confidence intervals for all estimates in this text box were + / - 6 percentage points or less. Unless otherwise noted, the difference for estimates is statistically significant between household types.

Removal of Retirement Funds via Loans Among Married Households

Regarding loans, the subset of married households that took loans from their retirement accounts in 2021 had different characteristics than married households that took out retirement funds in other ways. For example, the average married household that took a loan from a retirement account was younger than other married households that removed funds (see table 6). This likely reflects the fact that plans that permit loans typically only offer loans to workers rather than retirees. Conversely, among married households taking funds other than loans, an estimated 89 percent were age 65 or older and 91 percent report that at least one person was retired.[43] This suggests most of those households were primarily taking out funds for use in retirement.

Table 6: Selected Characteristics of Married Households That Took Retirement Account Loans and Those That Removed Funds in Other Ways

|

|

Married Households Taking Loans from Their Accounts in 2021 |

Other Married Households Taking Funds from Their Accounts in 2021 (Excluding Loans) |

|

Average age of respondent |

48 years |

72 years |

|

Median household retirement savings |

$111,200* |

$344,200* |

|

Median household income |

$117,600 |

$168,000 |

|

Percent of respondents with a college degree |

27% |

70% |

|

Percent of respondents who are White (non-Hispanic) |

66% |

97% |

Source: GAO analysis of 2022 Survey of Consumer Finances data. | GAO‑26‑107536

Notes: Retirement accounts include defined contribution accounts, such as 401(k) accounts. They do not include Individual Retirement Accounts or defined benefit (pension) plans. For estimates marked with an asterisk (*), the difference between household types is not statistically significant. For the estimate of respondent age in households that took loans, the 95 percent confidence interval was + / - 3 years. It was + / - 2 years in other households taking out funds. For the estimate of household retirement savings in households that took loans, the 95 percent confidence interval was + / - $37,300. It was + / - $246,000 in other households taking out funds. For the estimate of income in households that took loans, the 95 percent confidence was + / - $10,500. It was + / - $36,100 in other households taking out funds. For the estimate of respondents with a college degree in households that took loans, the 95 percent confidence interval was + / - 9 percentage points. It was + / - 13 percentage points in other households taking out funds. For the estimate of White (non-Hispanic) respondents in households that took loans, the 95 percent confidence interval was + / - 10 percentage points. It was + / - 4 percentage points in other households taking out funds.

The average loan amount was about $10,800 for married households that took them in 2021.[44] About half (49 percent) of these respondents to the 2022 Survey of Consumer Finances took a loan of $5,000 or less.[45] This likely reflects the requirement that defined contribution account loans generally cannot exceed $50,000 or 50 percent of the vested account balance, whichever amount is less. While participants are expected to repay retirement plan loans, loans can reduce the total possible amount accumulated (see text box).

|

Loans in 401(k) Plans Just over half of all 401(k) plans offered loans to their participants in 2022, according to the Employee Benefit Research Institute and Investment Company Institute. After taking a loan from a 401(k) plan, participants must repay it with interest within five years and must make regular payments at least quarterly. If the participant uses the loan to purchase a primary residence, the plan may allow the participant a longer timeline to repay the loan. If the participant does not pay back the loan within the specified period, the loan is considered a distribution. Any taxable portion of the loan is then subject to income tax and may also be subject to a 10 percent early distribution tax. |

Source: GAO review of retirement industry reports and federal agency guidance. | GAO 26 107536

When Participants Take Out Retirement Funds Without Consent, Their Spouses May Experience Varied Degrees of Financial and Personal Hardship

Spouses May Experience Reduced Financial Security and Emotional Well-Being When Participants Take Out Funds Without Their Consent, According to Stakeholders

When participants take out retirement funds without consent, stakeholders said their spouses may be financially worse off, particularly as it relates to their retirement security. According to legal stakeholders, those representing a range of retirees, and spouses we interviewed, once a participant takes out retirement funds, those funds may be irreversibly gone from the retirement account.[46] As we reported in 2019, when participants permanently remove assets from retirement accounts, it can reduce the amounts they accumulate before retirement, including the loss of compounded interest.[47]

|

One spouse said: “[I was hoping I] could use some of the [retirement] money to pay bills, but now those expectations and options are gone.” Source: GAO interview. | GAO‑26‑107536 |

In addition to reduced retirement security, the participants’ removal of funds without spousal consent may result in other financial and personal hardships for their spouses, according to some stakeholders. For example, two spouses we spoke with said the participant’s removal of funds had an immediate financial effect on them, such as causing the spouse to delay retirement. Additionally, some stakeholders said fund removals without consent can lead to a divorce, which can have additional detrimental financial effects. As we reported in 2023, households that separated, divorced, or were widowed frequently experienced a decline in their retirement account balance, and low-income households experienced these marital status changes more often than high-income households did.[48]

|

One spouse said: “[My husband] had taken the whole amount out of the 401(k) account without informing me or telling me anything. I only found out because he was overspending on…things he usually did not spend money on.” Source: GAO interview. | GAO‑26‑107536 |

While the loss of retirement funds may lead to financial strain, some stakeholders said not all spouses end up experiencing financial hardship as a result. For example, the couple may have previously agreed to a particular expenditure, such as remodeling their kitchen or paying for an emergency, even if the spouse did not explicitly consent to use the participant’s retirement funds. Other couples may be financially secure enough that a loss of some retirement funds would not degrade their quality of life.

|

One spouse said: “I don’t understand why he would— I want to say betrayal. I think if we had talked, a lot of it wouldn’t have come to this.” Source: GAO interview. | GAO‑26‑107536 |

Spouses who did not know of or consent to the removal of retirement funds may feel lied to and betrayed, which can lead to personal hardship and marital discord, according to legal stakeholders, those representing retirees, and spouses we interviewed. Stakeholders said discovering the deceit can erode trust in the marriage. For example, the three spouses we spoke with, who each had retirement funds taken, all said they felt betrayed by the participants’ removal of funds without their consent. Dishonesty such as this can strain the relationship, according to stakeholders. One legal stakeholder and a spouse said that retirement fund removal without consent is a form of infidelity, which they referred to as “financial infidelity” (see text box).

|

“Financial Infidelity” According to a 2020 Harris Poll survey, about two in five individuals reported that a spouse or partner financially deceived them, among Americans who said that they have ever combined finances in a current or past relationship. Such deceptions included hiding purchases, bills, cash, or bank accounts, or lying about money. According to the survey, the financial deception, or “financial infidelity,” most commonly resulted in an argument or less trust in the relationship. In general, more minor deceptions, such as hiding bills, were more common than more significant deceptions, such as hiding their amount of debt or income. Similarly, more minor effects, such as arguments, were more common than more significant effects, such as separation or divorce. |

Source: The Harris Poll, Financial Infidelity Survey (July 7, 2021). | GAO 26 107536

|

One spouse said: “I thought we had a relationship where we could communicate at least that much, where he’d be telling me what was going on.” Source: GAO interview. | GAO‑26‑107536 |

The experience of learning that the participant removed funds without the spouse’s knowledge or consent can also take an emotional toll on spouses and harm their sense of well-being, according to stakeholders we interviewed. Legal stakeholders, those representing retirees, and spouses said that removing funds without consent can also lead spouses to discover troubling aspects about their marital relationship or the participant. For example, some stakeholders described participants removing funds in anticipation of a divorce. In addition, stakeholders said participants may conceal their removal of retirement funds from their spouse for several reasons, including to pay for an addiction, to repay debt, for expenses related to an extramarital relationship, or because they were experiencing dementia. One spouse said she learned that her husband had been liquidating his retirement account for years while pretending to be employed.

While Extent Is Unknown, Stakeholders Said the Incidence of Retirement Fund Removal Without Spousal Knowledge Is Likely Low and the Affected Spouses Tend to Be Women

The overall incidence of the removal of retirement funds without spousal consent is unknown due to the lack of nationally representative data on the topic. But legal stakeholders and those representing retirees we interviewed said, based on their experience, they think it is uncommon for participants to take out retirement funds against their spouse’s will. Based on their experience, some legal stakeholders and those representing retirees said they believe most participants inform their spouse or obtain their spouse’s verbal approval before taking funds from a retirement account. Some stakeholders said that it is difficult to identify affected spouses, in part because there are no requirements to document consent in most defined contribution plans, so spouses who did not consent to having funds removed have no legal avenue to seek recourse.

Some stakeholders said it is common for one person to manage the family finances, which may make it easier for one person to remove funds without the other’s knowledge or consent. During focus groups for our 2020 report on women’s retirement security, some women described being in marriages where they never discussed finances with their spouses, or said they relied on their spouses to handle the finances.[49] As we reported in 2020, some people may not even know that their spouse has a retirement account.[50] One stakeholder we spoke to added that having a shared understanding of the family’s finances is important in a marriage (see text box on financial literacy).

|

Financial Literacy Financial literacy—the ability to make informed decisions and take effective actions regarding money—is essential to helping ensure the financial health and stability of individuals and families. We have reported on the financial literacy of individuals, including retirement plan participants. For example, we reported that several economic, demographic, and technological trends have emerged that affect the need for financial literacy. These include the retirement of the baby boomers, the emergence of new digital financial products, and the increasing costs of retirement. In a 2011 forum we held on financial literacy, participants discussed the vulnerability of older Americans, noting their potentially increased susceptibility to fraud and the inability to recover from financial difficulties later in life. Plan participants and retired individuals, both married and unmarried, need to make sound financial decisions—such as when and how to take withdrawals and distributions from their retirement plan—so their savings can last throughout their lifetime. |

Source: Summary of GAO reports, including Highlights of a Forum: Financial Literacy in a Digital Age (GAO‑25‑107168). | GAO‑25‑107536

Women tend to be most affected by participants removing funds without consent, according to stakeholders we interviewed. For example, legal stakeholders, those representing retirees, and spouses with direct experience said that it was typically a husband who had removed funds without his wife’s consent.[51] Further, some stakeholders reiterated that the average woman earns less and lives longer than men, making women more vulnerable to retirement fund losses.

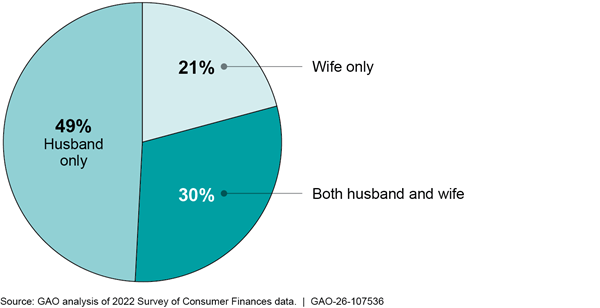

Survey data also indicate that women are more likely to be affected by a participant’s removal of funds without consent. Specifically, 2022 Survey of Consumer Finances data show that fewer married women had defined contribution accounts than married men (see fig. 2). The median balance in their accounts was an estimated $60,400 for women and $81,600 for men).[52] For a broader discussion that includes ownership of IRAs, see text box.

Figure 2: Ownership of Defined Contribution Retirement Accounts Among Married Households with at Least One Account, 2022

Note: Data are about opposite-sex married couples. Same-sex married couples represent an estimated one percent of married households in the survey data and are not included here. Retirement accounts include defined contribution accounts, such as 401(k) accounts. They do not include Individual Retirement Accounts or defined benefit (pension) plans. The 95 percent confidence interval was + / - 3 percentage points for these estimates.

|

Ownership of Retirement Accounts in Individual Retirement Accounts (IRA) While our analysis focused on 401(k)-type defined contribution accounts, we conducted additional analysis including IRAs using Survey of Consumer Finances data. Including IRAs in our analysis resulted in a somewhat more even ownership of retirement accounts within married households than when including defined contribution accounts alone. Among married households with either type of retirement savings account, the husband was the sole owner of the account(s) in about 34 percent of households. The wife was the sole owner in about 13 percent of households, and both husband and wife had one or more accounts in about 53 percent of the households. When including IRAs, the median balances were higher overall than for defined contribution accounts alone, with women still having a lower median balance than men (an estimated $70,000 for women compared to $101,000 for men). This suggests that IRAs, which typically exist outside of employment, may make it possible for more women to have retirement accounts, though their balances are typically lower than their male spouses. |

Source: GAO analysis of 2022 Survey of Consumer Finances. | GAO‑26‑107536

Notes: Data are about opposite-sex married couples. Same-sex married couples represent an estimated one percent of married households in the survey data and are not included here. The 95 percent confidence intervals for all percentage point estimates in this text box were + / - 3 percentage points or less, and for all dollar estimates they were + / - $11,300 or less

Severity of Negative Effect on Spouses Depends on Economic Impact of Fund Removal as well as Their Personal Circumstances

The severity of any effect of a participant removing retirement funds without their spouse’s consent depends on several things, including the economic impact on their spouse, according to stakeholders we interviewed. While the overall incidence may be low, some legal stakeholders and those representing retirees described cases that involved severe consequences for the affected spouse. Two stakeholders we spoke with had encountered cases in which a participant removed half a million dollars or more from a 401(k) account without the spouse’s knowledge or consent. One legal representative said their client experienced homelessness after her husband drained his 401(k) account.

|

One spouse said: “[As a single mother], all this affects how I live, work, and provide care for my children.” Source: GAO interview. | GAO‑26‑107536 |

Further, the economic impact on a spouse can be large if the amount of funds a participant removes makes up a significant share of the couple’s overall retirement savings, even if the dollar amount they removed is modest. For example, one spouse said that when her husband drained his retirement account, she had to start over to save for retirement. One stakeholder added that individuals in lower-income households have the most potential to be harmed by fund removal because the loss of funds has a disproportionate effect on their future retirement income.

Demographics also drive the extent to which fund removal may affect a spouse, such as the age of the spouse. Fund removal can affect both older and younger spouses negatively, though in different ways. Younger spouses can face the loss of decades of compound interest, as we reported in 2019.[53] In contrast, some stakeholders added that older spouses have fewer working years to recoup the lost funds. One stakeholder said spouses with a reduced capacity to work may be more negatively affected, such as those with disabilities or caregiving needs.

In addition to spouses being affected by the removal of funds without their consent, there can be negative consequences from an unexpected loss of beneficiary status. Some stakeholders described situations in which a participant died and the spouse discovered someone else was the beneficiary of retirement funds they had anticipated receiving (see text box).

|

Select Cases of Spouses Discovering They Are Not the Beneficiary Spouses are generally the default beneficiary in 401(k) plans, and changing the beneficiary requires the spouse to waive this right. Nonetheless, some stakeholders described concerns with non-spousal beneficiary designation in other retirement accounts that do not require spousal consent to change the beneficiary (such as Individual Retirement Accounts) or in cases involving divorce. One legal service provider said they encountered spouses who did not receive funds they anticipated because the participants designated someone other than their spouse as the beneficiary of their Individual Retirement Account. One ex-spouse we spoke to had divorced, and upon her ex-husband’s death was surprised to discover his current spouse was the beneficiary of retirement funds she had expected to receive as part of the divorce settlement.. |

Source: Interviews with stakeholders. | GAO 26 107536

Stakeholders Cited Heightened Risks of Spouses Losing Retirement Funds During and After Divorce

|

One spouse said: “When they first told me I have to get a lawyer, I was

confused. You’re going through a divorce and you’re not thinking right, and

you’re like, ‘a lawyer?’ I was trying to figure out how I was going to do

this. Source: GAO interview. | GAO‑26‑107536 |

Whether a couple ultimately divorces also influences the effect on a spouse of a participant removing funds without their consent, including how the spouse discovers the event. One of the three spouses we spoke with said that she discovered after the divorce that her husband had removed retirement funds without her knowledge or consent. The other two spouses said they discovered during divorce proceedings that funds had been removed. Some stakeholders said participants occasionally remove funds without consent in anticipation of divorce, for example to pay for divorce lawyers.

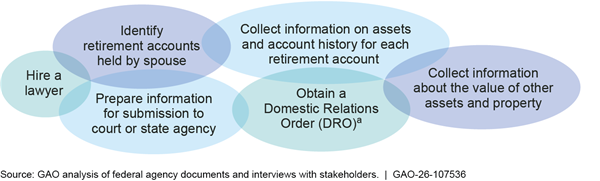

During divorce proceedings, spouses may take actions to legally regain a share of the funds the participant removed prior to divorce, though the effort is not always successful (see fig. 3).[54] For example, some stakeholders pointed out that not all divorcing individuals hire lawyers, in part because hiring a lawyer can be costly and not everyone knows about or has access to legal assistance programs. Some other stakeholders said that it can be difficult to locate funds, for example, if the participant does not disclose the existence of the account. One legal service provider said that most lawyers do not have the time and resources to track down assets that participants do not disclose. Once the spouse knows how much the participant took out of the retirement account, it may not be possible to compensate the spouse if the funds have already been spent and alternate funds are not available. For example, another legal service provider said that in households with many assets, the spouse’s loss can be offset by an alternate asset equal in value to the funds removed, but in households with few or no assets that may not be possible.

Figure 3: Illustration of Potential Actions to Regain Retirement Funds Taken Out Without Spouse’s Knowledge Prior to a Divorce

aA DRO is a judgment, decree, or order that includes the approval of a property settlement made pursuant to state domestic relations law. It relates to marital property rights for the benefit of a spouse, former spouse, child, or other dependent of a participant. A DRO can be sought without the existence of a divorce proceeding. While a DRO may be contained in a property settlement, it needs to be submitted to the plan administrator of the retirement account and be determined to be a Qualified Domestic Relations Order to secure funds from a retirement account.

|

One spouse said: “I work full time and don’t have a lot of time to go to court to get the money.” Source: GAO interview. | GAO‑26‑107536 |

A Qualified Domestic Relations Order is a court order to divide retirement assets in a divorce. Two record keepers we spoke with said they may pause the ability of participants to remove retirement funds when they are notified that a participant is divorcing. This prevents the participant from removing assets that might be divided in the divorce. They said this pause is temporary unless a Qualified Domestic Relations Order is put in place. Few divorcing parties seek and obtain Qualified Domestic Relations Orders, according to plans and record keepers we spoke to for a report published in 2020. We reported that this is in part because Qualified Domestic Relations Orders can be costly and people may not know what they are or how to obtain one.[55]

|

One spouse said: She had obtained a divorce but not a Qualified Domestic Relations Order to divide the funds in her ex-husband’s defined contribution account. Regarding the division of funds, her husband said, “Don’t worry about it, you’ll get it, you’ll get it.” But then, she said, he drained his account. Source: GAO interview. | GAO‑26‑107536 |

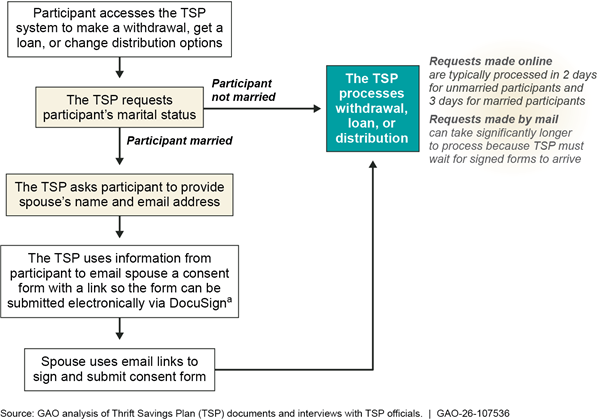

Even if divorcing parties seek such an order, spouses may not have complete information to ensure the order is processed quickly and correctly. For example, some legal service providers said spouses did not know the whereabouts of the retirement funds or have enough information to complete the process quickly. As a result, they said, some participants removed retirement funds before the order was in place to divide funds with the spouse. In 2020, we recommended the Department of Labor take steps to ensure that information regarding the requirements for these orders is available and easily accessible for retirement plan participants and their spouses.[56] The agency agreed with our recommendation. In 2025, the Department of Labor published new guidance that provides tips to help divorcing parties understand the process for obtaining a Qualified Domestic Relations Order to divide retirement assets.[57] Figure 4 illustrates the process to obtain a Qualified Domestic Relations Order.

aThe plan administrator will promptly notify the participant and all alternate payees of the DRO and provide a copy of the plan’s procedures for determining whether a DRO is qualified. A Qualified Domestic Relations Order (QDRO) is a DRO that creates or recognizes the existence of another’s (spouse, former spouse, etc.) right to receive or assigns all or a portion of the benefits payable to a participant under a retirement plan.

bThe plan administrator will notify the participant and interested parties of the determination. No withdrawals are allowed for up to 18 months while the determination is being made, according to the Department of Labor.

Stakeholders Said Additional Spousal Consent Requirements Could Increase Safeguards for Spouses but Could Have Adverse Effects on Plans and Participants

Additional Spousal Consent Requirements May Increase Financial Safeguards and Transparency for Spouses

Additional spousal consent requirements could increase financial safeguards for spouses by enabling the spouse to withhold consent for the participant to remove funds, according to some stakeholders representing a range of retirees, plan sponsors, or record keepers we interviewed. Such requirements may protect the spouse from the plan participant’s unilateral decision-making, which is similar to provisions guaranteed by the REA. In passing the REA, lawmakers noted that “a spouse should be involved in making choices with respect to retirement income on which the spouse may also rely.”[58] In 2025, the American Academy of Actuaries noted that unilateral decisions by a participant could jeopardize the spouse’s future retirement security.[59]

|

Glossary of Terms · Plan sponsor: The plan sponsor is the employer in the case of an employee benefit plan established or maintained by a single employer. · Record keeper: A record keeper is a service provider that maintains systems, referred to as recordkeeping platforms, to account for contributions to and distributions from the plan, among other services. Source: GAO analysis of agency and stakeholder documents. | GAO‑26‑107536 |

A married individual’s financial security in retirement depends on both their own savings behavior and financial decision-making as well as that of their spouse. As we reported in 2024, financial decision-making, including retirement savings behavior, is important to ensure the financial health and stability of individuals and families.[60] Additionally, we reported in 2020 that women’s financial security is linked to their household where resources are shared among household members.[61]

Spousal consent requirements may increase financial safeguards particularly in divorce proceedings, according to a legal stakeholder. As noted above, two legal stakeholders recounted instances of clients’ spouses removing funds or liquidating their plan account without the knowledge of their spouse during a divorce proceeding. Spousal consent requirements may also protect against the removal of funds that may affect marital assets as well as potentially avoiding additional legal expenses to identify and locate secreted assets for the purpose of the divorce settlement.

Spousal consent requirements to remove funds from all types of defined contribution plans, including 401(k) accounts, could further increase transparency of retirement finances for spouses, according to stakeholders from national organizations representing retirees and women, and multiple legal stakeholders. For example, such requirements may ensure that spouses are aware of any loans and withdrawals that could affect their retirement security, according to officials at the TSP. It may also aid nonworking spouses who are unaware of their spouse’s account balances, a record keeper said.

Private sector plans not subject to the REA can decide to voluntarily include spousal consent provisions in their plan to further protect employee retirement benefits, according to some stakeholders. For example, a representative from a large record keeper noted they offer all their clients—employers that sponsor retirement plans—the option to include spousal consent provisions. However, they said that only a few plan sponsors have voluntarily included spousal consent protections in their plans. Most plans that include spousal consent requirements are legally required to do so because of the type of plan they offer, according to two large record keepers.

A legal stakeholder we spoke with said when establishing their 401(k) retirement plan for their firm, they decided to voluntarily include spousal consent requirements. Their plan requires spousal consent for all transactions. They noted that spousal consent requirements could help to protect their plan and financial institution since the documentation required for spousal consent can prevent them from getting subpoenaed in the case of a plan participant’s divorce. They see the inclusion of spousal consent requirements for all transactions as beneficial to protect themselves and their employees’ spouses.

Spousal Consent Requirements May Increase Costs and Delay Processing Time for Both Participants and Plans

Some stakeholders also cited potential adverse effects of additional spousal consent requirements, including that they may increase administrative burdens and costs for plans.

Potential for Increased Administrative Burdens and Plan Costs

Requiring spousal consent for all 401(k) plans when a participant requests to remove funds may increase administrative burdens and costs for plan sponsors and record keepers, according to retirement industry stakeholders. Specifically, plan sponsors and record keepers may need to complete additional administrative tasks that carry additional costs to implement the requirements associated with spousal consent. Some stakeholders said plans may need more staff to manage transactions and verify compliance with spousal consent requirements. Additionally, all affected plans would need to change plan rules and notify participants of the changes, noted one stakeholder. These costs may be passed on to plan participants, they said.

Adding spousal consent requirements for all 401(k) plans may increase costs, particularly for small employers, according to representatives of two national organizations representing plan sponsors. For example, a large plan sponsor or record keeper can spread the costs across a larger number of participants. However, the cost increases could be expensive for smaller plan sponsors that have less ability to absorb the cost increases and fewer participants to spread the cost among, according to representatives of two national stakeholder organizations representing plan sponsors.

Yet, two record keepers who implement spousal consent requirements for numerous retirement plans of various sizes said the process is not overly difficult. One said it provides recordkeeping services to plans with and without spousal consent requirements and does not need a different record keeping system for these plans. They said they did not face any challenges or increased burden to provide spousal consent services to these clients, as their record keeping system is the same for all clients. Only the process is different.

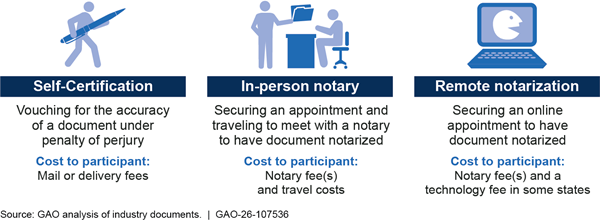

Extra Time to Process Participants’ Requests to Remove Funds

Spousal consent requirements in defined contribution plans may delay the receipt of funds by plan participants, according to some industry association representatives and a record keeper we interviewed. For example, plans may need additional time to determine marital status or obtain notarized consent from the participant’s spouse, according to some stakeholders.