Report to Congressional Committees

United States Government Accountability Office

A report to congressional committees

For more information, contact: Danielle T. Giese at GieseD@gao.gov or Michael Hoffman at HoffmanME@gao.gov

What GAO Found

Empirical studies assessing the effects of domestic airline mergers generally found that, in the short run, consumers faced higher fares and lower service quality (e.g., on-time performance) on routes where the merger resulted in fewer competitors. For example, based on three studies that used particularly strong methodologies, fares increased between 1 and 8 percent following the merger. Other studies found mergers sometimes led to some improvements in airlines’ efficiencies (e.g., cost reductions), but challenges, such as combining workforces, sometimes reduced or eliminated anticipated gains.

GAO’s analyses of airline competition metrics provide a longer-term perspective than the studies and suggest that there has been increased competition in the past two decades. For example, estimated domestic fares that incorporated available airline ancillary fees were lower in 2024 as compared to 2007—even after they were higher in 2012, around the time of a wave of domestic airline mergers. In addition, market share and other key market structure indicators show increased presence of ultra-low-cost airlines in 2022 compared to 2007. These indicators remained largely unchanged from 2022 through 2024.

Note: GAO divided domestic routes into five “quintiles” (based on number of passengers), where the first quintile generally includes the most-travelled routes, and the fifth generally includes the least.

Stakeholders identified five key factors that affect airline competition, including airport access and introduction of basic economy fares by network airlines. Most stakeholders GAO interviewed described intense competition in an uneven environment, posing challenges for lower-cost airlines going forward. They also pointed to a relatively recent development: the increasing importance of airline credit card revenue. This helps airlines weather industry volatility, while also bolstering passenger loyalty by providing rewards (e.g., seat upgrades). Some stakeholders said these cards provide competitive advantages for larger airlines because consumers are less attracted to cards offered by lower-cost airlines, which generally have smaller operations and reward programs.

Why GAO Did This Study

Domestic airlines carried nearly 850 million passengers throughout the U.S. in 2025, according to Department of Transportation (DOT) data. Robust competition in the air transportation industry can promote lower fares and provide consumers with more travel options and destinations. Some observers, however, have raised questions about the effects of mergers, suggesting that consumers may ultimately face higher airfares and reduced service.

The FAA Reauthorization Act of 2024 includes a provision for GAO to review competition and consolidation in the U.S. airline industry. This report examines (1) findings from empirical studies since 2005 on the effects of U.S. airline mergers on consumers and on airlines’ efficiency, (2) the current state (2022-2024) of airline competition in the U.S. compared to 5, 10, and 15 years prior, and (3) stakeholders’ views on the factors affecting the evolution of competition in the U.S. airline industry.

GAO summarized the findings of 40 empirical studies with sufficiently rigorous methodologies that assessed the effects of U.S. airline mergers. Of those, GAO found 13 studies particularly robust and reported quantitative effects that are statistically significant. GAO also analyzed airline data collected by DOT to examine U.S. airline competition over time.

GAO interviewed or obtained written responses from all 12 major U.S. airlines and 19 other knowledgeable stakeholders, including academic researchers, consumer advocacy groups, and equity analysts. GAO selected stakeholders based on its prior work, recommendations from others, and the stakeholders’ knowledge of the U.S. airline industry. GAO also interviewed officials from DOT and the Department of Justice.

|

Abbreviations |

|

DB1B Department of Transportation Origin and Destination Survey |

|

DOJ Department of Justice |

|

DOT Department of Transportation |

|

EDIFACT Electronic Data Interchange for Administration, Commerce and Transport |

|

FAA Federal Aviation Administration |

|

HHI Herfindahl-Hirschman Index |

|

NDC New Distribution Capability |

|

QSI Quality of Service Index |

This is a work of the U.S. government and is not subject to copyright protection in the United States. The published product may be reproduced and distributed in its entirety without further permission from GAO. However, because this work may contain copyrighted images or other material, permission from the copyright holder may be necessary if you wish to reproduce this material separately.

June 25, 2026

The Honorable Ted Cruz

Chairman

The Honorable Maria Cantwell

Ranking Member

Committee on Commerce, Science, and Transportation

United States Senate

The Honorable Sam Graves

Chairman

The Honorable Rick Larsen

Ranking Member

Committee on Transportation and Infrastructure

House of Representatives

In 2025, U.S. airlines carried nearly 850 million passengers domestically and generated over $250 billion in operating revenues from those flights, according to Department of Transportation (DOT) data.[1] Nearly 90 percent of Americans reported having flown in their lifetime, while more than 50 percent reported flying in 2024, according to Airlines for America, an airline industry association. Airlines compete for those passengers through fares as well as non-price strategies, such as reliability, loyalty programs, and other service offerings, like airport lounges.

The current U.S. airline industry reflects a significant transformation in response to numerous challenges and shocks experienced over several decades. For example, in the aftermath of the September 11, 2001, terrorist attacks and the financial crisis and economic recession of 2007 to 2009, the industry experienced heavy financial losses that contributed to a wave of bankruptcies and drove consolidation through several major airline mergers. From 2008 through 2013, eight airlines consolidated to become four airlines. As a result, there are fewer major U.S. airlines today than at any time since deregulation in 1978. Following the wave of mergers and acquisitions, lower-cost airlines (i.e., “low-cost” and “ultra-low-cost” airlines) contributed to growth, and the industry experienced several years of profitability. Following the COVID-19 pandemic, however, domestic airlines have faced increased labor and other costs. Lower-cost airlines, which rely on lower operating costs to charge lower fares, have been particularly hard hit.

Some observers have raised questions about the effects of mergers and acquisitions (hereafter referred to simply as “mergers”) on airline competition, suggesting that consumers may ultimately face higher airfares and reduced service. Others, including representatives from several airlines that have merged, argue that airlines and consumers can benefit from consolidation, as merging airlines expand their networks and gain efficiencies through workforce integration, information technology system integration, and other synergies. The Department of Justice (DOJ) and DOT have stated that robust competition in the air transportation industry promotes lower fares; improves working conditions; and enhances the ability of Americans to travel, whether for business or leisure.

We last reported on competition in the airline industry in 2014, shortly after the last wave of mergers.[2] The FAA Reauthorization Act of 2024 includes a provision for us to study competition and consolidation in the U.S. airline industry.[3] While the regional airline industry sector has also experienced consolidation over the last two decades, this report focuses on consolidation among the major airlines. This report examines (1) findings from empirical studies since 2005 on the effects of U.S. airline mergers on consumers and on airlines’ efficiency, (2) the current state (2022 through 2024) of airline competition in the U.S. compared to 5, 10, and 15 years prior, and (3) stakeholders’ views on the factors affecting the evolution of competition in the U.S. airline industry.

To examine studies’ findings on the effects of U.S. airline mergers, we identified and reviewed empirical economic studies that assessed the effects of one or more of the six domestic airline mergers completed from 2005 through 2016. We identified and reviewed 143 economic studies relevant to our review. Of those, we selected 40 empirical studies that assessed merger effects and had sufficiently rigorous methodologies. We determined that 13 of those 40 studies had particularly robust methodologies (hereafter referred to as “particularly strong studies”).[4] We reported quantitative effects that are statistically significant from these particularly strong studies and qualitatively described the results from the other studies.

To examine airline competition in the U.S. over time, we used several metrics, such as airfares and market concentration, to compare the current state of the domestic airline industry (2022 through 2024) to prior selected years (2007, 2012, and 2017).[5] Analyzing metrics for 2007 and 2012 provides information before and after several large mergers in our review, while 2017 provides a data point prior to the COVID-19 pandemic. We calculated these metrics using data collected by DOT from airlines and processed by a private data vendor, including air traffic, fares, and origin and destination ticket data. To assess the reliability of the data, we reviewed the quality control procedures that DOT and the private data vendor used. We also conducted electronic data testing for missing data and outliers. We determined the data were sufficiently reliable for the purpose of comparing the state of the airline industry in various years.

To examine stakeholders’ views on the factors affecting the evolution of competition in the U.S. airline industry, we reviewed the more than 100 comments submitted by stakeholders in response to DOJ and DOT’s October 2024 request for information on competition in the airline industry and in other segments of the air transportation industry.[6]

In addition, to address all three objectives, we reviewed relevant federal laws, regulations, and agency documentation related to airline competition and consolidation in the U.S. aviation industry. We also identified and reviewed studies that assessed topics related to the current state of airline competition or airline competition in general. We interviewed DOT and DOJ officials and representatives from all 12 major U.S. airlines.[7] We also interviewed 19 other relevant stakeholders, including representatives from industry trade associations, consumer advocacy groups, and a technology firm; equity analysts from financial services firms; and academic researchers. We identified and selected these stakeholders based on our prior work, a literature review of relevant academic research, and the stakeholders’ knowledge in their field. The interviews were conducted from October 2024 to January 2026. Their views are not generalizable to the views of all industry stakeholders but provide a range of perspectives on competition in the industry. See appendix I for more details on our scope and methodology.

We conducted this performance audit from August 2024 to June 2026 in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

Background

U.S. Airlines and Other Key Stakeholders

The domestic passenger airline industry is generally composed of four types of airlines. However, given the dynamic nature of the industry and airlines’ individual business models, an airline may not perfectly fall into a single category across all years and for all purposes.[8] For the purposes of this report, we use the following four categories that are reflective of their different business models, service levels, fare structures, and target markets.

· Network airlines were in operation before the Airline Deregulation Act of 1978 and support large, complex hub-and-spoke operations with thousands of employees and hundreds of aircraft.[9] These airlines provide service at various fare levels to a wide variety of domestic and international destinations.

· Low-cost airlines generally entered the market after deregulation and tend to operate less costly point-to-point service using fewer types of aircraft than network airlines.[10] While low-cost airlines serve international markets, they focus more heavily on domestic markets than do network airlines.

· Ultra low-cost airlines provide service often to leisure destinations at discount fares, but with ancillary fees, such as for carry-on and checked baggage.[11]

· Regional airlines generally operate smaller aircraft (up to 76 seats) and provide service to smaller communities through arrangements with network airlines. Some regional airlines are owned by a network airline, while others are independent.

Although not considered part of the airline industry, other key aviation stakeholders support how consumers purchase airline tickets. Specifically, consumers can purchase airline tickets for airline travel directly from the airline (i.e., from the airline’s website, by calling the airline’s call center, or from the airline’s ticket counter at the airport) or from third parties, such as online travel agents (e.g., Priceline or Expedia) and traditional or corporate travel agents. Prior to purchase, consumers may obtain some information about flight schedules, fares, and some optional services—including checked baggage, seat selection, and reservation changes or cancellations fees—from metasearch companies (e.g., Kayak or Skyscanner). Generally, online travel agents, traditional or corporate travel agents, and metasearch companies obtain fare and some optional service fee information from global distribution systems, which are companies that package airline information so that travel agents can query and “book” (i.e., reserve and purchase) flights for airline customers.

Financial Performance of the U.S. Airline Industry

The airline industry has historically operated with volatile earnings and is also highly susceptible to business cycles and other external shocks that reduce demand. As discussed above, the September 11, 2001, terrorist attacks and the financial crisis and economic recession of 2007 to 2009 were among the external shocks that impacted the U.S. airline industry and contributed to the wave of airline consolidations.

Since we last reported on competition in the U.S. airline industry in 2014, the industry experienced a period of unprecedented stability and profitability through 2019, according to DOT’s Federal Aviation Administration (FAA). According to DOT officials, during this time, lower-cost airlines had cost advantages over other airlines. These officials further explained that this created a cycle of growth that enabled lower fares, which stimulated air travel demand, leading to high aircraft utilization and profitability, and further reduced costs.

This period of sustained strong financial performance was disrupted in early 2020 by the COVID-19 pandemic. Collectively, the U.S. airline industry lost billions in 2020 and 2021, as air passenger demand plummeted to historic lows.[12] Domestic passenger traffic was 96 percent lower in April 2020 than in April 2019, with traffic in 2021 remaining 25 percent below traffic in 2019, according to DOT data.

From 2022 through 2024, the industry rebounded from the losses incurred during the pandemic, with total operating revenue exceeding pre-pandemic levels. However, the recovery has been uneven, with several airlines posting annual net losses, according to financial filings by the airlines.[13]

The airline industry also is facing significant cost and operational challenges. For example, according to Bureau of Labor Statistics data, the real annual median wage for airline pilots, copilots, and flight engineers was 31 percent higher in 2023, compared to 2017.[14] Our 2024 and 2025 reports discussed other challenges affecting the U.S. airline industry, including air traffic controller shortages, airspace congestion, and difficulty obtaining new aircraft and parts. We reported that these challenges could lead to delayed or cancelled flights or airlines reducing their numbers of scheduled flights.[15]

Merger Activity in the U.S. Airline Industry

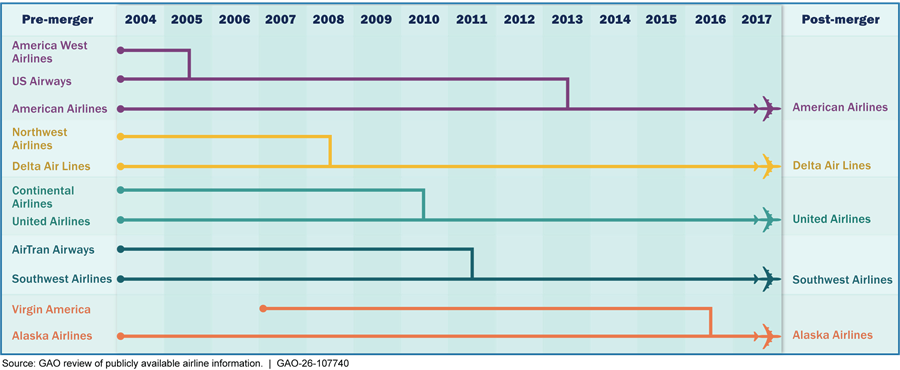

From 2005 through 2016, the U.S. airline industry experienced considerable merger activity. By 2013, six network and three low-cost airlines had consolidated, forming what is now commonly referred to as the “Big Four” airlines, while another major merger between Alaska Airlines and Virgin America closed in 2016 (fig. 1).

Note: For the purposes of this report, the year of each merger reflects the publicly announced date the merger or acquisition closed.

Several airlines have also pursued mergers in recent years. In 2024, a federal judge blocked a proposed acquisition of Spirit Airlines by JetBlue Airways, finding that it would likely result in less competition, impacting prices and innovation, and likely hurt consumers. Later in 2024, Alaska Airlines acquired Hawaiian Airlines.[16] And, on May 13, 2026, Allegiant Air completed its acquisition of Sun Country Airlines.[17]

Airlines may seek to merge to improve their strategic position by, for example, expanding route networks and combining fleets and loyalty programs. Airlines often anticipate benefits from a merger, such as increased revenues from expanding their networks and increased market shares, and cost savings, such as from combining complementary assets and reducing or eliminating duplicative activities, such as management and administrative functions. Several airlines involved in mergers in the 2000s and 2010s publicly reported that the proposed merger could provide benefits, with estimates in revenue synergies ranging from $175 million annually to $2 billion annually.[18] To the extent a merged airline realizes these benefits, they could benefit not only the airline, but also consumers if the airline passes cost savings to consumers through lower fares or improved service.

How Mergers Can Change the Structure of Competition Among Airlines

To evaluate the extent of competition among airlines, researchers and DOJ typically measure competition at the market level (i.e., travel between two cities, or “city-pair” route), instead of the national or global network level.[19] Mergers can affect fares and service quality on different routes when a merger results in the elimination or entry of a competing airline.

When a merger eliminates a competitor on a route, the merged airline could have more market power to raise fares and service quality may decline. In addition, consumers have fewer choices. A direct competitor is eliminated on a route when, before the merger, both merging airlines provided service on the same route (referred to as an “overlap” route), and, after the merger, only the merged airline provided service. A potential competitor is eliminated when one of the merging airlines operated a route pre-merger, and the other merging airline had a presence in at least one of the two airports on that route, which would have made it easier for that airline (the potential competitor) to have entered the route.

In contrast, when an airline enters a route, competition may increase on that route and spur lower fares and improved service quality. The entry airline can be the merged airline, which enters a route following a merger when it begins operating on a route that neither of the merging airlines operated prior to the merger.

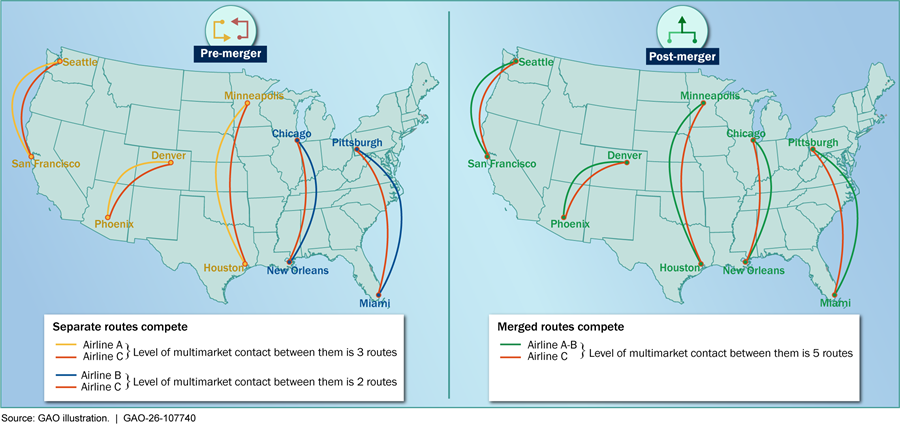

Mergers can also increase the level of multimarket contact between airlines. Multimarket contact describes conditions when airlines compete with the same rival airlines on multiple routes. Multimarket contact may increase following a merger, especially if the merging airlines had few overlap routes prior to the merger (see fig. 2). This occurs because, instead of a rival airline competing separately on a set of routes with each of the pre-merger airlines, the rival airline may now compete with the merged airline on many more routes served by the merged airlines. Multimarket contact can influence incentives to compete aggressively on certain routes if a rival airline has more opportunities to retaliate on other routes. Further, increased multimarket contact can increase the risk of airlines coordinating on fares and capacity, according to DOJ officials, which could lead to higher fares and lower capacity.

On the other hand, as discussed above, mergers may result in increased efficiency and cost reductions for the airline, which could lead to lower fares and better service quality. The net effect of mergers in practice will depend on a number of factors, including any changes in airlines’ market power and the extent of efficiency gains, if any.

Federal Agencies’ Roles

Two federal agencies—DOJ and DOT—play key roles in promoting and evaluating competition in the U.S. airline industry, including DOJ’s role in allowing mergers to proceed or suing to block them, and DOT’s role in ensuring safe and efficient access across the air transportation system.

DOJ has the lead role in reviewing proposed mergers and acquisitions in the airline industry, given its statutory authorities to enforce U.S. antitrust laws. In carrying out its antitrust responsibilities, DOJ examines whether the effect of any consolidation of two airlines “may be substantially to lessen competition or tend to create a monopoly” in violation of the Clayton Act, as amended.[20] If so, DOJ may sue to block a merger.[21]

DOJ principally uses the analytical framework established in the Merger Guidelines to analyze whether a proposed merger or acquisition involving actual or potential competitors raises antitrust concerns.[22] As part of its analysis, DOJ considers several potential effects of a proposed merger, including effects on market concentration, barriers to entry, and merger-specific airline efficiencies.[23] For example, DOJ typically uses the Herfindahl-Hirschman Index (HHI) to assess whether a merger is likely to significantly increase concentration and raise anti-competitive concerns in the relevant markets.[24] Depending on the airlines involved, the relevant markets are often considered origin and destination (also referred to in the industry as “city-pair”) routes operated by the merging airlines.[25]

DOT also conducts analyses of the merits of any airline merger and acquisition and submits its views and provides its subject matter expertise in advising DOJ. DOJ and DOT may seek certain concessions from the merging airlines to ensure the competitiveness of the market for the benefit of the consumer.[26] Concessions may include divesting (i.e., giving up) gates or takeoff and landing slots at certain airports, as well as maintaining service on routes serving small communities.

When seeking to merge, airlines typically provide estimates of anticipated benefits of the proposed merger to DOJ and DOT. According to the 2023 Merger Guidelines, agencies conducting merger reviews examine whether the evidence presented by the merging parties shows the merger will produce substantial competitive benefits that could not be achieved without the merger, benefits are verifiable and have been verified using reliable methodology and evidence, benefits will prevent the risk of a substantial lessening of competition, and benefits are not anticompetitive.[27] According to the guidelines, however, such benefits are often difficult to quantify and verify.

Separate from examining individual proposed mergers, DOT considers a range of related issues, including international route transfers, economic fitness, and code-sharing (an agreement whereby carriers place their marketing code on a flight operated by another carrier).[28] In addition, DOT has statutory authority to investigate and address unfair or deceptive practices or unfair methods of competition by airlines.[29] DOT also monitors fundamental changes in the industry, analyzes industry trends, and assesses factors related to competitive air service, such as perceived barriers to entry or expansion at airports. For example, certain airports must maintain an FAA-approved Competition Plan demonstrating the availability of the necessary infrastructure, such as gates and related facilities, and how it will accommodate new or expanding service.

Studies Generally Found That, in the Short Run, Mergers Increased Fares on Routes Where the Number of Competitors Decreased and Had Inconsistent Effects on Merged Airlines’ Efficiencies

Empirical studies we reviewed and found methodologically rigorous generally concluded that mergers, in the short run, led to higher fares and lower service quality (e.g., worse on-time performance or more cancelled flights) for consumers on routes where the number of competitors decreased, and lower fares and improved service quality on routes where a merged airline entered following a merger. In addition, some of these studies found that mergers resulted in some improvements in airlines’ efficiencies, but challenges associated with merging the airlines, such as combining workforces, sometimes led to reduced or no efficiency gains.[30]

The 40 studies did not evaluate efficiency gains realized by those mergers, if any, against those projected by the merging airlines, in part due to the lack of proprietary cost data that is available to researchers. Further, these studies are generally designed to draw conclusions about merger effects on a subset of routes, not about the overall competitive effects of specific mergers. Since the overall industry-wide competitive effects of a merger would require an assessment of all routes and all players in the industry, researchers would have to construct an alternative scenario (counterfactual) of what the airline industry would have looked like had the merger not happened. Such counterfactuals are challenging to quantify and require various assumptions that could affect the result of such an analysis. As such, researchers on this topic generally focus on a subset of routes affected by the merger, which have a plausible counterfactual in real world data. To characterize the degree of competition over time and to provide additional evidence on how competition evolved after the wave of airline mergers, we present several metrics, such as airfares and market concentration, in the next section of this report.

Consumers Generally Faced Higher Fares and Decreased Service Quality in the Short Run on Routes Where the Number of Competitors Decreased

In general, studies found that mergers, in the short run, led to higher fares and lower service quality for consumers on routes where the number of competitors decreased, and lower fares and improved service quality on routes where the number of competitors increased. Twenty seven studies that met our criteria for inclusion evaluated the effects of individual U.S. airline mergers on consumer fares, service quality, or both.[31] These 27 studies sought to isolate and quantify the effects of one or more mergers from other factors that might have affected fares and certain aspects of service quality (e.g., on-time performance or number of cancelled flights) within a specified time frame (i.e., a few quarters to a few years) after the mergers.[32]

Effects on Fares

Of the 27 studies assessing merger effects on consumers, 12 studies assessed fares, including three studies that we determined had particularly robust methodologies (hereafter referred to as “particularly strong studies”). Nine of those 12 studies found that, in the short run, (1) fares increased on routes where the merger reduced the number of competitors, or (2) fares decreased on routes where a merged airline entered that route following a merger.[33] These 12 studies specifically examined or used data from the time period encompassing five of the six mergers in our review: Delta Air Lines / Northwest Airlines, United Airlines / Continental Airlines, Southwest Airlines / AirTran Airways, American Airlines / US Airways, and Alaska Airlines / Virgin America.[34]

Fares on Routes Where a Direct or Potential Competitor Was Eliminated

Eight of the 12 studies, including three particularly strong studies, found that, on average, fares increased on routes when a merger eliminated a direct competitor.[35] The three particularly strong studies found that fares increased between 1 and 8 percent following a merger, comparing fares across time frames ranging from 1 to 4 years before the merger to 1 to 4 years following the merger, depending on the individual study’s methodology (see table 1).

Table 1: Price Effect of Mergers on Routes Operated by Both Airlines (Overlap Routes) from Empirical Studies GAO Determined to Be Particularly Strong

|

Study |

Merger |

Estimates of price increase range |

Number and type of overlap routes |

Time frame |

|

1 |

United Airlines / Continental Airlinesa |

7.8 to 8.3 percentb |

9 nonstop overlap routes |

Pre-merger: 4 years before merger announcement (2006Q1–2010Q1). Post-merger: 4 years since merger announcement (2010Q2–2013Q4). |

|

2 |

Southwest Airlines / AirTran Airwaysc |

2.1 to 5.3 percentd |

104 nonstop and connecting overlap routes |

Pre-merger: 1 year before DOJ announced the closing Post-merger: 1 year after full integration (2014Q2–2015Q1). |

|

3 |

Delta Air Lines / Northwest Airlinese |

0.2 to 1.8 percentf |

More than 4,000 connecting overlap routes |

Pre-merger: 2 years before merger announcement (2006Q1–2008Q1). Post-merger: 2 years after merger closed (2009Q2–2011Q4). |

Source: GAO review of selected empirical studies. | GAO‑26‑107740

Note: GAO determined these studies to be particularly strong because they adopted a strong causal research design, such as a research design that included the most appropriate control group.

aYing Shen, “Market competition and market price: Evidence from United/Continental airline merger,” Economics of Transportation, vol. 10 (2017): 1–7.

bThe price increase range is derived from different regression specifications.

cHuubinh B. Le, “An Empirical Analysis of the Price and Output Effects of the Southwest/AirTran Merger,” Competition and Regulation in Network Industries, vol. 17, no. 3–4 (2016): 226–240.

dThe price increase range represents the 95 percent confidence interval of the point estimate of 3.7 percent. Unless otherwise noted, the confidence intervals for studies cited in this report were calculated by GAO economists using the point estimates and standard errors presented in the studies. Two other studies also found an increase in price of the overlap routes between Southwest and AirTran. See Alexander McGlothlin, “Mavericks and mergers in concentrated markets,” (Nov. 20, 2019), https://ssrn.com/abstract=3490329; and Pukar KC, “Three Essays in Applied Economics: Topics in Transportation, Industrial Organization and Health Economics, Chapter 2– Higher Together: Price and Welfare Effects of a Merger between two Low Cost Carriers,” PhD diss. (Northeastern University, 2018).

eAditi Mehta and Nathan H. Miller, “Choosing the Appropriate Control Group in Merger Evaluations,” More Pros and Cons of Merger Control, Swedish Competition Authority, 2012.

fThe price increase range represents the 95 percent confidence interval of the point estimate of 1 percent.

Four of these 12 studies, including one particularly strong study, also assessed effects on fares for routes where a merger eliminated a potential competitor and found that, on average, fares increased.[36] For example, the particularly strong study compared fares 1 year before DOJ announced the closing of its investigation into the Southwest Airlines and AirTran proposed acquisition to 1 year after the airlines fully integrated their operations.[37] It found that fares increased both on routes where Southwest Airlines was eliminated as a potential competitor (4.3 to 8.9 percent increase), and on routes where AirTran Airways was eliminated as a potential competitor (2.0 to 4.5 percent increase).[38]

Four of the studies that assessed the effects on fares when a merger eliminated a direct competitor found that, on average, fares decreased, had mixed effects, or did not change post-merger.[39] The variation in findings may be explained by the different time frames analyzed or different definitions of the pre- and post-merger period.[40]

Fares on Routes Where a Merged Airline Entered Following a Merger

Of the three studies that assessed the effects on fares for routes where the merged airline entered, two found that fares, on average, decreased.[41] Of these two, one study, which analyzed fares on 128 routes that Southwest Airlines entered after its merger with AirTran Airways, was a particularly strong study. This study found that, following the entry of the merged airline, fares decreased by 3 to 9 percent, on average, 1 year following the merger when compared to 1 year prior to the merger.[42] The third study—which we did not identify as particularly strong— found mixed effects, either evidence of decreased fares or no evidence of fare changes, depending on different regression models used.[43]

Effects on Service Quality

Of the 27 studies assessing merger effects on consumers, seven studies assessed certain aspects of service quality, such as flight frequency, on-time performance, duration of flight delays, or number of cancelled flights. Six of the seven studies—including five particularly strong studies—found that, in the short run, service quality 1) declined on routes where a competitor was eliminated or 2) improved on routes where the merged airline entered. One study—which we did not identify as particularly strong—found effects differed depending on the time frame analyzed. These seven studies examined four of the six mergers in our review.[44]

Service Quality on Routes Where a Competitor Was Eliminated

Two of the three studies that assessed routes where a direct competitor was eliminated—including one particularly strong study—found that service quality declined. The third study—which we did not identify as particularly strong—found mixed results.[45] These three studies analyzed service quality in terms of routing quality (e.g., availability of nonstop flights versus connecting flights), on-time performance, and flight frequency. They compared differences in service quality over time frames ranging from 3 quarters of a year to 5 years before or after the merger.[46]

The particularly strong study found that on routes United Airlines and Continental Airlines competed on pre-merger, the number of passengers flying nonstop decreased by about 1.1 percent in the 3-year period following their merger.[47] The same study found that on routes Delta Air Lines and Northwest Airlines competed on pre-merger, the percentage of passengers flying nonstop decreased by about 1.4 percent in the 5-year period following their merger.[48] According to the study, these declines could be explained by the merged airlines eliminating or reorganizing hubs following the merger.

Three other particularly strong studies found that service quality declined when market concentration increased at different points in time during the wave of airline mergers.[49] More specifically, the studies found the following:

· If market concentration meaningfully increases, the duration of arrival delays would increase by approximately 2 to 5 minutes, and the probability of airline-caused flight delays of at least 15 minutes would increase by 1.3 to 4.9 percentage points.[50]

· When the number of competitors decreased from three to two in a market, the average delay length increased by 25 percent, and the flight cancellation rate increased by 7 percent.[51]

· If two hypothetical equal-sized competitors, each with a market share of 40 percent merge with each other, the merger would lead to an estimated increase in the average arrival delay of approximately 3 to 5 minutes. Also, an increase of 10 percent in market concentration would be associated with a 0.07 to 0.17 percent increase in the cancellation rate.[52]

Service Quality on Routes Where Merged Airline Entered Following a Merger

The one particularly strong study that assessed service quality on routes after a merged airline’s entry found that, on average, service quality improved.[53] Specifically, this study found that the length of arrival delays decreased by 11 to 29 percent, and the length of departure delays decreased by 4 to 10 percent, on average, within 3 years after the merger.[54] This study assessed four mergers using data from 1993 to 2013 and compared the number of arrival delays and departure delays between 2 years prior to each merger announcement and up to 3 years following each merger.[55]

Multimarket Contact

Nine additional studies, including three particularly strong studies that focused on multimarket contact, found that the level of multimarket contact increased post-merger and that higher levels of multimarket contact led to higher airfares and lower service quality. As previously discussed, multimarket contact describes conditions when airlines compete with the same rival airlines on multiple routes. Following a merger, multimarket contact may increase because, instead of a rival airline competing separately on a set of routes with each of the pre-merger airlines, it may now compete on many more routes served by the merged airline. Multimarket contact can reduce the incentives for an airline to compete aggressively on certain routes if a rival airline has more opportunities to retaliate.

Of the nine studies:

· Three studies—including two particularly strong ones—assessed the extent to which multimarket contact increased following a merger. One particularly strong study found that the level of multimarket contact increased by about 29 percent when comparing the level of contact 2 years post-merger with 2 years pre-merger.[56] The second particularly strong study analyzed the 1,000 largest routes by passenger volume from a time frame encompassing four major mergers and found that multimarket contact generally increased.[57]

· Seven studies—including three particularly strong ones—assessed the extent to which increased multimarket contact affected fares or service quality. All seven found that higher levels of multimarket contact led to higher airfares or lower service quality.[58] For example, one particularly strong study found that a 30 percentage point increase in multimarket contact resulted in a 6.5 to 14.5 percent increase in the least expensive fares and a 3.0 to 9.7 percent increase in the most expensive fares, respectively.[59] Another particularly strong study similarly found a 29 percent increase in multimarket contact, which resulted in airlines cutting flights by roughly 2 to 2.5 roundtrips per week, on average, for routes where they competed with either merging airlines pre-merger.[60] Two other studies found that increased levels of multimarket contact led to a reduction in the number of seats offered and increased flight delays.[61] However, one study found that the presence of Southwest Airlines mitigated the effect on fares of increased multimarket contact.[62] In addition, one particularly strong study found that, if multimarket contact was already very high, an increase in multimarket contact had little effect on fares.[63]

Effects on Small and Rural Communities

None of the 40 studies we selected for review assessed the effects of airline mergers on small and rural communities. In our interviews with stakeholders, some offered thoughts on why studies have not focused on the effects in these communities.[64] One academic researcher explained that because the available air traffic data on small markets are very limited, researchers may prefer to prioritize their resources on studying bigger markets that have more data. Another academic researcher we spoke with said that because these markets tend to be served only by one airline, they did not believe that mergers had much effect on these markets.

Some stakeholders we interviewed suggested airline mergers affected service quality for small and rural communities, but opinions of those effects differed. Some pointed to positive effects. For example, one academic researcher told us that, theoretically, mergers could have benefits for small and rural markets through the creation of larger networks that provided more connections to airlines’ hubs. Representatives from three network airlines told us that mergers have enabled them to expand service to small and rural communities in this way. However, two equity analysts and a consumer advocate told us that mergers had reduced service to some small communities because the merged airlines stopped using certain airports those communities connected to as hub airports. At the same time, they acknowledged that in some cases, even without the merger, it may not have been sustainable for the airlines to continue to serve those communities at the same level. For example, following the Delta Air Lines and Northwest Airlines merger, Memphis International Airport was no longer a hub airport for Northwest Airlines. One equity analyst explained that the small communities that used to have direct flights to Memphis International Airport were instead connected to Atlanta International Airport, which resulted in less frequent flights on larger aircrafts. And, while these two equity analysts explained that it would not be economically efficient for the merged airline to operate at both hubs, they and the consumer advocate recognized that the elimination of hubs can have detrimental effects on the communities and economies where those hubs were formerly located.

Several stakeholders we interviewed stated that the reduced service that many small and rural communities have seen in recent years did not result from mergers.[65] For example, one equity analyst and representatives from several airlines told us that the unfavorable economics of providing airline service to these communities, such as higher labor cost, led to the reduction.[66] Representatives from a lower-cost airline explained that an airline’s decision to operate in a smaller market is typically based on profitability, and if a small market is not profitable, airlines will not operate in that market without government subsidies. Representatives from two network airlines also pointed to the lack of suitable replacement aircraft for routes that were previously served almost exclusively by small turboprops or regional jets. According to representatives of one network airline, as of 2025, these small turboprops are no longer being produced, contributing to reduced service in small and rural communities. We discuss competition for routes serving small and rural communities later in this report.

Studies Found That Some Mergers Improved Fleet Optimization, While Challenges Integrating Operations Reduced Efficiency or Prevented Efficiency Gains

Three of the six studies assessing airline efficiencies found that mergers resulted in some efficiency gains for airlines when examining two common types of efficiencies: cost efficiencies and network efficiencies, such as improved fleet optimization (matching the right aircraft, in terms of size and fuel efficiency, to the right route). None of these three studies were among those we identified as particularly strong. Three other studies, including two particularly strong studies, found challenges associated with mergers that may reduce efficiency or prevent the realization of potential efficiency gains. These six studies examined five of the six mergers in our review. None of the studies, as previously noted, evaluated efficiency gains achieved by those mergers, if any, against those projected by the merging airlines.

Specifically, three of six studies found that a merger resulted in at least some gain in network or cost efficiencies, including reduced fuel consumption, improved fleet utilization, and cost reductions.[67] For example, one study found evidence that two different merged airlines were able to operate larger aircraft with reduced frequency from hubs, resulting in more efficient operations and fuel consumption savings.[68]

In addition to the studies, representatives we spoke to from several network and lower-cost airlines, as well as equity analysts, told us that mergers have resulted in cost and network efficiencies, such as cost savings by eliminating redundancies and more efficient fleet utilization post-merger. For example, representatives from Southwest Airlines told us that after the merger with AirTran, Southwest moved some of AirTran’s aircraft to locations where they could be more efficiently operated and enter more international markets. By doing so, Southwest Airlines representatives said they could lower prices in those markets, which also benefited consumers.

The three studies that discussed challenges (e.g., consolidating workforces, capital, and technology systems) found that challenges that a merged airline faced after the merger either 1) reduced efficiency compared to before the merger, as measured by decreases in on-time performance, or 2) prevented the realization of potential efficiency gains.[69] Of the three studies:

· One particularly strong study examined the effects that merger-related challenges, such as integrating labor contracts, had following three different mergers and found that those challenges reduced the merged airline’s on-time-performance.[70] Specifically, the challenges resulted in an increase in the average minutes of delays for the three merged airlines by 0.52, 0.37, and 1.05 minutes (or, 16 percent, 11 percent, and 34 percent of the industry average delays of about 3 minutes) in the 2 years after the merged airlines integrated their operations as compared to 3 years prior to that integration.[71] For two of the mergers, the study found that the increase in delay generally faded away over the course of roughly 2 years.[72]

· The second particularly strong study examined four different mergers and found that both United Airlines and Southwest Airlines faced substantial integration costs, so much so that the mergers reduced productive efficiency. The study also found the four mergers on average did not result in efficiency gains when comparing traffic and financial data in each quarter up to 2 years prior to each merger closing and 4 years after the mergers.[73]

Airlines anticipate challenges related to integrating workforces and information systems and recognize that these challenges may result in smaller efficiency gains than projected, according to our review of relevant airline public documents.[74] Several equity analysts also told us that while mergers can face such challenges, some workforce and information system efficiencies still had been gained over the long term.

Fare and Market Structure Indicators Suggest Increased Competition Overall in the Past Two Decades

Our analyses of airline competition metrics—which provide a broader look at airline competition over a longer time frame—found that, compared to 2007, competition in the past two decades had increased. This finding was generally consistent across key metrics we assessed—fares; total number of seats offered by airlines; and market structure indicators (i.e., market share, number of effective competitors, and market concentration)—though the market structure indicators plateaued from 2022 through 2024.

In analyzing each metric, we divided domestic routes into five equal segments, or “quintiles,” based on passenger traffic. For simplicity in this report, we use “route” to refer to both travel between two specific airports and between city-pairs, when a city has multiple airports.[75] Because certain routes carry more passengers than others, the number of routes in each quintile differs substantially.[76] See Appendix I for more details on our data analyses.

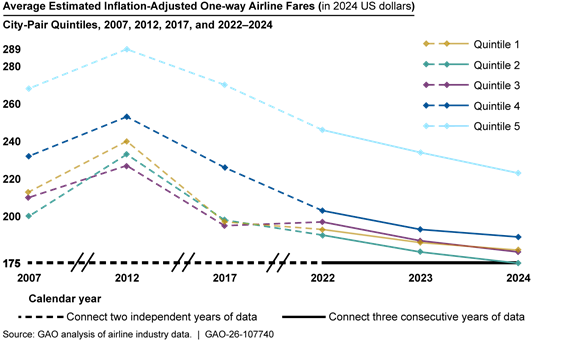

After an Increase in 2012, Average Estimated Fares on Most Routes Were Lower in 2024 Compared to 2007

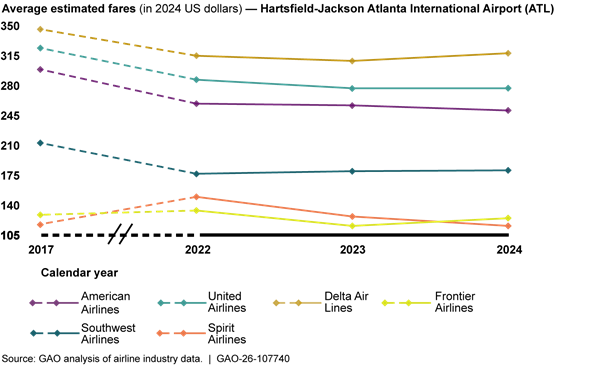

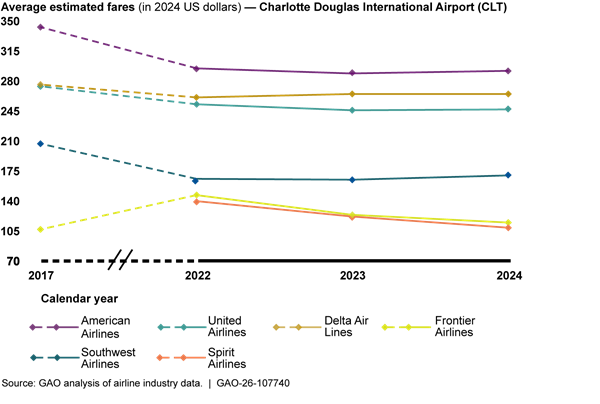

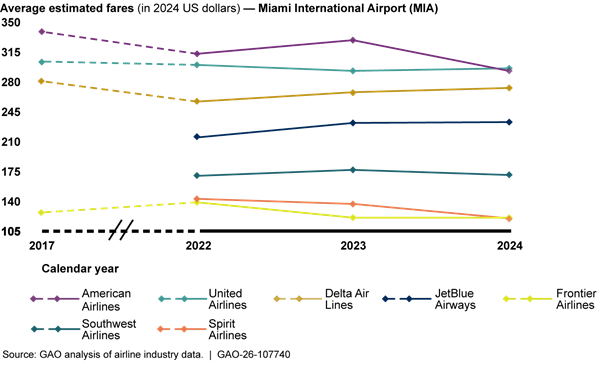

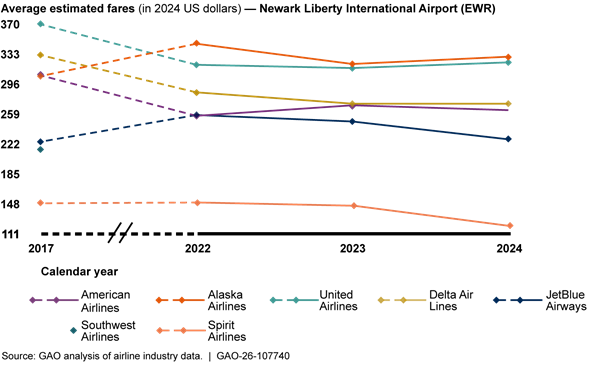

Through our data analysis, we found that average inflation-adjusted estimated domestic fares (average fares) were lower in 2024 as compared with 2007, an average of 15 percent across all quintiles (see fig. 3). Fares are the sum of estimated average base fares and average available airline-reported ancillary fees. Specifically, we added ancillary fees that airlines are required to account for separately in their reports to DOT—average baggage fees and reservation change and cancellation fees—to the base fare estimates.[77] Base fares are one-way ticketed fares in either direction, excluding taxes and fees.

The average fares on the less-traveled routes (fourth and fifth quintile)—generally routes to small and rural communities—experienced the largest decrease in fares of about 18 percent (an average of about $44 per ticket) in 2024 as compared with 2007. By comparison, average fares for the busier routes (first through third quintile) were about 14 percent lower (about $28 per ticket). When examining the trend across the most current years of our analysis (2022, 2023, and 2024), we found that fares decreased around 8 percent (about $16 per ticket) across all five quintiles from 2022 through 2024.

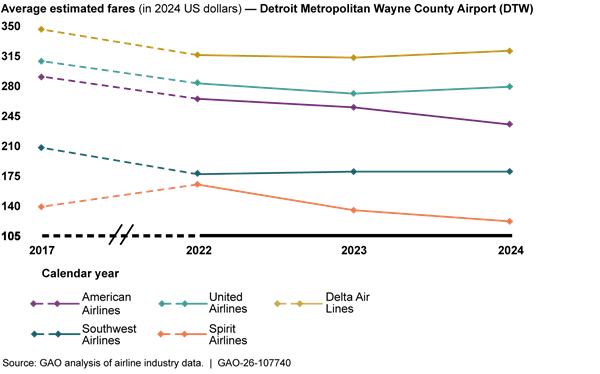

Figure 3: Average Estimated Inflation-Adjusted One-Way Airline Fares, City-Pair Quintiles, 2007, 2012, 2017, and 2022–2024

Notes: Fares reflect one-way fares in either direction, excluding taxes and fees, and include average baggage fees and reservation change and cancellation fees.

Each quintile contains approximately the same number of passengers, but the number of city-pair routes differs. For example, in 2024, the first, second, third, fourth, and fifth quintile contained 55, 128, 267, 775, and 10,526 city-pair routes, respectively, each with 20 percent of the roughly 570 million passengers in our sample for 2024.

When examining the number of routes that experienced a decrease in fares, we found that, across all quintiles, the majority of routes (79 percent) experienced lower fares in 2024 compared with 2007. Moreover, on the most-heavily traveled routes (first quintile), 94 percent of those routes had lower fares.

However, consistent with the findings from most of the empirical studies we reviewed, average fares in all five quintiles were higher in 2012 compared to 2007. The time frame between 2007 and 2012 generally coincides with several mergers included in our review. We previously reported that several factors also contributed to fare increases from 2007 to 2012, including “capacity restraint” exercised by airlines (i.e., limiting the supply of available seats in relation to the level of demand) and less price pressure exerted during this time by low-cost airlines.[78]

While increased competition could explain the lower fares in 2024 as compared to 2007, we identified three other factors that could explain the lower fares: the unbundling of fares, changes in airlines’ operating costs, and potential shifts in route distance over time. We determined that each of the factors is less likely to explain the lower fares in 2024 relative to 2007 than the effect of increased competition.

· Fare unbundling. Between 2008 and 2017, U.S. airlines began “unbundling” and introducing new fees for services, such as for carry-on bags, beverages, wireless internet access, and priority boarding. Some of these services used to be included in the base ticket fare. Due to the expansion of these ancillary fees and the lack of available data on those fees beyond baggage and reservation fees, our comparison of 2024 fares to 2007 may overestimate the drop in fares. Therefore, to provide the most equivalent fare comparison, we compared fares in 2024 to those in 2017, when unbundling was generally fully incorporated in fare structures, and found fares decreased 12 percent, on average, across all quintiles.[79] Regarding the number of routes that experienced a decrease in fares, we found that 88 percent of routes across all quintiles experienced lower fares in 2024 compared to 2017. On the most-heavily traveled routes (first quintile), 73 percent of those routes had lower fares.

· Operating costs. Major airlines’ unit operating costs—as measured by cost per available seat mile—were generally higher in 2024, ranging from a 1 percent to 24 percent increase after inflation adjustment, as compared to 2007.[80] We analyzed selected airlines’ cost per available seat mile to compare any changes in operating costs over time to the changes in fares we observed in our analysis.[81] While fluctuations in costs from year to year are to be expected due to changes in labor, fuel, and maintenance costs, we would also expect that, in a competitive environment, airlines would find it challenging to raise fares when experiencing higher costs. Fares were lower when costs were generally higher in 2024 as compared to 2007, suggesting that airlines were generally unable to pass along cost increases to consumers.

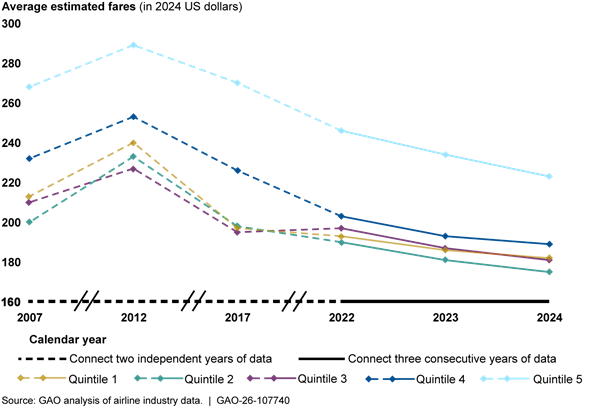

· Route distance. Analyzing the change in average estimated airline yields—a measurement of fare per unit of distance—accounts for potential changes in the length of routes over time. For example, if the number of long-haul routes decreased over time, then lower fares may reflect shorter routes. However, if airline yields also decreased over time, lower fares would not be explained by any potential changes in the length of routes. Like fares, we found that yields were lower in 2024 as compared with 2007 (see fig. 4). Specifically, we found a 19 percent decrease across all quintiles in 2024 compared to 2007—exceeding the 15 percent decrease in fares.

Figure 4: Average Estimated Inflation-Adjusted Airline Yields, City-Pair Quintiles, 2007, 2012, 2017, and 2022–2024

Notes: Stage-length-adjusted yields (“yields”) are calculated as fare per mile multiplied by the square root of flight distance in miles divided by 1,000. Fares reflect one-way fares in either direction, excluding taxes and fees, and include average baggage fees and reservation change and cancellation fees.

Each quintile contains approximately the same number of passengers, but the number of city-pair routes differs. For example, in 2024, the first, second, third, fourth, and fifth quintile contained 55, 128, 267, 775, and 10,526 city-pair routes, respectively, each with 20 percent of the roughly 570 million passengers in our sample for 2024.

One factor that may have contributed to decreasing fares and yields is the growth in lower-cost airlines throughout the last three decades.[82] Despite barriers to entry at some airports, which we discuss below, our analysis found that lower-cost airlines expanded their presence nationwide, including at hub airports that are dominated by a network airline.[83] The increase in market share of lower-cost airlines and the potential effects is discussed more below.

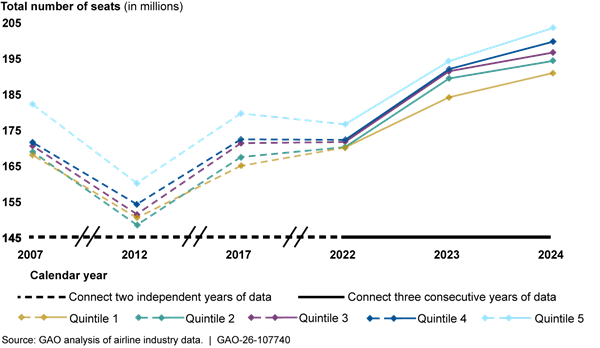

Airlines Offered More Total Seats in 2024 as Compared to 2007, While Decreases in Total Flights Since 2007 Recently Began to Plateau

We found, when comparing 2024 to 2007, that total seats—a measure of capacity—increased across all quintiles, but not on a consistently upward trend (see fig. 5). Total seats were lower across all quintiles in 2012, compared to 2007, which is consistent with our prior report’s discussion of the “capacity restraint” exercised by airlines.[84] But the number of total seats in 2017 and 2022 returned to levels generally similar to those observed in 2007. From 2022 through 2024, however, airlines increased capacity considerably, as evidenced by a 14 percent increase in total seats across all quintiles.

Notes: The data used to calculate the number of seats are based on nonstop segment data. A passenger on a one-stop flight is counted twice in each flight segment.

Each quintile contains approximately the same number of passengers, but the number of city-pair routes differs. For example, in 2024, the first, second, third, fourth, and fifth quintile contained 53, 108, 189, 381, and 1,999 city-pair routes, respectively, each with 20 percent of the roughly 800 million passengers in our sample for 2024.

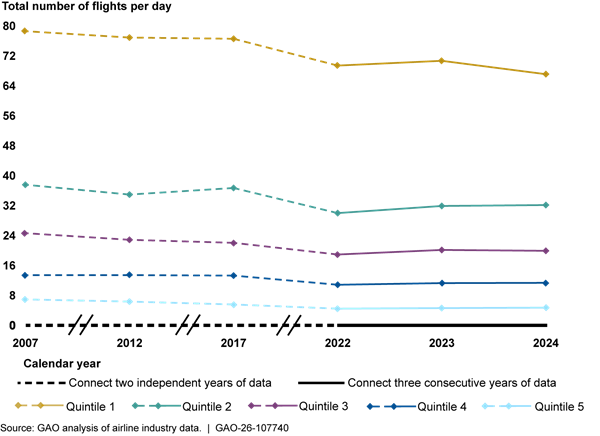

Airlines increased their capacity—or total seats—while operating fewer flights, as evidenced by a general decrease in total domestic flights per day on an average route (see fig. 6). Specifically, total flights per day were lower in all quintiles in 2022, as compared to 2007, and remained largely the same from 2022 through 2024. For the busiest routes (first quintile), airlines averaged 79 flights per day on any route in 2007, whereas in 2024, the same quintile averaged about 67 flights per day, a 15 percent decline. On the least-traveled routes (fifth quintile), airlines averaged seven flights per day on a given route in 2007 and under five flights per day in 2024, about a 32 percent decline.

Notes: The data used to calculate the flights per day are based on nonstop segment data. A passenger on a one-stop flight is counted twice in each flight segment.

Each quintile contains approximately the same number of passengers, but the number of city-pair routes differs. For example, in 2024, the first, second, third, fourth, and fifth quintile contained 53, 108, 189, 381, and 1,999 city-pair routes, respectively, each with 20 percent of the roughly 800 million passengers in our sample for 2024.

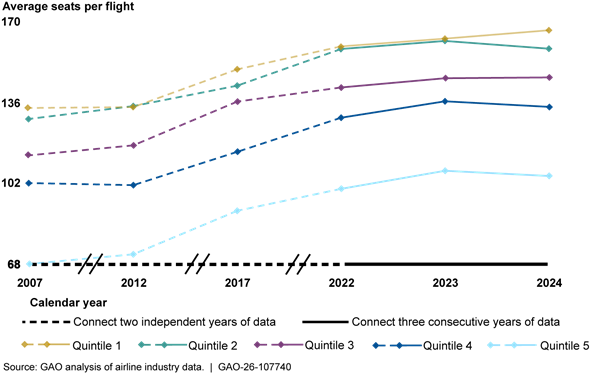

Increasing the number of seats with decreased flights refers to “up-gauging,” whereby airlines increasingly operate larger aircraft (see fig. 7). For example, the average aircraft flown on the busiest routes (first quintile) was 166 seats in 2024 compared to around 134 seats in 2007, a 24 percent increase. Aircraft size for the least-traveled routes (fifth quintile) increased 54 percent, or 105 seats in 2024 compared to 68 seats in 2007. Up-gauging is generally a reflection of airlines’ desire to increase operational efficiency and lower unit costs (i.e., cost per passenger) by carrying more passengers on fewer planes.

However, up-gauging can have varying effects on consumers. It could benefit consumers if airlines achieve cost-savings through increased operational efficiency and pass on those savings to the consumer through lower fares. On the other hand, reducing the number of flights can harm some consumers. For example, when the base number of flights is lower, such as in the fifth quintile, there are fewer flights per day from which a traveler from a smaller community can choose, reducing the likelihood the traveler can find a flight for their preferred time of the day.[85]

Notes: The data used to calculate the average seats per flight are based on nonstop segment data. A passenger on a one-stop flight is counted twice in each flight segment.

Each quintile contains approximately the same number of passengers, but the number of city-pair routes differs. For example, in 2024, the first, second, third, fourth, and fifth quintile contained 53, 108, 189, 381, and 1,999 city-pair routes, respectively, each with 20 percent of the roughly 800 million passengers in our sample for 2024.

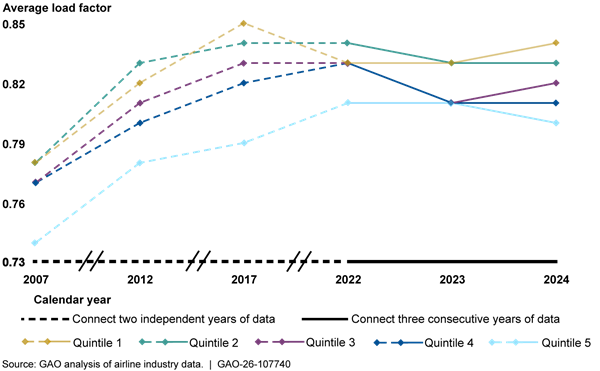

Further, our analysis found that load factors—the proportion of available seats occupied by passengers on a given flight—were overall higher in 2024 as compared to 2007, despite slight decreases from 2022 through 2024 (see fig. 8). Specifically, load factors were highest in 2017 for busier routes (first through third quintiles) as compared to 2007. And, for less-traveled routes (fourth and fifth quintiles), average load factors were highest in 2022, as compared to 2007. While higher load factors indicate that airlines are using aircraft fleets more efficiently, fuller flights also may have consequences for passenger experiences, such as less overhead space, less flexibility to rebook, or more time spent getting on and off the plane.

Notes: The data used to calculate the average load factor are based on nonstop segment data. A passenger on a one-stop flight is counted twice in each flight segment.

Each quintile contains approximately the same number of passengers, but the number of city-pair routes differs. For example, in 2024, the first, second, third, fourth, and fifth quintile contained 53, 108, 189, 381, and 1,999 city-pair routes, respectively, each with 20 percent of the roughly 800 million passengers in our sample for 2024.

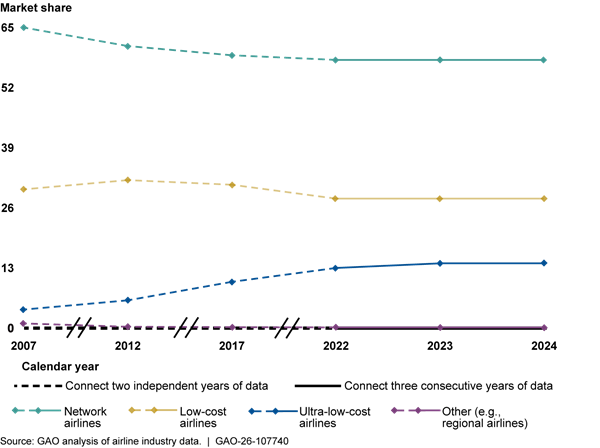

Key Market Structure Indicators Show Increased Presence of Ultra-Low-Cost Airlines in 2022 as Compared to 2007, with Indicators Plateauing Since 2022

Our analysis of three market structure indicators—market shares for each airline type, the number of effective competitors, and market concentration measured by the Herfindahl–Hirschman Index (HHI)—found that compared to 2007, competition in recent years generally increased, even though indicators remained largely unchanged from 2022 through 2024.

Market Share

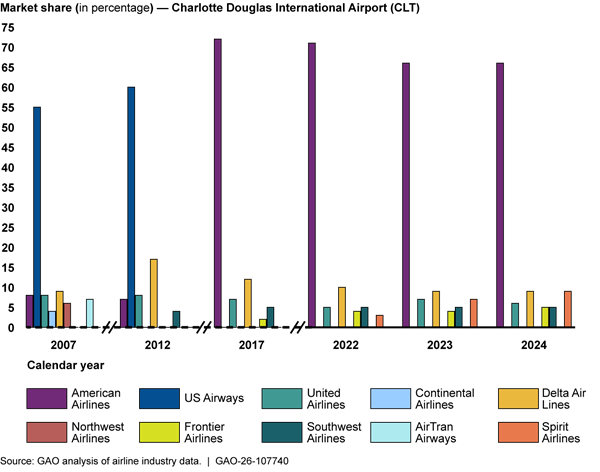

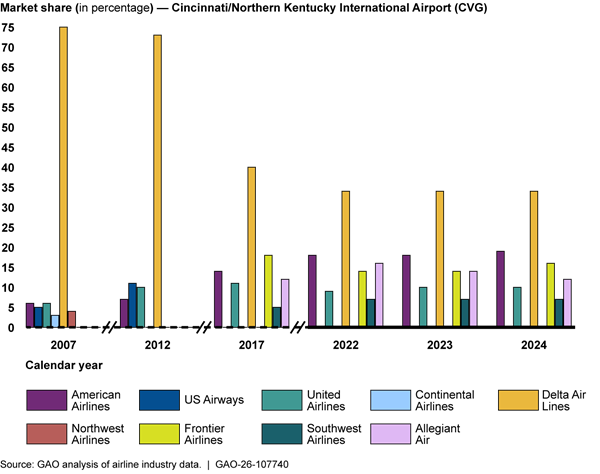

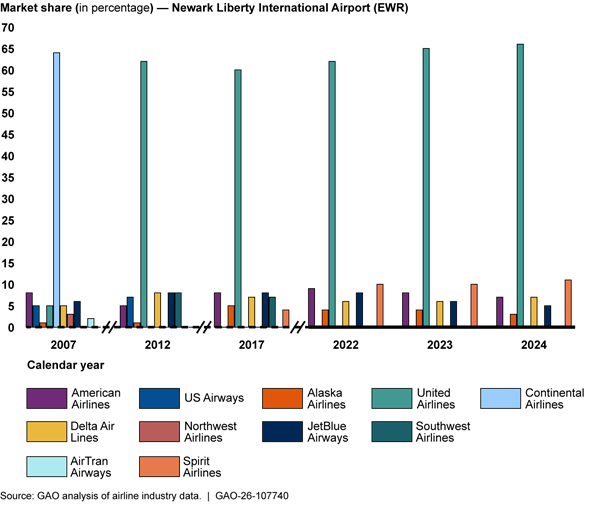

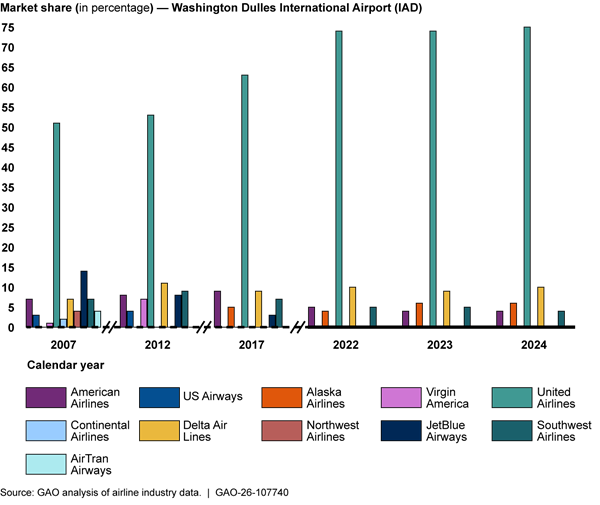

In 2022, compared with 2007, we found a decrease in network airlines’ market share and an increase in market share for ultra-low-cost airlines.[86] From 2022 through 2024, market shares across all airline types remained relatively flat (see fig. 9). Market share describes the proportion of total passengers transported by different types of airlines, including network, low-cost, ultra-low-cost, and other (e.g., regional) airlines each year. In the airline industry, the effect of market share on price competition can depend on the type of airline.

Specifically, while network airlines collectively transport the most passengers each year, we found that their market share in 2022 decreased by 7 percentage points compared with 2007, from 65 percent to 58 percent. Low-cost airlines saw a slight decrease, from 30 percent to 28 percent over the same period. In contrast, ultra-low-cost airlines’ market share in 2022 increased by almost 10 percentage points compared with 2007, from 4 percent to 13 percent. As discussed previously, lower-cost airlines (i.e., low-cost and ultra-low-cost airlines), like Southwest Airlines and Spirit Airlines, exert more price pressure on network airlines than network airlines exert on one another, ultimately resulting in lower fares.[87]

Note: For analytical purposes, we categorized airlines into four types. However, given the dynamic nature of the industry and airlines’ individual business models, an airline may not perfectly fall into a single category across all years and for all purposes.

The market shares are calculated as the weighted average of market shares for each airline type across city-pairs in the U.S. (weighted by passenger count).

From 2022 through 2024, the market share of each airline type changed less than 1 percentage point. The recent stability in market share may be the result of network airlines’ expansion into basic economy services, discussed more in the next section of the report, which has contributed to the plateau of lower-cost airlines’ growth.[88]

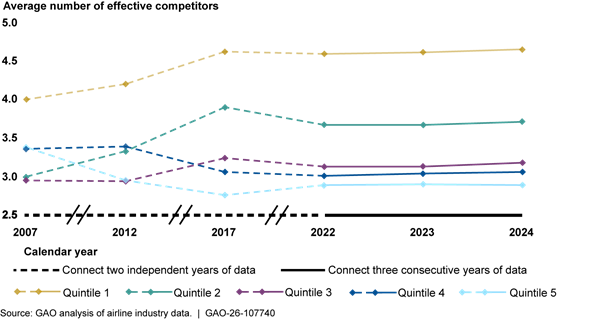

Effective Competitors and Market Concentration

In 2022 compared with 2007, the average number of effective competitors—any airline that carries at least 5 percent of the passenger traffic on a given route—and market concentration suggest increased competition on the busiest routes and decreased competition on routes with lower passenger traffic.[89] However, from 2022 through 2024, these indicators remained largely unchanged.

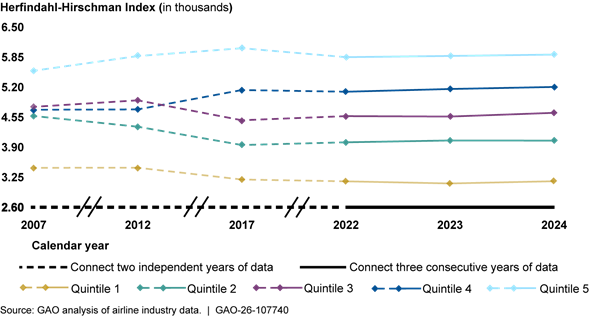

In the airline industry—an industry with relatively few competitors—a higher number of effective competitors on any route typically indicates a higher level of competition. By contrast, an increase in market concentration, which we measured using the Herfindahl-Hirschman Index (HHI), often indicates weakening competition, which increases the likelihood that one or more airlines can exert market power and influence overpricing.[90]

Our analysis found that for the busiest routes (first through third quintiles), the average number of effective competitors was higher in 2022 compared with 2007 and generally flat from 2022 through 2024 (see fig. 10). For example, on the most heavily traveled routes (first quintile), the average number of effective competitors increased from 3.99 in 2007 to 4.58 in 2022 (15 percent), and was 4.64 in 2024, an increase of 1.3 percent from 2022.[91]

Figure 10: Effective Domestic Airline Competitors, City-Pair Quintiles, 2007, 2012, 2017, and 2022–2024

Note: Each quintile contains approximately the same number of passengers, but the number of city-pair routes differs. For example, in 2024, the first, second, third, fourth, and fifth quintile contained 55, 128, 267, 775, and 10,526 city-pair routes, respectively, each with 20 percent of the roughly 570 million passengers in our sample for 2024.

The increase in effective competitors observed in 2022 compared with 2007 was likely a result of entry of ultra-low-cost airlines on routes that previously had no ultra-low-cost presence, corresponding to the growth in ultra-low-cost airlines’ market share leading up to 2022. For example, for the most-heavily-traveled routes (first quintile), 56 percent of the routes saw the entrance of an ultra-low-cost effective competitor at some point between 2007 and 2022.[92]

Consistent with the higher number of effective competitors in 2022 compared to 2007, we found that HHI was lower for the busiest routes (first through third quintiles) in 2022 compared with 2007, and relatively flat from 2022 through 2024 (see fig. 11).[93] While similar to the number of effective competitors, HHI provides a more comprehensive measure of market concentration because it also considers the relative size and market share of each firm, giving more weight to larger airlines.[94] As such, lower HHI and a higher number of effective competitors typically indicate increased competition.

Figure 11: Market Concentration (as measured by HHI) in the Domestic Airline Industry, City-Pair Quintiles, 2007, 2012, 2017, and 2022–2024

Notes: Each quintile contains approximately the same number of passengers, but the number of city-pair routes differs. For example, in 2024, the first, second, third, fourth, and fifth quintile contained 55, 128, 267, 775, and 10,526 city-pair routes, respectively, each with 20 percent of the roughly 570 million passengers in our sample for 2024.

HHI is a measure of market concentration and is calculated by summing the squares of the individual airline’s market shares. Higher values of this index on a route mean more market power for one or a select few airlines.

In contrast to the busier routes, we found that routes with lower passenger traffic (the fourth and fifth quintiles)—which likely include routes serving small communities—had fewer effective competitors on average and higher HHI in 2022 compared with 2007, indicating decreased competition. Specifically, effective competitors decreased from 3.35 in 2007 to 3 in 2022 for routes in the fourth quintile (HHI increased by 8 percent) and from 3.37 in 2007 to 2.88 in 2022 for routes in the fifth quintile (HHI increased by 5 percent). From 2022 through 2024, number of average effective competitors essentially remained the same, and HHI slightly increased for the fourth and fifth quintiles.[95] Together, the slight increase in HHI and the same number of effective competitors suggest that competition on routes in the fourth and fifth quintile, on average, decreased slightly from 2022 to 2024.

In addition, we found no significant presence of low-cost or ultra-low-cost effective competitors in the fifth quintile, in 2022 as compared with 2007. Specifically, while all routes in the first quintile had either a low-cost or ultra-low-cost effective competitor in each year we analyzed, 58 percent of routes in the fifth quintile had no effective low-cost or ultra-low-cost airline competitor in any year in our sample. According to three stakeholders we spoke with, service in these markets does not offer sufficient passenger traffic to attain profitability for lower-cost airlines that do not operate in hub and spoke systems.[96] However, as we mentioned above, average estimated fares in the fourth and fifth quintiles were still lower in 2022 compared to 2007.

Stakeholders Identified Key Factors That Affect Competition and Some Raised Concerns About Less Robust Competition in the Future

Growth of Airline Credit Cards and Basic Economy Products Are Newer Factors Cited Alongside Other Longstanding Ones

From our interviews with more than 30 stakeholders from various segments of the industry—including airlines, equity analysts, academic researchers, consumer advocates, and industry associations—five key factors that affect airline competition emerged.[97] Two of the key factors reflect new competitive dynamics in the industry—expanded airline credit card reward programs and the introduction of basic economy products. Three other cited factors are those we have discussed in prior work and, according to stakeholders, continue to affect airline competition—airport access, global alliances, and price transparency.[98] These five key factors are not an exhaustive list of factors that may affect competition.

Airline Credit Card Rewards Programs

While airline loyalty and rewards programs have existed for many years, a majority of stakeholders discussed the expanded importance of airline credit cards to these loyalty programs as a key factor affecting competition today. Some of these stakeholders discussed how airlines compete against each other through these programs and associated credit cards. Others discussed how such credit cards can provide some airlines with competitive advantages over the other airlines that are unable to take advantage of the credit card programs in the same way.

Over the past two decades, card holders’ use of airline credit cards has become the predominant method of earning airline rewards.[99] Traditionally, airline loyalty programs were frequent flier programs, where passengers earned “miles” and exchanged them for free or discounted travel or other rewards. As we reported in 2014, traditional loyalty programs can incentivize travelers to concentrate their flying with one airline to accumulate miles and rewards, even though other airlines’ fares may be more competitively priced.[100]

Airlines compete fiercely through reward programs, according to representatives of four airlines and an equity analyst, which may include the benefits offered to card holders. For example, representatives from one network airline told us they invested significantly in their cardholder airport lounges to make their loyalty program more appealing and competitive to consumers. The cards also provide benefits for airline customers by allowing them to redeem points for air travel, seat upgrades, and access to exclusive airport lounges, as well as benefits beyond air travel, such as hotels or restaurants. However, one consumer advocate explained that while these reward programs are popular, consumers may not be wholly better-off, in part because they may overvalue the benefits, and loyalty to the airline may disincentivize comparison shopping. Further, three consumer advocates stated in public comments that the quality of these programs has declined over time, as airlines have devalued points and made rewards more difficult to acquire.[101] For example, one consumer advocate highlighted that some airlines have imposed expiration dates for points.

According to stakeholders, airlines that offer credit cards can obtain competitive advantages by generating revenue beyond the airlines’ operating revenue and further solidifying customer loyalty. Eleven stakeholders, including seven airlines and four equity analysts, stated that airline credit cards have become an increasingly valuable source of revenue to many airlines. For example, Delta Air Lines recently announced that its American Express credit card relationship generated over $8 billion in 2025.[102] Airlines generate significant revenue by selling frequent flyer points—which are predominately accumulated through co-branded credit card transactions and whose value the airlines control—to third parties, such as banks. The banks then use the airline points as a means of attracting and rewarding customers who select their credit cards, according to a study we reviewed.[103]

According to DOT officials, these programs help provide airlines’ revenue stability, particularly in periods of lower travel demand, since the revenue generation is tied to credit card transactions. Further, 10 stakeholders, including representatives from the airlines and equity analyst community, said that airlines with these credit card reward programs may use that revenue to help offset operating costs. For example, according to representatives from one airline, the $3.2 billion in 2024 revenue earned from their airline credit card helped cover operating costs and enabled them to offer lower fares and more services to consumers than it otherwise could have without the credit card program.

However, some stakeholders stressed that not all airlines are able to take advantage of airline credit card programs or leverage their broader reward programs in the same way. These 10 stakeholders, including airline representatives, equity analysts, and a consumer advocate, told us that the reward programs created by smaller airlines, particularly lower-cost airlines, are less attractive than larger airlines due to their relatively small scale of operation. In addition, DOT officials stated that smaller airlines may not receive the best deals with credit card companies because these airlines have fewer passengers and therefore potential card users. As a result, the officials explained the smaller airlines generate much less revenue from such cards.

Introduction of Basic Economy Products

Some stakeholders discussed how network airlines’ introduction of basic economy products changed how they compete with lower-cost airlines and increased competition for customers in the lower-cost space. By 2018, network airlines had launched basic economy—economy tickets offered at a lower price but with fewer included amenities, such as checked baggage, seat selections, or ticket refunds—which DOJ officials stated was in response to competition from lower-cost airlines.[104] One network airline representative and three equity analysts attributed this new offering to changes in consumer preferences following the growth of the low-fare sector. They also mentioned that in the wake of decreased business travel following the pandemic, network airlines reallocated some capacity into leisure markets, which were traditionally held by lower-cost airlines.

Representatives from two network airlines said that basic economy products are popular with consumers and help airlines attract and increasingly compete for the most price-sensitive customers. Furthermore, other stakeholders, including equity analysts and academic researchers, said network airlines’ entry into basic economy fares has increased competition for customers in the lower-cost space. The supply of basic economy seats from the large network airlines now makes up a significant portion of the overall low-cost market, according to two equity analysts and a lower-cost airline. Three equity analysts said there is currently too much capacity in the low-cost sector, and they expect the number of low-cost seats to shrink in the future.

Basic economy products make competing in the low-cost space more challenging for lower-cost airlines, according to some stakeholders, including three lower-cost airline representatives and an equity analyst. Specifically, these products lower the price gap for a price sensitive customer choosing between a flight with a network airline that offers more expansive service or a lower-cost airline that offers more limited service.

Following the introduction of basic economy products by network airlines, two airline representatives and two equity analysts told us lower-cost airlines have begun introducing premium offerings—traditionally outside of the low-cost space—for an extra fee, such as seating with extra legroom, to generate additional revenue. DOT officials and some other stakeholders said these actions are a response to a shift in consumer preferences towards more premium offerings following the COVID-19 pandemic.

Airport Access

Twenty-three stakeholders, including a broad representation of airlines, equity analysts, academic researchers, and consumer groups, told us that airport access—particularly at hub airports—continues to be a significant issue and affects some airlines’ ability to compete. When access is limited, consumers may be affected by fewer airline or scheduling choices. Stakeholders discussed how three access issues (use/lease agreements, gate access, and slot-controlled airports) affect the extent to which airlines can gain access to or maintain their presence at certain airports.[105]

· Provisions in airport use and lease agreements. Stakeholders identified two provisions in airport use and lease agreements that they say can impede an airline’s ability to compete and grow, particularly at the busiest airports.[106]

Fixed fee. Six stakeholders, including airline representatives and equity analysts, pointed to fixed fee provisions in some airports’ use and lease agreements that allocate a proportion of some airport common-use fees (e.g., for baggage claim areas or gates) evenly across all airlines (historically around 20 percent), rather than on the number of passengers carried by each airline. According to these stakeholders, that fee structure disproportionally affects smaller airlines since they pay the same fee amount despite having much fewer passengers than other airlines. Representatives from an industry association told us that some airports have shifted toward fees based more on passengers carried, which would likely lower fees for airlines with a smaller presence at these airports.[107]