Report to Congressional Requesters

United States Government Accountability Office

GSA Should Create Goals to Ensure New Approach Saves Money and Accelerates Disposals of Unneeded Property

A report to congressional requesters

For more information, contact: David Marroni at MarroniD@gao.gov

What GAO Found

From October 2013 through November 2025, the General Services Administration (GSA) sold hundreds of properties owned by GSA and other federal agencies. These properties generated $1.4 billion in revenue and were primarily sold through GSA’s auction website. While residential properties were the most frequently sold property, most of the sales revenue (75 percent) came from commercial and industrial properties. Since 2018, GSA has sold fewer properties, but more of these sales were higher value, leading to an increase in sales revenue. When selling GSA-owned properties, GSA took about 1 year or less to dispose of about half of its properties, while other properties took several years. Delays in selling federal properties were caused by a number of factors, such as agencies needing to secure funds to relocate, prolonged environmental remediation efforts and time needed to evaluate interest from other government entities in claiming the property, according to GSA officials.

Since 2025, GSA has taken initial steps to change its approach to disposing and selling properties, including centralizing how disposals are managed and creating a website that lists properties for accelerated disposal. However, GAO found GSA’s efforts do not fully align with selected key practices. For example:

· GSA estimates the approach could save agencies billions of dollars in avoided repair and operations costs. GSA has not established performance goals linked to the accelerated approach. For example, GSA’s 2026 performance plan does not include goals for reduced timelines or avoided costs. Establishing such goals could help GSA better define the approach, simplify disposals, and gain greater cost savings from avoided operations and maintenance costs.

· GSA has not determined how to evaluate the effectiveness of using private brokers to lead its public sales, compared to other methods such as its auction website. In 2025, concurrent with a one-third reduction in staff in its disposal office, GSA hired private real estate brokers to lead public sales. Using data on the timeliness of completion, costs to pay brokers, and sales revenue could help GSA select the most optimal method for future sales.

Why GAO Did This Study

GSA assists federal agencies in disposing of and selling unneeded real property, from office buildings to undeveloped land. Preparing and selling federal real property has historically presented challenges that can result in disposals taking years to complete and lead to agencies paying millions of dollars to operate unneeded buildings. In March 2025, GSA announced it would begin disposing of properties using a new accelerated approach to disposals and sales.

GAO was asked to review GSA’s efforts to conduct sales of federal real property. This report examines (1) how GSA sold excess real property from 2013 to 2025 and the results; and (2) how GSA plans to sell federal real property under its accelerated disposal approach, and the extent that changes to its process meet selected key policymaking practices.

GAO analyzed GSA’s real property data for all completed sales from October 2013 through November 2025, reviewed GSA documentation related to its accelerated disposal approach, including internal policies on sales and budget and performance plans. GAO compared this information with selected key policymaking practices identified in prior work.

What GAO Recommends

GAO is making three recommendations to GSA, including that GSA establish performance goals for GSA sales that link to the accelerated approach, and evaluate the effectiveness of using private real estate brokers. GSA agreed with GAO’s recommendations and described activities it would undertake to implement them.

|

Abbreviations |

|

|

|

FAR |

Federal Acquisition Regulation |

|

|

FASTA |

Federal Assets Sale and Transfer Act of 2016 |

|

|

FMR |

Federal Management Regulation |

|

|

GSA |

General Services Administration |

|

This is a work of the U.S. government and is not subject to copyright protection in the United States. The published product may be reproduced and distributed in its entirety without further permission from GAO. However, because this work may contain copyrighted images or other material, permission from the copyright holder may be necessary if you wish to reproduce this material separately.

April 9, 2026

The Honorable Gary C. Peters

Ranking Member

Committee on Homeland Security and Governmental Affairs

United States Senate

The Honorable James Lankford

Chairman

Subcommittee on Border Management, Federal Workforce and Regulatory Affairs

Committee on Homeland Security and Governmental Affairs

United States Senate

The federal government owns hundreds of thousands of buildings that cost billions of dollars annually to occupy, operate, and maintain. Disposing of real property that federal agencies do not need—but continue to pay for—has been a longstanding challenge.[1] The General Services Administration (GSA) plays an important role in disposing of excess federal real property.[2] GSA’s disposal of federal properties may include transfers to other government agencies or to state and local entities for a public use, but most properties (about 70 percent) are sold in competitive public sales.[3] These sales have generated billions of dollars in revenue and include a wide range of property types in varying conditions, including residential homes, industrial sites, commercial office buildings, courthouses, and undeveloped land. Preparing and selling these properties has historically presented challenges that can result in disposals taking years to complete.

In March 2025, GSA announced it would begin disposing of federally owned office buildings using what it described as an accelerated approach. As of March 2026, GSA has identified 47 federal properties for this accelerated approach. GSA has typically used its own staff and auction website to sell unneeded property.[4] However, in spring 2025, GSA began to reevaluate the strategic direction for its disposal program amid staffing reductions. As part of these efforts, it is considering changes for managing sales under the accelerated disposal approach, including using private real estate brokers to complete real property sales on its behalf. In December 2025, GSA rescinded the majority of regulations implementing its disposal authority with the intent to, according to GSA, streamline its disposal process.[5]

You asked us to review GSA’s efforts to conduct public sales of federal real property. This report examines (1) how GSA sold excess real property from 2013 to 2025 and the results, and (2) how GSA plans to sell federal real property under its accelerated disposal approach, and the extent that changes to its process meet selected key practices for evidence-based policymaking. Our review examined GSA’s disposal process prior to the December 2025 regulatory changes.

To address our first objective, we analyzed GSA’s real property data for all completed sales from October 2013, the earliest available sales in GSA’s data, through November 2025. We analyzed the data to identify characteristics of the sales, including 1) methods used to complete the sales, 2) types of property sold, 3) agencies that owned the properties, 4) costs incurred by GSA in preparing and completing the sale, and 5) the length of time it took to prepare and sell properties. We assessed how well GSA met its initial sales revenue goals in each closed sale occurring from October 2013 through November 2025. We also reviewed GSA’s online auction bidding data for completed auctions that were available from October 2015 through November 2025 to identify how long it took to complete sales.

To address our second objective, we reviewed GSA documentation and information on its website to identify and assess its accelerated disposal approach. We reviewed GSA’s annual performance and budget documentation to identify annual performance goals and measures related to disposals and sales of federal real property. We also reviewed GSA documentation to identify whether GSA has created new goals, sales methods, and plans to oversee and assess progress toward its accelerated approach. We assessed this information against selected key practices for evidence-based policymaking.[6] These selected practices were defining goals, assessing and improving evidence quality, and using evidence to understand results. We based our selection of the key policymaking practices on whether they are applicable to how GSA oversees and assesses its accelerated disposal approach. In addition, we interviewed GSA officials for additional context and perspectives on GSA’s real property sales process, associated challenges, and the accelerated disposal approach. Further details on our scope and methodology can be found in appendix I.

We conducted this performance audit from August 2024 to April 2026 in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

Background

Federal Property Disposal Process

GSA generally acts as the disposal agency for surplus real property, including surplus real property that is owned by other agencies.[7] During the time period relevant for our review, GSA followed a multi-step process to dispose of excess real property, which may or may not have resulted in a competitive public sale.[8]

As part of this process, GSA prepared properties for disposal, which included:[9]

· Conducting an initial review of the property when a federal agency determined it no longer needed its property and notified GSA of the excess property.[10]

· Determining if GSA could formally accept the property for disposal based on its initial review. GSA referred to this formal acceptance as the “date of acceptance.”[11]

· Offering the property to other federal agencies and transferring it if an agency identified a mission-related need for the property.[12]

· Prioritizing the property for homeless assistance providers, state and local governments, or eligible nonprofits if it was deemed suitable to assist individuals experiencing homelessness.[13]

· Offering the property to a state or local government, or an eligible non-profit entity, at up to a 100 percent discount for other public benefit purposes, such as for educational facilities, historical monuments, and public parks.[14]

· In limited circumstances, negotiating the sale of the property. For instance, state and local entities could acquire property through a negotiated sale for fair market value if the negotiated sale will result in a public benefit that would not be realized from a competitive sale.[15]

· Completing a competitive public sale if GSA has not transferred or disposed of the property through the above processes.

Competitive Public Sale Process

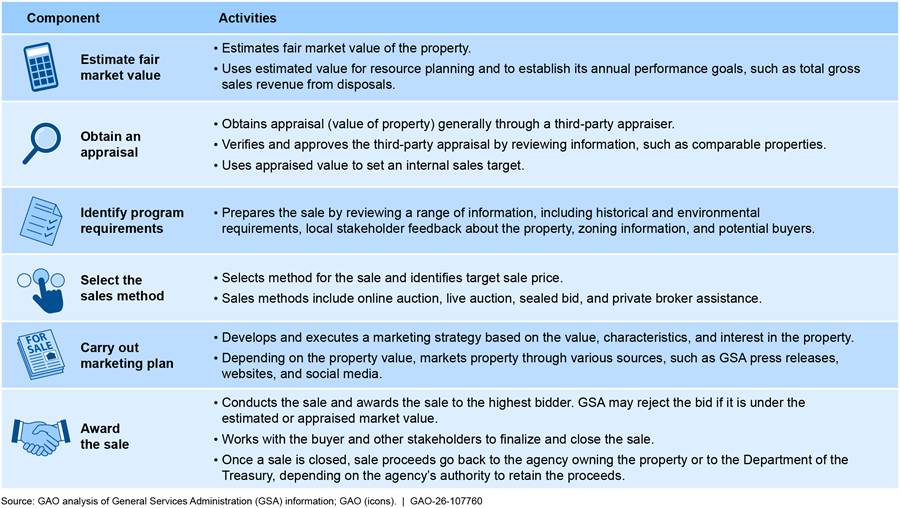

GSA takes several steps, sometimes concurrently, when preparing and carrying out a competitive public sale, as shown in figure 1.

Note: Some of these components are completed concurrently or may occur earlier in the disposal process than portrayed in the figure.

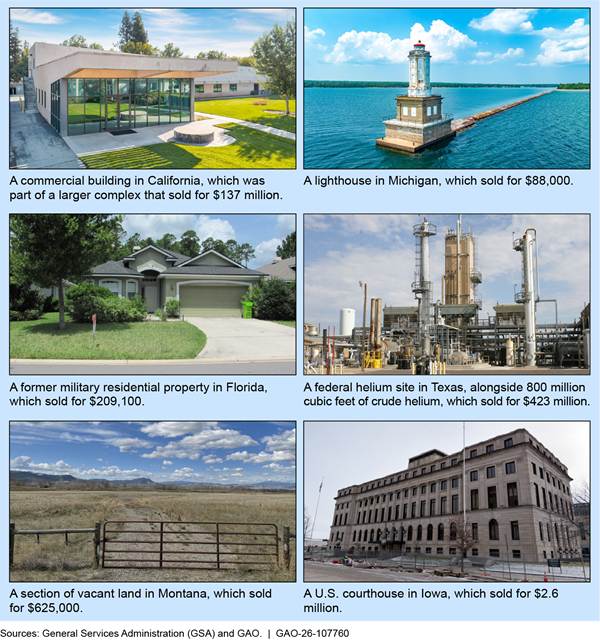

Through its competitive public sale process, GSA sold a wide range of properties across the country. For example, recent sales included a lighthouse that sold for under $100,000 and an industrial facility that sold for hundreds of millions of dollars (see fig. 2).

Sales Methods and Costs

GSA uses several methods to competitively sell a property.[16] GSA chooses the sales method based on factors including property characteristics, local market demand, costs to complete the sale, and which method is expected to bring the highest monetary return. The primary methods that GSA uses include the following:

· Online auction. GSA uses its auction website to post photos and videos of the property and other information about the sale’s auction schedule. Interested buyers or “bidders” register on the website and may bid on an auction through two options: manual one-time bids or automatic bid escalation against other bidders in real time.

· Live auction. A live auction is conducted at a physical location with an auctioneer. Bidders register, submit a deposit, and bid until the highest bid is determined by the auctioneer.[17]

· Sealed bid. Bidders mail in sealed deposits and bids to GSA. GSA opens all of the bids on a designated date. The highest bid received is awarded the sale.

· Private broker sales. Contracted brokers may be used for high-profile properties that require national exposure, have unique features, or may be difficult to sell.[18] While GSA has previously obtained assistance for certain tasks from private brokers in its sales, GSA began tasking private brokers to sell properties on its behalf in 2025.

Operating, maintaining, and disposing of federal buildings is costly. GSA data indicates the government’s annual maintenance and operating costs for its more than 246,000 owned buildings exceeded $17 billion in fiscal year 2024.[19] Additionally, GSA incurs several costs when preparing and selling federal buildings, such as for appraisal fees, marketing and advertising, site preparation, sales services, and staff work and travel to the property location.

GSA Sold $1.4 Billion in Properties Since October 2013, Mostly Using Online Auctions

GSA Sold Hundreds of Properties That Generated $1.4 Billion Since 2013 and Generally Met Its Annual Performance Goals for Revenue

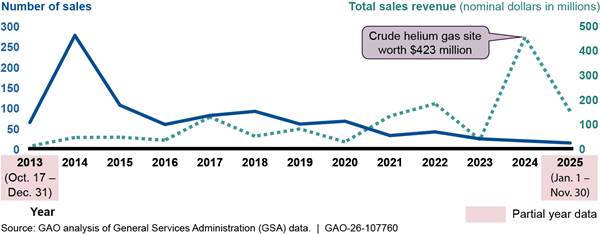

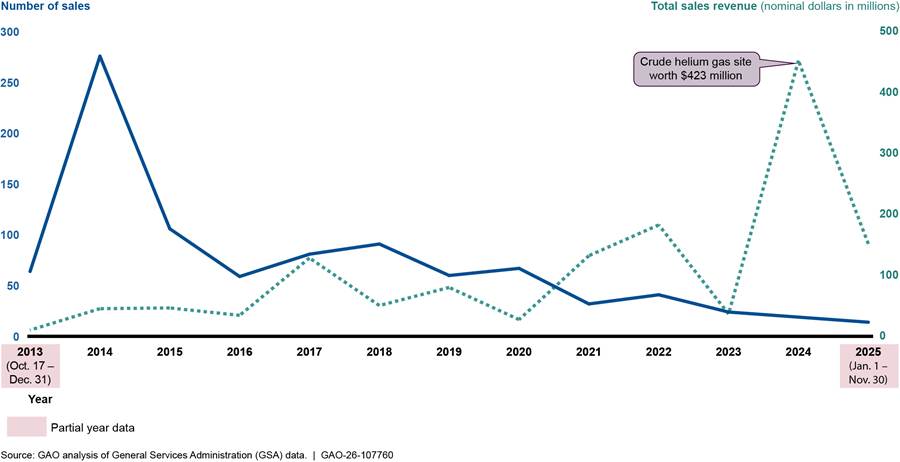

GSA completed a total of 921 real property sales from October 2013 through November 2025 that generated a total of $1.4 billion (see fig. 3).[20] The number of sales peaked in 2014 and 2015, primarily as the result of GSA assisting federal agencies, including the Department of Defense, in selling hundreds of military residential homes, which are typically low value (under $300,000).[21]

Notes: This analysis includes closed sales from October 17, 2013 through November 30, 2025. The number of sales in a year is based on the date GSA awarded the sale and not the date on which the sale transaction closed, which can occur up to 180 days after the sale award date. This analysis presents sales revenue in nominal dollars and is not adjusted for inflation. The sales revenue increase in 2024 was largely due to a sale of a Department of Interior owned crude helium gas site worth $423 million. Without this sale, total sales revenue in 2024 was $28 million.

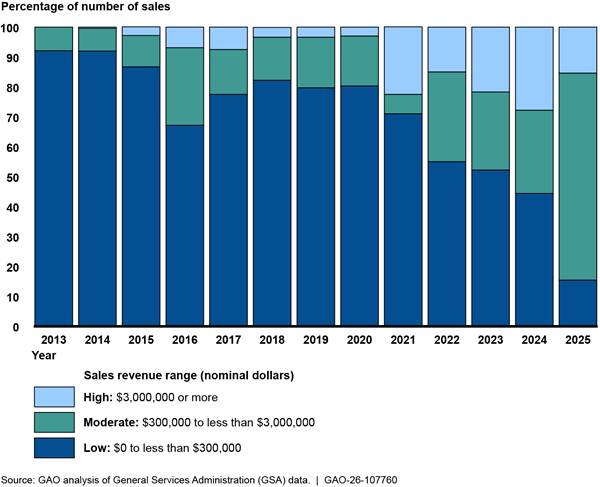

Since October 2013, GSA began to sell fewer, but more high-value, properties each year. Specifically, the number of sales began to decrease after 2018, from 90 sales in 2018 to 13 sales in 2025. During this period, GSA began to sell more moderate ($300,000 to under $3 million) and high ($3 million or more) value properties (see fig. 4). As a result, moderate to high-value properties make up a higher proportion of sales than they did in the past, especially over the last 5 years. For example, moderate and high-value properties accounted for an average of 18 percent of all sales annually from 2013 to 2020 but increased to an average of 52 percent of all sales annually from 2021 to 2025.[22]

Figure 4: Annual Percentage of GSA Sales of Real Property by Sales Revenue Range, October 2013–November 2025

Notes: This analysis includes closed sales from October 17, 2013 through November 30, 2025. The number of sales in a year is based on the date GSA awarded the sale and not the date on which the sale transaction closed, which can occur up to 180 days after the sale award date. In addition, this analysis presents sales revenue in nominal dollars and is not adjusted for inflation.

With GSA selling more moderate to high-value properties, sales revenue has generally increased since 2020. This increase was driven by a small number of high-value industrial and commercial properties sold. For example:

· In 2021 and 2022, GSA sold 10 properties under the Federal Assets Sale and Transfer Act of 2016 (FASTA)—a temporary program intended to reduce the cost of federal real estate by selling high-value assets and facilitating and expediting the sale or disposal of unneeded federal real property, among other things.[23] These sales accounted for nearly two-thirds of sales revenue during that period ($194 million out of $312 million).

· Another high-value sale in 2024 also drove this increase–a federally owned crude helium gas site managed by the Department of the Interior. This property sold for $423 million, representing about 31 percent of the total revenue from sales since 2013.

· In August 2025, GSA sold one commercial property in Menlo Park, California, for $137 million under the FASTA program.

GSA has generally met its annual performance goal for revenue from governmentwide disposals managed by GSA from fiscal year 2022 to fiscal year 2024.[24] To set this goal, GSA estimates an initial fair market value for each property as it begins to prepare it for disposal. Then, GSA aggregates all initial estimates of fair market value to determine: (1) the total revenue goal for all expected disposals in the upcoming budget year in its annual performance report and; (2) the budget GSA will need to carry out the disposals for the year.[25] GSA’s goal does not examine the extent to which proceeds for individual sales or groups of sales (e.g., by value range or property type) meet initial fair market value estimates. In recent years, GSA exceeded its performance goal for total revenue in fiscal year 2022 and fiscal year 2024 but did not meet its goal in fiscal year 2023 due to the delay of a high-value sale.

While GSA does not measure performance in meeting an estimated fair market value for each individual sale or by different property types, we analyzed GSA sales data from October 2013 through November 2025 and found that GSA’s sales met these initial estimates for the majority of properties sold, especially for higher value properties. In particular, GSA achieved its initial estimate of fair market value for 89 percent of moderate-value and high-value properties. GSA was not as successful in meeting this estimate for low-value properties, which was achieved in 76 percent such sales. The extent that GSA met the initial estimates of fair market value has varied by property type, as we describe in further detail below.

GSA Has Sold Many Different Types of Properties, Mostly for Other Federal Agencies

GSA has sold a wide range of property types for many federal agencies.

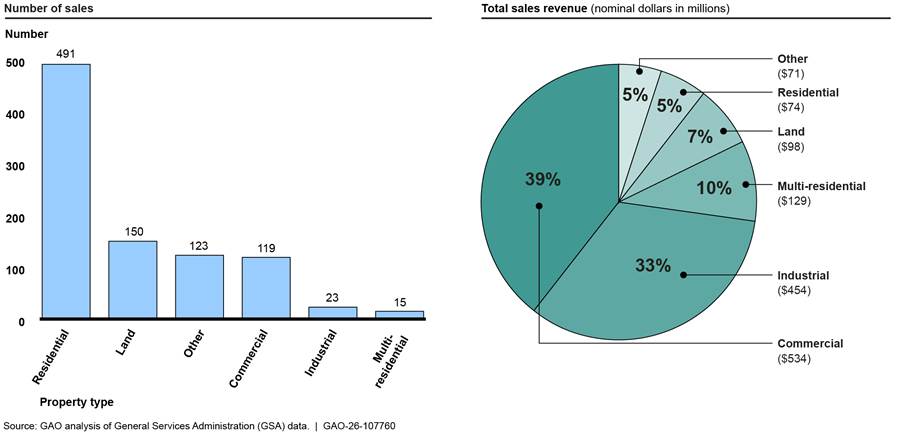

Property type. GSA sold a wide range of properties from October 2013 through November 2025. While most of these sales involved lower-value properties like residences or land, almost 75 percent of sales revenue resulted from a smaller number of industrial and commercial sales (see fig. 5).

· Single and multi-residential properties, land, and “other” properties such as lighthouses made up 85 percent of the total number of properties sold but only 27 percent of the total revenue since 2013. Half of these properties sold for about $100,000 or less.[26] Within this group, single residential properties made up more than 50 percent of all properties sold but only five percent of revenue.

· Industrial and commercial properties accounted for 15 percent of the total number of properties sold but almost 75 percent of the total sales revenue since 2013. Half of the industrial properties sold for $500,000 or less while half of the commercial properties sold for $283,000 or less.[27]

Figure 5: Total Number of GSA Real Property Sales and Revenue by Property Type, October 2013–November 2025

Notes: “Other” includes property types such as agricultural, lighthouse, special use such as schools or research facilities, and properties that GSA labelled a combination of property types. Residential sales generally involve a single-family home while multi-residential sales may include a few to many family homes generally used for military housing. Most of the revenue in the industrial category is due to the sale of a crude helium gas site worth $423 million. Percentages do not add up to 100 percent due to rounding.

GSA was more likely to meet its initial estimate of fair market value for high-value industrial and commercial properties. Specifically, from October 2013 to November 2025, GSA met or exceeded its initial estimate of fair market value for:

· 87 percent of industrial sales and 86 percent of commercial property sales,

· 68 percent of residential property sales, and

· Between 88 and 100 percent of all other property type sales.

According to GSA officials, there are several reasons why sales revenue might not meet initial estimates of fair market value. For example, officials said most of the residential sales that did not meet GSA’s estimate were properties owned by agencies that had their own disposal authority. In those sales, according to officials, agencies determine the property’s appraisal value, thus limiting GSA’s ability to ensure the estimates are accurate. In addition, officials said federal agencies that own the properties provide GSA with a final approval on a sale offer, which can influence the final sales price.

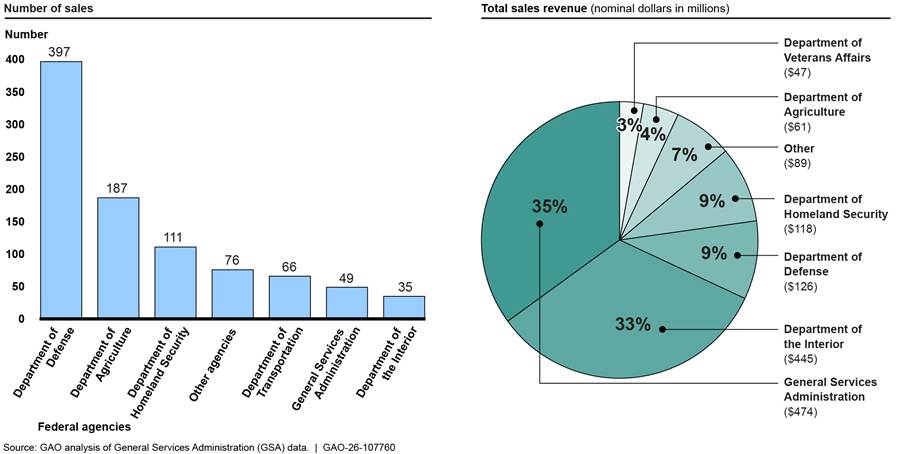

Agency. While most properties GSA sold since 2013 were owned by other federal agencies, sales of GSA-owned properties generated the most revenue of any single owner. Specifically, GSA-owned properties made up 5 percent of all properties it sold but made up more than one third of the total revenue ($474 million out of $1.4 billion) (see fig. 6). This is driven by higher value commercial properties GSA has sold, with half of them selling for $1.1 million or more.[28] About 75 percent of the properties GSA sold were owned by the Departments of Defense, Agriculture, and Homeland Security; these properties included a range of property types but were mostly low to moderate-value residential and multi-residential properties, of which half sold for $113,000 or less.

Figure 6: Total Number of GSA Real Property Sales and Revenue by Owning Agency, October 2013–November 2025

Notes: For total number of sales, “Other agencies” includes the Departments of Commerce, Education, Energy, Health and Human Services, Justice, and Labor; Environmental Protection Agency, National Aeronautics and Space Administration; National Credit Union Administration; and United States Postal Service. For total sales revenue, “Other agencies” includes the aforementioned agencies and the Department of Transportation.

GSA Sold Most Properties Using Online Auctions Due to Lower Costs

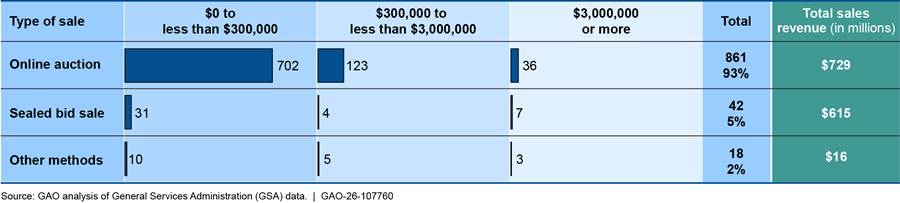

GSA primarily uses online auctions and, to a much lesser extent, sealed bids to conduct sales.

· GSA used online auctions for about 93 percent of sales since 2013, a majority of them for low-value properties (see fig. 7). Properties sold via online auction accounted for $729 million (54 percent) of total sales revenue.

· GSA has also used the sealed bid approach for 5 percent of sales since 2013, particularly for a few higher-value sales. Properties sold using sealed bids accounted for $615 million (45 percent) of total sales revenue.

Figure 7: GSA Real Property Sales by Sales Method and Sales Revenue Range, October 2013–November 2025

Note: The “Other” category includes live auctions and other types of sales methods that were infrequently used.

GSA officials said GSA’s online auction was the preferred sale method due to the low cost of using the website and the ability to hold a competitive, public sale on a national level. Officials pointed to a 2020 GSA-contracted study that examined the cost effectiveness of its online auctions compared to practices used in the private sector.[29] The report found that GSA’s online auctions had low transaction costs compared to sales practices used in the private sector, such as by private real estate brokers.

Limitations with GSA’s cost data—discussed later in this report—prevented us from completing a comprehensive cost analysis of different sales methods. However, we were able to analyze costs for 35 high-value sales ($3 million or more) and found online auctions cost less to complete than sales via sealed bid.[30]

· Thirty of these properties were sold through online auctions; half of them with costs of about $90,000 or less. These sales cost an average of 1 percent of the sale price, ranging from below 1 percent to 8 percent.

· Five of these properties were sold using sealed bids; half of them with costs of about $104,000 or less. These sales cost an average of 2 percent of the sale price, with a range of below 1 percent to 8 percent.

GSA recently tasked private brokers to assist with selling properties on its behalf. As of November 2025, GSA had planned four private broker-led sales which may cost the agency up to 3.5 percent of the sale price, depending on the sale price range and if brokers offer discounted pricing.[31] Further, GSA officials said GSA incurs costs while they pay for the use of private brokers to lead the sale. For example, officials said GSA staff manage any historical or environmental preparation issues while brokers primarily focus on the marketing and carrying out the sale. Additionally, officials said GSA staff travel to attend broker-led tours of the property at the property owner’s request.

In addition to cost considerations, GSA officials also said they preferred online auctions due to their flexibility, including how a sale can be designed to allow GSA to set different bidding and timing rules for each sale. For example, GSA may use a “24-hour” inactivity rule that either awards or extends an auction depending on whether a bid was received within a 24-hour period. Officials said the 24-hour rule can generate competition between bidders and escalate the sale price.

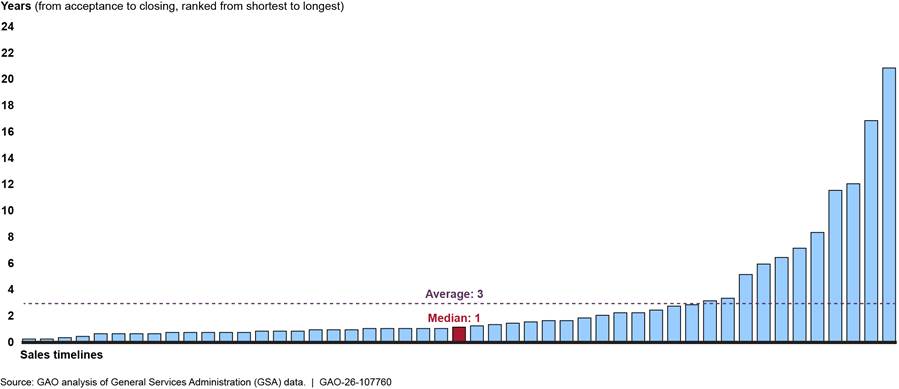

Preparing GSA-Owned Properties for Sale Took Substantially More Time Than Selling Them

According to sales data of GSA’s owned properties, two-thirds of the time needed to dispose of and sell federal property on average occurred during the initial disposal preparation of the property. As described earlier, GSA’s public sale of real property is the final step in a longer disposal process.

For the 49 GSA-owned properties that GSA sold from October 2013 through November 2025:[32]

· About half (25) of the 49 properties had disposal timelines of about 1 year or less (see fig. 8).[33]

· Two of the properties sold in 2025 were identified for the accelerated disposal approach. One of these sales, a commercial office building in Racine, Wisconsin, took about 1 year to complete the overall disposal, with four months to complete the online auction and final closing. The other sale, a federal courthouse in Des Moines, Iowa, took about 2.5 years to complete the disposal from when GSA accepted the property, with 2 months to complete the online auction and four months for its final closing. The courthouse timeline was more than twice as long as half of the disposals of GSA-owned properties in our analysis of 49 sold properties. Officials said GSA had to wait to initiate the courthouse’s sale due to a delayed construction of a new courthouse.

· Eleven properties had timelines above the average of about 3 years, ranging from 3 years to over 20 years. For one building that took 7 years to prepare and sell, officials attributed the lengthy timeline to a debate between local parties on how the building should be used once it was sold. GSA’s data also showed another building with a 20-year timeline that officials attributed to the property being in an “inactive” status in their system. In that example, GSA officials said they transferred the building to a local organization in a public benefit conveyance and believed the disposal was completed. However, the organization returned the property to GSA many years later after reporting to GSA it could no longer maintain it, according to officials. Officials said other properties may be labelled as inactive or on hold for disposal until an environmental remediation is completed.

Figure 8: Number of Years to Prepare and Close Sales of GSA-Owned Properties, October 2013–November 2025

Selling properties using online auctions, from initiating the auction to the sale’s final closing date, accounted for about one-third of the overall disposal timeline on average in 33 sales with available auction data.[34] For example:

· Completing the auctions and financial closing periods took an average of about 5 months, with a range of 2 months to about 1 year.

· Selling properties using the sealed bid method, from the award date to the final closing date, accounted for 17 percent of the disposal timeline on average for the 5 sealed bid sales of GSA-owned properties. Combined, these closing periods for sealed bids averaged 4 months, with a range of 1 month to 7 months.

We have previously reported on the longstanding challenges in federal real property disposals that can result in long timelines.[35] Officials identified similar challenges they have experienced that can add to the time it takes to prepare and sell a property:

· Securing funds for an agency to relocate is the most common reason disposals are delayed. Absent secured funding for the agency to relocate, GSA officials said they cannot move forward on disposal of a tenant-occupied property.

· Additional time may be needed for some properties to resolve issues related to environmental remediation or historic preservation requirements. For example, officials said the disposal timeline will be extended if a property has historic preservation requirements and interested buyers intend to repurpose the building.

· Officials said disposals are typically delayed the longest when a federal, state, or local entity is interested in a property transfer or using the property for public benefit purposes. For example, officials described the disposal of a large warehouse in a major metropolitan area that was delayed for multiple years. Officials said the delays were due to other federal agencies expressing interest in the property and a request by the city to use the site for homeless assistance. Officials said once these options were ruled out, GSA then sold the property about a year later.

GSA Aims to Accelerate Disposals but Has Not Established Performance Goals for Its New Approach

GSA Made Changes to Accelerate Disposals Amidst Staffing Reductions

GSA has taken initial steps to change its disposal and sales process, including creating a new disposal plan and website for properties it intends to sell on an accelerated timeline. In spring 2025, GSA developed a high-level plan that outlines its overall priorities for its accelerated disposal process, citing a need for an aggressive and data-driven analytic approach to carrying out disposals.[36] To gain greater oversight over decisions, officials said they centralized control for managing disposals and sales. Specifically, officials said they enhanced coordination between leadership at the headquarters level and regional project teams managing decisions on how to sell properties. In addition, GSA officials noted ongoing efforts to examine existing processes and regulations to identify ways to streamline property disposals. As described above, after we completed our audit work in November 2025, GSA rescinded a majority of regulations implementing its disposal authorities with the intent to streamline its disposal process, according to GSA.[37] Our review did not include an analysis of these regulatory changes or analyze their potential impact.

GSA also created a new website that identifies properties for an accelerated disposal approach.[38] Officials said they published a list of these properties on GSA’s website to: (1) encourage tenants to begin identifying relocation strategies, and (2) generate market interest among prospective buyers by announcing that GSA intends to dispose of properties in the future. This list of properties marks a shift in GSA’s prioritization of disposal projects to focus more on commercial office space. While GSA’s sales of commercial properties generally decreased from 2018 to 2024, commercial sales made up a higher proportion of total sales in 2025 than previous years. And, as of March 2026, 41 of the 47 properties on the new website were commercial office properties (about 90 percent).[39] To prepare for the increase in commercial properties, GSA officials said they planned to increase the use of private brokers to sell properties on GSA’s behalf. We describe these efforts in further detail below.

While GSA began making changes to its disposal and sales approach, it also sustained significant staffing reductions that created new challenges, according to GSA officials. In March 2025, GSA’s Public Buildings Service began a major reorganization, which has included reducing staff levels by about 50 percent.[40] As of September 2025, GSA officials told us that the office that manages real property disposals had lost about one-third of its staff since January 2025, going from 75 staff to 48 staff, including from five appraisers to two appraisers.[41] GSA officials cited a range of new challenges from the staffing reductions:

· Knowledge gaps. Staff have struggled to locate or use previously completed work needed to manage disposals. For example, officials said asset managers have had to fill in for departed staff on projects outside their regional area of expertise, such as an asset manager located in the Midwest also managing disposals in a major market in the Southeast. In this instance, staff have had to restart the disposal process, including developing and procuring new reports such as title and environmental remediation studies. In another case, a property sale stalled because the team managing the sale left GSA, and it was unclear whether the necessary work to help the tenants relocate had been completed. As a result, GSA had to restart the disposal process for this property. Officials also said some GSA staff responsible for processing disposals of GSA-owned properties left the agency, creating uncertainty on whether properties were properly vetted and approved to begin the process. To address these knowledge gaps, GSA officials responsible for real property disposal stated that they were working with the office within GSA that manages the strategy and performance of its owned properties to determine the readiness of properties for disposal.

· Limited capacity for preparing properties. Officials stated that having fewer staff located across the country has created challenges in accessing and preparing properties for sale. For example, officials said they could not provide timely access or tours of a property being sold by private brokers because there were no GSA staff in the area. In addition, officials said reduced staff in different locations combined with lower travel budgets has resulted in fewer visits to properties to confirm critical information on the condition of properties slated for disposal, such as historical designation or any needed environmental mitigation. As a result, officials said there is an increased risk that a property may be put up for sale before important issues that could have been discovered earlier in the process are resolved, potentially resulting in longer disposal timelines.

· Service delivery. Officials said GSA had to reduce technical support to other agencies and prioritize helping agencies to prepare their properties for disposal. Officials said their office had typically hosted several workshops a year providing analytical and technical support to agencies seeking assistance. As a result, agencies may be less prepared for GSA’s disposal process, according to officials.

GSA Does Not Have Performance Goals, Use Quality Data, or Fully Assess Results in Its New Approach to Disposals and Sales

In prior work, we identified key policymaking practices that can help executive agencies manage and assess the results of federal efforts by developing and using evidence.[42] We selected three of these key practices as relevant to GSA’s efforts to reevaluate its disposal strategy under the accelerated disposal approach: (1) define an activity’s purpose and goals, (2) assess and improve evidence quality; and (3) use evidence to understand and inform results. These key practices can help federal agencies, including GSA, plan for results, develop data as evidence, and inform decision makers on whether approaches are effective. These key practices could better position GSA to achieve its desired results for its disposal and sale planning efforts.

As previously stated, GSA has begun an effort to reevaluate and make changes to its strategic approach with an emphasis on accelerated disposals and sales. However, our analysis of the initial steps GSA took to change its disposals and sales process found GSA did not fully follow the three selected key practices for planning for results, as described below.

Define an activity’s purpose and goals. An agency should define an activity’s purpose and goals, communicating the results that an organization seeks to achieve.[43] GSA has generally defined the purpose of its accelerated approach as accelerating the process for disposing of properties. However, its stated approach for accelerating the process has changed over time. In March 2025, GSA’s website stated that the approach aims to dispose of properties that are obsolete or unsuitable to use, but also to engage the market, attract interested parties, and inform strategies that will expedite disposals. In May 2025, GSA officials told us that this approach aimed to expedite the overall disposal of federal assets. Officials also said they were reviewing preparation steps in the disposal process for ways to resolve issues such as environmental remediation earlier. However, in September 2025, officials told us the approach was focused only on accelerating the pace of identifying federal properties for disposal, not to expedite the overall steps to dispose of unneeded properties. As of February 2026, how GSA plans to expedite disposals remains unclear.

While GSA has generally defined the purpose of the accelerated approach, it has not established performance goals linked to the approach. For example, GSA’s fiscal year 2026 performance plan—a key document in which GSA identifies its strategic goals, objectives, and performance measures—does not refer to the accelerated approach, nor does it have goals or measures that define the outcomes GSA hopes to achieve through its new approach. GSA has continued to measure projected sales revenue from disposals in the last 5 years of GSA’s annual performance reports, including the 2026 report.[44] However, the fiscal year 2026 performance plan does not have goals linking the accelerated approach with efforts to improve the timeliness of disposals. Further, the plan does not identify benefits that could be achieved from accelerating disposals, including reducing two significant drivers of property management costs: annual operations and maintenance costs and deferred maintenance and repair:

· Annual operations and maintenance. According to GSA, the accelerated approach could potentially save GSA tens of millions of dollars in avoided annual operating and maintenance costs. As of November 2025, GSA has sold two of its own properties in 2025 that demonstrate the potential benefit GSA could target. According to GSA press releases, these two sales have saved GSA about $5 million in total annual operation and maintenance costs and a combined $134 million in needed repairs over 10 years.

· Deferred maintenance and repair. Federal agencies may postpone or defer annual maintenance or needed repairs, depending on available funding or mission needs. We have reported that the backlog of deferred maintenance and repair projects across the federal government more than doubled between 2017 and 2024, from $170 billion to $370 billion.[45] And, in December 2025, GSA estimated deferred maintenance and repair costs for its own properties had risen to about $26 billion.[46] While this estimate represents all GSA-owned properties, selling the unneeded or obsolete properties could help GSA address the backlog of deferred costs. For governmentwide properties on GSA’s list of accelerated disposals, GSA estimates agencies could avoid at least $3 billion in deferred maintenance and repair costs over a 10-year period through completed sales of the properties.

Officials said they had not yet developed goals or measures for the accelerated disposal approach because they are waiting for a period of stability following leadership changes and staffing reductions at GSA. Officials also stated that the Office of Management and Budget encouraged agencies to briefly define performance measures in their annual performance plans in an effort to focus on fewer, more targeted goals. For example, GSA discontinued a performance goal for 2026 that measured avoided building operations costs through disposals.[47] Officials stated they will consider adding performance goals on the accelerated disposal approach in the future but noted several data reliability concerns. For example, GSA identified data quality issues with government-wide cost data, which we describe in further detail below.

As GSA considers what improvements it hopes to achieve through the accelerated approach, targeted and measurable goals could help the agency clarify how it plans to accelerate and simplify disposals and gain greater cost savings. As described earlier, the amount of time it took for GSA to prepare and sell GSA-owned properties varied, with some sales occurring in months and others taking several years. While a variety of factors can affect a disposal schedule, GSA can leverage its timeline data to set reasonable schedule targets for the accelerated approach based on a property’s characteristics and the remaining work needed for its disposal. Taking this step could help GSA assess whether disposal projects that share similar characteristics are on schedule and target disposal strategies to ensure more timely outcomes. Similarly, by setting cost savings targets for disposals that eliminate operations and maintenance expenses, GSA can more clearly demonstrate to the public and Congress the costs it is saving annually by disposing of properties in an accelerated manner.

Assess and improve evidence quality. An agency should assess the quality of its information and, if necessary, develop a data improvement plan.[48] Ensuring GSA’s sales data contains complete and accurate information can help management evaluate whether changes to its disposal approach lead to improved outcomes. However, our analysis of GSA sales data found data necessary to understand disposal timelines and costs were often missing. For example, we found incomplete disposal closing dates in 55 of 327 sales (17 percent) from 2018 to 2024. Similarly, GSA’s data had incomplete cost information for 172 of 327 sales (53 percent) over the same time period. In addition, we found three properties sold that were not recorded in GSA’s sales system.

According to officials, GSA has experienced challenges in managing the quality of disposal data due to having disparate systems across the country. For example, officials said GSA does not track disposal and sale costs in one centralized system, and regional offices have tracked costs differently.[49] Officials said it was also unclear in sales occurring several years prior if staff had consistently tracked hours worked on their timecards when preparing and closing sales.[50] Officials further said staffing reductions have hindered their ability to effectively oversee sales data. Specifically, the office’s lead data analyst responsible for managing its sales system data left GSA during the deferred resignation program in spring 2025, according to officials.

To address data quality issues, GSA officials said they have taken several steps. Specifically:

· Officials said they created project billing guidance that they believe has improved the collection of certain information in recent years, such as costs incurred by GSA when preparing and selling a property.

· Officials described efforts to retroactively confirm and verify the accuracy and completeness of sales data, but noted staff have had to prioritize updating information for properties currently in the disposal process over reviewing information for closed sales. Officials said they are considering adding data accuracy as part of annual performance evaluations for staff to elevate the importance of accurate data.

· GSA requested information from technology vendors in September 2025 on ways to modernize its real property data systems. In this request, GSA stated it plans to improve the efficiency of its disposal activities, including reducing costs to hold properties, achieving faster disposal timelines, increasing revenue in sales, and improving real property data management, among other things.[51]

However, as of November 2025, GSA had not developed a plan for project teams managing disposals to verify that data are complete and accurate. Officials acknowledged they have developed policies and best practices guiding other aspects of the disposal program. However, officials noted that GSA leadership had directed staff to pause developing new policies in 2025 while the agency is undergoing significant organizational and workforce changes.

Establishing and implementing a plan to ensure the quality of the disposal and sales data would allow GSA to better analyze the disposal and sales results and identify any needed changes to improve the implementation of its accelerated disposal approach. Further, by having more complete and accurate data, GSA would be better informed on which disposals and sales are suitable to accelerate through the process.

Use evidence to understand results and inform decisions. An agency should use data as evidence to understand why results were or were not achieved and leverage the data to inform decisions.[52] Data-driven reviews can help management determine if strategies are performing as planned or if there is an opportunity to make adjustments to existing methods and drive improvements where performance declines.

As described earlier, GSA has used its auction website in the vast majority of its real property sales (about 93 percent), primarily due to this sales method’s low cost to GSA. In spring 2025, however, GSA began contracting with private real estate brokers to take the lead in selling a few federal properties. Previously GSA had used brokers to assist in the marketing of properties or other minor aspects of the sale, but officials had not used them to take steps to carry out the sale, because they believed brokers were less cost effective and could potentially result in longer timelines. For certain properties, however, officials said there are advantages in broker-led sales, including: (1) developing marketing materials for complex and unique features and (2) working with architectural firms to find ways to reuse properties. In addition, officials said using private brokers to lead sales would help alleviate GSA’s limited capacity resulting from the recent staffing reductions. In 2025, GSA awarded a blanket purchase agreement to 10 real estate companies to obtain a range of services, including tasking brokers to provide sales-related services to assist in disposing of real property assets, according to officials.

As of November 2025, officials told us that GSA had issued orders to private broker companies to market and seek offers for the sale of four federal properties on GSA’s behalf.[53] As of November 2025, none of the four sales had yet closed. Therefore, GSA had not yet had an opportunity to evaluate using private brokers as a sales method in comparison to its other sales methods.[54] GSA officials said they planned to evaluate the performance of private brokers in comparison to its other sale methods after about one year of broker-led sales. However, officials said they had not yet determined how they would conduct the evaluation. Among the measures officials said they are considering are how well brokers assisted GSA in meeting its sales revenue goals, the length of time it took GSA and the brokers to complete the sales, and the cost of the brokers’ services.

As GSA completes these sales with the assistance of private brokers, assessing broker completed sales would enable it to understand if the desired results were achieved. Using the performance data that GSA collects from the completed sales can help determine whether the use of private brokers as a sales method, in comparison to its other sales methods, is an efficient and cost-effective option to use for completing sales. For example, GSA could evaluate and compare the average costs to pay brokers to carry out sales or average timelines for completion to the performance of comparable GSA-led sales in which GSA used its own staff and auction website. GSA can then make more informed decisions on which sales methods to use to generate the most advantageous sales price and pursue cost effective sales options. Information from these assessments could help inform management on the adjustments GSA should make to ensure its sales methods are as efficient and effective as possible under the new accelerated approach.

Conclusions

Federal agencies pay millions of dollars to maintain buildings that are not needed for their mission. Disposing of them can also take several years to complete. Deferred maintenance and repairs for these properties are estimated to cost billions of dollars. Since 2013, GSA has assisted agencies in selling hundreds of these properties, generating more than $1 billion in revenue. While notable, GSA now has fewer staff managing disposals and continues to face longstanding challenges in disposing of unneeded real property, which can result in lengthy and costly delays.

While GSA is in a period of change, the new accelerated disposal approach may help the agency identify and dispose of properties more efficiently and effectively. However, GSA has not established goals that could result in potential benefits from timelier outcomes.

Implementing a new approach successfully also requires quality information and leveraging that information to inform decision making. However, several important gaps in GSA’s sales data remain. Implementing a data improvement plan would provide GSA a more accurate and complete picture of the characteristics of successful disposals and better enable it to identify which properties could be suitable for accelerated disposal in the future.

Finally, as GSA tests sales strategies under the new approach, such as using private brokers to lead sales, it has an opportunity to evaluate what method provides the best results. A review of the benefits and costs of different sales strategies could help GSA understand if a strategy is performing as planned and inform any needed adjustments.

Recommendations for Executive Action

We are making the following three recommendations to GSA:

The Administrator of GSA should ensure the Public Buildings Service establishes performance goals for GSA sales that link to the accelerated disposal approach. Such goals could address obtaining maximum value for the property, timeliness of project schedules, reducing deferred maintenance and liabilities, and avoided operations costs for properties from completed disposals and sales. (Recommendation 1)

The Administrator of GSA should ensure the Public Buildings Service establishes and implements a plan to ensure that disposal and sales data are of sufficient quality to assess the accelerated disposal approach. (Recommendation 2)

The Administrator of GSA should ensure the Public Buildings Service, where applicable, evaluates the effectiveness of using private real estate brokers to lead real property sales in comparison to other GSA-led sales methods. Such an evaluation could include an examination of information from both GSA-led sales and broker-led sales on sales revenue generated, timeliness of completing the sales, and the costs of the brokers’ services versus GSA-led sales. (Recommendation 3)

Agency Comments

We provided a draft of this report to GSA for review and comment. GSA provided written comments, reprinted in appendix II.

In its written comments, GSA agreed with our three recommendations and provided information about activities that GSA would undertake to implement our first and third recommendations. Specifically, in response to our first recommendation, GSA stated that it had begun efforts to develop new performance measures to track (1) avoided costs and (2) timeliness of disposals and sales. In response to our third recommendation, GSA stated that it plans to monitor the effectiveness of using real estate brokers to carry out its sales of unneeded federal real property. We will review GSA’s efforts to address these recommendations once they are finalized. GSA also provided technical comments, which we incorporated as appropriate.

We are sending copies of this report to appropriate congressional committees and the Administrator of the GSA. In addition, the report is available at no charge on the GAO website at http://www.gao.gov.

If you or your staff members have any questions about this report, please contact me at MarroniD@gao.gov. Contact points for our Offices of Congressional Relations and Media Relations may be found on the last page of this report. GAO staff who made key contributions to this report are listed in appendix III.

David Marroni, Director

Physical Infrastructure

This report examines (1) how the General Services Administration (GSA) sold excess real property from 2013 to 2025, and the results and (2) how GSA plans to sell federal real property under its accelerated disposal approach, and the extent that changes to its process meet selected key practices for evidence-based policymaking.

To describe the methods and results from GSA’s sales of real property, we analyzed GSA’s sales data for all completed sales from October 2013, the earliest data were available, through November 30, 2025.[55] We analyzed the data to identify characteristics of the sales, including (1) methods used to complete the sales, (2) types of property sold, (3) agencies that owned the properties, (4) costs incurred by GSA in preparing and completing the sale, and (5) the length of time it took to prepare properties for disposal and sell them. To assess the reliability of the data, we reviewed related GSA documentation such as data dictionaries, performed electronic testing and logic checks, and interviewed GSA officials to understand the data and systems used.

In reviewing the sales data, we found a select group of variables were reliable for reporting the characteristics of sales from October 2013 through November 30, 2025. These included sales revenue, method, property type, and agencies owning the properties. In instances where we identified incomplete information from GSA’s central database, we requested GSA use individual records to provide updated data and ensure our analysis included complete information.

We determined other variables were unreliable due to many missing values (e.g., cost data for older sales), which limited our ability to extend an analysis across multiple variables. For example, the cost data do not include itemized costs for all sales within our analysis, and therefore, we limited the scope of our analysis on costs. Additionally, due to incomplete timeline information for all sales, we limited our analysis to the most reliable timeline data in the 49 sales of GSA-owned properties occurring from October 2013 through November 2025. Of the 49 sales of GSA-owned property, GSA sold 44 using online auctions and five using sealed bids. We reviewed online auction bidding data for 33 of the 44 sales to identify the percentage of the disposal timelines that were associated with carrying out the sales on GSA’s auction website or using the sealed bid method.[56]

To describe how well GSA met its annual performance goal for revenue, we assessed GSA sales data from October 2013 through November 2025 to identify the extent to which GSA met the estimated fair market value GSA identified for each property sale. We assessed GSA’s performance in meeting these initial estimates by sales value and property type. While GSA does not measure performance in meeting these initial estimates for individual sales, we evaluated the extent to which sales met these values because GSA uses the estimates to set gross revenue goals for all expected disposals in upcoming budget years.

To identify and assess GSA’s plans under its accelerated disposal approach and the extent that they met selected key practices for evidence-based policymaking, we reviewed GSA documentation and its website to describe GSA’s revised disposal approach.[57] We reviewed GSA’s annual performance and budget documentation to identify annual performance goals and measures related to disposals and sales of federal real property. We reviewed GSA documentation to identify whether GSA has created new goals, sales methods, and plans to oversee and assess progress toward its accelerated approach. We also reviewed GSA documentation to identify estimates of deferred maintenance and liabilities costs and annual operating and maintenance costs for the properties GSA intends to dispose of using the accelerated approach.

We assessed this information against selected key practices for evidence-based policymaking.[58] These selected practices were defining an activity’s purpose and goals, assessing and improving evidence quality, and using evidence to understand results and inform decisions. We selected key policy making practices relevant to the timing and progress of GSA’s efforts to establish and oversee the revised approach. In addition, we interviewed GSA officials for additional context and perspectives on GSA’s real property sales process, associated challenges, and the accelerated disposal approach.

In performing our assessment, we assessed GSA’s plans as meeting or not meeting selected policy making key practices based on GSA-provided documentation, sales data, and information on its website describing the new accelerated approach. We shared our preliminary results with GSA officials. Officials subsequently provided additional documentation and clarification. When warranted, we updated our analyses based on GSA responses and the additional information provided.

We conducted this performance audit from August 2024 to April 2026 in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

David Marroni at MarroniD@gao.gov

In addition to the contact named above, Matt Cook (Assistant Director), Michael Sweet (Analyst-in-Charge), Emily Crofford, Adrian Good, Terence Lam, Susan Murphy, Joshua Ormond, Amy Rosewarne, Ben Theuma, Frances Tirado, Alicia Wilson, and Elizabeth Wood made key contributions to the report.

The Government Accountability Office, the audit, evaluation, and investigative arm of Congress, exists to support Congress in meeting its constitutional responsibilities and to help improve the performance and accountability of the federal government for the American people. GAO examines the use of public funds; evaluates federal programs and policies; and provides analyses, recommendations, and other assistance to help Congress make informed oversight, policy, and funding decisions. GAO’s commitment to good government is reflected in its core values of accountability, integrity, and reliability.

Obtaining Copies of GAO Reports and Testimony

The fastest and easiest way to obtain copies of GAO documents at no cost is through our website. Each weekday afternoon, GAO posts on its website newly released reports, testimony, and correspondence. You can also subscribe to GAO’s email updates to receive notification of newly posted products.

Order by Phone

The price of each GAO publication reflects GAO’s actual cost of production and distribution and depends on the number of pages in the publication and whether the publication is printed in color or black and white. Pricing and ordering information is posted on GAO’s website, https://www.gao.gov/ordering.htm.

Place orders by calling (202) 512-6000, toll free (866) 801-7077,

or

TDD (202) 512-2537.

Orders may be paid for using American Express, Discover Card, MasterCard, Visa, check, or money order. Call for additional information.

Connect with GAO

Connect with GAO on X,

LinkedIn, Instagram, and YouTube.

Subscribe to our Email Updates. Listen to our Podcasts.

Visit GAO on the web at https://www.gao.gov.

To Report Fraud, Waste, and Abuse in Federal Programs

Contact FraudNet:

Website: https://www.gao.gov/about/what-gao-does/fraudnet

Automated answering system: (800) 424-5454

Media Relations

Sarah Kaczmarek, Managing Director, Media@gao.gov

Congressional Relations

David A. Powner, Acting Managing Director, CongRel@gao.gov

General Inquiries

[1]GAO, High-Risk Series: Heightened Attention Could Save Billions More and Improve Government Efficiency and Effectiveness, GAO‑25‑107743 (Washington D.C.: Feb. 25, 2025). Managing real property has remained on our High-Risk List since 2003 due in part to challenges with disposing of federal real property.

[2]Federal law requires federal agencies to identify and report excess real property. 40 U.S.C § 524. Once excess real property has been identified as surplus, GSA is required to supervise and direct its disposition. Id. § 541.

[3]The percent of sales from disposals is based on data presented in GSA’s fiscal year 2023 performance report covering fiscal years 2019 through 2023. See General Services Administration, Public Buildings Service, FY 2023 Performance Overview, Office of Real Property Disposition, (Washington, D.C.).

[4]GSA’s real property auction website can be accessed at https://realestatesales.gov/.

[5]Until December 2025, GSA’s Federal Management Regulation laid out a detailed process for disposing of such property. 41 C.F.R. part 102-75 (2024). The majority of these regulations have been rescinded. See Federal Management Regulation; Aligning the Federal Management Regulation (FMR) With the Administration's Deregulatory Priorities, 90 Fed. Reg. 58,408 (Dec. 16, 2025). see also 91 Fed. Reg. 3214 (Jan 20, 2025) (ratification notice). For the purposes of our report, we did not assess how the removal of these regulations would affect GSA’s management of its disposal and sales process. We describe the process GSA used throughout our review period, including relevant portions of 41 C.F.R part 102-75. We also footnote statutory provisions and include reference to those regulatory provisions that still exist.

[6]GAO, Evidence-Based Policymaking: Practices to Help Manage and Assess the Results of Federal Efforts, GAO‑23‑105460 (Washington, D.C.: July 12, 2023).

[7]Statute provides that the Administrator of General Services (Administrator) is to supervise and direct the disposition of surplus property, with some exceptions. 40 U.S.C. § 541. 41 C.F.R. §§ 102-75.5; 102-75.296 (2024). GSA’s previous regulations encouraged agencies with independent disposal authority “to obtain utilization, disposal, and related services from those agencies with expertise in real property disposal, such as GSA, as allowed by 31 U.S.C. § 1535 (the Economy Act), so that they can remain focused on their core mission.” 41 C.F.R. § 102-75.20 (2024).

[8]As noted above, our review did not evaluate changes in GSA’s December 2025 disposal process following GSA’s changes to its real property disposal regulations.

[9]GSA’s Office of Real Property Disposition manages the disposal process, including federal properties that are identified for disposal by GSA or other landholding agencies. GSA’s Office of Portfolio Management manages properties for which GSA is the landholding agency and works with the Office of Real Property Disposition once properties are identified for disposal. Our summary of the disposal process reflects discussions with officials, as well as relevant legal authorities.

[10]Each executive agency is required by statute to, among other things, continuously survey property under its control to identify excess property, promptly report it to GSA. 40 U.S.C. § 524(a)(2), (3); 41 C.F.R. § 102-71.145. Agencies make this determination in a “Report of Excess” submitted to GSA, which GSA was required to review to determine if it was prepared adequately and complies with GSA’s disposal regulations.

[11]GSA could accept the report as adequate, determine the report is insufficient, or accept on a conditional basis and identify deficiencies that must be addressed. Following an initial review of the property and its circumstances, such as through site visits, GSA could then formally “accept” the property in its disposal process. We further discuss this “acceptance date” in our analysis in the report.

[12]Per relevant statute, surplus property may be disposed of by “sale, exchange, lease, permit, or transfer, for cash, credit, or other property, with or without warranty, on terms and conditions that the Administrator considers proper.” 40 U.S.C. § 543.

[13]Title V of the McKinney-Vento Homeless Assistance Act, as amended, contains provisions that enable the transfer of certain unutilized, underutilized, excess, and surplus property to assist the homeless. 42 U.S.C. §11411. Screening property to determine if it is suitable for this purpose is required by the statute. Id. See also associated regulations in 41 C.F.R. Part 102-71, subpart B (previously 41 C.F.R. Part 102-75 subpart H (2024)) (GSA); 24 C.F.R. Part 581 (Department of Housing and Urban Development); 45 C.F.R. Part 12a (Department of Health and Human Services).

[14]Various provisions of federal law authorize disposal of surplus property for specified public benefit conveyance uses. See, e.g., 40 U.S.C. § 550(c) (educational use); 40 U.S.C. § 550(e) (public park or recreation area use); 40 U.S.C. § 550(h) (historic monument use).

[15]40 U.S.C. 545(b)(8). Negotiated sales may also be conducted in other limited circumstances, such as if the fair market value does not exceed $15,000 or if the character or condition of the property make it impractical to advertise for competitive bids. Id.

[16]Under statute, GSA must generally publicly advertise for bids, under regulations the Administrator prescribes. 40 U.S.C. § 545(a). The time, method, and terms and conditions of advertisement permit full and free competition consistent with the value and nature of the property involved. Id.

[17]According to GSA officials, live auctions are not commonly used. GSA may use this method when a client or stakeholder requests a live auction.

[18]Under statute, GSA may use contract realty brokers for disposal of surplus real property, and when used, these disposals shall be made in the manner followed in similar commercial transactions under regulations the Administrator prescribes. 40 U.S.C. § 545(c). The regulations must require that brokers give wide public notice of the availability of the property for disposal. Id. Pursuant to the Federal Acquisition Regulation (FAR), brokers are not allowed to complete some activities, as contractors cannot perform inherently governmental functions. For instance, brokers may not determine what Government property will be disposed of and on what terms. FAR 7.503(c)(11). GSA’s recent solicitations for brokers to assist in property disposal require the brokers to market the property and solicit offers, among other responsibilities, while leaving GSA the ultimate decision to accept or reject any or all offers.

[19]These figures are based on data in GSA’s Federal Real Property Profile Management dataset.

[20]We analyzed closed sales data from October 2013, the earliest available sales in GSA’s data, through November 2025. Due to limitations in closing date information, this analysis refers to closed sales in the year the sale was awarded, not the date the sale closed, which can occur up to 180 days after the date of award. In addition, the analysis in this report presents sales revenue in nominal dollars, and revenue figures are not adjusted for inflation.

[21]In our analysis, we use three value ranges to describe a property’s sale price: low-value (under $300,000), moderate-value ($300,000 to under $3 million), and high-value ($3 million or more). GSA uses similar ranges to guide its market planning for properties of differing value.

[22]This average includes sales completed from January through November 2025.

[23]Under FASTA, the independent Public Buildings Reform Board must submit a list of real property disposal recommendations to the Office of Management and Budget for approval. Upon approval, GSA is responsible for executing the approved recommendations.

[24]Starting in GSA’s Fiscal Year 2022 Annual Performance Report, GSA began tracking proceeds from all GSA-led disposals, not just disposals of GSA-owned properties.

[25]These initial market value estimates are used to determine the need for an appraisal performed by an outside contractor, the suggested marketing budget, and the inclusion of certain marketing plan elements. GSA also hires a third party to develop an appraised fair market value of the property that GSA uses for its final benchmark for the sale. For the purposes of this report, our analysis focuses on GSA’s initial estimates of fair market value as these estimates align to GSA’s projected sales revenue goals in its annual performance plan.

[26]Within this group, some properties sold for higher prices. For example, 15 multi-residential properties generated an average of $8.6 million in sales revenue, but half of them sold for $600,000 or less. Nineteen special use properties, such as a school or a research facility, generated an average of $1.5 million in sales revenue, with half selling for $583,000 or less.

[27]The 23 industrial and 119 commercial properties generated an average of $20 million and $5 million in revenue per sale, respectively.

[28]GSA owned properties generated an average of $9.7 million in revenue per sale.

[29]General Services Administration, Office of Real Property Utilization and Disposal, Online Sales Auction Website Effectiveness, (Sept. 2020). The study also cited benefits of GSA’s online auction, including a streamlined platform for GSA and bidders, enhanced transparency during bidding, and the flexibility the website provides in selling unique and low-value properties in remote locations where large private real estate brokers are less likely to operate. We did not assess the report’s methodology, evidence, or conclusions.

[30]We found the sales data since 2013 to generally have incomplete cost information, with older sales lacking information on costs. Although the sales data do not provide detailed information on costs for all sales within our analysis, we found the most reliable were related to 43 sales worth at least $3 million. Of these 43 sales, we excluded eight sales from our analysis due to incomplete cost information and to remove “other” sales methods. We analyzed the costs of the remaining 35 sales, which GSA sold using its auction website (30 properties) and through the sealed bid method (five properties). Our analysis focuses on the 35 high-value sales sold on the auction website and sealed bid approach because these methods represent more than 98 percent of GSA’s sales by volume.

[31]With no sales yet closed through November 2025, we could not compare actual costs from these private broker-led sales. Commission rates vary across the different companies. Based on our review of commission rates provided by GSA for five of the 10 real estate companies under agreement with GSA, companies generally charge a lower percentage rate for higher value sales and a higher percentage rate for lower value sales.

[32]Sales of GSA-owned properties made up 5 percent (49 out of 921) of all sales from October 2013 through November 2025. Our timeline analysis focused on these sales due to the availability of data, which was not consistently reported for sales of properties owned by other agencies. Of the 49 sales of GSA-owned property, GSA sold 44 using online auctions and five using sealed bids.

[33]The starting date for our analysis uses the date when GSA formally accepted a Report of Excess from another agency requesting GSA carry out a disposal. The end date is the date that the sale is financially closed and completed. According to officials, agencies and GSA typically take preliminary steps to complete due diligence activities on a possible disposal prior to GSA accepting the Report of Excess. This analysis does not include this informal part of the disposal process.

[34]We analyzed GSA’s sales data and auction website for 33 online auction sales of GSA-owned properties from October 2015 through November 2025. We excluded 11 sales from 2014 to 2015 within this group due to missing auction data for these sales.

[35]See GAO, Federal Real Property: GSA Should Leverage Lessons Learned from New Sale and Transfer Process, GAO‑23‑104815 (Washington, D.C. Oct. 7, 2022) and GAO, Federal Real Property: Additional Documentation of Decision Making Could Improve Transparency of New Disposal Process, GAO‑21‑233 (Washington, D.C. Jan. 29, 2021).

[36]Executive Order 14222 required GSA to develop and submit to the Office of Management and Budget a new plan for the disposition of Government-owned real property deemed by the agency as no longer needed. 90 Fed. Reg. 11,095 (Feb. 26, 2025).

[37]See Federal Management Regulation; Aligning the Federal Management Regulation (FMR) With the Administration's Deregulatory Priorities, 90 Fed. Reg. 58,408 (Dec. 16, 2025).

[38]The website can be found at: https://www.gsa.gov/real‑estate/real‑estate‑services/real‑property‑disposition/assets‑identified‑for‑accelerated‑disposition.

[39]Officials told us that almost all of these properties had been identified previously for disposal prior to being listed on the accelerated disposition website. This includes 31 properties that were publicly announced for disposition by GSA in 2023 and 2024 or included as recommendations by the Public Buildings Reform Board for disposal through the FASTA process.

[40]GAO, Federal Real Property, Successful Public Buildings Service Reorganization Is Critical for Addressing Longstanding Challenges, GAO‑26‑108785 (Washington, D.C.: Dec. 11, 2025). We have ongoing work assessing GSA’s reorganization efforts.

[41]Officials said the reductions were a result of employees electing to participate in the deferred resignation program (DRP), which provided employees an opportunity to voluntarily resign in exchange for ongoing pay and benefits through their resignation date, no later than September 30, 2025.

[44]General Services Administration, Fiscal Year 2026, Annual Performance Plan, (May 28, 2025).

[46]Cutting Costs, Adding Value: The Future of Federal Property, Before the House Committee on Transportation and Infrastructure, Subcommittee on Economic Development, Public Buildings and Emergency Management, 119th Cong. (2025) (statement of Andrew Heller Acting Commissioner of the Public Buildings Service of the U.S. General Services Administration).

[47]General Services Administration, Fiscal Year 2026, Annual Performance Plan, (May 28, 2025).

[49]GSA officials said agencies typically do not submit cost information when requesting a disposal.

[50]GSA officials said appraisal information was also previously stored across regions until 2024, when GSA implemented a policy that required staff to move appraisal data into a central data repository.

[51]In the request, GSA sought vendor input on commercial real estate software that could streamline GSA processes and improve data integration. General Services Administration, Request for Information, Strategic Replatforming and Modernization of GSA’s Real Estate Technology Portfolio, Sept. 30, 2025.

[53]As of November 2025, GSA issued orders for broker-led sales for the following properties: Gus J. Solomon U.S. Courthouse, Portland, Oregon; Federal Office Building, 7th and D, Washington, D.C.; Liberty Loan (Building), Washington, D.C.; and River Road Federal Office Building in Riverdale, Maryland.

[54]GSA officials told us they plan to assess performance of broker-led sales based on the objectives and deliverables in the contract documentation. The FAR requires that performance-based contracts for services include measurable performance standards (in terms of quality, timeliness, quantity, etc.) and the method of assessing contractor performance against performance standards. FAR 37.601. The FAR section that establishes procedures for agency evaluations of contractor past performance generally requires that agencies assess a contractor’s cost control and schedule/timeliness. FAR 42.1503(b)(2). The same section also requires agencies to evaluate a contractor’s quality of service, management, and small business subcontracting, if applicable. Id.

[55]According to GSA officials, GSA paused its disposal activities on October 1, 2025 until November 13, 2025, due to a lapse in appropriations.

[56]Due to missing auction data for 11 sales from 2014 to 2015, we excluded 11 sales and analyzed sales from October 2015 through November 2025.