Report to Congressional Committees

United States Government Accountability Office

A report to congressional committees

For more information, contact: Danielle T. Giese at GieseD@gao.gov

What GAO Found

Following the COVID-19 pandemic, the airline industry faced challenges filling pilot vacancies, which network and low-cost airlines addressed by hiring from regional airlines, according to the Federal Aviation Administration (FAA). Those regional pilots’ departures contributed to reductions in regional airline service to small communities, according to selected stakeholders. For example, one network airline told GAO that in 2022 it had to withdraw regional air service from 29 airports, many of which serve small communities. Several trends—like increased airline operating costs and travelers driving to their destination or to a larger airport—have also contributed to the decrease in regional air service to small airports and communities over the last 20 years, according to GAO’s prior work.

Data and selected stakeholders indicate that pilot supply has been rebounding in recent years. From 2017 through 2024, for example, pilot certifications grew about 10 percent, with most of the increase starting in 2021. In 2024, pilot hiring slowed at the network and low-cost airlines, in part due to aircraft delivery delays, according to selected stakeholders. This hiring slowdown may have allowed regional airlines to retain pilots and move toward pre-pandemic staffing levels. In addition, regional airlines significantly increased pay to attract and retain pilots, raising the average hourly rate for a first-year first officer from about $52 an hour in 2021 to about $93 an hour in 2024.

To help strengthen the pilot pipeline, the FAA Reauthorization Act of 2024 required FAA to take action on two pilot training initiatives by November 2024.

· Enhanced Qualification Program (EQP). Requires FAA to establish requirements so that qualified air carriers, among others, may provide enhanced training based on a nationally standardized curriculum that includes instruction on airline operations and procedures for eligible pilots seeking a restricted-privileges airline transport pilot certificate.

· Nationwide office for Designated Pilot Examiners (DPE). Requires FAA to establish a nationwide oversight office and to submit reports to congressional committees evaluating the use of DPEs—experienced pilots designated by the FAA to conduct tests with student pilots.

Industry stakeholders told GAO that progress on both initiatives could expedite pilot training.

In February 2026, FAA officials told GAO the agency has established EQP requirements internally and set up the DPE national oversight office and has begun oversight. FAA officials said that additional time is needed to complete internal processes before issuing the EQP requirements and the DPE report and that no timelines have been established for issuing either.

Establishing and publicly communicating the timelines for issuing the EQP and DPE products would inform external stakeholders—including Congress—of FAA’s plans for meeting the requirements in the FAA Reauthorization Act. Having this timeline information would also help industry stakeholders, such as aviation schools, prepare to support these initiatives and enhance FAA transparency and accountability.

Why GAO Did This Study

Commercial airline pilots, including regional airline pilots, play a crucial role in facilitating economic activity by ensuring safe and efficient air travel. As in many other highly specialized fields, becoming a commercial airline pilot takes years of training and experience.

The FAA Reauthorization Act of 2024 includes a provision for GAO to review the supply of regional airline pilots. This report examines (1) how pilot supply and other factors affected regional airline service during the post-pandemic recovery, according to selected stakeholders; and (2) what the available data and stakeholders indicate about the current and future supply of regional airline pilots.

GAO analyzed FAA pilot certification data, Department of Transportation data on regional pilot employment, and data from the Air Line Pilots Association on hourly pay rates for first-year regional airline pilots. GAO interviewed FAA officials to obtain perspectives on pilot supply and agency actions. GAO also interviewed representatives from a nongeneralizable sample of 29 aviation stakeholders, such as network and regional airlines, collegiate aviation schools, and industry associations.

What GAO Recommends

GAO recommends that FAA establish and publicly communicate timelines for issuing (1) the Enhanced Qualification Program requirements and (2) the first required report for the Designated Pilot Examiner’s national office. DOT concurred with the recommendations.

|

Abbreviations |

|

|

|

ATP |

Airline Transport Pilot |

|

|

DOT |

Department of Transportation |

|

|

DPE |

designated pilot examiners |

|

|

EQP |

Enhanced Qualification Program |

|

|

FAA |

Federal Aviation Administration |

|

|

FAPA |

Future and Active Pilot Alliance |

|

|

R-ATP |

restricted privilege ATP |

|

This is a work of the U.S. government and is not subject to copyright protection in the United States. The published product may be reproduced and distributed in its entirety without further permission from GAO. However, because this work may contain copyrighted images or other material, permission from the copyright holder may be necessary if you wish to reproduce this material separately.

April 30, 2026

The Honorable Ted Cruz

Chairman

The Honorable Maria Cantwell

Ranking Member

Committee on Commerce, Science, and Transportation

United States Senate

The Honorable Sam Graves

Chairman

The Honorable Rick Larsen

Ranking Member

Committee on Transportation and Infrastructure

House of Representatives

The U.S. civil aviation workforce is responsible for helping move over half a billion people and millions of tons of goods each year. Commercial airline pilots play a crucial role in facilitating this economic activity by ensuring safe and efficient air travel. As in many other highly specialized fields, becoming a commercial airline pilot takes years of training and experience. As we have previously reported, industry actions to address the impacts of the COVID-19 pandemic affected the supply of commercial airline pilots.[1] When demand for air travel decreased sharply in 2020, airlines took actions to manage labor costs by offering pilots early retirement. Then, as air travel demand rebounded in 2021 from 2020 levels, network and low-cost airlines filled their pilot vacancies by hiring from regional airlines, according to the Federal Aviation Administration (FAA).[2] This, in turn, contributed to concerns about small community air service, as we and others have previously reported.[3]

The regional airline industry plays a key role in the broader domestic passenger airline industry. In 2024, regional airlines operated about one-third of all domestic flights and carried about 14 percent of all domestic airline passengers, according to the Regional Airline Association.[4] Regional airlines typically enter into agreements with network airlines and operate as extensions of the network airlines by using smaller, lower-cost aircraft to carry passengers between larger airports and smaller outlying cities.[5]

For many pilots, regional airlines are the entry point to the commercial aviation industry. Regional airlines allow entry-level pilots to build the experience needed to work for the larger airlines, while connecting smaller communities to the national transportation system. Pilots often start their careers as first officers with regional airlines.[6] Then, after gaining experience, a pilot could seek to move to a network airline with larger aircraft and the revenue potential to support higher wages.

The FAA Reauthorization Act of 2024 includes a provision for us to conduct a study on the extent and effect of the pilot shortage on U.S. regional airlines.[7] This report examines (1) how pilot supply and other factors affected regional airline service to small and rural communities during the post-pandemic recovery, according to selected stakeholders; and (2) what the available data and stakeholders indicate about the current and future supply of regional airline pilots.[8]

To understand stakeholders’ views on how pilot supply has affected regional airline service during the post-pandemic recovery, we conducted interviews with, or received written responses from, a nongeneralizable sample of 29 aviation industry stakeholders. These stakeholders consisted of (1) eight network, low-cost, and regional passenger airlines; (2) five collegiate flight schools; (3) eight small airports; (4) three aviation industry analysts, consultants, and academics; and (5) five industry associations representing pilots, aviation university education, and regional airlines. The focus of this report is regional airline pilot supply and its impact on small and rural communities. However, we recognize that regional airlines provide air service to larger communities as well. Our criteria for selecting these stakeholders included the type of commercial airline, subject-matter expertise, and geographic distribution. Because we used a judgmental sample of industry stakeholders, findings from these interviews cannot be generalized to a broader population. However, we determined that the selection of these stakeholders was appropriate for our design and research objectives and that these interviews would generate valid and reliable anecdotal evidence to support our work. See appendix I for the list of stakeholders we interviewed.

In addition, to understand factors affecting regional air service, we analyzed hourly pay rates offered to first-year pilots by selected airlines from 2017 through 2024 using data obtained from the Air Line Pilots Association, a pilot labor union.[9] To assess the reliability of the data we analyzed, we conducted manual and electronic tests of the data. We determined these data were sufficiently reliable for our purposes. We also reviewed prior GAO reports, as well as relevant government reports and industry studies on the airline pilot workforce and air service to small communities.

To determine what available data and stakeholders indicate about the current and future supply of regional airline pilots, we examined data on professional certifications and on students enrolled in training programs, as well as employment and hiring data for the regional pilot occupation.[10] We analyzed FAA data on new airline transport pilot (ATP) certificates issued from 2017 through 2024, as well as the total number of certificates FAA estimated to be active over that time frame; newly issued certificates are a subset of that total number.[11] Regional airlines are a common entry point for pilots, so we use these data as a proxy for understanding regional pilot trends, since the government data do not differentiate by type of airline employer. We also analyzed data provided by the University Aviation Association, a nonprofit organization representing collegiate aviation programs, on student enrollment, school tuition, and mandatory laboratory fees at 4-year collegiate aviation programs from 2017 through 2024.[12] We analyzed regional airline employment data reported to the Department of Transportation (DOT) from 2017 through 2024—the most recent data available at the time of our analysis.[13] We also analyzed data on pilot hiring for the years 2017 through 2024 provided by Future and Active Pilots Alliance (FAPA.aero, hereinafter FAPA), a consultancy service for current and aspiring pilots.[14] There are no publicly available data on regional pilot hiring, so we use these data as a proxy for understanding network and low-cost airline hiring trends.[15] We analyzed the most recently available DOT, FAA, FAPA, and University Aviation Association data at the time of our analysis. To assess the reliability of the data, we reviewed documentation and conducted manual and electronic tests of the data. We determined the data were sufficiently reliable for our purposes.

To examine future pilot hiring projections, we analyzed government aviation forecasts.[16] These forecasts were identified and selected based on our prior work on aviation workforce supply.[17] All forecasts are based on assumptions, and actual demand may differ from projected demand, due to a variety of factors. However, the forecasts provide useful information on what might be expected for the future, given the assumptions.

As part of our work reviewing current and future regional pilot projections, we reviewed FAA and airline’s efforts to support the development of the aviation industry workforce. We reviewed relevant federal laws and regulations and FAA documentation and rulemaking documents. We also interviewed and received written responses from FAA program officials with subject-matter expertise in areas such as pilot certification, education, and outreach programs. We reviewed the status of FAA’s efforts on pilot training initiatives required by the FAA Reauthorization Act of 2024.[18] We reviewed selected project management best practices for organizations as they apply to how an organization should plan and execute activities such as creating a schedule with milestones and time frames (or timelines).[19] In addition, we determined that the information and communication component of federal internal control standards was significant to this evaluation, specifically the principle of communicating externally. The relevant attribute of that principle states that management should communicate relevant and quality information externally so that appropriate parties can help the managed entity achieve objectives and address related risks.[20] We also received written responses from the selected network and regional airlines regarding their efforts to support and strengthen their pilot pathways.

We conducted this performance audit from September 2024 to April 2026 in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

Background

Passenger Airline Industry

The passenger airline industry is primarily composed of network, low-cost, regional, and commuter airlines.

· Network airlines, such as American Airlines, Delta Air Lines, and United Airlines, operate large, complex, hub-and-spoke operations. They partner with regional airlines to provide air service from their hubs to smaller airports.[21]

· Low-cost airlines, such as JetBlue Airways and Southwest Airlines, and ultra-low-cost airlines, such as Allegiant Air and Spirit Airlines, tend to operate point-to-point service using fewer types of aircraft.[22] These airlines do not have agreements with regional airlines but may compete with regional and network airlines for pilots.

· Regional airlines provide regularly scheduled passenger service typically using aircraft with 76 seats or less, generally referred to as regional jets. These airlines generally provide service to smaller communities through agreements with network airlines.[23]

Regional airlines operate as extensions of the network airlines’ route structure and are integrated into the overall market strategy of the network airline. The regional airlines fly under the network airline’s regional “brand” name. Some regional airlines are wholly owned by a network airline, while others operate independently. For example, American Airlines owns three regional airlines (Envoy Air, PSA Airlines, and Piedmont Airlines) while SkyWest Airlines is an independent regional airline and has partnerships with network airlines (see table 1).

|

Network airline |

Regional airline |

Flying under brand name |

|

American Airlines |

Envoy Air Piedmont Airlines PSA Airlines Republic Airways SkyWest Airlines |

American Eagle |

|

Delta Air Lines |

Endeavor Air Republic Airways SkyWest Airlines |

Delta Connection |

|

United Airlines |

CommuteAir GoJet Airlines Republic Airways SkyWest Airlines |

United Express |

Legend: Bold indicates wholly owned subsidiaries of network airlines.

Source: Regional Airline Association. | GAO‑26‑107856

In addition to network, low-cost, and regional airlines, there are smaller commuter airlines (also known as Part 135 operators), such as Southern Airways Express and Key Lime Air, that fly aircraft such as those with a passenger seat configuration of 30 seats or fewer.[24] These operators provide a wide range of services, including passenger air service to small communities, as well as cargo operations, private charters (for corporate business), air medical services, and travel by seaplanes and helicopters.[25]

Federal Regulations for Pilot Certification

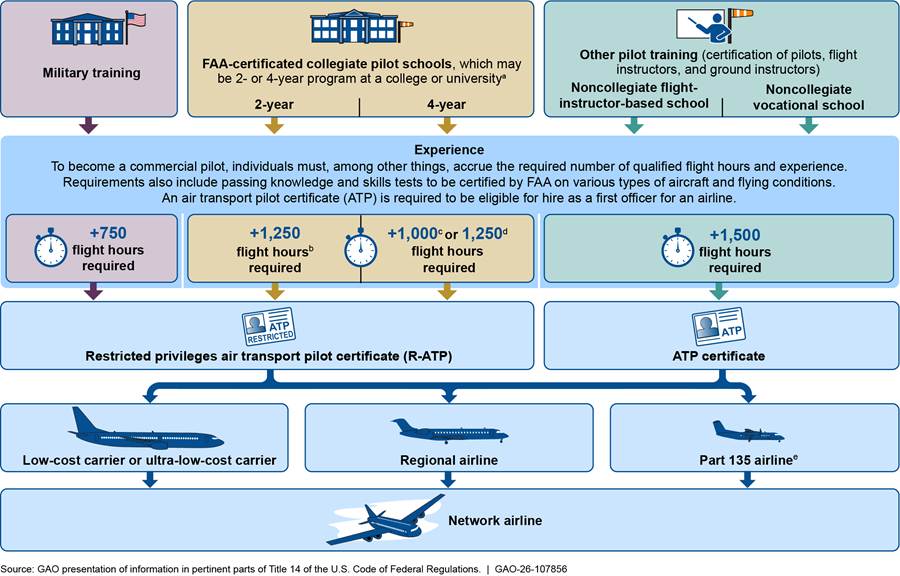

FAA is responsible for regulating the safety of civil aviation in the United States, including the administration of pilot certification and safety oversight of pilot training. FAA issues pilot certificates through which airline pilots progress—including student pilot, private pilot, commercial pilot, and ATP.[26] Federal aviation regulations establish the minimum requirements for each level of certificate, including the applicable eligibility requirements, aeronautical knowledge and experience, and flight proficiency standards. Regulations also govern what pilots with each certificate can do.[27] For example, a private pilot certificate allows pilots to fly solo for recreational purposes or carry passengers in any aircraft for which they are qualified but not to fly for compensation or hire, while a commercial pilot certificate is generally necessary for a variety of nonnetwork airline pilot jobs carrying persons or property for compensation or hire. The ATP certificate is the highest level of pilot certification, requires the highest amount of cumulative flight time, and is necessary to fly as a captain or first officer for a Part 121 network or regional airline.

Pilot Training and Pipeline

Becoming eligible for a job as a pilot for a commercial airline requires meeting FAA requirements, such as FAA’s certification and aeronautical experience qualifications, a process that may take many years of training and significant financial resources.[28] Multiple training paths to obtaining a commercial pilot’s certificate exist, and obtaining a certificate is the first step toward a job as an airline pilot. According to FAA, typical paths are training directly with a flight instructor at a pilot school, which may be associated with a 2- or 4-year program at a college or university; training at a noncollegiate vocational school; or training received through the military.[29] All pilot schools must comply with FAA’s pilot training requirements. Upon completion of training from either a collegiate or noncollegiate program, or separation from the military, students obtain pilot certificates by passing FAA’s knowledge tests, oral evaluations, and practical exams.

Some airlines operate partnerships with pilot schools, called bridge or pathway programs, to attract pilots and better align pilot training with an airline’s needs. In these programs, airlines and students at pilot schools enter into agreements that in some cases provide tuition assistance and may provide mentorship and a conditional offer of employment with the airline once a student reaches a certain amount of flight experience. We have previously reported on the role these programs play in the pilot training and hiring pipeline, and airlines have expanded these programs in recent years.[30]

Becoming a commercial airline pilot also involves obtaining an ATP certificate mentioned above, which requires 1,500 hours of flight experience. In certain circumstances, an individual may be certified under a “restricted privileges” ATP (R-ATP) until the hours of flight experience requirement are met.[31]

Once such a pilot has an ATP or an R-ATP certificate, they are eligible for employment as a first officer. Typically, new pilots with an ATP certificate start at a regional airline or Part 135 (e.g., commuter) airline. After gaining years of experience, many pilots move on to larger, Part 121 airlines, including low-cost or network airlines (see fig.1).

aThese schools may apply for Federal Aviation Administration (FAA) authorization to provide training toward the certification of graduates for R-ATP certificates. Graduates of these schools may proceed with reduced flight time requirements under this certificate.

b1,250 hours of qualified flight time are needed for an R-ATP if the individual holds an Associate’s degree with an aviation major from an institution of higher education that meets certain specifications, has completed at least 30 semester hours of aviation and aviation-related coursework, and holds a commercial pilot certification with an airplane category and instrument rating obtained at the school’s approved Part 141 training program.

c1,000 hours of qualified flight time are needed for an R-ATP if the individual holds a Bachelor’s degree with an aviation major from an institution of higher education that meets certain specifications, has completed 60 semester hours of aviation and aviation-related coursework, and holds a commercial pilot certification with an airplane category and instrument rating obtained at the school’s approved Part 141 training program.

d1,250 hours of qualified flight time are needed for an R-ATP if the individual holds a Bachelor’s degree with an aviation major from an institution of higher education that meets certain specifications and has at least 30, but fewer than 60, semester hours of aviation and aviation-related coursework.

e14 C.F.R. Part 135 prescribes rules governing the commuter or on-demand operations to hold an air carrier certificate. For Part 135 operations, the certificate holder is required to designate a pilot-in-command and a first officer (second-in-command) for each flight requiring two pilots.

FAA Reauthorization Act of 2024

The FAA Reauthorization Act of 2024, enacted in May 2024, authorizes FAA activities through fiscal year 2028. It communicates statutory authorizations, requirements and direction for how FAA is to, and in some instances, should carry out aspects of its mission, and aims to help ensure the safety and efficiency of the U.S. airspace system. The act includes provisions on FAA’s organizational structure and the aviation workforce, among other things. In particular, the act includes two pilot training provisions designed to help increase the supply of pilots.[32]

The first provision required FAA to establish requirements for a program to be known as the Enhanced Qualification Program (EQP) no later than 6 months after enactment, thus by November 16, 2024. The EQP requirements are to include a nationally standardized training curriculum to ensure that prospective pilots are introduced to concepts associated with airline operations, such as aircraft automation, standard operating procedures, and aircraft-specific instruction in appropriate flight simulation training devices. Under this program, qualified air carriers certified by FAA may provide enhanced training, either directly by the air carrier or by a certified training institution, for eligible pilots seeking to obtain a restricted privileges ATP certificate (described above). The second provision requires FAA to establish an office to provide oversight and facilitate national coordination of designated pilot examiners (DPE). These examiners are private persons acting as representatives for the FAA and are authorized to perform practical flight tests to issue temporary pilot certificates to qualified applicants. This provision also required FAA to begin submitting reports to Congress evaluating the use of DPEs no later than 180 days after enactment, thus by November 12, 2024.

Selected Stakeholders Identified Pilot Shortfalls and Other Factors That Contributed to Regional Airline Service Reductions Following the Pandemic

In the aftermath of the pandemic, the entire airline industry, including the regional airlines, faced a pilot supply challenge that contributed to small community air service reductions, according to selected stakeholders.[33] In an effort to attract and retain pilots, regional airlines significantly increased pay, raising average first officer hourly pay from about $52 an hour in 2021 to about $93 an hour in 2024, according to our analysis of data from the Air Line Pilots Association. While pilot supply affected service to small communities during the pandemic recovery, other persistent factors, like increased airline operating costs and travelers choosing to drive to their destination or a larger airport, have contributed to the decrease in regional air service to small airports and communities over the last 20 years, according to our prior work.[34]

Selected Stakeholders Said Post-Pandemic Pilot Shortfalls Contributed to Regional Airline Service Reductions

According to selected aviation stakeholders, the shortfall of experienced pilots at regional airlines, specifically captains, contributed to multiple airlines ending service to small communities. Representatives from one network airline told us that it had to withdraw its regional air service from 29 airports, many of which were serving small communities, at the height of the pilot shortage in 2022. Representatives from one small airport that lost service told us that reduced air service to the local community has impacted how locally based businesses serve existing and future customers, with the potential to further negatively affect the local economy, such as tourism.

Aviation stakeholders said that the post-pandemic pilot supply challenge occurred because network airlines needed to replace many pilots that accepted early retirement offers during the pandemic. According to data from the Future and Active Pilots Alliance (FAPA), over 15,000 pilots were hired by the network and low-cost airlines during 2021-2022.[35]

This hiring surge affected regional pilot supply because, as noted previously, the hiring of experienced pilots from the regional airlines by the larger network airlines is common and part of a normal pilot career progression. According to stakeholders we interviewed, captains at regional airlines with 2 years of experience are generally competitive for first officer positions at the network airlines. However, as demand for air travel recovered and pilot hiring increased from 2021 to 2022, the major network and low-cost airlines also hired brand-new captains and even first officers from the regional airlines, according to Regional Airline Association representatives. In turn, the regional airlines were not able to fill captain vacancies with pilots at the needed experience levels, according to interviews and information we reviewed from the regional airlines. Although the regional airlines were able to hire first officers directly out of flight training schools with the required level of experience, stakeholders told us that these efforts did not address the deficiency in captains, as that position requires additional flight experience in certain operations.[36]

Regional Airline Association representatives noted some effects of the constrained regional pilot supply post-pandemic, including the following:

· Regional airlines were limited in the number of aircraft they could operate, due to an insufficient supply of both captains and new first officers; and

· First officers were not able to build their flight hours toward captaincy at a normal pace, which further strained the pilot pipeline.

These intertwined situations contributed to regional airlines being unable to regain the same level of regional service as in the pre-pandemic year of 2019.

Regional Airlines Responded to Pilot Shortfalls with Increased Pay and Bonuses

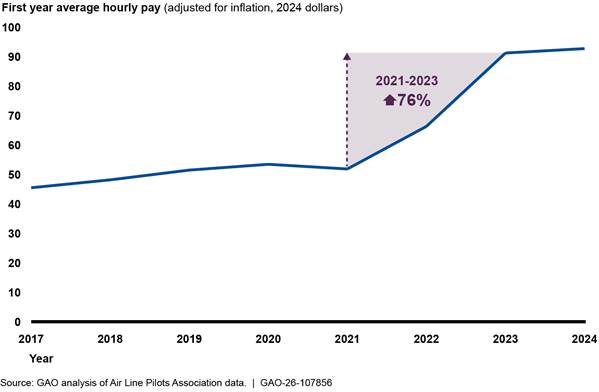

To attempt to address the loss of captains to the network airlines, regional airlines took steps to attract and retain pilots, including significantly increasing pay and offering bonuses. Regional airline first officer wages rose from 2017 to 2024, according to our analysis of data from the Air Line Pilots Association. The data show that at 12 selected regional airlines, hourly pay for a first officer’s first year rose from an average of $45 an hour in 2017 to almost $93 an hour in 2024, after adjusting for inflation, an annualized rate increase of 11 percent.[37] Most of this increase occurred between 2021 and 2023 during the post-pandemic recovery, when wages increased by 76 percent, from almost $52 an hour to about $91 an hour (see fig. 2).[38]

Figure 2: Average Hourly Pay for First-Year First Officers at 12 Selected Regional Airlines, 2017–2024

In addition to increases in hourly pay and base salaries, several regional airlines offered bonuses to respond to increased pilot attrition to network airlines, as we previously reported.[39] For example, in 2022, representatives of one regional airline told us they offered a $15,000 signing bonus to new pilots and up to $150,000 in retention bonuses through its Pilot Retention and Bonus Program. As we previously reported, according to these representatives, the airline started this program to retain more experienced first officers and address personnel imbalances when it began to lose many of its captains to higher-paying network airlines. However, in March and April 2025, one selected network airline and two regional airlines told us that many of the pilot bonus programs have ended as pilot hiring and retention challenges have eased.

Long-Standing Factors Affecting Regional Airline Service to Small Communities Persist

Although pilot supply was one factor affecting air service to small communities during the post-pandemic recovery, multiple long-standing factors have contributed to the decrease in regional air service to small airports and communities. Since deregulation of scheduled air carriers, mainline airlines have made their business decisions based on consumer demand, route profitability, and network planning and allocate flights and frequency of service accordingly, according to a stakeholder. We have previously reported that scheduled passenger air service to small airports and small communities, typically provided by regional airlines, has been declining for 2 decades.[40] For example, from 2000 to 2018, departures from small and nonhub airports fell 32 percent and 47 percent, respectively, compared with a 7 percent decrease in departures from large hub airports, according to a 2020 National Academies study.[41] Coming out of the pandemic, airlines made substantial changes to meet pandemic-market and post-pandemic market demand, reducing service to markets deemed less economically viable as leisure travel replaced business travel, according to a stakeholder representing pilots. Furthermore, in our analysis of air service trends in small communities from 2018 through 2023, we found a further decrease in departures but an increase in the average seats per departure.[42]

As we reported in 2024, some of the factors contributing to the decrease in air service to small communities include

· higher operating costs, such as labor, jet fuel, and maintenance costs;

· declining population levels in communities surrounding small airports;

· the replacement of small regional jets in airline fleets with larger jets (a practice known as “upgauging”);

· travelers choosing to drive to their destination or a larger airport; and

· regulatory changes to pilot training and certification that have affected the supply of qualified pilots for airlines.[43]

Data and Selected Stakeholders Indicate Regional Airline Pilot Supply Has Grown, but Retirements May Pose Future Supply Challenges

Data and stakeholders indicate that regional pilot supply has been rebounding recently. Pilot certifications grew about 10 percent from 2017 through 2024, with most of the increase starting in 2021, according to FAA. In addition, pilot student enrollment increased 67 percent during the same period, according to industry data. Further, both airlines and FAA have taken actions intended to strengthen the pilot pipeline. In 2024, pilot hiring slowed at the network and low-cost airlines, in part due to aircraft delivery delays, allowing regional airlines to retain pilots and move toward pre-pandemic staffing levels, according to selected stakeholders. However, over half of certified pilots (as of 2024) will reach the mandatory retirement age for commercial airline pilots within the next 20 years, which may affect future pilot supply for all airlines.

The Number of Certified Pilots Has Grown

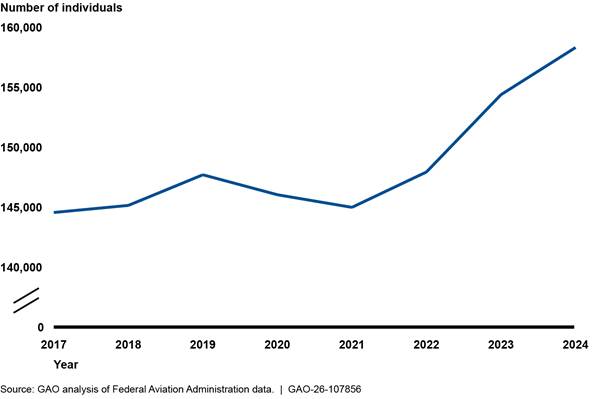

FAA data show that the number of individuals qualified to be commercial passenger airline pilots[44]—which includes regional airline pilots—grew by about 10 percent from 2017 through 2024, from 144,557 to 158,311 (see fig. 3).[45] The number of new ATP certificates issued each year by FAA more than doubled between 2017 and 2024 (from 4,449 to 9,513 certificates per year, respectively).[46]

Figure 3: Number of Individuals with the Qualifications to Be U.S. Commercial Passenger Airline Pilots, 2017— 2024

Note: This pool of airline transport pilot (ATP) certificate holders may include persons who are unavailable for work or are not employed by airlines. Individuals under the age of 65 who hold active ATP certificates but are not employed by airlines might also be serving as pilots in the U.S. military, employed as pilots in nonairline operations, employed by foreign airlines, employed in nonpilot jobs in the aviation industry, or working in nonaviation careers. Data were not available to determine or verify how many active ATP certificate holders were employed outside airlines. Qualified commercial airline pilots are those under 65 years old who hold both an ATP and active medical certificate. At age 65, commercial airline pilots are no longer eligible for employment as a pilot with U.S. commercial airlines but could work as pilots or instructors elsewhere.

Student Pilot Enrollment Has Also Grown in Recent Years

In addition to growth in the number of certified pilots, the number of individuals enrolled in pilot training schools has also grown in recent years. For example, in the 2017 and 2024 time frame, pilot student enrollment increased 67 percent, from 11,585 to 19,404 students, according to University Aviation Association data for the 31 schools that reported data for both years.[47] In addition, faculty from five collegiate aviation programs told us their student enrollment has increased in recent years, which they attributed to ongoing demand for pilots. Stakeholders told us, however, that not all students will graduate or work for an airline, due to factors such as the significant cost to attend and the rigors of training.

FAA Is Taking Actions to Strengthen the Pilot Pipeline but Has No Timeline for When It Will Publicly Issue Key Products

For many years, airlines and FAA have pursued various strategies to strengthen the pilot pipeline. Selected network and regional airlines told us that they have pilot development programs leading into their pilot pipeline. For example, Delta Air Lines’s Propel program provides a pathway to enter the pilot career pipeline and receive support, either financially or programmatically, until the individual is eligible for a position as a Delta pilot.[48] Southern Airways, a much smaller commuter airline, told us that it partners with two flight schools to help develop and recruit new pilots. These two schools have a customized program, and students are taught the airline’s procedure and avionics systems, as well as to fly on its aircraft type. This allows the students to have direct entry into the airline’s network as positions become available.

FAA is also pursuing a variety of efforts to help strengthen the pilot pipeline. FAA’s actions include the following:

· Awarding grants under its Aviation Workforce Development Grant Program. This program aims to help support the education and recruitment of the next generation of aviation professionals. The program was mandated by section 625 of the FAA Reauthorization Act of 2018, which required FAA to establish separate grant programs for pilots and aviation maintenance workers—Aviation Workforce Development Grants for Aircraft Pilots and Aviation Maintenance Technical Workers. Amendments in the FAA Reauthorization Act of 2024 added a grant program for aviation manufacturing technical workers and aerospace engineers.[49] According to FAA, the intent of the grant program for pilots is to support meaningful education designed to help students become aircraft pilots, as well as other aviation professionals. We previously reported, in May 2023, that stakeholders supported the program but expressed concerns that the amount of funding provided was not likely large enough to make a substantial impact.[50] Under the statute, FAA may not award a grant more than $1,000,000 to any eligible entity in any one fiscal year.[51] According to FAA officials, $1.69 million was awarded to 460 recipients for the fiscal year 2024 program. As of December 2025, FAA officials reported that, in accordance with the current administration’s priorities, five recipients were approved for fiscal year 2025 grants, totaling $2.02 million. The officials further reported that the bulk of the funding supported aviation maintenance technical workers. The next round of aviation workforce development funding is anticipated to be awarded no later than September 30, 2026.

· Drafting requirements for the Enhanced Qualification Program. The FAA Reauthorization Act of 2024, enacted in May 2024, requires FAA to establish requirements for EQP, in which air carriers may provide structured training for eligible pilots seeking a R-ATP certificate.[52] The requirements were to be established by November 2024. FAA officials stated that the EQP is designed to give pilots an introduction to air carrier knowledge and practical skills, thereby better preparing student pilots to start their initial pilot training at an airline. Selected stakeholders told us they were supportive of the program and are waiting for FAA to issue requirements. Without published FAA requirements, aviation schools cannot confidently design curricula, formalize airline partnerships, or make capital investments aligned with the program, according to one selected stakeholder. In December 2025, FAA officials told us the agency had established EQP requirements internally to meet the statutory due date, but additional time was necessary to implement these requirements through an Advisory Circular communicating the EQP requirements, and the agency remained committed to fully implementing the EQP, in accordance with the law.[53] The Advisory Circular was still under review in February 2026, according to FAA officials. At that time, these officials told us that a specific timeline for the EQP Advisory Circular approval process was not yet available.

· Creating an office to provide oversight and facilitate national coordination of designated pilot examiners. The FAA Reauthorization Act of 2024 also required FAA to establish an office to provide oversight and facilitate national coordination of designated pilot examiners.[54] A DPE is an experienced pilot who is designated by the FAA to conduct oral examinations and in-flight practical tests (check rides) with student pilots to determine their suitability to be issued a pilot certificate.[55] The act also requires FAA to submit reports to congressional committees evaluating the use of DPEs.

FAA officials told us that FAA established a National Oversight Office to manage DPEs in early 2024, and the office was in the process of staffing up and centralizing DPE oversight in a phased approach, based on geographic areas. In December 2025, FAA officials reported that the National Oversight Office was providing oversight to approximately 200 DPEs. At that time, FAA officials also told us that the agency planned to release a report to Congress outlining how it will implement the new office and how it is working with industry to reduce wait times for check rides.

However, as of February 2026, FAA had yet to issue the first required report evaluating the use of DPEs. FAA officials told us the report was still under internal review, and no timeline for its release had been established. The report, when issued, could help inform stakeholders about the use and coordination of DPEs and check rides. Selected stakeholders we interviewed stated that long wait times to schedule check rides with examiners have added to the cost and length of time to become a pilot and that they support FAA’s efforts.

We previously reported that project management standards state that organizations should estimate the duration of activities and create a schedule with milestones and time frames (or timelines) to execute them.[56] In addition, Standards for Internal Control in the Federal Government state that management should externally communicate relevant and quality information so that appropriate external parties can help the entity achieve its objectives and address related risks.[57] In FAA’s case, such objectives include making the most of the initiatives set forth by Congress to support the aviation industry and workforce and to help ensure a reliable supply of pilots.

As stated in the Standards for Internal Control in the Federal Government, establishing timelines for completing the EQP and DPE activities would provide a means for FAA to measure its progress in meeting the aforementioned requirements in FAA Reauthorization Act of 2024, and to make adjustments, as needed. Additionally, publicly communicating the timelines would inform external stakeholders—including industry stakeholders and Congress—of FAA’s plans, enabling industry to plan for upcoming actions and Congress to oversee FAA’s efforts.

Selected Stakeholders Said the Pilot Shortfall Has Eased as Network and Low-Cost Airline Hiring Has Slowed

Stakeholders said that reduced hiring by network and low-cost airlines has allowed regional airlines to move toward pre-pandemic pilot staffing levels. In addition, our analysis of industry data indicates that a pilot hiring slowdown occurred at the network and low-cost airlines in 2024 after the pilot hiring surge during 2022 and 2023.

According to data we reviewed from FAPA, nine U.S. airlines collectively hired about 22,600 pilots in 2022 and 2023, and the rate of hiring at those nine U.S. airlines slowed to just over 4,000 pilots in 2024.[58] Selected regional and network airlines told us that the hiring slowdown was due, in part, to aircraft supply chain issues causing aircraft delivery delays.[59] In addition, DOT’s employment data show an increase in regional airline pilot employment in 2024. According to the latest available full-year data reported to DOT by regional airlines, for example, the number of employed regional pilots in 2024 rose to 15,216, up from 14,051 in 2023, but slightly lower than the 15,334 regional pilots employed in 2022.[60]

However, selected stakeholders, including representatives from one regional airline, cautioned that this improvement may be temporary. They said they expect that network airlines will increase hiring once aircraft deliveries from Boeing and Airbus resume to their anticipated levels. Stakeholders representing airline pilots note that reductions in hiring also reflect network carriers employing more pilots for operational reliability purposes in the post-pandemic environment, as well as the reduced need to replace pilots that left the industry during the pandemic.

In both the spring and December 2025, selected network and regional airlines told us that pilot availability—including regional pilots—is not a constraint to operating their planned schedules. One network airline told us that the easing of pilot shortfalls has allowed their regional air service to grow closer to pre-pandemic air service levels, despite working with fewer regional affiliates. Easing of pilot shortfalls can also be seen through the growth of block hours, which are a measure of aircraft usage that can also be used to measure pilot utilization. Block hours are a common measure of aircraft usage that refers to the amount of time from the moment aircraft doors close at departure until they open at arrival. One network airline stated that its regional affiliate monthly block hours have increased approximately 40 percent since 2023.

Upcoming Pilot Retirements May Pose Challenges to Future Pilot Supply

While the regional airline pilot shortfall has eased somewhat, the number of pilot retirements in the next 20 years may challenge the future supply of all pilots, including pilots working for regional airlines.[61]

Commercial airline pilots who reach the mandatory retirement age of 65 are no longer eligible to be employed as a U.S. commercial airline pilot by such airlines. According to FAA data, over half of the pilots with an ATP certificate as of December 2024 (who may or may not be actively employed as airline pilots) will reach the mandatory retirement age of 65 in the next 2 decades.[62] FAA’s data include all individuals with an ATP certificate, including those not employed by the airlines.

Trade industry data, which reflect these pilots employed by 20 passenger airlines and cargo operators, show several thousand pilots turning 65 each year over the next few years. Specifically, according to data from the Air Line Pilots Association as of February 2026, on average, about 3,000 currently employed pilots will reach age 65 annually from 2025 through 2029.

Airline demand for some number of future pilots to replace retiring pilots may arise, but the extent of this demand is dependent on a variety of factors, such as demand for air travel.

We have long reported that the demand for air travel is highly cyclical in relation to the state of the economy, as well as to political, international, and health-related events.[63] Forecasts of the demand for air travel rest on assumptions made about these factors.

For any forecast, if the assumptions or data on which it was based change or were inaccurate, the forecast’s applicability and usefulness could change. For example, early retirement by a pilot or a pilot’s nonretirement departure from the industry would reduce pilot supply prior to that pilot’s assumed retirement at 65. Nevertheless, forecasts provide information on potential risks for the future, given the assumptions, and can help inform agency and industry planning efforts.

Conclusions

The 2021-2022 pilot hiring surge by network and low-cost airlines mainly drew pilots from the regional airlines, which affected regional airlines’ operations to such a degree that they reduced air service to multiple small airports. The reduction—and in some cases total loss—of air service to small communities highlighted why having a consistent and predictable supply of pilots is vital to the industry and why Congress, in statute, directed FAA to establish two training initiatives to help increase the pilot supply. According to FAA, the agency has developed the EQP requirements internally and established a National Oversight Office to coordinate DPEs. However, FAA has not established timelines for issuing the EQP requirements nor the report evaluating the use of DPEs. Establishing and publicly communicating the timelines for issuing the EQP requirements and the first DPE report would inform external stakeholders—including Congress—of FAA’s plans for meeting these requirements in the FAA Reauthorization Act of 2024. Having timeline information would also help external stakeholders, such as aviation schools, prepare to support these initiatives, and it would improve FAA’s accountability and transparency as FAA continues to work with industry to develop certified pilots.

Recommendations for Executive Action

We are making the following two recommendations to FAA:

The Administrator of FAA should establish and publicly communicate a timeline for when FAA will issue the FAA Reauthorization Act of 2024 mandated Enhanced Qualification Program requirements. (Recommendation 1)

The Administrator of FAA should establish and publicly communicate a timeline for when FAA will issue the first FAA Reauthorization Act of 2024 required report on the Designated Pilot Examiner’s National Office. (Recommendation 2)

Agency Comments

We provided a draft of this report to the Secretary of Transportation for review and comment. DOT agreed with our two recommendations. The agency’s comments are reproduced in appendix II. DOT referred generally to its efforts to improve pilot training and certification and fulfill all requirements of the FAA Reauthorization Act of 2024. DOT also provided technical comments, which we incorporated in the report as appropriate.

We are sending copies of this report to the appropriate congressional committees, the Secretary of Transportation, and other interested parties. In addition, the report is available at no charge on the GAO website at https://www.gao.gov.

If you or your staff have any questions about this report, please contact me at GieseD@gao.gov. Contact points for our Offices of Congressional Relations and Media Relations may be found on the last page of this report. GAO staff who made key contributions to this report are listed in appendix III.

Danielle T. Giese

Director, Physical Infrastructure Issues

|

U.S. federal agencies |

|

Federal Aviation Administration |

|

Passenger airlines |

|

United Airlines |

|

American Airlines |

|

Delta Air Lines |

|

Allegiant Airlines |

|

Alaska Airlines |

|

JSX |

|

Key Lime Air |

|

Southern Airways Express |

|

Collegiate flight schools |

|

University of North Dakota |

|

Embry-Riddle Aeronautical University |

|

Middle Tennessee State University |

|

University of Dubuque |

|

Liberty University |

|

Small airports |

|

Kalamazoo/Battle Creek International Airport, Kalamazoo, MI |

|

Eastern Iowa Airport, Cedar Rapids, IA |

|

Grand Junction Regional Airport, Grand Junction, CO |

|

Helena Regional Airport, Helena, MT |

|

Rapid City Regional Airport, Rapid City, SD |

|

Knox County Regional Airport, Rockland, ME |

|

Wichita Dwight D. Eisenhower National Airport, Wichita, KS |

|

Williamsport Regional Airport, Williamsport, PA |

|

Financial services firms |

|

Raymond James |

|

Deutsche Bank |

|

Industry associations |

|

Air Line Pilots Association |

|

Coalition of Airline Pilots Associations |

|

National Air Carrier Association |

|

Regional Airlines Association |

|

University Aviation Association |

Source: GAO. | GAO-26-107856

GAO Contact

Danielle T. Giese, GieseD@gao.gov

Staff Acknowledgments

In addition to the contact named above, Jonathan Carver (Assistant Director), Nick Nadarski (Analyst in Charge), Melissa Bodeau, Stephen Brown, Geoffrey Hamilton, Bonnie Pignatiello Leer, Josh Ormond, and Elizabeth Wood made key contributions to this report.

The Government Accountability Office, the audit, evaluation, and investigative arm of Congress, exists to support Congress in meeting its constitutional responsibilities and to help improve the performance and accountability of the federal government for the American people. GAO examines the use of public funds; evaluates federal programs and policies; and provides analyses, recommendations, and other assistance to help Congress make informed oversight, policy, and funding decisions. GAO’s commitment to good government is reflected in its core values of accountability, integrity, and reliability.

Obtaining Copies of GAO Reports and Testimony

The fastest and easiest way to obtain copies of GAO documents at no cost is through our website. Each weekday afternoon, GAO posts on its website newly released reports, testimony, and correspondence. You can also subscribe to GAO’s email updates to receive notification of newly posted products.

Order by Phone

The price of each GAO publication reflects GAO’s actual cost of production and distribution and depends on the number of pages in the publication and whether the publication is printed in color or black and white. Pricing and ordering information is posted on GAO’s website, https://www.gao.gov/ordering.htm.

Place orders by calling (202) 512-6000, toll free (866) 801-7077,

or

TDD (202) 512-2537.

Orders may be paid for using American Express, Discover Card, MasterCard, Visa, check, or money order. Call for additional information.

Connect with GAO

Connect with GAO on X,

LinkedIn, Instagram, and YouTube.

Subscribe to our Email Updates. Listen to our Podcasts.

Visit GAO on the web at https://www.gao.gov.

To Report Fraud, Waste, and Abuse in Federal Programs

Contact FraudNet:

Website: https://www.gao.gov/about/what-gao-does/fraudnet

Automated answering system: (800) 424-5454

Media Relations

Sarah Kaczmarek, Managing Director, Media@gao.gov

Congressional Relations

David A. Powner, Acting Managing Director, CongRel@gao.gov

General Inquiries

[1]GAO, Aviation Workforce: Current and Future Availability of Airline Pilots and Aircraft Mechanics, GAO‑23‑105571 (Washington, D.C.: May 17, 2023).

[2]Federal Aviation Administration, FY 2024-2044 FAA Aerospace Forecast); and FY 2025-2045 FAA Aerospace Forecast.

[3]See, for example, GAO, Commercial Aviation: Trends in Air Service to Small Communities, GAO‑24‑106681 (Washington, D.C.: Sept. 25, 2024); and Regional Airline Association, Small Community Air Service & the Pilot Shortage (Washington, D.C.: Feb. 6, 2023).

[4]Regional Airline Association, 2025 Annual Report. The Regional Airline Association advocates for regional air service on behalf of its member airlines.

[5]Network airlines support large, complex, hub-and-spoke operations with thousands of employees and hundreds of aircraft. These airlines provide service at various fare levels to a wide variety of domestic and international destinations.

[6]The first officer (second-in-command) is the second pilot of an aircraft and works in the cockpit alongside the captain (first-in-command) to navigate and operate the flight. Among other things, the first officer must hold the appropriate pilot certificate and ratings applicable to the aircraft being flown. According to FAA regulations, the pilot-in-command (captain) of an aircraft is the person aboard the aircraft who is directly responsible for, and is the final authority as to, the operation of that aircraft. The first officer is the second pilot of an aircraft designated to be second-in-command of an aircraft during flight time.

[7]FAA Reauthorization Act of 2024, Pub. L. No. 118-63, § 422, 138 Stat. 1025, 1165. The mandate language for this study covers air carriers operating under both Part 121 (authorizing scheduled air service for air carriers that, according to FAA, are generally large, U.S.-based airlines, regional air carriers, and all cargo operators) and Part 135 (authorizing on-demand, unscheduled air service that, according to FAA, varies from small single-aircraft operators to large operators that often provide a network to move passengers and cargo to larger Part 121 air carriers). However, there was little differentiation in responses we received regarding pilot supply between air carriers operating under Part 121 and Part 135. For that reason, we address them together with respect to discussions of pilot supply for regional airlines.

[8]The post-pandemic recovery for the aviation industry is generally considered to have started in 2021 and beyond. Federal Aviation Administration, The Economic Impact of U.S. Civil Aviation (September 2024).

[9]We updated with 2023 and 2024 data the analysis that we conducted in a prior report. See GAO‑23‑105571.

[10]For the employment data, we focused on pilots who were employed by U.S. airlines providing scheduled passenger service. Other employers of pilots, which are outside the scope of this review, include aircraft operators, such as air taxis and business jets, that provide unscheduled, charter, and on-demand passenger service, and cargo airlines that operate aircraft configured specifically for carrying cargo.

[11]To be eligible for hire as either a first officer or captain at an airline providing scheduled passenger air service, individuals must obtain an ATP certificate, in addition to other certifications, ratings, and requirements.

[12]According to a representative, the University Aviation Association did not collect 2023 enrollment data, due to a major storm that impacted their facility.

[13]Certain airlines are required to report monthly full-time and part-time employment statistics to DOT. Those include airlines that operate at least one aircraft with more than 60 seats or the capacity to carry combined passengers, cargo, and fuel of 18,000 pounds, according to DOT. In 2024, 12 regional airlines reported these data to DOT.

[14]The U.S. passenger airlines for which FAPA makes pilot hiring data publicly available are Alaska Airlines, Allegiant Air, American Airlines, Delta Air Lines, Frontier Airlines, JetBlue Airways, Hawaiian Airlines, Southwest Airlines, Spirit Airlines, and United Airlines. However, FAPA began tracking pilot hiring data for Hawaiian Airlines in 2023, so we did not include Hawaiian Airlines in our analysis.

[15]Total hirings includes any individual pilots that are hired more than once in a calendar year, such as when a pilot is hired at one airline and then moved to another airline within the same year. FAPA estimates double-counting to be no greater than 15 percent of the total reported.

[16]Federal Aviation Administration, FAA Aerospace Forecast Fiscal Years 2024–2044; and FAA Aerospace Forecast, Fiscal Years 2025-2045.

[17]See GAO‑23‑105571, as well as GAO, Aviation Workforce: Supply of Airline Pilots and Aircraft Mechanics, GAO‑23‑106769 (Washington, D.C.: Apr. 19, 2023); Aviation Workforce: Current and Future Availability of Airline Pilots, GAO‑14‑232 (Washington, D.C.: Feb. 28, 2014); and Current and Future Availability of Aviation Engineering and Maintenance Professionals, GAO‑14‑237 (Washington D.C.: Feb. 28, 2014).

[18]FAA Reauthorization Act of 2024, Pub. L. No. 118-63, §§ 372, 833, 138 Stat. 1025, 1139, 1339.

[19]Project Management Institute, Inc., A Guide to the Project Management Body of Knowledge (PMBOK® Guide), 7th ed. (Newtown Square, PA: 2021). PMBOK is a trademark of the Project Management Institute, Inc. The Project Management Institute is a not-for-profit association that, among other things, provides standards for managing various aspects of projects, programs, and portfolios.

[20]GAO, Standards for Internal Control in the Federal Government, GAO‑14‑704G (Washington, D.C.: September 2014).

[21]Air carriers authorized to operate under Part 121 of Title 14 of the Code of Federal Regulations are generally large, U.S.-based airlines, regional air carriers, and all cargo operators, according to FAA.

[22]For the purposes of this report, we refer to both types of airlines as low-cost airlines.

[23]These agreements include what are commonly referred to as “capacity purchase agreements” and “prorate agreements.” One airline’s annual report has, for example, described that under a capacity purchase agreement, a network airline pays the regional airline a fixed fee to provide air service. Under this arrangement, the regional airline pays for the aircraft, and increases in costs (e.g., higher fuel costs) are paid for by the network airline. By contrast, the annual report notes that under a prorate agreement, the regional airline receives a percentage of the overall fare paid by the passengers for flights marketed by their partner network airline(s), shifting the risk to the regional airline, together with any resulting profit.

[24]14 C.F.R. Part 135 prescribes rules governing the commuter or on-demand operations to hold an air carrier certificate. For Part 135 operations, the certificate holder is required to designate a pilot-in-command and a first officer (second-in-command) for each flight requiring two pilots.

[25]Under Part 135 rules, for example, smaller commuter airlines are allowed to provide scheduled air service in non-turbojet aircraft, such as piston-powered or turboprop aircraft with nine or fewer seats. Airlines may also conduct on-demand operations under Part 135 regulations using aircraft with 30 passenger seats or fewer. Part 135 operators with commuter authority may also conduct limited on-demand operations, according to published flight schedules, using non-turbojet aircraft with nine or fewer passenger seats.

[26]To become eligible for pilot training, prospective students generally must be cleared by a medical examination and obtain medical and student pilot certificates from FAA.

[27]14 C.F.R. Part 61. These regulations prescribe the requirements for issuing pilot, flight instructor, and ground instructor certificates, ratings, and authorizations; the conditions under which those certificates, ratings, and authorizations are necessary; and the privileges and limitations of those certificates, ratings, and authorizations. FAA regulations also prescribe requirements for issuing pilot school certificates, provisional pilot school certificates, and associated ratings, and the general operating rules applicable to a holder of the certificate or rating issued under 14 C.F.R. Part 141.

[28]We have previously reported that the cost of a collegiate flight education is a challenge for some colleges in recruiting and retaining students. The average cost of a 4-year degree in 2021, plus flight training “lab fees,” was $85,745 (for in state) and $138,511 (for out of state). These costs exceed the maximum amount of certain types of federal student loans available to eligible students. See GAO‑23‑105571.

[29]More specifically, according to FAA, such typical paths are training with a flight instructor under Part 61, training at a Part 141 pilot school (that may be associated with a 2- or 4-year degree program at a college or university), training at a noncollegiate vocational school, or training received through the military. All training credit must meet either Part 61 or Part 141 requirements, as appropriate, according to FAA. Upon completion of training, students obtain pilot certificates by passing FAA knowledge tests and practical tests, according to FAA. U.S. military pilots, according to FAA, may receive a commercial pilot certificate or a flight instructor certificate under Part 61, after showing compliance with special rules for military pilots or former military pilots at 14 C.F.R. § 61.73, which includes passing the appropriate FAA knowledge test(s) for a U.S. military pilot or U.S. military flight instructor or examiner.

[31]FAA allows pilots with fewer than 1,500 hours of total time as a pilot to obtain an R-ATP certificate when they meet certain requirements. The R-ATP certificate allows pilots to serve as first officers until they obtain the necessary 1,500 hours of total time as a pilot needed for an ATP certificate.

[32]See, FAA Reauthorization Act of 2024, Pub. L. No. 118-63, §§ 372, 833, 138 Stat. 1205, 1139, 1339.

[33]The supply of, and demand for, pilots determines how many are employed and the wages they earn. For this occupation, supply refers to the current economy’s ability to produce employable pilots at a given wage rate, whereas demand refers to employers’ desire to hire them at a given wage rate. The industry’s demand for pilots is driven by several factors, including projected demand for air travel and the number of aircraft that airlines expect to use to fulfill that demand, as well as anticipated workforce attrition and retirements. See GAO‑23‑105571.

[34]See GAO‑24‑106681.

[35]Total hiring includes any individual pilots that are hired more than once in a calendar year, such as when a pilot is hired at one airline and then moved to another airline within the same year. FAPA estimates double-counting to be no greater than 15 percent of the total number of pilots reported.

[36]GAO‑23‑105571. In commercial aviation, to serve as a pilot-in-command for regularly scheduled air carriers, a pilot must have an additional 1,000 hours experience performing certain operations.

[37]According to the Air Line Pilots Association, they monitor these 12 because they are largest airlines by block hours, available seat miles, and aircraft hulls and cumulatively operate the largest regional aircraft.

[38]We used the calendar year consumer price index to adjust for inflation (2024 dollars).

[41]National Academies of Sciences, Engineering, and Medicine, Building and Maintaining Air Service Through Incentive Programs (Washington, D.C.: The National Academies Press, 2020). Small hub airports are defined as those airports that have 0.05 percent to 0.25 percent of the annual U.S. commercial enplanements. Nonhub primary airports are defined as those airports that have less than 0.05 percent but more than 10,000 of the annual U.S. commercial enplanements. Nonprimary nonhub airports are defined as those airports that have scheduled passenger service and between 2,500 and 10,000 annual enplanements.

[42]See GAO‑24‑106681.

[43]GAO‑24‑106681. The regulatory change discussed in the 2024 report relates to the pilot training and certification requirement for an individual to complete 1,500 flight hours to be eligible to be hired as a first officer, which was effective in 2013 made in response to a statutory requirement. See FAA’s July 2013 final rule setting out certification and qualification requirements for pilots in air carrier operations at 78 Fed. Reg. 42324 (July 15, 2013).

[44]Qualified commercial airline pilots are those under 65 years old who hold both an ATP and active medical certificate. The statutory retirement age for these pilots is 65. See 49 U.S.C. § 44729. See also 14 C.F.R. § 121.383. Such pilots ages 65 and over are no longer eligible for employment as a pilot with scheduled U.S. passenger airlines but could work as pilots or instructors elsewhere.

[45]The data on these qualified pilots do not contain any indicator as to whether a pilot flies for a network or regional airline, or whether they are flying at all. Individuals under the age of 65 who hold an active ATP certificate and an active medical certificate but are not employed by airlines might also be serving as pilots in the U.S. military, employed as pilots in nonairline operations, employed by foreign airlines, employed in nonpilot jobs in the aviation industry, or working in nonaviation careers. Data are not available to determine or verify how many active ATP certificate holders were employed outside airlines.

[46]New (also referred to as original) ATP certifications include those approved by FAA examiners and inspectors, as well as those issued without a test. According to FAA, individuals who comply with the special conditions listed within the Implementation Procedures for Licensing could be issued an ATP certificate without a test.

[47]A total of 118 private or public collegiate flight schools reported student enrollment data to the University Aviation Association in the 2017-2024 period; however, the number of schools reporting in each year varied. Enrollment data do not indicate the percentage of international students who may be ineligible to become a pilot in the United States.

[48]Propel currently addresses approximately 40 percent of the pilot hiring needs for Delta’s subsidiary and regional airline, Endeavor Air, which, in turn, supports approximately 20 percent of Delta's mainline hiring needs, according to the airline.

[49]FAA Reauthorization Act of 2018, Pub. L. No. 115-254, div B, tit.VI, subtit. C, § 625, 132 Stat. 3186, 3405, as amended by Pub. L. No. 116-92, div A, tit. XVII, subtit. B, § 1743(a), 133 Stat. 1198, 1842; and Pub. L. No. 118-63, § 440(a), 138 Stat. 1025, 1179.

[51]Eligible entities for the aircraft pilot program include an air carrier (as defined in 49 U.S.C. § 40102), an accredited institution of higher education; a postsecondary vocational institution, or high school or secondary school; a labor organization representing professional aircraft pilots; and a state, local, territorial, or tribal governmental entity, among others. See 49 U.S.C. § 40132, note.

[52]FAA Reauthorization Act of 2024, Pub. L. No. 118-63, § 372, 138 Stat. 1025, 1139.

[53]This requirement in the FAA Reauthorization Act of 2024 provides, in part, that “not later than 6 months after the date of enactment of this Act, the Administrator shall establish the requirements for a program to be known as the Enhanced Qualification Program.”

[54]FAA Reauthorization Act of 2024, Pub. L. No. 118-63, § 833, 138 Stat 1025 1339.

[55]A check ride is the flight portion of the practical test in which the candidate being examined flies in an aircraft with the DPE or other authorized examiner to demonstrate competency in the skills that are required for an aircraft pilot’s certification. FAA designates these examiners to support FAA’s pilot certification process, especially when FAA-employed examiners are not available.

[56]GAO, Further Action Needed to Implement Foodborne Illness Prevention Law and Assess Its Results, GAO‑26‑107394 (Washington, D.C.: Jan. 7, 2026).

[58]As mentioned previously, the U.S. passenger airlines for which FAPA makes pilot hiring data publicly available are Alaska Airlines, Allegiant Air, American Airlines, Delta Air Lines, Frontier Airlines, JetBlue Airways, Hawaiian Airlines, Southwest Airlines, Spirit Airlines, and United Airlines. FAPA began tracking pilot hiring data for Hawaiian Airlines in 2023, so we did not include Hawaiian Airlines in our analysis.

[59]We reported that Airbus and Boeing have had challenges, resulting in delivery delays for airlines. GAO, Commercial Aviation Manufacturing: Supply Chain Challenges and Actions to Address Them, GAO‑24‑106493 (Washington, D.C.: Mar. 6, 2024).

[60]Regional airline pilot hiring data are not publicly available, but FAPA airline hiring data can be used as a proxy.

[61]In terms of pilot supply, based on FAA’s forecast of ATP certificate growth, the number of ATP certificate holders under 65 may increase by up to 30,590 by 2044.

[62]Specifically, 90,780 out of 158,311 current ATP certificate holders will reach age 65 in the next 20 years. This pool of ATP certificate holders may include persons who are unavailable for work or are not employed by airlines. Individuals under the age of 65 who hold active ATP certificates but are not employed by airlines might also be serving as pilots in the U.S. military, employed as pilots in non-airline operations, employed by foreign airlines, employed in non-pilot jobs in the aviation industry, or working in non-aviation careers. Data were not available to determine or verify how many active ATP certificate holders were employed outside airlines.

[63]See, for example, GAO, Commercial Aviation: Airline Industry Contraction Due to Volatile Fuel Prices and Falling Demand Affects Airports, Passengers, and Federal Government Revenues, GAO‑09‑393 (Washington, D.C.: Apr. 21, 2009).