Report to Congressional Committees

United States Government Accountability Office

A report to congressional committees

Contact: Derrick Collins at CollinsD@gao.gov

What GAO Found

The Federal Aviation Administration (FAA) created the Certification Activity Tracking System (CATS) website for officials at commercial service airports to file and certify their annual financial data, such as operating expenses and revenues. This database is the only centralized source of airport financial data. FAA, industry stakeholders, and researchers have used the data for multiple purposes. For example, a researcher used CATS data on airport revenues and expenses to develop policy options for Congress to improve airport financing.

Most airports required to submit data to CATS did so, but the extent of the timeliness and accuracy of CATS data is unknown. Airports that receive certain federal grants, provide commercial service, and had at least 2,500 passenger boardings in the prior year are required to submit data. Most of these airports did so for fiscal year 2023 (the most recent data available at the time of GAO’s review), but some of the smallest airports did not, for reasons that included staff turnover. Limitations in CATS make it difficult for FAA to track whether airports meet reporting deadlines. Moreover, airports must report data within a certain period after the end of their fiscal year, which varies by airport. As a result, CATS users must wait almost a year to obtain data for a particular fiscal year. Further, CATS data have anomalies and potential errors, such as data from airports that were not required to file, which can affect totals for a given year.

Note: While 506 airports were required to submit data, FAA allowed two airport sponsors to consolidate multiple airports into a single submission, resulting in 446 expected airport submissions.

FAA has taken some steps to improve CATS data quality, such as performing occasional data checks. However, FAA does not have sufficient data controls to ensure the quality of CATS data. For example, FAA does not have a procedure to consistently identify airports newly required to submit data due to increased passenger boardings. FAA officials told GAO they planned to update the CATS website, which could add this and other functions, but that the update had been delayed. Implementing data controls would result in better quality data to inform policy and other decisions. Additionally, FAA has not communicated specific data limitations to users. For example, information about the number of airports that submitted their financial data for a particular fiscal year could help users understand the completeness of the data and qualify the data for their purposes.

Why GAO Did This Study

Each year, approximately 500 commercial service airports must submit their financial data to FAA, within the Department of Transportation. These reporting requirements were enacted in 1994 to enable FAA to evaluate airports’ compliance with revenue-use requirements and inform the public on how airports collect and spend funds, according to FAA. These airports are generally publicly owned and rely on a mix of revenue sources, such as airline payments, parking revenue, and federal grants.

The FAA Reauthorization Act of 2024 includes a provision for GAO to review airport financial reporting. This report examines (1) how FAA and stakeholders have used CATS data; (2) the extent to which CATS data are complete, timely, and accurate; and (3) the extent to which FAA has taken actions to improve CATS data quality and communicated any data limitations to users.

GAO reviewed CATS data for fiscal years 2019 through 2023; FAA guidance; and publications that cited CATS, identified through a literature search. GAO interviewed officials from FAA headquarters and nine regions; 12 industry stakeholders and researchers; and officials from 10 airports, selected at random but to reflect a range of sizes and regions. GAO also compared CATS data quality policies with federal data standards.

What GAO Recommends

GAO is making three recommendations to FAA, including that FAA implement controls to improve the quality of CATS data and disclose known limitations of the data on the CATS website. The Department of Transportation concurred with the recommendations.

|

Abbreviations |

|

|

|

|

|

CATS |

Certification Activity Tracking System |

|

CPE |

cost per enplanement |

|

DOT |

Department of Transportation |

|

FAA |

Federal Aviation Administration |

|

NPIAS |

National Plan of Integrated Airport Systems |

This is a work of the U.S. government and is not subject to copyright protection in the United States. The published product may be reproduced and distributed in its entirety without further permission from GAO. However, because this work may contain copyrighted images or other material, permission from the copyright holder may be necessary if you wish to reproduce this material separately.

April 14, 2026

The Honorable Ted Cruz

Chairman

The Honorable Maria Cantwell

Ranking Member

Committee on Commerce, Science, and Transportation

United States Senate

The Honorable Sam Graves

Chairman

The Honorable Rick Larsen

Ranking Member

Committee on Transportation and Infrastructure

House of Representatives

Commercial service airports, which support air service for the traveling public, play a critical role in the nation’s aviation network. These airports are generally publicly owned by airport sponsors such as local governments, state governments, or regional authorities.[1] Airports rely on a mix of revenue sources, such as payments from airlines, revenue from parking and airport retail, and federal grants. In general, commercial service airport sponsors receiving federal grants for airport development projects are required by statute to file annual financial reports with the Federal Aviation Administration (FAA).[2] Each year, approximately 500 such airports—ranging from large airports like George Bush Intercontinental Airport in Texas, to much smaller airports like Devils Lake Regional Airport in North Dakota—must submit their financial data. FAA is responsible for ensuring these airports meet federal financial reporting requirements.[3]

FAA created the Certification Activity Tracking System (CATS) website for airport officials to file and certify their annual financial data, such as operating expenses, revenues, and debt, as well as financial transactions with government entities. The data reported by airports through the CATS website are publicly accessible, and stakeholders—such as aviation industry associations—and researchers can use the data.

The FAA Reauthorization Act of 2024 includes a provision for GAO to review FAA’s airport financial reporting program.[4] This report examines 1) how FAA and stakeholders have used data from CATS; 2) the extent to which CATS data are complete, timely, and accurate; and 3) the extent to which FAA has taken actions to improve CATS data quality and communicated any data limitations to users.

CATS comprises two parts: 1) Form 126, which records financial transactions between airports and other government entities; and 2) Form 127, which captures general financial information, such as operating expenses, revenue, and debt. For the purposes of this report, “CATS data” refers to Form 127. We did not include Form 126 data in our review, because we found that these data are primarily used within FAA to monitor airport compliance with revenue requirements and are not as often used outside of FAA.

To address all three objectives, we interviewed officials from FAA and 10 airports.[5] We selected the airports randomly but ensured our selection met certain criteria, such as covering a range of FAA regions and submission statuses for fiscal year 2023 CATS data (six airports submitted CATS data on time, two airports edited submissions after the deadline, and two airports had not submitted CATS data).[6] We also selected airports to represent a range of sizes (two large hub, two medium hub, two small hub, two nonhub, and two nonprimary nonhub airports) as determined using FAA’s calendar year 2022 enplanement (i.e., passenger boardings) data.[7] The information provided by the 10 selected airports is not generalizable to all airports, but provides illustrative examples of airport officials’ views on and experiences with financial reporting. We also reviewed applicable federal statutes, regulations, policies, and procedures related to airport financial reporting and compliance reviews.

To examine how FAA and stakeholders have used CATS data, we conducted a literature search and reviewed reports from FAA, aviation industry stakeholders, and researchers.[8] To identify relevant publications using CATS data, we conducted a literature search for academic and think tank publications from calendar years 2020 through 2025.[9] We also interviewed 10 aviation industry stakeholders—five aviation industry associations, two airport consultants, and three bond rating agencies—and two researchers.[10] We selected aviation industry stakeholders based on our prior aviation work and recommendations by FAA and others.[11] We selected researchers to interview based on the results of our literature search.

To describe the extent to which CATS data are complete, timely, and accurate, we reviewed CATS data for fiscal years 2019 through 2023.[12] At the time of our review, fiscal year 2023 was the most recent year of CATS data available.[13] To determine the completeness of the data, we compared the airports that submitted CATS data for these years with the airports required to file due to boarding at least 2,500 passengers based on the preceding year’s FAA enplanement data. We reviewed the timeliness of airports’ submissions to CATS by comparing an airport’s fiscal year end date with its submission date, and we discussed the limitations of CATS data for this use with FAA officials. Additionally, to describe the accuracy of the data, we performed data reliability checks to identify missing or outlying data, negative entries in inappropriate fields, and other anomalies.[14]

To determine the extent to which FAA has taken actions to improve CATS data quality and communicated any data limitations to users, we reviewed FAA documents on CATS.[15] We interviewed officials at FAA’s headquarters and the nine FAA regions about financial reporting guidance, compliance reviews, and other CATS data verification efforts. We also interviewed FAA officials about the costs of administering CATS, including the number of estimated staff hours and the cost of any associated contracts. We evaluated FAA’s CATS data quality practices against the Department of Transportation (DOT) Information Dissemination Quality Guidelines, which DOT developed in accordance with what is commonly referred to as the Information Quality Act.[16] We also evaluated FAA’s CATS data policy and practices against FAA’s Data and Information Management Policy.[17] In addition, we reviewed FAA’s CATS website for communications that accompanied the data and evaluated FAA’s communication of CATS data limitations against one of our five key practices for transparently reporting government data—specifically, to fully describe the data.[18] Furthermore, we evaluated FAA’s procedures for CATS against federal internal control standards for quality information and external communication.[19]

We conducted this performance audit from November 2024 to April 2026 in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

Background

Commercial Service Airports

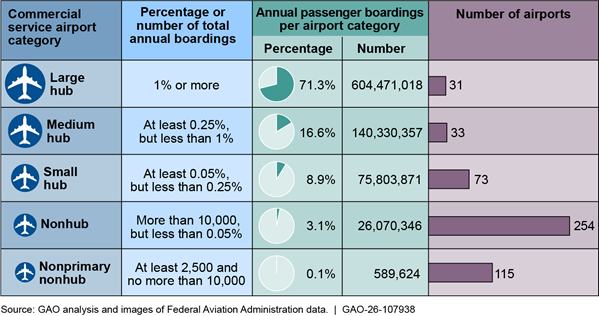

Of the thousands of U.S. airports designated by FAA as part of the national airspace system, about 500 are commercial service airports, which are publicly owned, have scheduled air service, and board at least 2,500 passengers per year.[20] Commercial service airports are classified in statute into five categories based on their annual passenger enplanements, or boardings.[21] The 137 airports in the largest three categories—large hub, medium hub, and small hub—support the vast majority of passenger boardings, accounting for about 97 percent of boardings in 2022.[22] The remaining two categories, nonhub and nonprimary nonhub, comprised over 360 airports but accounted for about 3 percent of total passenger boardings in 2022. (See fig. 1.)

Figure 1: Categories and Characteristics of the 506 Commercial Service Airports in the U.S., Based on Calendar Year 2022 Passenger Boarding Data

Airport Funding and Financial Reporting Requirements

According to FAA, airports in the national airspace system have an estimated $67.5 billion in capital development expenses from 2025 through 2029, including for airport terminal and other projects.[23] Airports receive funding from a variety of sources for these expenses, including federal Airport Improvement Program grants, Passenger Facility Charge fees added to airline tickets, revenue generated through airport parking and concessions, and fees paid by airlines.[24] We have reported that collectively, smaller airports receive more federal Airport Improvement Program grant funding than larger airports.[25] Some airports also obtain financing for airport infrastructure projects by issuing revenue bonds. Bond rating agencies work with airport sponsors going to the bond market to assign risk ratings to airport bonds. We have also reported that larger airports are able to generate more bond proceeds than smaller airports, in part because larger airports are more likely to have a greater, more certain revenue stream to repay debt.[26]

Airport sponsors receiving federal grants for airport development projects are required by statute to file annual financial reports with FAA.[27] As implemented by FAA, recipients of Airport Improvement Program grants, such as commercial service airport sponsors, that had 2,500 or more passenger boardings in the prior calendar year are required to file such reports with FAA.[28] According to FAA, these reporting requirements were enacted in 1994 to provide FAA with a means of evaluating airports’ compliance with revenue-use requirements, and to inform the public on how airports collect and spend funds. In general, under federal statute and regulation, airport revenue must be used for airport purposes and may not be diverted for other uses.[29] However, expenditures from certain airport sponsors, called grandfathered airport sponsors, are exempt from this requirement.[30]

Separate from their financial reporting to FAA, airport sponsors might prepare annual financial statements that combine a single airport’s financial information with the financial information of other airports or infrastructure managed by the same state government, local government, or regional authority.[31] For example, the Maryland Department of Transportation reports financial information for Baltimore/Washington International Thurgood Marshall Airport together with financial information for Martin State Airport.[32] And the Port of Oakland financial statements include one airport, Oakland San Francisco Bay Airport, along with a major maritime seaport, a publicly owned electric utility, and commercial real estate holdings.

FAA Oversight of Airports’ Financial Reporting

FAA’s Office of Airports Compliance and Management Analysis (compliance office), within FAA’s headquarters, enforces the statutory requirements for airport revenue use, conducts grant assurance compliance reviews, and issues program guidance. The compliance office’s Financial Compliance Division administers CATS and had 10 staff as of December 2025, according to FAA officials. Officials reported that the Financial Compliance Division had three staff as of March 2024, but the staffing level grew between then and January 2025. FAA also has regional compliance officers that operate in its nine regional offices, most of which also support airport district offices that oversee airport planning, development, and safety in their respective states.

FAA’s CATS website is publicly accessible, with airport data available for any year starting from 1996. The website also has protected access for airport officials to log in and self-report their data as outlined in FAA’s guidance to airports. Specifically, an FAA Advisory Circular instructs airports how to submit their information to CATS.[33] For instance, the guidance states that an airport’s chief financial officer must certify the accuracy of the information reported. CATS data fields include aeronautical revenue (e.g., landing fees charged to airlines and fuel sales), nonaeronautical revenue (e.g., parking, rental car, and concessions), operating expenses, capital expenditures, and debt service. See appendix I for examples of CATS data sections and descriptions.

FAA and Stakeholders Have Used CATS for Multiple Purposes, as the Only Centralized Source of Airport Financial Data

FAA Has Used CATS to Report on Airport Financial Performance and Allocate Pandemic Relief Funding

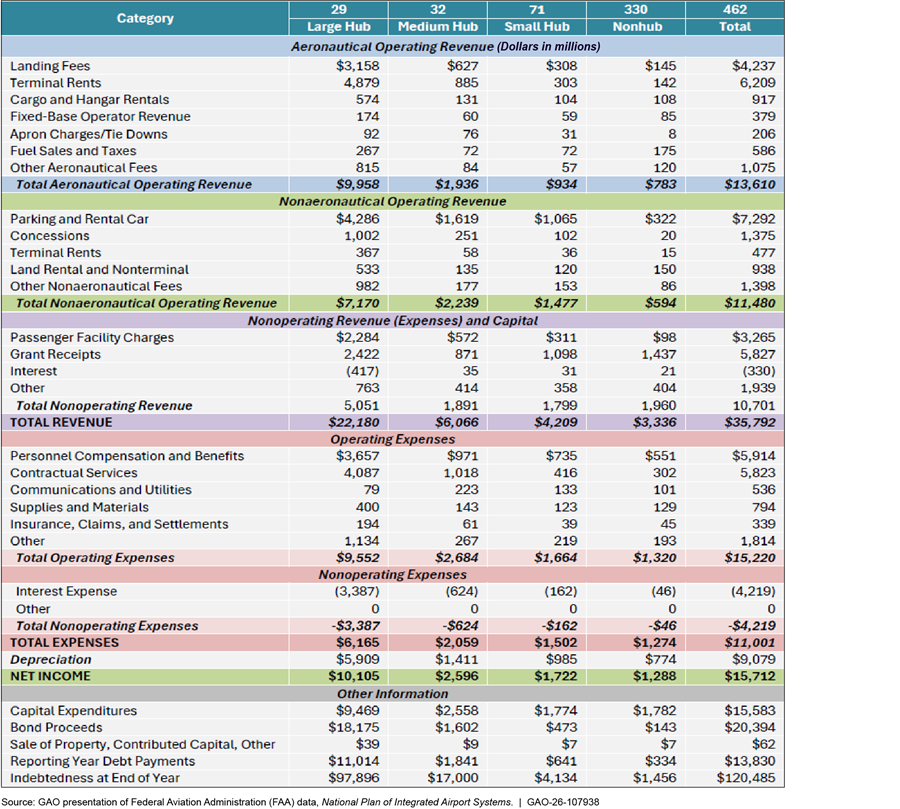

FAA reports CATS data in its biennial National Plan of Integrated Airport Systems (NPIAS) to describe the financial performance of the airport system.[34] FAA officials stated that NPIAS, which describes the infrastructure needs of public airports in the U.S., is one of the most downloaded files on FAA’s website and of particular interest to aviation industry associations. According to officials, FAA has included CATS data in NPIAS for at least the last 20 years, and NPIAS is currently the only place where FAA reports CATS data. The current NPIAS includes key financial totals from 2022 across commercial service airports, such as total airport revenue of $35.8 billion and bond proceeds of $20.4 billion, as well as subtotals by airport size.[35] NPIAS also includes a table containing data for over two dozen revenue and expenditure categories from CATS, including aeronautical revenue, nonaeronautical revenue, and operating expenses. See appendix II for this table.

In May 2020, FAA used CATS data to calculate allocations of about $7.4 billion in CARES Act emergency pandemic relief funding to commercial service airports.[36] FAA officials said this was the only time FAA had used CATS data to determine airport grant allocations. FAA implemented the statutory CARES Act allocation formula using airports’ unrestricted cash reserves and debt service from fiscal year 2018 CATS data.[37] As we previously reported, FAA officials had stated that making these allocations expeditiously required them to rely on airports’ CATS financial data filings.[38]

Our prior work found that this approach to allocating CARES Act funding resulted in some small airports being allocated large amounts of funding relative to their passenger activity or annual budgets. Specifically, we previously reported that 31 airports had an initial grant allocation of over four times their annual operating expenses, according to FAA.[39] Commercial service airports with high amounts of cash reserves relative to debt service received a higher share of grant funds.[40] In addition, officials said there may have been instances of zeroes or blank fields in the CATS data that could have affected an airport’s allocation, as we had reported.[41] FAA took actions to limit some airports’ initial CARES Act grant amounts to no more than four times their annual operating expenses and required airports to provide justification for accessing additional allocated funds. FAA allocated the two subsequent rounds of COVID relief airport funds—provided in the Coronavirus Response and Relief Supplemental Appropriations Act, 2021[42] and American Rescue Plan Act of 2021[43]—based on passenger boardings.

Stakeholders Have Used CATS to Analyze the Aviation Industry, As It Is the Only Centralized Source of Financial Data on Airports

Aviation industry stakeholders have used CATS to analyze airport financial performance. Seven of the 10 aviation industry stakeholders we interviewed have used CATS data for purposes that include assessing airport trends, informing airport credit ratings, or helping to benchmark airports against comparable airports.[44]

Five aviation industry stakeholders told us they have used CATS data for internal purposes. For example, representatives of a bond rating agency said they have used CATS data to compare similar airports and examine general trends but would not use the data in their formal analyses without additional corroboration. Similarly, an airport consultant said they have used CATS data for wide-ranging comparisons across large groups of airports and for initial information on an airport’s finances. However, the consultant stated they would need to verify the data for assessments requiring more confidence, such as those informing business decisions.

Two stakeholders we spoke with—an aviation consultant and bond rating agency—have cited CATS data in reports or airport financial analyses. For example, an aviation consultant used CATS data to report the cost per enplanement (CPE) trends for large and medium hub airports.[45] The aviation industry uses CPE—the average airline payment to the airport per passenger—to evaluate an airport’s performance. The consultant preferred to use data from airport financial reports or bond rating agency analyses for this purpose, but used CATS if the data from those sources were unavailable. In another example, a bond rating agency used CATS data on airport revenues such as parking and rental car revenue to compare the individual airport with all large hub airports.[46] This report showed that in contrast with large hub airports on average, the individual airport relied more on airline revenue than on parking and rental car revenue.

Researchers from academia and think tanks have also used CATS data. We identified 22 articles published from 2020 through 2025 authored by 10 different lead researchers that cited CATS data. Generally, these researchers used the data to provide background financial information on airports or in analyses to support key findings. For example, a researcher from a think tank used CATS data to compare totals of airport revenues and expenses and develop options for airport revenue policies.[47] The study aimed to inform Congress on whether federal policies enable airports to receive and raise sufficient funds for infrastructure investments to meet future demand. In addition, a researcher from academia who authored 13 of the articles we identified told us that his research on airport competition, airport market structure, and productivity and efficiency of airports uses CATS data for financial and economic analyses.[48] For example, the researcher said that when assessing an airport’s cost efficiency, he used CATS data on airline and passenger revenues and operating costs to understand how well an airport was performing.

We found that CATS is the only centralized source of financial data on airports, according to information from FAA and our own analysis. FAA officials stated that CATS is the agency’s only source of airport financial data. Furthermore, in our analysis of publicly available airport financial statements, we found that the financial data in these statements could not be easily aggregated across airports. Specifically, to verify the accuracy of CATS data, we attempted to reconcile CATS data with publicly available airport financial statements for a sample of 50 airports. However, we were unable to do so for many airports, because the statements did not isolate airport data from other entities; because the information fields differed from those in CATS; or both.[49] An aviation consultant told us that unlike individual airports’ financial statements, CATS provides financial data quickly and uses a common set of data fields.

Five aviation industry stakeholders and two researchers we spoke with also noted that CATS is the only publicly available source of financial information on all commercial service airports.[50] For example, representatives from an airline industry association viewed CATS as valuable because it is the only industry-wide airport financial database and allows them to analyze trends in airports’ operational costs, including for key metrics and across airports for a single line item. A think tank researcher told us that CATS provides clear and impartial data because airports directly report the data to FAA, and that there is no equivalent source of such information.

Most Airports Submitted CATS Data, but the Extent of Timeliness and Accuracy Is Unknown

Most Airports Submitted CATS Data for Fiscal Year 2023, but Some of the Smallest Airports Did Not

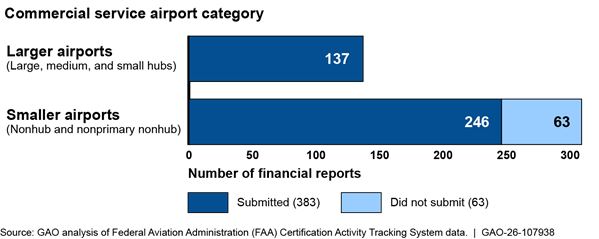

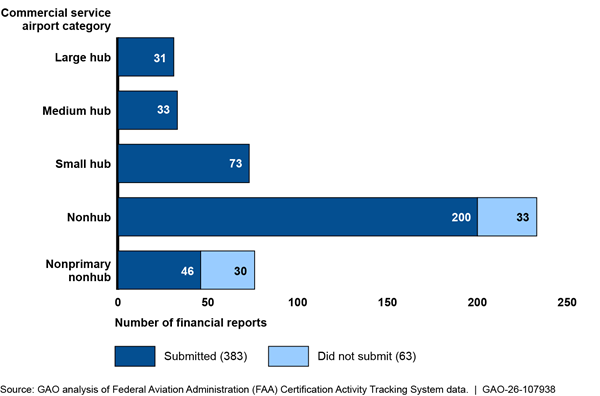

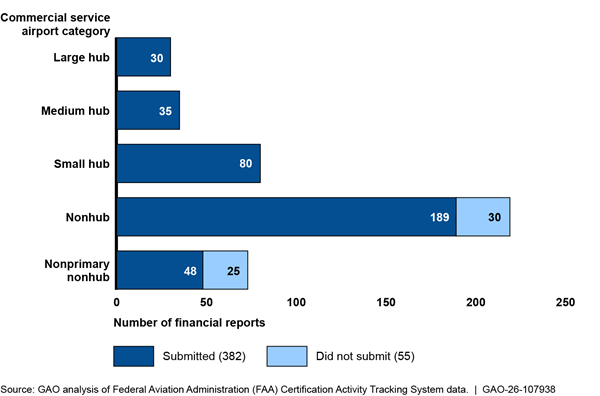

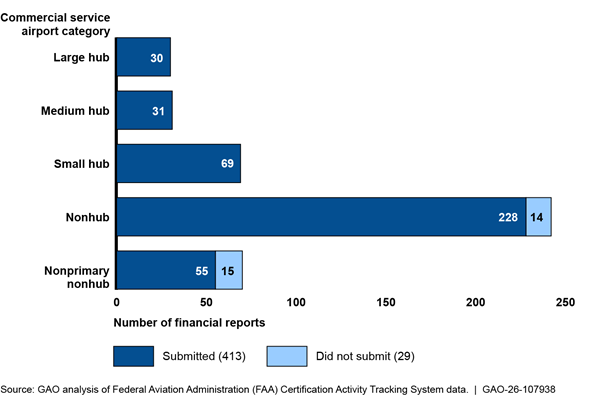

For fiscal year 2023, all large, medium, and small hub airports submitted CATS data, but some of the smallest airports did not do so. Specifically, 63 airports—33 nonhub and 30 nonprimary nonhub airports—did not submit fiscal year 2023 data. These 63 airports represent 14 percent of the total 446 required airport submissions (see fig. 2). While 506 airports were required to submit financial data to CATS in fiscal year 2023, FAA allowed two airport sponsors to consolidate multiple airports into a single submission, resulting in 446 required airport submissions.[51] We also reviewed CATS data for fiscal years 2019 through 2022. See appendix III for data for each of these fiscal years.

Figure 2: Number of Airport Financial Reports Required to Be Submitted to FAA by Airport Category, Fiscal Year 2023

Note: We used data as of March 31, 2025, for our analysis. While 506 airports were required to submit financial data to the Certification Activity Tracking System, FAA allowed two airport sponsors to consolidate multiple airports into a single submission, resulting in 446 airport submissions. Commercial service airports are classified in statute into five categories based on their annual passenger enplanements, or boardings. See 49 U.S.C § 47102(7), (11), (13), (14), (16), and (25).

Additionally, we found that 14 airports required to submit CATS data in fiscal years 2019 through 2023 had not done so for any of those 5 years at the time of our review. Officials from the two airports we selected that had not submitted CATS data told us they did not do so partly due to staff turnover. For example, officials from a nonhub airport said that they have had multiple finance directors since 2019. An official from another airport stated he had been in his role for several months and was unaware of CATS submission requirements. Officials from both selected airports told us that after our interview, they submitted CATS data. FAA officials stated that they periodically communicate with airports that are required to submit CATS data but have not done so, including these 14 airports, and request they submit the data.[52] We discuss FAA’s efforts to communicate with airports regarding their data submissions later in the report.

Limitations in CATS Make It Difficult for FAA to Track the Timeliness of Airports’ Submissions

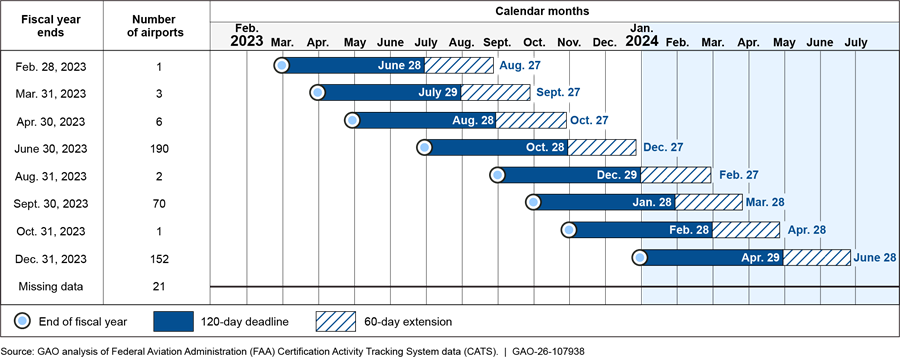

FAA requires airports to submit CATS data within 120 days of the end of the airport’s fiscal year. Airports may request an additional 60-day extension, which is granted automatically in CATS.[53] Therefore, airports effectively have 180 days after the end of their fiscal year to submit data to CATS.

There is no single annual deadline for CATS reporting, because CATS data are reported by the airport’s fiscal year, which varies by airport. Therefore, airports submit data throughout the year. Based on 2023 CATS data, we found that airports’ most common fiscal year ends are June 30, September 30, and December 31 (see fig. 3). Thirteen airports had other fiscal year ends. Consequently, fiscal year 2023 CATS submissions were expected to occur over a range of time, with the earliest expected reporting date for 2023 on June 28, 2023, and the latest reporting date (including the 60-day extension period) on June 28, 2024.

Figure 3: Airport Fiscal Year Ends and CATS Submission Deadlines, Based on Fiscal Year 2023 CATS Data as of March 31, 2025

Notes: Our analysis does not include airports that submitted data to CATS that were not required to do so (i.e., those airports that did not have more than 2,500 passenger boardings in 2022).

Three airports reported fiscal year end dates that were not at the end of a month. We used these airports’ publicly available audited financial statements to confirm they had fiscal year end dates at the end of June, September, and December.

Given the variation in CATS reporting deadlines for airports, and in the timeliness of data submissions, users of CATS data must wait almost a year to obtain data for a particular fiscal year. For example, an aviation industry stakeholder told us they waited until December 2024 to download 2023 CATS data, to account for the time it takes airports to submit their information to CATS. Further, FAA’s most recent NPIAS report—published on September 30, 2024—used CATS data from 2022 and noted it was the latest year of available data.[54]

We found that the following factors make it difficult for FAA to accurately determine the timeliness of airports’ CATS submissions:

· The CATS website displays the date of an airport’s latest submission and does not record an airport’s data submission history, according to FAA officials. As a result, if an airport submits data by the deadline and later updates its submission, then its original submission date is overwritten with the date of the update. FAA guidance allows for such updates, stating that FAA prefers airports submit audited information to CATS; airports may submit unaudited information to meet the filing deadline and then resubmit when audited information becomes available.[55] We asked FAA for data on the number of airports that submitted unaudited data and later submitted audited data, but due to the limitations in the website, officials told us CATS could not reliably summarize such information.

· CATS allows airports to submit data for any year at any time. Officials at one selected airport told us they originally submitted their CATS data on time, but resubmitted data for multiple prior years after discovering an accounting error, such that the year-to-year data would be comparable. The original submission dates for those years were overwritten by the last submission date.

· In reviewing CATS data for fiscal years 2019 through 2023, we found that the “Date Filed” field for about 1 percent of airports, on average, was not populated. FAA officials told us the “Date Filed” field could be blank if airport staff save their data as a work in progress in the system instead of submitting their data in CATS.

We discuss FAA’s efforts to track the extent to which airports meet reporting deadlines later in this report.

CATS Data Have Anomalies and Potential Errors, but the Extent of Accuracy Is Unknown

We found that CATS data have anomalies and potential errors that could affect financial data totals for any given year. The CATS website notes that the data are self-reported by airports and accordingly, FAA makes no representation about the validity and accuracy of the data. FAA officials also told us the data may have errors, given the inherent risk of self-reported data.

Specifically, in our review of CATS data for fiscal years 2019 through 2023, we found the following anomalies and potential errors:

· The data include airports that were not required to file financial information based on the preceding year’s passenger boardings. We found that on average, 27 airports per year that were not required to submit CATS data had done so.[56] FAA officials told us they do not remove such airports from CATS because doing so would delete the airports’ past filing history, and the airports may have previously met the requirement to report. One airport sponsor said they submit CATS data for all three airports they oversee, regardless of whether each airport is required to report. The additional data submissions from airports that do not meet the passenger boardings threshold could inflate the data totals, resulting in inaccurate reporting. For example, the CATS summary data for total commercial service airport revenue could be overstated if additional revenue data from airports that did not meet the definition of such airports were also included.

· Some airports may not have accurately entered data in CATS with the correct positive or negative dollar amount. For instance, in 2023, four airports entered negative rather than positive amounts for unrestricted cash and investments, which FAA officials said could be an error. According to FAA officials, airports might enter their change in net assets in this field, contrary to what the advisory circular guidance states. FAA officials said that because data are self-reported by airport sponsors, they cannot ensure the data are entered correctly. They also stated that the CATS website does not restrict the format of data that the airport user can enter into the data fields. Therefore, a user could, for example, enter negative numbers in fields that should only include positive numbers.

We discuss FAA’s efforts to address data errors and anomalies later in this report.

FAA Has Taken Some Steps to Improve CATS Data but Does Not Have Sufficient Quality Controls and Has Not Communicated Data Limitations

FAA Has Taken Some Steps to Improve CATS Data Quality, Including Reviewing CATS Submissions

FAA has taken some steps to improve CATS data quality, including conducting annual compliance reviews of some airports and periodically reviewing CATS data for timeliness of submissions and any errors or anomalies.[57] In addition, FAA makes guidance available to airports on how to submit data to CATS. FAA officials said they had planned to update the CATS system to help improve data quality, but the update has been delayed due to other priorities.

FAA headquarters staff conduct compliance reviews of airport sponsors that include a review of CATS data quality. According to the FAA Airport Compliance Manual, FAA conducts these compliance reviews to determine if airport sponsors are complying with federal statutes, regulations, and grant assurances, including CATS reporting requirements.[58] As part of these reviews, FAA officials said they meet with airport officials on-site and reconcile 6 years of the airport’s submitted CATS data with the airport’s financial records and audited financial statements to identify any discrepancies.[59] FAA has completed and publicly issued 18 compliance reports since 2012, according to its website. FAA officials said they intended to increase the number of compliance reviews to four a year, given the increase from three to 10 staff in the Financial Compliance Division as of December 2025. In its Airport Compliance Manual, FAA states that given the number of airports, it cannot conduct on-site compliance reviews at each airport annually, and that periodic monitoring of airports is necessary.

In addition, FAA officials stated they monitor airports’ compliance with reporting requirements by periodically reviewing airports’ submissions of CATS data and communicating with airport sponsors about potential reporting errors. FAA headquarters officials said they aim to review CATS data quarterly, to determine whether the airports required to submit their financial data have done so; FAA then reaches out to airports that have not submitted information. These officials, as well as officials at one regional FAA office, also told us they periodically perform CATS data checks for errors and anomalies and reach out to airports that have errors or anomalies in their data. In the regional office that regularly performs such data checks, the regional compliance official created a review tip sheet that notes common CATS errors, such as a $0 value for grant receipts (which includes federal Airport Improvement Program grants distributed by FAA) or Passenger Facility Charges.

FAA also makes its 2011 CATS Advisory Circular available for airports. The guidance provides information designed to help airports report complete, timely, and accurate data to CATS. For example, the guidance states that FAA requires that airports’ chief financial officer certify the accuracy of the data and describes FAA’s monitoring and compliance actions. Specifically, the Advisory Circular states: “If a sponsor fails to submit its reports, the FAA will issue a letter notifying the sponsor of the overdue report. If the reports are not received within 30 days of the letter, the FAA will take action.” According to the guidance, these actions may include withholding future funds or suspending existing grant payments. According to FAA officials, airports generally file CATS data after being contacted by FAA, without the need to take the step of withholding funding to the airport.

FAA officials told us they had planned to update the CATS website, but the update has been delayed. According to the officials, the update is intended to enhance the functionality of CATS to help ensure financial data are complete, timely, and accurate.[60] FAA solicited input from aviation industry associations in 2019 on how to improve CATS, according to FAA and represent GAO-26-107938 atives from one association. FAA officials said the original CATS update was planned for completion in November 2023. However, due to delays, other technology priorities, and a leadership change, the update has been paused. As of December 2025, FAA officials said they had recently restarted discussions with a contractor about the update and were developing plans and a project timeline.

FAA Does Not Have Sufficient Data Controls or Defined Roles and Responsibilities for Monitoring the Quality of CATS Data

Although FAA officials have taken some steps to improve CATS data quality, our review identified several issues with CATS data quality, as discussed above. FAA officials stated that airports are responsible for certifying the completeness and accuracy of the data they submit. However, by implementing additional data controls and clearly defining the roles and responsibilities of its headquarters and regional officials for ensuring the quality of CATS data, FAA could improve the completeness, timeliness, and accuracy of the data.

FAA Does Not Have Sufficient Data Controls to Ensure the Quality of CATS Data

According to DOT’s Information Dissemination Quality Guidelines, agency components, including FAA, should ensure disseminated information is accurate, clear, complete, and unbiased as a basic standard of quality.[61] Moreover, federal internal control standards state that management should process relevant data obtained or generated from reliable sources into quality information through the entity’s information system.[62] However, FAA does not have sufficient controls to ensure the quality of CATS data. Specifically, FAA does not have controls or functions in place to ensure it consistently 1) identifies the commercial service airports required to submit CATS data each year; 2) verifies that all required airports submit data to CATS; 3) tracks airports’ submissions relative to deadlines to determine the submissions’ timeliness; and 4) reviews CATS data to identify errors and anomalies.

· Identifying the airports required to submit CATS data. FAA does not have sufficient controls to identify the commercial service airports required to submit data to CATS each year. The number of airports required to do so varies by year, depending on airports’ passenger boardings the prior year. Some airports may fall below the 2,500 annual passenger boardings threshold and no longer need to file, while other airports may have increased their passenger boardings and be newly required to file. However, according to FAA officials, FAA’s annual passenger boarding data are housed in a separate FAA data system that does not interface with CATS. According to FAA officials, the planned update of CATS could include enabling it to interface with FAA’s passenger boarding data, such that CATS could automatically track the airports that met the passenger boardings threshold for the year. FAA staff currently perform this function manually. FAA does not have a procedure for doing so consistently, as officials said they were awaiting the CATS website update to better track the airports required to submit data.

· Verifying that all required airports submit CATS data. According to FAA guidance, FAA officials are to verify whether airports have submitted information to CATS and contact airport sponsors that have not done so. The CATS website does not currently send automated alerts to FAA officials about submission deadlines, so FAA officials must manually review CATS data for completeness before reaching out to airports. Officials from three regional offices said they check CATS at least twice a year to determine whether airports in their region submitted data.[63] FAA headquarters officials also stated that they periodically communicate with airports that have not submitted data to request they do so. According to FAA officials, until recently, headquarters staffing levels had limited their ability to contact airports that had not submitted CATS data. As mentioned earlier, we identified 63 airports that had not submitted 2023 data, and 14 airports that had not submitted data in any of the 5 years we reviewed, but should have done so.[64] In December 2025, FAA headquarters officials told us that with additional staff, they were in the process of contacting these airports, some of which subsequently submitted CATS data. FAA officials said they hoped the CATS update would enable the system to send alerts to FAA when an airport had not met its submission deadline.

· Tracking airport submissions to determine their timeliness. As discussed above, CATS overrides the prior submission date each time an airport edits its entries, making it difficult for FAA to determine whether an airport submitted data after the deadline or originally submitted data on time but later edited the data. FAA officials in three regions track whether airports submitted information on time by conducting reviews, such as checking CATS multiple times a year.[65] According to FAA officials, to enable officials to determine whether airports submitted information on time, CATS could be updated such that the system records each time an airport modifies its submission.

· Identifying data errors and anomalies. According to FAA, self-reported data have an inherent risk of errors. To identify errors and anomalies, FAA officials told us they have periodically reviewed CATS data and reached out to the airport sponsors to address issues they identified. However, the officials said they did not have documented procedures specifying the kinds of errors or anomalies that regional office staff should identify or when to review the data. As discussed above, the CATS website does not restrict data entry formats. FAA officials said CATS could be updated to include controls limiting the format of the data entered by airport users, which would reduce the risk of errors. For example, a CATS data field that should have a negative value, such as the interest expense field, would not allow the user to enter a positive value.[66]

FAA’s efforts to update the CATS website have recently resumed, but it is too early to determine the extent to which the updates will address the issues we identified. By implementing data controls to address the quality issues identified above, such as identifying airports required to submit data and tracking submission deadlines, FAA could improve the completeness, timeliness, and accuracy of CATS data. Doing so would enable FAA to better inform the public on how airports collect and spend funds. FAA and aviation industry stakeholders would also have better data to inform policy and other decisions affecting airport financial performance.

FAA Has Not Clearly Defined the Roles and Responsibilities Between Headquarters and Regional Staff for Monitoring CATS

FAA’s Data and Information Management Policy promotes the proactive governance and management of data and information at the agency by establishing the roles and responsibilities of FAA’s different levels.[67] For instance, the policy states that officials at the operational level are responsible for validating and ensuring the quality of data. Moreover, federal internal control standards state that in establishing an organizational structure, management should consider how divisions, operating units, and functions interact to fulfill their overall responsibilities.[68] According to these standards, management should also assign responsibilities and delegate authority to key roles throughout the agency.[69] However, FAA has not clearly defined or implemented the roles and responsibilities for ensuring airports’ compliance with financial reporting requirements of headquarters staff, which includes 10 staff in its Financial Compliance Division, or of the regional compliance officers in its nine regional offices.

FAA’s Airport Compliance Manual states that the FAA headquarters compliance office is responsible for implementing and managing the airport financial reporting program.[70] The manual also states that FAA regional and district offices are responsible for monitoring airports’ compliance with financial reporting requirements by downloading their region’s status reports in CATS. FAA headquarters officials said that the regional offices are more familiar with the airports in their region and have greater insight into an airport’s likely financial situation than headquarters officials. However, FAA regional offices have not consistently monitored airports’ financial reporting requirements.

In particular, we found that regional offices differed in their understanding of their role in monitoring airports’ compliance with reporting requirements. Officials at two of the nine regional offices said monitoring was the responsibility of FAA headquarters, while officials at three of the regional offices said it was their responsibility.[71] Furthermore, regions differed in the extent to which they conducted monitoring activities. Officials from one region described their process for identifying airports required to submit CATS data, sending deadline notices to airports, tracking airports that miss the deadline, and reviewing the data for errors and anomalies. In contrast, officials from another region said that headquarters was responsible for overseeing CATS, and that their region did not communicate with airports about CATS submissions. Officials from three regions told us they regularly tracked whether airports submitted CATS data, while officials from the other six regions said they did not do so. Of the six regions that did not track airports that submitted CATS data, officials at four regions said they had currently or previously relied on headquarters officials to track such information.

FAA officials told us that their anticipation of a CATS website update and recent changes in staffing have contributed to their current approach to monitoring airports’ compliance with reporting requirements. According to FAA officials, the CATS website update that FAA expected to complete by 2023 included automated review functions that could affect the roles of headquarters and regional staff in monitoring CATS. However, as mentioned earlier, FAA has not implemented this update. Furthermore, with the recent increase in headquarters staff, FAA officials said they expected the new staff would perform additional CATS review functions, conduct more airport compliance reviews, and assume more of the responsibilities shared with regional offices. For instance, after the end of a fiscal quarter, headquarters officials may review the data to see whether required airports have submitted data to CATS and contact airports that have not done so. Officials also told us the regional offices have had some staff turnover, which has affected their familiarity with the CATS compliance review functions.

Clearly defining roles and responsibilities for monitoring airports’ compliance with reporting requirements, including who is responsible for following up with airports to submit data, would help FAA ensure that airports submit CATS data on time and that the data have fewer errors and anomalies, thereby improving the quality of the data.

FAA Has a Disclaimer on the CATS Website but Has Not Communicated Specific Data Limitations to Users

Our key practices for transparently reporting government data include fully describing the data, including disclosing known quality issues such as those related to the completeness, timeliness, and accuracy of the data.[72] Providing such information helps users determine whether and how to use the data. In addition, federal internal control standards state that agencies should communicate relevant and quality information with appropriate external parties.[73]

While FAA has a general disclaimer on the CATS website about the quality of CATS data, it has not communicated specific data limitations to users. The disclaimer notes that CATS data are self-reported by airports, and it encourages users to obtain a certified version of the information from airports. The disclaimer reads:[74]

“Airports submit their financial data in accordance with FAA policy and Public Law 103-305. The information is made available via the internet solely for the convenience of the public. The FAA makes no representation as to the validity and accuracy of the information. Individuals relying on this information to make decisions should obtain a separate certified version directly from the airport.”

However, the disclaimer does not provide specific information about the limitations of CATS data, which may be especially important for users that aggregate the data. For instance, as discussed above, not all airports that are required to submit financial information to CATS do so; some airports may not be timely in their CATS submissions; airports have different fiscal year ends; and airport sponsors may update their data over time. FAA officials said that while they had not communicated such limitations, they hoped to do so through a CATS update. They said that in the meantime, users could contact the CATS help desk to obtain this information.

As discussed above, we found that CATS is the only publicly available source of financial data on airports, and stakeholders use the data for multiple purposes. However, users may not be aware of the specific data quality issues we found in our review. For example, representatives of one organization that uses CATS data told us they sometimes download data for a fiscal year only to find that half of the airports have not yet submitted their information. They said it would be helpful if the CATS website included information about how many airports have submitted their information for a given year, so they can know when to download the data. By providing information on the specific limitations of CATS data, FAA could help users understand the completeness of the data, decide whether and how to use the data, and qualify the data for their purposes.

Conclusions

FAA is responsible for ensuring commercial service airports file financial reports that inform the public on how they collect and spend funds. To do so, FAA has established the CATS website, which is the only publicly accessible, centralized source of airport financial data. Aviation industry stakeholders and researchers rely on the quality of CATS data for their reporting and analysis. However, we found that not all airports required to submit CATS data had done so, and that the extent of the data’s timeliness and accuracy were unknown. While FAA has taken some steps to enhance CATS data quality, implementing data controls and clarifying roles and responsibilities for monitoring airports’ compliance with reporting requirements would enable FAA to further improve the completeness, timeliness, and accuracy of the data. Moreover, by communicating the specific limitations of CATS data, FAA could help stakeholders better understand the quality of the data and appropriately qualify it for their purposes. FAA’s planned update of the CATS website and recent staffing changes may present opportunities to take these steps.

Recommendations for Executive Action

We are making the following three recommendations to FAA:

The Administrator of FAA, either through a CATS update or other means, should implement controls to improve the quality of CATS data, such as identifying airports required to submit data, tracking submission history, and identifying errors and anomalies. (Recommendation 1)

The Administrator of FAA should clearly define the roles and responsibilities between headquarters and regional office staff in ensuring airports’ compliance with CATS requirements, including clarifying the staff responsible for following up with airports to submit data. (Recommendation 2)

The Administrator of FAA should disclose on the CATS website the known limitations of CATS data, such as the number of airports that have submitted financial information out of the total that were required to do so and the fact that airport sponsors may update their data over time. (Recommendation 3)

Agency Comments

We provided a draft of this report to DOT for review and comment. In its comments, reproduced in appendix IV, DOT agreed with our three recommendations. DOT referred generally to its efforts underway to improve CATS data, such as engaging a contractor to enhance the CATS website. In addition, DOT provided a technical comment, which we incorporated as appropriate.

We are sending copies of this report to the appropriate congressional committees, the Secretary of Transportation, and other interested parties. In addition, this report is available at no charge on the GAO website at https://www.gao.gov.

If you or your staff have any questions about this report, please contact me at CollinsD@gao.gov. Contact points for our Offices of Congressional Relations and Media Relations may be found on the last page of this report. GAO staff who made key contributions to this report are listed in appendix V.

Derrick Collins

Director, Physical Infrastructure

Table 1: Examples of Data Sections in FAA’s Certification Activity Tracking System (CATS) That Are Filled Out by Commercial Service Airports

|

Section |

Data section |

Description (from FAA Advisory Circular 150/5100-19D) |

|

1.0 |

Passenger Airline Aeronautical Revenue |

All revenue derived from the aeronautical use of the airport by passenger airlines, as opposed to cargo, general aviation, and military. Aeronautical use is any activity that involves, makes possible, is required for the safety of, or is otherwise directly related to the operation of aircraft. Passenger aeronautical revenues include landing fees, terminal rentals and leases, gate use fees, federal inspection fees, and any other costs associated with the terminal that may be billed to the passenger airline separately, such as terminal area apron charges and aircraft tie down fees. The total of this category when divided by total enplanements yields the industry metric, Airline Cost (or Payments) Per Enplanement Passenger. |

|

2.0 |

Non-Passenger Aeronautical Revenue |

Other aeronautical revenues not associated with the direct transport of passengers. Non-passenger aeronautical revenues include landing fees paid by cargo airlines and general aviation and military aircraft; fees charged to Fixed Base Operators to provide flight and aircraft support services to aeronautical users of the airport; cargo and hanger rentals; aviation fuel tax retained for the capital or operating costs of the airport; fuel sales net profit or loss or fuel flowage fees; security reimbursements from the Transportation Security Administration or other federal or state organizations; and other non-passenger aeronautical revenue. |

|

3.0 |

Total Aeronautical Revenue |

This is the sum of Passenger Airline Aeronautical Revenue (Section 1.0) and Non-Passenger Aeronautical Revenue (Section 2.0). |

|

4.0 |

Nonaeronautical Revenue |

Nonaeronautical revenues from airport operations (not derived from uses described in Sections 1.0 and 2.0 above). Nonaeronautical revenue includes land and non-terminal facility leases and revenues; fees and revenue from concessions in the terminal; revenue from retail and duty free operations in the terminal; revenues for terminal services such as telecommunications, advertising, shoeshine stands, and other such sources; revenue from rental car operations; parking and ground transportation revenue; hotel operations revenue; and other nonaeronautical operating revenues. |

|

5.0 |

Total Operating Revenue |

This is the sum of Total Aeronautical Revenue (Section 3.0) and Nonaeronautical Revenue (Section 4.0). |

|

6.0 |

Operating Expenses |

The annual operating expense incurred for each of the following categories: personnel compensation and benefits; communication services and utilities; supplies and materials; contractual services; insurance, claims, and settlements; and other operating expenses. |

|

6.8 |

Depreciation |

If the airport depreciates its assets, the airport reports the depreciation for the reporting fiscal year. |

|

7.0 |

Operating Income (Loss) |

The difference between Total Operating Revenue (Section 5.0) and Operating Expenses (Section 6.0). |

|

8.0 |

Non-Operating Revenue (Expenses) and Capital |

Revenues and expenses that are not derived from operations. Non-operating revenue (expenses) and capital can include: interest income (from restricted and non-restricted investments); interest expense; grant receipts; Passenger Facility Charges; capital contributions; special items (loss); and other revenues and expenses not otherwise reported. |

|

9.0 |

Net Assets |

Net assets, or net position, is the difference between an entity’s total assets and total liabilities. Net asset categories include: change in net assets; net assets (deficit) at the beginning of the reporting period; and net assets (deficit) at the end of the airport’s fiscal year. |

|

10.0 |

Capital Expenditures and Construction in Progress |

Capital expenditures include airfield expenditures; terminal expenditures; parking expenditures; roadways, rail, and transit expenditures; and other capital expenditures even if the structure did not become operational during the fiscal year. |

|

11.0 |

Indebtedness at End of Year |

Indebtedness at the end of year includes the airport’s debt levels in long term bonds (such as General Airport Revenue Bonds); loans and interim financing; and special facility bonds at the end of the reporting period. |

|

12.0 |

Externally Restricted Assets |

Externally restricted assets include restricted assets (such as restricted cash, investments, and accounts receivables— less restricted payables) that are restricted to the repayment of principal and interest or for other debt purposes and restricted assets recorded for purposes other than debt and capital renewal and replacement. |

|

13.0 |

Unrestricted Cash and Investments |

Unrestricted cash and cash equivalents, and unrestricted short-term investments from the current asset section, and unrestricted long-term investments from the non-current assets section of the Statement of Net Assets. If the Statement of Net Assets information is not available, airports should leave blank. |

|

14.0 |

Reporting Year Proceeds |

Reporting year proceeds includes proceeds from the sale of bonds during the reporting period and proceeds from the sale of property. |

|

15.0 |

Debt Service |

Debt service includes the amount of principal and interest paid during the airport’s fiscal year for long-term bonds and indebtedness. |

|

16.0 |

Operating Statistics |

(*optional for airports having fewer than 25,000 enplanements in the preceding calendar year) The purpose of this section is to identify some of the key airport operating statistics for the airport’s fiscal year. This includes: number of passenger boardings; landed weight in pounds; signatory landing fees; annual aircraft operations; passenger airline cost per enplanement; full time equivalent employees at the end of the year; security and law enforcement costs; costs of Aircraft Rescue and Fire Fighting services; cost of repairs and maintenance of airport facilities and equipment; and costs of airport marketing, advertising, and incentives paid to, or on behalf of, air carriers. |

Source: Federal Aviation Administration (FAA) information. | GAO‑26‑107938

Note: This information is found in FAA, Guide for Airport Financial Reports Filed by Airport Sponsors, Advisory Circular 150/5100-19D, (June 23, 2011).

Figure 4: Certification Activity Tracking System (CATS) Data Table from FAA’s National Plan of Integrated Airport Systems 2025-2029

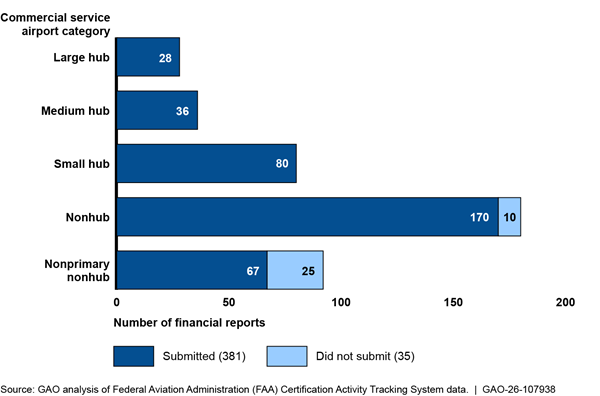

In general, commercial service airport sponsors receiving federal grants for airport development projects are required by statute to file annual financial reports with the Federal Aviation Administration (FAA).[75] FAA created the Certification Activity Tracking System (CATS) website for airport officials to file and certify their annual financial data, such as operating expenses, revenues, and debt. For fiscal years (FY) 2019 through 2022, all large, medium, and small hub airports submitted CATS data, but some of the smallest airports did not do so, as shown in figures 5 through 8. FAA officials said they periodically communicate with airports that are required to submit CATS data but have not done so, and request that the airports submit their data.

Figure 5: Number of Airport Financial Reports Required to Be Submitted to FAA by Airport Category, Fiscal Year 2022

Note: We used data as of March 31, 2025, for our analysis. While 478 airports were required to submit financial data to the Certification Activity Tracking System, FAA allowed two airport sponsors to consolidate multiple airports into a single submission, resulting in 437 airport submissions. Commercial service airports are classified in statute into five categories based on their annual passenger enplanements, or boardings. See 49 U.S.C § 47102(7), (11), (13), (14), (16), and (25).

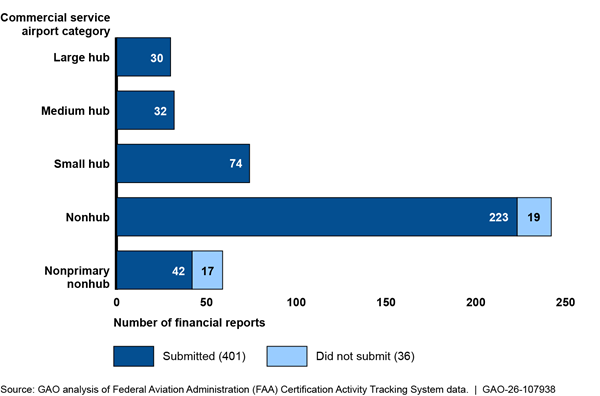

Figure 6: Number of Airport Financial Reports Required to Be Submitted to FAA by Airport Category, Fiscal Year 2021

Note: We used data as of March 31, 2025, for our analysis. While 446 airports were required to submit financial data to the Certification Activity Tracking System, FAA allowed two airport sponsors to consolidate multiple airports into a single submission, resulting in 416 airport submissions. Commercial service airports are classified in statute into five categories based on their annual passenger enplanements, or boardings. See 49 U.S.C § 47102(7), (11), (13), (14), (16), and (25).

Figure 7: Number of Airport Financial Reports Required to Be Submitted to FAA by Airport Category, Fiscal Year 2020

Note: We used data as of March 31, 2025, for our analysis. While 522 airports were required to submit financial data to the Certification Activity Tracking System, FAA allowed two airport sponsors to consolidate multiple airports into a single submission, resulting in 437 airport submissions. Commercial service airports are classified in statute into five categories based on their annual passenger enplanements, or boardings. See 49 U.S.C § 47102(7), (11), (13), (14), (16), and (25).

Figure 8: Number of Airport Financial Reports Required to Be Submitted to FAA by Airport Category, Fiscal Year 2019

Note: We used data as of March 31, 2025, for our analysis. While 519 airports were required to submit financial data to the Certification Activity Tracking System, FAA allowed two airport sponsors to consolidate multiple airports into a single submission, resulting in 442 airport submissions. Commercial service airports are classified in statute into five categories based on their annual passenger enplanements, or boardings. See 49 U.S.C § 47102(7), (11), (13), (14), (16), and (25).

GAO Contact

Derrick Collins at CollinsD@gao.gov

Staff Acknowledgments

In addition to the contact named above, Emily Larson (Assistant Director), Brian Chung (Analyst in Charge), Lynda Downing, Kathleen Drennan, Geoff Hamilton, Zachary Kinger, Rebecca Rogers, Laurel Voloder, Malika Williams, and Elizabeth Wood made key contributions to this report.

The Government Accountability Office, the audit, evaluation, and investigative arm of Congress, exists to support Congress in meeting its constitutional responsibilities and to help improve the performance and accountability of the federal government for the American people. GAO examines the use of public funds; evaluates federal programs and policies; and provides analyses, recommendations, and other assistance to help Congress make informed oversight, policy, and funding decisions. GAO’s commitment to good government is reflected in its core values of accountability, integrity, and reliability.

Obtaining Copies of GAO Reports and Testimony

The fastest and easiest way to obtain copies of GAO documents at no cost is through our website. Each weekday afternoon, GAO posts on its website newly released reports, testimony, and correspondence. You can also subscribe to GAO’s email updates to receive notification of newly posted products.

Order by Phone

The price of each GAO publication reflects GAO’s actual cost of production and distribution and depends on the number of pages in the publication and whether the publication is printed in color or black and white. Pricing and ordering information is posted on GAO’s website, https://www.gao.gov/ordering.htm.

Place orders by calling (202) 512-6000, toll free (866) 801-7077,

or

TDD (202) 512-2537.

Orders may be paid for using American Express, Discover Card, MasterCard, Visa, check, or money order. Call for additional information.

Connect with GAO

Connect with GAO on X,

LinkedIn, Instagram, and YouTube.

Subscribe to our Email Updates. Listen to our Podcasts.

Visit GAO on the web at https://www.gao.gov.

To Report Fraud, Waste, and Abuse in Federal Programs

Contact FraudNet:

Website: https://www.gao.gov/about/what-gao-does/fraudnet

Automated answering system: (800) 424-5454

Media Relations

Sarah Kaczmarek, Managing Director, Media@gao.gov

Congressional Relations

David A. Powner, Acting Managing Director, CongRel@gao.gov

General Inquiries

[1]With respect to airport development, the term “airport sponsor” is defined in statute to mean (1) a public agency that submits to the Secretary under this subchapter an application for financial assistance; and (2) a private owner of a public-use airport that submits to the Secretary under this subchapter an application for financial assistance for the airport. Title 49 U.S.C. § 47175(2) defines the term “airport sponsor” by reference to 49 U.S.C. § 47102(26).

[2]See, 49 U.S.C. § 47107(a)(15), (19).

[3]FAA requires that airports submit financial data within 120 days of the end of the airport’s fiscal year, although airports may request an additional 60-day extension.

[4]Pub. L. No. 118-63, § 734, 138 Stat. 1025, 1274.

[5]The 10 selected airports are: Baltimore/Washington International Thurgood Marshall (BWI), Maryland; Corpus Christi International (CRP), Texas; Devils Lake Regional (DVL), North Dakota; George Bush Intercontinental (IAH), Texas; Gunnison-Crested Butte Regional (GUC), Colorado; Jack McNamara Field (CEC), California; Kansas City International (MCI), Missouri; Oakland San Francisco Bay (OAK), California; Northwest Florida Beaches International (ECP), Florida; and Patrick Leahy Burlington International (BVT), Vermont.

[6]Fiscal year 2023 CATS data were the most recently available data at the time of our review.

[7]FAA 2022 passenger boardings are used to identify the airports required to submit fiscal year 2023 CATS data.

[8]For example, we reviewed Federal Aviation Administration, National Plan of Integrated Airport Systems 2025-2029 (Sept. 30, 2024); Moody’s Investors Service, Airports - U.S.: Airports reach short-term lease agreement extensions with airlines under similar terms (Feb. 3, 2021); and RAND, U.S. Airport Infrastructure Funding and Financing: Issues and Policy Options Pursuant to Section 122 of the 2018 Federal Aviation Administration Reauthorization Act (Santa Monica, CA: 2020).

[9]We conducted searches of various databases, such as Google Scholar, Harvard Think Tank search engine, and Nexis. From these sources, we identified 22 publications that contained the terms “CATS database,” “Certification Activity Tracking System (CATS),” or “FAA CATS.”

[10]We interviewed the following aviation industry stakeholders: five aviation industry associations (Airlines for America, Airport Consultants Council, Airports Council International - North America, American Association of Airport Executives, and National Association of State Aviation Officials); two airport consultants (GRA, Inc. and WJ Advisors LLC); and three bond rating agencies (Moody’s Investors Service, S&P Global, and Fitch Ratings). We also interviewed two researchers (an academic researcher and RAND Corporation).

[11]See, for example, GAO, Airport Infrastructure: Information on Funding and Financing for Planned Projects, GAO‑20‑298 (Washington, D.C.: Feb. 13, 2020).

[12]Airports submit data according to the airport’s fiscal year, which varies by airport, as we describe later in the report.

[13]FAA provided us a download of the CATS data as of March 31, 2025.

[14]As described later in the report, to verify the accuracy of CATS data, we also attempted to reconcile 2023 CATS data with publicly available airport financial statements for a sample of 50 airports. (We selected the airports randomly but ensured they covered the range of airport sizes.) However, we were unable to do so for many airports because the statements did not isolate airport data from other entities; because the information fields differed from those in CATS; or both. Specifically, we were able to locate financial statements that contained airport-specific data for only 11 of the 50 airports.

[15]FAA documents we reviewed included Federal Aviation Administration, Guide for Airport Financial Reports Filed by Airport Sponsors, Advisory Circular 150/5100-19D (June 23, 2011); Airport Compliance Manual, Order 5190.6B Change 3 (Sept. 15, 2023); and Certification Activity Tracking System (CATS) User Guide (March 2011).

[16]Consolidated Appropriations Act, 2001, Pub. L. 106-554, tit. V. § 515, 114 Stat. 2763, 2763A-153 to 2763A-154 (2000). In general, the act requires the Office of Management and Budget to issue guidelines providing policy and procedural guidance to federal agencies for ensuring and maximizing the quality, objectivity, utility, and integrity of information disseminated by federal agencies. In response to the act, the Office of Management and Budget issued Guidelines for Ensuring and Maximizing the Quality, Objectivity, Utility and Integrity of Information Disseminated by Federal Agencies, 67 Fed. Reg. 8452 (Feb. 22, 2002), which, in turn, requires federal agencies to issue their own guidelines to, among other things, ensure and maximize the quality, objectivity, utility, and integrity of information disseminated by the agency. In April 2019, the Office of Management and Budget issued Memorandum M-19-15, Improving Implementation of the Information Quality Act, to reinforce, clarify, and interpret agency responsibilities under the Information Quality Act. Accordingly, DOT updated its Information Dissemination Quality Guidelines in October 2019 (DOT-OST-2019-0135).

[17]Federal Aviation Administration, Data and Information Management Policy, Order 1375.1F (Nov. 4, 2021).

[18]The other four key practices for transparently reporting government data are: provide free and unrestricted data, engage with users, provide data in useful formats, and facilitate data discovery for all users. We did not evaluate FAA’s CATS website against these key practices. GAO, Open Data: Treasury Could Better Align USAspending.gov with Key Practices and Search Requirements, GAO‑19‑72 (Washington, D.C.: Dec. 13, 2018).

[19]GAO, Standards for Internal Control in the Federal Government, GAO‑25‑107721 (Washington, D.C.: May 2025).

[20]Approximately 3,300 airports are identified in FAA’s National Plan of Integrated Airport Systems as part of the national airspace system and are eligible for federal assistance. Federal assistance in the form of project grants by the Secretary of Transportation to maintain a safe and efficient nationwide system of public-use airports that meet the present and future needs of civil aeronautics are authorized at 49 U.S.C. § 47104(a). Applications for such project grants are to, among other things, propose a project only for a public-use airport included in the current National Plan of Integrated Airport Systems. 49 U.S.C. § 47105(b)(2).

[21]49 U.S.C. § 47102. FAA collects passenger boarding data by calendar year in its Air Carrier Activity database.

[22]We used passenger boarding data from 2022 to determine which airports were required to file CATS data in 2023, the most recent year of CATS data available at the time of our review.

[23]Federal Aviation Administration, National Plan of Integrated Airport Systems 2025-2029.

[24]National system airports are eligible to receive federal Airport Improvement Program grant funding for infrastructure development, such as runways, airfield lighting, and navigational aids. The Passenger Facility Charge is a federally authorized user fee paid by passengers at the time of ticket purchase and remitted to the airport where the passenger boards a plane.

[25]GAO‑20‑298. Here, “larger airports” refers to large and medium hubs, and “smaller airports” refers to small hub, nonhub, and nonprimary nonhub airports, as well as reliever airports, general aviation airports, and new airports.

[27]49 U.S.C. § 47107(a)(15), (19). According to FAA, to meet this statutory annual final reporting requirement, FAA created CATS to gather and disseminate such mandated airport financial information.

[28]For example, airports that have 2,500 or more passenger boardings in calendar year 2022 must submit financial information in 2023.

[29]See, for example, 49 U.S.C. § 47133, 14 C.F.R. § 158.13. In addition, airport owners or operators receiving Airport Improvement Program grants must agree to revenue use grant assurance provisions to be approved for such federal grant funding. 49 U.S.C. § 47107(b).

[30]As we have previously reported, federal law allows certain grandfathered airport sponsors to lawfully divert airport revenue to use for nonairport purposes. See 49 U.S.C. § 47107(b)(2), 47133(b) as reported in GAO, Airport Funding: Information on Grandfathered Revenue Diversion and Potential Implications of Repeal, GAO‑20‑684 (Washington, D.C.: Sept. 8, 2020).

[31]Under Office of Management and Budget Single Audit Act regulations, nonfederal entities (such as airports) that spend $1 million or more in federal awards from all sources in a fiscal year must undergo a single audit, which is an audit of an entity’s financial statements and federal awards, or a program-specific audit, for the fiscal year. See 2 C.F.R. § 200.501. Prior to fiscal year 2024, the threshold was $750,000.

[32]Martin State Airport is a general aviation reliever airport. A general aviation airport is defined as a public-use airport that does not have scheduled service or has scheduled service with fewer than 2,500 passenger boardings each year. A reliever airport is designated by the Secretary of Transportation to relieve congestion at a commercial service airport and to provide general aviation access to the overall community. See 49 U.S.C. § 47102(8), (23).

[33]Federal Aviation Administration, Guide for Airport Financial Reports Filed by Airport Sponsors.

[34]The Secretary of Transportation is required by statute to maintain the plan for developing public-use airports in the U.S. and include the kind and estimated cost of eligible airport development necessary to provide a safe, efficient, and integrated system of public-use airports. 49 U.S.C. § 47103. CATS data include approximately 500 commercial service airports, out of approximately 3,300 total NPIAS airports. The remaining NPIAS airports are not required to report financial information to FAA, which makes compiling comprehensive data on the financial performance of all NPIAS airports difficult, according to FAA.

[35]See Federal Aviation Administration, National Plan of Integrated Airport Systems 2025-2029.

[36]Pub. L. No. 116-136, div. B, tit. XII, 134 Stat. 281, 596-97 (2020).

[37]The total allocation to an airport was to be determined by a formula that considered an airport’s passenger boardings for calendar year 2018 (50 percent), the airport sponsor’s debt service (25 percent), and the sponsor’s ratio of unrestricted reserves to debt service (25 percent), both for fiscal year 2018. See, Pub. L. No. 116-136, div. B, tit. XII, 134 Stat. 281, 596-97 (2020).

[38]GAO, COVID-19: Opportunities to Improve Federal Response and Recovery Efforts, GAO‑20‑625 (Washington, D.C.: June 25, 2020); and COVID-19: Federal Efforts Could Be Strengthened by Timely and Concerted Actions, GAO‑20‑701 (Washington, D.C.: Sept. 21, 2020).

[40]The fiscal year 2018 CATS data that FAA used were as of March 14, 2020. FAA officials stated that the specific CATS Form 127 fields used were Lines 13.0 “Unrestricted Cash and investments” and 15.1 “Debt service, excluding coverage.” See appendix I for examples of fields in CATS.

[42]Pub. L. No. 116-260, div. M, tit. IV, 134 Stat. 1909, 1939 (2020). The 31 airports that received CARES Act funds in excess of four times their annual operating expenses were excluded from receiving grants-in-aid for airports made available under the Coronavirus Response and Relief Supplemental Appropriations Act, 2021. Id.