United States Government Accountability Office

Report to Congressional Committees

A report to congressional committees

For more information, contact: Jeff Arkin at arkinj@gao.gov

What GAO Found

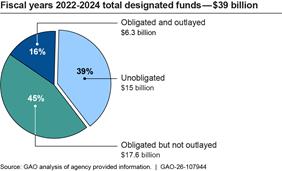

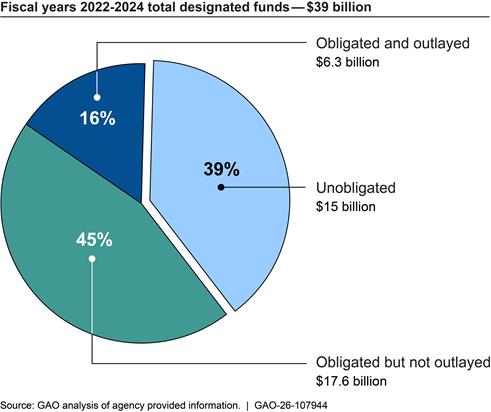

GAO estimates that agencies recorded obligations for around 61 percent of the $39 billion in appropriated funds designated for Community Project Funding/Congressionally Directed Spending (CPF/CDS) projects in fiscal years (FY) 2022, 2023, and 2024, as of the end of FY 2024—the most recently completed fiscal year at the time that GAO started its review. GAO also estimates that around 16 percent of the funds have been outlayed as of the end of FY 2024. See figure below. GAO estimates that around 1 percent of FY 2022–2024 projects are not moving forward, for reasons such as recipients declining funds or not submitting required documentation.

Estimated Amount and Percent Obligated and Outlayed of Fiscal Year 2022-2024 Community Project Funding/Congressionally Directed Spending Funds, as of 9/30/24

Note: For more details, including confidence intervals for the estimates, see figure 4 in GAO-26-107944. Dollar amounts do not sum to the total due to rounding.

GAO estimates that nearly all (between 98 and 100 percent) of the FY 2022 and 2023 projects moving forward had a purpose consistent with the purpose cited in the joint explanatory statement designating the funding and that around two-thirds of these projects were underway or complete. An estimated 60 percent of recipients reported experiencing at least one challenge in implementing their CPF/CDS project, such as managing time frames for completing the project.

The 19 agencies administering CPF/CDS funds conducted various oversight activities based on existing policies and guidance for monitoring federal awards, such as reviewing recipient spend plans, conducting site visits, and monitoring project time frames. Officials from most of the agencies (16 of 19) stated they incorporated lessons learned from oversight of the projects in previous fiscal years to improve the overall CPF/CDS process. Most agencies (16 of 19) reported challenges that affected their ability to conduct oversight activities, such as working with recipients receiving funds for the first time and agency staffing issues.

Why GAO Did This Study

As part of recent congressional appropriations processes, Members of Congress could request that funds be designated to a particular recipient—such as a local government or nonprofit organization in their community—for a specified project. These projects are called CPF in the House of Representatives and CDS in the Senate.

The joint explanatory statements accompanying the appropriations acts designating funds for these projects include provisions for GAO to review a sample of projects as part of Congress’s commitment to increased transparency for CPF/CDS funds.

For this report, GAO used generalizable samples to describe (1) the amount of CPF/CDS funds from FY 2022, 2023, and 2024 annual appropriations that have been obligated and outlayed as of the end of FY 2024, (2) the implementation status of FY 2022 and 2023 projects, and (3) how agencies are overseeing implementation for the FY 2022 and 2023 projects.

GAO reviewed data on obligations and outlays for a generalizable sample of 790 projects from the 19 agencies that administer CPF/CDS funds; interviewed a generalizable sample of 167 project recipients about their use of funds; conducted 36 in-person site visits; reviewed recipient spend plans, audit reports, and other documents from 30 randomly selected projects; and interviewed officials from the 19 agencies regarding oversight activities.

Abbreviations

CDS Congressionally Directed Spending

CPF Community Project Funding

FY fiscal year

JES joint explanatory statement

This is a work of the U.S. government and is not subject to copyright protection in the United States. The published product may be reproduced and distributed in its entirety without further permission from GAO. However, because this work may contain copyrighted images or other material, permission from the copyright holder may be necessary if you wish to reproduce this material separately.

July 16, 2026

Congressional Committees

As part of recent congressional appropriations processes, Members of Congress could request that funds be designated to a particular recipient—such as a local government or nonprofit organization in their community—for a specified project. These projects are called Community Project Funding (CPF) in the House of Representatives and Congressionally Directed Spending (CDS) in the Senate. Since 2022, Congress has designated roughly $39 billion for more than 20,000 projects in annual appropriations acts for a broad range of purposes, including education, health care, and transportation. These projects accounted for approximately 1 percent of discretionary appropriations each year since fiscal year (FY) 2022.[1] Nineteen federal agencies are responsible for administering these funds.[2]

Congress also established requirements to help ensure transparency over this funding. Since 2022, joint explanatory statements (JES) accompanying appropriations acts have included requirements for us to review the implementation of the funds, including how intended recipients have received and spent the funds and the recipients’ expenditures, among other things.[3]

This report uses generalizable samples to describe (1) the amount of CPF/CDS funds from FY 2022, 2023, and 2024 annual appropriations that have been obligated and outlayed as of the end of FY 2024, (2) the implementation status of FY 2022 and 2023 projects, and (3) how agencies are overseeing implementation for the FY 2022 and 2023 projects.[4]

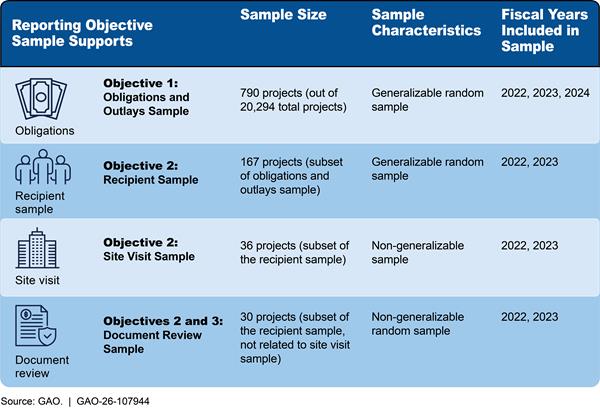

We selected generalizable samples of CPF/CDS projects to determine the amount of funds that have been obligated and outlayed and project implementation status. We also selected non-generalizable samples to provide additional information on project implementation status and agency oversight activities. Figure 1 below summarizes the use of generalizable and non-generalizable samples in this report. Appendix I provides additional details on our scope and methodology.

Figure 1: Summary of Generalizable and Non-generalizable Samples Used to Collect Information on Community Project Funding/Congressionally Directed Spending

To determine the amount of funds that have been obligated and outlayed, we

collected obligations and outlays data from the agency responsible for each of

the 790 projects in our obligations and outlays sample for FYs 2022, 2023, and

2024 as of September 30, 2024. We also interviewed agency officials and

reviewed agency data and documents to obtain information about the funds they

reported as obligated and outlayed as of September 30, 2024. We used the

collected data to make generalizable estimates about the funds for each fiscal

year.

To help assess the reliability of the agency-reported data, all the agencies that submitted data also responded to questions about quality controls in place for collecting their data. We did not compare the obligations and outlays data agencies submitted to us against agency records. Therefore, the obligations and outlay amounts included in this report are reported according to the agencies’ data. We did not evaluate whether each agency’s administration of CPF/CDS funds complied with the legal requirements that generally apply to the obligation and expenditure of appropriated funds.

We found the data reliable for purposes of reporting the status of agency-reported obligations and outlays and estimating total obligations and outlays for FY 2022-2024.

To determine the implementation status of FY 2022 and 2023 projects, we interviewed 167 recipients of FY 2022 and 2023 funds. This sample was a subset of our obligations and outlays sample of 790 projects. We used recipient responses to a structured set of questions to make generalizable estimates for FY 2022 and 2023 projects. For a subset of 36 projects in this sample, we conducted site visits, which included in-person interviews with project recipients. We selected site visits based on a variety of factors, such as the project’s status with respect to agency obligations and outlays as of the end of FY 2023. We also ensured that our site visits were geographically dispersed across the United States.

To further determine how agencies conduct oversight, we also randomly selected a subset of 30 projects from the larger recipient sample, for a document review. We selected at least one project from each of the 19 agencies administering CPF/CDS funds. We obtained supporting documentation (e.g., applications, spend plans, progress reports) to determine whether the reported project purpose is consistent with the description in the appropriations acts or JES that accompany them. We also used this information to corroborate information obtained during recipient interviews. In addition, we reviewed results of audits required by the Single Audit Act for the recipients in our document review sample that were subject to this requirement, including at least one from each of the 19 agencies administering CPF/CDS funds.[5] We also conducted an analysis of the 167 recipients in our recipient sample to determine if any recipients were included in the Department of the Treasury’s Do Not Pay list.[6]

We conducted this performance audit from November 2024 through July 2026 in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

Background

How Congress Designates CPF/CDS Projects

Congress provides budget authority to federal agencies to incur financial obligations through annual appropriations acts or other legislation. As part of the annual appropriations process, Congress can include CPF/CDS provisions either in the appropriations act themselves or in the accompanying JES. These provisions designate a specific recipient or project to receive the funds.

Congress has established rules and requirements for CPF/CDS funds. For example, in FY 2022, the House and Senate limited the funds designated through these provisions to 1 percent or less of total discretionary appropriations. They also placed other limitations on the funds, such as prohibiting members from designating funds directly to for-profit entities. The Senate and House observed similar rules for these requests in FY 2023 and 2024.

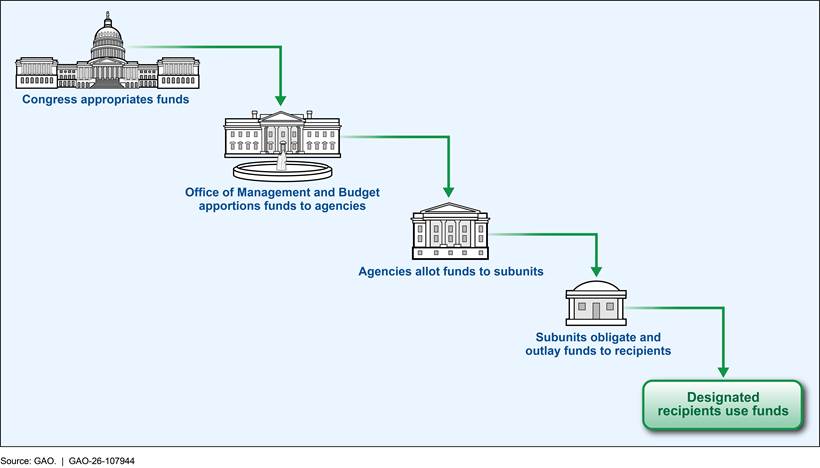

How Funds Flow to Designated Recipients

After Congress appropriates funds, the Office of Management and Budget and agencies take multiple steps before funds become available to recipients. Specifically, after Congress appropriates funds, the Office of Management and Budget apportions, or distributes, the funds to executive branch agencies. Agencies then allot the apportioned funds to program offices or subunits, consistent with the agency’s funds control system. Once the funds have been allotted, the program office or subunit can begin the process of making the funds available to recipients by first obligating the funds and then outlaying them (see fig. 2). In some cases, the designated recipient is a federal agency, such as the U.S. Army Corps of Engineers, which will use the funds to implement the project itself. However, in most cases, recipients are nonfederal entities, such as tribal, state, territorial, or local governments. Funds for nonfederal recipients are often administered through grants.

Figure 2: Community Project Funding/Congressionally Directed Spending Funding Execution: From Congress to Designated Recipient

Note: Some agencies reported providing Community Project Funding/Congressionally Directed Spending funds to a pass-through entity—such as a state agency—to manage the project on behalf of the recipient or pass the funding through to the designated recipient.

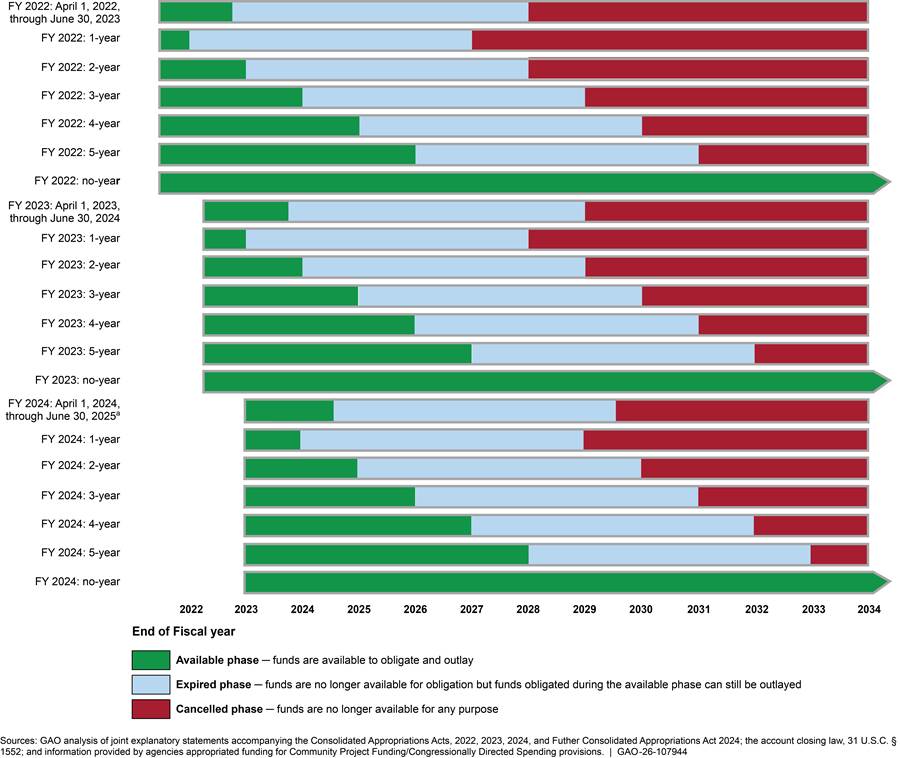

The funds designated through CPF/CDS provisions are part of larger lump-sum appropriations that cover a number of programs, projects, or other items. For each appropriation, Congress specifies the time period during which funds are available for obligation, known as the funds’ period of availability. Agencies may only obligate funds during the period in which they are available.[7] See table 1 for definitions of obligations, outlays, and other key terms in the budget process.[8]

|

Budget Term |

Definition |

|

Appropriation |

Budget authority to incur obligations and to make payments from the Department of Treasury for specified purposes. |

|

Obligation |

Definite commitment that creates a legal liability on the part of the federal government for the payment of goods and services ordered or received, or a legal duty on the part of the United States that could mature into a legal liability by virtue of actions on the part of the other party beyond the control of the United States. Payment may be made immediately or in the future. An agency incurs an obligation, for example, when it places an order, signs a contract, awards a grant, purchases a service, or takes other actions that require the government to make payments to the public or from one government account to another. |

|

Outlay |

An outlay occurs, for example, upon the issuance of checks, disbursement of cash, or electronic transfer of funds made to liquidate a federal obligation. |

|

Period of availability |

When Congress appropriates funds, it specifies the period during which the funds are available to the agency to incur new obligations, referred to as the period of availability. |

Source: GAO‑05‑734SP. | GAO‑26‑107944

About 65 percent of the CPF/CDS funds from FY 2024 annual appropriations were available for agencies to obligate for a fixed period, ranging from 1 to 5 years. Once the period of availability ends, agencies generally have 5 years to outlay the funds. The remaining 35 percent of funds from FY 2024 are not time limited; the funds are available for obligation until expended. These percentages were similar for FYs 2022 and 2023. See figure 3 for a summary of the periods of availability for the FYs 2022-2024 CPF/CDS funds.

Figure 3: Periods of Availability for Fiscal Year (FY) 2022, 2023, and 2024 Community Project Funding/Congressionally Directed Spending Provisions in the Consolidated Appropriations Acts, 2022, 2023 and 2024

Agencies Obligated Over Half of the Designated Funds Between FY 2022-2024

As of the end of FY 2024, we estimate that agencies recorded obligations for about 61 percent of the $39 billion in FY 2022, 2023, and 2024 CPF/CDS funds.[9] We also estimate that about 16 percent of the funds across these 3 years have been outlayed.[10] See figure 4.

Figure 4: Estimated Amount and

Percent Obligated and Outlayed of Fiscal Years 2022-2024 Community Project

Funding/Congressionally Directed Spending, End of Fiscal Year 2024

Figure 4: Estimated Amount and

Percent Obligated and Outlayed of Fiscal Years 2022-2024 Community Project

Funding/Congressionally Directed Spending, End of Fiscal Year 2024

Note: We express our confidence in the precision of the sample’s results as a 95 percent confidence interval. For obligated but not outlayed funds, the 95 percent confidence interval is ($14 billion, $21 billion) or (36 percent, 54 percent). For obligated and outlayed funds, the 95 percent confidence interval is ($5 billion, $8 billion) or (12 percent, 21 percent). For unobligated funds, the 95 percent confidence interval is ($11 billion, $19 billion) or (29 percent, 48 percent). Amounts do not add up to the total dollars due to rounding.

We estimate that the rate of obligations and outlays for funds that had been appropriated in earlier years was slightly higher than the overall rate. Specifically, we estimate that agencies recorded obligations for about 66 percent (or $16 billion) of about $24 billion in funds designated for FYs 2022 and 2023, as of the end of FY 2024.[11] We estimate that agencies outlayed about 23 percent (or $6 billion) of the funds.[12]

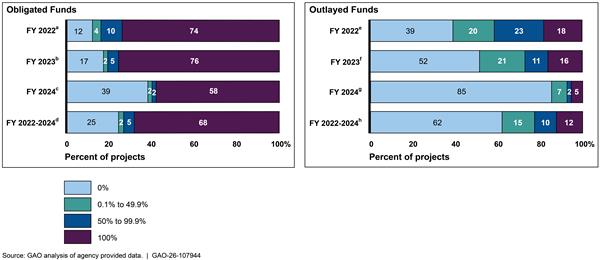

In addition, we analyzed the number of projects from the 20,294 projects from FYs 2022-2024 with funds obligated and outlayed. We estimate that agencies fully obligated the funds for over 70 percent of projects from FY 2022 and 2023 and almost 60 percent from FY 2024, as of the end of FY 2024. We estimate that agencies fully outlayed the funds for almost 20 percent of the projects from FY 2022. See figure 5 for estimates of projects with funds obligated and outlayed by fiscal year.

Figure 5: Distribution of Fiscal Years (FY) 2022-2024 Community Project Funding/Congressionally Directed Spending Projects by Extent of Estimated Funds Obligated or Outlayed, End of FY 2024

Notes: The amounts do not add up to 100 percent because of rounding. We express our confidence in the precision of the sample’s results as a 95 percent confidence interval.

aThe 95 percent confidence intervals are (8, 17), (2, 8), (6, 14), and (68, 79).

bThe 95 percent confidence intervals are (13, 22), (1, 4), (3, 8), and (71, 81).

cThe 95 percent confidence intervals are (33, 45), (0.4, 4), (1, 4), and (52, 64).

dThe 95 percent confidence intervals are (22, 28), (1, 4), (4, 7), and (65, 71).

eThe 95 percent confidence intervals are (33, 45), (15, 24), (18, 28), and (14, 23).

fThe 95 percent confidence intervals are (46, 57), (16, 26), (7, 15), (12, 21).

gThe 95 percent confidence intervals are (80, 89), (4,11), (1, 4), and (3, 9).

hThe 95 percent confidence intervals are (59, 65), (13, 18), (8, 12), and (10, 15).

About $39 billion was designated for FY 2022, 2023, and 2024 projects. We estimate that as of the end of FY 2024, approximately 1 percent of these projects, representing $408 million in designated funds, are not moving forward.[13] Agencies cited a variety of reasons for why projects in our sample were not moving forward as of May 2025, including instances where the recipient declined the funds; could not meet the specific agency requirements for the project; or did not submit required documentation.

When an agency does not move forward with a CPF/CDS project and the period of availability of the funds has not ended, the agency may have authority to reprogram (shift funds within an appropriation account) or transfer (move funds between appropriations accounts) the funds for other authorized purposes.[14] If the funds are not outlayed by the end of the period of availability, the funds expire and may not be used for new obligations, but can be used to record, adjust, and make outlays toward prior obligations that were properly incurred. Generally, appropriated funds remain expired for 5 fiscal years after the period of availability ends. Any remaining funds are cancelled and returned to the general fund of the Treasury at the end of the five-year period.

Two-Thirds of FY 2022 and 2023 Projects Were Underway or Complete, Although Some Recipients Faced Challenges

Two-Thirds of Projects Were at Least in the Planning and Design Phase and Nearly a Third Were Completed

We asked recipients to identify the phase that best describes their projects—not yet begun, planning and design, implementation, or completion.

Among recipients of FY 2022 and 2023 projects that moved forward, we estimate that as of the summer of 2025, 67 percent had taken some action toward implementation—these projects were either in the planning and design or the implementation phase.[15]

Not yet begun. We estimate that about 3 percent of the projects moving forward have not yet begun.[16] For example, we interviewed a recipient of funds for a project to beautify a Tennessee public square and business district. According to the recipient, the project has not started because sewage and water treatment projects needed to be completed first.

Planning and design. We estimate that 30 percent of projects moving forward were in the planning and design stage.[17] For example, representatives of the National Archives and Records Administration’s project on the Modernization of the Carter Presidential Library told us the purpose of the project was to convert the auditoriums into one large auditorium, a smaller classroom, create a hallway, and make these spaces compliant with the Americans with Disabilities Act (see fig. 6).[18] While the agency has obligated and outlayed some of the CPF/CDS funds to help begin the work, project representatives said they had not started construction because project costs were higher than when they requested project funding in 2021.

Implementation. We estimate that 37 percent of projects moving forward

were in the implementation stage.[19]

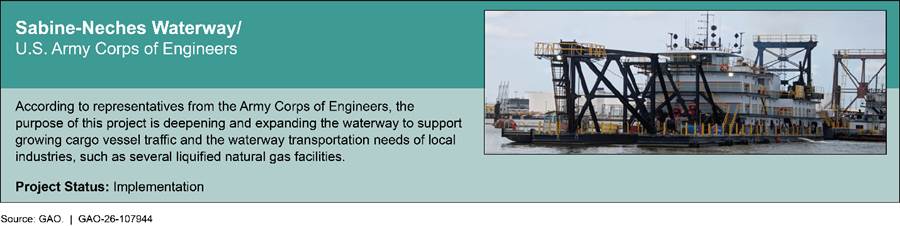

For example, the Sabine-Neches Waterway project in Texas is being led by the

U.S. Army Corp of Engineers. Army Corps of Engineers officials told us the

purpose of the project is to deepen and expand the waterway to support cargo

vessel traffic and the waterway transportation needs of local industries. The

agency has obligated all the CPF/CDS funds, and officials said the project is

in the implementation stage until the contract work for the dredging vessel

begins. See figure 7 below for a photo from the site visit.

Figure 7: Sabine-Neches Waterway Project to Deepen the Waterway for Cargo Vessels and Local Industry

Completion. We estimate 30 percent of projects moving forward were

completed.[20]

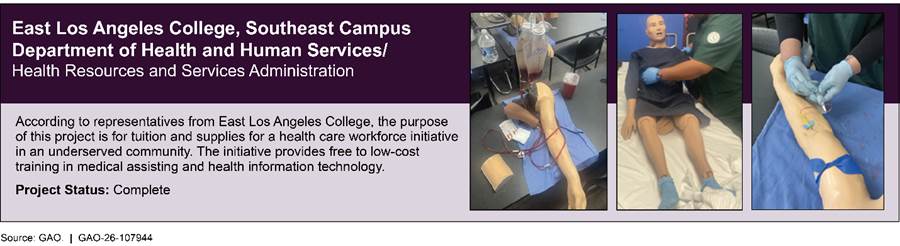

For example, we conducted a site visit with representatives from East Los

Angeles College, Southeast Campus. The recipients stated that the purpose of

their project is to provide tuition and supplies for a health care workforce

initiative in an underserved community. They also noted that this project

provided free or low-cost training in medical assisting and health information

technology. The agency has obligated all the CPF/CDS funds for the project, and

the recipient told us that the project was complete. See figure 8 below for

photos from the site visit.

Note: The left photo is of a prosthetic arm and simulated blood, middle photo is of a student with simulated patient, and right photo is of student practicing a blood draw technique.

Nearly All Projects Had a Purpose Consistent with the Relevant Joint Explanatory Statement

Generally, recipients’ descriptions of projects’ purposes were broadly consistent with the joint explanatory statement (JES) descriptions associated with FY 2022 and 2023 appropriations. We compared the project purposes cited in our interviews with recipients in our sample to the project purposes included in the JES, and we found that all of the projects in our sample that moved forward with funding had a purpose that aligned with its description in the JES.[21] Based on our sample, we estimate that 98 to 100 percent of all FY 2022 and 2023 CPF/CDS projects had a project purpose that aligned with its description in the JES.

Additionally,

we requested CPF/CDS project documentation from 19 agencies for 30 projects in

our sample. Agencies sent us documentation for 28 projects, and we found the

documentation generally matched the purpose listed in the JES. We did not

receive documentation for two Department of Housing and Urban Development

projects. According to the Department of Housing and Urban Development, the two

recipients’ projects were early in the process, and the recipients had not

submitted the documentation to the agency during the period we requested it.

Additionally,

we requested CPF/CDS project documentation from 19 agencies for 30 projects in

our sample. Agencies sent us documentation for 28 projects, and we found the

documentation generally matched the purpose listed in the JES. We did not

receive documentation for two Department of Housing and Urban Development

projects. According to the Department of Housing and Urban Development, the two

recipients’ projects were early in the process, and the recipients had not

submitted the documentation to the agency during the period we requested it.

Almost All Projects Had a Plan to Spend the Funds

We estimate that as of the summer of 2025, 94 percent of the FY 2022 and 2023 projects moving forward had a documented plan to spend the funds, such as a project narrative and budget.[22] For the subset of nonfederal recipients that had a documented plan, we estimate that 94 percent were asked to provide this plan to the agencies that are administering the funds.[23] For example, a project recipient we interviewed said they had to submit a plan for a statewide STEM ecosystem network to the agency that included a budget, a budget narrative, project timelines, goals, objectives, performance measures, and identification of key personnel to develop a statewide education network in Minnesota.

Some recipients from our sample have not submitted a documented plan to spend the funds. They said that they were either in the process of completing a documented plan to spend the funds or they had not completed all the processes needed to receive the funds. For example, one recipient said that they were expected to spend the funds on medical equipment, and they were working to identify the specific equipment and associated costs.

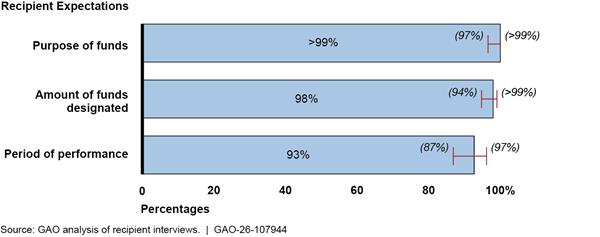

The Amount of Funds Received and Period of Performance Mostly Met Recipients’ Expectations with Their Projects

We found that the FY 2022 and 2023 CPF/CDS funds were generally made available to designated recipients in an amount, for a purpose, and for a period of performance consistent with their expectations, as of the summer of 2025.[24] See figure 9.

Figure 9: Estimated

Percentages of Fiscal Year 2022 and 2023 Community Project

Funding/Congressionally Directed Spending Recipients for Which the Designated

Funds Met Recipients’ Expectations, as of Summer 2025

Figure 9: Estimated

Percentages of Fiscal Year 2022 and 2023 Community Project

Funding/Congressionally Directed Spending Recipients for Which the Designated

Funds Met Recipients’ Expectations, as of Summer 2025

Note: We express our confidence in the precision of the sample’s results as a 95 percent confidence interval. We show the confidence interval for each recipient expectation response. The amount of funds designated is generalizable to all projects. The other estimates in this figure are generalizable to the projects moving forward. We interviewed project recipients in the summer of 2025.

Purpose of funds. We estimate almost all recipients (more than 99 percent) with projects moving forward have a project purpose that aligns with their expectations.[25] Only one recipient in our sample reported that the project purpose did not align with their expectations. This is because the recipient did not realize that their project to improve statewide regional emergency communications systems required adherence to National Environmental Policy Act requirements.[26] According to the recipient, meeting these requirements resulted in additional work and resources for which they had not planned.

Amount of funds designated. We estimate that almost all recipients (98 percent) were designated an amount of funds that aligned with their expectations.[27] In rare instances, recipients that we interviewed said that the amount of funds did not align with their expectations. For example, prior to receiving CPF/CDS funds, one recipient determined that $900,000 would be needed to complete the project. Once the CPF/CDS project was awarded, the designated amount for the project was less than the amount the recipient determined they needed for the project. Eventually the project recipient withdrew the project and did not accept any of the funding.

Period of performance. We estimate that 93 percent of the projects moving forward for FY 2022 and 2023 had a period of performance that met recipient’s expectations for project completion.[28] One recipient said that the period of performance for completing a cybersecurity education center at a university did not meet their expectations. The recipient said that the funds were provided later than expected, but the completion date was not changed. According to the recipient, the period of performance was effectively 6 months shorter than what they had expected, and the agency did not respond to the recipient’s request for an extension. As a result, the recipient was unable to complete all the project objectives and use all the designated funding.

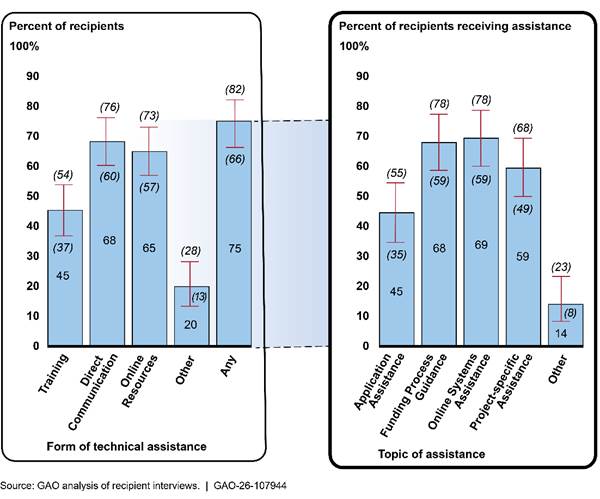

Most Recipients Received Technical Assistance from Agencies

For projects moving forward, we estimate that 75 percent of nonfederal recipients had received technical assistance from the agency providing the funds, as of the summer of 2025.[29] Technical assistance refers to programs, activities, and services provided by federal agencies to strengthen the capacity of grant recipients and to improve their performance of grant functions.[30] See figure 10.

Figure 10: Estimated Percentages of Agency Technical Assistance Provided to Nonfederal Recipients for Fiscal Year (FY) 2022 and 2023 Community Project Funding/Congressionally Directed Spending Projects, as of Summer 2025

Note: We express our confidence in the precision of the sample’s results as a 95 percent confidence interval. We show the confidence interval for each technical assistance type. Estimated percentages are generalizable to FY 2022-2023 projects moving forward. We conducted interviews with recipients in the summer of 2025.

We asked all of the recipients with projects moving forward to identify additional technical assistance that would have helped them. Recipients told us that the following examples of additional technical assistance could be helpful:

· additional direct communication while preparing initial grant applications and submitting required paperwork;

· additional training, such as a refresher for recipients who have not worked on CPF/CDS projects recently;

· uploading documents into agencies’ systems;

· on-demand training for recipients who missed agency webinars; and

· documentation checklists to help ensure all steps of the process are followed.

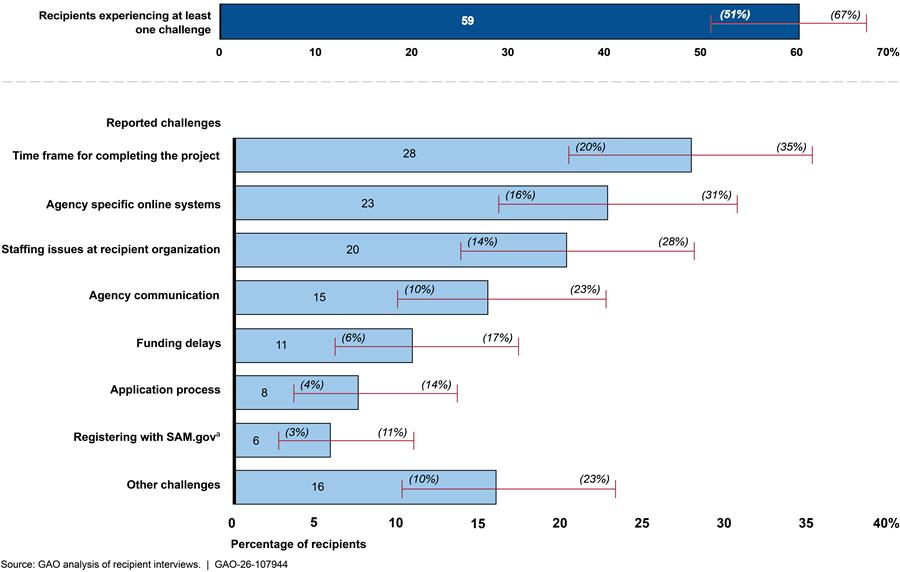

Over Half of Recipients Experienced at Least One Challenge

We

estimate that 59 percent of the recipients with projects moving forward

experienced one or more challenges during the year preceding our recipient

interviews.[31]

Examples of challenges were (1) time frames for completing the project, (2)

agencies’ online systems, (3) staffing issues at recipient organizations, and

(4) communications.[32]

See figure 11 for a summary of the challenges recipients experienced.

We

estimate that 59 percent of the recipients with projects moving forward

experienced one or more challenges during the year preceding our recipient

interviews.[31]

Examples of challenges were (1) time frames for completing the project, (2)

agencies’ online systems, (3) staffing issues at recipient organizations, and

(4) communications.[32]

See figure 11 for a summary of the challenges recipients experienced.

Figure 11: Estimated Percentages of Recipients Who Experienced Challenges with Fiscal Year 2022 and 2023 Community Project Funding/Congressionally Directed Spending Projects

Notes: Estimated percentages are generalizable to FY 2022-2023 projects moving forward. We conducted these interviews in the summer of 2025. We asked the recipients about challenges they had experienced in the prior year. We express our confidence in the precision of the sample’s results as a 95 percent confidence interval. We show the confidence interval for each reported challenge.

aSAM.gov is the System for Award Management and is administered by the General Services Administration.

Time frame for completing the project. Recipients reported experiencing challenges with managing project time frames because of specific project requirements, the agency process for completing projects, and other issues. For example, a recipient said they had to extend the time frame for a solar panel installation project because they had not understood requirements for products under the Build America, Buy America Act, and the requirements were not made clear to them by the agency. These requirements required extra resources to use products and equipment that comply with the act, which resulted in delays to the initial time frame of the project.[33]

Agency-specific online systems. Recipients reported challenges with agency payment systems or grant management systems used to upload documentation, communicate with agencies, and register for grant payments. For example, some recipients said online systems such as agency payment systems were hard to navigate and required recipients to complete the same information in more than one online system.

Staffing issues at recipient organizations. Recipients reported staffing challenges within their organizations. Some recipients said that staff previously responsible for their projects left their organizations, which left a gap in the organizations’ staffing. One recipient said staffing issues at their organization can lead to delays in the projects or may result in the recipient not using all the funding. For example, the recipient said they would not use all the designated project funding because it was challenging to hire and keep employees to manage the project.

Agency communication. Recipients identified challenges with identifying a point of contact for agency staff, lack of support on the status of project funds, and insufficient communication on how recipients may use the funds. For example, a recipient said it would have been helpful to have an agency point of contact at the beginning of the project because requirements for CPF/CDS projects were not the same as other projects. Another recipient told us that the agency did not communicate on the status or timing of project funding, which almost caused a stop in construction of the CPF/CDS project.

Agencies Oversaw Projects Based Largely on Existing Policies and Guidance for Monitoring Federal Awards

The 19 agencies that oversee the FY 2022 and 2023 CPF/CDS projects reported various oversight activities that they conduct to help ensure the projects are moving forward as intended. These oversight activities include reviewing recipients’ plans, reviewing periodic and final reports, conducting site visits, and monitoring project time frames, among other actions. Table 2 summarizes how many of the 19 agencies that oversee CPF/CDS projects reported conducting oversight activities. The U.S. Army Corps of Engineers and General Services Administration were the direct recipients of CPF/CDS funds in our sample of 167 projects, so certain oversight activities were not applicable to them (e.g., providing technical assistance and conducting risk assessments).

Table 2: Agency Oversight Activities for Fiscal Year 2022 and 2023 Community Project Funding/Congressionally Directed Spending Projects

|

Oversight activity |

Number of agencies that reported performing oversight activity |

|

Apply existing policies and guidance |

19 |

|

Conduct risk assessments |

19 |

|

Ensure project purpose aligns with the joint explanatory statement |

18a |

|

Review key documentation (applications, spend plans, performance reports, financial reports) |

17b |

|

Provide technical assistance to recipients |

17b |

|

Incorporate lessons learned |

16 |

|

Monitor project time frames |

15 |

Source: GAO analysis of information obtained during interviews with agency officials. | GAO‑26‑107944

Note: Nineteen federal agencies are responsible for administering the community project funding/congressionally directed spending (CPF/CDS) funds.

aThe Department of Housing and Urban Development did not respond to our request for an interview to discuss this topic.

bThe U.S. Army Corps of Engineers and General Services Administration were direct recipients of CPF/CDS, so these oversight activities were not applicable to them.

Agencies provided information on specific actions they have taken for the 167 projects in our recipient sample at the time of our review, which we used to make generalizable estimates for all FY 2022 and 2023 projects where applicable. The following are examples of these oversight activities.

Apply Existing Policies and Guidance

Officials from all agencies that oversee CPF/CDS projects (19 of 19) stated they follow standard policies and guidance consistent with their other grant and award programs. These include adhering to the Office of Management and Budget’s Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards—commonly referred to as the Uniform Guidance—as well as other relevant guidance to determine project documentation requirements.[34] Some agencies also have created guidance tailored specifically to CPF/CDS projects. The Office of National Drug Control Policy, for example, developed standard operating procedures specifically for CPF/CDS projects based on federal laws, regulations, and internal requirements.

Conduct Risk Assessments

All 19 agencies identified risk assessment activities they conduct before obligating funds to project recipients, such as reviewing financial audits, including single audits, or checking that recipients do not appear on the Department of the Treasury’s Do Not Pay list. For example, we estimate that agency officials had reviewed financial audits for 42 percent of the FY 2022-2023 projects, as of the spring of 2025.[35] Agency officials told us that they review single audits or other financial audits, as applicable, to determine that recipients can manage funds throughout the course of the project.[36] Some agencies, such as the Department of Housing and Urban Development and the Office of National Drug Control Policy, did not request to review independent financial audits of grant recipients because they use their own processes to assess recipient financial risk. Agencies also use audit results to identify potential risks and determine what financial controls they need to provide oversight and support to recipients.

Based on information provided by the agencies on the 167 projects in our recipient sample, we estimate that 47 percent of the FY 2022 and 2023 projects did not have a financial statement audit or single audit review by the agency because the requirement was not applicable.[37]

We conducted an independent analysis of selected recipients’ single audit reports as described in the text box below.

|

Single Audit Act Compliance Of the 30 community project funding/congressionally directed spending (CPF/CDS) projects we reviewed, the responsible entities filed reports for 19 projects in FY 2022 or 2023 as required by the Single Audit Act. The recipients for remaining projects were either federal agencies or were not subject to the Single Audit Act requirement given the dollar amount of the recipients’ expenditure of federal awards. We found that the entities for 18 out of the 19 CPF/CDS projects had an unmodified (“clean”) or qualified opinion.a Only one entity had an adverse financial opinion, the highest risk category. However, we determined that the risks were not related to work with the federal agency providing CPF/CDS funds. |

Source: GAO analysis of audit documentation | GAO‑26‑107944

aA qualified opinion arises when the auditor is able to express an opinion on the financial statements except for specific areas where the auditor was unable to obtain sufficient appropriate evidence, and the auditor concludes that the possible effects on the financial statements of undetected misstatements, if any, could be material but not pervasive. GAO, Financial Audit: FY 2025 and FY 2024 Consolidated Financial Statements of the U.S. Government, GAO- 26-108073 (Washington, D.C.: Mar. 19, 2026).

Another risk assessment activity included verifying that recipients did not appear on the Department of the Treasury’s Do Not Pay list.[38] We estimate that agencies confirmed that recipients were not on the Do Not Pay List for 83 percent of all FY 2022 and 2023 CPF/CDS projects, as of April 2026.[39] Agencies did not use the Do Not Pay list for particular projects because the recipient was a federal agency or the agency used alternative tools to assess eligibility for federal fund receipt, such as SAM.gov’s Exclusions and Responsibility Qualification records. We estimate that agencies required a unique entity identifier for 92 percent of FY 2022 and 2023 projects.[40] We used the unique entity identifier to conduct an independent analysis of our recipient sample to determine if any recipients were included in the Do Not Pay database, as described in the text box below.

|

Do Not Pay List and Unique Entity Identifier Enrollment Of the 167 projects in our recipient sample, 14 did not have a unique entity identifier that was listed within SAM Entity Registration records. Of the 14 results, six were federal projects that either did not have a unique entity identifier or had a likely invalid unique entity identifier. Of the 14 results, eight were nonfederal projects that had a unique entity identifier that the Do Not Pay system could not find in the SAM.gov registration. Using the unique entity identifier, we verified that agencies correctly determined recipients were not on the Do Not Pay list. We found that none of recipients in our sample with a unique entity identifier had a result indicating that they were debarred, excluded, or suspended from U.S. Treasury payments in the Do Not Pay System. We conducted this analysis as of April 17, 2026. |

Source: GAO analysis of Do Not Pay information against the recipient sample. | GAO‑26‑107944

All 19 agencies stated that they had not encountered any instances of improper payments or mismanaged funds related to the FY 2022 and 2023 CPF/CDS projects. The Department of the Interior told us that sometimes recipients draw down funding too early when they do not understand that they need to wait to be reimbursed.[41] This issue is typically identified early, and recipients can return the funds. The agency shared that this situation occurs less frequently as recipients learn about federal requirements and become more experienced with receiving federal grants.

Ensure Project Purpose Aligns with the Joint Explanatory Statement

Eighteen out of the 19 agencies stated they ensure the project purpose aligns with the JES.[42] Agency officials stated that they compare the purpose as described in the recipient’s application to the JES. The agencies work with recipients to address any scope issues that could arise during the CPF/CDS process. Some agencies, such as some components of the Department of Transportation, work with recipients to revise their scope if a project’s purpose is not consistent with the JES. Agencies also incorporate checks related to project purpose during different phases of the CPF/CDS process. The National Aeronautics and Space Administration designates officials to conduct two phases of review: (1) examining grants during the pre-award phase to guarantee alignment with the agency’s mission and the project’s purpose, and (2) examining spend plans during the implementation phase to ensure funds are spent in line with the designated purpose.

Review Key Documentation

Officials from all agencies that oversee nonfederal CPF/CDS recipients (17 of 17) stated they require recipients to submit key documentation, such as grant applications, spend plans, performance reports, and financial reports.[43] Agencies review pre-award documents, such as applications and spend plans, prior to the recipient receiving the funds. We estimate that 69 percent of recipients submitted an application for agencies to review prior to the award for FY 2022 and 2023 projects.[44] Agencies did not require applications for projects they managed themselves.[45] Five recipients in our sample declined their CPF/CDS grant, so the agencies ultimately did not need an application from them.

All agencies reported that they require nonfederal recipients to submit documented spend plans before spending CPF/CDS funds. Agencies review these plans to ensure that proposed costs are allowable and that recipients spend funds as outlined in the plans. We estimate that at the time of our review, agencies verified recipient funds were spent in accordance with their plans for 58 percent of FY 2022-2023 projects.[46] Agencies provided reasons why they did not take this confirmation step in some cases. For example, this step was not applicable for recipients who were still in the application or planning and design phase and for projects that were not moving forward.

Officials from all 17 agencies that oversee nonfederal recipients require and review oversight documentation after the grant is awarded including periodic progress reports, final reports, and financial reports. The agencies use these reports to monitor project progress and ensure that recipients spend funds properly. As part of our review, we requested progress reports and financial reports for a sample of 30 projects and confirmed that agencies obtained progress and financial reports for 25 out of the 30 projects. Agencies did not have progress reports for five projects that were not far enough along in the process at the time that we requested them.

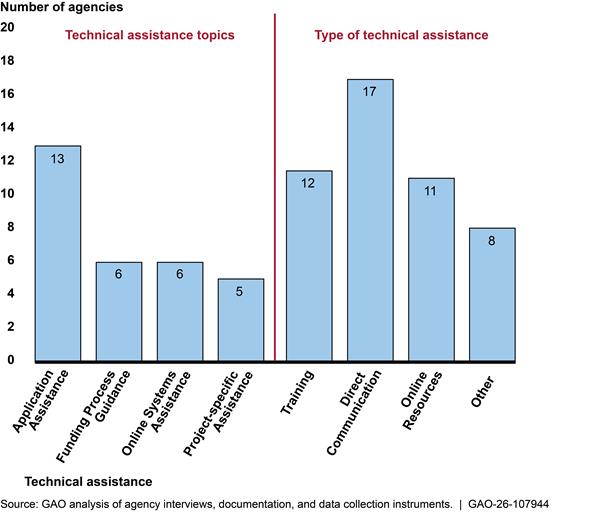

Provide Technical Assistance to Recipients

All agencies overseeing nonfederal FY 2022 and 2023 CPF/CDS projects (17 of 17) reported offering technical assistance to recipients in our sample.[47] Technical assistance refers to programs, activities, and services provided by federal agencies to strengthen the capacity of grant recipients and improve their performance of grant functions. It could include application assistance, meetings with recipients, online resources, or training. See figure 12 for examples of technical assistance the agencies reported providing to CPF/CDS recipients.

Figure 12: Types and Topics of Technical Assistance Agencies Reported Providing to Fiscal Year 2022 and 2023 Community Project Funding/Congressionally Directed Spending Project Recipients

Direct communication with designated recipients was the most common form of

technical assistance agencies provided. Direct communication included emails,

meetings, and phone conversations.

Agencies shared examples of the training opportunities and online resources they have provided to recipients. For example, the Federal Emergency Management Agency shared that it maintains websites with guidance and technical forms for nonfederal recipients. In addition, the Federal Emergency Management Agency has a grants manual for recipients to use. The Federal Emergency Management Agency also shared that each of its grants has a separate website domain and notice of funding opportunity detailing project requirements. The agency also told us that its staff update guidance on the website for each grant. To provide support at a more localized level, officials told us that it offers a regional financial audit liaison for recipients to consult with and ask questions.

According to officials from several agencies, recipients with no prior experience receiving federal funds require frequent communication and technical assistance. The Department of Labor and the Environmental Protection Agency, for example, shared that they offer tailored, individualized support based on recipient needs. The Office of National Drug Control Policy provides additional explanations of project requirements to new grant recipients that have not previously applied for and received federal funds. Also, staff request regular status updates, remind recipients of deadlines, and provide individual technical assistance.

Incorporate Lessons Learned

Officials from most of the agencies (16 of 19) stated they incorporated lessons learned from oversight of the projects in previous fiscal years to improve the overall CPF/CDS process for recipients and agency officials.[48] The following examples show how agencies applied lessons learned to oversight activities:

Improving technical assistance. The Department of Commerce published a webpage based on frequently asked questions from previous years. The Department of Commerce also ensured recipients were aware of the nuances of certain laws such as the Historical Preservation Act and the National Environmental Policy Act.

Improving the award process. The Department of the Interior holds internal meetings to discuss issues that have previously occurred in the CPF/CDS awards process and train staff accordingly. Staff are then equipped to anticipate issues before they arise and address them in a timely manner.

Improving databases and software systems. Office of National Drug Control Policy officials stated that the agency started using a grants software system in FY 2023 that helped staff better manage grant documentation and communicate requirements and deadlines to recipients.

Staffing adjustments. The Department of Labor has assigned a federal project officer for each individual recipient, and the Environmental Protection Agency has used contractors to enhance oversight capacities.

Monitor Project Time Frames

Officials from 15 of the 19 agencies reported that they monitored CPF/CDS project time frames as part of their standard oversight activities. This included reminding recipients of deadlines, comparing project progress to established plans, or checking in directly to ask recipients about adherence to project timelines. Agencies that did not complete this activity as part of their standard oversight process either delegated time frame monitoring to funding recipients or chose to focus on other project metrics. In the case of the Federal Emergency Management Agency, for example, recipients oversee the project while subrecipients carry out major project functions. The recipient is the one that performs time frame monitoring on a regular basis.

Agencies’ Oversight Challenges Involved Recipient Issues and Agency Resource Constraints

Most agencies (16 of 19) reported challenges that affected their ability to conduct oversight activities, such as working with recipients and agency staffing issues.

Recipient issues. Officials from 8 of the 19 agencies stated that they have had issues overseeing non-responsive grantees, grantees that are receiving federal funds for the first time, and organizations with high staff turnover. For example, Department of Labor officials stated that high turnover at recipient organizations created challenges because agency officials had to spend a significant amount of time re-explaining project requirements to the recipients’ new staff throughout the period of performance.

Agency resource constraints. Officials from most agencies (12 of 19) stated that they faced resource constraints, such as staffing and funding issues. First, officials from about half of the agencies (8 of 19) stated that federal staffing reductions have affected their oversight capacity. For example, according to Department of Energy officials, a number of staff resigned during the past year, and workload increased for remaining staff. As a result, officials stated they have increased written correspondence with recipients, in lieu of meetings. Second, officials from some agencies (4 of 19) stated that recent funding levels have affected their ability to conduct oversight activities, such as in-person site visits. As a result, agencies have switched to virtual site visits to continue these oversight activities.

Agency Comments

We provided a draft of this report to the 19 agencies that administered CPF/CDS funds for FYs 2022, 2023, and 2024 for review and comment. The Department of Energy, the Department of Housing and Urban Development, the Environmental Protection Agency, and the Office of National Drug Control Policy provided technical comments, which we incorporated as appropriate. The remaining 15 agencies did not have any comments.

We are sending copies of this report to the appropriate congressional committees, the 19 agencies that administered CPF/CDS funds, and other interested parties. In addition, the report is available at no charge on the GAO website at https://www.gao.gov. If you or your staff have any questions about this report, please contact me at arkinj@gao.gov. Contact points for our Offices of Congressional Relations and Media Relations may be found on the last page of this report. GAO staff who made key contributions to this report are listed in appendix II.

Jeff Arkin

Director, Strategic Issues

List of Committees

The Honorable Susan Collins

Chair

The Honorable Patty Murray

Vice Chair

Committee on Appropriations

United States Senate

The Honorable Bill Hagerty

Chair

The Honorable Jack Reed

Ranking Member

Subcommittee on Financial Services and General Government

Committee on Appropriations

United States Senate

The Honorable Deb Fischer

Chair

The Honorable Martin Heinrich

Ranking Member

Subcommittee on Legislative Branch

Committee on Appropriations

United States Senate

The Honorable Tom Cole

Chairman

The Honorable Rosa DeLauro

Ranking Member

Committee on Appropriations

House of Representatives

The Honorable Dave Joyce

Chairman

The Honorable Steny Hoyer

Ranking Member

Subcommittee on Financial Services and General Government

Committee on Appropriations

House of Representatives

The Honorable David Valadao

Chairman

The Honorable Adriano Espaillat

Ranking Member

Subcommittee on Legislative Branch

Committee on Appropriations

House of Representatives

This report uses generalizable samples to describe (1) the amount of Community Project Funding/Congressionally Directed Spending (CPF/CDS) funds from fiscal years (FY) 2022, 2023, and 2024 annual appropriations that have been obligated and outlayed as of the end of FY 2024, (2) the implementation status of FY 2022 and 2023 projects, and (3) how agencies are overseeing implementation for the FY 2022 and 2023 projects.[49] We express our confidence in the precision of these results as a 95 percent confidence interval. This is the interval that would contain the actual population value for 95 percent of the samples that could have been drawn.

To determine the amount of FY 2022, 2023, and 2024 funds that have been obligated and outlayed as of the end of FY 2024, we drew a generalizable, stratified random sample of projects (790 out of the population of 20,294 projects). To select the sample, we included the highest-dollar FY 2023 project from each of the 19 agencies responsible for administering these funds, then stratified the remaining projects by year of appropriation for FY 2022, 2023, and 2024.[50] The obligations and outlays sample projects account for about $2.4 billion of the $39 billion total appropriation for CPF/CDS (or roughly 6 percent).

To calculate generalizable estimates for the total dollar values of obligations and outlays for FYs 2022–2024 and 2022–2023, we estimated the ratios of obligations and outlays to the total amounts designated during the periods, then multiplied those ratios by the designated amount to obtain dollar value estimates.[51] We used an expansion estimator to obtain the dollar value estimate.[52]

We created agency-specific spreadsheets to collect obligations and outlays data for each project in our sample for FY 2022-2024 as of the end of FY 2024. We interviewed agency officials at each of the 19 agencies and reviewed agency data and documents to obtain information about the funds they reported as obligated and outlayed as of September 30, 2024.

We performed logic checks on reasonability of agency-reported data. For example, we verified that the agency-reported obligations did not exceed appropriated amounts for each project. There were projects for two agencies where obligations exceeded appropriated amounts. We determined the reasons for these inconsistencies and resolved the issues.[53] The obligations and outlays data we include in this report are reported according to the agencies. We did not compare the obligations and outlay data agencies submitted to us against agency records. We did not evaluate whether each agency’s administration of CPF/CDS funds complied with the legal requirements that generally apply to the obligation and expenditure of appropriated funds.

To help assess the reliability of the agencies’ data, we included standardized questions to help assess data quality in a spreadsheet. We verified that all the agencies that submitted data to us also responded to the data quality questions. We did not receive answers to these questions from the Department of Housing and Urban Development. We used responses the agency provided as part of our prior work.[54] We also used agency financial reports to review each agency’s financial statement opinion; internal controls; and compliance with Federal Financial Management Improvement Act of 1996 requirements.[55] We found the data reliable for purposes of reporting the status of agency-reported obligations and outlays and estimating total obligations and outlays for FY 2022-2024.

To determine the implementation status of FY 2022 and 2023 projects, we drew a generalizable, stratified random sample of projects across the 19 agencies for FYs 2022 and 2023 (167 out of a population of 12,196 projects). This is a subsample of the larger sample described for objective 1. We oversampled projects receiving funds with a shorter period of availability and excluded FY 2024 projects, because we wanted to select projects that were more likely to have started.[56] We also included a certainty stratum with the highest-dollar FY 2023 project from each of the 19 agencies administering CPF/CDS funds. The recipient sample projects account for about $1.2 billion of the $24 billion in total CPF/CDS appropriations for FY 2022 and 2023 (or roughly 5 percent).

We conducted structured interviews with 167 recipients in the sample to obtain information on their experience obtaining funds and implementing projects. We modified an interview protocol that was developed for our prior work examining a sample of the FY 2022 projects.[57] The interviews consisted of both closed- and open-ended questions, covering such topics as project purpose, challenges experienced with receiving funds, and the status of efforts to spend funds. We used a structured interview approach to ensure uniformity in the interview experience across projects. We used the responses from interview questions to make generalizable estimates for all FY 2022 and 2023 projects.

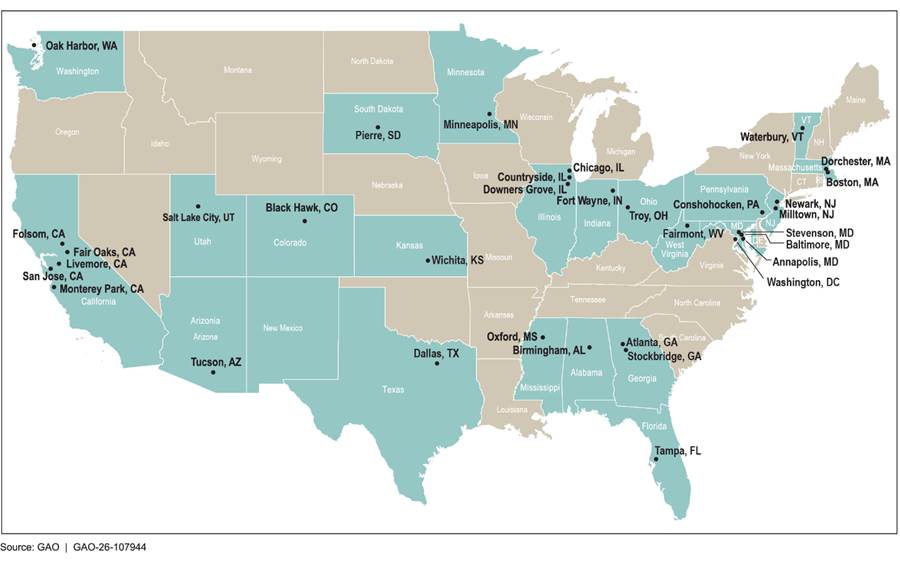

For 36 of the 167 projects in the sample, we conducted in-person interviews and site visits. The remaining recipient interviews were conducted virtually. We selected the 36 recipients for in-person interviews by considering factors such as variety in geographic location, the number of agencies represented, and whether recipients’ funds had been obligated or outlayed as of the end of FY 2023. Our selection process was designed to increase the likelihood that we would be able to observe in person progress on projects. These in-person interviews were conducted by GAO staff who work in relatively close proximity to project locations, minimizing the need for additional resources to travel to the locations. Figure 13 illustrates the locations of our in-person site visits.

Figure 13: Locations of the In-Person Site Visits for the Selected Community Project Funding/Congressionally Directed Spending Projects

Note: We conducted two site visits in Baltimore, Maryland and two site visits in Birmingham, Alabama.

We conducted additional verification and checks for the 167 projects in our sample. We verified that recipients were not identified on the Department of the Treasury’s Do Not Pay list to confirm that the recipients were eligible to receive payments.[58] We collected participant names from the joint explanatory statement (JES), unique entity identifier from structured recipient interviews, and USAspending.gov Award IDs from spreadsheets completed by overseeing agencies. We took steps to match this information to USAspending.gov data from October 2024 through July 2025 and SAM.gov registration data from December 2025 to augment and correct the recipients’ names and identifiers. We ran the data through the Do Not Pay System to look for exclusionary results. The Do Not Pay exclusionary datasets are System for Awards Management exclusions and the Office of Foreign Asset control sanction list.

Using the information we collected through our interviews, we also compared how recipients in our sample described their stated project purpose with the project or recipient description in the FY 2022 and 2023 JES to ensure the purpose was consistent with the law.[59]

To describe agency oversight activities, we conducted interviews with all 19 agencies administering CPF/CDS funds. We covered topics such as oversight guidance, lessons learned, use of spend plans, and technical assistance provided to recipients. We conducted a content analysis of responses provided by agency officials and recipients. We reviewed these responses to categorize (1) technical assistance that agencies provided and recipients used prior to receiving funds, and (2) challenges that agencies experienced related to the CPF/CDS funding process. We also requested data from the agencies on oversight activities for each project in our recipient sample using a spreadsheet.

To determine the implementation status of these projects and how agencies are overseeing these projects, we also selected a subset of 30 projects from the larger recipient sample for a document review, including at least one from each of the 19 agencies. We reviewed relevant agency and recipient documents, including guidance, grant applications, spending plan templates, and progress reports to determine whether agencies are following processes discussed during interviews and collected through our data collection instruments. This document review was also used to corroborate information provided by recipients, such as the purpose of the project and whether the recipient has submitted a plan to spend the funds. We also reviewed results of audits required by the Single Audit Act for the recipients in our document review sample who were subject to this requirement.[60] The act requires an independent audit of financial statements and compliance with federal grant requirements, with reports submitted within 30 days of receipt or 9 months after the end of the period audited.

We conducted this performance audit from November 2024 through July 2026 in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

GAO Contact

Jeff Arkin, Arkinj@gao.gov

Staff Acknowledgements

In addition to the contact named above, Thomas McCabe (Assistant Director), Janice Latimer (Assistant Director), Gina Flacco (Analyst in Charge), Britt Bovbjerg, Mariana Calderon, Justine D’Souza, Holly Firlein, Joseph Fread, Gina Hoover, Krista Loose, Fritz Manzano, Gabe Nelson, Tara Porter, Paula Rascona, Jason Rodriguez, Nina Rostro, Jared Smith, Cree Townsend, Walter Vance, and John Villecco made key contributions to this report.

GAO’s Mission

The Government Accountability Office, the audit, evaluation, and investigative arm of Congress, exists to support Congress in meeting its constitutional responsibilities and to help improve the performance and accountability of the federal government for the American people. GAO examines the use of public funds; evaluates federal programs and policies; and provides analyses, recommendations, and other assistance to help Congress make informed oversight, policy, and funding decisions. GAO’s commitment to good government is reflected in its core values of accountability, integrity, and reliability.

Obtaining Copies of GAO Reports and Testimony

The fastest and easiest way to obtain copies of GAO documents at no cost is through our website. Each weekday afternoon, GAO posts on its website newly released reports, testimony, and correspondence. You can also subscribe to GAO’s email updates to receive notification of newly posted products.

Order by Phone

The price of each GAO publication reflects GAO’s actual cost of production and distribution and depends on the number of pages in the publication and whether the publication is printed in color or black and white. Pricing and ordering information is posted on GAO’s website, https://www.gao.gov/ordering.htm.

Place orders by calling (202) 512-6000, toll free (866) 801-7077,

or

TDD (202) 512-2537.

Orders may be paid for using American Express, Discover Card, MasterCard, Visa, check, or money order. Call for additional information.

Connect with GAO

Connect with GAO on X,

LinkedIn, Instagram, and YouTube.

Subscribe to our Email Updates. Listen to our Podcasts.

Visit GAO on the web at https://www.gao.gov.

To Report Fraud, Waste, and Abuse in Federal Programs

Contact FraudNet:

Website: https://www.gao.gov/about/what-gao-does/fraudnet

Automated answering system: (800) 424-5454

Media Relations

Sarah Kaczmarek, Managing Director, Media@gao.gov

Congressional Relations

David A. Powner, Acting Managing Director, CongRel@gao.gov

General Inquiries

[1]Congress did not designate any funds for CPF/CDS projects in FY 2025. We plan to review the implementation of FY 2026 CPF/CDS funds in the future. For more information on our work, see https://www.gao.gov/tracking-funds.

[2]For a list of the 19 agencies, see our public website at https://www.gao.gov/tracking-funds.

[3]GAO, Tracking the Funds: Agencies Continued Executing FY 2022 and 2023 Community Project Funding Congressionally Directed Spending Provisions, GAO‑25‑107274 (Washington, D.C.: Nov. 21, 2024); Tracking the Funds: Specific Fiscal Year 2024 Provisions for Federal Agencies, GAO‑25‑107549 (Washington, D.C.: Nov. 21, 2024); Tracking the Funds: Sample of Fiscal Year 2022 Projects Shows Funds Were Awarded for Intended Purposes but Recipients Experienced Some Challenges, GAO‑24‑106334 (Washington, D.C.: Sept. 25, 2024).

[4]For objectives 2 and 3, we did not include FY 2024 projects because we wanted to select projects that were more likely to have started.

[5]Under the Single Audit Act and implementing Office of Management and Budget guidance, nonfederal award recipients that expend at least a certain threshold amount of federal award funds from all sources in a fiscal year are required to undergo either a single audit, which is an audit of an entity’s statements and federal awards, or a program-specific audit for the fiscal year. See 31 U.S.C. § 7502; 2 C.F.R. § 200.501. The Office of Management and Budget updated its guidance to increase the threshold from $750,000 to $1 million or more in April 2024, with an effective date of October 1, 2024. See 89 Fed. Reg. 30,046 (Apr. 22, 2024).

[6]Do Not Pay is a service managed by the Department of the Treasury that checks multiple data sources at once to allow agencies to verify a recipient’s eligibility for payments. Recipients can be manually searched in Do Not Pay using a recipient’s unique entity identifier, business name, employment identification number, or a combination of the three.

[7]An agency may record an obligation only when an obligational event occurs. We did not determine when the obligational event would arise for each action that agencies may take for funds designated through the CPF/CDS provisions in the appropriations acts for FYs 2022-2024. For some grants, the obligational event may occur when the agency awards the grant while, for others, it may occur immediately when the appropriation for the grant becomes law. For more information regarding obligational events for grants, see GAO, Tracking the Funds: Specific Fiscal Year 2022 Provisions for Federal Agencies, GAO‑22‑105467 (Washington, D.C.: Sept. 12, 2022), appendix VI.

[8]See GAO, A Glossary of Terms Used in the Federal Budget Process, GAO‑05‑734SP (Washington, D.C.: Sept. 1, 2005).

[9]The 95 percent confidence interval for this estimate is (52, 71).

[10]The 95 percent confidence interval for this estimate is (12, 21).

[11]The 95 percent confidence interval is (54 percent, 78 percent) or ($13 billion, $19 billion).

[12]The 95 percent confidence interval is (16 percent, 30 percent) or ($4 billion, $7 billion).

[13]The 95 percent confidence interval for the estimated percentage of projects is (0.3 percent, 2 percent) or ($118 million, $698 million).

[14]An agency’s ability to reprogram or transfer CPF/CDS funds will depend on the agency’s statutory authorities, as well as the terms of the appropriation which provided the funds. In addition, as discussed above, for some CPF/CDS funds, the obligational event may occur as soon as the appropriation becomes law. This may also affect the agency’s ability to repurpose the funds.

[15]The 95 percent confidence interval for this estimate is (59, 75). Unless otherwise stated, estimates from the recipient sample are generalizable to all FY 2022 and 2023 projects that recipients reported as moving forward and accepting the funds as of the summer of 2025 (162 of the 167 projects in the sample). We began interviews with the recipients of the sample of projects in April 2025 and ended the interviews in September 2025. We refer to this broad time range as summer of 2025 throughout the report.

[16]The 95 percent confidence interval for this estimate is (1, 8).

[17]The 95 percent confidence interval for this estimate is (22, 37).

[18]The Americans with Disabilities Act is a federal civil rights law that prohibits discrimination against people with disabilities in everyday activities and requires measures to be taken to provide physical access to facilities.

[19]The 95 percent confidence interval for this estimate is (29, 45).

[20]The 95 percent confidence interval for this estimate is (23, 37).

[21]Project descriptions in the JES vary and sometimes provide only high-level information about the intended use of funds. For example, the JES may indicate that the funds are for “facilities and equipment” or “early childhood education”.

[22]The 95 percent confidence interval for this estimate is (89, 98).

[23]The 95 percent confidence interval for this estimate is (87, 97).

[24]The period of performance is the time frame set by agencies for project recipients to complete the CPF/CDS projects.

[25]The 95 percent confidence interval for this estimate is (97, >99.9).

[26]The National Environmental Policy Act requires federal agencies to assess the environmental effects of proposed major federal actions prior to making decisions.

[27]The 95 percent confidence interval for this estimate is (94, >99.6).

[28]The 95 percent confidence interval for this estimate is (87, 97). According to the recipients we interviewed, agencies provided periods of performance that varied from 4 months to 11 years. The period of performance varied due to the type of project and the availability of project funding, among other reasons.

[29]The 95 percent confidence interval for this estimate is (66, 82).

[30]GAO, Grants Management: Agencies Provided Many Types of Technical Assistance and Applied Recipients’ Feedback, GAO‑20‑580 (Washington, D.C.: Aug. 11, 2020).

[31]The 95 percent confidence interval for this estimate is (51, 67). We interviewed 167 recipients during the summer of 2025. There are 162 project recipients who reported their projects were moving forward. In 2024, we reported that 68 percent (107 of 158) of recipients faced challenges completing the steps necessary to receive and implement the FY 2022 funds. See GAO‑24‑106334.

[32]Agency specific online systems include any challenges with online system issues, but does not include registering with SAM.gov (the System for Award Management administered by the General Services Administration). See GAO, Grants Management: Recent Guidance Could Enhance Subaward Oversight, GAO‑25‑107315 (Washington, D.C.: Mar. 26, 2025) for additional information on SAM.gov.

[33]The Build America, Buy America Act required in part that federal agencies ensure the application of a domestic content procurement preference to their federal financial assistance programs for infrastructure projects no later than May 14, 2022, but only to the extent that a domestic content procurement preference meeting the act’s requirements does not already apply. See Infrastructure Investment and Jobs Act, Pub. L. No. 117-58, §§ 70914, 70917, 135 Stat. 429, 1298—1299, 1301 (2021).

[34]Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards, 2 C.F.R. § 200.

[35]The 95 percent confidence interval for this estimate is (35, 50). We asked agencies to respond to questions about their oversight activities in April – May 2025.

[36]Under the Single Audit Act and implementing Office of Management and Budget guidance, nonfederal award recipients that expend at least a certain threshold amount of federal award funds from all sources in a fiscal year are required to undergo either a single audit, which is an audit of an entity’s statements and federal awards, or a program-specific audit for the fiscal year. See 31 U.S.C. § 7502; 2 C.F.R. § 200.501. The Office of Management and Budget updated its guidance to increase the threshold from $750,000 to $1 million or more in April 2024, with an effective date of October 1, 2024. See 89 Fed. Reg. 30,046 (Apr. 22, 2024).

[37]The 95 percent confidence interval for this estimate is (39, 55).

[38]Do Not Pay is a service managed by the Department of the Treasury that checks multiple data sources at once to allow agencies to verify a recipient’s eligibility for payments. Agencies can manually search for recipients in Do Not Pay using a recipient’s unique entity identifier, business name, employment identification number, or a combination of the three.

[39]The 95 percent confidence interval for this estimate is (76, 89). Agencies can use the Do Not Pay list to check various data sources to verify eligibility of a vendor, grantee, loan recipient, or beneficiary to receive federal payments. The Do Not Pay list identifies whether a payee is deceased, ineligible for payment, delinquent on debts, or incarcerated, among other things.

[40]The 95 percent confidence interval for this estimate is (85, 96).

[41]In some instances, agencies disburse funds up front to recipients in full, and the recipients draw down the funds as they incur costs. However, in other cases, recipients incur costs prior to receiving funds from agencies and need to request reimbursement.

[42]The Department of Housing and Urban Development did not respond to our request for an interview to discuss this topic. During our recipient interviews, all but three recipients stated the project purpose aligns with the JES. The three recipients stated they did not know.

[43]Two agencies, the U.S. Army Corps of Engineers and General Services Administration, do not oversee projects with nonfederal recipients in our sample of 167 project recipients.

[44]The 95 percent confidence interval for this estimate is (62, 76).

[45]In addition, the Department of Housing and Urban Development did not require applications for 27 out of the 167 projects in our sample and did not respond to our request for clarification.

[46]The 95 percent confidence interval for this estimate is (51, 66).

[47]Two agencies, the U.S. Army Corps of Engineers and General Services Administration, do not oversee projects with nonfederal recipients in our sample of 167 project recipients.

[48]The Department of Housing and Urban Development did not respond to our request for an interview to discuss this topic.

[49]For this report, we count the U.S. Army Corps of Engineers and Office of National Drug Control Policy, within the Executive Office of the President, as agencies.

[50]For a list of the 19 agencies, see our public website at https://www.gao.gov/tracking-funds.

[51]To inform our estimates, we incorporated the known distribution of appropriated amounts in the population of FY 2022–2024 projects. Using the 10th, 25th, 50th, 75th, and 90th percentiles as boundaries, we defined 6 post-strata for each fiscal year—a total of 19 post-strata, including the certainty stratum of 19 projects.

[52]An expansion estimator is a survey sampling technique that estimates a total population value by weighting sample observations by the inverse of their selection probability.

[53]Two agencies reported obligations data greater than the appropriated amount. One agency clarified that the CPF/CDS grants were used to implement a larger project, and those dollar values represented the obligations for the total project, not just the CPF/CDS portion. One agency clarified there was an error.

[54]GAO‑25‑107274 and GAO, Tracking the Funds: Agencies Have Begun Executing FY 2022 Community Project Funding/Congressionally Directed Spending, GAO‑23‑106318 (Washington, D.C.: Sept. 28, 2023).

[55]The Federal Financial Management Improvement Act of 1996 requires the 24 agencies listed in 31 U.S.C. § 901(b) to implement and maintain financial management systems that comply substantially with (1) federal financial management system requirements, (2) applicable federal accounting standards, and (3) the United States Government Standard General Ledger at the transaction level. Pub. L. No. 104-208, div. A, §101(f), title VIII, 110 Stat. 3009, 3009-389 (Sept. 30, 1996), reprinted in 31 U.S.C. § 3512 note.