Report to Congressional Addressees

United States Government Accountability Office

A report to congressional addressees

Contact: Sharon Silas at silass@gao.gov

What GAO Found

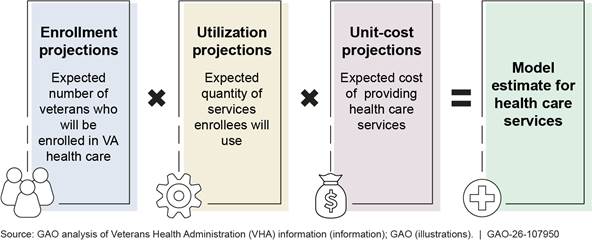

To support its health care budget projection each year, the Veterans Health Administration (VHA) contracts with an actuarial consultant to assist VHA with the annual Enrollee Health Care Projection Model update. The model produces three basic outputs: enrollment, utilization, and unit cost. Each output is subject to several complex adjustments to account for the characteristics of VHA health care and the veterans who access VHA’s health care services.

Basic Outputs of VHA’s Enrollee Health Care Projection Model

GAO found VHA’s processes for developing the model’s estimates align with most but not all relevant standards. For example, VHA’s Office of Enrollment and Forecasting (E&F) does not have a formalized process requiring VHA’s actuarial consultant to incorporate newly emerging data into the model after initial model delivery. According to VHA officials, incorporating newly emerging data after the delivery of its initial model scenario is not required because it depends on factors such as data availability, the timing of the President’s budget, and requests from the VHA Office of Finance. However, incorporating newly emerging data, when possible, could ensure that VHA’s health care cost estimates reflect the most current data, improve the accuracy and completeness of the model estimates, and potentially support a more informed budget request.

VHA uses performance measures to assess its actuarial consultant, but VHA’s standard operating procedure does not specify what E&F staff should be doing to ensure that the consultant adequately performs the tasks outlined in the performance work statement. According to VHA documents, VHA conducts a monthly review of the actuarial consultant’s invoices to ensure it is producing the deliverables laid out in the contract. However, because the invoices only indicate when the work was done, this review does not allow VHA to assess the quality of the consultant’s work. By not including specific oversight tasks in its standard operating procedures, such as establishing a formalized process for assessing the quality of specific tasks in the performance work statement, VHA may miss opportunities to improve the accuracy of its budgetary support provided by its actuarial consultant.

Why GAO Did This Study

VHA, within the Department of Veterans Affairs, serves about 9.1 million enrollees. In its budget request, VHA estimated the fiscal year 2025 medical care total obligational level to be $149.5 billion. Determining needed funding to ensure veterans have access to quality health care involves accurately projecting potential costs.

VHA and its actuarial consultant use a model to project cost estimates for health care services. These estimates are used to inform VA’s budget projection included in the President’s budget request. For fiscal year 2025, VA requested $6 billion in additional funding, beyond the level included in the President’s budget. Given this and that VHA has underestimated its funding needs for health care services in prior years, Congress has raised questions about VHA’s process for developing its budget estimates.

In this report, GAO (1) describes VHA’s current process for updating the actuarial model used to estimate its health care funding needs; (2) examines the extent to which VHA’s processes for developing VA’s health care model estimates align with relevant professional standards; and (3) examines VHA’s oversight of the performance of its actuarial consultant.

GAO reviewed documents from VHA and its actuarial consultant on the processes used to develop health care model estimates, as well as documents for assessing contractor performance. GAO also interviewed VHA officials and VHA's actuarial consultant.

What GAO Recommends

GAO is making five recommendations on VA’s development and oversight of its budget estimate. VA did not provide comments on the report.

Abbreviations

E&F Office of Enrollment and Forecasting

EHCPM Enrollee Health Care Projection Model

OMB Office of Management and Budget

VA Department of Veterans Affairs

VHA Veterans Health Administration

This is a work of the U.S. government and is not subject to copyright protection in the United States. The published product may be reproduced and distributed in its entirety without further permission from GAO. However, because this work may contain copyrighted images or other material, permission from the copyright holder may be necessary if you wish to reproduce this material separately.

June 4, 2026

Congressional Addressees

The Department of Veterans Affairs’ (VA) Veterans Health Administration (VHA) operates one of the largest health care delivery systems in the nation, serving about 9.1 million enrollees through its VHA-operated (i.e., direct care) medical facilities and community health care providers.[1] Determining how much funding the agency needs to ensure veterans have access to quality health care involves projecting potential costs as accurately as possible. Each year, VHA and its actuarial consultant produce an actuarial model, the Enrollee Health Care Projection Model (EHCPM), that VHA uses in its budgeting and planning processes for health care services.[2] VHA uses these model estimates to inform its budget projection for health care services included in the President’s annual budget request.[3]

In July 2024, 4 months after the President submitted the fiscal year 2025 budget request wherein VHA estimated the 2025 medical care total obligation level to be $149.5 billion, VHA informed Congress that it needed additional funding of nearly $12 billion for fiscal year 2025. According to VHA, this increased amount was for health care services, driven by higher-than-expected costs for community care, staffing, medicines, and prosthetics for fiscal years 2024 and 2025. In November 2024, VHA reduced its projected need for fiscal year 2025 to roughly $6.6 billion. As part of the reason for this decrease in additional funding needs, VA reported to Congress that VHA had finished fiscal year 2024 with an additional $2.5 billion in unobligated balances.[4] In mid-March 2025, Congress appropriated to VHA an additional $6 billion using funds from the Cost of War Toxic Exposures Fund.[5] In response to VHA’s projected funding gap in fiscal years 2024 and 2025, along with projected funding gaps in certain fiscal years prior to fiscal year 2024, Congress has raised questions about VHA’s process for developing its budget projection.[6]

Along with the VA Office of Inspector General, we have reported on challenges VA has faced regarding the reliability and accuracy of its budget projection for health care services, as well as its supplemental funding requests.[7] For example, in February 2024, we reported that VA was not prepared to estimate the amount of supplemental funding needed during a catastrophic event, such as the COVID-19 pandemic, because it did not have the modeling capacity to do so.[8]

We performed our work at the initiative of the Comptroller General. In this report, we

1. describe VHA’s current process for updating the actuarial model used to estimate its health care funding needs;

2. examine the extent to which VHA’s processes for developing VA’s health care model estimates align with relevant standards, including actuarial standards of practice and federal internal control standards; and

3. examine VHA’s oversight of the performance of its actuarial consultant.

To describe VHA’s current process for updating the actuarial model used to estimate its health care funding needs, we reviewed documentation provided by VHA and its actuarial consultant, Milliman, describing the actuarial model update process, including procedures such as adjusting for discrepancies between actual workload (i.e., utilization of services) and model estimates. We also interviewed and reviewed written responses from VHA’s Office of Enrollment and Forecasting (E&F) and VHA’s Office of Finance.[9]

To examine the extent to which VHA’s processes for developing VA’s health care cost model estimates align with relevant standards, including actuarial standards of practice and federal internal control standards, we reviewed documentation from VHA and its actuarial consultant on the methods and processes used to develop health care model estimates produced by the EHCPM. For example, we reviewed the annual EHCPM documentation and analysis report, and a model risk assessment report that identifies sources of risk and describes the degree of uncertainty for the projection supporting the VA health care budget. We also reviewed budget impact analyses for fiscal years 2022 through 2025 that examine the drivers responsible for cost increases from the previous year. We interviewed VHA officials from E&F about their processes for communicating data quality and limitations. We also interviewed or received written responses from officials in VA’s Office of Actuarial Services, as well as key program offices including the Office of Integrated Veteran Care; Office of Productivity, Efficiency and Staffing; Pharmacy Benefits Management Services; Prosthetics and Sensory Aids Service; and officials from the Veterans Benefit Administration regarding their involvement in VHA’s budget development process.[10] We assessed these processes against eight relevant actuarial standards of practice.[11] We also identified five federal internal control standards that were relevant to our work.[12]

We examined VA’s actuarial consultant’s role in the actuarial modeling processes in the context of actuarial standards of practice. Our actuarial work on this engagement was conducted by a GAO Assistant Director and Actuary and GAO’s Chief Actuary (identified in the Staff Acknowledgment section of this report) who meet the qualification standards of the American Academy of Actuaries to conduct the actuarial aspects of our work for this report. While we conducted actuarial reviews of VHA’s models and processes, we did not evaluate the accuracy of VHA’s EHCPM model output or their underlying assumptions, as that type of analysis was outside the scope of this report.

To examine VHA’s oversight of the performance of its actuarial consultant, we reviewed VA documentation, including VHA’s standard operating procedure and quality assurance surveillance plan for assessing contractor performance, and the Actuarial Support Services contract and performance work statement that were in effect as of March 31, 2025. We also reviewed documentation related to VHA’s oversight activities, including contractor performance reviews, reviews of invoices, and contractor performance assessment reports for fiscal years 2019 through 2024. To understand the processes in place to monitor and assess contractor performance, we interviewed or received written responses from officials in VHA’s E&F and Office of Finance, and VA’s Office of Management, Office of Actuarial Services, and the Strategic Acquisition Center.[13] We also reviewed documentation and information from VHA officials regarding how oversight responsibilities are defined and executed in relation to tasks and deliverables outlined in the consultant’s performance work statement. We assessed these oversight practices against the Federal Acquisition Regulation, and VA Acquisition Regulation in the context of federal internal control standards for information and communication.[14]

Additional information about our scope and methodology is described in appendix I.

We conducted this performance audit from November 2024 to June 2026 in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

Background

Developing VHA’s Health Care Budget Projection Using the EHCPM

In preparation for the annual appropriations process, VHA develops an estimate of the resources needed to provide health care services—known as its health care budget projection—for two fiscal years.[15] For fiscal year 2025, VHA used the EHCPM estimates—known as model estimates—to develop approximately 89 percent of its health care budget projection and uses other methods for the remainder of the projection.[16] For example, the EHCPM projects cost estimates for outpatient and inpatient health care services provided at VHA facilities (i.e., direct care) and available through community providers (i.e., community care).[17] VA uses the health care budget projection to develop its budget request that is included in the President’s budget request for federal agencies.

The EHCPM projects 20 years into the future for health care services. VA uses the model estimates from EHCPM to make projections 3 and 4 years into the future for budget purposes based on data from the most recently completed fiscal year. For example, in 2023, VHA used data from fiscal year 2022 to develop its health care budget projection for the President’s fiscal year 2025 budget request and advance appropriation request for fiscal year 2026.

The EHCPM incorporates assumptions that affect the model estimate over time. The EHCPM produces three basic outputs: enrollment, utilization, and unit cost. Each output is subject to several complex adjustments to account for the characteristics of VHA health care and the veterans who access VHA’s health care services. (See fig. 1.)

Notes: The EHCPM makes several complex adjustments to projections for VHA health care services to account for the characteristics of VHA health care and enrolled veterans. For example, the EHCPM includes adjustments to account for reliance on the Department of Veterans Affairs (VA) health care—that is, the extent to which enrolled veterans will choose to access health care services through VHA as opposed to other health care programs. Unit costs are the costs to VHA for providing a unit of service, such as a 30-day supply of a prescription or a day of care at a medical facility. The EHCPM produces model estimates to inform its budget projection for health care services that may be revised by the Office of the Under Secretary of Health.

Role of VHA and Its Actuarial Consultant in Developing Health Care Model Estimates

VHA’s E&F is responsible for (1) overseeing work performed by VHA’s actuarial consultant; (2) acting as the liaison between the actuarial consultant and VHA’s finance, leadership, and program offices; (3) gathering VA data and creating various files that are submitted to the actuarial consultant to update the EHCPM; and (4) at the request of VHA’s Office of Finance, VA and VHA leadership, and the Office of Management and Budget (OMB), working with the actuarial consultant to run different scenarios with changes in assumptions—estimates about uncertain future events used to assess risk and make informed decisions—several times a year.

According to VHA’s contract with its actuarial consultant, the consultant provides VHA with EHCPM estimates of VHA health care costs that are used to inform VHA’s budget projection.[18] The consultant’s contracted services include

· annually updating the EHCPM throughout the modeling cycle with VHA health care data, such as workload and cost of health care services, from the most recently completed fiscal year and other newly available data;

· using a variety of tools and methods for conducting technical reviews during the development of the EHCPM for testing and assessing the EHCPM and ensuring that the EHCPM is functioning as intended;

· responding to requests for comparisons of actual to projected enrollment, patients, utilization, and costs;

· providing VA staff and stakeholders, such as OMB and Congress, with trainings, briefings, tools, and databases to provide information about EHCPM methodology, assumptions, and projections; and

· assisting stakeholders, such as OMB and Congress, in understanding the EHCPM and the key drivers of projected veteran demand for VA health care.[19]

VHA’s Budget Projection for Inclusion in the President’s Budget Request

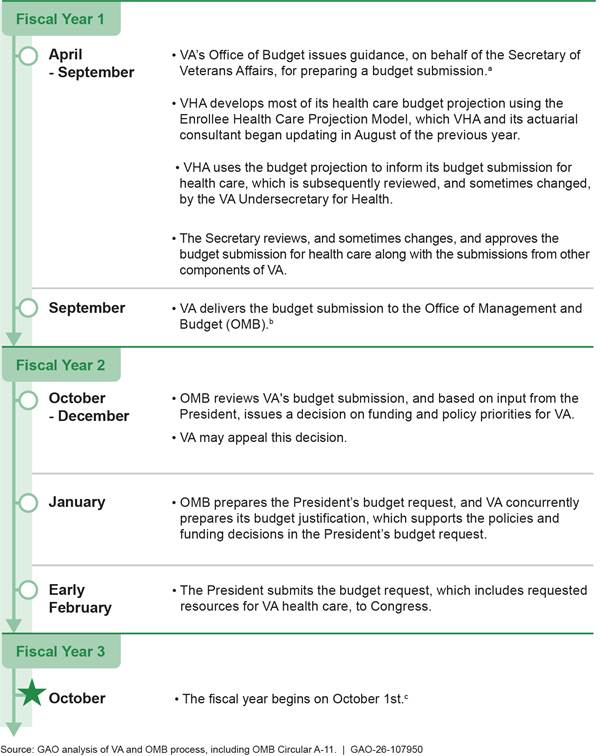

VHA’s annual budget projection—which includes the health care model estimates—is reviewed within VHA, by the Secretary of Veterans Affairs, and finally within OMB to inform the President’s budget request.[20] VHA generally starts to develop a health care budget projection in April of each year, approximately 10 months before the President submits the fiscal year budget request to Congress, which, by law, should occur no later than the first Monday in February.[21]

The VHA budget projection changes during the 10-month budget development process, in part, due to the various levels of review at VA and OMB before the President’s budget request is submitted to Congress. The Secretary of Veterans Affairs considers the health care budget projection developed by VHA when assessing resource requirements among competing interests within VA. OMB considers overall resource needs and competing priorities of other federal agencies to inform decisions on the level of funding to request for VHA’s health care services. OMB passes back decisions, known as a “passback,” to VA and other agencies on their budget projection, along with funding and policy proposals to be included in the President’s budget request.[22] (See fig. 2.)

Figure 2: Timeline for Developing the Budget Projection for VA Health Care Services Included in the President’s Budget Request

Notes: Under 31 U.S.C. § 1105, the President’s budget submission should be submitted by the first Monday in February. In practice, however, the President’s budget request is sometimes delivered later than early February.

aOMB coordinates the development of the President’s budget proposal by issuing circulars, memoranda, and guidance documents to the heads of executive agencies throughout the federal government. Executive agencies, including the Department of Veterans Affairs (VA), may then prepare their budget requests in accordance with the instructions and guidance provided by OMB. OMB’s Circular A-11, which is updated annually, is an extensive document that contains instructions and schedules for agency submission of budget requests and justification materials to OMB.

bThe VA budget submission includes the Veterans Health Administration’s (VHA) health care budget projection, as well as budget information from other VA components such as the Veterans Benefits Administration and the Office of Information and Technology.

cThis is the fiscal year in which VA is appropriated funds developed in fiscal year one.

Concurrent with OMB’s preparation of the President’s budget request, VA develops its congressional budget justification. The congressional budget justification contains actual obligations for the most recently completed fiscal year at the time of the release, and estimated obligations for the current fiscal year, as well as the 2 years for which appropriations are requested. For example, the VA’s congressional budget justification related to the President’s fiscal year 2025 budget request, which was released in March 2024, contains actual obligations for fiscal year 2023 and estimated obligations for fiscal years 2024 through 2026.

VHA’s Process for Updating its Actuarial Model Estimates Includes Gathering Data and Meeting with Program Offices

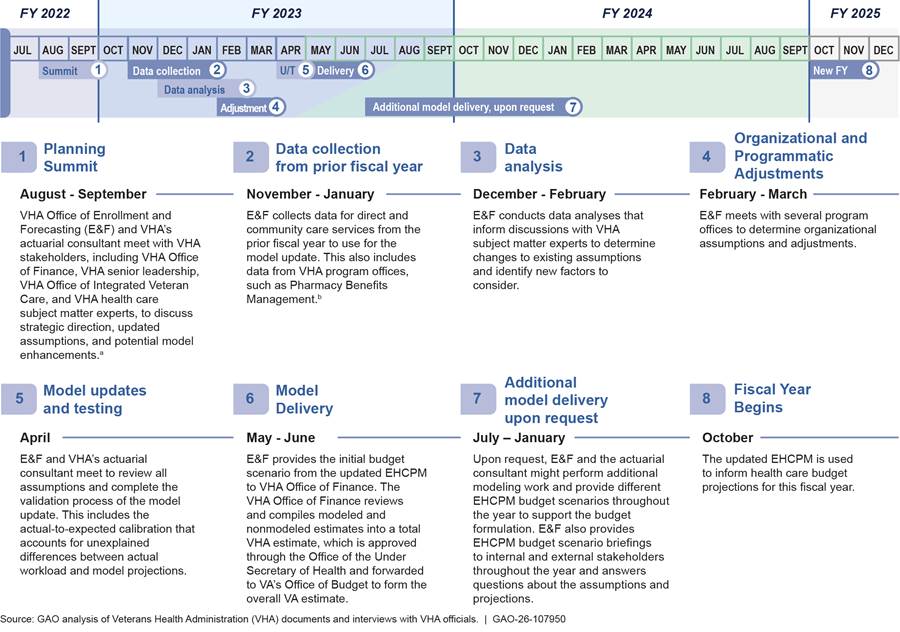

To develop its actuarial model estimates to support its health care budget projection each year, at the direction of E&F, VHA’s actuarial consultant conducts an EHCPM update. (See fig. 3.) At the beginning of the EHCPM update, E&F and VHA’s actuarial consultant hold a planning meeting with various VHA program offices, VHA stakeholders, and VHA officials. Each year, E&F and VHA’s actuarial consultant update the EHCPM to account for the most recently completed fiscal year’s actual data, including data on enrollment and health care costs, known as the base year. For example, the base year for the 2023 EHCPM uses fiscal year 2022 actual data to develop cost projections for fiscal years 2025 and 2026 to inform the health care budget request.

Figure 3: VHA Process for Updating the Enrollee Health Care Projection Model (EHCPM) and Model Delivery

Note: The EHCPM provides health care model estimates for the budget year and the following year’s advance appropriation. For example, the 2023 EHCPM provides estimates for fiscal year 2025 budget and fiscal year 2026 advance appropriation.

aAccording to VHA officials, E&F meets with program offices such as Pharmacy Benefits Management Services; Primary Care; Geriatrics and Extended Care Services; and the Office of Productivity, Efficiency and Staffing.

bThe initial budget scenario includes a budget impact workbook, a report of the model data that includes projected costs for each service category broken out by direct and community care, and a projection supplement workbook that has projections for populations not modeled in the EHCPM.

E&F and VHA’s actuarial consultant update model assumptions—such as projected changes in relative morbidity, and veteran reliance on VHA health care estimates about uncertain future events used to assess risk and make informed decisions. For example, using actual data on currently enrolled and previously enrolled veterans from multiple years, VHA and the consultant might develop assumptions about the impact of a legislative change on enrollment eligibility. The Honoring our PACT Act of 2022 expanded benefits for veterans exposed to certain toxins in the course of their military service, which led to changes in the modeled assumptions for new enrollment and priority transitions.[23] There are three outputs of the EHCPM: enrollment, workload, and costs. The outputs are the projections that change based on assumptions such as enrollee demographic mix, reliance, geographic migration, and impacts of legislative initiatives. These assumptions may be updated or other assumptions added during the EHCPM update.

According to documentation and VHA officials, as part of the EHCPM update and development process, VHA’s actuarial consultant uses tools and methods for conducting technical reviews that test and update the model during the development of the EHCPM. According to VHA officials, this ensures that the EHCPM is functioning as intended. For example:

· Enrollment key driver review. According to VHA documentation, this analysis measures the impact of updates to key drivers using all available years of enrollment data. Each key driver contributes to the change in enrollment from one period to the next, and each is reviewed for material changes over time. If material changes occur, then an explanation is sought through further analysis or engagement with VHA experts. For example, key drivers such as new enrollment, mortality, suspension, reinstatement, ineligibility, priority transitions, and geographic migration are measured on a monthly and annual basis.

· Unit costs and budget reconciliation. According to VHA documentation, as part of each annual update, unit costs—expected costs of providing health care services—are reviewed in relation to unit costs from prior years. As part of the annual update, any services where unit cost levels changed by what VHA considers a moderate amount are reviewed in more detail. Once detailed base year unit costs are calculated, they are loaded into the EHCPM. VHA’s actuarial consultant then conducts a budget reconciliation process by comparing the projected costs (resulting from applying the base year unit costs to the modeled base year utilization) to actual obligations.[24] For example, there are 31 budget reconciliation categories, split between community care and VA direct care, and each year the actuarial consultant validates that actual base year cost projections tie to the actual base year budget obligations.

· Actual to expected adjustment. According to VHA documents and officials, the base year projection in the EHCPM attempts to appropriately capture major impacts of veteran demand for health care services. That is, the EHCPM projection of the base year attempts to approximately align with actual workload experience. However, according to VHA documents and officials, there will always be unexplained differences between actual workload experience and what is projected in the base year prior to model calibration. This adjustment allows E&F and its actuarial consultant to identify and quantify areas of unexplained differences in utilization for further review and refinement. This adjustment may then be used to account for unexplained differences in utilization by calibrating what is estimated in the base year to what VA actually experienced. For example, if the EHCPM estimates 1,000 visits for a given health care service in the base year, but there were actually 500 visits, then a review would be conducted as to why the base year projections deviated significantly from actuals prior to the model being finalized.

·

Budget impact analysis. According to VHA documentation,

during model development, within the budget impact analysis, each key driver

that contributes to a change in projected utilization and costs is specifically

identified and quantified. As most of these drivers are present from one year

to the next, these outcomes are compared to the outcomes from the previous

model and against external sources, such as policy impact estimates developed

outside of the model. For example, the budget impact analysis reveals (1) the

drivers that are responsible for the majority of the cost increases from the

prior year; (2) if the drivers are population driven, program driven, or policy

driven; and (3) the projected cost bounds for certain drivers (i.e., the amount

of money saved by removing or changing a policy).

According to VHA officials, once the EHCPM update is complete, VHA’s E&F provides the initial budget scenario, which includes the model estimates for health care services, to VHA’s Office of Finance.[25] This includes a budget impact analysis, a report with projected costs for each service category broken out by direct and community care, and a projection supplement workbook that has projections for populations not modeled in the EHCPM.

The Office of Finance reviews, calculates, and combines both modeled and nonmodeled estimates into an overall VHA budget projection for review and approval by the Office of the Under Secretary for Health. The projection is sent to VA’s Office of Budget for approval before it is presented to VA’s Assistant Secretary for Management. The Secretary of Veterans Affairs approves and submits the overall budget request to OMB around September of each year.

According to VHA officials, E&F provides several EHCPM budget scenario briefings to internal and external stakeholders, such as Congress, as well as answers questions about the assumptions and projections. Additionally, E&F may produce additional budget scenarios based on other factors that arise between the delivery of the initial budget scenario and the publication of the President’s budget.[26]

VHA’s Processes for Developing its Health Care Cost Model Align with Most but Not All Relevant Standards

VHA’s Processes Largely Align with Relevant Standards

VHA’s processes for having its actuarial consultant develop EHCPM estimates align with most aspects of relevant actuarial standards of practice.[27] The following are examples of areas for which VHA’s processes align with these standards:

· Incurred Health and Disability Claims. According to VHA, its actuarial consultant adjusts utilization projections for changing economic conditions and includes unit cost reconciliation adjustments to account for administrative components of claim costs, which aligns with the Actuarial Standards of Practice No. 5.

· Risk Classification. According to VHA, its actuarial consultant classifies veteran enrollees based on their risks in terms of the expected cost of providing VA health care coverage or services. As a result, the EHCPM projects enrollment, utilization, and unit costs for VHA health care services based on veteran enrollee characteristics, including age, gender, priority group, period of service, and geographic location, which aligns with the Actuarial Standards of Practice No. 12.

· Expert Testimony by Actuaries. In April 2019, VHA’s actuarial consultant provided testimony before the Senate Committee on Veterans’ Affairs on implementing the Veterans Community Care Program. During the testimony, the consultant provided the description of EHCPM and disclosed some of the assumptions used in the model, which aligns with the Actuarial Standards of Practice No. 17.

See appendix II for more information on actuarial standards of practice relevant to VHA’s processes for developing EHCPM estimates, including other aspects of standards that VHA’s processes align with, and examples of VHA’s actuarial consultant’s work.

VHA is also taking steps to improve its processes for involving program offices and subject matter experts in assisting E&F and VHA’s actuarial consultant in developing the EHCPM inputs for specific areas such as community care, pharmacy services, and prosthetics services. In March 2025, the VA Office of Inspector General recommended that VHA establish and implement a plan to review current processes and procedures for involving program offices and pertinent subject matter experts in developing the EHCPM inputs and formalize the expectations of their involvement in this process through guidance or protocols.[28] VHA agreed with the recommendation and, in response, stated that it is developing standardized guidance documents on VHA program office engagement protocols for the EHCPM update.

VHA’s Processes Do Not Fully Align with Certain Aspects of Relevant Standards

While our review found that VHA’s processes align with most aspects of the actuarial standards of practice we reviewed for the purpose of this report, we also found that VHA’s processes do not fully align with certain aspects of relevant actuarial standards of practice and internal control standards in areas related to (1) data quality, (2) incorporation of newly emerging data, and (3) model estimate variability.[29] By following the practices and standards we discuss below, VHA will be better positioned to ensure its actuarial consultant maintains integrity and reliability in determining VHA’s estimates for health care funding.

Data quality. According to relevant actuarial standards of practice, when actuaries use data provided to them by others, ensuring the accuracy and completeness of data is the responsibility of those who supply the data.[30] Furthermore, relevant federal internal control standards state that agencies should obtain relevant data from reliable internal and external sources and process the data into quality information.[31]

We found that E&F obtains recent data and provides it to the consultant. According to VHA officials and documents, E&F is responsible for providing its actuarial consultant with data, including utilization and cost data, for use in the EHCPM when projecting potential future costs. At the beginning of a new fiscal year, according to E&F officials, E&F obtains data from the prior fiscal year either from VHA’s corporate data warehouse or from program offices and transmits it to its actuarial consultant. E&F also obtains data from relevant program offices in response to emerging needs such as legislative changes. Further, VHA’s actuarial consultant relies on E&F to communicate to it the quality of the data provided for use in the actuarial model.[32]

In prior work, we found VHA did not communicate all relevant information on the quality of its community care utilization and cost data, including any limitations affecting these data, to its actuarial consultant and recommended VHA take steps to do this.[33] VHA has implemented this recommendation by establishing a formalized process for E&F to communicate information on the quality of the community care data it provides to the actuarial consultant.[34] However, E&F does not have a similar process to communicate information on the quality of direct care data. Rather, it does so on an ad hoc basis, according to E&F officials. These direct care data include utilization and cost data E&F obtains from program offices such as the Office of Productivity, Efficiency and Staffing; Pharmacy Benefits Management Services; Prosthetics and Sensory Aids Service; and Veterans Benefits Administration. Given that veterans receive the majority of their health care services through direct care, it is important that the actuarial consultant is aware of any data limitations that could inform cost estimates for these services.

E&F officials explained to us why they do not document information on any limitations of the direct care data and communicate this information to the consultant. According to E&F officials, the data come from various VHA offices and databases that all have quality assurance practices. E&F officials added that they are users, not owners, of the data and they take steps to try to ensure the data they provide are complete. However, E&F could establish a formalized process for communicating to the actuarial consultant information on the quality of the direct care data it provides, including any limitations of those data, similar to the process E&F already has to communicate such information on a monthly basis for the community care data it provides to its actuarial consultant. Without doing so, there is a risk that this information may not be communicated to the consultant and subsequently not taken into account as the actuarial consultant develops the health care model estimate. Having a formalized process to communicate all relevant information to the actuarial consultant on the quality of the direct care data used in the EHCPM, including any limitations, would help the consultant address any such limitations as part of the actuarial modeling, thus improving the actuarial modeling that informs VHA’s health care budget projection.

Incorporation of newly emerging data. The actuarial standards of practice we reviewed state that actuaries should use data that is sufficiently current and consider the availability of additional or alternative data and the potential benefits of such data.[35] Further, federal internal control standards state that management should design control activities to achieve objectives and respond to risks; implement such activities through policies; and use quality information that is appropriate, current, complete, accessible, and provided on a timely basis to make informed decisions.[36]

VHA has the opportunity to incorporate newly emerging data in its annual EHCPM update after the initial model for the budget scenario is delivered during the President’s budget request cycle.[37] For example, E&F and VHA’s actuarial consultant updated the 2023 EHCPM model estimates in fiscal year 2024 by incorporating newly emerging fiscal year 2023 data. However, according to E&F officials, E&F does not have a formalized process requiring VHA’s actuarial consultant to incorporate newly emerging data into the model after initial model delivery when possible. According to VHA officials, incorporating newly emerging data after the delivery of its initial model scenario is not required because it depends on factors such as data availability and appropriateness of the data for use in the EHCPM update, the timing of the President’s budget, and requests from the VHA Office of Finance. However, given that in recent years the President’s budget has often been released later than the first Monday in February, VHA has had opportunities to incorporate newly emerging data. According to VHA officials, in 4 of the past 5 years, VHA’s actuarial consultant has incorporated newly emerging data in the model after initial delivery. However, incorporating newly emerging data after the initial model delivery is currently dependent on a request from the VHA Office of Finance. In addition, without a formal process for incorporating newly emerging data, there is a risk that this effort will not be sustained in light of any organizational or leadership changes that may occur. Therefore, formalizing this process would support consistent and timely incorporation of newly emerging data when possible.

By identifying an approach to help ensure that the actuarial consultant establishes a formalized process to incorporate newly emerging data in the model after initial model delivery—unless there is insufficient time due to the scheduling of the President’s budget request or data availability—VHA could ensure that its health care cost estimates reflect the most current data, improve the accuracy and completeness of the model estimates, and potentially support a more informed budget request.[38]

Model estimate variability. According to the actuarial standards of practice we reviewed, actuaries should communicate uncertainties in the model output, including identifying possible variability of model output such as variability around expected health care cost estimates.[39] Furthermore, federal internal control standards state that management should communicate relevant quality information to achieve the agency’s objectives, and identify, analyze, and respond to risks related to achieving an agency’s defined objectives.[40]

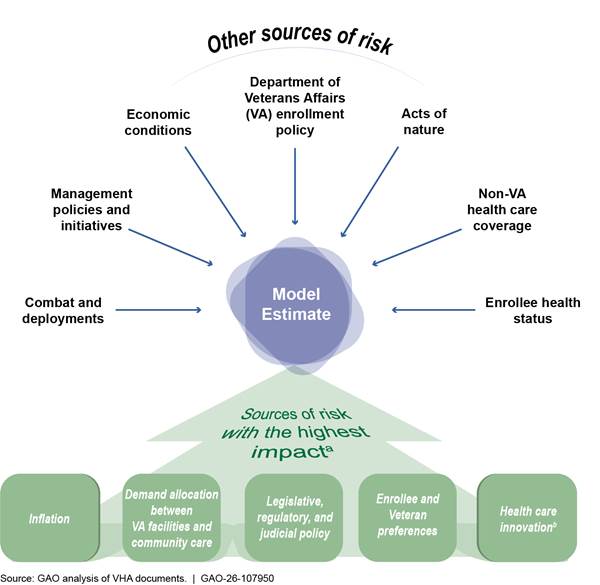

While E&F produces the EHCPM risk assessment report, based on the actuarial consultant’s work, to communicate model uncertainty associated with some of the key drivers, the report does not provide sufficient clarity about the extent to which the overall model estimate might vary due to the combination of all the key drivers identified.[41] According to VHA documentation, the EHCPM risk assessment report identifies sources of risk, such as economic conditions; enrollee and veteran preferences; and legislative, regulatory, and judicial policy. (See fig. 4.) However, the report does not include information on potential model output variability of health care cost estimates—that is, the extent to which the model estimate might vary. According to VHA officials, this is because VHA does not require its actuarial consultant to determine, document, and communicate the extent to which the model estimates might vary.

Figure 4: Sources of Risk Contributing to the Enrollee Health Care Projection Model (EHCPM) Estimate Used to Support the Veterans Health Administration’s (VHA) Fiscal Year 2025 Budget Projection

aSources of risk identified by VA as having the highest impact on the EHCPM budget scenario for fiscal year 2025.

bHealth care innovation refers to advancements in medical technology and pharmaceuticals such as the advancements in prosthetics for lost limbs. It is one of the highest impact sources of risk because its timing is difficult to predict, and it can change treatment utilization and costs.

VHA officials told us they do not require the actuarial consultant to provide certain information on the extent to which the model estimate might vary in the EHCPM risk assessment report due to concerns that sources of uncertainty cannot be statistically measured or assigned probabilities. However, according to actuarial literature on uncertainty, providing variability estimates is feasible.[42] For example, VHA’s actuarial consultant can use techniques such as scenario analysis and stress testing to provide information on potential output variability of health care model estimates.[43]

By having information on potential output variability of health care model estimates in the EHCPM risk assessment report, VHA can be better informed on how the model estimates might vary from actual obligations when using the EHCPM to make decisions and to develop budget requests. This lack of information could affect VHA’s decision-making as it uses the EHCPM to develop budget requests, potentially leading to underestimations of required funding and, as a result, the need for unexpected requests for supplemental funds as occurred in fiscal year 2025, for example. By identifying an approach to help ensure that the actuarial consultant better documents and more effectively communicates information on potential output variability of health care model estimates, VHA could ensure VA stakeholders, such as VA leadership, understand how to best use model estimates to support the formulation of VHA’s budget projection. Additionally, if this model estimate variability information were included and clearly communicated in the consultant’s risk assessment report, it could help VHA justify the need for additional funding if required.

VHA Uses Performance Measures to Assess Consultant, but Lacks Specific Oversight Responsibilities in its Standard Operating Procedure

In order to oversee the performance of its actuarial consultant, VHA’s E&F office conducts reviews of its actuarial consultant using performance metrics, defined in the quality assurance surveillance plan as outlined in VHA’s standard operating procedure.[44] E&F uses these performance metrics to ensure that the consultant is performing the services required by this performance work statement in an acceptable manner.[45] For example, according to VHA documentation, E&F can conduct periodic inspections, often reviewing a random sample of the actuarial consultant’s database and statistical output, actuarial analyses and briefing materials, and the EHCPM analysis report for accuracy and completeness. Additionally, VHA staff, who regularly work with VHA’s actuarial consultant and E&F, provide input and feedback to E&F to help ensure that the consultant is available for VHA staff and is meeting their needs. (See app. IV for a full list of quality assurance surveillance plan performance metrics used to assess VHA’s actuarial consultant.)

However, we found that VHA’s standard operating procedure does not specify what E&F staff should be doing to ensure that the consultant adequately performs the tasks outlined in the performance work statement. According to the Federal Acquisition Regulation, quality assurance is necessary to ensure the contractor complies with the work laid out in the contract’s requirements.[46] In contrast, VHA’s standard operating procedure only provides a broad overview of what E&F’s oversight responsibilities should be. For example, according to the VHA’s standard operating procedures, E&F is responsible for conducting (1) a monthly review of the consulting hours and deliverables of the actuarial consultant, and feedback that the deliverables met or did not meet the performance standards identified in the quality assurance surveillance plan; and (2) performance review meetings with the actuarial consultant and other VA staff, if necessary, to ensure that the consultant is providing the appropriate expertise and staffing level to successfully complete assigned tasks within required deadlines and discuss any performance issues.

According to VHA documents and officials, E&F conducts a monthly review of the actuarial consultant’s invoices to ensure it produces the deliverables laid out in the performance work statement and holds performance review meetings when needed with the consultant. However, because the invoices only indicate when the work was done, reviewing them does not allow E&F to assess the quality of the work. Additionally, according to VHA officials, E&F does review all deliverables produced by the actuarial consultant and will notify the consultant via email if there is an issue. However, there is no formal assessment of the quality of the documents. According to VHA documents and officials, E&F works closely and meets on an ad hoc basis at various times throughout the year with its actuarial consultant and does not believe there to be any concerns about the performance of the consultant. These officials also stated that they rely on the consultant’s internal review process to assess quality control for the consulting, modeling, and analytical services it provides to VHA. While VHA’s actuarial consultant may share aspects of the internal review, E&F does not formally review information pertaining to this process.

Given that for fiscal year 2025, VHA used the EHCPM estimates to develop approximately 89 percent of its health care budget projection, it would be beneficial to update the standard operating procedure to include responsibilities that require E&F to assess the quality of the consultant’s tasks and deliverables that are included in the performance work statement. For example, the standard operating procedure could include that E&F conduct a formal review process to assess the quality of the actual-to-expected analysis, the consultant’s model validation procedures, and the EHCPM analysis report, among other things. Additionally, the standard operating procedure could include that E&F conduct a formal review of the consultant’s internal review so it can ensure it was completed and is aware of any issues identified in this review. VHA officials told us that because E&F does not have actuaries on staff, it is unable to assess the actuarial merits of the consultant’s deliverables.

However, according to VHA officials, VA has set a goal for VA’s Office of Actuarial Services to be involved in VHA’s actuarial consultant’s development of model estimates for health care. According to VHA officials, this would include conducting an independent review of the reasonableness of these estimates.[47] As of September 2025, VHA officials told us that VA’s Office of Management was still in the process of operationalizing the Office of Actuarial Services’ oversight role in overseeing the consultant’s work and could not provide us with a formalized plan for this oversight role. Our body of work has shown that by setting implementation goals, an organization builds momentum and can show progress from day one, thereby helping ensure an initiative’s successful completion.[48] Furthermore, relevant federal internal control standards state that agencies should internally communicate relevant quality information—including objectives and responsibilities—down, across, and up the organization to achieve entity objectives.[49]

VA officials told us that the Office of Actuarial Services executive director is still learning more about VHA’s actuarial consultant’s process of developing model estimates for VHA’s budget projections. As of October 2025, VHA officials told us that the Office of Actuarial Services had started its involvement with the VHA budget process to provide comments on the fiscal year 2028 budget. As of January 2026, VHA officials told us that E&F and its actuarial consultants have had two meetings with the Office of Actuarial Services related to data inputs for the EHCPM. As of that time, there was no formal process, such as a Memorandum of Agreement, to ensure that the Office of Actuarial Services would provide assistance with oversight of the consultant’s work.

Effective contract management and oversight are essential to ensuring the government receives the goods and services it has contracted for. By not updating its standard operating procedure to specify in more detail how E&F should oversee the quality of the work produced by the actuarial consultant, VHA may not be able to reasonably ensure that its actuarial consultant is fulfilling the work requirements agreed upon in the performance work statement. Additionally, by not including specific oversight tasks, such as developing formal processes for reviewing the quality of the actuarial consultant’s work, VHA may miss opportunities to improve the accuracy of its budgetary support provided by the actuarial consultant. Additionally, by having a formalized process, such as a Memorandum of Agreement, for implementing VA’s goal for the Office of Actuarial Services to be involved in VHA’s actuarial consultant’s development of model estimates for health care, VA could help improve the efficiency and effectiveness of its efforts to oversee the quality of the work produced by its actuarial consultant.

Conclusions

While the amount of VHA’s budget projections are determined by several factors, including VA policy decisions and the President’s priorities, the EHCPM plays a critical role in projecting VA’s budgetary needs. Given that VHA has underestimated its funding needs for health care services in prior years, it is especially important that VHA takes steps to accurately project its funding needs for future health care services. Otherwise, VHA may run the risk of underestimating or overestimating the resources needed to provide health care services to veterans.

We found that VHA’s processes for developing EHCPM estimates align with most but not all relevant actuarial and internal control standards. These standards are important to ensuring that VHA’s contracted actuaries maintain integrity and reliability in determining VHA’s estimates for health care funding. We identified deficiencies in VHA’s budget development process related to relevant standards including (1) data quality, (2) incorporating newly emerging data, and (3) model estimate variability. Developing a formalized process to ensure limitations affecting direct care data are properly communicated to VHA’s actuarial consultant would help the agency ensure the reasonableness of the model estimates for the budget. Additionally, by including newly emerging data in the annual model update, VHA could ensure that the model reflects the most current data, improve the accuracy and completeness of the model estimates, and potentially support a more informed budget request. Further, reporting information on the extent to which the EHCPM estimates can vary could better inform VHA’s decision-making as it uses the EHCPM to develop its health care budget requests.

In addition, because VHA is reliant on an actuarial consultant to help develop budget estimates for veterans’ health care services, it is critical that VHA assess the performance of its consultant. However, VHA’s standard operating procedure does not outline specific responsibilities for overseeing the actuarial consultant’s tasks, such as formalized processes for reviewing the quality of the work produced by the consultant. This limits the agency’s ability to ensure the consultant properly carries out its work in estimating VHA’s needed resources for health care services. Establishing specific oversight responsibilities in the standard operating procedure would better enable VHA to reasonably ensure that its actuarial consultant is fulfilling its work requirements. Additionally, because E&F does not have actuaries on staff to assess the actuarial consultant’s technical code or calculations, it is important that VA have a formal process to ensure that VA implements its goal that the Office of Actuarial Services provide assistance with oversight of the consultant’s work. By having a formalized process, such as a Memorandum of Agreement, VA could help improve the efficiency and effectiveness of its efforts to oversee the quality of the work produced by its actuarial consultant.

Recommendations for Executive Action

We are making the following five recommendations to VA:

The VA Undersecretary for Health should establish formalized processes for communicating to its actuarial consultant during the annual model update process information on the data quality, including any limitations, of VA direct care data used in the actuarial modeling that informs VA’s health care budget projection. (Recommendation 1)

The VA Undersecretary for Health should identify an approach to help ensure that there is a formalized process for incorporating newly emerging data, when possible, in the model after initial model delivery and prior to submitting the health care budget projection for the President’s budget request. (Recommendation 2)

The VA Undersecretary for Health should identify an approach to help ensure that information on the extent to which the EHCPM estimates can vary are documented and reported, such as in the annual risk assessment report and take action to implement that approach. (Recommendation 3)

The VA Undersecretary for Health should update its standard operating procedure for assessing its actuarial consultant’s performance to include a formalized process for assessing the quality of the consultant’s deliverables to ensure the consultant complies with the work laid out in the performance work statement. (Recommendation 4)

The VA Undersecretary for Health should ensure it has a formalized process, such as a Memorandum of Agreement, for meeting its goal for VA’s Office of Actuarial Services to be involved in VHA’s development of model estimates for health care. (Recommendation 5)

Agency Comments

We are sending copies of this report to the appropriate congressional committees and the Secretary of Veterans Affairs. The report is also available at no charge on GAO’s website at http://www.gao.gov.

If you or your staff has any questions regarding this report, please contact me at silass@gao.gov. Contact points for our Offices of Congressional Relations and Media Relations may be found on the last page of this report. GAO staff who made key contributions to this report are listed in appendix V.

Sharon M. Silas

Director, Health Care

List of Addressees

The Honorable Jerry Moran

Chairman

Committee on Veterans’ Affairs

United States Senate

The Honorable John Boozman

Chairman

Subcommittee on Military Construction, Veterans Affairs, and Related Agencies

Committee on Appropriations

United States Senate

The Honorable Mike Bost

Chairman

The Honorable Mark Takano

Ranking Member

Committee on Veterans’ Affairs

House of Representatives

The Honorable John R. Carter

Chairman

Subcommittee on Military Construction, Veterans Affairs, and Related Agencies

Committee on Appropriations

House of Representatives

The Honorable Mariannette Miller-Meeks

Chairwoman

Subcommittee on Health

Committee on Veterans’ Affairs

House of Representatives

The Honorable Jen Kiggans

Chairwoman

Subcommittee on Oversight and Investigations

Committee on Veterans’ Affairs

House of Representatives

The Honorable Jack Bergman

House of Representatives

The Department of Veterans Affairs’ (VA) Enrollee Health Care Projection Model (EHCPM) projects enrollment, utilization, and costs for the enrolled veteran population in more than 140 categories of health care services 20 years into the future. In fiscal year 2025, the EHCPM supported approximately 89 percent of the VA medical care budget.

We performed our work at the initiative of the Comptroller General. In this report, we

1. describe Veterans Health Administration’s (VHA) current process for updating the actuarial model used to estimate its health care funding needs;

2. examine the extent to which VHA’s processes for developing VA’s health care model estimates align with relevant standards, including actuarial standards of practice and federal internal control standards; and

3.

examine VHA’s oversight of the performance of its actuarial consultant.

Data Used and Data Reliability

Our review uses the following information from VHA:

· VHA’s annual actuarial report for base years 2021 through 2023 that describes the methodology, supporting analyses, and assumptions for the EHCPM.

· VHA model risk assessment report that identifies sources of risk and uncertainty for the projections supporting the VA health care budget.

· Budget impact analyses for fiscal years 2022 through 2025 that presents the specific characteristics of the scenario used for that year’s EHCPM.

To assess the reliability of these data, we reviewed VHA documentation, conducted electronic and manual testing of the data, and interviewed VHA officials responsible for maintaining the data. We found the data sufficiently reliable for our purposes of examining the extent to which VHA’s processes for developing VA’s health care model estimates align with relevant standards.

Methodology

To describe VHA’s current process for updating the actuarial model used to estimate its health care funding needs, we reviewed documentation provided by VHA and its actuarial consultant, Milliman, describing the actuarial model update process, including procedures such as adjusting for discrepancies between actual workload (i.e., utilization of services) and model estimates. We also interviewed and reviewed written responses from VHA’s Office of Enrollment and Forecasting (E&F) and VHA’s Office of Finance.[50]

To examine the extent to which VHA’s processes for developing VA’s health care model estimates align with relevant standards, including actuarial standards of practice and federal internal control standards, we reviewed and analyzed the extent to which VHA’s modeling processes for projecting future health care demands follow selected key practices and standards.[51] Additionally, we reviewed actuarial documents and other modeling documents provided by E&F.[52] We also reviewed the cost projections for fiscal years 2022 through 2027 developed for E&F by its actuarial consultant. We reviewed data sources used for developing the cost projection.

To evaluate the actuarial modeling process, we reviewed E&F documents about the actuarial assumptions and methods E&F used to develop the 20-year projection of future health care service costs. We reviewed a model risk assessment report that identifies sources of risk and describes the degree of uncertainty for the projections supporting the VA health care budget. In addition, we reviewed the morbidity and reliance model adjustments for veteran reliance and utilization of VHA services. Further, we reviewed the E&F model’s use of external data including data from other government agencies, such as the Department of Defense and U.S. Census. We assessed these processes against eight relevant actuarial standards of practice.[53] We also identified five federal internal control standards that were relevant to our work.[54] We selected these standards because they describe the procedures an actuary should follow when performing actuarial services and identify what the actuary should disclose when communicating the results of those services. Finally, we interviewed VHA officials and VHA’s actuarial consultant on the development and validation of the model and how the model’s outputs are used to support VHA’s budget formulation for veteran health care.

We interviewed VHA officials from E&F about their processes for communicating data quality and limitations. We also interviewed or received written responses from officials in VA’s Office of Actuarial Services, as well as key program offices including the Office of Integrated Veteran Care; Office of Productivity, Efficiency and Staffing; Pharmacy Benefits Management Services; Prosthetics and Sensory Aids Service; and officials from the Veterans Benefit Administration regarding their involvement in VHA’s budget development process.[55]

We examined VA’s actuarial consultant’s role in the actuarial modeling processes in the context of actuarial standards of practice. Our actuarial work on this engagement was conducted by a GAO Assistant Director and Actuary and GAO’s Chief Actuary (identified in the Staff Acknowledgment section of this report), who meet the qualification standards of the American Academy of Actuaries to conduct the actuarial aspects of our work for this report. While we conducted actuarial reviews of models and processes, we did not evaluate the accuracy of VHA’s projections or their underlying assumptions, as that type of analysis was outside the scope of this report.

To examine VHA’s oversight of the performance of its actuarial consultant, we reviewed VA documentation, including VHA’s standard operating procedure and quality assurance surveillance plan for assessing contractor performance, the Actuarial Support Services contract and performance work statement, as well as documentation related to oversight activities including contractor performance reviews, reviews of the actuarial consultant’s invoices, and the contractor performance assessment report. To understand the processes in place to monitor and assess contractor performance, we interviewed or received written responses from officials in VHA’s E&F and Office of Finance, and VA’s Office of Management, Office of Actuarial Services, and the Strategic Acquisition Center.[56] We also reviewed documentation and information from VHA officials regarding how oversight responsibilities are defined and executed in relation to tasks and deliverables outlined in the performance work statement. We assessed these oversight practices against the Federal Acquisition Regulation, and VA Acquisition Regulation in the context of federal internal control standards for information and communication.[57]

Limitations

In performing this analysis, we relied on actuarial reports and documentation provided by E&F. We reviewed the documents for reasonableness, but did not audit them for accuracy. We performed all reviews in accordance with actuarial principles and relevant Actuarial Standards of Practice (Actuarial Standards Board), including Actuarial Standard of Practice No. 12, Risk Classification; Actuarial Standard of Practice No. 23, Data Quality; Actuarial Standard of Practice No. 25, Credibility Procedures; Actuarial Standard of Practice No. 41, Actuarial Communications; and Actuarial Standard of Practice No. 56, Modeling. To the extent that there are material deficiencies in completeness and accuracy in E&F’s actuarial reports, the cost estimates may be materially different from those shown in the report had these deficiencies not been present. This review is not a technical review, and we did not verify the accuracy of the calculations performed by the third-party actuaries.

We conducted this performance audit from November 2024 to June 2026 in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

We identified actuarial standards of practice relevant to the Enrollee Health Care Projection Model (EHCPM), the actuarial modeling that the Veterans Health Administration (VHA) uses to inform the Department of Veterans Affairs’ budget estimates for health care services. Table 1 lists relevant actuarial standards of practice we identified, along with examples from the actuarial consultant’s work.

Table 1: Actuarial Standards of Practice Relevant to Enrollee Health Care Projection Model (EHCPM) Modeling and Examples of How the VHA’s Work Addresses Those Standards

|

Actuarial standards of practice |

Examples from EHCPM work |

|

Incurred Health and Disability Claims (No. 5): Provides guidance for estimating health care claims. The standard states an actuary should make a reasonable effort to understand changes in plan provisions or business practices and consider how such changes are likely to affect projections of claims costs. This standard also states that an actuary should consider including economic influences, among other things, in projecting claims. |

According to the Veterans Health Administration (VHA), its actuarial consultant estimates the Department of Veterans Affairs’ (VA) community care claims and adjustments to utilization projections that reflect the effects of changing economic conditions over time. For example, during the unit cost and budget reconciliation process for community care services the unit cost reconciliation adjustment loads in certain administrative components of the unit costs. Unit costs for these services are developed using the claims costs on the baseline data, since source data lacks the administrative costs. As part of the model update, VHA’s actuarial consultant confirms the total claims cost on the baseline data is close to the actual obligations once the delivery operations billing and processing costs, care coordination costs, and the proportional distribution of national overhead are accounted for. |

|

Risk Classification (No. 12): Provides guidance for designing, reviewing, and changing risk classifications. This standard defines risk classification as a system used to assign the individuals into groups intended to reflect the relative likelihood of expected outcomes. The standard states that when selecting which risk characteristics to use in a risk classification system, the actuary should consider the relationship of risk characteristics and the expected outcomes. |

According to VHA, its actuarial consultant classifies veteran enrollees based on their risks in terms of the expected cost of providing VA health care coverage or services. As a result, the EHCPM projects enrollment, utilization, and unit costs for VHA health care services based on veteran enrollee characteristics, including age, gender, priority group, period of service, and geographic location. For example, Vietnam-era enrollees exhibit higher utilization patterns than non-Vietnam era enrollees for some health care services. |

|

Expert Testimony by Actuaries (No. 17): Provides guidance for giving expert testimonies (e.g., congressional testimony). In offering expert testimony, the actuary should comply with all rules of evidence and procedure, and any other rules applicable in the forum. In addition, the actuary should review and comply with any applicable actuarial standards of practice, the Qualification Standards for Actuaries Issuing Statements of Actuarial Opinion in the United States, and the Code of Professional Conduct. |

VHA’s actuarial consultant provides support to VHA for congressional hearings, as needed. An example was an April 2019 testimony before the Senate Committee on Veterans’ Affairs on implementing the Veterans Community Care Program. During the testimony, VHA’s actuarial consultant provided the description of EHCPM, disclosed some of the assumptions used in the model, and discussed how the VA Maintaining Internal Systems and Strengthening Integrated Outside Networks Act of 2018 might affect veterans’ reliance on VHA health care and projected obligations. |

|

Data Quality (No. 23): Provides guidance for (1) selecting the data that underlie the actuarial work product; (2) relying on data supplied by others; (3) reviewing data; (4) using data; (5) preparing data to be used by other actuaries in an actuarial work product; and (6) making appropriate disclosures with regard to data quality. |

According to VHA, its actuarial consultant reviews the reasonableness (e.g., consistency with past data) of data used for modeling, including both the VA data and other external data. |

|

Credibility Procedures (No. 25): Provides guidance for selecting or developing credibility procedures and the application of those procedures to sets of data. |

According to VHA, its actuarial consultant considers the credibility of data (i.e., the extent to which data can be relied on to predict trends and explain veterans’ behavior) when developing adjustments for enrollment rates, morbidity, reliance, unit costs, and other factors used in the actuarial modeling. For example, adjustments for veteran enrollment rates are developed based on priority rating, a 5-year age band (e.g., 30 to 34 years of age), and a geographic area, such as a sector—the smallest geographic location considered by the EHCPM, which consists of one or more contiguous counties. Because too few veterans may be within a particular priority group or 5-year age band living in a particular sector, VHA’s actuarial consultant develops enrollment rates using a blend of rates from the sector level, which has low credibility, and from larger geographic locations, including the area covered by a regional Veterans Integrated Service Network, to improve the data credibility. |

|

Actuarial Communications (No. 41): Provides guidance for preparing actuarial communications, including those that may be required by other actuarial standards of practice. The performance of a specific actuarial engagement or assignment typically requires significant and ongoing communications between the actuary and the intended users regarding the following: the scope of the requested work; the methods, procedures, assumptions, data, and other information required to complete the work; and the development of the communication of the actuarial findings. |

According to VHA, its actuarial consultant communicates the effects of model enhancements resulting from the annual update of the EHCPM. Briefings are provided for internal and external budget stakeholders, which include communicating the assumptions in the current budget scenario and enhancements to the newly updated EHCPM. These briefings include information on how updates and enhancements to the model and material changes to the assumptions between the current budget scenario and the previous budget scenario affected projected spending for a particular year or years in the future. In addition, the annual EHCPM report documents model updates, including enhancements and changes to assumptions. |

|

The Use of Health Status Based Risk Adjustment Methodologies (No. 45): Provides guidance for applying health status-based risk adjustment methodologies to quantify differences in relative health care resource use due to differences in health status. |

According to VHA, its actuarial consultant uses non-VA utilization benchmarks developed for commercial and Medicare markets when projecting utilization for many VA health care services. The actuarial consultant adjusts these benchmarks to account for differences in the morbidity, or health status, of the veteran enrollee population compared to the commercial and Medicare populations. |

|

Modeling (No. 56): Provides guidance to actuaries when performing actuarial services with respect to designing, developing, selecting, modifying, using, reviewing, or evaluating models. |

According to VHA, its actuarial consultant works with VHA in ensuring the EHCPM serves its intended purpose, selecting relevant data used for projections, setting assumptions, and developing projections of veteran health care costs. They also review the models including their inputs, calculations, and outputs to ensure the outputs are reasonable and consistent with program office expectations. |

Source: GAO review of VHA’s EHCPM against relevant actuarial standards of practice. | GAO‑26‑107950

Appendix III: VHA’s Actuarial Consultant’s Tasks, Deliverables, and Required Due Dates for the Deliverables

The Veterans Health Administration’s (VHA) actuarial consultant, Milliman, performs its work under an actuarial support services contract, which is managed by VHA’s Office of Enrollment and Forecasting (E&F). As part of the contract, the actuarial consultant is responsible for several tasks as outlined by the performance work statement. The consultant supports VHA in its development of budget estimates, including updating the Enrollee Health Care Projection Model (EHCPM), developing projections for workforce planning, and developing EHCPM briefings for stakeholders, among other things. (See table 2.)

Table 2: Full List of Project Tasks, Deliverables, and Required Delivery Dates for VHA’s Actuarial Consultant as Outlined in the Performance Work Statement, as of April 2025

|

Project task |

Deliverables |

Required delivery date |

|

Enrollee Health Care Projection Model (EHCPM) Project Plan Updates |

Actuarial consultant shall provide a Project Management Plan that lays out the consultant’s approach, timeline, and tools to be used in execution of the contract. |

Monthly |

|

Progress reports |

The actuarial consultant shall provide status reports to the contracting officer’s representative via a joint bi-weekly conference call with the actuarial consultant EHCPM Project Team and the Chief Strategy Office EHCPM Project Team. |

Bi-weekly |

|

Travel and other direct cost reports |

Report with cover sheet containing the actuarial consultant’s name, contract number, purchase order number, invoice number, date, and period of performance covered by the invoice, cost, and travel, and a list of deliverables for the month and cumulative year to date. |

Monthly |

|

Actuarial consulting, modeling, and analyses |

The actuarial consultant shall provide the Department of Veterans Affairs (VA) support to use the EHCPM to assess the impact of an evolving VA health care system and the broader environment, proposed polices, regulations, and legislation, as well as support for the VA medical care budget process, VA leadership, and stakeholders including the Office of Management and Budget (OMB), Congress, the GAO, Congressional Budget Office, and the Veteran Service Organizations. At the direction of the contracting officer’s representative, the actuarial consultant shall provide documentation that includes data summaries and documentation at a level of detail appropriate for stakeholders and identifies the data, assumptions, and methods used with sufficient clarity that another actuary qualified in the same practice area could evaluate the reasonableness of the actuary’s work. |

Ongoing |

|

Special analyses |

This task provides for consultation to meet VA’s needs for special analyses. Tasks will be defined and accomplished with internal or external workgroups led by VA staff. VA staff that have clinical and programmatic expertise in the task area provide insight into the VA health care system, data, policies, and programmatic guidance. The actuarial consultant shall provide technical and analytical expertise to the workgroup and serve as a member of the workgroup. The workgroup will assess the potential impact on VA and develop assumptions for input into the EHCPM. This consultation will be coordinated by the consultant’s project manager and the VA contracting officer’s representative to support VA staff, specific workgroups or external groups as authorized by VA. |

As requested |

|

VA medical care budget support |

Actuarial consultant shall provide consulting, analyses, modeling, and briefing support to educate VA leadership, the OMB, Congress, the GAO, Congressional Budget Office, Veteran Service Organizations, and other stakeholders regarding the enrollment, utilization, and cost projections supporting the VA medical care budget, including supporting analyses, assumptions, methodology, and key factors driving demand for VA health care. |

Ongoing |

|

EHCPM projection scenarios |

This task permits VA to use the EHCPM to assess the impact of adjusting various model assumptions to support the VA medical care budget; policy analysis; strategic, capital, and workforce planning; or to respond to stakeholder requests. The actuarial consultant shall project enrollment, utilization, and costs that reflect the assumptions specified by VA as directed by the VA contracting officer’s representative. At the direction of the VA contracting officer’s representative, the actuarial consultant shall provide a range of deliverables from each EHCPM scenario depending on the needs of the stakeholder requesting the scenario. |

As requested |

|

Maintain, enhance, and update the EHCPM |

VA requires actuarial consulting and modeling support to maintain, enhance, and annually update the EHCPM. The actuarial consultant shall assume responsibility for the EHCPM at the level of detail and functionality as currently structured. VA will provide the necessary data, documentation of the methodology and assumptions, and the SAS or SQL code that constitutes the 2024 EHCPM (expected to be developed during the final option periods of the existing contract) to the actuarial consultant. The actuarial consultant shall use the current EHCPM as the starting point for updating and producing the 2025 EHCPM. |

April 30 |

|

Maintain, enhance, and update the EHCPM veteran, enrollment, and patient projection models |

The actuarial consultant shall assume responsibility for the EHCPM enrollment model at the level of detail and functionality as currently structured. |

April 30 |

|

Maintain, enhance, and update the EHCPM utilization, unit cost, and cost projection models |

The actuarial consultant shall assume responsibility for the EHCPM utilization, unit cost, and cost models at the level of detail and functionality. VA will provide the necessary data, documentation of the methodology and assumptions, and the SAS or SQL code that constitutes the 2024 EHCPM to the actuarial consultant. The actuarial consultant shall use the current EHCPM as the starting point for updating, enhancing, and producing the EHCPM. The actuarial consultant shall need to propose a comparable methodology and/or benchmarks for the private sector-based utilization projection model in place of those used by the incumbent. |

April 1 |

|

EHCPM documentation and analysis report |

The actuarial consultant provides an accurate, complete report detailing methodology, analyses, assumptions, and data used to develop the updated EHCPM. |

October 30 |

|

Maintain and update the EHCPM global relative value units |

The actuarial consultant shall maintain the proper functioning of the model to conduct analysis, updates, and validate the integrity of the system. The actuarial consultant shall also enhance the system via updates to SAS and SQL coding, etc., to ensure the proper functioning of the model to conduct proper maintenance, analysis, updates, and validate the integrity of the system. The actuarial consultant shall assume responsibility for the EHCPM at the level of detail and functionality as currently structured. |

June 30 |

|

EHCPM projections for strategic, capital, and workforce planning |