Committee on Ways and Means

House of Representatives

United States Government Accountability Office

A report to the Chairman of the Committee on Ways and Means, House of Representatives.

For more information, contact: Alicia Puente Cackley at cackleya@gao.gov.

What GAO Found

The National Association of Insurance Commissioners (NAIC) supports its members—state insurance regulators—in their regulation of insurance companies by

· providing a forum (such as committees, task forces, and working groups) to develop standards for insurance companies through model laws that states may consider enacting (see figure);

· facilitating standardization in monitoring the financial solvency of insurance companies across states through its accreditation program; and

· managing centralized data systems to help states carry out oversight and share information.

Since 1955, NAIC has been excepted from filing Form 990, a type of annual information return that tax-exempt organizations file with the Internal Revenue Service (IRS) unless an exception applies. According to NAIC documents, IRS granted the exception after determining that NAIC meets the exception as a wholly-owned instrumentality of the states, specifically as an organization that carries out functions on behalf of state governments. IRS reaffirmed this exception in 1999 when NAIC reorganized, became a corporation, and reapplied for federal tax-exempt status and a Form 990 filing exception, according to NAIC documentation.

GAO’s review of publicly available NAIC documents found that they included governance and financial information generally comparable to that in Form 990. For example, NAIC reported revenues and expenses in its annual budget and audited financial statements, which its executive committee reviews. NAIC also described its activities and membership structure in annual reports and bylaws.

In some cases, the information NAIC publicly reports is less granular than what Form 990 collects. For example, NAIC’s conflict-of-interest policy describes disclosure requirements for members but not for key employees, such as its chief executive officer. In addition, NAIC did not publicly report compensation for key employees. NAIC’s publicly available information also did not include certain items collected in Form 990, such as information related to fundraising and lobbying.

Why GAO Did This Study

The U.S. insurance industry is primarily regulated by states through state insurance regulators. NAIC is a private, tax-exempt organization whose membership comprises state insurance regulators.

GAO was asked to review NAIC’s role and its history of IRS filing requirements. This report describes NAIC's role in the state regulation of insurance and reviews and compares IRS's applicable filing requirements with what NAIC publicly reports.

GAO reviewed NAIC documents, including annual reports, budgets, and bylaws, and compared NAIC governance and financial information with that required by IRS Form 990. GAO also interviewed representatives of NAIC and IRS. In addition, GAO interviewed a nongeneralizable sample of five state insurance regulators (selected to reflect a range of agency sizes, geographic locations, and other factors) and six stakeholder groups (selected to reflect the perspectives of insurers, state legislators, and consumers).

|

Abbreviations |

|

|

|

|

|

IRS |

Internal Revenue Service |

|

NAIC |

National Association of Insurance Commissioners |

This is a work of the U.S. government and is not subject to copyright protection in the United States. The published product may be reproduced and distributed in its entirety without further permission from GAO. However, because this work may contain copyrighted images or other material, permission from the copyright holder may be necessary if you wish to reproduce this material separately.

June 18, 2026

The Honorable Jason Smith

Chairman

Committee on Ways and Means

House of Representatives

Dear Chairman Smith:

In the United States, the insurance industry is primarily regulated by the states, with each state’s insurance commissioner’s office or similar department responsible for overseeing insurance entities. The National Association of Insurance Commissioners (NAIC) is a private, tax-exempt organization whose membership comprises state insurance commissioners’ offices or departments (state insurance regulators). As of March 2026, state insurance regulators from all 50 states, the District of Columbia, and the U.S. territories were NAIC members.[1]

You asked us to review the role that NAIC plays in the state regulation of insurance and its filing requirements with the Internal Revenue Service (IRS). This report (1) describes NAIC’s role in state regulation of insurance and (2) reviews IRS filing requirements for NAIC and examples of similar organizations and compares NAIC’s publicly reported information with requirements in IRS filings.

For the first objective, we reviewed NAIC governance, financial, and guidance documents, including annual reports, policies, budgets, bylaws, handbooks, manuals, and public information on the activities of its committees. We also interviewed officials from NAIC and the U.S. Department of the Treasury’s Federal Insurance Office, which coordinates federal insurance policy. In addition, we interviewed a nongeneralizable sample of five state insurance regulators, selected to reflect diversity in size, insurance premium volume, and geography.[2] We also interviewed six stakeholder groups, which included industry associations, a national legislative organization, and a nonprofit advocacy group. These stakeholder groups were selected because they represented different types of insurance and had previously participated in NAIC meetings, among other factors.[3] The information gathered from our interviews cannot be generalized to all state insurance regulators or stakeholder groups that interact with NAIC.

For our second objective, we reviewed documentation provided by NAIC on its IRS filing requirements, including documentation related to its Form 990 exception status and IRS private letter rulings.[4] We compared information NAIC disclosed in its governance and financial documents with disclosures required in IRS Form 990. Additionally, we identified four examples of tax-exempt organizations similar to NAIC by analyzing publicly available data from IRS’s August 2025 Exempt Organizations Business Master File Extract and reviewing prior GAO reports.[5] We used the IRS data to determine these organizations’ requirements for filing Form 990. We also used information from NAIC documentation and interviews with IRS officials. For more detailed information about our scope and methodology, see appendix I.

We conducted this performance audit from November 2024 to June 2026 in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

Background

Background

History of the National

Association of Insurance Commissioners

Insurance in the United States is primarily governed by state law, and state insurance regulators carry out regulation and enforcement responsibilities for their state. For example, each state’s insurance regulator licenses insurance companies and agents that do business in their state and reviews insurance product filings and premium rates for approval, as required. Regulators also conduct periodic examinations to monitor insurance companies’ financial solvency, which helps ensure that these companies can pay claims, and to monitor their market conduct.

NAIC was established in 1871 as a support organization for state insurance regulators. While each state establishes its own insurance laws and regulations, regulators needed a forum to discuss common regulatory concerns. NAIC developed resources to support the national system of state-based insurance regulation, including the accreditation program and standardized data collection efforts. As of March 2026, NAIC’s membership included the state insurance regulators from all 50 states, the District of Columbia, and the U.S. territories (American Samoa, Guam, Puerto Rico, U.S. Virgin Islands, and Northern Mariana Islands).

NAIC Committees and Offices

NAIC conducts its work through a member-led committee structure, composed of an executive committee and standing committees. The executive committee also selects the NAIC chief executive officer, who oversees NAIC staff offices that provide support to members.

Executive committee. NAIC is led by an executive committee that helps ensure its business and affairs are consistent with its certificate of incorporation and bylaws.[6] The executive committee identifies organizational priorities and provides recommendations to members related to committee work. It also oversees NAIC’s chief executive officer and staff offices, including revising the annual budget and reviewing senior management compensation.

Standing committees. NAIC established eight standing committees to organize its work.[7] Within these committees, members consider issues such as market regulation and consumer affairs, financial regulation standards, and innovation and technology. Each committee may also establish working groups or task forces to carry out its responsibilities.

NAIC staff offices. NAIC staff offices are managed by NAIC’s chief executive officer, who is selected by and works at the direction of the executive committee. According to NAIC bylaws, the chief executive officer cannot be a state insurance regulator. The offices consist of staff who work for the organization and provide administrative, technical, legal, and other support to NAIC committees and members. For example, NAIC’s legal division supports the accreditation program by reviewing state laws and reporting to the accreditation committee. These staff are not state insurance regulators, and NAIC bylaws outline the various functions in which the staff may be involved. NAIC has staff offices in Washington, D.C.; Kansas City, Missouri; and New York, New York.

NAIC Publications and Meetings

NAIC publishes reports and documents related to its internal governance, data collection efforts, and procedures on its website.[8] These include

· bylaws, certificate of incorporation, conflict-of-interest policy, and committee membership lists;

· annual budgets and annual reports that include audited financial statements; and

· handbooks, manuals, and procedures used as resources for state insurance regulators.

NAIC organizes multiple meetings throughout the year. According to its bylaws, NAIC must hold at least two national meetings each year to, among other things, bring members together to consider and vote on various issues. NAIC committees also hold meetings throughout the year. Some meetings are open to the public, while others are restricted to members.[9] Information and summaries of national and committee meetings are posted on NAIC’s website.[10]

NAIC Interactions with Federal

and Other Entities

NAIC, at the direction of its members, works with federal agencies on insurance-related issues, including flood insurance, terrorism insurance, health insurance, and crop insurance. These agencies include the Federal Insurance Office, Federal Emergency Management Agency, U.S. Department of Health and Human Services, and U.S. Department of Agriculture. For example, NAIC works with the Federal Insurance Office to develop and support the annual collection of insurance company data related to terrorism risk insurance.[11] These data are also provided to state insurance regulators.

NAIC’s executive committee designates a state insurance regulator to serve as a nonvoting member on the Financial Stability Oversight Council, which was created in 2010 to identify and respond to potential risks to the stability of the U.S. financial system, among other responsibilities.[12]

In addition, NAIC and its members work with international insurance regulators on insurance issues. NAIC facilitates and coordinates its members’ interactions with international insurance regulators. For example, NAIC and its members are part of the International Association of Insurance Supervisors, an international standard-setting body composed of insurance regulators from more than 200 jurisdictions. The other U.S. participants are the Board of Governors of the Federal Reserve System and the Federal Insurance Office.

NAIC’s Role in State

Regulation of Insurance

What is NAIC’s role in developing

standards for the insurance industry?

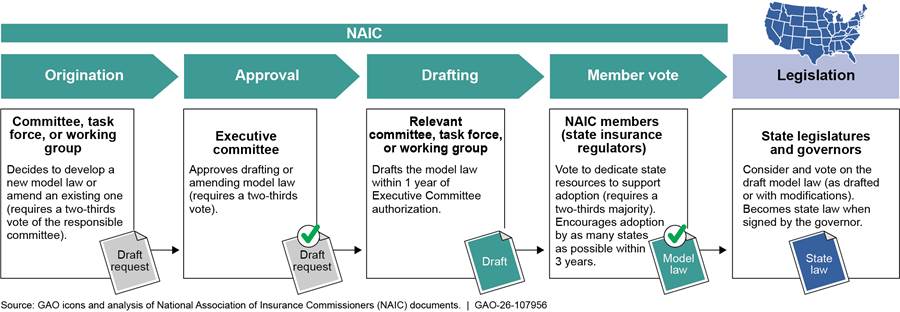

NAIC provides a forum to help its members develop nationwide industry standards in areas where regulatory consistency is needed. NAIC committees develop these standards by drafting model laws—draft legislation intended to be enacted across states.[13] According to NAIC staff, model laws are generally developed around issues where uniformity among state insurance regulators could assist the regulation of financial solvency or market conduct.[14] As part of the drafting process, committees solicit and consider comments from industry, consumer, and other groups, according to NAIC staff. Five of the six stakeholder groups we spoke with noted that they provided feedback to NAIC members on model laws in various ways. Once a model law is drafted, NAIC committees and members may vote to dedicate state resources toward encouraging the passage of the law in each state.

NAIC members then share the model law with their state legislatures, which ultimately decide whether and how to enact it. The model law becomes law only if enacted by a state’s legislature and signed by the governor. Figure 1 provides an overview of the process for developing and adopting model laws.

Note: NAIC committees may also draft model regulations that state regulators may choose to implement through the regulatory rather than the legislative process.

NAIC has drafted model laws to establish insurance industry standards across all insurance lines (including life, health, and property/casualty insurance) and for multiple parties in the insurance industry (such as insurance companies, agents, brokers, and producers). NAIC’s model laws address a range of regulatory areas, including financial solvency, risk management, financial reporting, and consumer protection.[15] For example:

· Risk-Based Capital Model Act: Establishes risk-based capital requirements and regulatory reporting requirements for insurance companies.[16]

· Unfair Trade Practices Act: Prohibits insurance companies and other insurance-related businesses from engaging in misrepresentation, false advertising, and unfair discrimination.[17]

· Producer Licensing Act: Outlines the qualifications and procedures for licensing certain insurance producers.[18]

How does NAIC’s accreditation

program support standardization?

NAIC’s accreditation program seeks to standardize state regulation of insurance by establishing baseline oversight requirements for monitoring insurance companies’ financial solvency.[19] As of March 2026, the state insurance regulators from all 50 states, the District of Columbia, Puerto Rico, and the U.S. Virgin Islands were accredited.

A state insurance regulator becomes accredited when it meets NAIC’s requirements for assessing whether insurance companies are financially solvent and able to pay out claims owed to policyholders. The requirements are broken out into the following categories:

· Model laws. NAIC model laws (or those substantially similar) pertaining to oversight of the solvency of insurance companies must be enacted into state law.[20] These model laws also require state insurance regulators to follow certain NAIC manuals and procedures, such as NAIC’s accounting procedures, valuation standards, and formats for collecting financial information from insurance companies.[21] In addition, they require state insurance regulators to periodically examine all licensed insurance companies but allow regulators to rely on examinations conducted by another accredited state insurance regulator.[22]

· Regulatory practices and procedures. Regulatory practices and procedures must be in place to support state insurance regulators’ oversight of insurance companies’ financial solvency. For example, state insurance regulators need to have sufficient qualified staff to assess insurance companies’ financial health and establish procedures for supervisory review of examination findings. These accreditation practices and procedures also include following certain NAIC handbooks and formats for documenting examination findings.[23]

· Organizational personnel and practices. Practices must be in place for establishing minimum educational and experience requirements for personnel and to provide necessary training for personnel responsible for financial surveillance and regulation.

· Primary licensing, redomestication, and change-of-control procedures. State regulators must have sufficient qualified staff and internal procedures related to licensing new insurance companies or companies looking to transfer their incorporation to another state (known as redomestication).

NAIC staff, an independent team of consultants, and committee members review whether a state insurance regulator meets these requirements for initial and continued accreditation, according to the NAIC accreditation handbook. To determine initial accreditation status and every 5 years thereafter, NAIC staff complete a legal and on-site review. Additionally, the state insurance regulator completes an interim review annually based on NAIC guidelines to evaluate its accreditation status, according to NAIC’s accreditation handbook:

· Legal review. NAIC’s legal division assesses whether state regulators meet the model law and regulation requirements.

· On-site review. An independent team of consultants examines a sample of the regulator’s reports and financial analysis files and interviews regulators’ staff to determine whether the required procedures and practices are in place.[24]

· Interim reviews. Every year, state insurance regulators complete an NAIC self-evaluation guide that asks about any changes to laws, regulations, or procedures required for accreditation. NAIC staff review the self-evaluation and provide a summary of the findings to the accreditation committee.

The NAIC committee responsible for the accreditation program considers findings from initial reviews to determine whether the state insurance regulator should be accredited. For subsequent reviews that occur every 5 years, the committee also considers the findings from the legal and on-site reviews to determine whether the state insurance regulator should remain accredited. NAIC does not make these findings public, and NAIC staff noted that committee discussions are limited to regulators.

If requirements are not met, NAIC may suspend or revoke a state insurance regulator’s accreditation status.[25] According to NAIC staff, seven state insurance regulators have had their accreditation status suspended since the program’s inception in 1990 and five were reaccredited within 2 years of suspension. Examples of reasons for suspension include not having the required model laws in place and noncompliance with examination or financial analysis standards. As previously noted, all state insurance regulators were accredited as of March 2026. NAIC publicly posts which regulators have had their accreditation status suspended or revoked under certain circumstances and removes the name of the regulator from the list of accredited jurisdictions, according to NAIC staff.[26] Additionally, regulators may publicly acknowledge a change in their accreditation status.

The five state insurance regulators we interviewed identified benefits from the standardization of insurance regulation through the accreditation program. For example, they said the accreditation program allows them to rely on other accredited regulators’ assessments of an insurance company’s financial health because those regulators meet NAIC oversight standards. In addition, they noted cost savings from being able to accept an examination completed by another accredited regulator rather than conducting a separate examination themselves. If a state insurance regulator was not accredited, other regulators might not trust the quality of its financial solvency oversight and examinations, according to state officials. As a result, each regulator might need to conduct an additional, potentially duplicative financial solvency examination of those insurance companies, increasing regulatory costs.

Two industry associations whose representatives we interviewed also identified benefits to the accreditation program. In particular, they noted that it reduces insurance companies’ regulatory burden because they generally need to respond only to one state regulator rather than regulators in each state in which they operate.

State insurance regulators also identified challenges with the accreditation program. For example, three regulators noted challenges meeting the organizational personnel requirement to maintain sufficient and qualified staff because of shrinking budgets or competition with the private sector for this type of talent. Two of these regulators noted that a lack of qualified staff also affected its ability to complete planned examinations and meet other examination-related standards to maintain accreditation. Lastly, one regulator noted meeting the requirement that certain model laws be enacted can be difficult because it can take years for a model law to become state law, particularly if the legislature meets infrequently or makes substantial changes to the model law language.

What is NAIC’s role in collecting

information to assist with state regulation of insurance?

NAIC manages centralized data systems that collect information from state insurance regulators and insurance companies. These systems help regulators fulfill oversight responsibilities and share information. According to NAIC, some of these data collection efforts are codified in state law. For example, laws required for accreditation may include requirements for insurance companies to file financial statements with NAIC.[27] NAIC also receives fees from insurance companies that submit data and from licensing and selling these data to third parties as part of its role as a central repository of information.

NAIC has created several data collection systems and resources to assist state insurance regulators, including:

· Interstate systems. These systems help regulators communicate and share regulatory information. For example, the Financial Exam Electronic Tracking System allows regulators to share their examination reports with each other. Two regulators we interviewed also noted that the Regulatory Information Retrieval System, which contains records of regulatory actions taken against insurance companies in different states, helped them proactively identify issues.

· Regulatory back-end systems. These systems help regulators perform day-to-day responsibilities, such as tracking consumer complaints, reviewing rate changes, and collecting taxes. For instance, the System for Electronic Rate and Form Filing is a centralized online platform through which insurance companies submit rate and form filings for regulatory review and approval. Three regulators told us that this system has helped streamline and expedite their reviews and that electronic filings allow them to run queries and reports across all filings to gain additional insights.

· Analyses. NAIC provides oversight resources and reports based on industry data to support regulatory oversight. For example, NAIC’s financial analysis solvency tools, such as company profiles and financial condition ratios, use information from insurance company filings stored in NAIC’s financial data repository. NAIC also collects and analyzes information on insurance companies’ securities holdings to assign a measure of investment risk, called an NAIC designation.[28] Regulators use these designations to assess insurance companies’ financial condition, particularly whether they can cover potential claims and remain solvent. All five regulators we interviewed said they rely on these analytical tools in their regulatory work, such as identifying troubled companies and focusing resources to monitor them. They also noted that NAIC staff expertise is helpful in technical areas such as securities valuation.

In 2024 (the most recent year actual revenue figures were available at the time of our analysis), approximately 94 percent of NAIC’s revenue came from fees paid by insurance companies to submit data to NAIC or from organizations that purchased NAIC data or used NAIC’s data systems.[29] For example, insurance companies pay a fee to file their financial statements with NAIC that is based on their premiums.[30] In addition, according to NAIC staff, NAIC sells nonconfidential data from its financial data repository to the public, including third party vendors that may redistribute the data, researchers, and academics.[31] According to NAIC’s budget documents, the revenue generated from filings supports the financial solvency monitoring tools provided to its members. Insurance companies also pay fees for NAIC to evaluate certain investment securities and assign NAIC designations and to use NAIC’s regulatory back-end systems.

NAIC’s IRS Filing Requirements

and Publicly Reported Information

What are IRS’s filing

requirements for tax-exempt organizations?

Tax-exempt organizations are required to file a Form 990-series information return or notice annually with IRS unless an exception applies.[32] Form 990 collects information about a tax-exempt organization’s mission, activities, governance, and finances, including

· information on the organization’s mission and accomplishments of its largest programs;

· governance information, such as the number of voting members of the governing body, the presence of various governance policies (e.g., whistleblower policies), and disclosure practices;

· compensation paid to key employees, officers, and directors; and

· financial information, including revenue, expenses, and assets.

Tax-exempt organizations use the Form 990-series returns to provide IRS with information required by the Internal Revenue Code.[33] The public may also rely on Form 990 or Form 990-EZ to obtain information on a particular tax-exempt organization, as stated in IRS’s Form 990 instructions.

The Form 990 filing exception applies to certain types of organizations, including

· governmental organizations and affiliates of governmental organizations (including wholly-owned instrumentalities of one or more states),[34] and

· churches.[35]

An organization that is excepted from the Form 990 filing requirement may request a ruling or determination from IRS confirming that it meets the requirements for the exception, but it is not required to do so.[36]

Under the Internal Revenue Code, tax-exempt organizations must make their Form 990 and their application for federal tax-exempt status available to the public.[37] Organizations must indicate in their Form 990 how they made these documents available (e.g., by posting them on their websites). In addition, IRS makes redacted copies of written determinations regarding Form 990 filing exceptions publicly available.[38]

What are NAIC’s IRS filing

requirements?

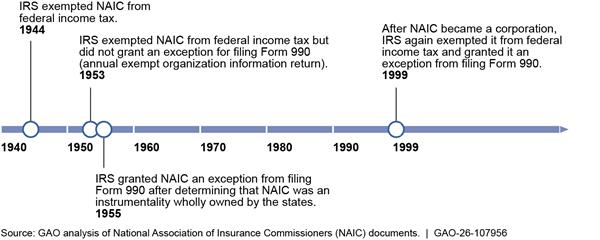

NAIC has been excepted from filing Form 990 since 1955 (see fig. 2), according to our review of NAIC’s tax-exemption application documents provided by NAIC. In these documents, IRS reaffirmed this exception in 1999 when NAIC reorganized, became a corporation, and reapplied for federal tax-exempt status and a Form 990 filing exception. NAIC is not required to file Form 990 because, according to NAIC documents, IRS determined in both 1955 and 1999 that NAIC was an instrumentality wholly owned by the states after it requested an exception from the filing requirement.[39] According to NAIC documents, for both requests, NAIC and its members provided information to IRS indicating that NAIC performed a governmental function on behalf of the states.

Note: IRS recognizes an organization’s exempt status if it meets specified eligibility criteria. See, e.g., 26 C.F.R. § 1.501(c)(3)-1(f)(1). NAIC is excepted from filing Form 990, which is a type of annual information return that tax-exempt organizations must file with the Internal Revenue Service (IRS) unless an exception applies. IRS considers certain criteria to determine whether an organization is an instrumentality wholly owned by the states, including whether the organization performs a governmental function on behalf of one or more states or political subdivisions.

What are the IRS filing

requirements for examples of organizations similar to NAIC?

We identified four illustrative examples of tax-exempt organizations similar to NAIC that are national organizations and conduct activities that support their state members.[40] Of these four organizations, all except the National Association of Attorneys General were required to file Form 990, according to IRS’s August 2025 exempt organizations data.[41]

These examples were identified using the August 2025 IRS exempt organization data and background research. Specifically, we identified one organization (National Association of Attorneys General) that was classified in a similar manner to NAIC in the IRS data and consisted of state regulators.[42] We identified the other three organizations by reviewing publicly available information and prior GAO reports for organizations whose members included state regulatory agencies and served a coordination role with a federal government entity. We identified the following four examples:

· The National Association of Attorneys General convenes state attorneys general, facilitates discussion and information sharing among its members, and provides members with technical resources and training.

· The North American Securities Administrators Association and the Conference of State Bank Supervisors consist of securities and banking regulators, respectively, from all U.S. states and serve as nonvoting members of the Financial Stability Oversight Council, similar to NAIC. Both organizations also provide forums for state members to share information and coordinate regulatory activities.

· The Money Transmitter Regulators Association convenes money transmitter regulators from states and territories. It provides a forum to exchange information among regulators’ staff, develops uniform examination standards, and offers educational opportunities.

What information collected by

Form 990 does NAIC make publicly available?

What information collected by

Form 990 does NAIC make publicly available?

NAIC generally provides publicly available information similar to information collected by Form 990, according to our review of available NAIC documentation.[43] For example, NAIC generally publishes governance and financial information in documents available online, including its certificate of incorporation, bylaws, annual reports, budgets, and audited financial statements. In particular, NAIC reports revenues and expenses in its annual audited financial statements and budgets, which are reviewed by NAIC’s executive committee. Additionally, NAIC describes its mission, activities, and membership structure in annual reports, bylaws, and certificate of incorporation.

In some cases, the information NAIC publicly reports is not as granular as the information Form 990 collects. For example:

· Governance policies. The Form 990 section on governance policies asks organizations to disclose conflict-of-interest policies applicable to key employees. Although NAIC’s conflict-of-interest policy is public and describes disclosure requirements for members, we could not find public information on requirements for key employees, such as the chief executive officer and other top management officials referenced in Form 990. NAIC staff told us that NAIC’s employee handbook includes a conflict-of-interest policy for employees covering issues such as accepting gifts, awarding contracts, and insider trading. In addition, certain employment contracts also include a conflict-of- interest policy. Both of these documents are not publicly available.

· Compensation disclosures. The Form 990 section on compensation requires organizations to disclose compensation for key employees, such as the chief executive officer. Based on our analysis, NAIC does not make this information publicly available, which NAIC staff confirmed. However, NAIC reported total employee salaries in its financial statements and budgets and provides confidential compensation information on key employees to some state and federal agencies.[44] For instance, NAIC is required to provide an annual report to the Michigan state insurance regulator and state legislature that includes such compensation information.[45]

We also could not find publicly available NAIC information on certain items collected in Form 990, including the following:

· Revenue or expense information related to NAIC fundraising or lobbying.

· The method for making NAIC’s tax exemption application available to the public. According to NAIC staff, the application is available upon request by e-mail or as a hard copy at its offices.

· Governance policies such as whistleblower policy and document retention and destruction policies. While IRS’s Form 990 instructions describe these policies as not legally required, they also state that tax-exempt organizations should consider adopting them to help ensure sound operations and compliance with tax law.[46]

Agency and Third Party

Comments

We provided a draft of this report to NAIC and the Department of the Treasury, including IRS and the Federal Insurance Office, for their review and comment. Each of these entities provided technical comments, which we incorporated as appropriate.

We are sending copies of this report to the appropriate congressional committees, the Secretary of the Treasury, and NAIC. In addition, the report is available at no charge on the GAO website at http://www.gao.gov.

If you or your staff have any questions about this report, please contact me at cackleya@gao.gov. Contact points for our Offices of Congressional Relations and Media Relations may be found on the last page of this report. GAO staff who made key contributions to this report are listed in appendix II.

Sincerely,

Alicia Puente Cackley

Director, Financial Markets and Community Investment

This report (1) describes the National Association of Insurance Commissioners’ (NAIC) role in state regulation of insurance and (2) reviews the Internal Revenue Service (IRS) filing requirements for NAIC and examples of similar organizations and compares NAIC’s publicly reported information with requirements in IRS filings.

For the first objective, we reviewed NAIC governance and organizational documents, including annual reports, policies, budgets, and bylaws. These included documents such as NAIC’s 2026 budget, open meeting policy, and committee index and responsibilities.[47] To describe NAIC’s role in developing industry standards and its accreditation program, we also reviewed NAIC’s list of model laws, accreditation handbook, and manuals related to accounting practices and valuation of securities.[48] To describe NAIC’s data collection efforts, we reviewed its technology products and services catalog, data collection tools used to collect financial and market conduct information from insurance companies, and revenue from these efforts reported in NAIC’s 2024 audited financial statements (the most recent year actual revenue figures were available). We also interviewed NAIC staff about how the organization supports state regulation of insurance and interviewed officials from the Department of the Treasury’s Federal Insurance Office, which coordinates federal insurance policy.

In addition, to obtain perspectives from NAIC members, we interviewed staff from a nongeneralizable sample of five state insurance regulators: the Illinois Department of Insurance, Kentucky Department of Insurance, North Dakota Insurance and Securities Department, Vermont Department of Financial Regulation, and Washington Office of the Insurance Commissioner.[49] We selected these regulators to reflect variation in staff size and resources. The selection also reflected variation in the number of insurance companies overseen. Other considerations included the volume of insurance premiums and geographic location. We discussed their interactions with NAIC and perspectives on its role. The information from our interviews cannot be generalized to all state insurance regulators that interact with NAIC.

We also interviewed representatives of six stakeholder groups: three industry groups—the American Property Casualty Insurance Association, Independent Insurance Agents and Brokers of America, and National Association of Mutual Insurance Companies—as well as the National Council of Insurance Legislators (a national legislative organization), the Center for Economic Justice (a nonprofit advocacy group), and the American Consumer Institute Center for Citizen Research (think tank). We selected the stakeholder groups to provide a range of perspectives from insurance market stakeholders, including those representing insurance companies and participants across various types of insurance and roles, state legislatures, and consumers. Other considerations included stakeholder groups’ membership size and prior participation in NAIC meetings. We discussed their perspectives on NAIC’s role in state insurance regulation. The information from our interviews cannot be generalized to all stakeholder groups that interact with NAIC.

For our second objective, we used documentation provided by NAIC and interviewed IRS officials. To describe NAIC’s IRS filing history and requirements, we reviewed documents provided by NAIC. These included NAIC proceedings for NAIC meetings from 1952–1956 and 1999, NAIC’s 1999 application for tax-exempt status, NAIC’s records pertaining to IRS private letter rulings, and IRS guidance on forms related to exception status.[50]

We also analyzed publicly available data from IRS’s Exempt Organizations Business Master File Extract as of August 2025. This dataset contains information on tax-exempt organizations, such as employer identification number, name, classification for tax deduction purposes, and filing requirements for the annual exempt organization return (Form 990).[51] To identify illustrative examples of exempt organizations that may be similar to NAIC, we reviewed 362 organizations that had the same data value as NAIC for the “foundation code” variable in the dataset (i.e., organizations classified as “governmental units”).[52] From these organizations, we searched their names for keywords such as “national,” “North America,” “state,” “regulators,” “supervisors,” or “administrators.” We chose these keywords to help identify entities that consist of state regulators across the United States. Through this analysis, we identified one example of an organization similar to NAIC.

We also reviewed publicly available information from our background research and prior GAO reports to identify additional organizations whose members include state regulatory agencies and that serve a coordination role with a federal government entity, such as the Financial Stability Oversight Council.[53] Through this method, we identified three additional examples of similar organizations to NAIC, bringing the total number of illustrative examples reviewed for this objective to four.[54]

We reviewed the websites of these four organizations to understand their membership structures, geographic coverage, activities, and resources provided to members. We also reviewed the August 2025 exempt organizations data to determine their tax classification and whether they were required to file Form 990. To assess the reliability of the IRS data, we reviewed IRS’s information on the variables of its dataset, conducted electronic data testing, and interviewed IRS officials. We determined the IRS data were sufficiently reliable for the purposes of providing information on the Form 990 filing requirements of selected tax-exempt organizations.

To determine what information NAIC makes publicly available compared with information IRS collects from tax-exempt organizations on Form 990, we identified NAIC documents on its website, including its 2024 annual report and audited financial statements, bylaws, and certificate of incorporation.[55] Our review may not have included all publicly available NAIC information. We compared this information with that required in parts I, III, VI, VII, VIII, IX, X, XI, and XII of IRS’s 2024 Form 990, which request information on organizational activities, governance, management, policies, and finances.[56]

We did not compare NAIC’s publicly disclosed information with the parts of Form 990 that require organizations to complete additional schedules based on specific activities or that request more detailed information on compliance with tax laws or completion of tax forms. Reviewing these would have required knowledge of NAIC’s internal operations and tax compliance history, which were not within the scope of our review.

We conducted this performance audit from November 2024 to June 2026 in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

GAO Contact

Alicia Puente Cackley, cackleya@gao.gov

Staff Acknowledgments

In addition to the contact named above, Nadine Garrick Raidbard (Assistant Director), Christine Ramos (Analyst in Charge), Lauren Capitini, Chelsea Carter, Anna Chung, LaToya Coleman, Jessica Lucas Judy, Jill Lacey, Krista Loose, Marc Molino, Sonya Phillips, Lindsay Shapray, Mary Stack, Jennifer Stratton, and See Yee (Denise) Wong made key contributions to this report.

Tax Administration: Opportunities Exist to Improve Oversight of Hospitals’ Tax-Exempt Status. GAO‑20‑679. Washington, D.C.: September 17, 2020.

Tax Exempt Organizations: IRS Increasingly Uses Data in Examination Selection, but Could Further Improve Selection Processes. GAO‑20‑454. Washington, D.C.: June 16, 2020.

Lender-Placed Insurance: More Robust Data Could Improve Oversight. GAO‑15‑631. Washington, D.C.: September 8, 2015.

Insurance Markets: Impacts of and Regulatory Response to the 2007-2009 Financial Crisis. GAO‑13‑583. Washington, D.C.: June 27, 2013.

Risk Retention Groups: Clarifications Could Facilitate States’ Implementation of the Liability Risk Retention Act. GAO‑12‑16. Washington, D.C.: December 8, 2011.

Consumer Finance: Regulatory Coverage Generally Exists for Financial Planners, but Consumer Protection Issues Remain. GAO‑11‑235. Washington, D.C.: January 18, 2011.

Title Insurance: Actions Needed to Improve Oversight of the Title Industry and Better Protect Consumers. GAO‑07‑401. Washington, D.C.: April 13, 2007.

Insurance Regulation: Common Standards and Improved Coordination Needed to Strengthen Market Regulation. GAO‑03‑433. Washington, D.C.: September 30, 2003.

Insurance Regulation: The NAIC Accreditation Program Can Be Improved. GAO‑01‑948. Washington, D.C.: August 31, 2001.

Regulatory Initiatives of the National Association of Insurance Commissioners. GAO‑01‑885R. Washington, D.C.: July 6, 2001.

Insurance Regulation: Scandal Highlights Need for Strengthened Regulatory Oversight. GAO/GGD‑00‑198. Washington, D.C.: September 19, 2000.

Insurance Regulation: The National Association of Insurance Commissioners’ Accreditation Program Continues to Exhibit Fundamental Problems. GAO/T‑GGD‑93‑26. Washington, D.C.: June 9, 1993.

Insurance Regulation: Weak Oversight Allowed Executive Life to Report Inflated Bonds Values. GAO/GGD‑93‑35. Washington, D.C.: December 9, 1992.

Insurance Regulation: The Financial Regulation Standards and Accreditation Program of the National Association of Insurance Commissioners. GAO/T‑GGD‑92‑27. Washington, D.C.: April 9, 1992.

Insurance Regulation: The Failures of Four Large Life Insurers. GAO/T‑GGD‑92‑13. Washington, D.C.: February 18, 1992.

Insurance Regulation: Assessment of the National Association of Insurance Commissioners. GAO/T‑GGD‑91‑61. Washington, D.C.: July 29, 1991.

Insurance Regulation: Assessment of the National Association of the Insurance Commissioners. GAO/T‑GGD‑91‑37. Washington, D.C.: May 22, 1991.

Insurance Regulation: The Insurance Regulatory Information System Needs Improvement. GAO/GGD‑91‑20. Washington, D.C.: November 21, 1990.

Insurance Regulation: Problems in the State Monitoring of Property/Casualty Insurer Solvency. GAO/GGD‑89‑129. Washington, D.C.: September 29, 1989.

The Government Accountability Office, the audit, evaluation, and investigative arm of Congress, exists to support Congress in meeting its constitutional responsibilities and to help improve the performance and accountability of the federal government for the American people. GAO examines the use of public funds; evaluates federal programs and policies; and provides analyses, recommendations, and other assistance to help Congress make informed oversight, policy, and funding decisions. GAO’s commitment to good government is reflected in its core values of accountability, integrity, and reliability.

Obtaining Copies of GAO Reports

and Testimony

Obtaining Copies of GAO Reports

and Testimony

The fastest and easiest way to obtain copies of GAO documents at no cost is through our website. Each weekday afternoon, GAO posts on its website newly released reports, testimony, and correspondence. You can also subscribe to GAO’s email updates to receive notification of newly posted products.

Order by Phone

The price of each GAO publication reflects GAO’s actual cost of production and distribution and depends on the number of pages in the publication and whether the publication is printed in color or black and white. Pricing and ordering information is posted on GAO’s website, https://www.gao.gov/ordering.htm.

Place orders by calling (202) 512-6000, toll free (866) 801-7077,

or

TDD (202) 512-2537.

Orders may be paid for using American Express, Discover Card, MasterCard, Visa, check, or money order. Call for additional information.

Connect with GAO

Connect with GAO on X,

LinkedIn, Instagram, and YouTube.

Subscribe to our Email Updates. Listen to our Podcasts.

Visit GAO on the web at https://www.gao.gov.

To Report Fraud, Waste,

and Abuse in Federal Programs

Contact FraudNet:

Website: https://www.gao.gov/about/what-gao-does/fraudnet

Automated answering system: (800) 424-5454

Media Relations

Sarah Kaczmarek, Managing Director, Media@gao.gov

Congressional Relations

David A. Powner, Acting Managing Director, CongRel@gao.gov

General

Inquiries

[1]Specifically, an NAIC member is the head official of a state insurance regulator that is charged by law with the principal responsibility of supervising insurance within their state, according to NAIC’s certificate of incorporation.

[2]The state insurance regulators we interviewed were the Illinois Department of Insurance, Kentucky Department of Insurance, North Dakota Insurance and Securities Department, Vermont Department of Financial Regulation, and Washington Office of the Insurance Commissioner.

[3]The stakeholder groups we interviewed were the American Consumer Institute Center for Citizen Research, American Property Casualty Insurance Association, Center for Economic Justice, Independent Insurance Agents and Brokers of America, National Association of Mutual Insurance Companies, and National Council of Insurance Legislators.

[4]Tax-exempt organizations are required to file a Form 990-series information return or notice annually with IRS unless an exception applies. 26 U.S.C. § 6033(a)(1), (i); 26 C.F.R. §§ 1.6033-2 and 1.6033-6. The Form 990-series includes Form 990 (Return of Organization Exempt from Income Tax), Form 990-EZ (Short Form Return of Organization Exempt from Income Tax), Form 990-N (e-Postcard), and Form 990-PF (Return of Private Foundation). Organizations determine which form to file based on their foundation status, gross receipts, and total assets. In general, tax-exempt organizations other than private foundations are required to file Form 990 if they have gross receipts of at least $200,000 or total assets of at least $500,000 at the end of the tax year. Gross receipts represent all sources of revenue, without subtracting any costs or expenses. For the purposes of this report, we focused our review on Form 990.

[5]To assess the reliability of the IRS data, we reviewed IRS documentation on the variables of its dataset, conducted electronic data testing, and interviewed IRS officials. We determined that the IRS data were sufficiently reliable for purposes of providing information on the Form 990 filing requirements of selected tax-exempt organizations.

[6]Only NAIC members may join the executive committee, which consists of NAIC’s officers (president, president-elect, vice president, and secretary-treasurer), the most recent past president, and members from each geographic zone. NAIC’s officers serve 1-year terms and are elected annually by NAIC members.

[7]“2026 Committee and Task Force Structure,” National Association of Insurance Commissioners, accessed Mar. 31, 2026, https://content.naic.org/sites/default/files/committee-structure.pdf. Standing committee members are appointed by the president and president-elect and serve until the succeeding president and president-elect appoint members for the following year. In addition to its eight standing committees, NAIC also has a consumer liaison committee to provide a forum between NAIC members and NAIC consumer representatives.

[8]“Resources for Insurance Industry Insights,” Publications, National Association of Insurance Commissioners, accessed Mar. 31, 2026, https://content.naic.org/publications. NAIC began making all publications publicly available for download free of charge in 2025.

[9]NAIC’s open meeting policy governs how members decide which meetings are open to the public or restricted to members. National Association of Insurance Commissioners, NAIC Policy Statement on Open Meetings (Apr. 1, 2014), https://content.naic.org/sites/default/files/meetings_naic_policy_mtg_801.pdf.

[10]“Proceedings of the NAIC,” Publications, National Association of Insurance Commissioners, accessed Mar. 30, 2026, https://content.naic.org/publications?name=proceedings+of+the+NAIC&field_publication_category_target_id=All.

[11]The Federal Insurance Office Act of 2010, Subtitle A of Title V of the Dodd-Frank Wall Street Reform and Consumer Protection Act, established the Federal Insurance Office in the Department of the Treasury in 2010. Pub. L. No. 111-203, § 502, 124 Stat. 1376, 1580–1589 (2010). The office does not have supervisory or enforcement authority over the insurance industry but has authority to monitor all aspects of the industry. The office also coordinates federal efforts, develops federal policy on prudential aspects of international insurance matters, and represents the United States in the International Association of Insurance Supervisors.

[12]The Dodd-Frank Wall Street Reform and Consumer Protection Act created the Financial Stability Oversight Council. Pub. L. No. 111-203, § 111, 124 Stat. 1376, 1392-1394 (2010). The Secretary of the Treasury chairs the Financial Stability Oversight Council. The act specifies that one of the council’s nonvoting members must be a state insurance commissioner to be designated through a selection process determined by the state insurance commissioners (a process conducted through NAIC). Other nonvoting members of the Financial Stability Oversight Council are the Director of the Office of Financial Research, the Director of the Federal Insurance Office, a state banking supervisor designated by the state banking supervisors (Conference of State Bank Supervisors), and a state securities commissioner designated by the state securities commissioners (North American Securities Administrators Association).

[13]According to NAIC staff, there are multiple ways an NAIC-developed standard may be implemented at the state level, and each state has flexibility in determining how to adopt the standard, such as through the legislative or regulatory process. More specifically, NAIC committees may draft model laws (to be enacted into state law) or model regulations (to be promulgated into regulation by state regulators), depending on several factors. NAIC staff indicated that in some instances, state regulators may choose to promulgate a regulation rather than pursue enactment of a model law. For the purposes of this report, we focus on model laws and their enactment through the legislative process.

[14]NAIC model laws can establish requirements for the insurance industry as well as for insurance regulators. As of 2007, NAIC’s criteria for developing a model law have involved a two-step test: (1) the subject matter must call for a minimum national standard or require uniformity among the states and (2) NAIC must dedicate significant state regulator and NAIC staff resources to supporting the adoption of the model law. If the issue does not meet this test, NAIC can develop a guideline, which is an insurance regulatory best practice.

[15]For the full list of NAIC model laws and related information on state adoption, see National Association of Insurance Commissioners, Model Laws, Regulations, and Guidelines (Spring 2026), Update No. 147 (2026).

[16]National Association of Insurance Commissioners, “Risk-Based Capital (RBC) for Insurers Model Act,” NAIC Model Laws, Regulations, Guidelines, and Other Resources, MO-312 (Jan. 2012).

[17]National Association of Insurance Commissioners, “Unfair Trade Practices Act,” NAIC Model Laws, Regulations, Guidelines, and Other Resources, MO-880 (2024).

[18]National Association of Insurance Commissioners, “Producer Licensing Model Act,” NAIC’s Model Laws, Regulations, Guidelines, and Other Resources, MO-218 (Jan. 2005).

[19]A list of related GAO products is included at the end of this report, including those related to NAIC’s accreditation program.

[20]According to NAIC staff, to assess whether a state law or regulation is “substantially similar” to the model law, NAIC’s legal division evaluates if the requirements are similarly enforced and no less effective than those in the model law. As previously discussed, a state may enact a law or adopt a regulation to meet the model law or regulation drafted by NAIC.

[21]For example, accreditation model laws require state insurance regulators to follow accounting procedures in NAIC’s accounting manual. National Association of Insurance Commissioners, Accounting Practices and Procedures Manual (Mar. 2026).

[22]Specifically, state insurance regulators seeking accreditation must have NAIC’s “Model Law on Examinations” or substantially similar provisions be part of state law. This model law establishes that a state insurance regulator shall, at a minimum, conduct an examination of every insurance company licensed to conduct business in the state every 5 years. In lieu of an examination, a state insurance regulator may rely on an examination report from the regulator of the insurance company’s state of domicile (the state in which the company is incorporated, chartered, or organized) if, among other things, that regulator is accredited. National Association of Insurance Commissioners, “Model Law on Examinations,” NAIC Model Laws, Regulations, Guidelines, and Other Resources, MO-390 (Oct. 1999).

[23]For example, state insurance regulator policies for conducting examinations should generally follow those set forth in NAIC’s examiner handbook. National Association of Insurance Commissioners, Financial Condition Examiners Handbook (2026).

[24]According to the NAIC accreditation handbook, the independent team that conducts the on-site review consists of experts in the insurance industry and at least one disinterested former executive-level regulator.

[25]In addition to suspending or revoking a state insurance regulator’s accreditation status, NAIC may place the regulator on probation and send a letter setting forth corrective actions for the regulator to address.

[26]NAIC’s accreditation handbook states that NAIC will publicly acknowledge that a regulator is no longer accredited if (1) the regulator’s accreditation is suspended or revoked and the regulator does not appeal the decision, or (2) the regulator appeals the accreditation status decision and the decision is upheld. For a list of NAIC’s currently accredited members, see https://content.naic.org/committees/f/financial-regulation-standards-accreditation/accredited-jurisdictions.

[27]NAIC’s accreditation handbook requires state insurance regulators to mandate the filing of annual and quarterly financial statements with NAIC. This requirement may be met—among other ways—through enacting a state law.

[28]NAIC designations measure the likelihood that an insurance company will receive an investment’s full principal and expected interest. There are six NAIC designation categories that indicate the level of investment risk. NAIC’s Purposes and Procedures Manual states that the analysis used to determine NAIC designations is solely for the purpose of designating the quality of an investment made by an insurance company so that NAIC’s members can better identify regulatory treatment. National Association of Insurance Commissioners, Purposes and Procedures Manual of the NAIC Investment Analysis Office (Dec. 2025).

[29]According to NAIC’s 2026 budget, the total actual operating revenues from 2024 (at the time of our analysis) were about $161.4 million.

[30]Database filing fees are calculated using an insurance company’s premiums or reinsurance assumed, multiplied by a base factor, and are subject to a minimum fee and individual and group caps. For 2026, NAIC’s budget notes that the filing fee cap is $108,817 for an individual company and $544,085 for a group.

[31]For information on the financial database products sold by NAIC, see https://content.naic.org/industry/insdata.

[32]26 U.S.C. § 6033(a)(1), (i); 26 C.F.R. §§ 1.6033-2 and 1.6033-6. As previously discussed, the Form 990-series includes Form 990 (Return of Organization Exempt from Income Tax), Form 990-EZ (Short Form Return of Organization Exempt from Income Tax), Form 990-N (e-Postcard), and Form 990-PF (Return of Private Foundation). Organizations determine which form to file based on their foundation status, gross receipts, and total assets. In general, tax-exempt organizations other than private foundations are required to file Form 990 if they have gross receipts of at least $200,000 or total assets of at least $500,000 at the end of the tax year. Gross receipts represent all sources of revenue, without subtracting any costs or expenses. For the purposes of this report, we focused on filing requirements for the Form 990.

[33]See 26 U.S.C. § 6033. A list of related GAO products is included at the end of this report, including those related to tax-exempt organizations and IRS’s use of Form 990. On April 23, 2026, the Department of the Treasury announced that IRS plans to revise Form 990 to improve transparency, strengthen tax administration, and provide clearer reporting on certain activities of tax-exempt organizations described in section 501(c)(3) of the Internal Revenue Code, including government contracts, government grants, and fiscal sponsorship arrangements. According to the announcement, Treasury and IRS will publish proposed regulations and provide an opportunity for public comment before any reporting changes are finalized.

[34]26 U.S.C. § 6033(a)(3)(B) and Rev. Proc. 95-48,1995-2 C.B. 418 provide that governmental units and affiliates of governmental units that are exempt from federal income tax under section 501(a) are not required to file annual information returns on Form 990. For purposes of the Revenue Procedure, governmental units and affiliates encompass state and local governments, tribal governments, political subdivisions and instrumentalities of one or more states. Generally, according to IRS, instrumentalities of states are used for a governmental purpose and perform a governmental function on behalf of one or more states or political subdivisions.

[35]26 U.S.C. § 6033(a)(3), 26 C.F.R. § 1.6033-2(g)(i), and Rev. Proc. 96-10, 1996-1 C.B. 577. This exception also includes integrated auxiliaries of a church and certain church-affiliated organizations. Church-affiliated organizations include those that are exclusively engaged in managing funds or maintaining retirement programs, schools below the college level affiliated with a church, and certain church-affiliated mission societies.

[36]Organizations generally can claim an exception from the Form 990 filing requirement when they apply for recognition of tax-exempt status. Additionally, according to IRS officials, organizations may file Form 8940 to seek a written determination from IRS that they meet the requirements to be excepted from filing Form 990, to obtain greater certainty regarding their compliance obligations. See Rev. Proc. 95-48,1995-2 C.B. 418.

[37]26 U.S.C. § 6104(d)(1)(A). Form 990 must be available for a 3-year period beginning with the due date of the return (including any filing extensions) or, if later, the date it is actually filed. 26 U.S.C. § 6104(d)(2), 26 C.F.R. § 301.6104(d)-1.

[38]26 U.S.C. § 6110, 26 C.F.R. § 301.6110-1. For written determinations open to public inspection, IRS redacts names, addresses, and identifying details, among other information. Certain exclusions may apply. See 26 U.S.C. § 6110(c), 26 C.F.R. § 301.6110-3.

[39]Exceptions from filing are contained at 26 U.S.C. § 6033(a)(3). Under Rev. Proc. 95-48, 1995-2 C.B. 418 (issued pursuant to discretionary authority under 26 U.S.C. § 6033(a)(3)(B)), an organization that is a “governmental unit” or “affiliate of a governmental unit” is not required to file Form 990. An “affiliate of a governmental unit” includes an organization that has a determination that it is a wholly-owned instrumentality of a state or a political subdivision thereof, as defined in sections 3121(b)(7) and 3306(c)(7) of the Internal Revenue Code. IRS Revenue Ruling 57-128, 1957-1 C.B. 311 describes criteria IRS considers in determining whether an organization is an instrumentality wholly owned by one or more states. For example, IRS considers, among other criteria, whether the organization is used for a governmental purpose and performs a governmental function, and whether performance of its function is on behalf of one or more states or political subdivisions, among other factors. For more information on NAIC’s role with state regulation of insurance, see the first objective of this report.

[40]The examples selected are meant to be illustrative and not comprehensive of all entities that may be considered similar to NAIC. See app. I for additional information on our methodology.

[41]The National Association of Attorneys General was one of the 362 organizations with the same tax classification (governmental unit) as NAIC for the “foundation code” variable in the IRS August 2025 exempt organization data. Of these 362 organizations, the National Association of Attorneys General and 108 other organizations were not required to file a Form 990. According to IRS officials, the “foundation code” variable or tax classification is used to help potential donors identify whether donations to an organization may be tax deductible. The “foundation code” variable contains 18 different codes or classifications, including governmental unit, school, church, hospital, and other types of organizations.

[42]In the IRS August 2025 exempt organization data, 362 organizations had the same data value (tax classification) as NAIC for the “foundation code” variable. We reviewed these 362 organizations to identify those with names containing keywords that could signal that the organization consisted of state regulators across the United States (e.g., “national”), and we verified this information by reviewing their websites. Through this review, we identified the National Association of Attorneys General as the only organization that met our criteria.

[43]Our review of publicly available information allowed us to generally identify items required on Form 990, but not all information was available in a single document. For this analysis, we reviewed the most recent available NAIC documents as of 2025. If the required information was not found in those documents, we also reviewed documents for 2023–2024. See app. I for additional information on our methodology.

[44]For example, as an employer, NAIC must file IRS Form W-3 to transmit wage and tax information from employees’ Forms W-2 to the Social Security Administration.

[45]Mich. Comp. Laws § 500.478.

[46]One part of Form 990 asks organizations whether they have certain governance policies. However, a positive response does not necessarily require organizations to disclose such policies publicly. We also did not review parts of Form 990 that require additional schedules based on specific activities, such as lobbying, or that request information on compliance with tax laws.

[47]National Association of Insurance Commissioners, 2026 NAIC Budget (Dec. 2025); National Association of Insurance Commissioners, NAIC Policy Statement on Open Meetings (Apr. 2014); and National Association of Insurance Commissioners, 2026 Charges (Mar. 25, 2026).

[48]Model laws are draft legislation developed by NAIC members and intended to be enacted across states to establish standards and assist with the uniformity of oversight. For the purposes of this report, we focus on model laws and their enactment through the legislative process.

[49]We also selected the New York State Department of Financial Services for our sample, but it did not respond to our requests for an interview.

[50]“Proceedings of the NAIC,” Publications, National Association of Insurance Commissioners, accessed Mar. 30, 2026, https://content.naic.org/publications?name=proceedings+of+the+NAIC&field_publication_category_target_id=All.

[51]The IRS dataset is updated monthly and presents cumulative data. We used August 2025 data because they were the most recent available when we conducted our analysis. The August 2025 dataset contained approximately 1.88 million organizations with unique employer identification numbers. As of March 2026, this number increased to about 1.9 million.

[52]According to IRS officials, the “foundation code” variable or tax classification is used to help potential donors identify whether donations to an organization may be tax deductible. The “foundation code” variable contains 18 different codes or classifications, including governmental unit, school, church, hospital, and other types of organizations.

[53]For examples of prior GAO reports, see GAO, Bank Secrecy Act: Views on Proposals to Improve Banking Access for Entities Transferring Funds to High-Risk Countries, GAO‑22‑104792 (Washington, D.C.: Dec. 16, 2021); Financial Technology: Information on Subsectors and Regulatory Oversight, GAO‑17‑361 (Washington, D.C.: Apr. 19, 2017); Financial Regulation: Complex and Fragmented Structure Could Be Streamlined to Improve Effectiveness, GAO‑16‑175 (Washington, D.C.: Feb. 25, 2016); and Securities Regulation: Factors That May Affect Trends in Regulation A Offerings, GAO‑12‑839 (Washington, D.C.: July 3, 2012).

[54]The four illustrative examples provide context on organizations that may have similar membership structures and conduct similar activities as NAIC. These examples are not intended to be comprehensive.

[55]If we did not find the Form 990 information in the most recent NAIC documents, we also reviewed documents for 2023–2024.

[56]The Form 990-series consists of Form 990 (Return of Organization Exempt from Income Tax), 990-EZ (Short Form Return of Organization Exempt from Income Tax), Form 990-N (e-Postcard), and Form 990-PF (Return of Private Foundation). Organizations determine which form to file based on their foundation status, gross receipts, and total assets. In general, tax-exempt organizations other than private foundations are required to file Form 990 if they have gross receipts of at least $200,000 or total assets of at least $500,000 at the end of the tax year. Gross receipts represent all sources of revenue without subtracting any costs or expenses. In 2024, NAIC’s total revenue and assets were $161.4 million and $275.9 million, respectively. The 2024 version of Form 990 was the most recent version available at the time of our review.