Report to Congressional Committees

United States Government Accountability Office

A report to congressional committees

Contact: Paula M. Rascona at RasconaP@gao.gov

What GAO Found

The Governmentwide Treasury Account Symbol Adjusted Trial Balance System (GTAS) is the central platform federal agencies use to submit standardized data for government-wide financial reporting. GTAS collects budgetary and proprietary data; validates them; and interfaces with other federal systems to support transparency, accountability, and fiscal oversight.

Federal laws, including the Chief Financial Officers Act of 1990, the Federal Financial Management Improvement Act of 1996, and the Digital Accountability and Transparency Act of 2014 (DATA Act), require agencies to report standardized financial data. These laws assign implementation responsibilities to the Office of Management and Budget (OMB) and the Department of the Treasury, which issue guidance on budget formulation, technical instructions on GTAS reporting procedures, U.S. Standard General Ledger crosswalks, and attribute requirements. Together, this guidance governs how agencies complete various accounting, validation, and reporting procedures.

Through a combination of manual and automated interfaces, GTAS exchanges data with fiduciary authoritative source agencies and major government-wide accounting systems, including the following:

· Central Accounting Reporting System (CARS)

· DATA Act Broker

· Government Invoicing (G-Invoicing)

· OMB Max

Why GAO Did This Study

GTAS plays a central role in the financial management and transparency of the U.S. federal government. It supports a wide array of government financial operations, helping to ensure the accurate reporting of intragovernmental transactions, cash flow, and other financial activities. Federal entities use GTAS as a key system to report financial and budgetary execution information to Treasury.

Treasury, in coordination with OMB, uses this information to prepare the annual financial report of the U.S. government. The financial report provides the President, Congress, and the public with a comprehensive view of the federal government’s finances—its revenue, debt, and expenditures.

The Government Management Reform Act of 1994 includes a provision for GAO to annually audit the consolidated financial statements of the U.S. government. Because of the importance of GTAS in preparing these financial statements and ensuring the accuracy and completeness of the data, GAO conducted this review to provide a system overview.

This report describes the (1) laws and guidance relevant to government-wide financial reporting requirements and the use of GTAS for that purpose, (2) major government-wide accounting systems that interface with GTAS, and (3) data flow and validation processes of GTAS.

To address these objectives, GAO reviewed applicable laws, Treasury and OMB guidance, and GTAS system documentation. GAO also discussed GTAS data transmission and validation processes with Treasury officials.

Treasury stated the agency did not have any comments on the report.

|

Abbreviations |

|

|

|

|

|

ATB |

adjusted trial balance |

|

BETC |

business event type code |

|

CARS |

Central Accounting Reporting System |

|

CFO Act |

Chief Financial Officers Act of 1990 |

|

DATA Act |

Digital Accountability and Transparency Act of 2014 |

|

DEFC |

disaster emergency fund code |

|

FFATA |

Federal Funding Accountability and Transparency Act of 2006 |

|

FFB |

Federal Financing Bank |

|

G-BETC |

Governmentwide Treasury Account Symbol Adjusted Trial Balance System business event type code |

|

G-Invoicing |

Government Invoicing |

|

GTAS |

Governmentwide Treasury Account Symbol Adjusted Trial Balance System |

|

NIST |

National Institute of Standards and Technology |

|

OMB |

Office of Management and Budget |

|

OPM |

Office of Personnel Management |

|

SF |

standard form |

|

TAS |

Treasury Account Symbol |

|

TFM |

Treasury Financial Manual |

|

USSGL |

U.S. Standard General Ledger |

This is a work of the U.S. government and is not subject to copyright protection in the United States. The published product may be reproduced and distributed in its entirety without further permission from GAO. However, because this work may contain copyrighted images or other material, permission from the copyright holder may be necessary if you wish to reproduce this material separately.

June 11, 2026

The Honorable Rand Paul, M.D.

Chairman

The Honorable Gary C. Peters

Ranking Member

Committee on Homeland Security and Governmental Affairs

United States Senate

The Honorable James Comer

Chairman

The Honorable Robert Garcia

Ranking Member

Committee on Oversight and Government Reform

House of Representatives

The Governmentwide Treasury Account Symbol Adjusted Trial Balance System (GTAS) plays a central role in federal financial management and transparency. The Department of the Treasury’s Bureau of the Fiscal Service maintains GTAS, which consists of a listing of all general ledger accounts and corresponding balances and supports a wide array of government-wide reporting. Agencies submit data into GTAS for use in various government-wide reporting initiatives, such as the annual financial report of the U.S. government, the President’s budget, and USAspending.gov.[1] Congress relies on information derived from GTAS to facilitate oversight and make informed decisions about spending, and such information promotes transparency of government spending for the public. Due to the considerable role GTAS plays in supporting congressional and public information needs, the integrity of the data it processes and maintains is critical.

GAO annually audits the consolidated financial statements of the U.S. government, consistent with a provision in the Government Management Reform Act of 1994.[2] We conducted this review to provide an overview of GTAS, which federal entities use to report proprietary financial and budgetary execution information. Fiscal Service uses this information to prepare the consolidated financial statements. Further, GTAS information is critical to other key public reports of government budgetary and spending information. This report describes (1) the laws and guidance relevant to government-wide financial reporting requirements and the use of GTAS for that purpose; (2) the major government-wide accounting systems that interface with GTAS; and (3) the data flows into and out of GTAS, and the data validation processes.

To address the first objective, we identified and reviewed the legal requirements for the reporting of agency financial data. We also reviewed applicable Treasury and Office of Management and Budget (OMB) guidance regarding the implementation of GTAS to facilitate government-wide transmission and reporting of financial data.

To address the second objective, we reviewed GTAS documentation, including its system security plan, and relevant Treasury standard operating procedures and interviewed Fiscal Service officials to gain an understanding of GTAS and its system interfaces.

To address the third objective, we reviewed system documentation and relevant Treasury standard operating procedures to gain an understanding of GTAS data transmission, validation, and report-generation processes. We also interviewed Fiscal Service officials to gain an understanding of data validation processes and how data flows into and out of GTAS.

We conducted this performance audit from November 2024 to June 2026 in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

Background

The mission of the Fiscal Service is to promote the financial integrity and operational efficiency of the U.S. government by providing accounting, financing, collections, payments, and shared services. To carry out these functions, Fiscal Service, in collaboration with OMB, has developed accounting and reporting systems to meet the needs of federal government managers, Congress, and the public for data and information about federal spending. Treasury implemented GTAS in fiscal year 2014 to help improve the accuracy and transparency of federal financial data. Fiscal Service plays the central role in operating GTAS, using the system to collect and exchange large volumes of financial and budgetary data that federal agencies report.

Fiscal Service compiled GTAS data for fiscal year 2025 to report $5.2 trillion in total receipts and $7.0 trillion in total outlays in the Monthly Treasury Statement of Receipts and Outlays of the United States Government.[3] GTAS data also supported OMB’s compilation of the fiscal year 2025 President’s budget, which reported estimated fiscal year 2024 receipts of $5.1 trillion and outlays of $6.9 trillion.[4] In addition, GTAS data supported USAspending.gov reporting of $10.3 trillion in obligations and $9.9 trillion in gross outlays for fiscal year 2025.

Laws and Guidance Over Reporting Government-Wide Financial Data Using GTAS

Federal Financial Management Laws Direct Agencies to Submit and Report Financial Information

Several laws have been enacted over time to establish requirements for federal financial reporting, often delegating authority to OMB and Treasury to establish guidance for federal agencies to meet those requirements.

See table 1 for select laws that govern government-wide financial reporting.

|

Law |

Relevant data transmission and reporting requirements |

|

Budget and Accounting Procedures Act of 1950, Pub. L. No. 784, ch. 946, § 114, 64 Stat. 832, 836, codified at 31 U.S.C. § 3513. |

Requires the Department of the Treasury to prepare reports to inform the President, Congress, and the public on the financial operations of the federal government and requires executive agencies to provide Treasury with such reports and information that Treasury may require in order to do so. |

|

Congressional Budget and Impoundment Control Act (July 12, 1974), Pub. L. No. 93-344, Title VIII, § 801, 88 Stat. 297, 327 (1974), codified as amended at 31 U.S.C.§ 1112(b). |

Requires Treasury and the Office of Management and Budget (OMB), in cooperation with GAO, to establish and maintain standardized data processing and information systems for fiscal, budgetary, and program information for use by agencies. |

|

Chief Financial Officers Act of 1990 (CFO Act), Pub. L. No. 101-576, 104 Stat. 2838 codified in relevant part at 31 U.S.C. §§ 503-504, 901-902. |

Requires OMB to establish financial management policies and requirements and to monitor establishment and operation of federal government financial management systems. Establishes an agency chief financial officer position for 23 (now 24) executive agencies, known as “CFO Act Agencies.” The chief financial officer of each such agency shall prepare and transmit an annual financial report to the agency head and to OMB. |

|

Government Management Reform Act of 1994, Pub. L. No. 103-356 § 405(c), 108 Stat. 3410, 3416, codified at 31 U.S.C. § 331(e). |

Mandates the Secretary of the Treasury, in coordination with OMB’s Director, to prepare an audited financial statement covering all accounts and associated activities of the executive branch of the U.S. government. GAO is required to audit the financial statement. |

|

Federal Financial Management Improvement Act of 1996, Pub. L. No. 104-208 Title VIII, §§ 801 et seq., 110 Stat. 3009, 3389-394, codified at 31 U.S.C. § 3512 note. |

Mandates that financial management systems of CFO Act agencies comply substantially with federal financial management system requirements, applicable federal accounting standards, and the U.S. Standard General Ledger at the transaction level. |

|

Federal Funding Accountability and Transparency Act of 2006 (FFATA), Pub. L. No. 109-282, 120 Stat. 1186, codified at 31 U.S.C. § 6101 note. |

Requires OMB to establish a single searchable website that lists specific data for each federal award: name, amount, information, location, unique identifier, and any other relevant information OMB specifies. |

|

Digital Accountability and Transparency Act of 2014 (DATA Act), Pub. L. No. 113-101, 128 Stat. 1146. codified at 31 U.S.C. § 6101 note. |

Expands FFATA by requiring disclosure of federal agency expenditures and linking federal award information to federal agency programs. |

Source: GAO analysis of various laws. | GAO‑26‑107961

OMB and Treasury Issue Guidance to Implement Financial Data Submission and Reporting

OMB Guidance

OMB provides guidance to executive agencies that submit financial data to GTAS for reporting purposes (see table 2).

Table 2: Office of Management and Budget (OMB) Guidance on Use of the Governmentwide Treasury Account Symbol Adjusted Trial Balance System (GTAS)

|

OMB guidance |

Relevant reporting requirements |

|

OMB Circular A-11: Preparation, Submission, and Execution of the Budget (August 2025) |

Informs federal agencies’ accounting office staff that reporting U.S. Standard General Ledger accounting information at the Department of the Treasury account level through GTAS enables inclusion of that information in the Standard Form (SF) 133, Report on Budget Execution and Budgetary Resources. |

|

OMB Circular A-136: Financial Reporting Requirements (July 14, 2025) |

Requires all significant reporting entities to use GTAS to provide fiscal year-end data to the Bureau of the Fiscal Service. All executive branch agencies must use GTAS to submit their preclosing adjusted trial balances, while legislative and judicial branches may use GTAS to submit their adjusted trial balances. |

|

OMB M-18-08: Guidance on Disaster and Emergency Funding Tracking (February 2, 2018) |

Establishes a requirement for executive agencies to report Disaster Emergency Fund Codes (DEFC) to GTAS in the new DEFC Attribute. Each DEFC value must have a self-balancing adjusted trial balance, including data on status of funding. |

|

OMB M-20-21: Implementation Guidance for Supplemental Funding Provided in Response to the Coronavirus Disease 2019 (COVID-19) (April 10, 2020) |

Amends guidance in OMB M-18-08 to use a unique DEFC value to include covered funds in the CARES Act that are not designated as emergency funds. |

|

OMB M-15-12: Increasing Transparency of Federal Spending by Making Federal Spending Data Accessible, Searchable, and Reliable (May 8, 2015) |

Establishes guidance for agencies to carry out current transparency reporting requirements pursuant to the Federal Funding Accountability and Transparency Act of 2006 and new reporting requirements pursuant to the Digital Accountability and Transparency Act of 2014. In addition, the memorandum establishes guidance for continued award-level reporting requirements, new requirements for both agency-level and award-level reporting, and implementation of data standards for data published on USAspending.gov (or its successor site). |

|

OMB Management Procedures Memorandum No. 2016-03: Implementing Data-Centric Approach for Reporting Federal Spending Information (May 3, 2016) |

Guides agencies on how to report appropriations account summary-level and award-level data to USAspending.gov and how to meet the requirement to associate data with an award identification number. It establishes requirements for agencies to submit data via GTAS to OMB, which aggregates and crosswalks the data to produce the SF 133. |

Source: GAO analysis of OMB guidance. | GAO‑26‑107961

Treasury Guidance

Treasury provides guidance and detailed instructions to GTAS users for financial reporting purposes (see table 3).

Table 3: Department of the Treasury Guidance Related to the Governmentwide Treasury Account Symbol Adjusted Trial Balance System (GTAS)

|

Treasury guidance |

Relevant reporting requirements |

|

Treasury Financial Manual, volume 1, part 2, chapter 4700 |

Prescribes how federal entities use GTAS to provide data to the Bureau of the Fiscal Service. |

|

U.S. Standard General Ledger, TFM Supplement, parts 1 and 2, section VII |

Describes GTAS’s validations and edits to ensure consistent reporting of agency trial balances. |

|

Treasury Standard Operating Procedures |

Provides step-by-step instructions and guidance for reporting federal financial data through GTAS and outlines clear steps and tasks for gathering supporting documentation and reporting financial data. |

Source: GAO analysis of Treasury guidance. | GAO‑26‑107961

Major Government-Wide Accounting Systems Interface with GTAS

Data from four major government-wide accounting systems flow to and from GTAS through interfaces, which the National Institute of Standards and Technology (NIST) defines as a “common boundary between independent systems or modules where interactions take place.”[5]

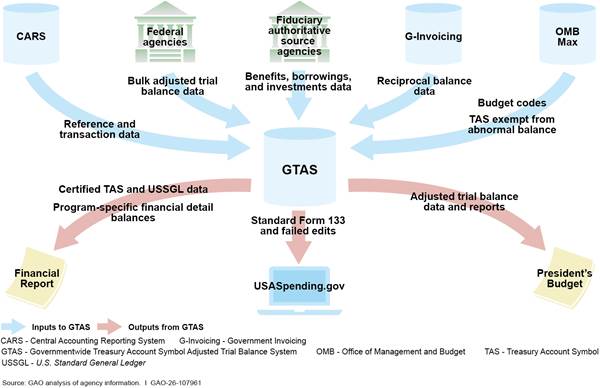

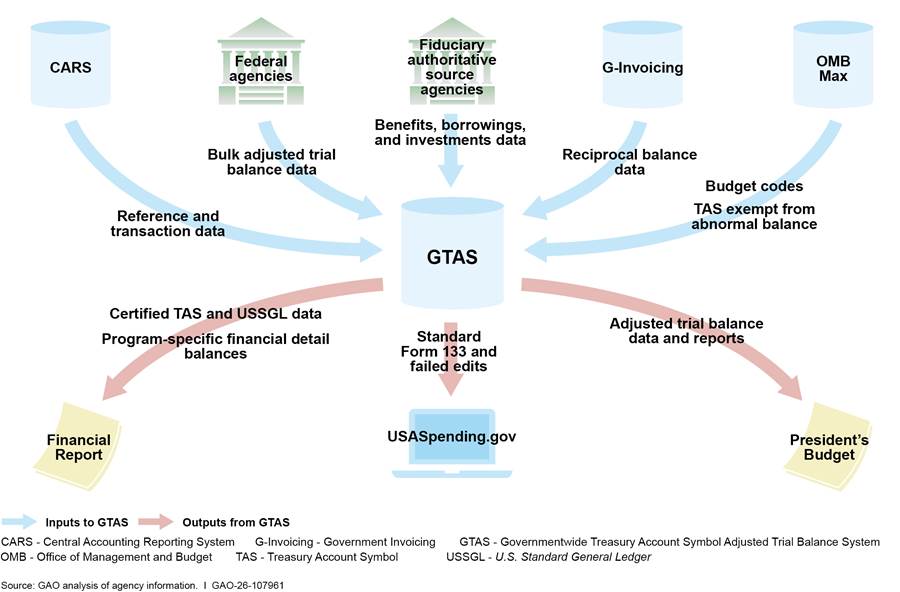

Specifically, GTAS exchanges data with three Fiscal Service-owned systems: (1) the Central Accounting Reporting System (CARS), (2) the DATA Act Broker, and (3) Government Invoicing (G-Invoicing). GTAS also exchanges data with the OMB Max budget system. CARS, G-Invoicing, and OMB Max data are inputs to GTAS, and GTAS data are inputs to CARS, the DATA Act Broker, and OMB Max.

CARS

CARS is the system of record for the government’s financial data and handles accounting and reporting for all federal agencies. CARS also produces and distributes budgetary reports, such as the Monthly Treasury Statement and Combined Statement. CARS supports streamlined agency reporting and government-wide standardization. CARS helps minimize data redundancy and enhances data sharing between the Fiscal Service central accounting system, financial service provider systems, and agency core financial systems. GTAS receives transaction data, Treasury Account Symbols, and business event type codes from CARS, and Fiscal Service uses these data to produce the U.S. government’s cash statement. Appendix I provides details on the types of accounting data that GTAS exchanges with CARS.

DATA Act Broker

Federal agencies are required to report complete and accurate spending data to USAspending.gov, which is a searchable website that displays these data. The DATA Act Broker is a system that collects and validates federal spending data for reporting on USAspending.gov. GTAS transmits data from the Standard Form (SF) 133, Report on Budget Execution and Budgetary Resources, to the DATA Act Broker for publication on USAspending.gov. The DATA Act Broker also performs a validation by checking the data collected from agencies against certain budgetary information obtained from GTAS. Appendix I discusses in more detail the data that GTAS transmits to USAspending.gov via the DATA Act Broker.

G-Invoicing

Federal agencies use G-Invoicing to support accounting for buy/sell transactions with other federal agencies. Agencies’ use of G-Invoicing also facilitates the arrangement and negotiation of interagency agreements and the exchange of buy/sell information. GTAS uses data from G-Invoicing to eliminate intragovernmental transactions when preparing the U.S. government’s financial report. See appendix I for details about how GTAS uses these data to reconcile intragovernmental transactions.

OMB Max

GTAS uses budget execution information from federal agencies along with reference data about apportionments and obligations from OMB Max to produce the SF 133. The SF 133 fulfills the requirements for the President to review federal expenditures at least four times a year and to report on unliquidated obligations, unobligated balances, canceled balances, and adjustments made to appropriations accounts during the completed fiscal year. OMB presents the SF 133 on the OMB Max budget community pages to help facilitate communication among accounting, budget, and audit staff. The same report is also available through OMB’s public website. Appendix I provides details on GTAS’s retrieval of data from OMB Max.

GTAS Data Flows and Data Validation Processes

Data Inflows and Outflows

GTAS functions as a centralized platform for receiving and distributing federal proprietary accounting and budgetary data. GTAS receives data inputs from multiple sources by a variety of methods and generates data outputs to support oversight, reconciliation, and public reporting. The data flow process involves integrating financial information across systems and agencies as it moves into and out of GTAS.

Figure 1 displays a simplified overview of selected data inflows to and outflows from GTAS.

Appendix II discusses in more detail the data inflows to and outflows from GTAS.

Data Validation Processes

Fiscal Service uses validations and edits to verify the integrity of agency data files and attributes and to help improve the consistency of agency GTAS reporting. GTAS performs the validation process for agency bulk adjusted trial balance (ATB) files, applying system-based checks and editing once the files are uploaded.[6] In addition, fiduciary authoritative source agencies validate their own source files for accuracy before emailing them to Fiscal Service. Fiscal Service then uploads those validated files into GTAS for reconciliation. See appendix III for additional details about the GTAS data validation processes.

Agency Comments

We provided a draft of this report to the Department of the Treasury’s Bureau of the Fiscal Service. Fiscal Service did not have any comments on the report.

We are sending copies of this report to the appropriate congressional committees and the Secretary of the Treasury. In addition, the report is available at no charge on the GAO website at https://www.gao.gov.

If you or your staff have any questions about this report, please contact me at RasconaP@gao.gov. Contact points for our Offices of Congressional Relations and Media Relations may be found on the last page of this report. GAO staff who made key contributions to this report are listed in appendix IV.

Paula M. Rascona

Director, Financial Management and Assurance

Table 4 lists systems that interface with the Governmentwide Treasury Account Symbol Adjusted Trial Balance System (GTAS) and the types of data they exchange.

Table 4: Governmentwide Treasury Account Symbol Adjusted Trial Balance System (GTAS) Interfaces and Data Descriptors

|

System |

Purpose |

Data |

Type |

|

Central Accounting Reporting System |

A system of record for federal financial data |

Reference data |

Reference |

|

Treasury Account Symbol and transaction data |

Proprietary |

||

|

GTAS Business Event Type code |

Budgetary |

||

|

DATA Act Broker |

Collects and validates federal spending data for publication on USAspending.gov |

Standard Form (SF) 133 Report on Budget Execution and Budgetary Resources |

Budgetary |

|

SF 133 failed edits |

Reference |

||

|

Government Invoicing (G-Invoicing) |

Manages intragovernmental transactions |

Reciprocal Category balance |

Proprietary |

|

OMB Max |

Gathers and publishes data on federal management and budgeting activities |

Apportionment Category B code |

Reference |

|

Program Report Category code |

|||

|

Budget Object Class code |

|||

|

Disaster Emergency Fund code |

|||

|

Treasury Account Symbol Exempt from abnormal balance |

Source: GAO analysis of Treasury system documentation. | GAO‑26‑107961

GTAS Exchanges Reference, Proprietary, and Budgetary Data with CARS

Federal agencies use the Central Accounting Reporting System (CARS) as an accounting system of record. Fiscal Service staff manually initiate GTAS to retrieve reference data from CARS, and they schedule GTAS to retrieve transaction data from CARS. Reference data include Treasury Account Symbol (TAS) attributes and all permissible values for the attribute (domain values), business lines and business event type codes (BETC), financial reporting entity and type code assignments, and agency identifiers. TASs are identification codes that the Department of the Treasury, in collaboration with the Office of Management and Budget (OMB) and the owner agency, assigns to an individual appropriation, receipt, or other fund account. BETCs indicate the type of reported activity.[7] Together, TASs and BETCs determine the effect a transaction has on the fund balance with Treasury. Transaction data, which are a type of proprietary accounting data, document net outlays and fund balance with Treasury transactions.[8] Treasury uses reference and transaction data to prepare the Financial Report of the U.S. Government.

Fiscal Service staff also schedule GTAS to send supplementary GTAS BETC (G-BETC) data to CARS. G-BETCs are budgetary accounting[9] U.S. Standard General Ledger (USSGL) accounts that are absent from CARS.[10] They detail borrowing and contract authorities and contribute to OMB’s compilation of the President’s budget.

GTAS Exchanges Budgetary and Reference Data with the DATA Act Broker for Publication on USASpending.gov

Federal agencies submit appropriation, obligation, and award financial data to the DATA Act Broker, which in turn presents the data on USAspending.gov.[11] GTAS provides financial data to the DATA Act Broker, which in turn transmits the data to USAspending.gov for publication on the website. The DATA Act Broker also uses data from GTAS to validate agency appropriations before they are presented on USAspending.gov.

GTAS uses federal agency-submitted adjusted trial balance data to produce the Standard Form (SF) 133, Report on Budget Execution and Budgetary Resources. This report lists an agency’s funds statuses and ties an agency’s financial statements to its budget. Bureau of the Fiscal Service staff schedule GTAS to send this report’s data to the DATA Act Broker. If the report contains any failed edits, Fiscal Service staff manually initiate GTAS to send information about the failed edits to the DATA Act Broker. Edits help to ensure that agencies adhere to accounting rules. For example, an edit confirms that a canceled TAS does not have a balance. The DATA Act Broker also validates appropriations account data against the SF 133. These budgetary and reference data contribute to OMB’s compilation of the President’s budget and Treasury’s government-wide reporting on USAspending.gov.

GTAS Exchanges Proprietary Data with G-Invoicing

Federal agencies use Government Invoicing (G-Invoicing) to reconcile intragovernmental transactions, such as documenting support for buy/sell transactions with other federal agencies. Fiscal Service staff manually initiate GTAS to retrieve reciprocal category balance data from G-Invoicing. Reciprocal categories are financial statement line items that are the reciprocal of each other and assist with eliminating intragovernmental transactions at the government-wide level in preparing the U.S. government’s financial report. For example, when two agencies enter into a reimbursable agreement, each agency has a reciprocal accounts payable and accounts receivable that net to zero. Reciprocal category data are proprietary data that contribute to Treasury’s preparation of the Financial Report of the U.S. Government.

GTAS Exchanges Reference Data with OMB Max

OMB uses OMB Max to collect and validate budget information to produce the President’s budget. Fiscal Service staff manually initiate GTAS to retrieve apportionment[12] and obligation data from OMB Max as follows:

· Apportionment Category B code data identify apportionment by program, project, or activity on the SF 132, Apportionment and Reapportionment Schedule;[13]

· Program Report Category code data identify the program report category that an agency uses when reporting obligations in its detailed financial information;

· Budget Object Class code data represent obligations by item or service;

· Disaster Emergency Fund code data identify budgetary line items associated with funding for events such as disasters, emergencies, or wildfire suppression; and

· TAS Exempt from abnormal balance data list TASs that are exempt from the abnormal balance validation of certain budgetary USSGL accounts.

These are types of reference data that contribute to OMB’s compilation of the President’s budget.

Agency Preparers and Fiscal Service Accountants Manually Upload Data into GTAS

Each month, agency preparers upload bulk adjusted trial balance files that detail the financial accounts and amounts for the monthly reporting period. These files include both budgetary and proprietary accounting data and required attributes, such as the Treasury Account Symbols (TAS), U.S. Standard General Ledger (USSGL) accounts, and domain values. Office of Management and Budget (OMB) Circular A-136 requires executive branch agencies to submit preclosing trial balances; in contrast, legislative and judicial branch agencies may submit their preclosing trial balances voluntarily.

On a quarterly basis, fiduciary authoritative source agencies email authoritative source files directly to the Bureau of the Fiscal Service, where accountants upload the authoritative data into the Governmentwide Treasury Account Symbol Adjusted Trial Balance System (GTAS).[14]

Fiscal Service Accountants Manually Generate Information from GTAS

Fiscal Service uses validated and agency-certified data to produce key financial outputs that support government-wide reporting, reconciliation, and oversight. While GTAS automates many processes, Fiscal Service accountants periodically generate specific reports and datasets manually to meet analytical, statutory, or policy needs. These outputs draw from multiple GTAS data sources, feed into other systems, and assist in the preparation of various reports.

The Department of the Treasury’s Fiscal Service General Ledger Accounting Branch accountants run the Digital Accountability and Transparency Act of 2014 (DATA Act) Standard Form (SF) 133 Report on Budget Execution and Budgetary Resources Failed Edits Interface periodically. GTAS sends the SF 133 budgetary data and any TASs that fail SF 133-related edits to the DATA Act Broker to help ensure the quality of SF 133 data reported on USAspending.gov.

Fiscal Service accountants who hold exclusive access to USSGL maintenance functions in GTAS also play a critical role in managing and updating USSGL data within GTAS. They are responsible for entering approved changes across multiple components, including the chart of accounts, account definitions, transactions, attributes, and USSGL crosswalks. Their updates reflect policy changes from OMB, updated accounting standards from the Federal Accounting Standards Advisory Board, and evolving business events. Fiscal Service accountants help to approve and consistently apply all changes, technical and nontechnical, across modules. They also collaborate with the General Ledger Control Team to update edits and validations, supporting the integrity of financial data used in the USSGL Supplement to the Treasury Financial Manual and in government-wide reporting.

CARS Automatically Generates Business Event Type Codes Data from GTAS on a Scheduled Basis

The Central Accounting Reporting System (CARS) plays a key role in automating financial data flows. On a scheduled basis, it automatically generates business event type code (BETC) data by systemically retrieving relevant information from GTAS. CARS pairs BETC data with TAS to classify federal financial transactions by type, such as disbursements, collections, and transfers. This automation process ensures consistent, timely classification across agencies and supports government-wide standardization of data.

Federal Agencies Use Information from GTAS

The information processed through GTAS, including information that Fiscal Service accountants manually generate, CARS automatically generates, and agencies retrieve, flows into a variety of important federal reporting initiatives:

1. Agencies’ accounting offices report USSGL information at the Treasury account level into GTAS. Annually, GTAS adjusted trial balance data are then translated and cross-walked and copied into the following reports: SF 133 (used to monitor SF 132 and as the basis of the audited Statement of Budgetary Resources) and much of the Prior Year column of the Program and Financing schedule of the President’s budget.

2. GTAS outputs inform periodic updates to the USSGL, helping to refine account definitions and ensure consistent federal accounting practices across agencies.

3. Treasury, in coordination with OMB’s government-wide data standards and reporting policies, publishes GTAS-derived data, including DATA Act files and award-level financial details, on the USAspending.gov website, promoting public transparency and enabling stakeholders to track federal government spending.

4. Agencies use the Intragovernmental transaction function in GTAS to identify buy/sell differences between federal trading partners. Using this GTAS function, agencies communicate and report to Treasury the root causes of their differences and the work being done to resolve them on the Material Difference Reports. GTAS generates the Material Difference Report, parts I, II, and III, that display all intragovernmental agencies/trading partners, their differences, reciprocal categories, types of differences, and the explanation of each difference.

The Governmentwide Treasury Account Symbol Adjusted Trial Balance System (GTAS) validation process includes checks and reconciliations to ensure that data transmitted are accurate and complete. Two validation processes take place when agency staff certify and upload data into GTAS: one for agency bulk adjusted trial balance (ATB) files and one for fiduciary authoritative source files.

After agencies upload their bulk ATB files, GTAS runs validation checks to ensure data completeness and compliance with federal requirements. These checks include validation and accounting edits to enforce compliance with the U.S. Standard General Ledger (USSGL), Treasury Financial Manual 2-4700 guidance, and Office of Management and Budget Circulars A-11 and A-136. Data that do not pass validation may not proceed further until they have been corrected in the bulk file. Once bulk ATB file validation is complete, GTAS performs accounting edits and prepares the data for government-wide reporting. These edits enforce USSGL rules and compare data reported in agency bulk ATB files with data from other sources, such as Central Accounting Reporting System and authoritative source files.

The fiduciary authoritative source agencies validate their program-specific financial detail balances for accuracy and completeness before emailing them to the Bureau of the Fiscal Service. Fiscal Service accountants upload these data into GTAS and reconcile them against agencies’ ATBs. Following validation, GTAS generates analytical edits and reports that agencies use to help ensure that their data align with authoritative sources before certification, which helps reduce intragovernmental differences. The certified data that GTAS processes support cross-government validation, reconciliation, and standardized reporting.

GAO Contact

Paula M. Rascona, RasconaP@gao.gov

Staff Acknowledgments

In addition to the contact named above, Nina Crocker, Wayne Emilien, and Janice Latimer (Assistant Directors); Mary Ann Hardy (Auditor in Charge); Marcia Carlsen, Tracy Davis-Ross; Joanne Howard; Jason Kelly; Jason Kirwan; Sarah Lisk; Rosemarie Lopez; David Rozeboom; and Stanley Yau made significant contributions to this report.

The Government Accountability Office, the audit, evaluation, and investigative arm of Congress, exists to support Congress in meeting its constitutional responsibilities and to help improve the performance and accountability of the federal government for the American people. GAO examines the use of public funds; evaluates federal programs and policies; and provides analyses, recommendations, and other assistance to help Congress make informed oversight, policy, and funding decisions. GAO’s commitment to good government is reflected in its core values of accountability, integrity, and reliability.

Obtaining Copies of GAO Reports and Testimony

The fastest and easiest way to obtain copies of GAO documents at no cost is through our website. Each weekday afternoon, GAO posts on its website newly released reports, testimony, and correspondence. You can also subscribe to GAO’s email updates to receive notification of newly posted products.

Order by Phone

The price of each GAO publication reflects GAO’s actual cost of production and distribution and depends on the number of pages in the publication and whether the publication is printed in color or black and white. Pricing and ordering information is posted on GAO’s website, https://www.gao.gov/ordering.htm.

Place orders by calling (202) 512-6000, toll free (866) 801-7077,

or

TDD (202) 512-2537.

Orders may be paid for using American Express, Discover Card, MasterCard, Visa, check, or money order. Call for additional information.

Connect with GAO

Connect with GAO on X,

LinkedIn, Instagram, and YouTube.

Subscribe to our Email Updates. Listen to our Podcasts.

Visit GAO on the web at https://www.gao.gov.

To Report Fraud, Waste, and Abuse in Federal Programs

Contact FraudNet:

Website: https://www.gao.gov/about/what-gao-does/fraudnet

Automated answering system: (800) 424-5454

Media Relations

Sarah Kaczmarek, Managing Director, Media@gao.gov

Congressional Relations

David A. Powner, Acting Managing Director, CongRel@gao.gov

General Inquiries

[1]The annual financial report of the U.S. government is available on Treasury’s website, www.fiscal.treasury.gov. The President’s budget is available on the Office of Management and Budget’s website, www.whitehouse.gov/omb/information-resources/budget/. USAspending.gov is the official website of federal spending information.

[2]31 U.S.C. § 331(e). See GAO, Financial Audit: FY 2025 and FY 2024 Consolidated Financial Statements of the U.S. Government, GAO‑26‑108073 (Washington, D.C.: Mar. 19, 2026).

[3]The Monthly Treasury Statement of Receipts and Outlays of the United States Government is prepared by Fiscal Service. The publication is based on data provided by federal entities, disbursing officers, and Federal Reserve Banks. Financial information reported in the statement is unaudited.

[4]For comparability of amounts reported on the Monthly Treasury Statement of Receipts and Outlays of the United States Government, the President’s budget, and USAspending.gov based on GTAS budgetary and financial data, we reviewed information that pertained to fiscal year 2025, which was the most recently available information across sources during our audit period. The President’s budget for fiscal year 2025 included estimated receipts and outlays for fiscal year 2024.

[5]National Institute of Standards and Technology, Security and Privacy Controls for Information Systems and Organizations, Special Publication 800-53, Revision 5 (Gaithersburg, Md.: September 2020).

[6]An ATB is a list of U.S. Standard General Ledger (USSGL) account numbers (assets, liabilities, equity, revenue, and expenses) in numerical order with attributes and balances prepared at a specified date (i.e., year-end). Federal entities submit their GTAS ATBs by Treasury Account Symbol (TAS), which includes USSGL accounts with attributes. The USSGL account balances should reflect preclosing adjusting entries. The total sum of the debit balances must equal the total sum of the credit balances in the ATB for each TAS. The ATB intradepartmental balances for the federal entity must eliminate. Federal entities must include the required attributes with the appropriate USSGL accounts.

[7]An appropriation allows an agency to incur obligations and to make payments from the U.S. Treasury for a specified purpose.

[8]Proprietary accounting refers to federal entities’ recording and accumulation of financial information on transactions and balances for purposes of reporting both internally to management and externally in an entity’s financial statements. Proprietary accounting is also referred to as “financial accounting” and is usually based on generally accepted accounting principles (GAAP), which follow established conventions, such as the recognition of the depreciation of capital assets over time as expenses, instead of recognition on the basis of strict association with the obligation or expenditure of appropriated funds.

[9]Budgetary accounting refers to the accounting systems, processes, and people involved in collecting financial information necessary to control, monitor, and report on all funds made available to federal entities by legislation.

[10]The U.S. Standard General Ledger provides a uniform Chart of Accounts and technical guidance used in standardizing federal entity accounting.

[11]An obligation is a legally binding agreement by the government to make a payment. Award financial data link budget data to award data.

[12]An apportionment is the action by which OMB distributes amounts available for obligation.

[13]The SF 132 displays (1) sources of actual and anticipated resources, (2) actual and anticipated reductions to resources, and (3) intended use of resources.

[14]Fiduciary authoritative source agencies include Fiscal Service, the Federal Financing Bank (FFB), the Office of Personnel Management (OPM), and the Department of Labor. These agencies compile and report certain data on behalf of all federal entities for specific transaction types. Specifically, Fiscal Service reports investments and borrowing activity, FFB reports borrowing activity, OPM reports employee benefits, and Labor reports Federal Employees’ Compensation Act benefits.