Report to the Subcommittee on Legislative Branch, Committee on Appropriations, House of Representatives

United States Government Accountability Office

A report to the Subcommittee on Legislative Branch, Committee on Appropriations, House of Representatives

Contact: Kristen Kociolek at KociolekK@gao.gov

What GAO Found

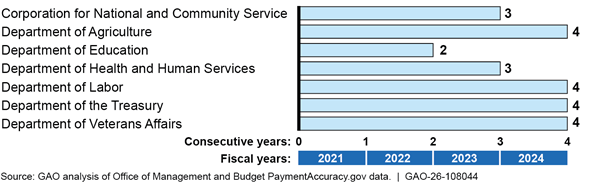

Executive branch agencies are required to report improper payment estimates for each risk-susceptible program. GAO identified seven agencies with programs reporting estimated improper payment rates of 10 percent or higher for 2, 3, or 4 consecutive fiscal years from 2021 through 2024.

Consecutive Fiscal Years of Noncompliance Reported for Agencies’ Improper Payment Rates Since Payment Integrity Information Act of 2019 Implementation

To improve transparency, agencies that are noncompliant under the Payment Integrity Information Act of 2019 (PIIA) are required to report annually to Congress and GAO. The Office of Management and Budget (OMB) provides guidance on PIIA requirements to agencies. However, GAO found that the guidance does not direct noncompliant agencies to submit the required annual reports. Unless OMB updates its guidance, Congress may not have the information it needs to assess agencies’ actions to address improper payments and hold them accountable.

Reporting requirements for noncompliant agencies vary, depending on how many consecutive fiscal years programs are noncompliant with PIIA. GAO found that all agencies with noncompliant programs for 2 consecutive years had either submitted additional program integrity proposals to OMB, as required, or taken other actions to help bring their programs into compliance.

Four of the six agencies with programs found noncompliant for 3 consecutive years submitted the required 3-year noncompliance information to Congress, OMB, and GAO. The Departments of Labor (DOL) and the Treasury did not submit the information timely, and the Treasury did not report to GAO.

All four agencies with programs found noncompliant for 4 consecutive years submitted reports to Congress and OMB as required by PIIA and OMB guidance.

Five of the seven agencies did not have sufficient documented policies and procedures to ensure consistent timely reporting for their noncompliant programs. When agencies do not meet PIIA’s annual and consecutive year reporting requirements, Congress loses visibility into which programs continue to pose elevated risks and whether agencies are taking meaningful steps to address them. Having such policies and procedures will help ensure that Congress receives timely information needed to inform legislative decision-making and support efforts for reducing government-wide improper payments and saving taxpayer dollars.

Why GAO Did This Study

Executive branch agencies have reported cumulative improper payment estimates of about $3 trillion since fiscal year 2003, including $186 billion for fiscal year 2025. To help save taxpayer dollars, it is imperative that agencies prioritize reducing their improper payments and timely report on their efforts to do so.

House Report 117-389, which accompanied the Legislative Branch Appropriations Act, 2023, includes a provision for GAO to provide quarterly reports on improper payments. This is GAO’s 11th and final report.

This report examines actions that agencies have taken to meet certain PIIA reporting requirements for programs that had estimated improper payment rates of 10 percent or higher for 2 or more consecutive years. For programs with reported noncompliance, GAO reviewed relevant laws and OMB guidance and analyzed agencies’ policies and procedures, budget information, and information on PaymentAccuracy.gov.

What GAO Recommends

GAO is making six recommendations, including one to OMB to clarify its guidance for agencies to report required annual information, and one each to the Departments of Labor, Education, Health and Human Services (HHS), the Treasury, and Agriculture (USDA) to design and implement a process to help ensure tracking and monitoring of PIIA reporting requirements for their programs and to help save taxpayer dollars. DOL, Education, HHS, Treasury, and USDA agreed with the recommendations. OMB did not provide comments.

In addition, GAO’s prior work has highlighted numerous actions that agencies and Congress can take to reduce improper payments and fraud.

Abbreviations

CFO chief financial officer

CNCS Corporation for National and Community Service

DOL Department of Labor

ECP Emergency Conservation Program

ETA Employment & Training Administration

FSA Farm Service Agency

HHS Department of Health and Human Services

IG inspector general

IRS Internal Revenue Service

OIG Office of the Inspector General

OMB Office of Management and Budget

PIIA Payment Integrity Information Act of 2019

RTC refundable tax credit

UI Unemployment Insurance

USDA Department of Agriculture

VA Department of Veterans Affairs

This is a work of the U.S. government and is not subject to copyright protection in the United States. The published product may be reproduced and distributed in its entirety without further permission from GAO. However, because this work may contain copyrighted images or other material, permission from the copyright holder may be necessary if you wish to reproduce this material separately.

June 4, 2026

The Honorable David Valadao

Chairman

The Honorable Adriano Espaillat

Ranking Member

Subcommittee on Legislative Branch

Committee on Appropriations

House of Representatives

Executive branch agencies have reported cumulative improper payment estimates of about $3 trillion since fiscal year 2003, including $186 billion for fiscal year 2025.[1] Given the magnitude of these estimates, it is imperative that agencies prioritize reducing improper payments. One way to help ensure that they do so, and thereby save taxpayer dollars, is by requiring they timely report to Congress, the Office of Management and Budget (OMB), and GAO. This is particularly important if their programs have reported estimated improper payment rates of 10 percent or higher for 2 or more consecutive years.

The Payment Integrity Information Act of 2019 (PIIA) requires agencies to manage improper payments.[2] Agencies are required to do so by conducting risk assessments, taking corrective actions, and estimating and reporting information on improper payments for programs they administer. PIIA also requires agencies’ inspectors general (IG) to issue annual reports on whether the agencies under their jurisdiction have complied with applicable PIIA criteria, such as conducting improper payment risk assessments and publishing improper payment estimates and corrective action plans for risk-susceptible programs.[3] If an agency’s program fails to meet any of these criteria, the IG reports the agency and its program as noncompliant under PIIA. Any such agency is then required to report certain information to Congress, OMB, and GAO. This reporting by agencies is a mechanism for identifying programs with ongoing noncompliance, which may indicate underlying payment integrity control weaknesses. Congress can use this information to inform legislative decision-making and support efforts for reducing government-wide improper payments and saving taxpayer dollars.

Our High-Risk List identifies government operations with serious vulnerabilities to fraud, waste, abuse, and mismanagement or that are in need of transformation.[4] The areas on the High-Risk List include programs reporting improper payment estimates, such as Medicare, Medicaid, the unemployment insurance system, and the Earned Income Tax Credit. While agencies are taking some steps to address improper payments, much more needs to be done to control billions of dollars in overpayments and prevent fraud. We have previously recommended matters for congressional consideration related to payment integrity across the government. See appendix I for a list of open payment integrity-related matters for congressional consideration.

House Report 117-389, which accompanied the Legislative Branch Appropriations Act, 2023, includes a provision for us to provide quarterly reports on improper payments. This is our 11th and final quarterly report. This report examines the extent to which (1) agencies met PIIA annual reporting requirements for noncompliant programs with estimated improper payment rates of 10 percent or higher for 2, 3, or 4 consecutive years; (2) agencies’ compliance efforts for programs with 4 consecutive years of noncompliance aligned with our key practices for addressing high-risk areas; and (3) these agencies had processes to track and monitor the reporting of PIIA noncompliance. Additionally, we have ongoing work assessing agencies’ steps to address improper payments, including identifying root causes and developing targeted corrective action plans.

To address these objectives, we reviewed relevant federal statutes, guidance, and standards related to reporting on improper payments, including PIIA and OMB guidance.[5] We obtained and analyzed improper payment data for fiscal years 2021 through 2024 on PaymentAccuracy.gov to identify agencies and programs that reported estimated improper payment rates of 10 percent or higher for consecutive fiscal years.[6] For such agencies, we reviewed IG compliance reports and agency financial reports from fiscal years 2021 through 2024. We also reviewed relevant GAO reports.

To address the first objective, we identified seven agencies—the Corporation for National and Community Service (CNCS)[7] and the Departments of Labor (DOL), Education, Health and Human Services (HHS), the Treasury, Agriculture (USDA), and Veterans Affairs (VA)—with programs reporting estimated improper payment rates of 10 percent or higher for 2, 3, or 4 consecutive fiscal years (2021, 2022, 2023, and 2024). We reviewed information these agencies reported on PaymentAccuracy.gov to assess whether annual PIIA reporting requirements were met. We also analyzed agencies’ budget information—posted on agency websites and reported in the fiscal year 2026 President’s Budget—to determine whether the agencies submitted additional program integrity budget proposals to help them come into compliance.[8] Further, we analyzed documentation from the seven agencies against applicable PIIA criteria and OMB implementing guidance to assess whether they submitted required information to appropriate congressional committees, OMB, and GAO.

To address the second objective, for the four agencies that had noncompliant programs or activities for 4 consecutive years—DOL, Treasury, USDA, and VA—we reviewed reported compliance efforts on PaymentAccuracy.gov to determine how these efforts aligned with our key practices for addressing high-risk areas.[9] See appendix II for a list of the questions we used to assess agencies’ reported compliance efforts.

To address the third objective, we obtained and reviewed documentation from the seven agencies to assess whether they had sufficient processes in place to track and monitor actions to meet the PIIA reporting requirements and to ensure that required reports are submitted to Congress, OMB, and GAO.

We conducted this performance audit from January 2025 to May 2026 in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

Background

Congress passed PIIA to improve efforts to identify and reduce government-wide improper payments. PIIA includes six criteria for compliance, which OMB guidance expands to 10 by breaking some criteria into subcomponents and, in some cases, adding new elements. PIIA and implementing OMB guidance require IGs to annually report on whether agencies and their programs met those criteria. For example, IGs report whether agencies published improper payment information with their annual agency financial reports and accompanying materials on their websites. See appendix III for the list of PIIA criteria and OMB guidance.

To assess whether agencies and programs are compliant, IGs, in part, review information that agencies reported on PaymentAccuracy.gov and analyze source data to ensure accuracy and completeness of payment integrity information in the financial statements and accompanying materials.[10] If an IG concludes that any of the agency’s programs or activities are noncompliant with PIIA in a given fiscal year, the agency is required to take additional actions for each consecutive year of noncompliance.

Since the implementation of PIIA in fiscal year 2021, IGs have reported that several federal programs consistently failed to comply with PIIA criteria because estimated improper payment rates exceeded certain statutory thresholds. PIIA instructs IGs to report agencies as noncompliant if any of the agency’s improper payment estimates equal or exceed 10 percent of that program’s outlays.

Agencies with programs that remain noncompliant with PIIA for multiple consecutive years are often the same programs that account for some of the largest improper payment estimates government-wide. PIIA establishes different reporting requirements for agencies depending on how many consecutive years their programs are found noncompliant. In reports for fiscal years 2021 through 2024, IGs found 13 programs from seven agencies noncompliant for 2 consecutive fiscal years (2021 and 2022) because the agencies reported estimated improper payment rates of 10 percent or higher. Eight programs from six agencies have done so for 3 consecutive fiscal years (2021, 2022, and 2023). Six programs from four agencies have done so for 4 consecutive fiscal years (from 2021 through 2024). Table 1 lists these programs and their reported estimated improper payment rates.[11]

Table 1: Estimated Improper Payment Rates Reported for Programs with Rates of 10 Percent or Higher for 2, 3, or 4 Consecutive Fiscal Years Since PIIA Implementation, Fiscal Years 2021–2024

|

Agency |

Program |

Fiscal year estimated improper payment rate (percent) |

Consecutive fiscal years of PIIA noncompliance |

|

||||||

|

2021 |

2022 |

2023 |

2024 |

Two years (2021-2022) |

Three years (2021-2023) |

Four years (2021-2024) |

||||

|

Corporation for National and Community Service |

The Foster Grandparent Program |

19.3 |

23.7 |

9.9 |

17.6 |

X |

n/a |

n/a |

||

|

The Retired and Senior Volunteer Program |

13.7 |

17.2 |

NR |

NR |

X |

n/a |

n/a |

|||

|

The Senior Companion Program |

20.4 |

26.2 |

15.6 |

NR |

X |

X |

n/a |

|||

|

Department of Agriculture |

Commodity Credit Corporation Trade Mitigation Program |

11.4 |

19.3 |

NR |

NR |

X |

n/a |

n/a |

||

|

Farm Service Agency Emergency Conservation Program - Disasters |

13.5 |

29.2 |

40.4 |

45.2 |

X |

X |

X |

|||

|

Department of Education |

Title I Grants to Local Educational Agencies |

14.8 |

35.7 |

0a |

NR |

X |

n/a |

n/a |

||

|

Department of Health and Human Services |

Centers for Medicare & Medicaid Services - Children’s Health Insurance Program |

31.8 |

26.7 |

12.8 |

6.1 |

X |

X |

n/a |

||

|

Centers for Medicare & Medicaid Services - Medicaid |

21.7 |

15.6 |

8.6 |

5.1 |

X |

n/a |

n/a |

|||

|

Department of Labor |

Employment & Training Administration - Federal State Unemployment Insurance |

18.9 |

22.2 |

16.5 |

15.9 |

X |

X |

X |

||

|

Department of the Treasury |

Internal Revenue Service - Additional Child Tax Credit |

13.3 |

15.8 |

14.5 |

10.7 |

X |

X |

X |

||

|

Internal Revenue Service - American Opportunity Tax Credit |

26.3 |

36.1 |

31.6 |

27.7 |

X |

X |

X |

|||

|

Internal Revenue Service - Earned Income Tax Credit |

27.8 |

31.6 |

33.5 |

27.3 |

X |

X |

X |

|||

|

Department of Veterans Affairs |

Purchased Long-Term Services and Supports |

72.8 |

47.5 |

38.7 |

13.5 |

X |

X |

X |

||

n/a = not applicable.

NR = Not reported. A designation of NR may be due to a program’s lack of a reporting requirement for that fiscal year, not failure to report.

PIIA = Payment Integrity Information Act of 2019.

X = PIIA noncompliant.

Source: GAO analysis of Office of Management and Budget PaymentAccuracy.gov data. | GAO‑26‑108044

Note: Estimated improper payment rates include both improper and unknown payments as reported on PaymentAccuracy.gov. Executive agency estimates of improper payments also treat as improper any payments that cannot be determined to be proper due to lacking or insufficient documentation. Agencies report payment integrity information in their annual agency financial reports and on PaymentAccuracy.gov. These sources contain additional agency-reported information, including estimated improper and unknown payment amounts and rates, root causes, and corrective actions.

aIn fiscal year 2023, the Department of Education reported that it implemented effective mitigation strategies that resulted in the reduction of the improper payment rate to 0 percent. However, in its audit of Education’s fiscal year 2023 compliance with the payment integrity information reporting requirements, Education’s Office of Inspector General found that the Title I improper payment estimate was not reliable due to issues with the sampling and estimation methodology.

Agency Reporting for Annual and Consecutive Years of Noncompliance

What does PIIA require noncompliant agencies to report to Congress and GAO?

For each year they are found noncompliant, PIIA requires agencies to, among other things, submit an annual report to the appropriate authorizing and appropriations congressional committees and GAO.[12] This report must include (1) a list of each program or activity that was determined to be noncompliant for 1, 2, 3, 4, or more consecutive years and (2) actions that the agency plans to take to bring the program or activity into compliance.[13]

Which agencies did not meet the annual reporting requirement?

We found that six of the seven agencies we reviewed—CNCS, DOL, HHS, Treasury, USDA, and VA—did not report all PIIA-required annual information about their noncompliant programs in fiscal year 2024. Specifically, while these agencies reported planned corrective actions to bring programs into compliance on PaymentAccuracy.gov, they did not report a list of all programs that have been noncompliant for consecutive years. Instead, these agencies reported the number of consecutive years that the agencies, not their programs, were noncompliant. Education reported that it reduced the Title I grant program’s estimated improper payment rate to 0 percent in fiscal year 2023 and that it had no programs determined to be noncompliant in fiscal year 2024.[14] Accordingly, Education did not report annual noncompliance information in fiscal year 2024.

Officials from all seven of the agencies stated that they follow OMB guidance regarding the reporting requirements by posting certain information on PaymentAccuracy.gov. We found that while the OMB guidance directs agencies to provide information in the OMB annual data call describing actions that the agency will take to come into compliance, it does not direct agencies to submit the separate annual report to Congress and GAO containing (1) a list of each noncompliant program or activity that was determined to be noncompliant for 1, 2, 3, 4, or more consecutive years and (2) actions planned to bring the program or activity into compliance,[15] as required by PIIA.[16]

Without updated OMB guidance clarifying agency annual reporting requirements, agencies will be less likely to timely provide the key payment integrity information needed for Congress to assess agencies’ actions for addressing improper payments and hold them accountable. In addition, reporting a list of noncompliant programs for consecutive years would provide Congress with valuable information for targeted oversight and assessment of whether corrective actions are appropriate and will help save taxpayer dollars.

What does PIIA require an agency to do for 2 consecutive years of noncompliance?

When an agency has been noncompliant with PIIA criteria for 2 consecutive fiscal years for the same program or activity, PIIA requires it to submit additional program integrity proposals to OMB that would help the agency come into compliance.[17] OMB guidance directs agencies to include these proposals in their next budget submissions supporting the development of the annual President’s Budget.

If OMB determines that additional funding would help an agency come into compliance, the agency must obligate additional funds in an amount that OMB determines. To do so, the agency must exercise available reprogramming or transfer authority.[18] If further funding is needed to reach the full amount OMB determined, the agency is required to request additional reprogramming or transfer authority from Congress.

Which agencies submitted additional program integrity proposals?

Two of the seven agencies that were noncompliant for 2 consecutive years (2021 and 2022)—DOL and HHS—submitted additional program integrity proposals to OMB for the fiscal year 2026 President’s Budget.[19]

DOL. The agency proposed a funding increase of $79 million to carry out its reemployment services and eligibility assessments program. According to an agency official, the purpose of the proposal included strengthening program integrity by reducing improper payments through detection and prevention. The proposal also included a separate increase of $25 million for unemployment insurance identity verification program integrity activities. The agency stated that these identity proofing services can significantly reduce overpayments due to identity fraud.

HHS. In its proposal, HHS requested an increase in mandatory Health Care Fraud and Abuse Control program funding to help address health care payment integrity, including activities related to identifying and reducing improper payments and preventing and detecting fraud.[20] HHS officials told us that the agency plans to intensify its compliance efforts. These efforts include working with states to implement corrective action plans, providing technical assistance to states, monitoring progress of its compliance efforts, and conducting audits of beneficiary eligibility determinations in states identified as having higher estimated improper payment rates.

What other actions did agencies take to help bring their programs into compliance?

The five agencies that did not submit additional program integrity proposals—CNCS, Education, Treasury, USDA, and VA—took other actions to help bring their programs into compliance.

CNCS. CNCS officials explained that the organizations receiving CNCS grants, rather than the agency itself, generally make payments. Therefore, CNCS officials told us that the agency plans to implement corrective actions in fiscal year 2025 targeted at such organizations. For example, CNCS will require written confirmation from grantees found to have made improper payments for which CNCS staff members responsible for the areas where improper payments occurred have reviewed all information and completed all related training.

Education. According to Education officials, the improper payment rates for Title I grants to local educational agencies in fiscal years 2021 and 2022 were due almost entirely to “unknown” payments.[21] Subsequently, in fiscal year 2023, Education reported that it implemented effective mitigation strategies that eliminated improper payments.[22]

Treasury. Officials from Treasury’s Internal Revenue Service (IRS) told us that IRS continues to focus on its compliance efforts. Such efforts relate to refundable tax credits and include improving outreach and education for taxpayers and paid tax preparers, collaborating with federal and state stakeholders, and conducting educational events to support tax preparer compliance. However, they stated that any budget reductions and limited staffing resources may affect the agency’s ability to continue these outreach and compliance efforts.

USDA. According to USDA officials, the agency did not submit timely additional program integrity proposals for its Emergency Conservation Program - Disasters program. However, these officials told us that the agency subsequently submitted a separate request through a memorandum to OMB for approval to proceed with proposed actions to reduce improper payments, including additional funding for software enhancements that will enable USDA to automatically generate a list of applications for compliance spot checks.

VA. VA officials stated that the agency’s corrective actions included implementation of a standardized rate schedule for community nursing home payments and transitioning more payments from a legacy system requiring manual validation to an automated claims adjudication system to help reduce improper payments in the Purchased Long-Term Services and Supports program.[23]

What does PIIA require an agency to do for 3 consecutive years of noncompliance?

When an agency’s IG determines the same program or activity has been noncompliant for 3 consecutive fiscal years, PIIA requires the agency to submit certain documentation to appropriate authorizing and appropriations committees and GAO. OMB guidance expands this requirement to include submission to OMB. All of these submissions must occur within 30 days of the noncompliance determination. Specifically, the agency generally must submit (1) reauthorization proposals for each relevant program or activity and (2) proposed statutory changes to bring the program or activity into compliance.[24]

However, if the agency determines that these actions will not bring the program or activity into compliance, the agency must alternatively submit to the committees, OMB, and GAO a description of the actions the agency is taking to bring its program or activity into compliance and a timeline for when it expects to achieve compliance.

Which agencies met the 3-year noncompliance reporting requirements?

Of the six agencies that were noncompliant with PIIA for 3 consecutive years (2021, 2022, and 2023), four met the reporting requirement.

Four agencies––CNCS, HHS, USDA, and VA––met the 3-year reporting requirement by submitting required information to the appropriate congressional committees, OMB, and GAO within 30 days of their IGs’ third consecutive noncompliance determination in fiscal year 2023.

Two agencies––DOL and Treasury––submitted required information but did not do so within 30 days, as required. DOL submitted its 3-year noncompliance information late to appropriate congressional committees, OMB, and GAO. Treasury submitted its information late to appropriate congressional committees and OMB and did not submit a report to GAO.

Table 2 summarizes these six agencies’ submissions of their 3-year noncompliance information.

|

Agency |

Did agency submit required information to Congress, OMB, and GAO? |

||

|

Congress |

OMB |

GAO |

|

|

Corporation for National and Community Service |

✓ |

✓ |

✓ |

|

Department of Agriculture |

✓ |

✓ |

✓ |

|

Department of Health and Human Services |

✓ |

✓ |

✓ |

|

Department of Labor |

✗ |

✗ |

✗ |

|

Department of the Treasury |

✗ |

✗ |

O |

|

Department of Veterans Affairs |

✓ |

✓ |

✓ |

✓ = Submitted on time; ✗ = Submitted late; O = Did not submit.

PIIA = Payment Integrity Information Act of 2019.

Source: GAO analysis of agencies’ submission of 3-year PIIA noncompliance information to Congress, the Office of Management and Budget, and GAO. | GAO‑26‑108044

What does PIIA require an agency to do for 4 consecutive years of noncompliance?

When an agency has been noncompliant for 4 or more consecutive fiscal years for the same program or activity, PIIA and OMB guidance direct the agency to submit certain documentation to appropriate authorizing and appropriations committees and OMB within 30 days of its IG’s noncompliance determination.[25] Specifically, the agency must submit a report that includes

· the activities the agency has taken to comply with the requirements for 1, 2, 3, 4, or more consecutive years of noncompliance;

· a description of any requirements that were fulfilled for 1, 2, 3, 4, or more consecutive years of noncompliance that are still relevant and that the agency is pursuing to bring the program or activity into compliance and prevent and reduce improper payments;

· a description of any new corrective actions; and

· a timeline for when the program or activity will achieve compliance based on the actions described within the report.

Which agencies met the 4-year noncompliance reporting requirements?

All four agencies noncompliant with PIIA criteria for the same program or activity for 4 consecutive years (2021 through 2024)––DOL, Treasury, USDA, and VA––met the requirement by submitting required information in a report to the appropriate congressional committees and OMB. Table 3 summarizes these four agencies’ submissions of their 4-year noncompliance information.

|

Agency |

Did agency submit required information to Congress and OMB? |

||

|

Congress |

OMB |

|

|

|

Department of Agriculture |

✓ |

✓ |

|

|

Department of Labor |

✓ |

✓ |

|

|

Department of the Treasury |

✓ |

✓ |

|

|

Department of Veterans Affairs |

✓ |

✓ |

|

✓ = Submitted.

PIIA = Payment Integrity Information Act of 2019.

Source: GAO analysis of agencies’ submission of 4-year PIIA noncompliance information to Congress and the Office of Management and Budget. | GAO‑26‑108044

How Agencies’ Reported Compliance Efforts for 4-Year Noncompliant Programs Aligned with GAO’s Key Practices for Addressing High-Risk Areas

What must agencies demonstrate for an area to be removed from GAO’s High-Risk List?

When determining which federal programs and functions should be designated as high-risk areas, we consider the potential for improper payments or fraud, among other factors. For programs identified as high-risk areas, our criteria for removal from the High-Risk List can help inform agency efforts to reduce improper payments and save taxpayer dollars. There are five key practices we use to assess agency progress in addressing high-risk areas: (1) leadership commitment, (2) agency capacity, (3) an action plan, (4) monitoring efforts, and (5) demonstrated progress (see fig. 1).[26]

How did agency-reported compliance efforts align with key practices for addressing high-risk areas?

Based on our review of the fiscal year 2024 information on PaymentAccuracy.gov, the four agencies that have been noncompliant with PIIA for 4 consecutive fiscal years (2021 through 2024)—DOL, Treasury, USDA, and VA—reported employing a variety of efforts to mitigate improper payments.[27] Some of these compliance efforts aligned with key practices for addressing high-risk areas. For example:

Leadership commitment. All four agencies designated accountable officials responsible for the progress of the agency coming into compliance with applicable PIIA criteria. Three agencies—Treasury, USDA, and VA—outlined accountability mechanisms, such as a process for holding the designated official responsible for leading compliance efforts under PIIA. DOL did not specify an accountability mechanism but did outline performance requirements focused on the program. While varied, all four agencies documented some level of internal coordination between intra-agency partners and stakeholders to increase access to information used to mitigate improper payments, such as involving chief financial officers and holding regular meetings to discuss improper payment topics.

Capacity. All four agencies reported on their funding or actions needed to improve or maintain payment integrity. For example, DOL reported that it requested funding increases to support technology modernization that will improve states’ abilities to detect and prevent fraud and other improper payments in the Federal State Unemployment Insurance program. VA reported that it had what it needed to improve or maintain payment integrity, including adequate funding to implement improvements planned to internal controls, human capital, information systems, and other infrastructure.

Treasury reported that it needed statutory changes and restructuring of refundable tax credits to reduce the improper payment rate to less than 10 percent.[28] USDA reported that it needed additional funding for software enhancements to improve the agency’s ability to monitor program implementation to improve and maintain payment integrity. All four agencies reported that they had some of the capacity needed in the form of technology, training, or both to help resolve the risk of improper payments over time.

Action plan. All four agencies identified root causes of improper payments, described corrective action plans, and included planned completion dates for their corrective actions in response to findings and recommendations made by their respective IGs in the fiscal year 2024 PIIA compliance reports. As summarized in appendix IV, IGs of the four agencies have made various recommendations for agency actions to address their findings. In addition, two of the four agencies—DOL and Treasury––have open GAO recommendations related to their programs that reported estimated improper payment rates of more than 10 percent for 4 consecutive years (see app. V). It is critical that these agencies take actions to implement IG and GAO recommendations to help reduce improper payments.

Monitoring. All four agencies reported steps they take to monitor and validate the effectiveness and sustainability of actions to correct PIIA noncompliance. For example, one agency reported that it requires states to conduct quality assurance audits to determine if payments were accurate or improper.

Demonstrated progress. Three agencies—DOL, USDA, and VA—described how they measured the effectiveness of corrective actions. However, Treasury did not provide this information on PaymentAccuracy.gov. Instead, Treasury emphasized that without significant restructuring of the refundable tax credits programs, including the legislative actions discussed above, the improper payment rate of those programs will not be reduced below 10 percent.

In addition, DOL, Treasury, and VA reported reductions in their improper payment estimates for their respective noncompliant programs from fiscal years 2023 to 2024, although their rates remained above 10 percent.

However, USDA continued to report increasing improper payment estimates for its Emergency Conservation Program from fiscal years 2023 to 2024. According to its IG, USDA and its state agencies did not have adequate policies and procedures to reduce improper payments. Specifically, USDA reported that while it continues to support state-level efforts to enhance payment integrity and prevent improper payments through training and technical assistance, states either did not properly follow statutory requirements for payment eligibility, failed to access data and information needed to validate payment accuracy, or did not properly review documentation prior to issuing payments.

See appendix IV for detailed information on agencies’ reported compliance efforts related to key practices for addressing high-risk areas.

Agency Processes for Reporting PIIA-Noncompliant Programs

Which agencies have processes to track and monitor their reporting for PIIA noncompliance?

Of the seven agencies we reviewed that had noncompliant programs with estimated improper payment rates of 10 percent or higher for 2 or more consecutive years, only VA and CNCS had established and documented sufficient processes in their policies and procedures to track and monitor their reporting for PIIA noncompliance.

VA. VA has established and documented processes in its policies and procedures to track and monitor reporting for PIIA noncompliance. VA’s policies and procedures describe its processes for tracking and completing required reporting activities for noncompliant programs. In addition, VA issues an annual internal memorandum to help ensure that it accomplishes reporting activities and milestones.

CNCS. In response to our inquiries, CNCS revised its payment integrity guidance in September 2025 to outline steps for addressing improper payments, including processes related to reporting for noncompliant programs.[29] Prior to these revisions, CNCS’s guidance did not include specific procedures, such as milestones for tracking and monitoring noncompliant programs and coordinating with stakeholders, to help ensure that the agency meets the PIIA reporting requirements.

Which agencies did not have processes to track and monitor their reporting for PIIA noncompliance?

We found that the five remaining agencies did not have sufficient processes, documented in policies and procedures, to track and monitor their reporting for PIIA noncompliance.

DOL. DOL’s process did not ensure timely submission of the required reporting for PIIA noncompliance. Its process for tracking and monitoring the reporting for PIIA noncompliance is not documented in policies and procedures. The current process consists of notifications that its Office of the Chief Financial Officer emails to responsible staff after the IG determines a program to be noncompliant. These emails remind the units that oversee the program of upcoming reporting requirements and due dates. We found that the agency’s Office of the Chief Financial Officer promptly sent its notification after the IG determined the unemployment insurance program to be noncompliant for 3 consecutive fiscal years. However, there were timing issues within DOL that resulted in it not submitting the required reporting information on time. Without establishing a process, documented in policies and procedures, to track and monitor the submission of required PIIA noncompliance reporting, there is an increased risk that DOL will not submit the required information timely.

Education. Education’s department-wide guidance on managing improper payments and related risks does not include processes to monitor and track the submission of required reporting for PIIA noncompliance.[30] Specifically, although Education officials told us that the agency has some processes to ensure that it meets required reporting submission timelines, such as internal reporting calendars and recurring meetings with the IG, these processes are not documented in policies and procedures.

Without a department-wide process, documented in policies and procedures, to track and monitor the submission of required PIIA noncompliance reporting, there is an increased risk that Education offices will not submit the required information timely.

HHS. Although not documented in formal policies and procedures, HHS officials told us that HHS has some processes and tools for tracking, monitoring, and submitting the required PIIA noncompliance reports. For example, it uses a spreadsheet to track its IG’s recommendations, delegates noncompliance reporting for each program to the respective operating division, and designates HHS’s Division of Payment Integrity and Improvement to oversee the department-wide noncompliance reporting process.

HHS officials told us they believe that HHS’s multiple layers of processes help ensure that it effectively tracks and monitors noncompliant programs. However, without these processes being documented in policies and procedures, there is an increased risk that they will not be consistently performed and that HHS will not submit the required information timely.

Treasury. Treasury’s process did not ensure timely submission of the required reporting for PIIA noncompliance. Treasury’s department-wide guidance provides general instructions for submitting the required PIIA noncompliance reporting.[31] However, this guidance does not include specific processes to track and monitor such reporting to help ensure timely submission.

Treasury is responsible for administering the improper payment compliance program for all its components, including IRS. IRS developed its own guidance, in addition to the department-wide guidance, which provides general instructions for responsible staff as well as a schedule for delivery of required information to Treasury.[32] As discussed above, although IRS officials prepared and sent the required information to Treasury recipients for approval and submission after the 3 consecutive fiscal years of noncompliance, Treasury did not submit the information to Congress, OMB, and GAO, as required.

According to Treasury officials, this was due to a departure of responsible staff at Treasury. Further, we found that Treasury’s guidance lacks sufficiently documented roles and responsibilities to help account for such a situation and ensure that it submits the required information on time. Treasury was unaware that it had not submitted the required information until we requested a copy of the submitted information. Subsequently, Treasury submitted the information to Congress and OMB in March 2025, about 9 months after the statutory due date. As indicated in table 2 above, Treasury did not submit the report to GAO.

Without a department-wide process, documented in policies and procedures, to track and monitor the submission of required PIIA noncompliance reporting, there is an increased risk that Treasury offices will not submit the required information timely.

USDA. According to USDA officials, USDA’s component agencies have some processes in place for monitoring noncompliant programs. However, these processes are not documented in departmental policies and procedures. USDA officials told us that they recognize that uniform, departmental guidance is necessary to ensure that staff consistently track all programs and identify PIIA noncompliance requirements for reporting. USDA officials said that the department has plans to develop such guidance; however, it has not developed any specific milestones or project plans to do so. Until USDA has a department-wide process, documented in policies and procedures, to track and monitor the submission of required PIIA noncompliance reporting, there is an increased risk that USDA will not submit the required information timely.

As applicable to all federal executive agencies, the federal internal control standards state that management should design control activities to mitigate risks to achieving the entity’s objectives and implement those control activities through policies and procedures. As part of these standards, management monitors the status of remediation efforts to ensure that they are completed timely.[33]

Without sufficiently detailed documented policies and procedures, these five agencies—DOL, Education, HHS, Treasury, and USDA—have less assurance that they will consistently and timely meet the PIIA reporting requirements, particularly in the event of staff turnover or changes in roles. Further, if agencies do not report timely, Congress and OMB may not have the key payment integrity information needed for their oversight of government-wide improper payment reduction efforts, which can lead to saving taxpayer dollars.

Conclusions

Improper payments are a long-standing, significant problem in the federal government. As we have reported, although agencies report improper payment estimates annually, the federal government is unable to determine the full extent to which improper payments occur or reasonably ensure that actions are taken to reduce them. We have previously noted that some IGs have also reported issues related to agencies’ improper payments. As such, it is critical that agencies take actions to implement IG and GAO recommendations to help reduce improper payments and save taxpayer dollars.

OMB provides government-wide guidance for agencies to meet the PIIA requirements. Unless OMB, through its guidance, explicitly directs agencies to report required annual information about program noncompliance, Congress may continue to lack the key payment integrity information needed to assess agencies’ actions to reduce improper payments and hold them accountable.

In addition, we found that five of the seven agencies we reviewed—DOL, Education, HHS, Treasury, and USDA—had some internal processes in place to help ensure that they met PIIA reporting requirements for their noncompliant programs or activities. However, they did not have sufficient processes, documented in policies and procedures, to track and monitor the reporting of PIIA noncompliance.

These findings also have important implications for congressional oversight. Agencies with programs that remain noncompliant with PIIA for multiple consecutive years are often the same programs that account for some of the largest improper payment estimates government-wide. When agencies do not meet PIIA’s annual and consecutive year reporting requirements, Congress loses visibility into which programs continue to pose elevated risks and whether agencies are taking meaningful steps to address them.

Having sufficient, documented processes is essential for agencies to meet the PIIA noncompliance reporting requirements and ultimately help save taxpayer dollars. Documentation of such processes would help ensure that agency staff are clear about what procedures to follow to meet the reporting requirements, particularly in the event of staff turnover or changes in roles, ultimately helping to ensure that Congress has the information needed to assess agency efforts to reduce improper payments and save taxpayer dollars.

Recommendations for Executive Action

We are making the following six recommendations—one each to OMB, DOL, Education, HHS, Treasury, and USDA.

The Director of the Office of Management and Budget should clarify that agencies found noncompliant with PIIA criteria should report required annual information to GAO and the appropriate authorizing and appropriations congressional committees. Pursuant to 31 U.S.C. § 3353(b)(5), this information should include (1) a list of programs that have been noncompliant for 1, 2, 3, 4, or more years and (2) actions planned to bring the programs or activities into compliance. (Recommendation 1)

The Secretary of Labor should design and implement a process, documented in policies and procedures, to help ensure the tracking, monitoring, and timely submission of required PIIA-noncompliant program information to appropriate authorizing and appropriations congressional committees, OMB, and GAO. (Recommendation 2)

The Secretary of Education should design and implement a process, documented in policies and procedures, to help ensure the tracking, monitoring, and timely submission of required PIIA-noncompliant program information to appropriate authorizing and appropriations congressional committees, OMB, and GAO. (Recommendation 3)

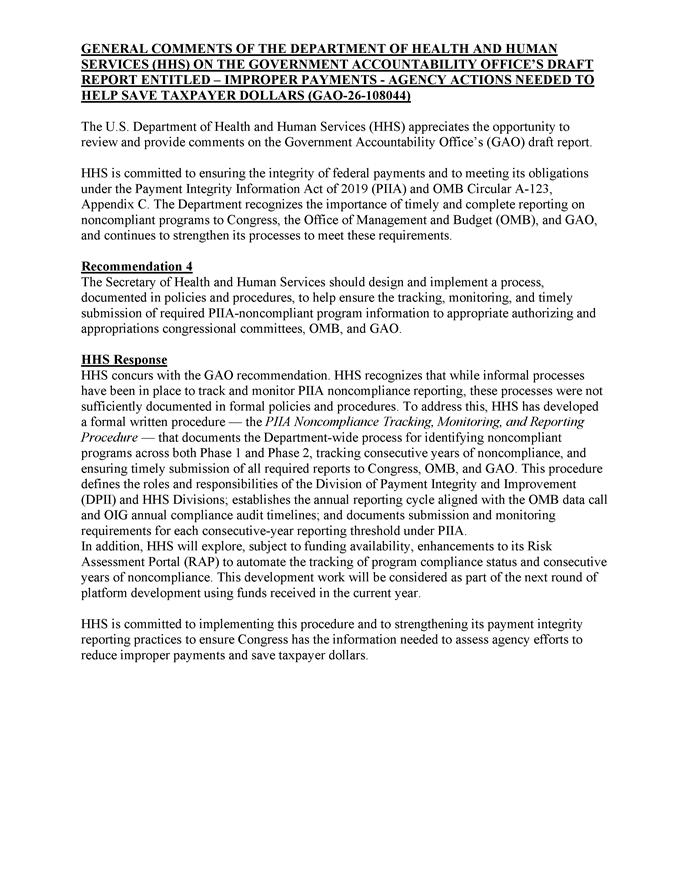

The Secretary of Health and Human Services should design and implement a process, documented in policies and procedures, to help ensure the tracking, monitoring, and timely submission of required PIIA-noncompliant program information to appropriate authorizing and appropriations congressional committees, OMB, and GAO. (Recommendation 4)

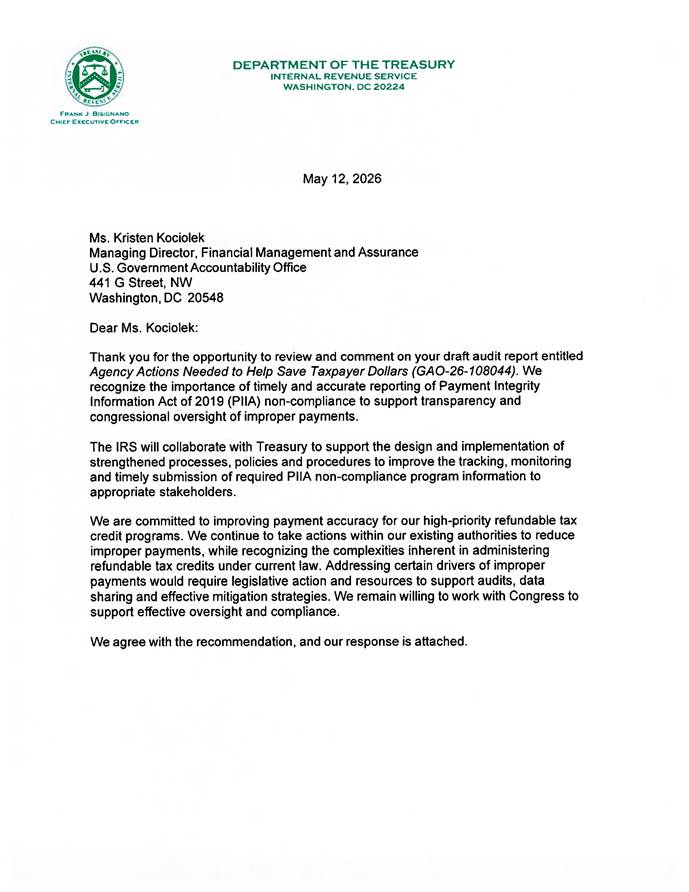

The Secretary of the Treasury, in coordination with the Commissioner of Internal Revenue, should design and implement a process, documented in policies and procedures, to help ensure the tracking, monitoring, and timely submission of required PIIA-noncompliant program information to appropriate authorizing and appropriations congressional committees, OMB, and GAO. (Recommendation 5)

The Secretary of Agriculture should design and implement a process, documented in policies and procedures, to help ensure the tracking, monitoring, and timely submission of required PIIA-noncompliant program information to appropriate authorizing and appropriations congressional committees, OMB, and GAO. (Recommendation 6)

Agency Comments

We provided a draft of this report to OMB, CNCS, DOL, USDA, Education, HHS, Treasury, and VA for review and comment.

CNCS, DOL, Education, HHS, and Treasury provided written comments, which are reproduced in appendixes VI, VII, VIII, IX, and X, respectively. DOL, Education, HHS, and Treasury agreed with our recommendations and expressed plans to design and implement processes to help ensure the tracking, monitoring, and timely submission of required PIIA-noncompliant program information; we made no recommendations to CNCS.

USDA provided comments via email stating that the agency agreed with our recommendation and stated that, within 30 days, USDA will draft internal policies and procedures to track, monitor, and timely submit required PIIA noncompliance information to the appropriate congressional committees, OMB, and GAO. USDA told us that it anticipates implementing the formal policy by September 30, 2026.

VA provided technical comments, which we incorporated as appropriate.

OMB did not provide comments on our draft report.

We are sending copies of this report to the appropriate congressional committees, the Director of the Office of Management and Budget, the Chief Executive Officer of the Corporation for National and Community Service, the Secretary of Agriculture, the Secretary of Education, the Secretary of Health and Human Services, the Secretary of Labor, the Secretary of the Treasury, the Secretary of Veterans Affairs, and other interested parties. In addition, the report is available at no charge on the GAO website at https://www.gao.gov.

If you or your staff have any questions about this report, please contact me at KociolekK@gao.gov. Contact points for our Offices of Congressional Relations and Public Affairs may be found on the last page of this report. GAO staff who made key contributions to this report are listed in appendix XI.

Kristen Kociolek

Managing Director, Financial Management and Assurance

We have previously recommended matters for congressional consideration to strengthen payment integrity across the government.[34] As of January 2026, these seven matters remain open.

1. Congress should consider passing legislation requiring the Office of Management and Budget (OMB) to provide guidance for agencies to develop plans for internal control that would then immediately be ready for use in, or adaptation for, future emergencies or crises and requiring agencies to report these internal control plans to OMB and Congress.

2. Congress should consider amending the Payment Integrity Information Act of 2019 (PIIA) to designate all new federal programs making more than $100 million in payments in any one fiscal year as “susceptible to significant improper payments” for their initial years of operation.

3. Congress should consider amending PIIA to reinstate the requirement that agencies report on their antifraud controls and fraud risk management efforts in their annual financial reports.

4. Congress should consider establishing a permanent analytics center of excellence to aid the oversight community in identifying improper payments and fraud.

5. Congress should consider clarifying that (1) chief financial officers (CFO) at Chief Financial Officers Act agencies have oversight responsibility for internal controls over financial reporting and key financial management information that includes spending data and improper payment information and (2) executive agency internal control assessment, reporting, and audit requirements for key financial management information, discussed in an existing matter for congressional consideration in our August 2020 report,[35] include internal controls over spending data and improper payment information.

6. Congress should consider requiring agency CFOs to (1) submit a statement in agencies’ annual financial reports certifying the reliability of improper payments risk assessments and the validity of improper payment estimates and describing the CFO’s actions to monitor the development and implementation of any corrective action plans and (2) approve any methodology that is not designed to produce a statistically valid estimate of improper payments.

7. Congress should consider legislation to require improper payment information required to be reported under PIIA to be included in agencies’ annual financial reports.

In addition to these government-wide matters for congressional consideration, we have also made recommendations to Congress that would enhance the integrity of individual programs that we reviewed. As of January 2026, these matters remain open.

1. If Congress agrees that significant paid preparer errors exist, it should consider legislation granting the Internal Revenue Service the authority to regulate paid tax preparers.[36]

2. Congress should consider granting the Department of Labor the additional authority it is seeking to access wage data to help verify claimants’ reported income and help ensure the proper payment of benefits.[37]

Appendix II: GAO Questions for Assessing Agencies’ Compliance Efforts Related to Key Practices for Addressing High-Risk Areas

GAO’s High-Risk List identifies government operations with serious vulnerabilities to fraud, waste, abuse, and mismanagement or in need of transformation. Listed below are the questions that we used to evaluate agencies’ reported information on PaymentAccuracy.gov to determine how agencies’ reported compliance efforts aligned with GAO’s five key practices for addressing the areas on our High-Risk List.

Leadership Commitment

1. Has the agency identified an official accountable for bringing the program into compliance under the Payment Integrity Information Act of 2019 (PIIA)?

2. Did the agency describe an accountability mechanism tied to the success of this official (e.g., establishing performance incentives or benchmarks)?

3. Did the agency facilitate internal collaboration through coordination between intra-agency partners and stakeholders to increase access to information used to mitigate improper payments (e.g., involving chief financial officers and holding regular meetings to discuss improper payment topics)?

Capacity

4. Does the agency report that it has what is needed to improve or maintain payment integrity?

5. Did the agency identify its efforts to provide technology, tools, and training designed to address root causes of improper payments (e.g., software, automation, information systems, and training on proper payment processing methods)?

Action Plan

6. For the noncompliant programs, has the agency identified root causes of improper payments and described corrective actions?

7. Did the agency establish and include planned completion dates for the corrective actions?

8. In the most recent PIIA compliance report, did the agency inspector general have any findings related to the reported root causes or corrective actions? If so, does the agency have planned actions to address them?

9. Are there any related open GAO recommendations? If so, does the agency have planned actions to address them?

Monitoring

10. Did agency report steps it would take to monitor and validate effectiveness and sustainability of actions to reduce improper payments (e.g., use the Department of the Treasury’s systems, such as Do Not Pay, to monitor improper payments)?

11. Did the agency monitor progress?

Demonstrated Progress

12. Did the agency report how it measures effectiveness of corrective actions (i.e., establishment of reduction targets)?

13. Has the agency reported year-over-year reductions in the improper payment estimates for the noncompliant programs?

Appendix III: Payment Integrity Information Act of 2019 Criteria and Office of Management and Budget Guidance

When an inspector general (IG) determines that the agency is not in compliance with applicable Payment Integrity Information Act of 2019 (PIIA) criteria or related Office of Management and Budget (OMB) guidance, the agency is subject to additional reporting and other requirements. PIIA, together with related OMB guidance, instructs IGs to report on whether their agencies are compliant with 10 criteria.[38] To meet these criteria, agencies must

(1a) publish payment integrity information with their annual financial statements,

(1b) post their annual financial statements and accompanying materials on their websites,

(2a) conduct improper payment risk assessments for each program with annual outlays greater than $10 million at least once every 3 fiscal years,

(2b) adequately conclude whether each program is likely to make improper payments and unknown payments above or below the statutory threshold (either $100 million or both 1.5 percent of program outlays and $10 million of all reported program and activity payments made by the agency during that fiscal year),

(3) publish improper payment and unknown payment estimates for programs susceptible to significant improper payments and unknown payments in the accompanying materials to their annual financial statements,

(4) publish corrective action plans for each program for which an estimate above the statutory threshold was published in the accompanying materials to their annual financial statements,

(5a) publish an improper payment and unknown payment reduction target for each program for which an estimate above the statutory threshold was published in the accompanying materials to their annual financial statements,

(5b) demonstrate improvements to payment integrity or reach a tolerable improper payment and unknown payment rate,

(5c) develop plans to meet their improper payment and unknown payment reduction targets,[39] and

(6) report improper payment and unknown payment estimates of less than 10 percent for each program for which they published estimates in the accompanying materials to their annual financial statements.

The criteria described above do not apply to all programs or agencies. For example, if an agency determines through its risk assessment that none of its programs or activities are susceptible to significant improper payments, criteria three through six would not be applicable.

Appendix IV: Alignment of Certain Agencies’ Actions with GAO’s Key Practices for Addressing High-Risk Areas

Agencies with programs or activities found to be noncompliant for 4 or more consecutive years under the Payment Integrity Information Act of 2019 (PIIA) are required to report on their compliance efforts. Table 4 provides detailed information that agencies reported on PaymentAccuracy.gov. We summarized such information based on how agencies’ reported compliance efforts to reduce improper payments aligned with our key practices for addressing high-risk areas.

Table 4: How Agencies’ Compliance Efforts for 4 Years of Noncompliance Aligned with GAO’s Key Practices for Addressing High-Risk Areas

|

Agency/program |

Key practice/agency efforts |

|

Department of Labor (DOL) Employment & Training Administration (ETA) – Federal State Unemployment Insurance (UI) |

Leadership commitment. To help initiate and sustain progress, DOL reported that it designated the Administrator of the Office of Unemployment Insurance as the accountable official for bringing the program into compliance with the Payment Integrity Information Act of 2019 (PIIA). According to DOL, the office’s performance management plan focuses on requirements for states to maintain improper payment rates below 10 percent, with corrective actions if they fail to do so. Additionally, DOL reported that its ETA, through the DOL-funded national UI Integrity Center, (1) assisted states with projects to provide UI, fraud prevention, and development of fraud risk management resources and strategies and (2) coordinated with the Office of Inspector General (OIG) to discuss emerging UI fraud issues and antifraud measures. Capacity. Capacity represents the resources (i.e., skilled staff, adequate funding, internal controls, technology, and management and organization infrastructure) to resolve key risks. DOL reported that its fiscal year 2025 budget requested funds for technology upgrades, ID verification services, and antifraud activities. DOL stated that it would continue to provide technical assistance on proposed UI integrity legislation as needed and promote the UI integrity legislative package as set out in DOL’s 2025 budget proposal. DOL also stated that the DOL-funded national UI Integrity Center provides resources, training, and enhanced data tools to help states reduce improper payments. Action plan. To define the root causes and solutions and provide an approach for substantially completing corrective measures, DOL reported identifying the following as its most commonly occurring UI improper payments: “Work search” improper payments occur when UI claimants fail to properly document their work search efforts or fail to comply with state work search requirements. · “Benefit year earnings” improper payments occur when UI claimants either fail to report earnings or incorrectly report earnings from employment. · “Separation” improper payments occur when UI claimants receive benefits and are later determined to be ineligible due to a disqualifying separation from previous employment. DOL reported that its corrective actions to address these types of improper payments include issuing guidance and technical assistance to states, strengthening ID verification, providing states with additional payment integrity data sources, and expanding fraud detection tools. DOL stated that its planned completion dates for these corrective actions are in fiscal year 2028. To improve DOL’s compliance efforts with PIIA, the OIG, in its report issued in May 2025, recommended that 1. the Assistant Secretary for ETA maintain ETA’s current focus on increasing technical assistance and funding to states to improve improper payment reduction strategies to reduce the improper payments estimate rate below the 10 percent threshold and 2. the Chief Financial Officer update review procedures to ensure accurate responses to Office of Management and Budget (OMB) payment integrity data call prompts; ensure compliance with PIIA; and ensure that information is complete, accurate, and consistent before the final submission of the OMB payment integrity data call, and further refine reviews of published information on PaymentAccuracy.gov. Monitoring. To help agency leaders track and independently validate effectiveness and sustainability of corrective measures, ETA reported that it holds states accountable for reducing UI improper payments through using performance measures and monitoring states to ensure that the administration of the state’s UI program is in compliance with federal law and state law. ETA also reports holding states accountable for UI performance deficiencies by requiring states to submit corrective action plans outlining milestones to improve program performance and requiring states to submit quarterly updates detailing state actions toward implementation of the milestones. Furthermore, DOL reported that its ETA requires states to conduct quality assurance audits of a sample of paid UI claims to determine if the payment was accurate or improper and that states use a diagnostic tool to report the audit findings, including the root cause and the responsibility for improper payments. Demonstrated progress. To demonstrate progress in implementing corrective measures that address the root causes of high-risk areas, ETA stated that it uses performance measures to evaluate states’ UI operations and has established a fiscal year 2025 agency priority goal of reducing the UI improper payment rate. According to DOL, ETA’s actions have helped decrease the estimated UI improper payment rate from 16.5 percent in fiscal year 2023 to 15.9 percent in fiscal year 2024. |

|

Department of the Treasury—Internal Revenue Service (IRS) Additional Child Tax Credit American Opportunity Tax Credit Earned Income Tax Credit |

Leadership commitment. To initiate and sustain progress, IRS reported that it designated the Director of IRS Refund Integrity and Compliance Services as the accountable official. In addition, IRS reported sharing data with the Department of Health and Human Services (HHS) and its Office of Child Support Enforcement and the Social Security Administration to enable IRS to identify discrepancies in taxpayer claims and improve detection of improper Additional Child Tax Credit claims. Capacity. Capacity represents the resources (i.e., skilled staff, adequate funding, internal controls, technology, and management and organization infrastructure) to resolve key risks. IRS reported using data sharing with HHS and outreach to improve payment accuracy. IRS also reported that it has the necessary controls and resources but cited statutory limits as the main barrier to reducing improper payments. IRS stated that it has proposed various legislative changes over the years aimed at providing more effective tools for managing refundable tax credits (RTC). For example, in the fiscal year 2025 President’s Budget, IRS stated that it proposed an increase and expansion of its authority to address noncompliance or inappropriate behavior by paid tax return preparers and e-file providers. Action plan. To define the root causes and solutions and provide an approach for substantially completing corrective measures, IRS reported that it identified statutory and program design limits as the main causes of RTC improper payments, along with taxpayer misreporting and complex eligibility rules. IRS stated that its planned corrective actions, including pre-refund examinations and preparer oversight, were scheduled for completion in fiscal year 2025. To improve Treasury’s compliance efforts, Treasury’s OIG, in its report issued in May 2025, recommended that the Commissioner, Taxpayer Services, 1. work with the Office of Tax Policy to request additional legislative considerations that will help IRS reduce improper payments associated with RTCs; 2. conduct an analysis of the new identity verification procedures to (1) identify the impact on taxpayer filing behavior and refundable credits claimed, (2) evaluate the number of returns selected for post-refund review, and (3) measure the dollar impact to tax administration and improper payments; and 3. upon completing the analysis noted in Recommendation 2, determine whether the new identity verification procedures should be continued. Monitoring. To help agency leaders track and independently validate effectiveness and sustainability of corrective measures, IRS stated that it annually updates its RTC compliance plans and internal revenue manuals. IRS also provides training to employees who administer RTCs. Demonstrated progress. To demonstrate progress in implementing corrective measures that address the root causes of high-risk areas, IRS cited recent declines in estimated improper payment rates for RTCs. From fiscal year 2023 to fiscal year 2024, the Additional Child Tax Credit improper payment rate decreased from 14.5 percent to 10.75 percent, the American Opportunity Tax Credit improper payment rate decreased from 31.6 percent to 27.7 percent, and the Earned Income Tax Credit improper payment rate decreased from 33.5 percent to 27.3 percent. However, IRS emphasized that without significant restructuring of RTCs, including legislative action, the RTC improper payment rate will not be reduced below 10 percent. |

|

Department of Agriculture (USDA) Farm Service Agency (FSA) Emergency Conservation Program (ECP) - Disasters |

Leadership commitment. To initiate and sustain progress, USDA reported that it designated the Acting Deputy Administrator for Farm Programs and the Deputy Administrator for Field Operations as the accountable officials for ECP - Disasters compliance. According to USDA, FSA’s employee performance plans focus on requirements for supervisors to timely address PIIA findings, provide training to employees, and ensure that processes for program integrity and proper audit documentation are included in software to monitor the administration of ECP - Disasters. Capacity. Capacity represents the resources (i.e., skilled staff, adequate funding, internal controls, technology, and management and organization infrastructure) to resolve key risks. USDA reported that it needs funds for future software upgrades. USDA stated that it developed and released new software to process applications more efficiently and reduce administrative errors. Additionally, USDA stated that it provides ongoing training to state office staff on updated policy requirements and PIIA deficiencies. Furthermore, USDA reported providing training on policy and software, PIIA findings, and root causes of improper payments to all FSA employees with ECP - Disasters responsibilities. Action plan. To define the root causes and solutions and provide an approach for substantially completing corrective measures, USDA reported that it identified administrative errors as the leading causes of its improper payments. According to USDA, these errors included applications for ineligible participants; incompletely or improperly filed payment documentation; and missing, incomplete, or improperly filed ECP - Disasters forms. USDA stated that its planned corrective actions include (1) integrating ECP - Disasters program spot-checks and program reviews into its internal Review and Documentation Tracking System to improve oversight and ensure timely review completion, (2) implementing a new policy requiring full completion of checklists before payments are issued, (3) reviewing a percentage of ECP - Disasters agreements to ensure adherence to policy, and (4) providing training to staff on updated policy requirements. USDA also stated that these planned corrective actions are scheduled for completion in fiscal year 2025. To improve USDA’s compliance efforts, the USDA OIG, in its report issued in May 2025, recommended that the agency work with the Office of Chief Financial Officer to take the following actions to ensure compliance with PIIA: 1. Improve processes and efforts to evaluate the effectiveness of corrective actions to assist in the reduction of the improper payments estimate rate below the 10 percent threshold. 2. Develop and monitor agency-level corrective actions corresponding to the identified root causes of improper payments. 3. Conduct ongoing monitoring of the state-level corrective actions and ensure that these corrective actions are being implemented. 4. Continue working with states to identify state-specific corrective actions and ensure that these corrective actions are being implemented. 5. Enhance corrective actions to specifically target and address the primary root causes associated with the highest improper payment percentage. Additionally, in its report issued in May 2025, OIG found that USDA failed to demonstrate improvements in payment integrity for FSA ECP-Disasters. To improve USDA’s compliance efforts in this area, the OIG recommended that management take the following actions to ensure compliance with PIIA: 1. Maintain a focus on continuous improvement in the development and implementation of new mitigation strategies (e.g., examination of existing controls in place and the implementation of more effective controls) to decrease improper payment and unknown payment rate to a tolerable rate each year. If a program’s improper payment and unknown payment rate does not improve or increases, take sufficient steps to identify root causes and implement appropriate corrective action that will reduce the rates year-over-year until the rate is below 10 percent. 2. Where applicable and cost effective, implement automated enhancements to better prevent and detect errors. Monitoring. To help agency leaders track and independently validate effectiveness and sustainability of corrective measures, USDA reported that it plans to incorporate internal FSA ECP-Disasters program spot-checks and program reviews into its Internal Review and Documentation Tracking System to document results, analyze results for training needs, evaluate the progress of corrective actions related to these reviews, and identify areas for improvement. Additionally, USDA stated that it solicited and received feedback from state and county offices on the effectiveness of the ECP training offered. Demonstrated progress. To demonstrate progress in implementing corrective measures that address the root causes of high-risk areas, USDA stated that it published a payment integrity dashboard in March 2025 to analyze internal review findings related to PIIA requirements. According to USDA officials, the results of this analysis will help USDA target corrective actions and provide additional training and oversight to states and counties with the highest rates of improper payments. Despite establishing reduction targets for ECP-Disasters, USDA reported that the improper payment rate for this program has increased from 40.4 percent in fiscal year 2023 to 45.2 percent in fiscal year 2024. |

|

Department of Veterans Affairs (VA) Purchased Long-Term Services and Supports |

Leadership commitment. To initiate and sustain progress, VA reported that it designated the Deputy Executive Director of Home and Community Based Purchase Care as the accountable official. According to VA, senior leaders are held to performance criteria covering prevention, detection, and remediation of improper payments, with oversight from VA’s Performance Review Board. VA also stated that it collaborates with third-party administrators to correct billing practices and transition to an automated claims adjudication system. Capacity. Capacity represents the resources (i.e., skilled staff, adequate funding, internal controls, technology, and management and organization infrastructure) to resolve key risks. VA reported that it has adequate resources and is not requesting additional funding. VA stated that it is continuing to implement new software to streamline claims, automate eligibility determinations, and enhance reporting and auditing capabilities. Additionally, VA stated that it plans to develop new and enhanced claims processing training. Action plan. To define the root causes and solutions and provide an approach for substantially completing corrective measures, VA reported identifying data access issues, manual processing errors, and documentation gaps as root causes. VA also reported identifying the automation of eligibility determinations and additional training as its primary mitigation strategies, with planned completion dates in fiscal year 2025. To improve VA’s compliance efforts, VA’s OIG, in its report issued in May 2025, recommended that the Under Secretary for Health reduce improper and unknown payment rates to below 10 percent for the Purchased Long-Term Services and Supports program. (This repeat recommendation has been in place since the VA OIG’s fiscal year 2020 report, which was the office’s first review under PIIA.) Monitoring. To help agency leaders track and independently validate effectiveness and sustainability of corrective measures, VA stated that it monitors the progress and results of corrective action implementation each quarter. Additionally, VA stated that it performs an annual effectiveness review to measure whether a corrective action has reduced or is properly designed to reduce improper and unknown payments for a specific root cause, based on a set benchmark. According to VA, the annual effectiveness review process allows VA to create or update corrective actions as necessary. Demonstrated progress. To demonstrate progress in implementing corrective measures that address the root causes of high-risk areas, VA stated that it updates its corrective action plans annually, monitors progress on implementing the corrective actions every quarter, and performs an annual effectiveness review to measure whether corrective actions have reduced or are properly designed to reduce improper payments, based on a set benchmark. Additionally, VA stated that it has demonstrated progress by reporting decreasing improper payment rates for the Purchased Long-Term Services and Supports program from 38.7 percent in fiscal year 2023 to 13.5 percent in fiscal year 2024. |

Source: GAO analysis of Office of Management and Budget PaymentAccuracy.gov data. | GAO‑26‑108044

GAO has made numerous recommendations to improve payment integrity for agencies. Table 5 identifies open recommendations as of January 2026 to the Departments of Labor’s (DOL) unemployment insurance program and the Treasury’s refundable tax credit program, which have been noncompliant under the Payment Integrity Information Act of 2019 (PIIA) for 4 consecutive fiscal years. There were no payment integrity-related GAO open recommendations for the Departments of Agriculture or Veterans Affairs for programs we reviewed.

Table 5: GAO Open Recommendations on Improper Payments and Fraud to the Department of Labor (DOL) and the Department of the Treasury

|

GAO report number |

GAO report title |

Recommendations |

|

Recommendations to DOL: Unemployment insurance |

||

|

COVID-19 Relief: SBA and DOL Should Improve Processes to Identify and Recover Overpayments |