Report to Congressional Committees

United States Government Accountability Office

A report to congressional committees.

For more information, contact: Jessica Lucas-Judy at lucasjudyj@gao.gov

What GAO Found

In the 2025 filing season, the Internal Revenue Service’s (IRS) tax return processing and customer service performance were similar to prior years. IRS did not meet its 13-day goal to process paper returns but took fewer days to do so in 2025 (16) than in 2024 (20). IRS also answered about 9 million phone calls in both years. IRS’s backlog of taxpayer correspondence remained above pre-pandemic levels at the end of filing season and fiscal year 2025 as IRS continued to struggle balancing demands of phone service and correspondence. But IRS does not have a plan to reduce the backlog. Without a plan, IRS risks not effectively reducing its backlog and may provide less timely service to taxpayers.

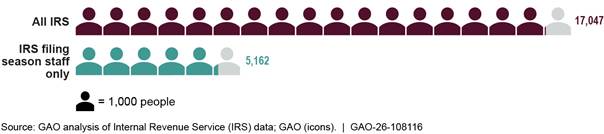

In 2025, IRS experienced large-scale changes to its workforce. IRS adjusted operations to comply with new directives, including return to in-person work. IRS data show that 17,047 employees—around 17 percent of IRS’s workforce as of January 2025—left IRS via deferred resignation and early retirement programs in 2025. This included 5,162 filing season staff in units that process returns and provide customer service. However, the 2025 filing season was mostly insulated from these changes. IRS required filing season staff who accepted deferred resignation or early retirement to stay until after the filing season. IRS officials told GAO that IRS is developing a new strategic workforce plan to align with the current administration’s priorities, and its prior plans are on hold. If IRS’s new plan does not address its workforce challenges, IRS will be unable to systematically identify future workforce needs and strategies for related goals.

Note: For more details on IRS’s 2025 separations data, see figure 9 in GAO-26-108116.

IRS had vacancies and turnover in leadership roles throughout 2025, including having seven different commissioners through August. IRS officials were uncertain about the status of some workforce changes like agency reorganization plans, and some modernization efforts for filing season functions have been in flux, such as activities to digitize paper documents. However, IRS lacks a team that is responsible for day-to-day management of agency reforms and ensuring quality information is shared across IRS. Without such an implementation team, IRS may struggle to ensure that reform efforts are successful and sustainable, which could in turn hinder IRS’s ability to provide quality services to taxpayers.

In addition, in December 2025 amid implementing the One Big Beautiful Bill Act (OBBBA), an IRS internal report stated that critical technology systems would not be ready for the 2026 filing season start. It also stated that return processing and customer service functions would enter the season undertrained or understaffed, which could result in errors and poor service for taxpayers.

Why GAO Did This Study

During the annual tax filing season, IRS processes millions of tax returns and issues hundreds of billions of dollars in taxpayer refunds. IRS also provides customer service to tens of millions of taxpayers. IRS carried out the 2025 filing season and its plans for 2026 during a time of swift, immense change for the federal workforce. IRS’s workforce changes and recent tax law changes could exacerbate the agency’s long-standing challenges to process tax returns on time and meet customer service demands.

GAO was asked to review IRS’s 2025 filing season performance. This report assesses IRS’s (1) staffing levels and processing and customer service performance during the 2025 filing season, and (2) through the end of fiscal year 2025, and (3) workforce planning and modernization efforts for future filing season operations. GAO reviewed IRS and Department of the Treasury documentation, executive orders, and OBBBA tax provisions. GAO analyzed IRS staffing and performance data related to tax return processing and customer service during and after the 2025 filing season. GAO visited one IRS processing facility and interviewed IRS officials and stakeholders from three tax industry groups.

What GAO Recommends

GAO is making three recommendations to IRS to implement a plan to address its correspondence backlog, update its strategic workforce plan, and establish an implementation team to manage agency reform efforts. IRS neither agreed nor disagreed with these recommendations and said it would provide additional details in its response to the final report.

Abbreviations

|

AM |

Accounts Management |

|

CEO |

Chief Executive Officer |

|

CSR |

Customer Service Representative |

|

DRP |

Deferred Resignation Program |

|

ERC |

Employee Retention Credit |

|

HCO |

Human Capital Office |

|

IRA |

Inflation Reduction Act of 2022 |

|

IRM |

Internal Revenue Manual |

|

IRS |

Internal Revenue Service |

|

OBBBA |

One Big Beautiful Bill Act |

|

OMB |

Office of Management and Budget |

|

OPM |

Office of Personnel Management |

|

RIF |

Reduction in Force |

|

SP |

Submission Processing |

|

SSA |

Social Security Administration |

|

TAC |

Taxpayer Assistance Center |

|

TDRP |

Treasury Deferred Resignation Program |

|

TIGTA |

Treasury Inspector General for Tax Administration |

|

VERA |

Voluntary Early Retirement Authority |

|

VSIP |

Voluntary Separation Incentive Payment |

This is a work of the U.S. government and is not subject to copyright protection in the United States. The published product may be reproduced and distributed in its entirety without further permission from GAO. However, because this work may contain copyrighted images or other material, permission from the copyright holder may be necessary if you wish to reproduce this material separately.

March 16, 2026

The Honorable Mike Crapo

Chairman

The Honorable Ron Wyden

Ranking Member

Committee on Finance

United States Senate

The Honorable Jason Smith

Chairman

The Honorable Richard E. Neal

Ranking Member

Committee on Ways and Means

House of Representatives

During the annual tax filing season, the Internal Revenue Service (IRS) undertakes a complex effort to process over 150 million paper and electronic tax returns from individuals and businesses, and issue hundreds of billions of dollars in taxpayer refunds. IRS also enforces tax laws and provides customer service to tens of millions of taxpayers on a range of critical issues, including providing information on delayed returns and suspected identity theft.

IRS carried out the 2025 filing season and its plans for 2026 during a time of swift, immense change for the federal workforce. For example, like other agencies, IRS adjusted operations to comply with directives to cease hiring efforts, return employees to in-person work, and reduce the federal government’s real estate footprint, among other things. IRS has also experienced long-standing operational challenges on which we have previously reported. For example, IRS faced challenges processing paper returns on time, reducing its backlog of millions of pieces of taxpayer correspondence, and managing ongoing human capital issues like staff attrition and use of overtime.[1]

Public Law 119-21—commonly known as the One Big Beautiful Bill Act (OBBBA)—was enacted in July 2025 and included several changes to federal taxes, credits, and deductions that will be in effect for the 2026 filing season.[2] When implementing tax law changes, IRS revises and updates tax forms, internal IT systems, and its public-facing website, among other things. We previously reported that IRS faced challenges implementing significant tax law changes in prior years, including provisions in the Tax Cuts and Jobs Act of 2017 and various COVID-19 pandemic relief legislation.[3]

You asked us to assess IRS’s performance during the 2025 filing season. Additionally, the Inflation Reduction Act of 2022 (IRA) includes a provision for us to support oversight of the use of funds appropriated in the IRA.[4] In this report, we assess (1) IRS’s staffing levels and performance processing individual and business tax returns and providing customer service during the 2025 filing season; (2) the extent to which IRS’s staffing levels and performance changed after the filing season; and (3) IRS’s workforce planning and modernization efforts, including those using IRA funds, for future filing season operations.

To address our first and second objectives, we analyzed IRS’s staffing data to determine agency headcounts and overtime use within IRS’s Submission Processing (SP) and Accounts Management (AM) units. We also analyzed IRS’s weekly filing season performance data on processing electronic and paper tax returns for individuals and businesses, and providing customer service (via telephone, correspondence, online, and in person). We reviewed relevant IRS documentation to understand IRS’s timeliness in processing returns and the volume of returns scanned; and ability to answer telephone inquiries, respond to taxpayer correspondence, provide in-person services, and provide service through its website. We also interviewed IRS officials to understand contextual factors related to performance, such as any staffing and technology changes.

The 2025 staffing data that we used in this report were from January to December 2025. The 2025 performance data that we used were from (1) the 2025 filing season, which began in late January 2025 and ended April 15, 2025, and (2) the post-filing season through the end of fiscal year 2025 (September 30), the most recent data available at the time of our review.[5] We compared these data to IRS’s staffing and performance in prior years. We assessed the reliability of IRS’s staffing and performance data by reviewing existing information about the data and the systems that produced them, and interviewing agency officials knowledgeable about the data. We determined that these data were sufficiently reliable for the purposes of our reporting objectives.

To provide additional context for the first two objectives, we visited the IRS facility in Austin, Texas, in April 2025 to observe return processing and customer service representatives (CSR) answering taxpayer calls and handling correspondence. We selected the Austin facility because it processes individual returns and answers taxpayer telephone calls.

To address our third objective, we reviewed Department of the Treasury and IRS documentation that included reports, guidance, and communications regarding IRS’s operations, workforce decisions, IRA spending, and public outreach. We reviewed executive orders, presidential memorandums, and guidance from the Office of Personnel Management (OPM) and Office of Management and Budget (OMB) that are relevant for IRS operations in 2025 and 2026. We also reviewed OBBBA as well as executive orders and other directives to identify key provisions that may require IRS operational changes in advance of the 2026 filing season.

In addition, we interviewed IRS officials to understand IRS’s workforce planning efforts, use of IRA funds to support filing season functions, and implementation of tax law changes for the 2026 filing season. We also used a nongeneralizable selection of three tax industry groups, including tax preparation and software development businesses and a professional organization. We interviewed industry stakeholders from these organizations about their views on the support IRS offered pertaining to tax law changes prior to the 2026 filing season.

We conducted this performance audit from January 2025 to March 2026 in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

Background

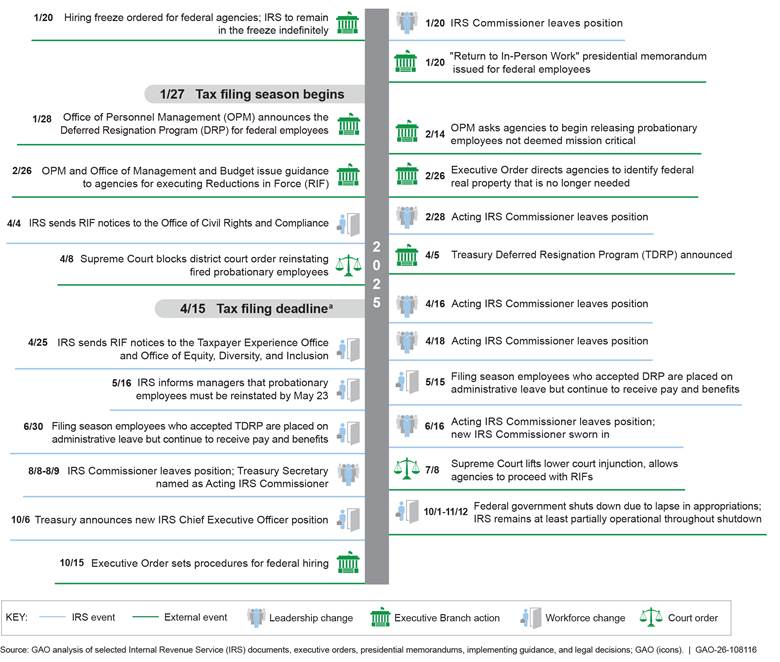

2025 Federal Workforce Changes

In 2025, the administration implemented multiple changes to federal workforce policies that had implications for IRS, as shown in figure 1. For example, in January 2025 the administration implemented a government-wide hiring freeze and ordered the return to in-person work for all employees of executive branch agencies with limited exceptions.[6] These and other related actions were aimed at restructuring and reducing the size of the federal civilian workforce as part of a larger executive initiative to streamline and transform agencies’ operations, according to the administration.

aTaxpayers who needed additional time could request an extension until October 15. However, taxpayers who owed taxes had to pay by April 15 to avoid penalties and interest.

In January 2025, OPM announced the Deferred Resignation Program (DRP), under which federal agencies could offer employees the ability to resign but retain all benefits and pay up to September 30, 2025. Eligible employees were also able to take the DRP in conjunction with the Voluntary Early Retirement Authority (VERA) and retain pay and benefits through September 30, 2025.[7] OPM’s website stated that an employee whose retirement date was between October 1, 2025 and December 31, 2025 could still take deferred resignation with certain exceptions, and that their deferred resignation date would be extended to match their retirement date.[8] In addition, the Voluntary Separation Incentive Payment (VSIP) program allowed for eligible employees to receive a lump sum payment to resign or retire. VSIP could also be taken in conjunction with VERA.

In April 2025, Treasury began offering a second resignation program called the Treasury Deferred Resignation Program (TDRP). This program offered the same incentives as the DRP, but it allowed employees to resign no sooner than April 28. The TDRP could also be taken in conjunction with VERA.

In response to a February 2025 executive order, OMB and OPM released a joint memorandum instructing agencies to create reduction in force (RIF) and reorganization plans that include initial cuts and reductions to agency staffing levels.[9] The memorandum also directed agencies to prepare for large-scale staff reductions. This guidance stated that agencies should submit plans in March and April 2025 for OMB and OPM’s review and approval. The plans were to propose the agency’s future organizational structure and functions, among other things.

OPM stated that probationary employees whose positions were deemed not mission critical were to be terminated no later than February 17, 2025.[10] The administration also issued an executive order directing agencies to identify termination rights for its federal real property leases and for the Administrator of the General Services Administration to submit a plan to OMB for disposing of property that the agency determined is no longer needed.[11]

Return Processing

Every filing season, individuals and businesses submit their tax returns to IRS electronically or on paper. IRS processes the returns to determine if the information provided is sufficiently accurate to post the return to the taxpayer’s master file account, and to collect the amount the taxpayer owes the government, or issue the amount the taxpayer is entitled to as a refund.[12]

During return processing, staff in IRS’s Submission Processing (SP) unit are to check for consistency and errors identified through manual and automated processes and correct the returns when possible and allowable.[13] If correction is not possible, IRS is to notify the taxpayer about any additional information that may be needed to complete the return. SP staff also issue refunds and tax notices.

IRS sets recommended timelines for how long certain types of paper tax returns should take to be initially reviewed and processed. For example, IRS policy states that Form 1040 paper returns (i.e., individual income tax returns) are to be processed within 13 working days.[14] As we have previously reported, automated processes are generally more efficient and cost effective than paper-based processes, and any delays in issuing refunds can increase costs to IRS and burden the taxpayer.[15]

Taxpayer Support

Taxpayers can get assistance from IRS in ways that include:

· Telephone. Throughout the year, taxpayers can speak with a customer service representative (CSR) in IRS’s Accounts Management (AM) unit to obtain information about their accounts. Taxpayers can also listen to recorded tax information or use automated phone services to learn the status of their refund or account information, such as a balance due.

· Correspondence. Taxpayers use paper, or in some cases digital, correspondence to communicate with IRS. Correspondence can cover a wide range of topics, including responding to IRS requests for information to help process a return or verify a taxpayer’s identity. It can also include complex account adjustments, such as amended returns and duplicate return filings, refund and account inquiries, and collection notice disputes, among others.

CSRs respond to taxpayer correspondence in addition to answering telephone calls. IRS’s policy is to generally respond to correspondence within 30 days of receipt. IRS considers correspondence that is older than 45 days to be “overage,” or late.[16]

· In person. Taxpayers can receive face-to-face assistance at Taxpayer Assistance Centers (TAC) across the country. TAC staff can provide taxpayers with help in a variety of ways. These include authenticating taxpayers whose returns have been held for potential identity theft, assisting taxpayers applying for an Individual Taxpayer Identification Number, handling cash payments from taxpayers, and assisting taxpayers with account adjustments.

· Online. Taxpayers can use IRS’s online services to, for example, check their refund status, get a tax transcript, and make payments or check on the status of a payment. They can also apply for plans to pay taxes due in scheduled payments (installment agreements).[17]

Recent IRS Appropriations and Changes in IRA Funding

IRS’s operating budget is funded by annual appropriations and other resources, such as unobligated balances from prior years and reimbursable items. For fiscal year 2025, Congress passed a continuing resolution that appropriated $12.3 billion to IRS—the same amount as in fiscal year 2024.

The funds were allocated among three budget activities as follows:

· $2.8 billion for taxpayer services, which includes many filing season operations like processing tax returns and providing assistance to taxpayers filing returns and paying taxes;

· $4.1 billion for operations support, which includes rent, facilities services, printing, postage, security, information systems, and telecommunications support; and

· $5.4 billion for enforcement, which includes determining and collecting owed taxes, providing legal and litigation support, and enforcing certain criminal statutes.

For fiscal year 2026, IRS was appropriated $11.2 billion—a 9 percent decrease from 2025 appropriations.[18] This included $3 billion for taxpayer services, which is a 9 percent increase from last year. Treasury had requested $3.6 billion for taxpayer services for fiscal year 2026, which would have been a 31 percent increase from 2025 appropriations.[19]

In August 2022, the IRA was enacted. The act provided approximately $79.4 billion in multi-year funding available for IRS to spend through fiscal year 2031.[20] Subsequent laws have rescinded or prevented IRS from spending over half of these funds, reducing the amount IRS can spend to $25.9 billion.[21] In January 2024 and January 2025, we reported that IRS used IRA funding to support hiring and modernization efforts for filing season operations.[22]

Tax Law Changes

The One Big Beautiful Bill Act (OBBBA) included new and updated tax deductions and credits that IRS and Treasury must implement for the 2026 filing season. For example:

· No Tax on Tips. Employees and self-employed individuals may deduct qualified tips received in occupations listed by IRS as customarily and regularly receiving tips on or before December 31, 2024. For individual taxpayers to claim the deduction, the tips must be reported on the appropriate tax forms (i.e., Forms W-2 or 1099) or reported directly by the individual on Form 4137 to figure the Social Security and Medicare taxes owed on tips not reported to the employer.

· No Tax on Overtime. Individuals who receive qualified overtime compensation may deduct the pay that exceeds their regular rate of pay (such as the “half” portion of “time-and-a-half” compensation) that is required by the Fair Labor Standards Act and reported on a Form W-2, 1099, or other specified statement furnished to the individual.

The 2025 Government Shutdown and IRS

From October 1, 2025, to November 12, 2025, much of the federal workforce was furloughed because of a lapse in appropriations for fiscal year 2026. Although IRS was one of the affected agencies that did not receive appropriations, IRS reported using IRA funding to continue normal operations through October 7.

IRS furloughed approximately half of its employees on October 8 and began limiting some activities, such as issuing some refunds and providing live telephone assistance. IRS also ceased other activities, including closing TACs and cancelling in-person appointments. IRS announced that during the shutdown the agency would continue operations critical to the 2026 filing season, including testing and preparing relevant programs.

2025 Filing Season Staffing and Performance Were Similar to Prior Years, but IRS Lacks a Plan to Reduce Its Correspondence Backlog

Federal Workforce Changes Had Some Impact on 2025 Filing Season Staffing and Overtime Use

During the 2025 filing season, IRS’s filing season operations were mostly insulated from IRS-wide workforce changes, including the deferred resignation and early retirement programs. As described above, IRS staff were given the opportunity to resign via the DRP, TDRP, and VSIP. Filing season staff who accepted the DRP or TDRP were required to continue working until May 15 and June 30, respectively, because Treasury determined filing season staff to be critical to IRS operations. IRS chose these dates to ensure that filing season staff did not leave the agency at times of peak taxpayer demand, according to IRS officials.

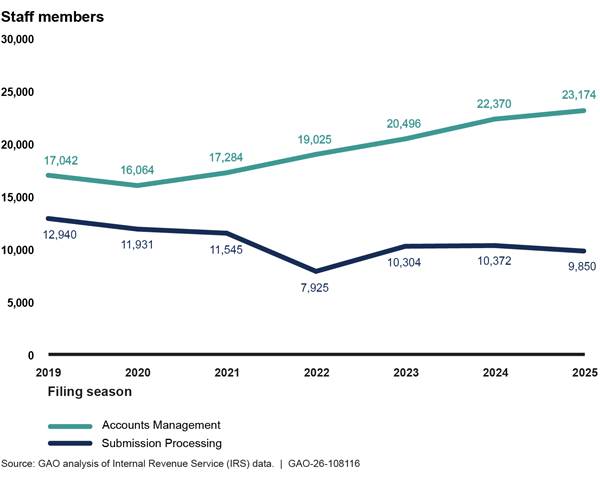

As a result, IRS ended the 2025 filing season with similar numbers of Submission Processing (SP) and Accounts Management (AM) staff as in 2024 (see fig. 2). IRS officials told us that being able to keep staff until after the filing deadline (April 15) allowed for a more successful filing season.

Figure 2: Number of IRS Accounts Management and Submission Processing Staff at the End of Each Filing Season, 2019-2025

Note: Staffing data are as of the last day of the pay period that ends that year’s filing season. The pay period ending dates are April 27, 2019; July 18, 2020; May 22, 2021; April 23, 2022; April 22, 2023; April 20, 2024; and April 19, 2025.

As described earlier, IRS was subject to a government-wide hiring freeze that limited federal agencies’ authority to hire new staff. The hiring freeze affected IRS’s ability to meet some of its fiscal year 2025 hiring goals, including within SP. At the time of the hiring freeze, SP had met 53 percent of its hiring goal (1,745 of 3,305 planned new hires) and ended the 2025 filing season with 9,850 staff—522 fewer employees than the same time in 2024. However, AM hired and onboarded most staff before the hiring freeze went into effect. As a result, AM met 103 percent of its hiring goal (4,824 of 4,700 planned new hires) and ended the filing season with 23,174 staff—an increase of 804 employees from the same time in 2024.

Other workforce changes had a minimal impact on 2025 filing season operations. For example:

· Probationary employee terminations. IRS designated almost all filing season probationary staff as critical. As a result, 14 of the 7,315 probationary employees whom IRS terminated in February 2025 were filing season staff. [23] In May 2025, IRS informed managers that all previously terminated probationary employees were reinstated and should be returned to a full-work status. IRS data show that, as of December 2025, 60 percent (4,419) of these probationary employees either did not return to IRS or separated through the deferred resignation programs. IRS officials told us that one of the 14 terminated filing season probationary employees did not return to IRS.

· Return-to-office requirements. In March 2025, IRS canceled telework agreements and generally required employees to work in the office to comply with a presidential memorandum requiring employees to return to in-person work. IRS officials told us that the agency experienced challenges with employees returning to the office full time, including insufficient workspaces and parking spaces to accommodate staff. As a result, they said that CSRs were allowed to continue teleworking periodically. IRS officials told us that SP staff who process returns were mostly unaffected by the return to in-person work because staff were already working in person.

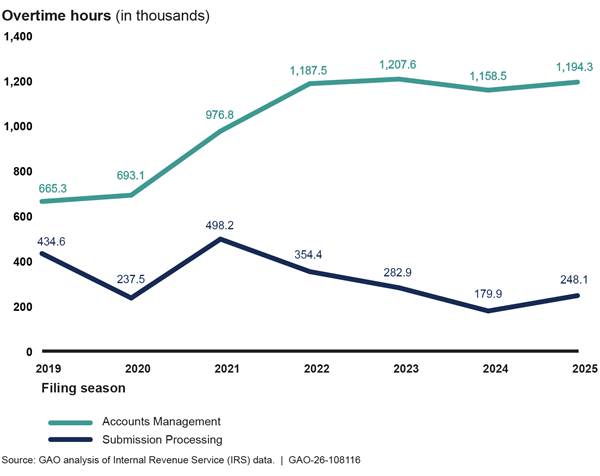

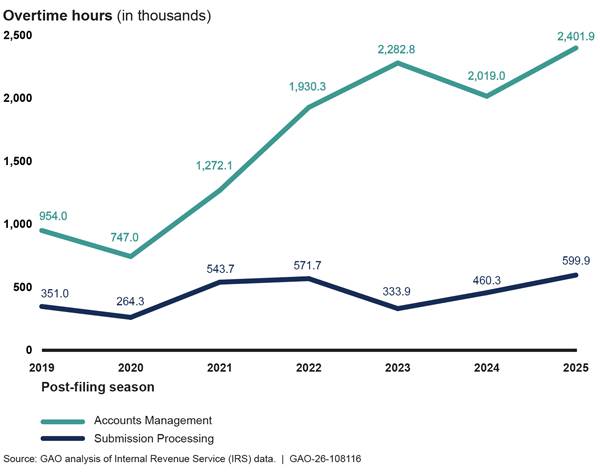

During the 2025 filing season, IRS continued to use overtime to carry out filing season operations, including for processing returns and answering taxpayer phone calls. AM’s use of overtime has generally increased in recent years, as shown in figure 3. IRS officials said that overtime increased during this period to address a backlog of taxpayer correspondence caused in part by staff attrition.

SP’s use of overtime declined from 2021 to 2024, in part because of the decrease in returns inventories following the COVID-19 pandemic, according to IRS officials. However, overtime used to process returns increased 38 percent from the 2024 to 2025 filing season. IRS officials said this increase was primarily due to the hiring freeze affecting their ability to meet hiring goals.

Figure 3: IRS Accounts Management and Submission Processing Total Overtime Hours, 2019-2025 Filing Seasons

Note: Overtime hour data are for hours charged in pay periods that span the filing season for each year. The dates for filing season pay period data are January 20, 2019, to April 27, 2019; January 19, 2020, to July 18, 2020; January 31, 2021, to May 22, 2021; January 16, 2022, to April 23, 2022; January 15, 2023, to April 22, 2023; January 28, 2024, to April 20, 2024; and January 26, 2025, to April 19, 2025. Therefore, some filing seasons include more pay periods than others.

In January 2020, we reported that IRS has consistently used overtime to meet processing milestones and respond to taxpayer phone calls and correspondence. We also noted that, if not well managed, overtime can be expensive, inefficient, contribute to skills gaps, and negatively affect employee morale. We recommended that IRS develop and implement a strategy for the efficient use of overtime.[24] IRS agreed with the recommendation but said that its existing process for the use and approval of overtime is sufficient and that the agency would not take any further action. In December 2025, IRS officials reaffirmed their position and told us that the agency continues to use overtime as a tool to address its workload. However, IRS’s use of overtime has remained high since we issued our recommendation, which may indicate an inefficient use of overtime. We continue to believe that a strategy would help ensure efficient use of overtime.

IRS Improved Processing of Returns Compared to Last Filing Season

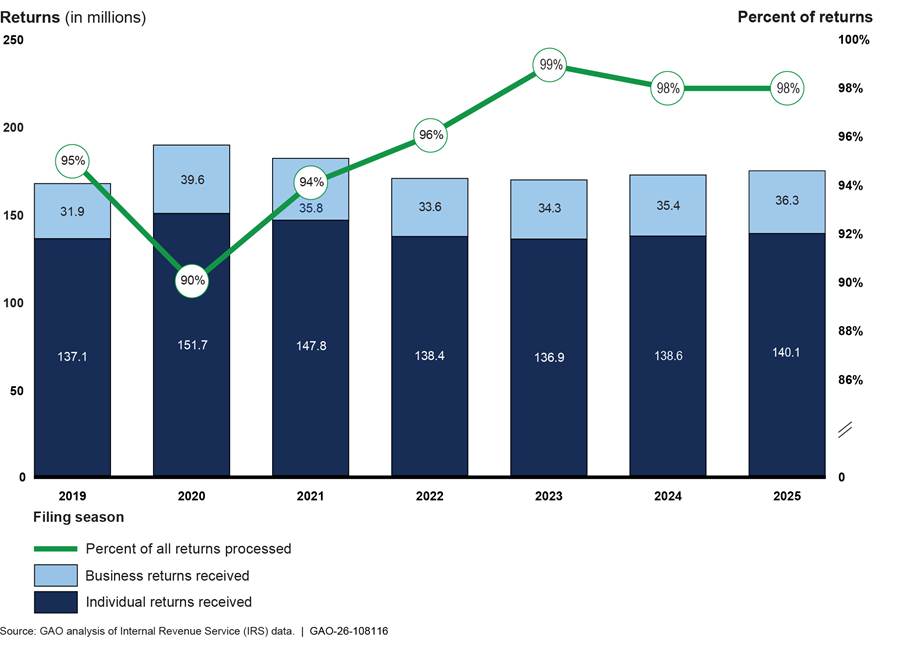

IRS’s 2025 filing season processing performance improved slightly from 2024. For example, IRS processed approximately 172 million individual and business returns by the end of the 2025 filing season. This was 1.9 million more returns (an increase of 1.1 percent) compared to the same time in 2024. See appendix I for a comparison of IRS’s 2025 return processing performance to prior years.

In addition, IRS took an average of 16 days to process individual paper returns (i.e., Form 1040s) during the 2025 filing season. While this time was an improvement from the 20-day average in 2024, it was above IRS’s policy of 13 days or less.[25] IRS officials said the SP unit used more voluntary and mandatory overtime and repurposed IRS staff from other units to help with workloads, but that insufficient staffing caused by the hiring freeze resulted in IRS not meeting its cycle time goal.

Overall, fewer taxpayers filed paper returns during the 2025 filing season, and IRS processed more of those returns compared to the 2024 filing season, as shown in table 1.

Table 1: Paper Individual (1040 Series) Income Tax Returns Received and Processed, Filing Seasons 2024-2025

|

Number of paper returns (in thousands) |

|

|

|

|

|

2024 |

2025 |

Percent Change (%), from 2024 to 2025 |

|

Received by |

|

|

|

|

Internal IRS Staff |

4,524 |

4,378 |

-3.24 |

|

Outside Vendor Scanning |

83 |

25 |

-69.45 |

|

Total Paper |

4,607 |

4,403 |

-4.43 |

|

Processed by |

|

|

|

|

Internal IRS Staff |

3,030 |

3,096 |

2.17 |

|

Outside Vendor Scanning |

76 |

24 |

-67.62 |

|

Total Paper |

3,106 |

3,121 |

0.47 |

Source: GAO analysis of Internal Revenue Service (IRS) data. | GAO‑26‑108116

Note: When IRS receives paper returns, it reviews, prepares, and transcribes the data into its processing systems. Outside vendors scan the returns using software that extracts the information and transmits it to IRS in the same format as an e-filed return. Once returns are entered into IRS’s processing systems, the returns may still not be fully processed and refunds provided to the taxpayer if the return was stopped for various reasons. These reasons include a miscalculated tax credit, incorrect Social Security Number or Employer Identification Number, or suspected fraud.

The slight increase in total paper returns processed was driven by SP staff, who processed about 66,000 (2 percent) more returns in 2025 compared to 2024. Conversely, the outside vendors who scan paper returns received and processed approximately 52,000 (68 percent) fewer individual returns during the 2025 filing season compared to 2024. IRS officials attributed these decreases to scanning contracts ending with several outside vendors.

In January 2025, we reported that IRS planned to move more scanning efforts in house to reduce its reliance on outside vendors.[26] In August 2025, SP officials told us that they continue to internally scan some historic forms at IRS’s three submission processing facilities.[27]

IRS Maintained Similar Telephone and In-Person Performance to Last Filing Season, but Lacks a Plan to Address Its Correspondence Backlog

Phone Service

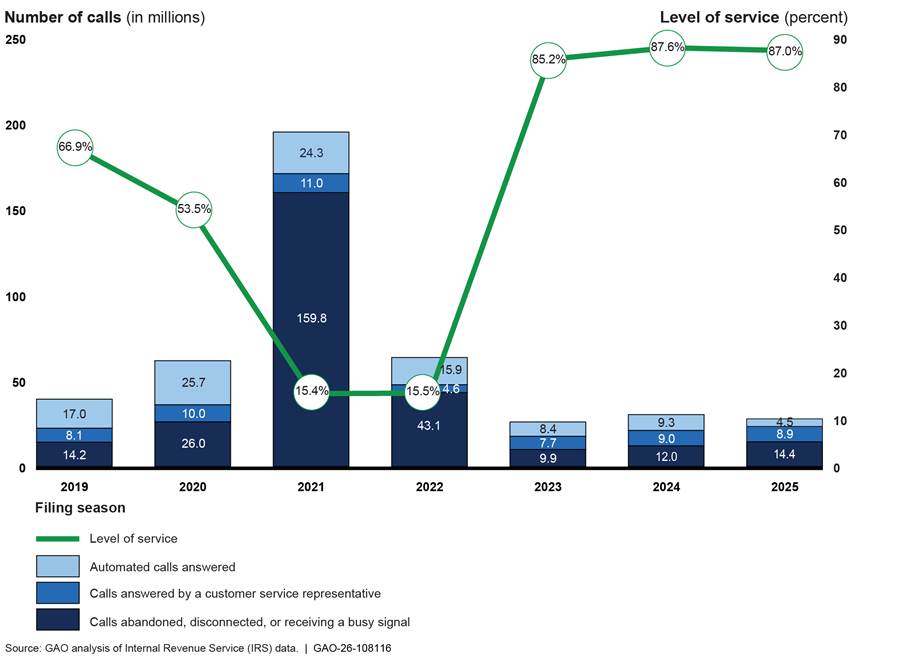

Each year, IRS sets a goal to answer a certain percentage of phone calls from taxpayers seeking live assistance, which it refers to as the “level of service.”[28] During the 2025 filing season, IRS reported an 87 percent level of service, exceeding the agency’s goal of 85 percent and just slightly under its performance in 2024 (see fig. 4). IRS’s level of service metric generally represents the number of taxpayers who reach a CSR divided by the number of calls the IRS system routes to them. However, not all calls that may require CSR assistance are routed directly to a CSR. For example, callers could be routed to an automated line, or after navigating IRS’s phone tree, decide to end calls without receiving information they need.[29]

Note: Telephone call data for the filing season are cumulative from January 1 of each year to: April 20, 2019; July 15, 2020; May 17, 2021; April 23, 2022; April 22, 2023; April 20, 2024; and April 19, 2025. IRS’s “level of service” calculation generally divides the number of taxpayers who reach a customer service representative (CSR) by the number of calls the IRS system routes to them. Calls routed for automated assistance and callers who hang up before they are placed in a queue are excluded from IRS’s calculation for “level of service.” Data from 2019 do not include all calls answered by a CSR, those that received a busy signal, or calls disconnected because IRS was not answering calls due to a 5-week lapse in appropriations, which ended in January 2019. For 2020, live telephone assistance was unavailable between late March and late April due to IRS closing all processing and customer service sites during the COVID-19 pandemic. IRS reopened live telephone assistance for identity theft-related issues on April 27, 2020, and began opening additional phone lines on May 11, 2020. All customer service telephone lines began reopening during the 2021 and 2022 filing seasons. IRS began its callback service in 2019, where taxpayers calling about certain services or topics can opt to receive a call back from IRS rather than wait on hold. According to IRS, all “callbacks” are included in phone volume figures from 2019 forward.

During the 2025 filing season, IRS received 27.9 million calls—about 2.4 million fewer than the agency received in 2024. CSRs answered 8.9 million of these calls in 2025, which was similar to 2024. Beginning in 2024, IRS transitioned to a new system for responding to phone calls using automation. By the beginning of the 2025 filing season, all calls were routed through this new system, according to agency officials. IRS officials told us that the number of calls answered by automation is not comparable between the 2024 and 2025 filing seasons because of this transition and differences in how the systems count calls answered by automation.[30] IRS’s automated systems answered 4.5 million calls during the 2025 filing season, compared to 9.3 million in 2024.

In addition, IRS officials told us that the number of calls disconnected or receiving busy signals increased during the 2025 filing season because of these differences in how the two systems count calls answered and outages that led to more taxpayers receiving a busy signal. The number of calls disconnected or receiving busy signals increased from 600,000 to 5.5 million between the 2024 and 2025 filing seasons. The majority (92 percent) of the increase was from disconnected calls, which IRS officials said were also not comparable between years because of the differences between the systems. See appendix I for additional data on IRS’s phone service and information on online services.

Correspondence Inventory

In addition to answering taxpayer calls, CSRs respond to taxpayer correspondence. IRS continued to face challenges responding to correspondence during the 2025 filing season. Millions of taxpayers waited for IRS to process a wide range of correspondence, including amended returns and documentation related to identity theft, both of which may result in a refund to the taxpayer.

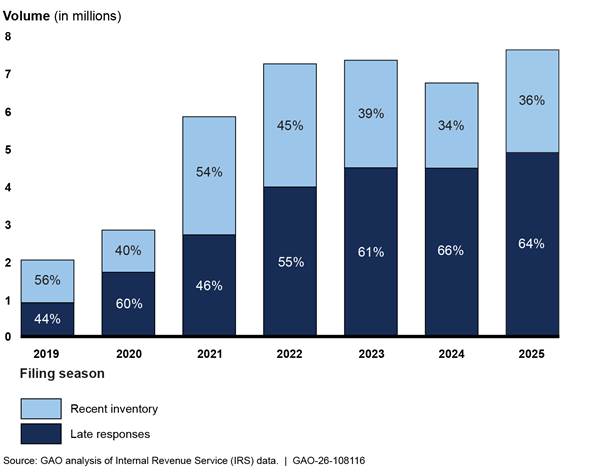

IRS’s inventory of taxpayer correspondence was 7.6 million at the end of the 2025 filing season, compared to 6.8 million at the end of the 2024 filing season—an increase of about 12 percent. Prior to the COVID-19 pandemic, IRS’s correspondence inventory at the end of the filing season was typically around 2 million pieces of correspondence.

IRS’s policy is to generally respond to correspondence within 30 days of receipt. Responses that take longer than 45 days are considered late, or what IRS calls “overage.”[31] At the end of the 2025 filing season, 4.9 million (64 percent) pieces of correspondence were considered late compared to 4.5 million (66 percent) in 2024. See figure 5 for IRS’s correspondence and overage rates for filing seasons 2019 through 2025.

Figure 5: IRS Correspondence Inventory and Overage Rates (Late Responses), as of the End of Each Filing Season, 2019-2025

Note: IRS’s policy is to generally respond to correspondence within 30 days of receipt, but it may take longer than that to respond to taxpayer correspondence depending on the type and complexity of the issue. IRS generally considers correspondence that is older than 45 days to be “overage.” Data reflect individual and business-related correspondence in IRS’s inventory as of the end of the filing seasons shown in the figure: April 20, 2019; July 18, 2020; May 22, 2021; April 23, 2022; April 22, 2023; April 20, 2024; and April 19, 2025. Inventory reflects all paper and digital correspondence IRS received but had not yet provided a response. Note that 2020 inventory does not reflect all taxpayer correspondence IRS received during 2020 due to IRS’s mail backlog (see GAO‑21‑251). As a result, some correspondence received in 2020 is reflected in the 2021 inventory.

We previously recommended that IRS estimate time frames for resolving its correspondence backlog and communicate this information to taxpayers and stakeholders.[32] IRS agreed with the recommendation and, in March 2024, launched a web page showing the receipt date (month and year) of the correspondence that IRS is currently processing.[33] In November 2024, IRS officials stated they do not intend to share information with taxpayers and stakeholders on how long taxpayers can expect to wait for a response once IRS begins to process a given piece of correspondence. In January 2026, IRS officials reaffirmed their position that they do not intend to share this information.

Without clear, timely information on IRS’s processing time frames for addressing taxpayer correspondence, taxpayers may continue to call, write, or visit IRS in person to try to obtain this information. As a result, the correspondence backlog may increase, and IRS will continue to struggle to meet demands for taxpayer customer service.

For years, IRS has struggled to balance demands to maintain quality telephone service levels and respond timely to written correspondence, as we have previously reported.[34] These different IRS customer service functions are interdependent, often sharing the same staff. Consequently, IRS’s ability to respond timely to written correspondence has been dependent on staff availability and the agency’s allocation of CSRs between answering phones and correspondence. During the 2025 filing season, CSRs spent 58 percent of their time on phone service and 42 percent responding to correspondence, according to IRS data.[35]

IRS officials told us that the agency prioritizes phone service over correspondence during the filing season. They also told us that to maintain an 85 percent level of service, CSRs must remain available to take calls, thus they often spend idle time waiting for the phones to ring. During the 2025 filing season, CSRs spent over 950,000 hours waiting for taxpayer calls—about 22 percent of total time spent providing phone service—according to IRS data.

High numbers of idle hours limit IRS’s ability to address the correspondence backlog because CSRs are not able to work correspondence inventory while awaiting a phone call. IRS officials told us that this is a policy requirement because it prevents multi-tasking and inadvertent disclosure of taxpayer information that could happen if CSRs are assisting taxpayers on the phone while having tax information of another taxpayer on their screen. IRS officials told us that the telephone level of service requirement was the primary challenge for reducing the agency’s correspondence inventory.

High numbers of idle hours can also increase the agency’s reliance on overtime (see fig. 6). During the filing season, Accounts Management (AM) staff, most of which are CSRs, also used nearly 1.2 million hours of overtime, as shown in figure 3 above.

Figure 6: IRS Prioritized High Level of Phone Service During the 2025 Filing Season, Which Contributed to Other Costs

IRS tracks its inventory across several categories of correspondence. IRS officials told us that IRS has identified critical levels of inventory in two of these categories—900,000 pieces for individual correspondence and 600,000 pieces for business correspondence. Officials told us that, beyond these critical levels, taxpayers will call or write again, increasing the overall demand on IRS’s CSRs. Throughout the 2025 filing season, IRS remained below these critical levels. However, these two categories of correspondence represent a small percentage of IRS’s total correspondence inventory—about 10 percent as of the end of the 2025 filing season. These two categories also represented about 8 percent of correspondence that was overage.

Additionally, we have previously reported on high correspondence inventories related to the Employee Retention Credit (ERC).[36] At the end of the 2024 filing season, ERC cases accounted for about 21 percent of the total correspondence inventory, according to IRS officials. However, in 2025, ERC cases accounted for about 8 percent of total inventory.[37]

Other categories of correspondence, such as those related to assisting identity theft victims, also affect taxpayers.[38] However, IRS did not identify critical levels for other categories or an overall critical correspondence level.

IRS officials told us that the agency was taking steps to reduce its correspondence backlog. They said that the agency had trained some CSRs to respond to more complex types of correspondence and had offered trainings on inventory management and efficiency to several IRS sites that respond to correspondence. However, the agency has not developed a comprehensive plan for reducing its correspondence backlog that addresses all types of correspondence that IRS receives, including types of correspondence not currently identified in the agency’s critical levels. A comprehensive plan could assess IRS’s allocation of resources between phones and correspondence or its use of improved technologies to respond to correspondence more efficiently.

According to IRS’s Internal Revenue Manual (IRM), IRS staff must initiate a final or interim letter within 30 days of IRS receiving the correspondence, and the overage inventory must not exceed 15 percent of the total inventory.[39] The IRM also requires managers to develop procedures for ensuring that these objectives (i.e., timeliness and a low overage rate) are met, among other things. In addition, Standards for Internal Control in the Federal Government states that management should identify, analyze, and respond to risks related to achieving an agency’s objectives.[40]

Without a plan that addresses the full range of correspondence that IRS receives, the agency risks not effectively reducing its correspondence backlog and thus may struggle to provide timely service to taxpayers. The delays that taxpayers experience may lead them to contact IRS again and ultimately increase the workload for CSRs. Finally, as we describe below, reduced staffing post-filing season presents an additional risk for IRS’s correspondence backlog, which may further exacerbate the demand on CSRs.

In-Person Services

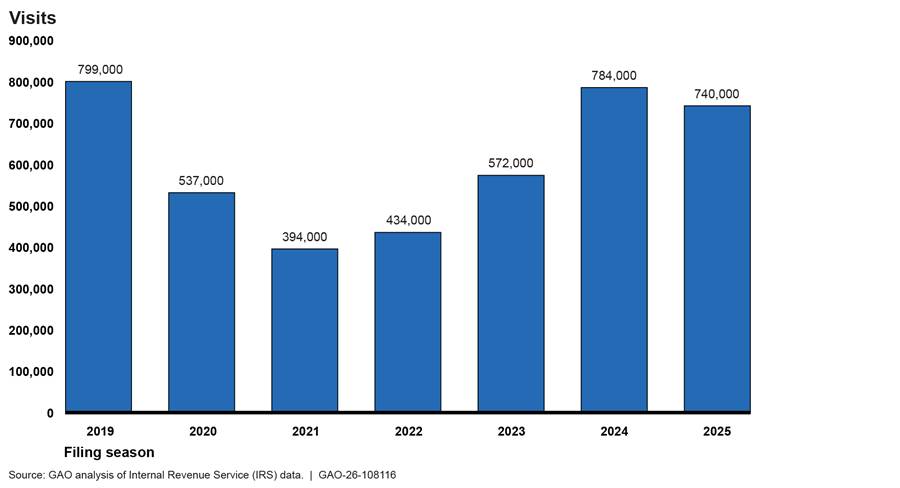

IRS’s in-person service at TACs during the 2025 filing season was similar to its performance last year. As shown in figure 7, IRS served 740,000 taxpayers in person at TACs during the 2025 filing season compared to 784,000 in 2024—a 6 percent decrease. IRS officials told us that this decrease was due to fewer open TACs and fewer taxpayers visiting TACs to address specific issues, such as identity verification.

Note: The dates for filing seasons data are January 28, 2019, to April 19, 2019; January 27, 2020, to July 17, 2020; February 12, 2021, to May 21, 2021; January 24, 2022, to April 22, 2022; January 23, 2023, to April 21, 2023; January 29, 2024, to April 20, 2024; and January 27, 2025, to April 19, 2025. Due to the COVID-19 pandemic, IRS closed all Taxpayer Assistance Centers in late March 2020, and began reopening them in late June 2020. IRS also extended the filing deadlines for the 2020 and 2021 filing seasons. As we reported in 2022, IRS’s in-person services took longer to resume full operations compared to other customer service functions.

While the total number of taxpayers served in person decreased, IRS served nearly twice as many “walk-ins” (i.e., taxpayers without an appointment)—177,000 in 2025 compared to 93,300 in 2024. IRS officials told us that this increase was in part because TACs offered more extended and Saturday hours and word of mouth encouraged taxpayers to visit TACs.

Although the number of taxpayers receiving in-person services during the 2025 filing season was similar to 2024, IRS continued to face challenges providing in-person services. IRS data show that fewer TACs were open and fully staffed at the end of the 2025 filing season compared to 2024 (see table 2). IRS officials told us that the hiring freeze negatively affected the agency’s ability to fully staff TACs. To avoid having to temporarily close additional TACs so that employees could attend training, IRS officials told us that the agency delayed some employees’ training until after the filing season. They also told us that TAC staff must be trained and certified to answer certain questions or otherwise must refer taxpayers to other resources.

Table 2: Staffing and Service Status of IRS Taxpayer Assistance Centers (TAC) as of the End of the Filing Season, 2024 and 2025

|

Number of TACs |

|

|

|

|

2024 |

2025 |

|

Fully staffed |

110 |

102 |

|

Understaffed but open |

235 |

240 |

|

Unstaffed or temporarily closed |

18 |

21 |

|

Total |

363 |

363 |

Source: GAO analysis of Internal Revenue Service (IRS) information. | GAO‑26‑108116

We previously reported that IRS has seen a general decline in visits to TACs since 2015. We recommended that the agency develop and communicate a plan for providing taxpayers in-person services relative to IRS’s plans for expanded virtual customer service options, and costs and benefits.[41] IRS agreed with this recommendation and, in August 2025, told us that the agency had completed a preliminary cost-benefit analysis. In January 2026, IRS officials told us that the agency was reviewing this analysis and will develop a communication plan once the review is completed. We continue to monitor IRS’s delivery of in-person services and plan to issue a separate report on these services.

High Staff Separations Negatively Affected Some Post-Filing Season Performance

Thousands of Filing Season Staff Separated Through Deferred Resignation and Early Retirement, and IRS Increased Its Use of Overtime

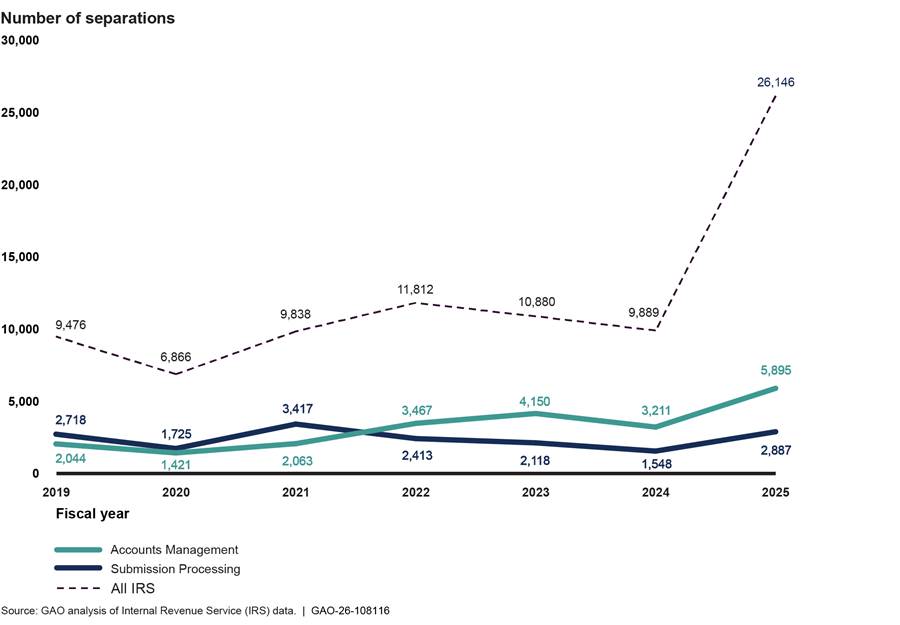

IRS lost large numbers of filing season staff after the 2025 filing season. Every year, IRS’s workforce includes thousands of seasonal employees who are hired to primarily assist with the annual tax filing season. However, IRS had several thousand more separations in fiscal year 2025 compared to previous fiscal years (see fig. 8). Approximately 2,900 SP staff and 5,900 AM staff separated from the agency during fiscal year 2025.

Note: The data are external separations (i.e., employees who separated from IRS). They do not include internal changes such as employees who accepted another position with the same or a different business unit at IRS.

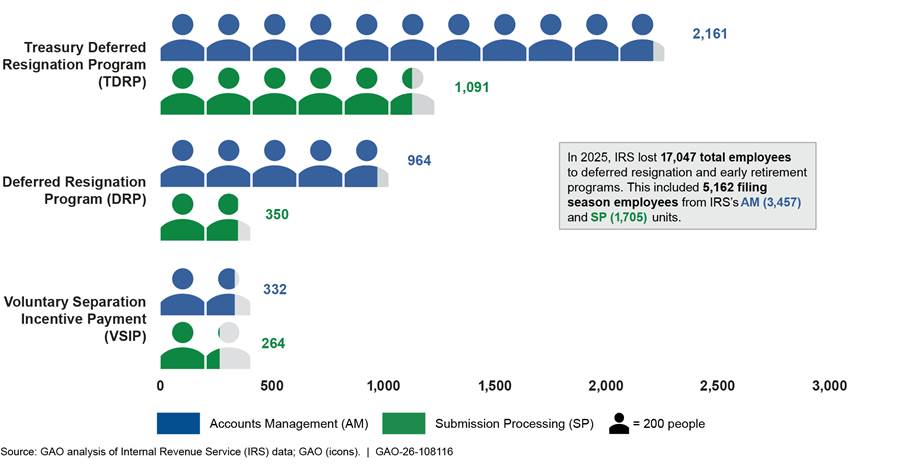

Most fiscal year 2025 separations were due to thousands of IRS employees accepting deferred resignation and early retirement offers (see fig. 9).[42] IRS data show that over 17,000 employees, or about 17 percent of IRS’s workforce as of January 2025, were approved for and separated from IRS through these programs in 2025. Nearly 5,200 SP and AM staff separated through these incentive programs—about 16 percent of all SP and AM staff as of the end of the filing season.[43]

Note: These data are as of December 2025 and include employees who separated via DRP, TDRP, or VSIP in conjunction with Voluntary Early Retirement Authority. The data are external separations (i.e., employees who separated from IRS). They do not include internal changes such as employees who accepted another position with the same or a different business unit at IRS. According to IRS officials, the number of separations through DRP, TDRP, and VSIP is lower than the number of employees who accepted an agreement at earlier points in 2025 because some employees accepted IRS’s offer to rescind agreements before the end of the fiscal year (September 30) and, as of February 2026, IRS continues to process the retirements for voluntary separation participants.

IRS continued to use overtime to perform post-filing season operations and account for lost staff, according to IRS officials. Both AM and SP staff used more overtime after the filing season compared to previous years (see fig. 10). IRS officials told us that more filing season staff were required to work overtime than in previous post-filing season periods and that staff who did work overtime were working more hours. IRS officials also said that the agency authorized managers to use overtime to address increased administrative tasks caused by staffing shortages.

Figure 10: IRS Post-Filing Season Total Overtime Hours, End of Filing Season Through End of Fiscal Year, 2019-2025

Note: Overtime hour data are for hours charged in pay periods that span from the first pay period after the end of the filing season through the end of the fiscal year for each year (September 30). The dates for post-filing season pay period data begin April 28, 2019; July 19, 2020; May 23, 2021; April 24, 2022; April 23, 2023; April 21, 2024; and April 20, 2025. Therefore, some post-filing season periods include more pay periods than others.

IRS’s Time to Process Paper Returns Increased Following Staff Separations

IRS data show that approximately 1,700 SP staff—17 percent of SP’s workforce as of the end of the filing season—separated from IRS through deferred resignation and early retirement offers. Most of these staff left at the end of June 2025, according to IRS officials. These post-filing season separations negatively affected IRS’s processing of paper returns during that time.

Specifically, IRS data show that the average time to process paper returns increased after the filing season. While IRS’s processing times are often longer in the post-filing season, IRS took an average of 36 days to process paper returns at the end of fiscal year 2025 compared to an average of 27 days at the end of fiscal year 2024. At the end of fiscal year 2019, which was prior to the COVID-19 pandemic that led to a significant backlog of returns, IRS took an average of 15 days to process paper returns. IRS officials said that staff separations in 2025, which included more tenured employees who had more experience processing paper returns, contributed to the much higher processing time post-filing season.

In addition, IRS officials told us that, due largely to the hiring freeze and staff separations cited above, IRS processed fewer individual paper returns during the 2025 post-filing season period compared to the same time in 2024, as shown in table 3. Specifically, in contrast to this year’s filing season, the number of returns processed by IRS staff during this period decreased by almost 10 percent.

Table 3: Paper Individual (1040 Series) Income Tax Returns Received and Processed, Post-Filing Seasons 2024-2025

|

Number of paper returns (in thousands) |

|

|

|

|

|

2024 |

2025 |

Percent Change (%), from 2024 to 2025 |

|

Received by |

|

|

|

|

Internal IRS Staff |

5,641 |

5,290 |

-6.22 |

|

Outside Vendor Scanning |

239 |

171 |

-28.45 |

|

Total Paper |

5,880 |

5,461 |

-7.13 |

|

Processed by |

|

|

|

|

Internal IRS Staff |

7,115 |

6,428 |

-9.66 |

|

Outside Vendor Scanning |

242 |

168 |

-30.58 |

|

Total Paper |

7,358 |

6,595 |

-10.37 |

Source: GAO analysis of Internal Revenue Service (IRS) data. | GAO‑26‑108116

Note: Data for the 2024 and 2025 post-filing seasons are from April 20, 2024, through October 4, 2024, and April 19, 2025, through October 3, 2025, respectively. The number of returns processed may include inventory received prior to these periods. When IRS receives paper returns, it reviews, prepares, and transcribes the data into its processing systems. Outside vendors scan the returns using software that extracts the information and transmits it to IRS in the same format as an e-filed return. Once returns are entered into IRS’s processing systems, the returns may still not be fully processed and refunds not provided to the taxpayer if the return was stopped for various reasons. These reasons include a miscalculated tax credit, incorrect Social Security Number or Employer Identification Number, or suspected fraud.

Moreover, IRS officials told us that the government shutdown negatively affected SP performance at the start of the 2026 fiscal year. They said that over 70 percent (5,630) of SP staff were furloughed throughout the shutdown and inventory levels increased substantially as a result. In January 2026, the Treasury Inspector General for Tax Administration reported that IRS’s inventory of individual paper tax returns increased 462 percent from approximately 52,000 returns in December 2024 to approximately 294,000 returns in December 2025.[44] We will continue to examine IRS’s 2026 staffing levels and performance processing returns as part of our annual filing season review.

Balancing Correspondence and Phones Remains a Challenge for IRS Following Staff Separations

IRS decreased its correspondence backlog following the end of the 2025 filing season, but its inventory remains high. As of the end of fiscal year 2025, IRS had decreased its correspondence inventory by about 1.3 million pieces compared to the end of the 2025 filing season, ending at 6.3 million.[45] In 2024, IRS decreased its inventory by about 200,000 from the end of the filing season, ending the fiscal year at 6.6 million. However, the inventory remained high in 2025 compared to IRS’s pre-COVID inventory; at the end of fiscal year 2019, the inventory was about 1.8 million.[46] In addition, as of the end of fiscal year 2025, 4.1 million pieces (65 percent) of correspondence were overage, or late.

Individual correspondence remained well below the critical level with 308,000 pieces of correspondence at the end of fiscal year 2025. However, IRS surpassed its critical inventory level for business correspondence with over 609,000 pieces of correspondence. These two categories of correspondence represented about 15 percent of IRS’s total correspondence volume at that time.

As we reported above, IRS prioritizes phone service over correspondence during the filing season. However, once the filing season ends, IRS officials told us that the agency focuses more resources on correspondence to help keep up with correspondence as it arrives. For example, IRS’s telephone level of service was about 87 percent during the 2025 filing season but was about 61 percent for the full fiscal year. Despite IRS’s focus on responding to taxpayer correspondence over answering taxpayer phone calls outside of filing season, IRS officials told us that they expect the correspondence backlog will remain high due to staff separations and annual training requirements. Officials also told us that, because of the government shutdown, IRS could not offer overtime, which led to fewer total hours available for customer service representatives (CSR) to respond to correspondence and thus an increase in the backlog.

Because IRS continues to prioritize phone service during the filing season, the correspondence backlog will likely remain a challenge in 2026. IRS officials told us that the agency was developing scenarios to predict how lowering the level of service goal during the filing season would affect phone service and the correspondence backlog. However, the agency continues to prioritize high levels of service and does not plan to lower the level of service goal for the 2026 filing season. With level of service as the priority, IRS officials told us that correspondence performance would suffer in the 2026 filing season. Reduced staffing may further exacerbate IRS’s challenges with its correspondence backlog. As we reported above, a comprehensive plan would help IRS address its correspondence backlog amid these challenges.

IRS Organizational Reform and Workforce Planning Uncertainties Pose Serious Risks to Future Filing Season Operations

Amid Leadership Turnover, IRS Has Not Established a Team to Manage Significant Organizational Changes

In 2025, IRS experienced extensive turnover at the highest levels of leadership. IRS had seven different commissioners between January and August, including one acting commissioner who served in the role for 3 days. In October 2025, Treasury announced that the commissioner of the Social Security Administration (SSA) would also serve as IRS’s first Chief Executive Officer (CEO). The new CEO is to manage IRS and oversee its day-to-day operations, according to Treasury’s announcement.

Throughout 2025, one individual served as the Chief of Taxpayer Services, the division that oversees filing season operations. However, during that time IRS experienced turnover and vacancies in other key leadership roles that support filing season operations. For example, in 2025 at least three individuals served as the IRS Human Capital Officer and two individuals served as the Chief Information Officer.[47]

In January 2026, the IRS CEO internally announced an updated IRS executive leadership team that increased the number of functions that report directly to the CEO. The announcement did not include specific roles and responsibilities for the leadership team.

In January 2026, IRS’s organization chart showed that 16 of the 28 top leadership positions were vacant or filled by an acting official. As of February 2026, IRS had updated the chart to show a revised reporting structure with 17 leadership positions. None of the positions were vacant, and two were filled by an acting official. We will continue to monitor changes to IRS’s leadership and organization.

Several directives and implementing guidance were issued in 2025 that have significant implications for IRS’s operations. These include developing plans to restructure workforce functions, evaluating IRS’s portfolio of leased office space, and returning to in-person work. IRS officials told us that IRS’s business divisions, including Taxpayer Services, must wait for guidance from Treasury and IRS leadership before implementing executive orders and other directives.

IRS officials were uncertain about the status and direction of significant organizational decisions stemming from executive orders and other directives that could affect filing season operations. For example:

· Reorganization plans. IRS human capital officials told us that Treasury had not provided IRS with IRS’s agency reorganization plan or a time frame to implement it, as of August 2025. They said that Treasury is the arbiter of IRS’s reorganization efforts with OMB and OPM and that IRS would execute Treasury’s staffing decisions. IRS human capital officials also told us that without this plan, IRS is unsure how a potential reorganization would affect the 2026 filing season.

· Lease cancellations. In March and April 2025, IRS officials who oversee in-person services at TACs told us that they were unaware of planned TAC lease cancellations and had not heard from leadership about next steps for TAC closures. IRS documentation showed that the agency closed 10 TACs in 2025, six of which were unstaffed at the end of the 2025 filing season. IRS officials told us that there may be more TAC closures and consolidations as the agency continues to evaluate additional real estate reduction projects.

· Guidance on paper checks. As of December 2025, IRS officials who oversee return processing told us that they were awaiting Treasury guidance for how to implement the March 2025 executive order that requires IRS to stop disbursing and receiving paper checks for refunds and taxes owed, among other things.[48] For example, they said a primary challenge is how to grant taxpayers exceptions and waivers to send or receive checks. In late January 2026, IRS posted on IRS.gov answers to frequently asked questions related to the executive order.[49]

IRS announced that it generally stopped issuing paper check refunds for individual taxpayers effective September 30, 2025, and encouraged taxpayers who do not have a bank account to open one to receive refunds by direct deposit. IRS officials told us that implementing this executive order is a multi-year effort and that IRS will not refuse paper checks from taxpayers in 2026.

IRS leadership also communicated significant workforce decisions to its employees that would subsequently change. For example:

· Reductions in force. In April 2025, IRS issued reduction in force (RIF) notices to three units: the Office of Civil Rights and Compliance; Taxpayer Experience Office; and Office of Diversity, Equity, and Inclusion within Taxpayer Services. However, in August IRS rescinded RIF notices for employees in these units. The rescission letters that IRS staff received did not explain why their RIF was canceled. IRS human capital officials told us that Treasury made RIF decisions without explaining them to IRS.

· Work schedules. In May 2025, IRS canceled work schedule flexibilities for non-bargaining unit employees but reestablished one of them with restrictions in August.[50] For example, these staff can work a minimum of 5 hours and a maximum of 10 hours on a given workday. IRS officials told us that IRS decided to reestablish workplace flexibilities to align with Treasury guidance and give non-bargaining unit employees the same in-office flexibilities as bargaining unit employees. They also said that any workplace flexibilities are subject to change because executive orders and court decisions could affect collective bargaining agreements.

Some IRA-funded IRS modernization projects that could help improve filing season operations have also been in flux with the ongoing organizational changes. In March 2025, IRS officials said that IRS disbanded the Transformation and Strategy Office that oversaw and guided all transformation efforts related to the IRA strategic objectives. As a result, IRS officials told us that some Transformation and Strategy Office functions would be discontinued, and others would be performed by other IRS offices. They also told us that IRS continued with IRA-funded initiatives and changed some of them to align with the new administration’s goals.[51] For example:

· Zero Paper.[52] The IRS’s goal is to allow taxpayers to go paperless and for IRS to digitize all paper documents to help eliminate errors from manually inputting data, reduce storage costs, and allow IRS to focus more resources on customer service. IRS determined this initiative was in line with the current administration’s priorities, but officials were unsure about the status of some related activities. For example, IRS officials told us that the contract for its scanning and storage efforts ended in May 2025 and IRS signed a 1-year bridge contract with an option to renew each month.

Given the lack of a long-term contract and the fact that increased scanning could affect staffing needs, officials were unsure how much return processing staff there should be for the 2026 filing season. In January 2026, IRS officials told us that they still could not determine staff targets after they had awarded a longer-term contract and ended the bridge contract in September.[53]

· Document Upload Tool. IRS launched this online tool in 2021 to make it easier and more convenient for taxpayers to respond to IRS correspondence by digitally submitting responses and documents. The tool continues as planned and IRS intends to increase the number of users to further reduce incoming mail, according to IRS officials. IRS data show that the number of submissions has steadily increased each year since IRS launched it, with nearly 1.1 million submissions in fiscal year 2025.

· Simple Notice. IRS is redesigning notices to help taxpayers easily understand why IRS is contacting them and the actions the taxpayer needs to take. IRS officials told us that 526 notices were redesigned and 28 notices were digitized in 2025. In addition, they said approximately 800 notices and letters have been either eliminated or consolidated. IRS officials also told us that attrition and the hiring freeze could negatively affect the agency’s progress with this initiative in the future.

· Call Center Modernization. IRS used IRA funds to ease burdens on call centers by hiring thousands of new CSRs and leveraging voice bots to free up employees from answering basic questions. IRS officials told us that they plan to roll out new tools to support managing calls and collecting data on call topics, among other things.

In December 2025, IRS officials told us that several efforts that were previously put on hold pending prioritization based on the new administration’s goals had since resumed. This included IRS piloting a system to allow CSRs to access the right information about the taxpayer at the right time and launching a new electronic workforce management system for scheduling Accounts Management staff.

· Online Service Enhancements. IRS has enhanced tools such as Where’s My Refund? and online accounts for individuals, businesses, and tax professionals. IRS officials told us that their list of projects has not changed but that some have been deprioritized as focus has shifted to other initiatives. For example, they said they prioritized and moved up work for the project that will enable taxpayers to provide direct deposit information, or indicate a need to receive a paper check, through their online accounts because it aligns with the March 2025 executive order requiring IRS to stop receiving paper checks.[54]

IRS reported spending $1.2 billion in IRA funds for taxpayer services in fiscal year 2025. As of September 2025, this spending accounted for nearly half of all IRA funds spent for taxpayer services ($2.5 billion) since the IRA was enacted. Treasury estimated that in fiscal year 2026 IRS would obligate $100 million of the remaining IRA funds appropriated for taxpayer services. If this projection is actualized, it could result in a significant decrease in resources for IRA-funded initiatives. IRS officials told us that the agency may use more than $100 million in IRA funds for taxpayer services because IRS needs $3.8 billion for taxpayer services in fiscal year 2026, which is approximately $800 million more than it received in annual appropriations.

For some organizational reform efforts, IRS officials told us that the agency is waiting on Treasury guidance to determine which leaders to involve and how those reforms are communicated across IRS. They said guidance from OPM and OMB is generally directed at Treasury, and that IRS relies on Treasury’s interpretation and further guidance before IRS will implement changes. IRS officials told us that how IRS implements reforms depends on the area of the agency being affected, whose leadership then determines which other officials to include based on the size and scope of the reform.

In our prior reports on leading practices for agency reforms, we reported that a team of high-performing individuals who have the capacity and necessary resources (i.e., an implementation team) should lead an agency’s major organizational reform efforts.[55] This team should be responsible for day-to-day management of the reforms and have authority to make timely decisions. We also identified that clear and regular communication between leadership and staff is essential for an agency to successfully implement its reform efforts. An implementation team could help ensure that the information shared regarding reform efforts is on time and of high quality and meets the needs of leadership and staff.

Without an implementation team, IRS may struggle to ensure that reform efforts are successful, sustainable, and uniformly understood across the agency. This in turn could foster staff uncertainty, delay the implementation process, and hinder IRS’s ability to provide quality services for taxpayers.

We also reported in February 2024 that IRS had not provided evidence that it was following leading practices to implement agency reforms.[56] As a result, we recommended that IRS show how it is using leading practices to implement its reform efforts. IRS agreed with the recommendation. As of August 2025, IRS was awaiting reorganization guidance from Treasury and had not yet provided evidence for how it was following these leading practices. We continue to monitor the extent to which IRS follows these practices as the agency implements reform efforts.

IRS Does Not Have an Updated Strategic Workforce Plan That Addresses Recent Workforce Challenges

IRS Workforce Reductions in 2025 Were Not Strategic

IRS staff reductions in 2025 were not targeted or strategic. For example, no IRS staff were denied the Deferred Resignation Program and nine filing season employees were denied the Treasury Deferred Resignation Program, according to IRS data. In addition, IRS officials told us that losing 17 percent of its human capital staff to deferred resignations and early retirement led the Human Capital Office (HCO) to prioritize processing the paperwork of separating IRS employees over its other duties, which included some strategic workforce planning activities.

IRS officials told us that Treasury decided which IRS staff to approve and deny for the deferred resignation programs and early retirements. In a May 2025 letter to Congress, Treasury said that “any staffing reductions contemplated at the IRS will only be undertaken in concert with modernization efforts to improve the efficiency of the IRS’s operations and customer support.” However, IRS human capital officials told us that no workforce reduction goals were being discussed or documented by HCO, either agencywide or for specific offices.

In July 2025, Treasury issued guidance that permitted its bureaus to offer employees the opportunity to rescind deferred resignation agreements to fill critical vacancies.[57] This guidance also outlined how bureaus can request exceptions to the hiring freeze. In August 2025, IRS HCO informed managers that IRS identified areas where staffing reductions created a potential gap in mission critical expertise. According to IRS officials, IRS identified 16 areas that included its taxpayer services, HCO, and IT business divisions.

As a result, IRS HCO said the agency would rescind deferred resignation agreements, reassign staff, and hire new staff to obtain the skill sets necessary to fulfill IRS’s mission. In December 2025, IRS officials told us that IRS had rescinded 565 agreements for deferred resignation and early retirement. They also said that in fiscal year 2026 IRS rehired some staff who previously separated from the agency via deferred resignation and early retirement.

IRS’s Prior Workforce Plans Are on Hold and New Workforce Planning Efforts Are in Progress

IRS officials told us in August 2025 that the agency’s strategic workforce plans, which predate the current administration, are on hold. They told us that IRS decided to halt these plans earlier in the calendar year because of IRS’s goal to align workforce planning efforts with the new administration’s priorities and congressional rescissions to IRA funding.

In our prior report on key principles for effective strategic workforce planning, we reported that strategic workforce planning addresses two critical needs: (1) aligning an organization’s human capital program with its current and emerging mission and programmatic goals, and (2) developing long-term strategies for acquiring, developing, and retaining staff to achieve programmatic goals.[58] Agency strategic workforce planning efforts should also include mechanisms to track progress toward achieving those goals and capacity-building efforts for essential positions.

In 2019, we reported on the serious risks that insufficient workforce planning efforts posed to IRS’s mission.[59] We recommended that IRS should fully implement its workforce planning initiative, including creating and implementing a workforce plan. IRS agreed with this recommendation and in June 2024 finalized a workforce plan for fiscal years 2024 through 2026. This plan outlined IRS’s strategies to cultivate an organizational culture to provide high-quality service for taxpayers and positioned the agency to effectively manage its workforce. As a result, we closed the recommendation as implemented. However, IRS officials told us that this plan is among the workforce plans that are on hold.

Before IRS can finalize a new strategic workforce plan, IRS officials told us that they need direction from Treasury on IRS’s strategic goals. In May 2025, Treasury informed IRS employees that it planned to approve the Treasury strategic plan for fiscal years 2026 through 2030 for internal use by September 2025 and publish it by February 2026. Treasury documentation states that its strategic plan will include details for goals and objectives to support agency decision-making and accountability. IRS will be a lead agency for implementing the objective to deliver a modern taxpayer experience to improve service, privacy, and collection.

IRS is developing a strategic plan that the agency plans to publish in summer 2026 and that aligns with Treasury’s strategic plan, according to IRS officials. In December 2025, IRS officials told us that IRS’s Chief Financial Officer has a draft of the Treasury plan and is working with Treasury to develop IRS’s strategic plan. They also said that neither plan had been approved for release.

IRS HCO leads annual workforce planning efforts with each IRS business division to determine needed staffing levels, according to IRS officials. They told us that HCO’s staffing plans typically result from “demand planning” with the divisions and support operational priorities and long-term workforce sustainability. HCO officials said demand planning involves the divisions providing staffing projections based on current staffing levels, historical attrition, and workload requirements, and HCO evaluating those projections before senior leaders review staffing plans.

IRS leadership halted demand planning in fiscal year 2025 due to RIF activities and uncertainty about future priorities and staffing, according to IRS officials. They also told us that HCO did not develop a demand plan in 2025 because much of the staff’s time was spent addressing various executive orders. However, IRS officials said that HCO launched a portal in 2025 for business divisions to request exceptions to the ongoing hiring freeze and identify staff needs for fiscal year 2026. They told us that HCO used this information to develop a staffing plan for fiscal year 2026. IRS officials said that the agency originally submitted this staffing plan to Treasury in August and sent an updated version in December 2025.

HCO officials said they are using the list of mission critical occupations from 2024 to identify IRS’s future critical hiring needs. This list included the job series for filing season CSRs and tax examiners. They told us that IRS needs Treasury’s strategic plan to identify new mission critical occupations and align them to strategic goals and priorities. HCO officials also said that, as of August 2025, they were waiting for Treasury to issue guidance that will help its bureaus define and identify mission critical occupations but did not know when Treasury would provide it.

IRS officials said HCO will do a comprehensive workforce planning process for fiscal years 2026 through 2030 as required under Treasury’s new strategic plan. They said that all Treasury bureaus must submit a workforce plan for this period that includes staffing plans, mission critical occupations, succession plans, knowledge and training initiatives, and plans to close skills gaps. The officials also told us that IRS would not use prior IRS workforce plans when developing its workforce plan to ensure that the agency is aligned with Treasury’s strategic plan. As of March 2026, we have not received documentation of IRS’s new workforce plan.

In addition, an October 2025 executive order established policies and procedures for future federal hiring efforts.[60] The order directed agencies to create an annual staffing plan and submit it to OPM and OMB by December 2025. Subsequent guidance from OPM and OMB stated that the staffing plans should cover agencies’ current workforce and staffing needs, gaps in skills areas, and strategies for recruitment. The plans should also identify opportunities for reorganization or staff reductions. IRS officials told us that the fiscal year 2026 staffing plans it sent to Treasury address this executive order.

We previously identified an agency’s careful consideration of long-term staffing plans and mission shortfalls before implementing workforce reduction strategies as a leading practice for agency reform efforts.[61] We also reported that without careful attention to strategic and workforce planning, the reduced investments in human capital may have lasting, detrimental effects on the capacity of an agency’s workforce to meet its mission.[62] In addition, we established that for an agency to improve performance, it should identify any gaps between its current capacity and what it needs to carry out current and future activities.[63]

With a new strategic workforce plan underway, IRS could leverage the strategies it developed in its plan for fiscal years 2024 through 2026 to effectively manage its workforce. If IRS’s new plan does not address its workforce challenges, IRS will be unable to systematically identify the workforce needed for the future and develop strategies to achieve it. As a result, IRS would be without a critical tool to help secure the staff necessary for achieving its mission to provide taxpayers top quality service.