Report to Congressional Committees

United States Government Accountability Office

A report to congressional committees

For more information, contact Yvonne Jones at jonesy@gao.gov.

What GAO Found

The Financial Data Transparency Act (FDTA) was enacted in December 2022 with the intent of eventually reducing the private sector’s regulatory compliance burden while enhancing transparency and accountability. The FDTA requires agencies that regulate the financial sector to create a set of joint data standards to ultimately help harmonize future reporting by promoting data sharing among financial regulators. Implementation of the FDTA requirements is in the early stages of the rulemaking process, with regulatory agencies working to finalize an August 2024 proposed rule. Subsequently, most regulatory agencies are required to issue their own regulations to implement the joint data standards.

The agency officials and stakeholders GAO spoke with identified potential benefits, costs, and challenges of implementing the FDTA.

Potential benefits of implementation

· Standardized data reporting, as well as the interoperability of data collected by different agencies, could improve the quality and efficiency of data analysis by regulators.

· More efficient data analysis could in turn improve oversight and more timely identification of compliance concerns.

· Common standards for reporting within the framework set forth by the FDTA could reduce reporting entities’ burden by making filing financial reports across multiple regulatory agencies more efficient.

Potential challenges and costs of implementation

· Regulatory agencies may need to modernize legacy data systems, coordinate across agencies, and manage data governance costs.

· Reporting entities could incur costs for adapting processes and systems to comply with the FDTA’s updated reporting requirements, as well as conducting system testing.

While the FDTA sets forth provisions for the sharing of certain key data elements in the context of financial regulation, there is interest in a broader, government-wide data standard, similar to Standard Business Reporting (SBR) that would reduce the burden on reporting entities while streamlining the reporting process across all government agencies. SBR refers to the government-wide adoption of a common taxonomy, or shared dictionary of data fields, in a way that enables data processing to be automated and data to be gathered from reporting entities and transferred to regulators. While the United States does not currently have SBR, other federal efforts have addressed the streamlining of government data reporting to better ensure its usefulness and improve its quality. Practitioners in the fields of data management, data governance, and regulations told GAO the FDTA could put the United States on a path towards a government-wide reporting system, similar to SBR. GAO’s past work on prior government-wide efforts to establish data standards provide effective practices on interagency collaboration and data governance that can guide regulators at such time as they should seek to build toward a government-wide regulatory standardization mechanism like SBR.

Why GAO Did This Study

Federal agencies regulate, supervise, and oversee banks, savings associations, credit unions, and financial markets that manage trillions of dollars in deposits and loans. Regulations often require entities to report information to the government to assess compliance and help ensure the soundness of financial markets. GAO has previously reported, however, that these reporting requirements also create burdens on reporting entities, especially if they are reporting the same or similar information to multiple agencies.

Congress included a provision in statute for GAO to review the feasibility, costs, and potential benefits of building upon the taxonomy established by the FDTA to arrive at a government-wide regulatory compliance standardization mechanism similar to SBR. This report (1) describes stakeholders’ views on potential benefits, costs, and challenges of the FDTA; and (2) describes effective practices to facilitate future government-wide data standardization efforts and stakeholders’ views on such potential efforts.

GAO reviewed documentation and corresponded with officials from nine regulatory agencies involved in implementing the FDTA. GAO met with four practitioner groups knowledgeable about data standards and the FDTA, including private entities that develop software solutions or other products to support data standardization, to understand the technology and their experiences with compliance reporting. GAO also interviewed four groups representing reporting entities, as well as two academic researchers knowledgeable about financial regulatory reform efforts. GAO also reviewed its prior work to identify effective practices in interagency collaboration and data governance structures.

Abbreviations

Board Board of Governors of the Federal Reserve System

CFPB Consumer Financial Protection Bureau

CFTC Commodity Futures Trading Commission

DATA Act U.S. Digital Accountability and Transparency Act of 2014

FDIC Federal Deposit Insurance Corporation

FDTA Financial Data Transparency Act of 2022

FFATA Federal Funding

Accountability and Transparency

Act of 2006

FSOC Financial Stability Oversight Council

GREAT Act Grants Reporting

and Efficiency and Agreements

Transparency Act

LEI International Organization for Standardization 17442-1:2020, Financial Services—Legal Entity Identifier

OCC Office of the Comptroller of the Currency

OMB Office of Management and Budget

SBR Standard Business Reporting

SEC Securities and Exchange Commission

XBRL eXtensible Business Reporting Language

XML eXtensible Markup Language

This is a work of the U.S. government and is not subject to copyright protection in the United States. The published product may be reproduced and distributed in its entirety without further permission from GAO. However, because this work may contain copyrighted images or other material, permission from the copyright holder may be necessary if you wish to reproduce this material separately.

May 14, 2026

The Honorable Tim Scott

Chairman

The Honorable Elizabeth Warren

Ranking Member

Committee on Banking, Housing, and Urban Affairs

United States Senate

The Honorable French Hill

Chairman

The Honorable Maxine Waters

Ranking Member

Committee on Financial Services

House of Representatives

The United States’ financial regulatory structure has evolved into an extremely complex system, with responsibilities spread across multiple regulators that have overlapping authorities. At the federal level, regulations often require entities to report information to the government to assess compliance and help ensure the soundness of financial markets.[1] For example, financial regulators collect a variety of information including financial reports filed by public companies, data on individual securities, and data on commodities trading. While this reporting enables regulatory oversight, it can create burdens on both the reporting entities having to compile and report data and the regulators having to accept and analyze data. As we have previously reported, these burdens can be significant, especially when entities are required to report data to multiple regulatory agencies.[2]

The Financial Data Transparency Act (FDTA) was enacted in December 2022, with the intent of eventually reducing the private sector’s regulatory compliance burden, while enhancing transparency and accountability.[3] The FDTA requires covered financial regulatory agencies to create joint data standards to ultimately help harmonize future reporting by promoting data standards among financial regulators.[4] These agencies regulate, supervise, and oversee banks, savings associations, credit unions, and financial markets that manage trillions of dollars in deposits and loans (see appendix I for more information). Collectively, these agencies administer more than 500 information collections, contributing to a complex reporting landscape across the federal financial regulatory system.[5] By mandating the development of interoperable data standards to the extent feasible, the FDTA is a first step towards transforming this landscape—enhancing regulators’ ability to analyze financial data while creating standard reporting requirements for regulated entities. However, these benefits will likely come with costs.

The FDTA focuses on promoting the interoperability of certain financial regulatory data across the covered agencies.[6] In contrast to the FDTA, some other countries, such as Australia and the Netherlands, have implemented Standard Business Reporting (SBR) systems to reduce reporting burdens and streamline regulatory reporting government-wide across all types of government agencies.[7] While the FDTA does not define SBR, SBR generally refers to the government-wide adoption of a common taxonomy, or shared dictionary of data fields, to enable data processing to be automated and data to be gathered from reporting entities and transferred to regulators.

The United States does not currently have SBR, but other federal efforts have addressed the streamlining of government data reporting to better ensure its usefulness and improve its quality. While full implementation of the FDTA could standardize key data elements used by the covered agencies, additional system reforms and more widespread adoption beyond these financial regulators would be necessary to establish a government-wide compliance standardization mechanism similar to SBR. Agencies’ implementation of the FDTA provisions is in the early stages and, therefore, it is too soon to know whether any additional reforms that follow the FDTA could put the United States on a path toward SBR. However, we have previously reported on agency use of government-wide data reporting standards, such as for federal spending data, that could help inform future efforts.[8]

The FDTA directs us to report on the feasibility, costs, and potential benefits of building upon the taxonomy established by the FDTA to arrive at a federal government-wide regulatory compliance standardization mechanism similar to SBR. This report (1) describes stakeholders’ views of the potential benefits, costs, and challenges of implementing the FDTA’s requirements for data standardization; and (2) describes effective practices to facilitate future government-wide data standardization efforts and stakeholders’ views on such potential efforts.

For both objectives, we reviewed our prior work about related legislation on government-wide data standards, specifically the Federal Funding Accountability and Transparency Act of 2006 (FFATA), the Digital Accountability and Transparency Act of 2014 (DATA Act), and the Grant Reporting Efficiency and Agreements Transparency Act of 2019 (GREAT Act).[9] We also reviewed available information about the implementation of SBR in Australia and the Netherlands. Finally, we interviewed two academic researchers knowledgeable about regulatory issues about past financial regulatory reform efforts, relevant leading practices, and potential challenges in interagency collaboration.

For the first objective, we reviewed available published information related to the FDTA or related efforts in the United States and abroad. We also corresponded with officials from the nine agencies involved in implementing the FDTA to understand the status of the required rulemakings and potential benefits, costs, and challenges of FDTA implementation. For context and background purposes, we also discussed the agencies’ processes and practices for collaborating on the August 2024 joint proposed rule. This included their governance structures and any policies or procedures they established as part of this collaboration. We met with four practitioner groups knowledgeable about data standards and the FDTA, including private entities that develop software solutions or other products to support data standardization, to understand the technology and their experiences with compliance reporting. We also interviewed four groups representing reporting entities to gain insight into potential effects of FDTA implementation on their regulatory compliance reporting, including categories of potential costs and benefits of FDTA implementation on their operations.

For the second objective, we reviewed our prior work to identify key and leading practices in interagency collaboration and data governance structures. We discussed with the four practitioner groups and the two academic researchers their knowledge of SBR and their views on the possibility of implementing government-wide data standards established by the FDTA.

A detailed explanation of our objectives, scope, and methodology can be found in appendix II.

We conducted this performance audit from April 2025 to May 2026 in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions, based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

Background

FDTA

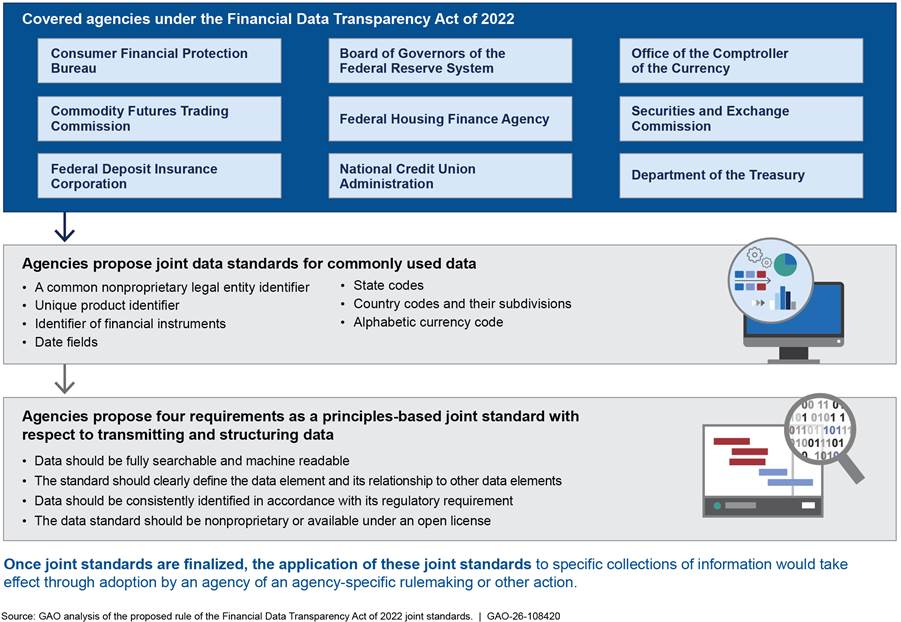

The FDTA established a two-step implementation process. The first step required the covered agencies to jointly promulgate a final rule by December 23, 2024, that establishes the data standards for collections of information reported to each covered agency by reporting entities under their jurisdiction as well as data collected on behalf of the Financial Stability Oversight Council (FSOC).[10] The FDTA requires that the standards established by the agencies include common identifiers, including a common legal entity identifier, and provides the characteristics identifiers shall have, such as being machine readable to the extent practicable. On August 22, 2024, the covered agencies issued a proposed joint rule and invited the public to comment by October 21, 2024.[11] However, the covered agencies did not promulgate a final joint rule by December 23, 2024. As of January 2026, the agencies had not identified a date to publish the final joint rule and continued to evaluate comments on it. As of May 1, 2026, a final rule has not been published. Figure 1 illustrates the covered agencies’ August 2024 proposed joint rule.

Figure 1: Summary of the Financial Data Transparency Act of 2022’s August 2024 Joint Proposed Rulemaking

Note: As permitted by statute, on May 3, 2024, the Secretary of the Treasury designated the Commodity Futures Trading Commission as an additional covered agency under the Federal Data Transparency Act of 2022.

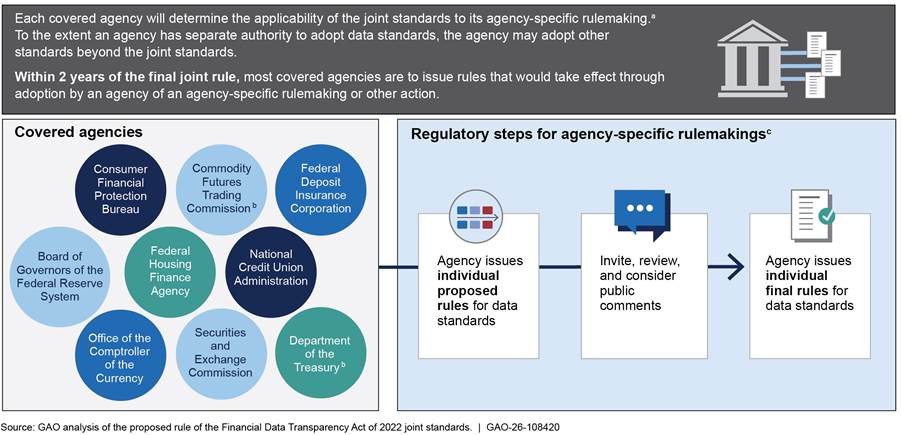

Next, once the joint rule is finalized, the FDTA requires most of the covered agencies to issue agency-specific rules that apply the joint standards, as appropriate, to certain data collected from reporting entities under their jurisdiction. These agency-specific rules are to incorporate and ensure compatibility with, to the extent feasible, the joint data standards. Additionally, the FDTA outlines the characteristics the joint data standards must have, to the extent practicable. Each agency is to determine the applicability of the joint standards to their specific reporting requirements (see fig. 2).

aConsistent with the Financial Data Transparency Act of 2022 (FDTA), the August 2024 joint proposed rule states that in issuing an agency-specific rulemaking, each implementing agency (1) may scale data reporting requirements to reduce any unjustified burden on smaller entities affected by the regulations; and (2) must seek to minimize disruptive changes to those entities or persons. Further, the FDTA provides that nothing in the FDTA may be construed to prohibit a covered agency from tailoring the joint data standards when adopting its own agency-specific standards.

bThe August 2024 joint proposed rule states that the FDTA does not specifically require Treasury and the Commodity Futures Trading Commission to issue individual rules, though they may do so at their discretion.

cRegulatory steps may involve other actions.

The data standards adopted by each agency through these individual rulemaking

efforts are to take effect—to the extent that each agency adopts them—no later

than 2 years after the final joint rule is promulgated. While the proposed rule

states that the FDTA does not specifically require the Department of the

Treasury and the Commodity Futures Trading Commission to issue individual

rules, they may do so at their discretion.

FDTA Joint Rulemaking Process

The covered agencies are all members of the FSOC and work together regularly on broader financial regulatory and oversight matters.[12] Agency officials told us they collaborate on the FDTA joint rulemaking through three workgroups:

· The FDTA Chief Data Officer’s group includes the Chief Data Officers of the covered agencies and primarily provides oversight and strategic direction for the overall rulemaking project. The group meets monthly or as needed and receives progress reports from the other two groups.

· The FDTA Brass Tacks group meets regularly and consists of staff from each covered agency. The Brass Tacks Workgroup is responsible for creating preliminary staff-level drafts of rulemaking documents.

· The FDTA Technical subgroup is a group of technical experts, including data architects, modelers, and taxonomists from the covered agencies, who meet as needed. This subgroup addresses specific technical questions coming from the FDTA Brass Tacks group, such as what the potential advantages and disadvantages of specific data standards are to both covered agencies and reporting entities.

According to officials from the covered agencies, leadership across the working groups is shared among them rather than designated to specific agencies or individuals, and decisions are made by consensus.

Ongoing Government-wide Data Standardization Efforts

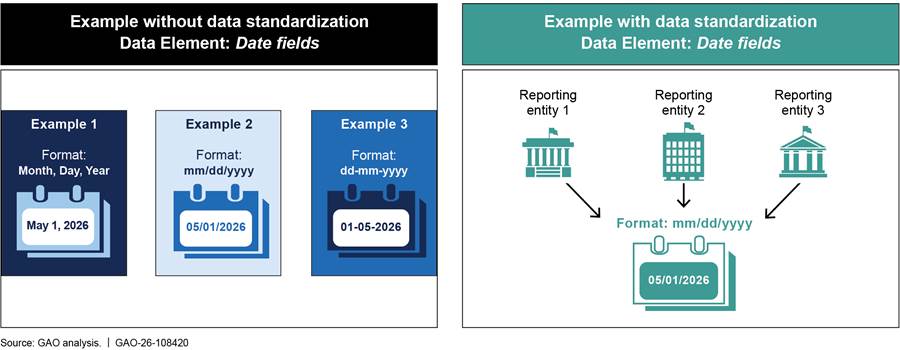

Data standards establish an agreed-upon approach for each data element, including its definition as well as technical specifications that describe the data’s format, structure, and transmission. Figure 3 illustrates standardization with a date field.

Data standardization is a recognized approach for increasing the consistency, and therefore the transparency, of data. We have previously reported that legislation to increase standardization of federal spending data has improved the completeness and accuracy and enhanced the usefulness of the data.[13] Government-wide data standards provide a consistent, government-wide approach for describing the substance and structure of data. Several acts have objectives to establish and implement data standards government-wide.

· FFATA required the Office of Management and Budget (OMB) to establish a free, publicly accessible website containing federal spending data, which became what is now known as USAspending.gov.[14]

· The DATA Act directed the OMB and Treasury to establish government-wide data standards by May 2015, to improve the transparency and quality of federal spending data.[15]

·

The GREAT Act requires the OMB and the Department of Health and

Human Services to create data standards for grantee reporting requirements

across the federal government, among other things.[16]

SBR

The FDTA focuses on promoting interoperability of financial regulatory data across the covered agencies. While implementation of the FDTA would standardize certain data elements used by the covered agencies, additional system reforms and more widespread adoption would be necessary to establish a government-wide compliance standardization mechanism similar to SBR.

SBR refers to the government-wide adoption of a common taxonomy, or shared dictionary of data fields. This enables highly automated data gathering and transfer from reporting entities to regulators. Because SBR focuses on standardization of data elements across multiple regulatory agencies, reported data can be shared between participating agencies, and reporting entities can fulfill multiple reporting requirements with a single data submission.

The Netherlands and Australia were early adopters of SBR, which the United States has not currently adopted.[17] Both countries originated their SBR systems in their tax revenue offices and then expanded them to other government agencies. According to a whitepaper by the Data Foundation and PwC, when the Netherlands adopted SBR, the number of unique data elements that entities reported to the government declined about 98 percent, from approximately 200,000 to approximately 4,500 over approximately the next decade.[18] Similarly in Australia, between 2008 and 2014, SBR reduced the number of unique reporting terms from 35,000 to 7,000, a more than 80 percent reduction.

In implementing SBR, the Netherlands and Australia used a specialized version of eXtensible Markup Language (XML) called eXtensible Business Reporting Language (XBRL) to apply labels, called tags, to elements of data.[19] For example, a data element may be the date of a transaction or the type of financial instrument. The tags provide additional machine-readable information about the data being submitted by reporting entities.[20] Currently, the covered agencies collect data from reporting entities in a variety of formats. Some use XML for certain information collections, and XBRL for others. Some agencies collect information over web-based form systems, and other financial regulatory information collections are conducted with PDF forms.

The Potential Benefits and Challenges of the FDTA Vary Depending on the Entity Affected

Potential Benefits of the FDTA Include Improved Accountability, Reduced Reporting Burden, and Enhanced Transparency

The FDTA was intended to lead to enhanced transparency and accountability and reduce regulatory compliance burdens resulting from financial data reporting requirements by establishing a harmonized financial reporting program. The FDTA requires information reported to financial regulatory agencies to be electronically searchable, machine readable, and suitable for artificial intelligence applications, to the extent practicable.

Officials at some of the covered agencies said they did not conduct a benefit-cost analysis of the proposed joint standards because they said that the individual agency rules that will follow the joint rule likely would include benefit-cost analyses specifically tailored to the agencies’ individual circumstances.[21] However, some agency officials, practitioner groups knowledgeable in the areas of data standards and the FDTA, groups representing state and local government finance offices, and an academic researcher knowledgeable in regulatory issues identified categories of potential benefits, costs, and challenges to covered agencies, reporting entities, and the public, of implementing the FDTA.

Covered agencies’ potential benefits: Some covered agencies reported that more standardized data reporting could promote the interoperability of data collected across different agencies, which could improve the quality and efficiency of data analysis by regulators. This could in turn improve oversight and allow for more timely identification of compliance concerns, according to covered agencies. For example, one of the FDTA’s requirements to guide the adoption of any data standard is that the data should be fully searchable and machine readable to the extent practicable.

According to reports to Congress by the Securities and Exchange Commission (SEC) in June and December 2025 about the current use of machine-readable data (SEC FDTA Reports), the availability of machine-readable data disclosures submitted to the SEC’s staff in the Division of Enforcement has allowed SEC to perform more efficient analyses of individual issuers’ disclosures and accounting practices.[22] The June SEC FDTA Report stated that machine-readable data enabled the SEC enforcement staff to review the financial data of thousands of public issuers to detect evidence of financial misconduct.[23] Further, according to the reports, machine-readability helped the agency implement more sophisticated analyses of disclosures and accounting practices across wide-ranging cross sections of issuers. The SEC reported that without the use or analysis of machine-readable data, the alleged violations would have been significantly more difficult to detect and pursue in a cost-effective or timely manner. According to SEC, the use of machine-readable data by its enforcement staff resulted in charges against six public companies and several related individuals over a several-year period for violations of the federal securities laws.

An official from one of the covered agencies we spoke with also specifically cited the benefits of the FDTA’s requirement for a common nonproprietary legal entity identifier and how its use could benefit agencies. As a legal entity identifier is unique and unambiguously identifies a legal entity, the adoption of legal entity identifiers would enable regulators and risk managers to identify parties to financial transactions instantly and precisely, according to this agency official. The agency official also cited other benefits of legal entity identifiers, including the increased transparency and interoperability of reported data, and more consistent and usable data. Additionally, officials from some of the covered agencies noted that this will help them to better analyze and monitor the stability of and threats to the financial system. Officials from some of the other covered agencies told us that, depending on the level of future data sharing that occurs between covered agencies, full FDTA implementation could lower agency data interoperability costs when data sharing occurs between them.

Additionally, we spoke with knowledgeable practitioners in the areas of data standards and the FDTA who also discussed the benefits of the FDTA not only in the context of its establishment of machine-readable data but also with its establishment of a legal entity identifier. For example, according to one practitioner, once the FDTA is implemented, legal entity identifiers could enable the Department of Commerce to better utilize entity-based data and calculate Gross Domestic Product figures, thereby improving the precision of overall economic data. In another example, the practitioner stated that the Environmental Protection Agency could use the legal entity identifier as an enforcement tool to help identify ownership of polluting factories to better target violators of environmental regulations.

Reporting entities’ potential benefits: According to some of the covered agencies, implementing the FDTA could result in common standards for reporting to multiple federal regulators within a simpler and more consistent regulatory reporting framework. These agency officials said this may reduce the burden on reporting entities and make it easier for them to file financial reports across multiple regulatory agencies. Also, given the FDTA’s machine-readability requirement, studies cited in the SEC FDTA Reports found that some reporting entities have benefitted from decreased audit fees and increased timeliness of audit and financial reports as a result of machine-readable disclosures that are already required.

Knowledgeable practitioners in the areas of data standards and the FDTA have also stated that reporting entities can benefit from a reporting framework where they generate machine-readable submissions that can be used for many reporting requirements and filed with many different agencies. Currently, according to these practitioners, reporting entities are required to file dozens, if not hundreds, of different forms with regulators. They noted that the FDTA’s simplified reporting standards have the potential to reduce compliance burdens and costs for reporting entities in the long run through greater reporting efficiency stated the practitioners.

Public potential benefits: According to the SEC FDTA Reports, a practitioner knowledgeable in the area of data standards, and an academic researcher versed in regulatory law, the machine-readability data format standard has potential to provide benefits to taxpayers, investors, markets, and issuers. Studies cited in the SEC FDTA Reports stated that for investors, and more broadly for markets, making corporate disclosures machine readable has, among other things, decreased the differences in the availability of information between firms and investors by reducing information processing costs, made stock prices more reflective of firm specific information, and reduced market inefficiencies and risks. Further, the reduction in information processing costs, according to an academic researcher we spoke with and the SEC FDTA Reports, has heightened monitoring of issuers by investors and other parties, such as financial analysts, the press, data aggregators, academic researchers, and financial media. Increased monitoring by investors, analysts, and other market participants may incentivize issuers to provide more complete and consistent disclosures resulting in improvements in transparency, enhanced market efficiency, and oversight, according to the SEC FDTA Reports. According to a practitioner knowledgeable in the area of data standards we spoke with, these effects may ultimately benefit taxpayers through more efficient reporting of higher quality financial data. The SEC FDTA Reports state that the higher level of monitoring provided by the availability of machine-readable data has driven firms to provide more quantitative disclosure and report earnings in a more consistent manner. The SEC reports that such benefits may increase over time as tools for investor use of machine-readable data become more widely available.

Potential FDTA Implementation Challenges Include Data System Revisions and Associated Costs

According to officials at the covered agencies, they expect some challenges when developing and implementing the final individual agency rules. Agencies and groups representing reporting entities also told us they anticipate FDTA implementation will pose potential challenges and costs for reporting entities as they transition to new reporting standards.

Covered agencies’ potential costs and challenges: Officials from some covered agencies told us they anticipate that the transition from their current information collection requirements to the revised information collections will be the primary challenge of full FDTA implementation. This may include, for example, modernizing legacy data systems, coordinating across the covered agencies, and managing data governance costs, according to one covered agency. Officials from some covered agencies told us that a primary driver of costs will include reconfiguring and testing systems to accept and store data reported in the FDTA’s new standard. Some covered agency officials also told us that they anticipate costs associated with hiring and training of staff due to updating data collection mechanisms and the preparation of policy and guidance documentation.

According to some of the covered agencies, as they adopt data standards in their agency-specific rulemakings, to the extent feasible, the covered agencies must incorporate and ensure compatibility with the applicable joint standards agreed to in the final joint rule. These agencies told us that this may create some challenges given the distinct data needs of each agency. For example, these agencies will need to harmonize the FDTA data standards with other existing statutory requirements governing data standards that preceded the FDTA.

Reporting entities’ potential costs and challenges: Reporting entities may face costs associated with the need to transition their business processes and systems to comply with updated FDTA standards adopted in subsequent agency rules and reporting requirements. Officials from some of the covered agencies said that the full extent of the costs and challenges these entities may face is difficult to estimate until agencies begin their individual rulemakings to implement the new data standards.

Reporting entities themselves have anticipated potential challenges and costs they may face with implementing the FDTA. According to officials we spoke with from two associations representing state and local government finance offices, these costs, which are difficult to estimate without having a final joint rule and individual agency rules, pose potential burdens on their members. The following are among the potential cost categories for reporting entities associated with FDTA implementation:

· Legal entity identifier: The FDTA requires that the joint data standards rule include a common non-proprietary legal entity identifier. The proposed rule identifies the International Organization for Standardization 17442-1:2020, Financial Services—Legal Entity Identifier (LEI) as the legal entity identifier joint standard. The proposed rule also states that it would not impose any requirements that any particular entity obtain an LEI and incur the associated costs; such requirements would be determined by the agency-specific rulemakings. However, a statement by a regulator indicated that entities may have to pay a fee to obtain and renew the LEI annually. Representatives we spoke with from an association representing state and local government finance offices expressed concerns regarding the costs and manageability challenges of requiring their members to use LEIs.

· System updates: Reporting entities may incur costs and face challenges for adapting processes and systems to comply with the FDTA’s updated reporting requirements, as well as conducting system testing, and obtaining and maintaining legal entity identifiers from customers or third parties. According to a representative we spoke with from an association representing state and local government finance offices, these updates or changes to their members’ financial and organizational systems could be costly. While the high upfront cost would likely taper off over time, the initial costs will pose a substantial obstacle to many of their members, according to the association representative.

· Staffing and training: Workforce related costs and challenges may include hiring staff to update data collection methods, training staff on the new FDTA standards and requirements, and updating data submission protocols. According to representatives from the two associations we spoke with representing state and local government finance offices, additional staffing requirements will likely disproportionally affect smaller entities, including small municipalities, which often operate with limited resources and staff.

· Structured data tagging: Reporting entities may face costs associated with the tagging and categorization of filing information. We spoke with representatives from two associations representing state and local government finance offices that are sometimes required to file reports in the context of the issuance of municipal bonds. According to representatives from these associations, data tagging and categorization may be a one-time cost, but could become a repeated cost. For example, the tagging and categorization may need to be repeated each time there are changes to reporting requirements.

Stakeholder Views and Our Work on Prior Government-wide Efforts Can Help Inform Potential Expansion Beyond the FDTA

While the FDTA sets forth provisions for the sharing of certain key data elements in the context of financial regulation, there is interest in a broader, government-wide data standard, similar to SBR that would reduce the burden on reporting entities while streamlining the reporting process across all government agencies. While the United States does not currently have SBR, other federal efforts have addressed the streamlining of government data reporting to better ensure its usefulness and improve its quality. Practitioners in the fields of data management, data governance, and regulations told us the FDTA could put the United States on a path towards a government-wide reporting system, similar to SBR. Our past work on prior government-wide efforts to establish data standards provide effective practices on interagency collaboration and data governance that can guide regulators at such time as they build toward a government-wide regulatory standardization mechanism like SBR.[24]

Prior Government Efforts and Stakeholder Views Provide Insight into Potential for Government-wide Regulatory Reporting

Over almost two decades, both Congress and the executive branch have taken steps to improve the availability, transparency, and quality of federal data. For example:

· Federal Funding Accountability and Transparency Act of 2006 (FFATA). Enacted in 2006, FFATA requires that information on federal awards, including contracts, loans, and grants, to be made available to the public.

· Digital Accountability and Transparency Act of 2014 (DATA Act). Enacted in 2014, the DATA Act expanded on FFATA by requiring the disclosure of direct federal agency expenditures and linking contract, loan, and grant spending to programs of federal agencies.

· Grant Reporting Efficiency and Agreements Transparency Act (GREAT Act). Enacted in 2019, the GREAT Act expanded on these prior efforts by requiring the creation of data standards to modernize grant reporting, reduce burden and compliance costs of grant recipients, and strengthen the management and oversight of federal grants.

While these efforts demonstrate the ability for some data standardization at the federal level, moving to a government-wide system like SBR would be a more substantial undertaking. According to the Organization for Economic Co-operation and Development, the fundamental basis of SBR, which distinguish it from other data reporting approaches, are:

· creating a national financial taxonomy, or shared dictionary of data fields, which can be used by businesses to report financial information to the government;

· using the creation of that taxonomy to drive out unnecessary or duplicated data descriptions;

· enabling use of that taxonomy for financial reporting to the government and facilitating straight-through reporting for many types of reports directly from accounting and reporting software in use by businesses and their intermediaries; and

· creating supporting mechanisms to make SBR efficient where they do not already exist (for example, a single government reporting service portal or gateway).[25]

We spoke with four groups of practitioners knowledgeable in the areas of data management, data standards, and regulatory issues, including those with experience working on SBR in the Netherlands and Australia, two academic researchers, and two representatives of state and local government finance offices on their thoughts of FDTA and the future of SBR in the United States. According to three of the four practitioner groups we spoke with, implementing the FDTA could be a first step towards moving the United States towards adopting a government-wide regulatory compliance reporting mechanism, similar to SBR. The fourth practitioner said that the FDTA alone will not put the United States on a path towards SBR given the FDTA’s narrow focus, but it is a step towards consistency across federal agencies and reporting entities. However, some of the practitioners noted that, given prior implementation experiences in other countries, it may ultimately take a decade or more to fully implement the FDTA before moving onto a government-wide mechanism.

Overall, representatives from all four of the practitioner

groups agreed that the technology for implementing a government-wide mechanism

such as SBR exists, but the primary areas of concern for potential future

efforts are interagency collaboration and establishing and maintaining data

standards. Our prior work identified effective practices in interagency

collaboration and data governance that can help address the concerns identified

by the practitioner groups when moving beyond the FDTA to a government-wide

standardized reporting mechanism similar to SBR. In addition, our prior work on

government-wide data standards efforts, such as the DATA Act, describes

challenges agencies faced during the implementation of data standards and how

they tried to address them.

Knowledgeable Practitioners and Our Leading Practices Cite the Importance of Interagency Collaboration Moving Forward

Using our prior work on government-wide efforts to establish data standards, such as the DATA Act in which OMB and Treasury established 57 data standards for reporting federal spending, among other things, we identified four areas that illustrate selected leading practices for interagency collaboration that would be particularly relevant to future data standardization efforts.[26]

|

GAO Leading Interagency Collaboration Practices Interagency collaboration involves collaboration between two or more federal entities. Collaboration can be broadly defined as any joint activity that is intended to produce more public value than could be produced when the organizations act alone. We have previously identified leading practices for interagency collaboration. These practices can provide valuable insight and guidance to improve collaboration between agencies, or within components of the same agency. · Define Common Outcomes · Ensure Accountability · Bridge Organizational Cultures · Identify and Sustain Leadership · Clarify Roles and Responsibilities · Include Relevant Participants · Leverage Resources and Information · Develop and Update Written Guidance and Agreements Source: GAO, Government Performance Management: Leading Practices to Enhance Interagency Collaboration and Address Crosscutting Challenges, GAO-23-105520 (Washington, D.C.: May 24, 2023). | GAO-26-108420 |

Identifying and sustaining leadership: We have reported that designating a leader can be beneficial because it centralizes accountability and speeds decision-making. We have previously reported that gaps in leadership can occur as administrations change. This can impair the effectiveness and efficiency of complex government-wide efforts, potentially resulting in delays and missed deadlines. We have further found that the influence of leadership can be strengthened by a direct relationship with the President, Congress, and other high-level officials. Alternatively, by sharing leadership, agencies can create buy-in and convey support for the collaborative effort.[27] For example, the DATA Act designated OMB and Treasury leadership responsibility for establishing government-wide financial data standards for any federal funds made available to or expended by federal agencies.

Clarifying roles and responsibilities: We have previously reported that collaborating agencies should work together to define and agree on their respective roles and responsibilities, including how the collaborative effort will be led. In doing so, agencies can clarify who will lead each task, organize their joint and individual efforts, and facilitate decision-making. Clarity over roles and responsibilities can be achieved when agencies work together to identify and leverage their strengths, resources, and authorities, as well as by agreeing to steps for decision-making.[28] For example, as leaders of the DATA Act government-wide implementation efforts, OMB and Treasury established an executive steering committee, which is responsible for setting overarching policy guidance and making key policy decisions affecting implementation of the act. The executive steering committee is supported by the Interagency Advisory Committee, responsible for providing recommendations to the steering committee related to DATA Act implementation.

Include relevant participants: We have reported that including relevant participants requires participating agencies to ensure that they have invited not only the relevant organizations but also any individuals who may have a stake in the collaborative effort. If these collaborative efforts do not consider the input of all relevant stakeholders, important opportunities for achieving outcomes may be missed. For example, we previously reported that Offices of Inspector General reported a variety of issues with the quality of agencies’ data submissions under the DATA Act. Specifically, the Offices of Inspector General reported their agencies need to work with Treasury, OMB, or other external stakeholders (e.g., a shared service provider or contractor) to resolve identified issues such as seeking clarification from OMB and Treasury to ensure the appropriate interpretation of DATA Act standards.

Developing and updating written guidance and agreements: We have reported that written guidance and agreements can also be used to document and monitor the application of interagency collaboration practices related to any collaborative effort. For example, in our early DATA Act work we reported that in the absence of detailed guidance related to policy, process, and technology changes, agencies faced challenges developing effective implementation plans or appropriately committing the necessary resources toward implementing the DATA Act. This was because implementation efforts and timelines were highly dependent on having timely and complete information. We recommended that OMB and Treasury take steps to align the release of finalized technical guidance to the implementation time frames specified.[29] OMB and Treasury implemented our recommendation by issuing finalized technical guidance and updates.

Any efforts to move beyond the FDTA to a government-wide regulatory compliance standardization mechanism, such as the SBR, will involve participation and collaboration across multiple federal agencies. Such collaboration can be especially difficult when agencies have different missions and regulatory requirements. A defined leadership structure with clearly defined and documented roles and responsibilities for all participating agencies will be important factors in any future wider effort’s potential success.

Representatives from all four practitioner groups and two academic researchers cited the importance of interagency collaboration to future data standardization efforts. For example, one practitioner group said that one of the main challenges facing efforts to create government-wide data standards are the people problems and not technology. This practitioner group stated that getting the agencies together to agree on data definitions is not an easy task. One practitioner group cited specific issues that could affect an agency’s ability to collaborate, including differing levels of institutional knowledge as well as an agency’s capacity to push forward the government-wide data standards. Another practitioner group stated that there is an unequal distribution of capabilities across the agencies and that some agencies may have more experience and a greater understanding of the regulatory process and will be further along than the other agencies during the individual-agency rulemaking process.

Another practitioner group noted that a primary challenge could arise if there is an absence of a lead agency to drive future rulemaking efforts. This practitioner group stated that establishing clear leadership allows for agencies of different capacities to implement standards moving forward. Another practitioner group stated that without a consistent team or staff, agencies may lose their institutional knowledge. Finally, an academic researcher stated that joint rulemakings can be difficult because agencies may struggle to reach consensus. In addition, another practitioner group noted that an additional challenge will be involving relevant stakeholders beyond the agencies. For example, according to this practitioner group, future data standardization efforts will need support from the local secretaries of state who will need to work together with federal agencies.

Knowledgeable Practitioners and Our Key Practices Cite Importance in Maintaining Consistency in Data Standards

According to key practices for data governance that we identified in our previous work, organizations should have documented policies and procedures for making and communicating decisions about changes to existing data standards (see sidebar).[30] Without transparent communication of changes, stakeholders—including staff at federal agencies required to report data according to these definitions—may miss important information relating to changes in how, when, and by whom definitions are to be applied.[31] Our prior work, for example, examined the quality of federal spending data under the DATA Act and identified the need for a data governance structure to ensure the integrity of data standards over time.[32] Moving forward beyond the FDTA’s joint rule, it will be important for agencies to communicate potential changes to their data standards as they implement their agency-specific regulations and the extent to which each agency varied or differed from another agency’s standards, for example.

|

GAO Key Practices for Data Governance Establishing a data governance structure—an institutionalized set of policies and procedures for providing data governance throughout the life cycle of developing and implementing data standards—is critical for ensuring that the integrity of the standards is maintained over time. Data governance is different from data management. Governance refers to the roles, responsibilities, policies, and procedures for making decisions to ensure effective data management, while data management involves implementing those decisions. A data governance structure can also provide consistent data management during times of change and transition. We identified the following key practices for data governance: Developing and approving data standards. · Managing, controlling, monitoring, and enforcing consistent application of data standards. · Making decisions about changes to existing data standards and resolving conflicts related to the application of data standards. · Obtaining input from stakeholders and involving them in key decisions, as appropriate. · Delineating roles and responsibilities for decision-making and accountability, including roles and responsibilities for stakeholder input on key decisions. Source: GAO, Data Act: OMB and Treasury Have Issued Additional Guidance and Have Improved Pilot Design but Implementation Challenges Remain, GAO-17-156 (Washington, D.C.: Dec. 8, 2016). | GAO-26-108420 |

Once the covered agencies have issued the FDTA’s final joint rule, and the agency-specific rulemaking is underway, more may be known about the extent to which the covered agencies are maintaining consistency in data standards. This process, as our prior work looking at past efforts to establish government-wide data standards has shown, can take a considerable period of time. The success of efforts to expand beyond the FDTA may depend, in part, on adherence to these key data governance practices and principles.

According to one practitioner group we interviewed, establishing and maintaining data standards may create better machine-readable data, resulting in increased interoperability and transparency of the data to all who would use it. According to another practitioner group, establishing the LEI as the required, nonproprietary, and open license identifier for legal entities in financial regulatory reporting may generate economies of scale for reporting entities and improve the transparency and useability of the data for regulators. Currently, according to this practitioner group, the use of different identifiers across agencies leads to inefficiency for reporting entities, as they need to have a variety of identifiers for different agencies that must be paid for and internally maintained. Through unifying on standards like a single identifier, the covered agencies establishing joint data standards could be seen as an important step towards the establishment of a government-wide regulatory compliance standardization mechanism.

However, representatives from three of the four practitioner groups cited concerns with maintaining the FDTA’s data standards when moving beyond the joint rule. As previously stated, each covered agency will determine the applicability of the joint standards when issuing their agency-specific rule. Specifically, to the extent that an agency has separate authority to adopt data standards, the agency may adopt other standards beyond the joint standards. One practitioner group questioned whether agencies would create or allow exceptions for different reporting entities during the agency-specific individual rulemaking step. The practitioner group suggested that smaller entities, which may have a harder time making the upfront investment, could potentially be granted a longer window to come into compliance (e.g., big banks could have 1 year, but smaller banks could have 3).

The same practitioner group stated that the risk of having differing standards is theoretical at this point in time given that the agency-specific rulemaking process has not begun. Further, another practitioner group stated that covered agencies should not have the discretion to define their own rules and standards because different standards across the covered agencies reduce the utility of each standard. Finally, an academic researcher questioned whether the goals of the FDTA, such as data standardization and interoperability, may be better suited to some regulatory agencies than others.

Agency Comments

We provided a draft of this product to the Board of Governors of the Federal Reserve System, Commodity Futures Trading Commission, Consumer Financial Protection Bureau, Federal Deposit Insurance Corporation, Federal Housing Finance Agency, National Credit Union Administration, Office of the Comptroller of the Currency, Securities and Exchange Commission, and the Department of the Treasury for comment. The Consumer Financial Protection Bureau, Federal Housing Finance Agency, and Office of the Comptroller of the Currency did not have any comments on the report. The Board of Governors of the Federal Reserve System, Commodity Futures Trading Commission, Federal Deposit Insurance Corporation, National Credit Union Administration, Securities and Exchange Commission, and the Department of the Treasury provided technical comments, which we incorporated as appropriate.

We are sending copies of this report to the appropriate congressional committees, the Chairman of the Board of Governors of the Federal Reserve System, Chairman of the Commodity Futures Trading Commission, Acting Director of the Consumer Financial Protection Bureau, Acting Chair of the Federal Deposit Insurance Corporation, Director of the Federal Housing Finance Agency, Chairman of the National Credit Union Administration, Chair of the Securities and Exchange Commission, Secretary of the Treasury, and other interested parties. In addition, the report is available at no charge on the GAO website at https://www.gao.gov.

If you or your staff have questions about this report, please contact me at JonesY@gao.gov. Contact points for our Offices of Congressional Relations and Media Relations may be found on the last page of this report. GAO staff who made key contributions to this report are listed in appendix III.

Yvonne D. Jones

Director, Strategic Issues

The nine agencies involved in implementing the Financial Data Transparency Act of 2022 are listed below, along with a summary description of their oversight provided by the covered agencies.

|

Financial Regulatory Agency |

Summary of Regulatory Oversight Role |

Oversight Population |

|

Board of Governors of the Federal Reserve System (Board) |

Supervises Federal Reserve Banks, state-chartered banks that opt to be members of the Federal Reserve System, and bank and savings and loan holding companies. Also supervises certain other entities, including the United States operations of foreign banks. The Federal Reserve System consists of the Board of Governors, 12 Reserve Banks, and the Federal Open Market Committee. The Board of Governors is an independent federal agency whose responsibilities include promoting the stability of financial markets and supervising financial institutions. The Board of Governors has delegated the authority to examine financial institutions to the Reserve Banks. |

As of June 2025, the Board supervises 3,640 banking organizations with a combined $17 trillion in assets, eight global systemically important banks with $16.6 trillion in total assets, and additional insurance and commercial savings and loan holding companies. |

|

Consumer Financial Protection Bureau (CFPB) |

Regulates the offering and provision of consumer financial products or services under federal consumer financial laws, enforces federal consumer financial law fairly and consistently, and educates and empowers consumers making financial decisions. |

CFPB has supervisory authority over insured depository institutions and insured credit unions with total assets of more than $10 billion, and their affiliates. CFPB also has supervisory authority over nondepository mortgage originators and servicers, consumer payday lenders, private student lenders, larger participants of other consumer financial markets as defined by CFPB rules, and other institutions if the CFPB has reasonable cause to determine, by order and after notice and a reasonable opportunity for such institution to respond, that the institution’s conduct poses risks to the consumer. |

|

Commodity Futures Trading Commission (CFTC) |

Primary regulator of futures, options, and swaps markets, including futures exchanges and intermediaries, such as futures commission merchants, and protects market users and the public from fraud, manipulation, abusive practices, and systemic risk related to derivatives subject to the Commodity Exchange Act, and fosters open, competitive, and financially sound futures markets. |

Over 41,400 entities and persons are under CFTC regulation, including trading entities, clearing entities, data repositories, registered market participants, and a registered futures association. |

|

Federal Deposit Insurance Corporation (FDIC) |

Supervises insured state-chartered banks that are not members of the Federal Reserve System, state-chartered savings associations, and insured state-chartered branches of foreign banks. At institutions where FDIC is not the primary federal regulator, FDIC staff work with other regulatory authorities as a back-up regulator to identify emerging risks and assess the overall risk profile of large and complex institutions. |

As of the quarter ending December 31, 2025, the FDIC supervised 2,744 insured depository institutions who reported holding $4.03 trillion in total consolidated assets. Included are 2,473 State nonmember banks, 265 savings institutions, and six insured branches of foreign banks. Institutions for which the FDIC has backup supervisory authority include 703 state member banks that reported $4.50 trillion in assets and 898 institutions that reported $16.87 trillion in assets. Included in the latter are 673 national banks, 222 savings institutions, and three insured branches of foreign banks. |

|

Federal Housing Finance Agency (FHFA) |

Regulates Fannie Mae, Freddie Mac, and the Federal Home Loan Bank System and has supervisory and enforcement authorities related to ensuring the enterprises operate in a safe and sound manner and comply with fair lending laws. |

Together, Fannie Mae, Freddie Mac, and the Federal Home Loan Bank System provide more than $8.1 trillion in funding for the United States mortgage markets and financial institutions. |

|

National Credit Union Administration (NCUA) |

Charters and supervises federally-chartered credit unions and insures savings and deposits in federal and most state-chartered credit unions. |

As of June 2025, total assets in 4,370 federally insured credit unions were approximately $2.38 trillion. |

|

Office of the Comptroller of the Currency (OCC) |

Charters and supervises national banks and savings associations and federally chartered branches and agencies of foreign banks. |

As of September 30, 2025, the federal banking system comprises 1,010 financial institutions, or 961 banks and 49 federal branches and agencies of foreign banks operating in the United States. Of the 961 banks, 695 have less than $1 billion in assets, while 54 have more than $10 billion. In total, the banks within the federal banking system hold $16.7 trillion (67 percent of the total assets held by all United States banks). |

|

U.S. Securities and Exchange Commission (SEC) |

Regulates and oversees securities and capital markets to protect investors, maintain fair, orderly, and efficient markets, and facilitate capital formation. Oversees self-regulatory organizations in the securities industry to ensure they carry out their regulatory responsibilities—for example, by conducting examinations to improve compliance, prevent fraud, monitor risk, and inform policy. |

Market participants under the SEC’s oversight include around 7,750 reporting companies, 14,300 registered funds, 16,400 investment advisers, 3,300 broker-dealers, 419 municipal advisors, 324 transfer agents, 29 national securities exchanges, 114 alternative trading systems, 10 credit rating agencies, seven active registered clearing agencies, and 3 security-based swap data repositories. In addition, the SEC oversees the Public Company Accounting Oversight Board, the Financial Industry Regulatory Authority, the Municipal Securities Rulemaking Board, the Securities Investor Protection Corporation, and the Financial Accounting Standards Board. |

|

Department of the Treasury (Treasury) Office of Financial Research (OFR) |

Serves the Financial Stability Oversight Council and its member agencies by improving the quality, transparency, and accessibility of financial data and information, conducting and sponsoring research related to financial stability, and promoting best practices in risk management. |

Treasury is responsible for promoting economic prosperity and ensuring the financial security of the United States. Treasury’s activities include advising the President on economic policy, fostering improved governance in financial institutions (markets), and protecting the integrity of the United States financial system. This results in oversight ranging from individuals to institutions. |

Source: GAO analysis of public and agency information. | GAO‑26‑108420

The Financial Data Transparency Act of 2022 (FDTA) directs us to report on the feasibility, costs, and potential benefits of building upon the taxonomy established by the FDTA to arrive at a federal government-wide regulatory compliance standardization mechanism similar to Standard Business Reporting (SBR).[33] This report (1) describes stakeholders’ views on the potential benefits, costs, and challenges of implementing the FDTA’s requirements for data standardization and (2) describes effective practices to facilitate future government-wide data standardization efforts and stakeholders’ views on such potential efforts.

For both objectives, we reviewed our prior work about related legislation on government-wide data standards, specifically the Federal Funding Accountability and Transparency Act of 2006 (FFATA), the Digital Accountability and Transparency Act of 2014 (DATA Act), and the Grant Reporting Efficiency and Agreements Transparency Act of 2019 (GREAT Act).[34] We also reviewed available information about the implementation of SBR in Australia and the Netherlands because they have mature SBR systems.[35] Finally, we interviewed two academic researchers knowledgeable in regulatory issues to obtain perspectives about past financial regulatory reform efforts, relevant leading practices, and potential challenges in interagency collaboration.

For the first objective, we reviewed available published information related to the FDTA or related efforts in the United States and abroad, to understand potential steps to implement the FDTA. We received written information from eight of the nine agencies involved in implementing the FDTA and interviewed the Office of the Comptroller of the Currency to understand the status of the required rulemakings and potential benefits, costs, and challenges of FDTA implementation.[36] For context and background purposes, we also discussed the agencies’ processes and practices for collaborating on the August 2024 joint proposed rule. This included their governance structures and any policies or procedures they established as part of this collaboration. These covered agencies are:

· Board of Governors of the Federal Reserve System,

· Commodity Futures Trading Commission,

· Consumer Financial Protection Bureau,

· Federal Deposit Insurance Corporation,

· Federal Housing Finance Agency,

· National Credit Union Administration,

· Office of the Comptroller of the Currency,

· Securities and Exchange Commission, and

· Department of the Treasury.[37]

Throughout this report, when we say “most” covered agencies, we mean between six and eight of the nine; when we say “some” covered agencies, we mean between two and five.

We identified eight external organizations to interview by reviewing the literature on the FDTA and SBR and added interviewees referred to us by our stakeholders and other interviewees.

· To understand the technology and their experiences with compliance reporting, we met with four practitioner groups knowledgeable about data standards and the FDTA, comprised of an advocacy group for data-driven public policy and three producers of software solutions or other products to support data standardization.

· To gain insight into potential effects of FDTA implementation on their operations and categories of potential costs and benefits, we also interviewed representatives of four entities that report information subject to the FDTA (reporting entities). To identify interviewees, we researched entities that were recommended to us or that submitted comment letters on the August 2024 proposed joint rule, including those representative of banks, broker-dealers, and asset managers. We reviewed publicly available information on the areas of focus and positions of each entity, focusing on those that did not have a direct financial position in the outcomes of specific decisions pending for the FDTA’s implementation. We contacted five potential interviewees based on our research, and we obtained responses from four of those. These interviewees included a financial sector trade association, a practitioner in the banking sector, and two groups representing state and local government finance offices.

For the second objective, we reviewed our prior work to identify effective practices in interagency collaboration and data governance structures.[38] Using our prior work on government-wide efforts to establish data standards, such as the DATA Act, in which the Office of Management and Budget and the Department of the Treasury established 57 data standards for reporting federal spending, among other things, we selected leading practices for interagency collaboration that would be particularly relevant to future data standardization efforts. We discussed with interviewees described above their knowledge of SBR and their views on the possibility of implementing government-wide data standards established by the FDTA.

We conducted this performance audit from April 2025 to May 2026 in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions, based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

GAO Contact

Yvonne D. Jones JonesY@gao.gov

Staff Acknowledgments

In addition to the contact named above, Danielle Novak (Assistant Director), Anthony Bova (Analyst-in-Charge), Michelle B. Bacon, Dewi Djunaidy, Eric Dobbie, Pamela Davidson, Robert Gebhart, Terence Lam, Alicia White, and Mercedes Wilson-Barthes made key contributions to this report.

The Government Accountability Office, the audit, evaluation, and investigative arm of Congress, exists to support Congress in meeting its constitutional responsibilities and to help improve the performance and accountability of the federal government for the American people. GAO examines the use of public funds; evaluates federal programs and policies; and provides analyses, recommendations, and other assistance to help Congress make informed oversight, policy, and funding decisions. GAO’s commitment to good government is reflected in its core values of accountability, integrity, and reliability.

Obtaining Copies of GAO Reports and Testimony

The fastest and easiest way to obtain copies of GAO documents at no cost is through our website. Each weekday afternoon, GAO posts on its website newly released reports, testimony, and correspondence. You can also subscribe to GAO’s email updates to receive notification of newly posted products.

Order by Phone

The price of each GAO publication reflects GAO’s actual cost of production and distribution and depends on the number of pages in the publication and whether the publication is printed in color or black and white. Pricing and ordering information is posted on GAO’s website, https://www.gao.gov/ordering.htm.

Place orders by calling (202) 512-6000, toll free (866) 801-7077,

or

TDD (202) 512-2537.

Orders may be paid for using American Express, Discover Card, MasterCard, Visa, check, or money order. Call for additional information.

Connect with GAO

Connect with GAO on X,

LinkedIn, Instagram, and YouTube.

Subscribe to our Email Updates. Listen to our Podcasts.

Visit GAO on the web at https://www.gao.gov.

To Report Fraud, Waste, and Abuse in Federal Programs

Contact FraudNet:

Website: https://www.gao.gov/about/what-gao-does/fraudnet

Automated answering system: (800) 424-5454

Media Relations

Sarah Kaczmarek, Managing Director, Media@gao.gov

Congressional Relations

David A. Powner, Acting Managing Director, CongRel@gao.gov

General Inquiries

[1]This report addresses only federal regulation of financial institutions and does not address state regulation.

[2]GAO, Analyzing Regulatory Burden: Policies and Analyses Under the Regulatory Flexibility Act and Retrospective Reviews Could Be Improved, GAO‑18‑404T (Washington, D.C.: Feb. 27, 2018); and Financial Regulation: Complex and Fragmented Structure Could Be Streamlined to Improve Effectiveness, GAO‑16‑175 (Washington, D.C.: Feb. 25, 2016).

[3]The stated purpose of the FDTA as originally introduced in the Senate included putting the United States on a path towards building a comprehensive Standard Business Reporting program to ultimately harmonize and reduce the private sector’s regulatory compliance burden, while enhancing transparency and accountability. This was included in the prefatory language to the FDTA as introduced in the Senate (S. 4295, 117th Cong. (2022)). The text of the Senate bill was incorporated with certain changes into H.R.7776 - James M. Inhofe National Defense Authorization Act for Fiscal Year 2023, Pub. L. No. 117-263.

[4]These covered agencies are Board of Governors of the Federal Reserve System, Consumer Financial Protection Bureau, Federal Deposit Insurance Corporation, Federal Housing Finance Agency, National Credit Union Administration, Office of the Comptroller of the Currency, Securities and Exchange Commission, and the Department of the Treasury. As permitted by statute, on May 3, 2024, the Secretary of the Treasury designated the Commodity Futures Trading Commission as an additional covered agency under the FDTA.

[5]Not all of the covered agencies’ information collections are subject to the FDTA.

[6]Interoperability of data refers to the ability of data collection systems to exchange information with and process information from other systems, which could include across agencies.

[7]In the Netherlands and Australia, SBR is a standardized approach to online or digital recordkeeping that was introduced to simplify business reporting obligations.

[8]GAO, Data Act: Data Standards Established, but More Complete and Timely Guidance Is Needed to Ensure Effective Implementation, GAO‑16‑261 (Washington, D.C.: Jan. 29, 2016).

[9]Federal Funding Accountability and Transparency Act of 2006, Pub. L. No. 109-282, 120 Stat. 1186; Digital Accountability and Transparency Act of 2014, Pub. L. No. 113-101, 128 Stat. 1146; and Grant Reporting Efficiency and Agreements Transparency Act of 2019, Pub. L. No. 116-103, 133 Stat. 3266. GAO, Grants Management: Action Needed to Ensure Consistency and Usefulness of New Data Standards, GAO‑24‑106164 (Washington, D.C.: Jan. 25, 2024).

[10]While the FDTA does not define “collection of information,” the covered agencies proposed to define “collections of information” as used in connection with the FDTA by reference to the following definition. Under 44 U.S.C. § 3502(3), the term ‘‘collection of information’’ means the obtaining, causing to be obtained, soliciting, or requiring the disclosure to third parties or the public, of facts or opinions by or for an agency, regardless of form or format, calling for either answers to identical questions posed to, or identical reporting or recordkeeping requirements imposed on, 10 or more persons, other than agencies, instrumentalities, or employees of the United States; or answers to questions posed to agencies, instrumentalities, or employees of the United States which are to be used for general statistical purposes.

[11]Financial Data Transparency Act Joint Data Standards, 89 Fed. Reg. 67890 (Aug. 22, 2024).

[12]The Dodd-Frank Wall Street Reform and Consumer Protection Act created FSOC in 2010 to identify and respond to potential risks to the stability of the United States financial system. The act granted FSOC authority to make recommendations and designate certain entities and activities for additional regulation or heightened supervision to allow it to respond to potential risks.

[13]The FDTA defines a data standard as “a standard that specifies rules by which data is described and recorded.” Pub. L. No. 117-263, § 5811(a),136 Stat. 2395, 3422 (2022). GAO‑24‑106164.

[14]Federal Funding Accountability and Transparency Act of 2006, Pub. L. No. 109-282, 120 Stat. 1186. GAO‑24‑106164.

[15]Digital Accountability and Transparency Act of 2014, Pub. L. No. 113-101, 128 Stat. 1146. GAO, Data Act: OMB and Treasury Have Issued Additional Guidance and Have Improved Pilot Design but Implementation Challenges Remain, GAO‑17‑156 (Washington, D.C.: Dec. 8, 2016).

[16]Grant Reporting Efficiency and Agreements Transparency Act of 2019, Pub. L. No. 116-103, 133 Stat. 3266. GAO, Grants Management: HHS Has Taken Steps to Modernize Government-wide Grants Management, GAO‑24‑106008 (Washington, D.C.: Dec. 14, 2023).

[17]Other countries with SBR include New Zealand, Finland, and Sweden.

[18]Data Foundation and PwC, Standard Business Reporting: Open Data to Cut Compliance Costs (Mar. 16, 2017).

[19]The FDTA does not require the use of XBRL or XML. Other options could be employed to meet the machine-readability standard set by the FDTA.

[20]We have previously reported that the term “machine-readable,” when used with respect to data, refers to data in a format that can be easily processed by a computer without human intervention, while ensuring no semantic meaning is lost. GAO‑24‑106164.

[21]The Office of the Comptroller of the Currency (OCC) told us that it did prepare an impact analysis for the proposed joint rulemaking and determined that rule did not create any new requirements on reporting entities and therefore resulted in a de minimis impact on OCC-supervised institutions. OCC stated that a separate impact analysis will be conducted for the subsequent agency-specific proposed rulemaking once it is drafted.

[22]Under 15 U.S.C. § 77b(a)(4), the term “issuer” includes every person who issues or proposes to issue any security with certain exceptions.

[23]The Financial Data Transparency Act of 2022 requires SEC to report semiannually on the public and internal use of machine-readable data for corporate disclosures. The FDTA requires the commission to submit this report to the Committee on Banking, Housing, and Urban Affairs of the Senate and the Committee on Financial Services of the House of Representatives every 180 days until December 23, 2029, when the provision requiring the report sunsets. Financial Data Transparency Act of 2022 included in the James M. Inhofe National Defense Authorization Act for Fiscal Year 2023, Pub. L. No. 117-263, § 5825, 136 Stat. 2395, 3429-3430. Securities and Exchange Commission, Semi-Annual Report to Congress, Regarding Public and Internal Use of Machine-Readable Data for Corporate Disclosures (Washington, D.C.: June 2025); Securities and Exchange Commission, Semi-Annual Report to Congress, Regarding Public and Internal Use of Machine-Readable Data for Corporate Disclosures (Washington, D.C.: December 2025).

[24]For the purposes of this report, we are not reporting views of covered agencies on the substance of the FDTA proposed rulemaking.

[25]The Organization for Economic Co-operation and Development, Centre for Tax Policy and Administration, Forum on Tax Administration: Taxpayer Services Sub-Group, Guidance Note Standard Business Reporting (2009), https://www.oecd.org/content/dam/oecd/en/topics/policy-issues/tax-administration/standard-business-reporting.pdf, accessed on January 21, 2026.

[26]GAO, Government Performance Management: Leading Practices to Enhance Interagency Collaboration and Address Crosscutting Challenges, GAO‑23‑105520 (Washington, D.C.: May 24, 2023).

[28]GAO‑23‑105520 and GAO, Managing for Results: Implementation Approaches Used to Enhance Collaboration in Interagency Groups, GAO‑14‑220 (Washington, D.C.: Feb. 14, 2014).