FEDERAL STUDENT LOANS

Education Needs to Address Gaps in Servicer Oversight

Report to Congressional Requesters

United States Government Accountability Office

A report to congressional requesters

For more information, contact: Melissa Emrey-Arras at EmreyArrasM@gao.gov.

What GAO Found

In February 2025, the Department of Education’s Office of Federal Student Aid (FSA) stopped assessing student loan servicers on accuracy and call quality due to lack of staff capacity, according to agency officials. Prior to discontinuing these quarterly assessments, FSA assessed servicers on these metrics for two quarters through the following actions.

· Accuracy. FSA would review data for borrowers in servicer systems and compare it to data in FSA systems to determine if servicers were keeping accurate records for borrowers.

· Call quality. FSA would review phone calls between borrowers and servicers to determine if servicers were providing good and accurate customer service.

The decision to stop assessing these performance metrics occurred shortly after the new administration began issuing presidential directives and guidance on downsizing the federal workforce in January 2025. Education reported that between January and December 2025, the number of staff at FSA dropped from 1,433 to 777, a reduction of 656 personnel.

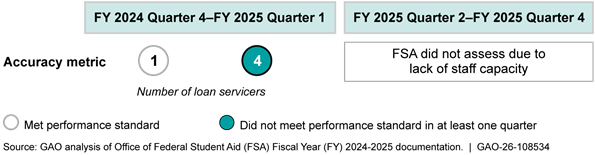

Prior to FSA discontinuing this oversight, most servicers did not meet the performance standards for accuracy and faced corresponding financial penalties of about $850,000. FSA continued to assess servicer performance on their other performance metrics, which it characterized as less labor intensive to monitor.

In September 2025, FSA officials said Education was working to implement more efficient oversight methods that leverage data analysis and exploring possible changes to the contract performance standards. However, as of December 2025, FSA was not using any replacement methods for overseeing accuracy and call quality and had not changed the performance standards.

By not assessing servicer accuracy and call quality, FSA lacks assurance that borrower records are correct and that servicers are giving borrowers quality information. Inaccurate records can result in borrowers being billed for incorrect amounts or placed in the wrong repayment status. Additionally, borrowers need to be given accurate information when they call for help. Addressing these gaps in servicer oversight will assist Education in carrying out its statutory responsibilities and also help the government avoid overpaying servicers for poor performance.

Why GAO Did This Study

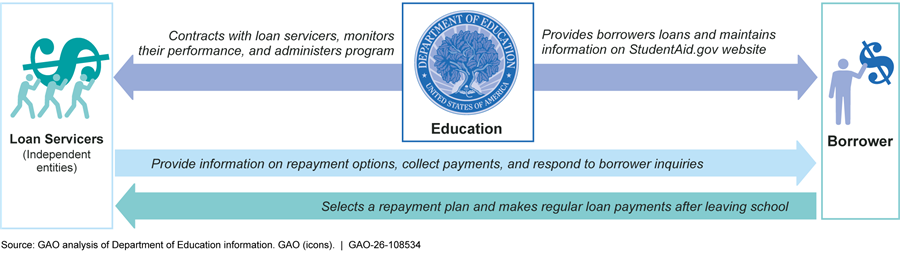

FSA is statutorily responsible for managing federal student aid programs and overseeing contracted student loan servicers. The servicers process loan payments, provide borrowers with information on repayment plans and forgiveness options, and maintain loan records.

In April 2024, FSA implemented new contracts for its student loan servicers that set performance standards for student loan servicers on six metrics, including accuracy and call quality. Under these contracts, FSA enforces financial penalties if servicers do not meet performance standards related to these metrics.

GAO was asked to review Education’s capacity to carry out its statutory responsibilities. This report examines the extent to which recent staffing reductions have affected how FSA carries out its responsibilities to oversee loan servicers. Additional reports will examine related topics at other offices within Education.

For this report, GAO reviewed FSA documentation, servicer performance and billing reports, and relevant laws. GAO also interviewed FSA officials as well as representatives of borrower advocacy organizations.

What GAO Recommends

GAO is making one recommendation to Education to assess servicer accuracy and call quality. Education disagreed with GAO’s recommendation, stating that it uses a variety of other methods to assess servicer performance. GAO does not believe these methods are effective substitutes and maintains the importance of assessing servicer call quality and accuracy.

|

Abbreviations |

|

|

|

FSA |

Office of Federal Student Aid |

|

|

FTE |

Full time equivalent |

|

|

OBBBA |

One Big Beautiful Bill Act |

|

|

RIF |

Reduction in force |

|

|

USDS |

Unified Servicing and Data Solution |

|

This is a work of the U.S. government and is not subject to copyright protection in the United States. The published product may be reproduced and distributed in its entirety without further permission from GAO. However, because this work may contain copyrighted images or other material, permission from the copyright holder may be necessary if you wish to reproduce this material separately.

March 5, 2026

The Honorable Bernard Sanders

Ranking Member

Committee on Health, Education, Labor and Pensions

United States Senate

The Honorable Robert C. “Bobby” Scott

Ranking Member

Committee on Education and Workforce

House of Representatives

Starting in January 2025, the Department of Education implemented various executive actions to cut the department’s workforce of about 4,100 workers by half. According to Education, this included the reduction of about 46 percent of the employees in Education’s Office of Federal Student Aid (FSA). This office is responsible for managing federal student aid programs authorized under Title IV of the Higher Education Act of 1965, as amended. FSA staff oversee the administration of federal grants, loans, and work-study funds to support students’ postsecondary education.

FSA’s responsibilities have grown substantially in recent years based on changes to the size and complexity of the federal student loan program, which now exceeds $1.6 trillion in outstanding loans. To support the administration of these loans, FSA contracts with five loan servicers to assist with billing and other tasks, such as communicating with borrowers about repayment options.

You asked us to examine Education’s capacity to carry out its statutory responsibilities. This report examines the extent to which recent staffing reductions have affected how FSA carries out its responsibilities to oversee loan servicers.[1] We recently reported on issues related to the impact of staffing reductions at Education’s Office for Civil Rights. We also plan to examine similar issues at Education’s Institute of Education Sciences.

To address our objective, we reviewed relevant federal laws and regulations. We also reviewed FSA’s servicer contracts, as well as servicer invoices and performance reports from April 2024 through July 2025, the time period covered under the current contracts and the most recent data available at the time of our review. Specifically, we reviewed servicer invoices and performance reports both before and after staffing reductions at FSA, to assess FSA’s capacity to oversee servicers and hold them accountable for their performance. We analyzed data in these documents to calculate financial penalties FSA assessed servicers as part of its oversight. To determine data reliability, we reviewed relevant documentation and interviewed knowledgeable officials. We determined that these data were sufficiently reliable for our purpose of reporting on financial penalties associated with FSA’s oversight of servicers.

We interviewed FSA officials regarding oversight of servicers and changes in operations since the staff reductions. We also interviewed representatives of three borrower advocacy organizations to obtain perspectives on the impact of staff reductions on how FSA performs its statutory responsibilities and FSA’s responsiveness to stakeholders. In addition, we reviewed previous GAO work on FSA’s oversight of loan servicers[2] and Education’s recent financial audits.[3]

We conducted this performance audit from June 2025 to March 2026 in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

Background

The Higher Education Amendments of 1998 established FSA as a performance-based organization to, among other things, provide greater flexibility in the management and administration of the federal student aid programs.[4]

FSA is statutorily responsible for a range of functions throughout the student aid life cycle.[5] FSA oversees the loan servicers it contracts with to help manage the portfolio of federal student loans the department owns.[6] Currently, FSA manages contracts with five student loan servicers. These servicers process payments, provide borrowers with information on repayment plans and forgiveness options, and maintain loan records (see fig. 1).

In April 2024, FSA implemented new contracts for five student loan servicers to support the transition to a new loan servicing environment called the Unified Servicing and Data Solution (USDS). The USDS contracts set performance standards for student loan servicers on six metrics: accuracy, call quality, call abandon rate, customer satisfaction, timeliness of completion of certain servicing tasks, and financial monitoring.[7]

As part of the USDS contracts, FSA can enforce financial penalties associated with these metrics by withholding payment for part of a servicer’s bill for the final month of the quarter if it determines that the servicer was unable to reach its performance standards that quarter. Generally, FSA can withhold up to 5 percent payment per metric from a given servicer’s bill, with an overall cap of a 20 percent penalty for the entire bill—even if the sum for the six metrics exceeds 20 percent. However, FSA will withhold additional funds from a servicer for repeated poor performance.[8]

Changes to Federal Student Loans

Over the next year, Education will implement various changes to federal student loan programs affecting millions of borrowers. Public Law 119-21—commonly known as the One Big Beautiful Bill Act (OBBBA)—included provisions changing the repayment plans available to borrowers starting in July 2026.[9] For example, the OBBBA sunsets existing income-driven repayment plans and creates a new Repayment Assistance Plan.[10] A new Standard repayment plan—with fixed monthly payments and repayment terms ranging from 10 to 25 years, based on the total outstanding loan amount—will also be available.

Timeline of Selected FSA Staff Reductions and Related Actions

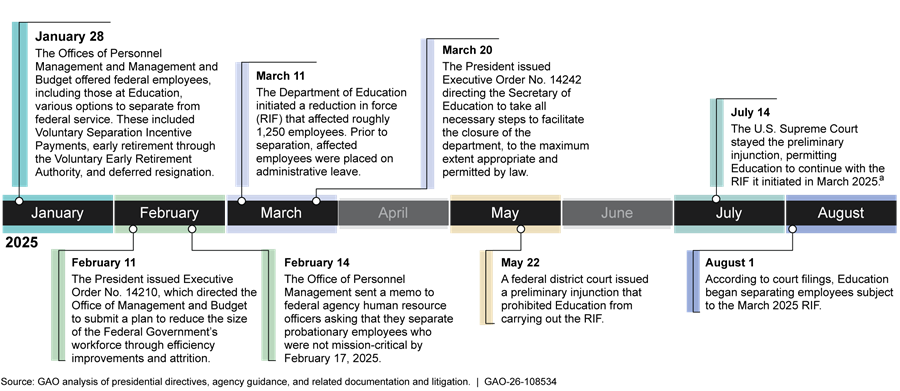

Education reported that between January 20, 2025, and December 1, 2025, the number of full time equivalent (FTE) personnel in FSA dropped from 1,433 to 777—a reduction of 656 FTE. Figure 2 displays a timeline of actions that relate to Education’s staffing levels from January through August 2025.

Figure 2: Timeline of Actions Related to Department of Education Staffing Levels, January–August 2025

aThis stay did not impact a separate preliminary injunction that prohibited Education from carrying out its RIF with respect to Office for Civil Rights employees. Education rescinded the RIF actions for Office for Civil Rights staff in early January 2026. The litigation related to Education’s RIFs is ongoing, as of February 2026.

Education Staff Reductions Have Led to Decreased Oversight of Servicers

In February 2025, Education stopped assessing accuracy and call quality for its student loan servicers due to lack of FSA staff capacity, according to agency officials.[11] The two metrics were intended to measure whether student loan servicers were (1) keeping complete and accurate records for borrowers and (2) providing borrowers good customer service.[12] Prior to discontinuing these quarterly assessments, FSA assessed servicers on these metrics for two quarters through the following actions (see textbox).

|

Office of Federal Student Aid (FSA) Assessments of Servicer Accuracy and Call Quality Prior to discontinuing these assessments in February 2025, FSA staff assessed servicers on: · Accuracy. FSA performed two types of quarterly reviews for each servicer: (1) data matches for samples of thousands of borrowers between servicer data systems and FSA data systems, and (2) targeted reviews of servicer data on borrowers in specific statuses, such as those temporarily postponing monthly payments through forbearance. · Call quality. FSA reviewed recordings of phone calls between borrowers and servicers to determine whether servicer representatives greeted borrowers, provided complete and accurate information, and displayed professionalism, among other things. |

Source: GAO review of FSA documents. Ɩ GAO‑26‑108534

The decision to stop assessing servicer performance in these areas followed presidential directives and guidance on the federal workforce from the Office of Personnel Management and Office of Management and Budget in January 2025. These directives and guidance directed federal agencies, including Education, to downsize the federal workforce and restructure the federal government. Education took various actions to implement this guidance and reduced the size of its workforce.

Prior to FSA discontinuing its oversight of these metrics, most servicers did not meet the performance standards for accuracy. In total, four of the five servicers did not meet the accuracy performance standard and faced associated financial penalties in at least one of the two quarters during which FSA assessed servicer accuracy.[13] Furthermore, two servicers were penalized the maximum 5 percent relating to the accuracy metric. Each servicer met its performance standard for call quality in those two quarters (see fig. 3).

By discontinuing its oversight of servicer accuracy, FSA limits its ability to identify and remedy systemic servicing issues. FSA previously used the results of assessments of servicer accuracy to identify systemic deficiencies and put servicers on corrective action plans to address them. For example, during the first quarter of fiscal year 2025, FSA discovered that one servicer was not processing payment refunds for borrowers in a timely manner.[14] FSA officials said the servicer subsequently developed a corrective action plan and implemented a system to ensure it issued refunds to borrowers on time.

Education is also likely missing opportunities to address material weaknesses raised by its independent auditor. In recent years, Education’s audits have cited concerns with the department using inaccurate data to estimate costs. Specifically, in fiscal years 2023 and 2024, Education’s auditor identified material weaknesses in the relevance and reliability of data the department uses to estimate the lifetime costs of the federal student loan program, including errors in loan status histories reported by servicers.[15] Prior to discontinuing its assessments of servicer accuracy, FSA reviewed loan status history data for borrowers as part of its oversight of servicers for this metric. By discontinuing assessments of servicer data, Education limits its ability to detect and correct inaccurate loan records for borrowers.

In addition, FSA is missing opportunities to ensure that servicers are providing borrowers complete and accurate information as it implements major statutory changes to student loan repayment options affecting millions of borrowers. For instance, servicers will need to accurately record the transition to new repayment plans for millions of borrowers. These repayment plan changes may also prompt significant borrower outreach to servicers.

The current USDS contracts state that FSA will perform quarterly monitoring of the accuracy and call quality metrics. Under the contracts, FSA can waive performance metrics in a given period. In September 2025, FSA officials said the department was working to implement more efficient oversight methods that leverage data analysis and exploring possible changes to the contract performance standards. However, as of December 2025, FSA was not using any replacement methods for overseeing accuracy and call quality and had not changed the performance standards.[16]

Education’s guidance states that every contract should be monitored to the extent appropriate to provide assurance that the contractor performs the work called for in the contract and develops a clear record of accountability for performance.[17] Furthermore, the Federal Acquisition Regulation states that to improve contractor performance, agencies shall collect relevant data to determine the effectiveness of incentive fees, such as the decreases tied to performance targets in the USDS contract.[18] In addition, Office of Management and Budget guidance states that agencies should ensure sufficient human resources are available to properly structure and monitor contracts.[19]

By not assessing servicer accuracy and call quality, FSA risks overpaying servicers that provide poor service to borrowers. For example, if servicers had not met their contractually required performance standards in the last three quarters of fiscal year 2025, FSA could have penalized them financially. Specifically, FSA previously withheld a total of about $850,000 from servicers who did not meet the performance standards for accuracy in the two quarters that FSA monitored servicers for accuracy under the USDS contracts, according to our analysis. Given FSA will increase financial penalties for repeated poor performance, it is possible that the total withheld could have grown had FSA continued its oversight of servicer accuracy. In addition, representatives from borrower advocacy organizations expressed concerns about FSA’s ability to oversee servicers given the reductions in capacity. Furthermore, representatives from one of these organizations told us that without the risk of financial penalties, they do not believe FSA can hold servicers accountable.

These gaps in oversight may also negatively affect borrowers and enable systemic servicing problems to go unnoticed, which is contrary to Education’s strategic objective to support borrowers in successfully repaying their loans and to hold contractors accountable.[20] FSA informed servicers that it has waived financial penalties relating to this oversight, so servicers may have less incentive to maintain accuracy and call quality. If servicers’ records are inaccurate, borrowers could, for instance, be placed in the wrong loan repayment status, billed for incorrect amounts, or not have a refund processed in time. Similarly, FSA has not monitored calls since February 2025, so there is a risk that borrowers have received or will receive incorrect information and poor customer service.

Conclusions

Education reduced its workforce by half and stopped key oversight of its loan servicers, which help manage a portfolio of more than $1.6 trillion in federal student loans. By discontinuing assessments of servicer accuracy and call quality, the agency risks overpaying servicers for poor service. In turn, borrowers may face financial consequences related to overbilling or being placed in the wrong loan repayment status.

Assessing servicer accuracy and call quality would assist Education in carrying out its statutory responsibilities. Without this oversight, inaccurate records and poor call quality loom as growing risks for borrowers and the federal government. These risks are magnified by FSA’s coming rollout of large-scale changes to the federal student loan program that will affect millions of borrowers. Those borrowers will need accurate and complete information when they call for help.

Recommendation for Executive Action

We are making the following recommendation to Education:

The Secretary of Education should ensure that FSA assesses servicer accuracy and call quality. (Recommendation 1)

Agency Comments and Our Evaluation

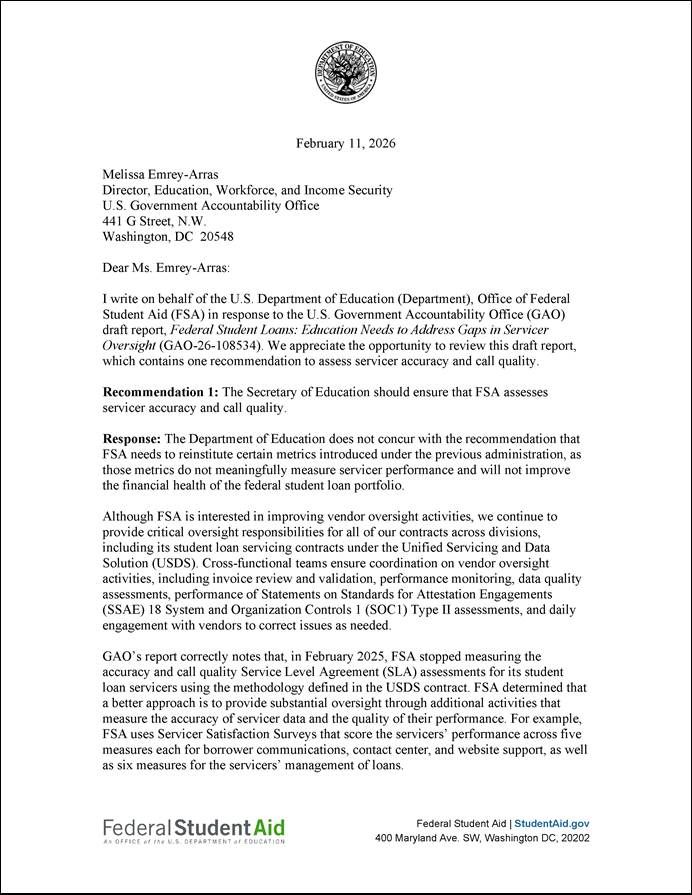

We provided a draft of this report to Education for review and comment. Education’s written comments are reproduced in appendix I. Education also provided technical comments, which we incorporated as appropriate.

In its written comments, Education said it did not concur with our recommendation to assess servicer accuracy and call quality. Education asserted that the servicer accuracy and call quality metrics do not meaningfully measure servicers’ performance and would not improve the financial health of the federal student loan portfolio.

Education’s written comments confirmed that, in February 2025, it stopped measuring the servicer accuracy and call quality metrics in its servicer contracts. Further, Education said that it uses a variety of robust methods to assess servicer accuracy and call quality to fulfill its servicer oversight responsibilities. Education said these methods include data quality assessments, cross-system data validation, audits, surveys, complaint reviews, operational meetings between FSA and servicers, and leadership oversight. Education asserted that these methods taken together provide a superior strategy to the assessments of servicer accuracy and call quality.

We do not dispute the value of Education using multiple methods to oversee its loan servicers, given the critical role they play in working with borrowers and helping administer more than $1.6 trillion in outstanding federal student loans. However, these oversight methods are not a substitute for directly assessing servicer accuracy and call quality and holding servicers accountable for their performance.

In its written comments, Education described working with loan servicers to validate data accuracy across FSA systems to improve the results of the department’s financial statement audit. While this effort was helpful, it was not sufficient to address longstanding data accuracy issues, and Education’s independent financial auditor reported in January 2026 that Education continued to have a material weakness related to the reliability of its student loan data.

Education also highlighted required audit reports, known as System and Organization Controls 1 (SOC 1) reports, that servicers submit on a semi-annual and annual basis. However, Education’s independent financial auditor recently identified the department’s controls over these reports as a significant deficiency in need of improvement. The auditor found that controls to ensure complete and timely monitoring of SOC reports were not operating effectively. This increases the risk of incomplete or inaccurate loan receivable information, data, and transactions that could result in incomplete and inaccurate financial statements.

Directly assessing servicer accuracy and holding them accountable for performance in this area would enable Education to better detect and correct inaccurate loan records for borrowers. As noted in the report, when the department used the accuracy metric it was able to identify systemic deficiencies and put servicers on corrective action plans to address them. In addition, Education was able to recoup $850,000 as a result of levying financial penalties on servicers for their errors.

In terms of assessing servicer call quality, the alternative strategies noted by Education in its comment letter do not directly and systematically review borrower calls to ensure that borrowers receive correct information when they call for help. In contrast, under the call quality metric, FSA reviewed recordings of phone calls between borrowers and servicers and identified whether borrowers were given complete and accurate information. As noted in the report, servicers may have less incentive to maintain call quality if they are not being assessed on it, putting borrowers at risk of receiving incorrect information.

Taken as a whole, Education has not outlined a systematic approach that ensures servicers are maintaining accurate records or providing correct information to callers. In addition, the monitoring tools Education described do not include mechanisms, such as financial penalties, to hold servicers accountable for accuracy and call quality and ensure the government is not overpaying them for poor performance. Therefore, we continue to believe that Education should ensure FSA assesses servicer accuracy and call quality.

As agreed with your offices, unless you publicly announce the contents of this report earlier, we plan no further distribution until 30 days from the report date. At that time, we will send copies to the appropriate congressional committees and the Secretary of Education. In addition, the report will be available at no charge on the GAO website at https://www.gao.gov.

If you or your staff have any questions about this report, please contact me at emreyarrasm@gao.gov. Contact points for our Offices of Congressional Relations and Media Relations may be found on the last page of this report. GAO staff who made key contributions to this report are listed in appendix II.

Melissa Emrey-Arras, Director

Education, Workforce, and Income Security Issues

Melissa Emrey-Arras, emreyarrasm@gao.gov

In addition to the contact above, the following staff made key contributions to this report: Debra Prescott (Assistant Director). Additional assistance was provided by Elizabeth Calderon, William Colvin, Justin Gordinas, Serena Lo, Abigail Loxton, Mimi Nguyen, Jessica Orr, Julie Phipps, Almeta Spencer, and Adam Wendel.

The Government Accountability Office, the audit, evaluation, and investigative arm of Congress, exists to support Congress in meeting its constitutional responsibilities and to help improve the performance and accountability of the federal government for the American people. GAO examines the use of public funds; evaluates federal programs and policies; and provides analyses, recommendations, and other assistance to help Congress make informed oversight, policy, and funding decisions. GAO’s commitment to good government is reflected in its core values of accountability, integrity, and reliability.

Obtaining Copies of GAO Reports and Testimony

The fastest and easiest way to obtain copies of GAO documents at no cost is through our website. Each weekday afternoon, GAO posts on its website newly released reports, testimony, and correspondence. You can also subscribe to GAO’s email updates to receive notification of newly posted products.

Order by Phone

The price of each GAO publication reflects GAO’s actual cost of production and distribution and depends on the number of pages in the publication and whether the publication is printed in color or black and white. Pricing and ordering information is posted on GAO’s website, https://www.gao.gov/ordering.htm.

Place orders by calling (202) 512-6000, toll free (866) 801-7077,

or

TDD (202) 512-2537.

Orders may be paid for using American Express, Discover Card, MasterCard, Visa, check, or money order. Call for additional information.

Connect with GAO

Connect with GAO on X,

LinkedIn, Instagram, and YouTube.

Subscribe to our Email Updates. Listen to our Podcasts.

Visit GAO on the web at https://www.gao.gov.

To Report Fraud, Waste, and Abuse in Federal Programs

Contact FraudNet:

Website: https://www.gao.gov/about/what-gao-does/fraudnet

Automated answering system: (800) 424-5454

Media Relations

Sarah Kaczmarek, Managing Director, Media@gao.gov

Congressional Relations

David A. Powner, Acting Managing Director, CongRel@gao.gov

General Inquiries

[1]GAO, Department of Education: Full Costs and Savings Estimate Needed for Reduction-in-Force and Restructuring of the Office for Civil Rights, GAO-26-108320 (Washington, D.C.: Jan. 29, 2026).

[2]GAO, Federal Student Loans: Further Actions Needed to Implement Recommendations on Oversight of Loan Servicers, GAO‑18‑587R (Washington, D.C.: July 27, 2018); Federal Student Loans: Education Could Improve Direct Loan Program Customer Service and Oversight, GAO‑16‑523 (Washington, D.C.: May 16, 2016); and Federal Student Loans: Key Weaknesses Limit Education’s Management of Contractors, GAO‑16‑196T (Washington, D.C.: Nov. 18, 2015).

[3]Department of Education, Fiscal Year 2023 Agency Financial Report (Washington, D.C.: Nov. 16, 2023) and Fiscal Year 2024 Agency Financial Report (Washington, D.C.: Nov. 14, 2024).

[4]Pub. L. No. 105-244, tit. I, § 101(a), 112 Stat. 1581, 1604-05 (codified as amended at 20 U.S.C. § 1018). Performance-based organizations are intended to be business-like, results-driven organizations that have clear objectives and measurable goals designed to improve an agency's performance and transparency.

[5]Specifically, FSA is statutorily responsible for the administrative, accounting, and financial management functions for federal student aid programs authorized under Title IV of the Higher Education Act of 1965, as amended. FSA’s specific statutory functions are outlined in 20 U.S.C. § 1018(b)(2).

[6]Education’s portfolio of student loans included $1.53 trillion in William D. Ford Federal Direct Loans and $79 billion in Federal Family Education Loans as of September 2025.

[7]FSA refers to call quality as “interaction quality.” These performance standards are referred to as “service level agreements” in the USDS contract.

[8]According to the USDS contract, in the event a servicer consecutively fails to meet a given performance standard for at least two periods, the financial penalty on a servicer increases by 50 percent for each additional failure.

[9]An Act to provide for reconciliation pursuant to title II of H. Con. Res. 14, Pub. L. No. 119-21, § 82001, 139 Stat. 72, 337-48 (2025) (hereinafter OBBBA).

[10]The eliminated income-driven repayment plans include the Income-Contingent Repayment plan and the Pay as You Earn plan. These plans will be closed to new borrowers who take out loans on or after July 1, 2026, and will close for current borrowers—those who take out loans before July 1, 2026—on July 1, 2028. In addition, in December 2025, Education announced a proposed joint settlement agreement that would end the Saving on a Valuable Education income-driven repayment plan and provide more than 7 million borrowers enrolled in the plan a limited time to select a new repayment plan. Payments on the Repayment Assistance Plan are tied to a borrower’s adjusted gross income, generally ranging from 1 to 10 percent depending on income, with forgiveness of remaining loan balances after 30 years of payments.

[11]In quarters 2 and 3 of fiscal year 2025, FSA continued to assess servicer performance for other metrics: call abandon rate, timeliness of completion of certain servicing tasks, and financial monitoring. In the first three quarters of fiscal year 2025, FSA assessed servicers on the customer satisfaction metric but did not penalize servicers who were unable to meet the performance standard. FSA officials said that it was more labor intensive to monitor the accuracy and call quality metrics than the other metrics, for which data collection is generally automated.

[12]FSA refers to the call quality metric as “interaction quality,” and FSA documentation states that FSA planned to review other types of servicer interactions with borrowers, such as emails and chats. However, at the time FSA stopped its reviews, it had only assessed quality for incoming calls to servicers. As such, we refer to this metric as “call quality.”

[13]While FSA implemented the USDS contract in April 2024, the start of the third quarter of fiscal year 2024, it waived assessments of accuracy and call quality for that quarter because its oversight processes for these metrics were not ready. As such, it assessed servicers’ performance on these two metrics in two quarters before discontinuing assessments in the second quarter of fiscal year 2025.

[14]As part of that quarter’s accuracy review of payment refunds, FSA found that one servicer had not cleared credit balances for about 90 percent of the borrowers in the sample within 45 days.

[15]Department of Education, Fiscal Year 2023 Agency Financial Report (Washington, D.C.: Nov. 16, 2023) and Fiscal Year 2024 Agency Financial Report (Washington, D.C.: Nov. 14, 2024).

[16]As of December 22, 2025, Education officials said the agency was exploring ways to automate oversight but had no specific plans or project time frames for doing so.

[17]Department of Education, Contract Monitoring for Program Officials, Departmental Directive ACSD-OFO-001 (Washington, D.C.: April 23, 2013; updated January 31, 2024).

[18]FAR 16.401.

[19]Office of Management and Budget, Office of Federal Procurement Policy, Appropriate Use of Incentive Contracts, Memorandum for chief acquisition officers and senior procurement executives (Washington, D.C.: Dec. 4, 2007). In addition, federal standards for internal control dictate that agencies should design appropriate oversight activities and effectively manage human capital in order to achieve mission-oriented results. See GAO, Standards for Internal Control in the Federal Government, GAO‑25‑107721 (Washington, D.C.: May 15, 2025).

[20]Department of Education, U.S. Department of Education Strategic Plan Fiscal Years 2022–2026 (Washington, D.C.: July 8, 2022).