Before the Subcommittee on Financial Services and General Government, Committee on Appropriations, House of Representatives

For Release on Delivery Expected at 10:00, a.m. ET

United States Government Accountability Office

A testimony before the Subcommittee on Financial Services and General Government, Committee on Appropriations, House of Representatives

Contact: David Marroni at MarroniD@gao.gov

What GAO Found

Many agencies rely on the General Services Administration (GSA) to manage facilities for them. The Federal Buildings Fund (Buildings Fund) was established for real property management and associated activities. GSA collects rent from tenant agencies; deposits it into the Buildings Fund; and uses that money for real property acquisition, operation, maintenance, and disposal. Through the appropriations process, Congress sets annual limits on how much of this funding GSA can obligate to various activities.

GAO’s work has highlighted the impact of uncertain funding on real property management:

· Capital projects. Obtaining upfront funding for large projects—such as constructing, purchasing, or renovating federal buildings—has been a challenge for federal agencies. Congressional spending limits require GSA to first use available funds to pay for other needs, including leasing, operations and maintenance, and debt costs, making funding for large capital projects less available and potentially costing more in the long run.

· Maintenance and repair. Agencies’ backlog of deferred maintenance and repairs has grown by billions of dollars in recent years due, in part, to funding constraints. Deferring maintenance can worsen the condition of agencies’ assets and lead to premature replacement, significantly increasing costs.

· Consolidation and disposal. Federal agencies have struggled to determine how much space they need to fulfill their missions and identify the funding to consolidate operations, reconfigure spaces, and prepare unneeded property for disposal. Funding uncertainty can result in missed opportunities to eliminate leases and consolidate agencies into federally owned space, costing the federal government hundreds of millions of dollars.

GAO has identified actions Congress and federal agencies could take to better manage real property and address funding-related challenges. For example:

· Disposal of underused buildings. GAO recommended that the Office of Management and Budget and GSA take steps to address challenges with federally underused space, including assisting agencies in monitoring building utilization and reducing underutilized space.

· Adopting alternative budgetary structures. GAO reported on different budgetary structures as options that could help Congress and agencies make more prudent fiscal decisions. For example, Congress could modify the Buildings Fund to exclude certain major renovations or grant tenant agencies the authority to manage buildings they occupy. GAO has identified issues Congress may wish to consider when granting additional budgetary authorities, including ensuring agencies have the necessary real property expertise.

Why GAO Did This Study

The federal government’s real property holdings are vast and diverse, costing billions annually to occupy, operate, and maintain. GAO designated federal real property as high risk in 2003 because of large amounts of underused property and the considerable difficulty agencies have faced in disposing of unneeded holdings. Historically, the Buildings Fund has not generated sufficient revenues to meet all real property needs.

This statement discusses: 1) the status of the Buildings Fund, 2) the impacts of funding uncertainty on federal real property management, and 3) some options to address funding challenges. This statement is primarily based on GAO’s prior work on the Buildings Fund and real property management, as well as updated information from GSA revenue and occupancy data, agency budget documents, GSA statements on its budget, and legislative proposals.

What GAO Recommends

We have made a number of recommendations to federal agencies to improve the management of federal real property and use existing funding more effectively, including on property disposal and the management of deferred maintenance and repair. Federal agencies have taken actions to address some of these recommendations, but additional action is needed to fully implement others.

Chairman Joyce, Ranking Member Hoyer, and Members of the Subcommittee:

I am pleased to be here today to discuss our work on the federal government’s management of its real property portfolio. The federal real property portfolio is large and vast, with federal agencies reporting almost 250,000 owned buildings.[1] Real property assets can require significant resources to construct, operate, and maintain over the course of their life cycle. The General Services Administration (GSA) is responsible for managing federal real property for many federal agencies, including providing workspace for more than 1 million federal employees. The Federal Buildings Fund (Buildings Fund) was established for real property management and associated activities.[2] GSA collects rent from tenant agencies; deposits it into the Buildings Fund; and uses that money to fund its real property acquisition, operation, maintenance, and disposal, subject to the appropriations process.

Since 2003, we have designated federal real property as a high-risk issue in need of reform, due to wide-ranging challenges, including the condition and underuse of federal buildings. Our work has also highlighted the impact of uncertain and limited funding on real property management.[3] Historically, the Buildings Fund has not generated sufficient revenues to meet all needs. We have reported that funding uncertainty has contributed to a variety of issues facing federal agencies, including challenges undertaking large construction and renovation projects, and relocating tenants and disposing of properties that agencies no longer need to meet their missions.

This statement discusses the status of the Buildings Fund, the impacts of funding uncertainty on federal real property management, and options to address funding challenges. This statement is primarily based on our prior work on the Buildings Fund and federal real property management. More detailed information on the objectives, scope, and methodology for that work can be found in the products referenced in this statement. In addition, for this statement we updated our prior work with information on sources of revenue for the Buildings Fund, tenant occupancy in GSA-owned buildings, GSA officials’ views on funding uncertainty, and agency requests for new budget authority. To do so, we reviewed GSA real property portfolio and budget documents for fiscal years 2024, 2025 and 2026, and government-wide occupancy data for fiscal year 2024.[4] We also reviewed GSA congressional testimony on its budget, and legislative proposals from the Office of Management and Budget (OMB), GSA, and the federal judiciary.[5] We provided GSA and the judiciary with a draft of this statement. GSA and the judiciary provided technical comments, which we incorporated as appropriate.

We conducted the work on which this statement is based in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

The Federal Buildings Fund

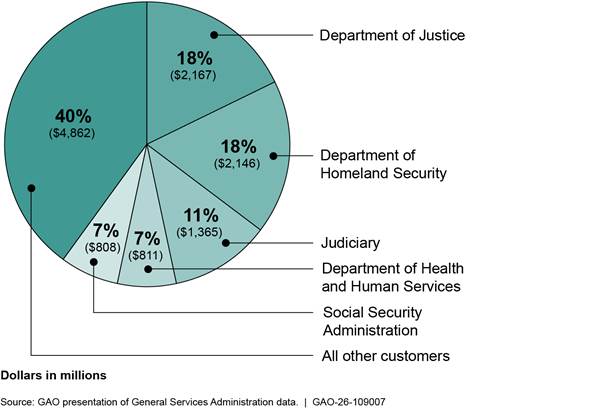

While some federal agencies have the authority to own facilities and receive federal appropriations to manage them, many pay rent to and rely on GSA to procure and manage facilities for them. Federal agencies that occupy property controlled by GSA pay rent into the Buildings Fund, which is GSA’s sole source of funds to manage those buildings. As of March 2026, the Buildings Fund supports about 8,100 buildings—including about 1,500 GSA-owned properties and about 6,600 GSA-leased properties.[6] Four federal agencies and the judiciary accounted for most of the revenue contributed to the Buildings Fund in fiscal year 2025 (see fig. 1).

Notes: The data presented are from GSA’s fiscal year 2025 Agency Financial Report. This public report describes how GSA used its resources for the year. Percentages for individual federal agencies do not add up to 100 percent, due to rounding.

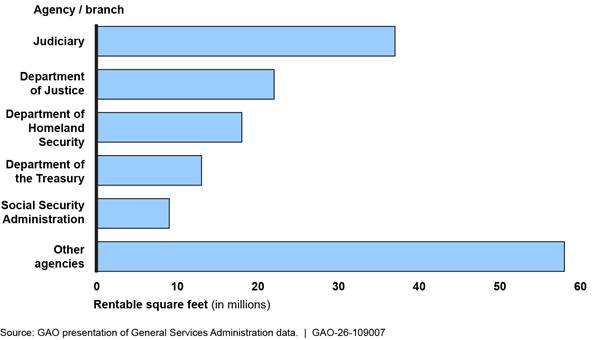

While a portion of revenues deposited into the Buildings Fund is used to pay for leases, those revenues do not increase the fund’s balances, since GSA passes these payments to private sector owners. As a result, the balance of the Buildings Fund is primarily driven by agency tenants in GSA’s federally owned space.[7] Figure 2 shows the tenant agencies occupying the most space in GSA-owned locations, as of fiscal year 2024, the most recent available data.

Figure 2: Top Five Tenant Agencies Occupying General Services Administration Owned Buildings, by Rentable Square Feet, as of Fiscal Year 2024

Notes: The data presented are from GSA’s fiscal year 2024 State of the Portfolio. This report provides an overview and relevant data for real property assets under GSA’s custody and control. According to GSA officials, these data are used to provide annual reports to Congress.

Congress exercises control over the Buildings Fund through the appropriations process that sets annual limits—which GSA refers to as Obligational Authority—on how much of the fund can be obligated for various activities, such as building construction and repairs. Each year, GSA’s congressional budget justification includes a request for New Obligational Authority. As part of annual appropriations legislation, GSA is provided authority to incur obligations and make expenditures from the Buildings Fund. GSA’s congressional budget justifications often closely mirror the rent it receives from tenant agencies, which may not reflect capital requirements. For fiscal year 2026, GSA requested $10.5 billion in New Obligational Authority, which is what it anticipates receiving in revenues and collections from its owned and leased properties for that year.

Building repairs and alterations, as well as construction and acquisition projects, that are expected to cost more than a specified dollar threshold—referred to as prospectus-level projects—must be submitted to certain congressional committees for authorization and funding.[8] GSA, in its annual budget justification, with approval from OMB, provides Congress with a prospectus for each construction and acquisition project and repair and alteration project estimated to exceed the prospectus-level threshold. The prospectus includes information on the size, cost, location, and other features of the proposed work; a justification for proceeding with the work; and an economic analysis of the alternatives to the requested repairs and alterations.

Since 2011, as part of the appropriations process, Congress has authorized GSA to spend less from the Buildings Fund than the rent it has received from tenant agencies. According to GSA’s fiscal year 2026 congressional budget justification, Congress did not provide Obligational Authority for approximately $14.9 billion in revenue and collections from the Buildings Fund that GSA requested from fiscal year 2011 through fiscal year 2025. Most of the difference between funds requested by GSA—which generally aligned with rents collected—and Obligational Authority appropriated by Congress was for two types of projects: (1) construction and acquisition and (2) repairs and alterations. As of the end of fiscal year 2025, there is a $10.6 billion unavailable balance in the Buildings Fund.[9]

Funding Impacts on Federal Real Property Management

For more than 20 years, we have designated federal real property as a high-risk issue in need of reform due to challenges related to underused buildings, data reliability, facility security, and building condition.[10] Our work has also highlighted the impact of uncertain funding on real property management, including on large capital projects, a large and growing maintenance backlog, and the ability of agencies to manage and dispose of underutilized facilities. We discuss recommendations we have made to address these challenges later in this statement.

· Capital projects. As we reported in September 2021, obtaining upfront funding for large projects—such as constructing, purchasing, or renovating federal buildings—has been a challenge for federal agencies.[11] Specifically, obligation limits on the Buildings Fund have particularly constrained real property funding for repairs, alterations, and new construction because, according to GSA officials, available funds are first used to pay leasing, operations and maintenance, and debt costs. As a result, funding for large capital projects is less available, potentially costing more for such projects in the long run.

· Maintenance and repair. As we reported in November 2023, according to agency officials, funding constraints have contributed to tens of billions of dollars in additional deferred maintenance and repair backlogs.[12] Agency officials cited large and growing costs associated with maintaining old and deteriorating assets, including for GSA buildings which, on average, are more than 50 years old and are beyond their useful lives. In December 2025, GSA estimated that deferred maintenance and repair costs for its own properties have risen to about $26 billion.[13] Deferring maintenance can worsen the condition of agencies’ assets and lead to premature replacement, which can be significantly more costly than the repairs, had they not been delayed. For example, according to GSA, 13 out of 17 major repair and alteration projects for GSA buildings included in GSA’s fiscal year 2024 congressional budget justification were submitted in prior years.[14] Collectively, GSA estimated that those 13 projects combined would cost $300 million more in fiscal year 2024 than in the years in which they were originally submitted.

· Consolidation and disposal. Uncertain upfront funding can hinder agencies’ willingness and ability to pursue space reduction efforts. We have previously reported on the need for upfront funding to consolidate federal agency operations, reconfigure spaces, and prepare unneeded properties for disposal.[15] In our prior work, agency officials often cited limited access to such funds as a challenge to participate in federal space reduction efforts, such as those created under the Federal Assets Sale and Transfer Act of 2016 (FASTA). GSA has reported that uncertain funding has resulted in missed opportunities to eliminate leases and consolidate into federally owned space, costing the federal government hundreds of millions of dollars in additional lease payments.[16]

Options to Address Federal Real Property Funding Challenges

GAO and others have proposed a variety of actions that Congress and federal agencies could take to better manage federal real property and address funding-related challenges we discussed above. These proposals include disposing of underused buildings, considering alternative funding mechanisms and budget structures, and changing the prospectus process.

· Disposal of underused buildings. In April 2025, we testified that reducing the federal government’s real property holdings could generate substantial cost savings.[17] Federal agencies have long struggled to determine how much space they need to fulfill their missions and to dispose of underused space—challenges exacerbated by increased telework during and following the COVID-19 pandemic. Retaining underused space costs millions of dollars and is one of the main reasons that federal real property management has remained on our High Risk List since 2003.

Congress has taken several actions to address underused buildings. Specifically, the Utilizing Space Efficiently and Improving Technologies (USE IT) Act, enacted in January 2025, requires agencies to measure building utilization and GSA and OMB to take steps to reduce underutilized space for tenant agencies that fail to meet the minimum utilization threshold two years in a row.[18] Agencies anticipate providing Congress with the first annual report on building utilization by the end of March 2026.[19] In addition, FASTA established a temporary process to help the federal government identify and dispose of unneeded federal real property.[20] In February 2026, the Consolidated Appropriations Act, 2026 appropriated $143 million for FASTA-related disposals.[21] As we have previously recommended, OMB and GSA could take additional steps related to these acts, including continuing to assist agencies in monitoring utilization; reducing tenant agencies’ underutilized space, as directed by the USE IT Act; and identifying and applying lessons learned from the FASTA process to improve future disposal efforts.[22]

· Alternate funding mechanisms. In March 2014, we reported on a variety of funding mechanisms federal agencies can use as alternatives to full upfront funding to meet real property needs.[23] Funding mechanisms leverage both monetary resources, such as retained fees, and nonmonetary resources (e.g., property exchanged in a land swap). For example, one option may be for agencies to enter into an enhanced use lease in which a portion of a federal property is leased out to the private sector, state, or local entity in exchange for payment or services, such as renovations.[24]

Our work has identified considerations when using alternative funding mechanisms:[25]

· Projects with alternative funding mechanisms involve multiple forms of risk—both implicit and explicit—that must be shared between the agency and any partner or stakeholder. Project decisions should reflect both the likely risk and the organization’s tolerance for risk.

· When working with a partner, it is important to actively manage the relationship. Formalizing collaborations between the partners, including documenting dispute resolution processes, can enable productive partner interactions.

· The availability of an appropriate partner—one that brings complementary resources, skills, and financial capacities—and the geographic location of the property may affect the use and success of an alternative funding mechanism.

· Alternative budgetary structures. In March 2014, we also reported on alternative budgetary structures that could change incentives for agencies and, therefore, help Congress and agencies make more prudent, long-term fiscal decisions.[26] These alternatives could also promote more complete consideration of the full costs of projects and associated returns over time as well as provide agencies with greater flexibility to manage their real property needs. Such alternatives could include changing existing or introducing new account structures to fund real property projects. For example, Congress could modify the Buildings Fund by (1) making the full balance available or (2) adjusting the pricing structure to exclude certain major renovations (e.g., provide direct appropriations to tenant agencies for certain renovation or construction projects).[27]

Federal agencies and the judiciary have made recent proposals for Congress to grant budgetary authorities for managing real property. For example:

· OMB and GSA have sought enactment of a Federal Capital Revolving Fund, which would be administered by GSA and could provide upfront funding for certain capital projects. GSA’s fiscal year 2026 congressional budget justification included a $1 billion request for this revolving fund to construct and acquire spaces to help GSA consolidate agencies into a smaller real estate footprint. We have previously reported on the concept of a revolving fund with borrowing authority (e.g., a capital acquisition fund) or a dedicated fund with permanent, indefinite budget authority and noted that such a fund could enable the recognition of costs and returns associated with complex real property projects upfront and over time.[28]

· In February 2026, the judiciary sought authority to take responsibility from GSA for directly managing certain federally owned and leased properties deemed critical for carrying out its mission. In making this request, the judiciary indicated that GSA had identified $8.3 billion in long-standing maintenance and repair issues and related health and safety concerns.[29] Based on our review of this proposal, such authority, if granted, would not provide additional funds. Instead, it would allow Congress to appropriate funds directly to the judiciary to manage their buildings.

When considering these kinds of options, we have highlighted the inherent tradeoffs in budgeting and noted that while alternative budgeting structures could increase flexibility for agencies in addressing their real property needs, they also could result in less fiscal control and oversight for Congress. Such changes may also affect the Buildings Fund or spending for other discretionary programs competing for mission-critical resources. For example, authorizing additional real property funding mechanisms could divert needed revenue away from the Buildings Fund, eroding its balances, cash flow, and operations funding that GSA must use to fund its portfolio needs. We have identified questions that Congress may wish to consider when contemplating additional authorities, including ensuring that agencies have the necessary expertise to implement and oversee real property management.[30]

· Prospectus process. In January 2022, we reported that, while the prospectus process provides Congress with important oversight information, it can make it challenging for GSA to effectively manage its assets and could result in increased project costs.[31] Since 1988, the GSA Administrator has had the statutory authority to annually adjust the prospectus threshold but is limited to the percentage change in construction costs during the previous calendar year.[32] According to GSA officials, the prospectus threshold for certain repair and alteration, construction, and lease projects limits GSA’s flexibility in managing its portfolio. Officials characterized the threshold as relatively low, in light of the average costs of such projects, so that projects for ordinary maintenance and repairs—particularly in large buildings or complexes—must go through the prospectus process. As a result, GSA is required to submit a large number of projects which we found take, on average, 19 to 24 months from when the prospectus is submitted until the projects are approved by Congress.[33] These timeframes can exacerbate management challenges, result in increased project costs, or require GSA to pursue interim measures, such as entering into a more costly lease extension.

In 2024, GSA proposed raising the prospectus threshold for capital and lease projects from around $4 million to $10 million.[34] Our work found that such a change could have reduced the number of projects submitted for prospectus approval from fiscal year 2014 through fiscal year 2020 by approximately 20 percent.[35] As of February 2026, Congress has not adopted GSA’s proposal and the fiscal year 2026 prospectus threshold for construction and lease projects is $3.961 million.[36]

Chairman Joyce, Ranking Member Hoyer, and Members of the Subcommittee, this completes my prepared statement. I would be pleased to respond to any questions that you may have at this time.

GAO Contact and Staff Acknowledgments

If you or your staff have any questions about this testimony, please contact David Marroni, Director, Physical Infrastructure, at MarroniD@gao.gov. Contact points for our Offices of Congressional Relations and Media Relations may be found on the last page of this statement. GAO staff who made key contributions to this testimony are Matthew Cook (Assistant Director), Michael Sweet (Analyst-in-Charge), and Ben Theuma. In addition, Emily Crofford, Keith Cunningham, Alexandra Edwards, Terence Lam, Kathleen Padulchick, Alicia Wilson, and Elizabeth Wood provided key support.

This is a work of the U.S. government and is not subject to copyright protection in the United States. The published product may be reproduced and distributed in its entirety without further permission from GAO. However, because this work may contain copyrighted images or other material, permission from the copyright holder may be necessary if you wish to reproduce this material separately.

The Government Accountability Office, the audit, evaluation, and investigative arm of Congress, exists to support Congress in meeting its constitutional responsibilities and to help improve the performance and accountability of the federal government for the American people. GAO examines the use of public funds; evaluates federal programs and policies; and provides analyses, recommendations, and other assistance to help Congress make informed oversight, policy, and funding decisions. GAO’s commitment to good government is reflected in its core values of accountability, integrity, and reliability.

Obtaining Copies of GAO Reports and Testimony

The fastest and easiest way to obtain copies of GAO documents at no cost is through our website. Each weekday afternoon, GAO posts on its website newly released reports, testimony, and correspondence. You can also subscribe to GAO’s email updates to receive notification of newly posted products.

Order by Phone

The price of each GAO publication reflects GAO’s actual cost of production and distribution and depends on the number of pages in the publication and whether the publication is printed in color or black and white. Pricing and ordering information is posted on GAO’s website, https://www.gao.gov/ordering.htm.

Place orders by calling (202) 512-6000, toll free (866) 801-7077,

or

TDD (202) 512-2537.

Orders may be paid for using American Express, Discover Card, MasterCard, Visa, check, or money order. Call for additional information.

Connect with GAO

Connect with GAO on X,

LinkedIn, Instagram, and YouTube.

Subscribe to our Email Updates. Listen to our Podcasts.

Visit GAO on the web at https://www.gao.gov.

To Report Fraud, Waste, and Abuse in Federal Programs

Contact FraudNet:

Website: https://www.gao.gov/about/what-gao-does/fraudnet

Automated answering system: (800) 424-5454

Media Relations

Sarah Kaczmarek, Managing Director, Media@gao.gov

Congressional Relations

David A. Powner, Acting Managing Director, CongRel@gao.gov

General Inquiries

[1]Reported data are as of fiscal year 2024, the most recent year for which government-wide data are available. These figures are based on data in the General Services Administration’s Federal Real Property Profile (FRPP) Management dataset. FRPP is a government-wide database the General Services Administration uses to track the federal government’s real property assets, which contains data submitted annually by agencies. Assets listed in FRPP include facilities owned by the General Services Administration as well as those owned by other federal agencies.

[2]See 40 U.S.C. § 592.

[3]GAO, High-Risk Series: Heightened Attention Could Save Billions More and Improve Government Efficiency and Effectiveness, GAO‑25‑107743 (Washington, D.C.: Feb 25, 2025).

[4]We used GSA’s fiscal year 2025 Agency Financial Report to present data on tenant agency contributions to the Building Fund. This public report describes how GSA used its resources for the year. We also used data from GSA’s fiscal year 2024 State of the Portfolio to present data on the amount of rentable space tenant agencies occupy in GSA-owned buildings. The report provides an overview and relevant data for real property assets under GSA’s custody and control. According to GSA officials, these data are used to provide annual reports to Congress.

[5]The federal judiciary consists of a system of courts that is responsible for ensuring the administration of justice in the United States. Within the judiciary, the Administrative Office of the U.S. Courts provides a broad range of services including administrative and program support to federal courts and federal defender organizations. For the purposes of this statement, we refer to the judiciary when describing those functions.

[6]These figures are based on data in GSA’s Inventory of Owned and Leased Properties database, which contains public data on GSA’s owned and leased real property assets. This database excludes assets for security reasons, as well as assets that are decommissioned or deemed excess, i.e., no longer needed to meet mission requirements.

[7]Deposits to the Buildings Fund also include charges for furnishing space and services, reimbursement for special services, and receipts from carriers and others for loss of, or damage to, property belonging to the Buildings Fund. 40 U.S.C. § 592(b).

[8]For capital and lease projects with an estimated cost above a certain dollar threshold, GSA must submit a proposal (prospectus) to its congressional-authorizing committees—the House Committee on Transportation and Infrastructure and the Senate Committee on Environment and Public Works. 40 U.S.C. § 3307. Prospectus-level projects involve major work or acquisitions that are estimated to cost more than a statutorily prescribed amount ($3.961 million for fiscal year 2026 construction projects), which GSA’s Administrator is authorized to adjust annually to reflect a percentage increase or decrease in construction costs during the prior calendar year.

[9]GSA officials told us that the unavailable balance in the Buildings Fund can fluctuate for a number of reasons, including (1) revenue divergence (rent estimated to be collected does not match the actual amount), (2) instances in which GSA requests a net positive budget, (3) rescissions or direct appropriations, and (4) rent credits given to agencies.

[10]GAO‑25‑107743. Our prior work has found that the federal government maintains large amounts of underused property and faces billions of dollars in annual operations and deferred maintenance costs. For example, we reported that the needed capital for deferred repairs across federal agencies properties increased from $170 billion to $370 billion from fiscal year 2017 through fiscal year 2024.

[11]GAO, Capital Fund Proposal: Upfront Funding Could Benefit Some Projects, but Other Potential Effects Not Clearly Identified, GAO‑21‑215 (Washington, D.C.: Sept. 10, 2021).

[12]GAO, Federal Real Property: Agencies Should Provide More Information about Increases in Deferred Maintenance and Repair, GAO‑24‑105485 (Washington, D.C.: Nov. 16, 2023).

[13]Cutting Costs, Adding Value: The Future of Federal Property, Before the House Committee on Transportation and Infrastructure, Subcommittee on Economic Development, Public Buildings and Emergency Management, 119th Cong. (2025) (statement of Andrew Heller, Acting Commissioner of the Public Buildings Service of the General Services Administration).

[14]Oversight of the Public Buildings Service, General Services Administration, Before the Senate Committee on Environment and Public Works, Subcommittee on Transportation and Infrastructure, 118th Cong. (2024) (statement of Elliot Doomes, Commissioner of the Public Buildings Service of the General Services Administration).

[15]GAO, Federal Real Property: Agencies Need New Benchmarks to Measure and Shed Underutilized Space, GAO‑24‑107006 (Washington, D.C.: Oct. 26, 2023); Federal Real Property: GSA Should Leverage Lessons Learned from New Sale and Transfer Process, GAO‑23‑104815 (Washington, D.C.: Oct. 7, 2022); GAO‑21‑215; and Federal Real Property: Additional Documentation of Decision Making Could Improve Transparency of New Disposal Process, GAO‑21‑233 (Washington, D.C.: Jan. 29, 2021).

[16]Doomes, testimony on Oversight of the Public Buildings Service, General Services Administration.

[17]GAO, Federal Real Property: Reducing the Government’s Holding Could Generate Substantial Savings, GAO‑25‑108159 (Washington, D.C.: Apr. 8, 2025).

[18]Thomas R. Carper Water Resources Development Act, Pub. L. No. 118-272 § 2302, 138 Stat. 2992, 3218 (2025). The USE IT Act required agencies to provide the first required report on building utilization by January 2026.

[19]Due to the fall 2025 lapse in appropriations, GSA informed Congress those reports would be delayed until March 31, 2026. Heller, testimony on Cutting Costs, Adding Value: The Future of Federal Property.

[20]Federal Assets Sale and Transfer Act of 2016, Pub. L. No. 114-287, 130 Stat. 1463 (codified as amended 40 U.S.C. § 1303 note).

[21]Pub. L. No. 119-75, tit. V (2026). GSA’s fiscal year 2026 congressional budget justification included approximately $558 million to help reconfigure existing space and to consolidate and dispose of unneeded space, including $193 million to carry out disposals under FASTA and $365 million for a new program to optimize space configurations.

[22]In October 2023, we recommended that OMB develop and use benchmarks for measuring building utilization (see GAO‑24‑107006). OMB agreed with our recommendation, and the USE IT Act established such a benchmark. To fully address our recommendation OMB should continue to assist federal agencies to implement data reporting requirements included in the Act. In October 2022, we recommended that GSA work with stakeholders to develop a process to collect, share, and apply lessons learned from the implementation of FASTA (see GAO‑23‑104815). GSA agreed with our recommendation and has compiled an initial list of lessons learned for the first round of disposal recommendations. While this is a positive step, to fully address our recommendation GSA should develop lessons learned for the remaining FASTA recommendation rounds.

[23]GAO, Capital Financing: Alternative Approaches to Budgeting for Federal Real Property, GAO‑14‑239 (Washington, D.C.: Mar. 12, 2014). Alternative funding mechanisms are not universally available to all agencies. Moreover, even within an agency, legal authorities may differ across agency components.

[24]We have reported on agency reported benefits of enhanced use leases, including additional cash rent revenue, but also found that some agencies did not attribute all costs of enhanced use lease costs to their programs in a consistent, appropriate manner. See GAO, Federal Real Property: Improved Cost Reporting Would Help Decision Makers Weigh the Benefits of Enhanced Use Leasing, GAO‑13‑14 (Washington, D.C.: Dec. 19, 2012).

[27]See GAO‑14‑239 for additional details on these options.

[28]See GAO‑14‑239. Borrowing authority is authority granted to a federal entity to borrow funds, then obligate against amounts borrowed. Generally, agencies with borrowing authority are expected to repay the borrowing out of future resources. Permanent, indefinite budget authority refers to budget authority for an unspecified amount made available as the result of previously enacted legislation and is available without further legislative action. Such budget authority can be the result of substantive legislation or appropriation acts.

[29]U.S. Courts, Judiciary Says Courthouses Are in Crisis, Seeks Real Property Authority (Feb. 24, 2026), https://www.uscourts.gov/data-news/judiciary-news/2026/02/24/judiciary-says-courthouses-are-crisis-seeks-real-property-authority.

[31]GAO, Federal Real Property: GSA Should Fully Assess Its Prospectus Process and Communicate Results to Its Authorizing Committees, GAO‑22‑104639 (Washington, D.C.: Jan. 21, 2022). We recommended that GSA fully assess the prospectus process, implement potential improvements to the process identified through the assessment, and communicate its assessment to Congress. We closed these recommendations as implemented after GSA completed an assessment and provided it to its congressional authorizing committees.

[32]The Public Buildings Amendments of 1988 raised the statutory prospectus limit to $1,500,000 and authorized the GSA Administrator to make this annual adjustment and provided that the Department of Commerce’s composite index of construction costs determines the percentage change in the previous calendar year’s construction costs. Pub. L. No. 100-678, §§ 2, 4, 102 Stat. 4049, 4050 (codified as amended at 40 U.S.C. § 3307(a), (h)). However, the Department of Commerce no longer publishes this table. In 2005, GSA began using the Building Cost Index published by McGraw-Hill’s Engineering News Record as an alternative index, at the recommendation of Commerce staff. In January 2021, GSA notified its committees that to expand the pool of information it uses to set the threshold, GSA would use the Marshall and Swift Quarterly Index for construction and repair and alterations projects and leasing trend data reported by REIS, CoStar, and CBRE for lease projects.

[34]General Services Administration, FY 2025 Congressional Justification (Mar. 11, 2024).

[36]Proposed legislation, if enacted, would temporarily increase the construction and lease threshold to $10 million. Prospectus Modernization Act of 2026, S. 3789, 119th Cong. (2026).