Before House Committee on Financial Services, Subcommittee on Housing and Insurance

For Release on Delivery Expected at 2:00 p.m. ET

United States Government Accountability Office

A testimony before the House Committee on Financial Services, Subcommittee on Housing and Insurance

Contact: Alicia Puente Cackley at CackleyA@gao.gov

What GAO Found

The Federal Emergency Management Agency (FEMA) administers three primary programs that mitigate flood risk for properties insured by the National Flood Insurance Program (NFIP). A small number of these properties—known as repetitive loss properties, which have flooded and received claim payments multiple times—contribute to the program’s fiscal challenges. According to FEMA, unmitigated repetitive loss properties make up about 2.5 percent of NFIP policies, but 48 percent of NFIP claims by dollar value have been paid to properties with two or more losses.

From 1989 through 2025, 77 percent of the properties FEMA mitigated were funded by the Hazard Mitigation Grant Program. FEMA supports four mitigation strategies—acquisition, elevation, relocation, and floodproofing. FEMA has mitigated flood risk primarily through acquisitions, which accounted for 69,415 (about 72.5 percent) of the properties mitigated from 1989 through 2025.

While acquisitions offer benefits, the process faces significant challenges that can discourage communities and homeowners from participating. These challenges include a lengthy and complex process, limited state and community capacity, and financial constraints.

NFIP represents a fiscal exposure to the federal government because FEMA is statutorily required to charge premium rates that do not fully reflect flood risk. Although mitigation reduces flood losses, it also requires substantial investment. Without addressing mitigation challenges, the number of repetitive loss properties will continue to grow, increasing costs to NFIP policyholders and federal taxpayers. One way to address the program’s fiscal exposure is to target mitigation efforts to those properties contributing most to the premium shortfall. These may disproportionately include repetitive loss properties, which face greater flood risk and higher full-risk premiums. By reducing risk, mitigation could also address affordability in the long term.

Why GAO Did This Study

Flooding is the most expensive natural disaster in the U.S., and in 2024, it caused over $8 billion in damages, according to FEMA. Congress created NFIP in 1968 to protect homeowners from flood losses, minimize property exposure to flood damage, and limit taxpayers' fiscal exposure to flood losses. However, the program faces multiple serious and longstanding challenges, primarily because it has two competing goals: keeping flood insurance affordable while maintaining the program’s fiscal solvency.

This statement discusses (1) the role of mitigation in addressing NFIP’s fiscal exposure from repetitive loss properties and (2) how targeting mitigation efforts could reduce NFIP’s exposure and address affordability.

This statement is based on GAO work issued in 2017–2023, including GAO-17-425, GAO-20-508, GAO-22-106037, and GAO-23-105977. Detailed information on the objectives, scope, and methodology can be found within each report.

What GAO Recommends

GAO has made nine recommendations to FEMA and eight to Congress related to improving the mitigation process, addressing challenges in property acquisitions, and reducing NFIP’s fiscal exposure while addressing affordability for policyholders. As of March 2026, FEMA has implemented four of these recommendations.

Chairman Flood, Ranking Member Cleaver, and Members of the Subcommittee:

Thank you for the opportunity to discuss our work on the National Flood Insurance Program (NFIP) and flood mitigation strategies, including those to address repetitive loss properties.

Flooding is the most expensive type of natural disaster in the United States, and in 2024, it caused over $8 billion in damages, according to the Federal Emergency Management Agency (FEMA). Congress created NFIP in 1968 to protect homeowners from flood losses, reduce property exposure to flood damage, and limit taxpayers’ fiscal exposure. FEMA administers the program. However, NFIP faces multiple serious and longstanding challenges, primarily because NFIP has two competing goals: keep flood insurance affordable and keep the program fiscally solvent.

Major flood events since 2005 and an emphasis on affordability have left the program with insufficient premium revenue to pay claims. As a result, some of the financial burden of flood risk has shifted from property owners to taxpayers. FEMA administers several mitigation grant programs that can reduce flood risk for NFIP-insured properties. A relatively small share of these properties, known as repetitive loss properties, have flooded and received payment for claims multiple times. These properties contribute to the program’s fiscal challenges. Since 2005, FEMA has had to borrow about $38.5 billion from the Department of the Treasury.[1]

For these reasons, we placed NFIP on our High-Risk List in 2006.[2] Since then, we have developed a body of work on NFIP, in which we have outlined a roadmap for comprehensive reform and identified specific actions Congress and FEMA could take and ways FEMA could improve its mitigation programs.[3] In April 2023, FEMA implemented a new pricing approach that more closely aligns premiums with risks. However, comprehensive reform is still needed. The program’s current authorization is set to expire on September 30, 2026.

In this statement, I will discuss (1) the role of mitigation in addressing NFIP’s fiscal exposure from repetitive loss properties and (2) how targeting mitigation efforts could reduce NFIP’s exposure and address affordability.

This statement draws primarily on our body of work on NFIP issued from April 2017 to July 2023. For those reports, we reviewed FEMA documentation, interviewed FEMA officials and relevant stakeholders, reviewed literature and legislation, and analyzed FEMA data. More detailed information on the objectives, scope, and methodology for that work can be found in the individual reports we cite.[4] We also updated selected facts and figures from those reports.

We conducted the work on which this statement is based in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

Mitigation Improvements Could Help Address the Increasing Fiscal Exposure from Repetitive Loss Properties

FEMA Administers Three Programs to Mitigate Flood Risk

FEMA funds flood mitigation through three primary programs:

· Hazard Mitigation Grant Program. This program may be authorized as part of a presidential major disaster declaration and helps communities implement various hazard mitigation measures to improve community resilience to future disasters. A formula based on the total federal contribution for the presidential major disaster declaration determines how much funding is available to the program.

· Flood Mitigation Assistance. Unlike FEMA’s other mitigation grant programs, this program funds projects and planning that reduce or eliminate long-term flood risk to structures insured under NFIP. It focuses particularly on NFIP-insured repetitive loss properties. Congress provides appropriations for these grants, and FEMA awards them on a nationally competitive basis.

· Building Resilient Infrastructure and Communities. This competitive annual grant program is designed to support a range of hazard mitigation activities. For example, recipients could build capability and capacity to reduce disaster risks, implement cost-effective hazard mitigation projects designed to increase resilience and public safety, and cover management costs associated with mitigation activities. The program succeeded the Pre-Disaster Mitigation program, which FEMA administered through fiscal year 2019. Congress established it in the Disaster Recovery Reform Act of 2018, and FEMA began awarding funding for fiscal year 2020. In April 2025, FEMA announced it was ending the program. However, in December 2025, a court ordered FEMA to reverse its termination of the program and prohibited the agency from taking any further actions to cancel or suspend the program.[5]

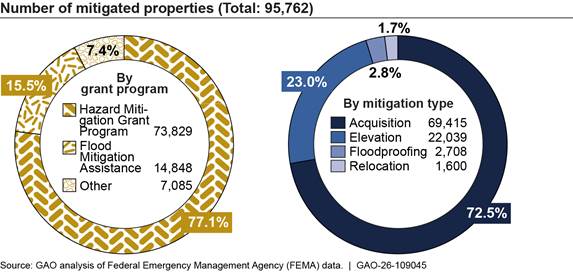

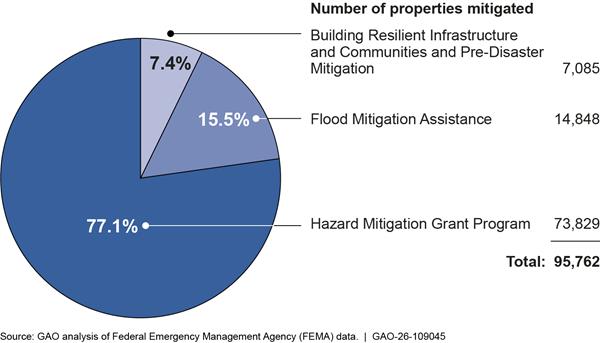

About 77 percent of property mitigations from 1989 through 2025 were funded by the Hazard Mitigation Grant Program (see fig. 1).[6]

Figure 1: FEMA Hazard Mitigation Assistance, Number of Properties Mitigated by Program, Fiscal Years 1989–2025

Note: For analyses by grant program area, we treated projects funded through the Severe Repetitive Loss and Repetitive Flood Claims grant programs as being part of the Flood Mitigation Assistance program and projects funded through the Legislative Pre-Disaster Mitigation program as being part of the Pre-Disaster Mitigation program. For data on the number of flood-mitigated properties, we used the final number of properties mitigated by a project.

FEMA Has Primarily Mitigated Flood Risk Using Acquisitions

At the individual property level, FEMA supports four primary flood mitigation strategies:

· Acquisition: A state or local government purchases land and structures that flooded or are at risk of flooding from willing sellers and demolishes the structures.

· Elevation: A state or local government pays to raise a structure so that the lowest occupied floor is at or above the area’s base flood elevation.[7]

· Relocation: A state or local government uses FEMA funding to help purchase land from willing sellers and assist the property owners with relocating the structure.

· Floodproofing: A state or local government pays to modify a structure to reduce flood damage. This can involve sealing the structure to keep floodwater out (dry floodproofing) or allowing water to enter and exit with minimal damage (wet floodproofing).

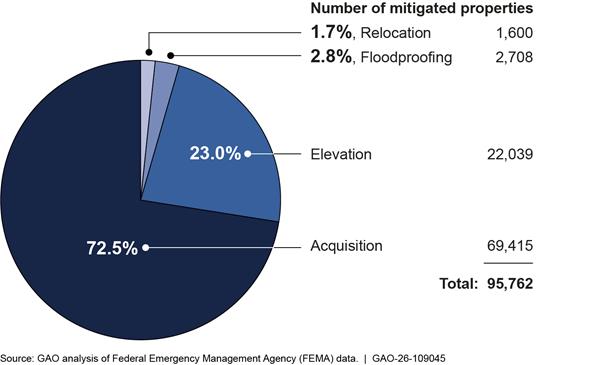

Since 1989, FEMA has mitigated flood risk at the property level primarily through acquisitions (see fig. 2). Acquisitions accounted for 69,415 (about 72.5 percent) of the 95,762 properties FEMA mitigated from 1989 through 2025. Elevation accounted for another 22,039 properties (about 23 percent).[8]

As we reported in June 2020, the average federal cost per property for mitigation was $136,000 for acquisitions and $107,000 for elevations, according to 2008–2014 FEMA data. As we have previously reported, according to FEMA officials and most stakeholders we interviewed, acquisition is particularly beneficial for communities that have experienced repeated deep or extensive flood damage and face high future risk of flooding. Acquired properties are converted to open space in perpetuity. The costs of acquisition and elevation are similar, but acquisition eliminates flood risk while elevation only reduces it. Elevation, however, may be the better choice in higher-cost areas or where homeowners do not want to leave their homes.

Repetitive Loss Properties Represent a Growing Financial Challenge for NFIP

Repetitive loss properties are NFIP-insured properties that have suffered multiple flood losses of a certain magnitude over a certain period.[9] These properties create significant challenges for the program.

They drive a large share of claims. In 2023, we reported that unmitigated repetitive loss properties make up about 2.5 percent of NFIP policies, but such policies have accounted for a disproportionate share of claims, according to FEMA. For example, as of December 2021, 48 percent of NFIP claims by dollar value had been paid to properties with two or more losses.[10]

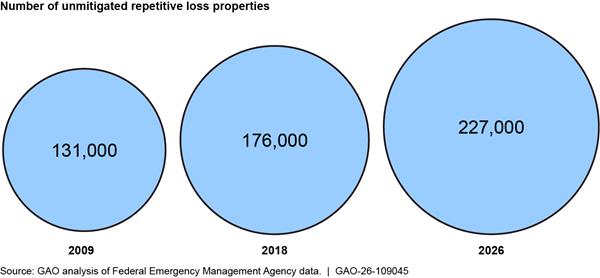

The number of unmitigated repetitive loss properties has increased. Despite FEMA’s mitigation efforts, the number grew by about 73 percent from about 131,000 in 2009 to 176,000 in 2018, and to 227,000 in 2026 (see fig. 3). The 112,640 repetitive loss properties insured by NFIP as of January 2026 represented approximately 2.5 percent of the 4.58 million NFIP policies in force as of December 2025. From 1989 through 2025, FEMA mitigated 12,972 repetitive loss properties across all its grant programs.[11]

FEMA’s new pricing approach accounts for the risk of repetitive loss properties. Under this approach, NFIP policies for repetitive loss properties are subject to a premium surcharge if they have more than one loss on or after April 1, 2023. For instance, a single-family home located outside a leveed area in South Carolina with a premium of $1,507 and one loss since April 2023 would face an additional surcharge of $482 at the owners’ next renewal if they filed a second claim. The surcharge would increase to $964 if they filed a third claim.

Certain Actions Could Improve Use of Property Acquisitions by Addressing Key Challenges

While acquisitions offer benefits, they face significant challenges that can discourage communities and homeowners from participating. In prior work, we identified four major categories of challenges. We also identified options to improve property acquisitions—each with its own strengths and limitations—and recommended that FEMA determine whether and how to implement one or more of them. Additionally, we recommended that Congress provide direction or authority to FEMA to implement one or more of the options we identified.[12]

Length and complexity of the acquisition process. According to FEMA officials and stakeholders we previously interviewed, planning a project, applying for and receiving a grant, and then purchasing and demolishing homes is complex and typically takes at least 2 to 3 years, and often longer. According to a FEMA analysis, on average, states took 16 months after a disaster declaration to submit Hazard Mitigation Grant Program acquisition applications.[13] As of February 2026, FEMA had approved 82 acquisitions of properties affected by Hurricane Helene, which occurred in September 2024, according to the North Carolina Department of Public Safety. More than 575 additional acquisition applications had been submitted but not yet approved.

We recommended in September 2022 that FEMA collect property-level data on acquisition project milestones across its hazard mitigation assistance grant programs, including the dates when properties are purchased and demolished, and use this information to support its efforts to reduce the overall length of the property acquisition process.[14] In addition, one option for improvement we identified was creating a preapproval mechanism for certain properties so FEMA could approve acquisition applications more quickly after a flood, when homeowners may be more willing to sell. FEMA agreed with our recommendations and has begun to take steps to address them but had not fully implemented them as of February 2026.

Limited state and community capacity. The complexity of the acquisition process is particularly challenging for communities that lack dedicated grant managers or technical staff. Developing a benefit-cost analysis to meet cost-effectiveness requirements, navigating environmental and historic preservation reviews, and managing ongoing outreach to property owners place significant demands on local officials. States also face capacity constraints in supporting communities through this process. An option for improvement we identified was permitting certain local governments to apply directly for hazard mitigation funding or allowing homeowners to receive acquisition funding directly from NFIP as part of the claims process. Another option we identified was to directly fund additional state hazard mitigation staff to help states manage the grant process.

Financial challenges. The nonfederal cost share—typically 25 percent of project costs, though lower in some circumstances—can deter community and homeowner participation. Some communities cannot afford the cost share from their own revenues and must rely on homeowners to cover it, reducing the net proceeds homeowners receive. In some cases, homeowners may owe more on their mortgage than an acquisition would yield. Communities also face concerns about losing property tax revenue when acquired land is permanently removed from the tax rolls. An option for improvement we identified was to lower or eliminate the nonfederal cost share or standardize it across all mitigation grant programs.

Challenges from voluntary participation requirements. Property owners participate in acquisitions voluntarily. While this protects homeowner autonomy, it can lead to “checkerboarding,” where some properties in a neighborhood are acquired and demolished while others remain. This limits overall flood-risk reduction and can leave communities paying for services in thinly populated areas. An option we identified was to allow states and localities to use eminent domain to acquire high-risk properties in certain cases. However, several stakeholders and FEMA officials said mandatory acquisitions could face significant opposition from homeowners, communities, or states.

Targeting Mitigation Efforts to Properties Driving Premium Shortfall Could Help Address Fiscal Exposure and Affordability

NFIP represents a fiscal exposure to the federal government because FEMA is statutorily required to charge premium rates that do not fully reflect flood risk. Two general approaches could address this exposure: decrease costs or increase revenue.

Decreasing costs involves mitigating flood-prone properties, especially repetitive loss properties. For example, properties can be acquired or elevated, rather than generating repeated large claims. Mitigation can be costly, but for some properties, the benefits of reduced flood risk will outweigh the cost. Mitigation may also be a cost-effective option for properties for which full-risk premiums would be cost-prohibitive.

Increasing revenue would require addressing NFIP’s premium shortfall. As mentioned above, in April 2023, FEMA implemented a new pricing approach that more closely aligns premiums with risks.[15] Over time, this approach should address the premium shortfall. However, FEMA faces statutory limits on how much it can increase premiums each year. As a result, premiums for many properties do not fully reflect the risk of loss.

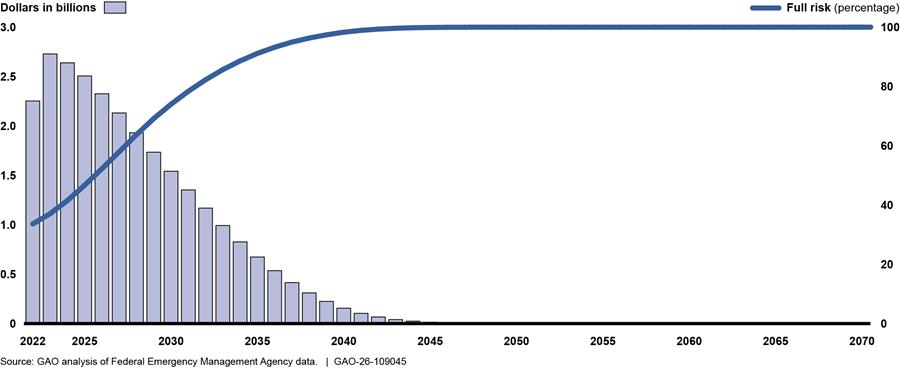

As we previously reported, as of December 2022, 66 percent of NFIP policies had discounted premiums. We estimated that it would take until 2037 for 95 percent of policies to reach their full-risk premium (see fig. 4). We calculated that this would result in a $2.7 billion premium shortfall in 2023 and a total premium shortfall of $26.7 billion over the period.

Figure 4: Estimated National Flood Insurance Program (NFIP) Premium Shortfall and Share of Policies at Full-Risk Premiums, by Year

By 2037, 95 percent of NFIP policies are expected to reach full-risk premiums.

To address this, in July 2023, we recommended that Congress authorize and fund means-based assistance for NFIP policyholders unable to afford their premiums rather than limiting how much premiums can increase each year. In doing so, Congress could shorten or eliminate the period of discounted premiums for those policyholders who do not qualify for assistance.[16] Among other things, this approach would make NFIP’s costs more transparent and would help address the premium shortfall. As of February 2026, Congress had not enacted legislation that would implement this recommendation.

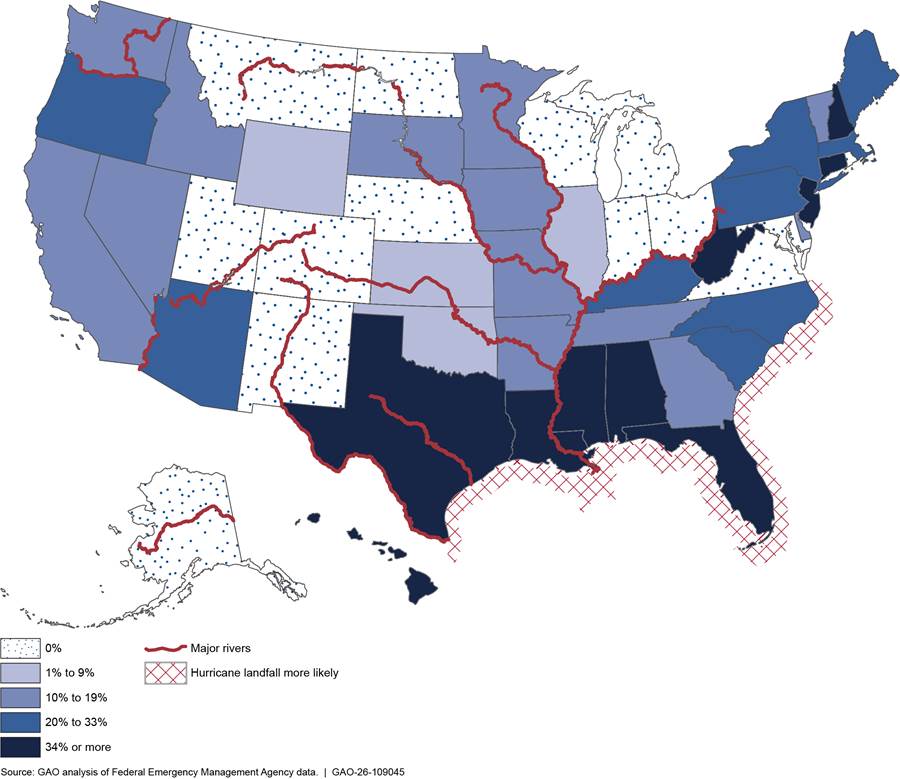

Targeting mitigation efforts to those properties contributing most to the premium shortfall (i.e., those with the most heavily discounted premiums) could help address NFIP’s fiscal exposure. These will be disproportionately repetitive loss properties, as they generally have greater risk and higher full-risk premiums. Mitigating these properties would also help NFIP achieve actuarial soundness sooner. States that require greater premium increases to achieve full-risk premiums, such as states along the Gulf Coast, might have more of such properties. Figure 5 illustrates the degree to which premiums would need to increase to reach full-risk premiums, as of December 2022.

Figure 5: Median Percent Change from December 2022 National Flood Insurance Program Premiums to Full-Risk Premiums, by State

States along the Gulf Coast and parts of the Northeast show the largest expected increases in premiums as policies transition to full-risk premiums.

Moreover, elevating, floodproofing, or relocating repetitive loss properties would reduce their risk of flooding and therefore their full-risk premiums, making these premiums more affordable. Specifically, these actions would reduce current premiums for policyholders already paying full-risk premiums now and reduce future premium increases for those currently paying discounted premiums.

In conclusion, mitigating flood risk for NFIP-insured properties can provide important benefits. We have made a number of recommendations to FEMA and Congress to improve the property acquisition process. Without addressing mitigation challenges, the number of repetitive loss properties will continue to grow, increasing costs to NFIP policyholders and federal taxpayers. However, mitigation alone will not resolve the program’s financial challenges. A more comprehensive approach that incorporates reforms to both mitigation processes and the program’s premium rates is needed. We have recommended several reforms that could help address the program’s fiscal exposure and affordability for policyholders.

Further, most U.S. homeowners lack the financial protection that a flood insurance policy provides. For this reason, we are currently conducting audit work on the nation’s flood insurance protection gap and options for addressing it. We expect to issue a report on this topic this summer.

Chairman Flood, Ranking Member Cleaver, this concludes my statement. I would be pleased to respond to any questions you may have.

GAO Contact and Staff Acknowledgments

If you or your staff have any questions about this testimony, please contact Alicia Puente Cackley, Director, Financial Markets and Community Investment, at CackleyA@gao.gov. Contact points for our Offices of Congressional Relations and Media Relations may be found on the last page of this statement. GAO staff who made key contributions to this testimony are Christopher Forys (Assistant Director), Matthew Levie (Analyst-in-Charge), Marc Molino, Jean Recklau, Jessica Sandler, and Jennifer Schwartz. Key contributors to the previous work discussed in this statement are listed in each of the cited reports.

This is a work of the U.S. government and is not subject to copyright protection in the United States. The published product may be reproduced and distributed in its entirety without further permission from GAO. However, because this work may contain copyrighted images or other material, permission from the copyright holder may be necessary if you wish to reproduce this material separately.

The Government Accountability Office, the audit, evaluation, and investigative arm of Congress, exists to support Congress in meeting its constitutional responsibilities and to help improve the performance and accountability of the federal government for the American people. GAO examines the use of public funds; evaluates federal programs and policies; and provides analyses, recommendations, and other assistance to help Congress make informed oversight, policy, and funding decisions. GAO’s commitment to good government is reflected in its core values of accountability, integrity, and reliability.

Obtaining Copies of GAO Reports and Testimony

The fastest and easiest way to obtain copies of GAO documents at no cost is through our website. Each weekday afternoon, GAO posts on its website newly released reports, testimony, and correspondence. You can also subscribe to GAO’s email updates to receive notification of newly posted products.

Order by Phone

The price of each GAO publication reflects GAO’s actual cost of production and distribution and depends on the number of pages in the publication and whether the publication is printed in color or black and white. Pricing and ordering information is posted on GAO’s website, https://www.gao.gov/ordering.htm.

Place orders by calling (202) 512-6000, toll free (866) 801-7077,

or

TDD (202) 512-2537.

Orders may be paid for using American Express, Discover Card, MasterCard, Visa, check, or money order. Call for additional information.

Connect with GAO

Connect with GAO on X,

LinkedIn, Instagram, and YouTube.

Subscribe to our Email Updates. Listen to our Podcasts.

Visit GAO on the web at https://www.gao.gov.

To Report Fraud, Waste, and Abuse in Federal Programs

Contact FraudNet:

Website: https://www.gao.gov/about/what-gao-does/fraudnet

Automated answering system: (800) 424-5454

Media Relations

Sarah Kaczmarek, Managing Director, Media@gao.gov

Congressional Relations

David A. Powner, Acting Managing Director, CongRel@gao.gov

General Inquiries

[1]See GAO, Flood Insurance: FEMA’s New Rate-Setting Methodology Improves Actuarial Soundness but Highlights Need for Broader Reform, GAO‑23‑105977 (Washington, D.C.: July 31, 2023). In 2023, we reported that FEMA had borrowed $36.5 billion from Treasury. Additionally, in 2025, FEMA borrowed an additional $2 billion from Treasury; see Federal Emergency Management Agency, “FEMA Exercises Borrowing Authority for National Flood Insurance Program,” press release HQ-25-28, February 10, 2025.

[2]See GAO, GAO’s High-Risk Program, GAO‑06‑497T (Washington, D.C.: Mar. 15, 2006); and High-Risk Series: Heightened Attention Could Save Billions More and Improve Government Efficiency and Effectiveness, GAO‑25‑107743 (Washington, D.C.: Feb. 25, 2025).

[3]GAO‑23‑105977; GAO, Flood Mitigation: Actions Needed to Improve Use of FEMA Property Acquisitions, GAO‑22‑106037 (Washington, D.C.: Sept. 13, 2022); National Flood Insurance Program: Fiscal Exposure Persists Despite Property Acquisitions, GAO‑20‑508 (Washington, D.C.: June 25, 2020); and Flood Insurance: Comprehensive Reform Could Improve Solvency and Enhance Resilience, GAO‑17‑425 (Washington, D.C.: Apr. 27, 2017). In these reports, we made nine recommendations to FEMA and eight to Congress. As of March 2026, FEMA has implemented four of these recommendations.

[4]See GAO‑23‑105977, GAO‑22‑106037, GAO‑20‑508, and GAO‑17‑425.

[5]Summary Judgment Order, State of Washington v. FEMA, 1:25-cv-12006 (D. Mass. Dec.11, 2025) (ECF No. 130).

[6]For analyses by grant program area, we treated projects funded through the Severe Repetitive Loss and Repetitive Flood Claims grant programs as being part of the Flood Mitigation Assistance program and projects funded through the Legislative Pre-Disaster Mitigation program as being part of the Pre-Disaster Mitigation program. For data on the number of flood-mitigated properties, we used the final number of properties mitigated by a project.

[7]FEMA defines base flood elevation as the computed elevation to which floodwater is anticipated to rise during a flood that has a 1 percent chance of being equaled or exceeded in any given year.

[8]Not all properties mitigated by FEMA were repetitive loss properties.

[9]FEMA has multiple definitions of repetitive loss properties. NFIP Repetitive Loss refers to an NFIP-insured structure that has incurred flood-related damage on two occasions during a 10-year period, each resulting in at least a $1,000 claim payment. Flood Mitigation Assistance Repetitive Loss refers to an NFIP-insured structure that (a) has incurred flood-related damage on two occasions in which the cost of repair, on average, equaled or exceeded 25 percent of the value of the structure at the time of each such flood event; and (b) at the time of the second incidence of flood-related damage, the flood insurance policy contained Increased Cost of Compliance coverage. Severe Repetitive Loss refers to an NFIP-insured structure that has incurred flood-related damage for which (a) four or more separate claims have been paid that exceeded $5,000 each and cumulatively exceeded $20,000; or (b) at least two separate claim payments have been made under such coverage, with the cumulative amount of such claims exceeding the fair market value of the insured structure.

[10]See GAO‑23‑105977. While these high-risk properties account for a disproportionate share of claims, they also likely pay higher premiums.

[11]The Hazard Mitigation Grant Program was created in 1989. Not all of the repetitive loss properties mitigated by FEMA were insured by NFIP.

[13]Based on FEMA’s analysis of Hazard Mitigation Grant Program data for 1998 to 2018.