Before the Committee on Education and Workforce, House of Representatives

For Release on Delivery Expected at 10:15 a.m. ET

United States Government Accountability Office

Opportunities Exist to Strengthen Accountability in Higher Education

A testimony before the Committee on Education and Workforce, House of Representatives

For more information, contact: Melissa Emrey-Arras at EmreyArrasM@gao.gov

What GAO Found

In March 2026, GAO reported on the impact of recent staffing reductions on the Department of Education’s oversight of its student loan servicers. In February 2025, Education stopped assessing student loan servicers on accuracy and call quality due to lack of staff capacity, according to Education officials. Prior to discontinuing these quarterly assessments, Education assessed servicers on these metrics for two quarters. These assessments were intended to measure whether servicers were (1) keeping complete and accurate records for borrowers and (2) providing borrowers good customer service.

The decision to stop these assessments occurred shortly after the administration began issuing presidential directives and guidance on downsizing the federal workforce in January 2025. Education reported that between January and December 2025, the number of staff at its Office of Federal Student Aid (FSA) decreased from 1,433 to 777.

Prior to FSA discontinuing this oversight, most servicers did not meet the performance standards for accuracy and faced corresponding financial penalties of about $850,000. FSA continued to assess servicer performance on the other performance metrics, which it characterized as less labor intensive to monitor.

In March 2026, GAO recommended that Education assess servicer accuracy and call quality. Education disagreed, stating that it uses other methods to assess servicer performance. GAO maintains these other methods are not effective substitutes. Moreover, GAO maintains these two assessments are important to protect borrowers and help the government avoid overpaying servicers for poor performance.

GAO also made other recommendations in prior work to help Education strengthen accountability. For example, implementing GAO’s 2019 recommendations to improve verification of borrower income and family size information could help reduce the risk of fraud and error in certain repayment plans and potentially save over $2 billion. Similarly, implementing GAO’s 2017 recommendation to update the formula for measuring colleges’ financial condition could help protect taxpayers against the financial risk of college closures. Finally, implementing GAO’s 2016 recommendation to improve tracking of borrower complaints could help Education better track trends and ensure the program effectively meets borrower needs. Education has taken some steps to address these recommendations; however, the agency needs to do more to implement them and strengthen accountability in higher education.

Why GAO Did This Study

In fiscal year 2025, about 10.5 million students received over $131 billion in federal student aid to help them pursue higher education. Education is responsible for maintaining accountability and protecting the federal investment in higher education. Education’s responsibilities include overseeing colleges, federal student aid, and the servicers that help administer the student loan program. Education’s responsibilities have grown substantially in recent years based on changes to the size and complexity of the federal student loan program, which now exceeds $1.6 trillion in outstanding loans.

This testimony summarizes the findings and recommendations from key GAO reports issued from 2016 through 2026. It includes recent work examining the impact of staffing reductions on Education’s oversight of student loan servicers (GAO-26-108534) and other prior work examining higher education accountability issues (GAO-19-347, GAO-17-555, and GAO-16-523). GAO also updated the status of related recommendations.

What GAO Recommends

GAO made 10 recommendations in the reports included in this statement. Education has not yet fully addressed seven of these recommendations. GAO will continue to monitor Education’s progress in implementing them.

Chairman Walberg, Ranking Member Scott, and Members of the Committee:

I am pleased to be here today to discuss the Department of Education’s role in ensuring accountability in higher education. In fiscal year 2025, 10.5 million students and their families received over $131 billion in assistance from Education to help them pursue higher education.[1] Education plays a key role in maintaining accountability and protecting the federal investment in higher education. Education’s responsibilities include overseeing colleges, federal student aid, and the servicers that help administer the student loan program.

My remarks today address recent work examining the impact of staffing reductions on Education’s oversight of its student loan servicers and key prior GAO recommendations that Education has yet to implement. My testimony is based on four prior reports issued from 2016 through 2026 and cited throughout this statement.[2] We used multiple methodologies to develop the findings, conclusions, and recommendations for these reports. A more detailed discussion of the objectives, scope, and methodologies, including our assessment of data reliability, is available in each report. In addition, we reviewed information we received in December 2025 and February and March 2026 from Education officials about steps they took to address our recommendations.[3]

The work upon which this statement is based was conducted in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

Background

Education’s Office of Federal Student Aid (FSA) is responsible for managing federal student aid programs authorized under Title IV of the Higher Education Act of 1965, as amended.[4] These federal student aid programs administered by FSA staff include federal grants, loans, and work study funds to support students attending more than 5,200 colleges. To safeguard these funds, Education monitors the financial health of these colleges on an annual basis to determine if they are financially responsible and able to fulfill their obligations.[5] Education uses a financial composite score to measure the financial health of colleges participating in federal student aid programs.

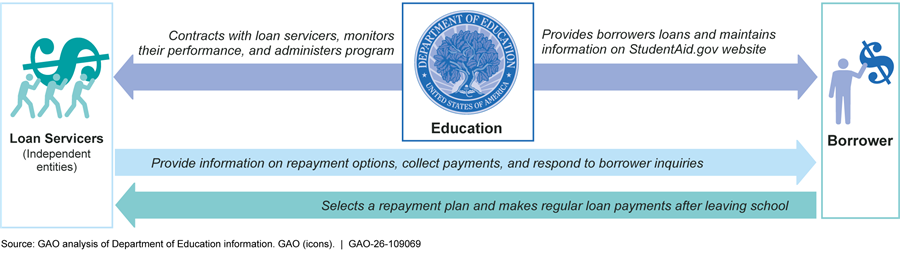

FSA’s responsibilities have grown substantially in recent years based on changes to the size and complexity of the federal student loan program, which now exceeds $1.6 trillion in outstanding loans. After a prospective borrower applies for and is awarded a federal loan, Education disburses it through the borrower’s college and assigns it to a loan servicer under contract with Education. These loan servicers are responsible for such activities as communicating with borrowers about the status of their loans, providing information about and enrolling borrowers in repayment plans, and collecting payments (see fig. 1). Once borrowers leave college, they are responsible for making payments directly to their assigned loan servicer.

A variety of repayment plans are available to eligible borrowers, including income-driven repayment (IDR) plans. IDR plans are designed to make loan repayment more manageable by basing monthly payment amounts on borrowers’ income and family size and forgiving any remaining balances at the end of the repayment period. To participate in an IDR plan, borrowers must submit an application to their loan servicer that, among other things, includes information about their income, marital status, and family size.

Over the next year, Education will implement various changes to federal student loan programs affecting millions of borrowers. Public Law 119-21—commonly known as the One Big Beautiful Bill Act (OBBBA)—includes provisions changing the repayment plans available to borrowers starting in July 2026.[6] For example, OBBBA sunsets existing IDR plans and creates a new Repayment Assistance Plan.[7]

Education Needs to Address Gaps in Servicer Oversight

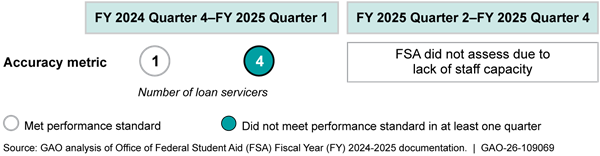

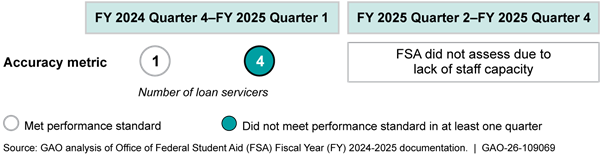

In March 2026, we reported on the impact of recent staffing reductions on Education’s oversight of its student loan servicers.[8] Specifically, we reported that in February 2025, FSA stopped assessing student loan servicers on accuracy and call quality due to lack of staff capacity, according to Education officials. The two metrics were intended to measure whether student loan servicers were (1) keeping complete and accurate records for borrowers and (2) providing borrowers good customer service.

The decision to stop assessing these performance metrics occurred shortly after the administration began issuing presidential directives and guidance on downsizing the federal workforce in January 2025. Education reported that between January and December 2025, the number of staff at FSA decreased from 1,433 to 777, a 46 percent reduction in personnel. FSA continued to assess servicer performance on the other performance metrics, which it characterized as less labor intensive to monitor.[9]

We reported that in total, four of the five servicers did not meet the performance standard for accuracy in at least one of the two quarters during which FSA previously assessed accuracy (see fig. 2). As a result, FSA levied financial penalties totaling $850,000 on the servicers for not meeting the performance standard.[10] Each servicer met its performance standard for call quality in those two quarters. However, servicers may have less incentive to maintain call quality if they are not assessed on it, putting borrowers at risk of receiving incorrect information.

Without this oversight, Education lacks reasonable assurance that borrower records are correct and that servicers are giving borrowers correct information. Inaccurate records can result in borrowers being billed for incorrect amounts or placed in the wrong repayment status. Additionally, borrowers need to be given correct information when they call for help. This is particularly important for the millions of borrowers affected by recent statutory changes to available repayment options.

To address these concerns, we recommended in March 2026 that Education assess servicer accuracy and call quality. Education disagreed with our recommendation, stating that it uses a variety of other methods to assess servicer performance. We maintain these methods are not effective substitutes and also maintain the importance of assessing servicer call quality and accuracy. Addressing gaps in servicer oversight will assist Education in carrying out its statutory responsibilities and also help the government avoid overpaying servicers for poor performance. We will continue to monitor Education’s efforts in this area.

Prior GAO Work Identified Additional Opportunities for Education to Strengthen Accountability

We previously reported on several areas in which Education could further strengthen its accountability efforts and made recommendations for improvement that remain open. These areas include:

· verification of borrower income and family size information on income-driven repayment applications;

· better measurement of colleges’ financial conditions;

· and streamlined tracking of borrower complaints.

Verification of Borrowers’ Income and Family Size for Income-Driven Repayment Plans. In our June 2019 report, we identified indicators of potential fraud or error in income and family size information for borrowers with approved IDR plans.[11] IDR plans base monthly payments on a borrower’s income and family size and offer forgiveness of any remaining balances at the end of the repayment period.

Findings included in our 2019 report indicated that some borrowers may have misrepresented or erroneously reported their income or family size.

· Zero income. About 95,100 IDR plans were held by borrowers who reported zero income yet potentially earned enough wages to make monthly student loan payments.[12] According to our analysis, about 32,600 of these plans (34 percent) were held by borrowers who had estimated annual wages of $45,000 or more, including some with estimated annual wages of $100,000 or more.

· Family size. About 40,900 IDR plans were approved based on family sizes of nine or more, which were atypical for IDR plans.[13] Almost 1,200 of these 40,900 plans were approved based on family sizes of 16 or more, including two plans for different borrowers that were approved using a family size of 93.

Because income and family size are used to determine IDR monthly payments, fraud or errors in this information could result in Education losing thousands of dollars of loan repayments per borrower each year and potentially increasing the ultimate cost of loan forgiveness.[14]

We reported that weaknesses in Education’s processes to verify borrowers’ income and family size information limited its ability to detect potential fraud or error in IDR plans. While borrowers applying for IDR plans must provide proof of taxable income, Education generally accepted borrower reports of zero income and borrower reports of family size without verification. In addition, Education had not systematically implemented other data analytic practices, such as using data it already had to detect anomalies.

Given these limitations, we recommended that Education obtain data to verify income information for borrowers who report zero income on IDR plan applications. We also recommended that Education implement data analytic practices and follow-up procedures to verify borrower reports of zero income and family size, respectively. Education generally agreed with these recommendations.

In response, Education has taken some steps to implement these recommendations. For example, to verify income information, Education established a direct data exchange with the Internal Revenue Service (IRS) and created a new IDR application in response to a law that granted statutory authority to access certain IRS data for the purpose of determining eligibility for IDR plans, among other things.[15]

Borrowers who apply for an IDR plan can now provide their consent for Education to automatically obtain their income information from their latest IRS tax return. Borrowers who provide such consent can have their IDR enrollment automatically recertified each year, rather than having to fill out an application every year to recertify.

However, borrowers can decline to provide this consent and instead self-certify that they have zero taxable income. We previously found there is a risk for potential fraud or error when borrowers self-certify they have zero taxable income. Education has reported that it does not use data to verify borrower reports of zero income. In addition, Education has not yet implemented specific data analytic practices or follow up procedures for verifying income for borrowers reporting zero income on their IDR applications. Similarly, Education has not yet implemented data analytic practices or follow-up procedures for verifying the family size entries provided by borrowers on their IDR applications. Taking these actions could help reduce the risk of using fraudulent or erroneous information to calculate IDR payments and save over $2 billion.[16] We will continue to monitor Education’s efforts.

Better Measurement of Colleges’ Financial Conditions. Our 2017 work found that Education should strengthen its efforts to hold colleges accountable for their financial condition to better protect taxpayers and students against the risk of college closure. Education uses a financial composite score to measure the financial health of colleges participating in federal student aid programs. The score can help Education identify schools that are struggling. If warranted, Education can require a letter of credit from at-risk colleges to help cover federal costs if the college later closes. Federal costs can be significant because eligible students may have their federal student loans discharged when a college closes. Closures can affect tens of thousands of students and result in hundreds of millions of dollars in financial losses for the federal government and taxpayers from unrepaid student loans.

However, we reported in 2017 that Education’s composite score has been an imprecise predictor of college closures.[17] Half of the colleges that closed in school years 2010-11 through 2015-16 received passing financial composite scores on their last assessment before they closed. We found the composite score’s inconsistent performance in identifying at-risk colleges was due in part to limitations of the underlying formula and the fact that it remained unchanged for more than 20 years.

We recommended in our 2017 report that Education update the composite score formula to better measure colleges’ financial conditions and capture financial risks.[18] Education has taken some steps to implement the recommendation; however, Education has yet to update the composite score to better measure colleges’ financial health by looking at issues such as liquidity and financial trends over time. We will continue to monitor Education’s efforts to fully implement this recommendation.

Streamlined Tracking of Borrower Complaints. Our May 2016 report identified a need for improvement regarding how Education tracks borrower complaints. We found that Education and the servicers used different systems to capture borrower complaints, which made it difficult to determine overall trends in borrower complaints.[19]

To strengthen oversight of federal student loans, we recommended in our 2016 report that Education ensure its complaint tracking system includes comprehensive and comparable information on the nature and status of borrower complaints made to both Education and the servicers. Education generally agreed with this recommendation.

In response, Education reported taking some steps to implement the recommendation. For example, Education requires that servicers provide monthly comprehensive lists of complaints, which Education can compile and use for review and trend analysis. However, Education does not have a unified complaint tracking system, and differences in complaint information maintained by Education and the servicers do not allow for easy comparison. To ensure the program effectively meets borrower needs, Education should collect comprehensive and comparable information on borrower complaints made to both Education and servicers. This would allow Education to track trends and better manage the program. We will continue to monitor Education’s efforts to fully address this recommendation.

In conclusion, the significant federal investment in higher education depends on the federal government maintaining a robust system of accountability to protect student loan borrowers and taxpayers. My statement has highlighted several actions Education could take to strengthen its accountability over student loans and colleges to protect borrowers and taxpayers. Fully implementing the recommendations discussed in this testimony would improve federal accountability, help borrowers, and potentially lead to financial savings for taxpayers.

Chairman Walberg, Ranking Member Scott, and Members of the Committee, this completes my prepared statement. I would be pleased to respond to any questions that you may have at this time.

GAO Contact and Staff Acknowledgments

If you or your staff have any questions about this testimony, please contact Melissa Emrey-Arras, Director of Education, Workforce, and Income Security, at emreyarrasm@gao.gov. Contact points for our Offices of Congressional Relations and Media Relations may be found on the last page of this statement. GAO staff who made key contributions to this testimony include Debra Prescott (Assistant Director), Kathryn O’Dea Lamas (Analyst-in-Charge), Charlotte Cable, Abby Marcus, Mimi Nguyen, and Lauren Shaman. Other staff who made key contributions to the reports cited in the testimony are identified in the source products.

This is a work of the U.S. government and is not subject to copyright protection in the United States. The published product may be reproduced and distributed in its entirety without further permission from GAO. However, because this work may contain copyrighted images or other material, permission from the copyright holder may be necessary if you wish to reproduce this material separately.

The Government Accountability Office, the audit, evaluation, and investigative arm of Congress, exists to support Congress in meeting its constitutional responsibilities and to help improve the performance and accountability of the federal government for the American people. GAO examines the use of public funds; evaluates federal programs and policies; and provides analyses, recommendations, and other assistance to help Congress make informed oversight, policy, and funding decisions. GAO’s commitment to good government is reflected in its core values of accountability, integrity, and reliability.

Obtaining Copies of GAO Reports and Testimony

The fastest and easiest way to obtain copies of GAO documents at no cost is through our website. Each weekday afternoon, GAO posts on its website newly released reports, testimony, and correspondence. You can also subscribe to GAO’s email updates to receive notification of newly posted products.

Order by Phone

The price of each GAO publication reflects GAO’s actual cost of production and distribution and depends on the number of pages in the publication and whether the publication is printed in color or black and white. Pricing and ordering information is posted on GAO’s website, https://www.gao.gov/ordering.htm.

Place orders by calling (202) 512-6000, toll free (866) 801-7077,

or

TDD (202) 512-2537.

Orders may be paid for using American Express, Discover Card, MasterCard, Visa, check, or money order. Call for additional information.

Connect with GAO

Connect with GAO on X,

LinkedIn, Instagram, and YouTube.

Subscribe to our Email Updates. Listen to our Podcasts.

Visit GAO on the web at https://www.gao.gov.

To Report Fraud, Waste, and Abuse in Federal Programs

Contact FraudNet:

Website: https://www.gao.gov/about/what-gao-does/fraudnet

Automated answering system: (800) 424-5454

Media Relations

Sarah Kaczmarek, Managing Director, Media@gao.gov

Congressional Relations

David A. Powner, Acting Managing Director, CongRel@gao.gov

General Inquiries

[1]This assistance is provided through financial aid programs authorized under Title IV of the Higher Education Act of 1965, as amended (Higher Education Act) (codified at 20 U.S.C. §§ 1070-1099d).

[2]GAO, Federal Student Loans: Education Needs to Address Gaps in Servicer Oversight, GAO‑26‑108534 (Washington, D.C.: March 5, 2026); GAO, Federal Student Loans: Education Needs to Verify Borrowers' Information for Income-Driven Repayment Plans, GAO‑19‑347 (Washington, D.C.: Jun 25, 2019); GAO, Higher Education: Education Should Address Oversight and Communication Gaps in Its Monitoring of the Financial Condition of Schools, GAO‑17‑555 (Washington D.C.: Aug. 21, 2017); and GAO, Federal Student Loans: Education Could Improve Direct Loan Program Customer Service and Oversight, GAO‑16‑523 (Washington, D. C.: May 16, 2016).

[3]We made a total of 10 recommendations to Education in the four reports included in this statement. Seven have yet to be addressed, six of which are discussed in the statement.

[4]For this statement, we define federal student aid programs as financial aid programs authorized under Title IV of the Higher Education Act.

[5]In order to participate in federal student aid programs, colleges must meet the Higher Education Act’s definition of an institution of higher education for purposes of student assistance programs and comply with other requirements, including those related to financial responsibility.

[6]An Act to provide for reconciliation pursuant to title II of H. Con. Res. 14, Pub. L. No. 119-21, § 82001, 139 Stat. 72, 337-48 (2025) (hereinafter OBBBA). The eliminated IDR plans include the Income-Contingent Repayment plan and the Pay as You Earn plan. These plans will be closed to new borrowers who take out loans on or after July 1, 2026, and will close for current borrowers—those who take out loans before July 1, 2026—on July 1, 2028. The Income-Based Repayment plan will also be closed to borrowers who take out loans on or after July 1, 2026, but will remain an option for loans taken out before then. In addition, in December 2025, Education announced a proposed joint settlement agreement that would end the Saving on a Valuable Education (SAVE) IDR plan, and on March 10, 2026, a federal court order granted the parties’ joint motion and vacated the SAVE plan.

[7]Payments on the Repayment Assistance Plan are tied to a borrower’s adjusted gross income, generally ranging from 1 to 10 percent depending on income, with forgiveness of remaining loan balances after 30 years of payments.

[9]The servicer contracts set performance standards for student loan servicers on six metrics: accuracy, call quality, call abandon rate, customer satisfaction, timeliness of completion of certain servicing tasks, and financial monitoring. In quarters 2 and 3 of fiscal year 2025, FSA continued to assess servicer performance for call abandon rate, timeliness of completion of certain servicing tasks, and financial monitoring. In the first three quarters of fiscal year 2025, FSA assessed servicers on the customer satisfaction metric but did not penalize servicers who were unable to meet the performance standard.

[10]FSA can enforce financial penalties associated with these metrics by withholding payment for part of a servicer’s bill for the final month of the quarter if it determines that the servicer was unable to reach its performance standards that quarter.

[12]This analysis was based on wage data from the National Directory of New Hires, a federal dataset that contains quarterly wage data for newly hired and existing employees.

[13]We considered IDR plans with family sizes of nine or more atypical because they comprised the top 1 percent of all family sizes in Education’s data at the time of our analysis.

[14]Where appropriate, we referred these results to Education for further investigation.

[15]Fostering Undergraduate Talent by Unlocking Resources for Education Act (FUTURE Act) Pub. L. No. 116-91, § 3, 133 Stat. 1189, 1189-92 (2019).

[16]Our recommendation for Education to obtain data to verify income information for borrowers reporting zero income on IDR plans was highlighted as having the potential to yield more than $2 billion in cost savings over 10 years in GAO’s review of federal efforts to reduce fragmentation, overlap, or duplication and achieve cost savings. GAO, 2025 Annual Report: Opportunities to Reduce Fragmentation, Overlap, and Duplication and Achieve an Additional One Hundred Billion Dollars or More in Future Financial Benefits, GAO‑25‑107604 (Washington, D.C.: May 13, 2025), 32.

[18]At the time the report was issued, Education generally disagreed with this recommendation and stated that the issues identified in our report did not necessarily mean that the composite score was an unreliable measure of colleges’ financial strength.