Before the Subcommittee on Government Operations, Committee on Oversight and Government Reform, House of Representatives

For Release on Delivery Expected at 2:00 p.m. ET

United States Government Accountability Office

A testimony before the Subcommittee on Government Operations, Committee on Oversight and Government Reform, House of Representatives

Contact: Asif Khan at khana@gao.gov, Vijay D’Souza at dsouzav@gao.gov, or Seto Bagdoyan at bagdoyans@gao.gov

What GAO Found

The Department of Defense (DOD) has never achieved an unmodified (“clean”) opinion on its financial statements. Over the last 30 years, DOD's auditors have issued thousands of notices of findings and recommendations and identified associated material weaknesses. In recent years, DOD and its components have made some progress in their remediation efforts by achieving important milestones. For example, the Marine Corps first achieved a clean audit opinion for fiscal year (FY) 2023 and has achieved a clean opinion each subsequent year. DOD’s financial statement audits and related efforts have also resulted in a range of benefits, including cost savings and avoidances, improvements to systems, and enhanced visibility over assets and inventory. These benefits, in turn, support improvements to operations, enhancements to DOD’s overall readiness, and warfighter priorities.

After decades of unauditable financial statements and 8 years of undergoing full scope financial audits, DOD is taking a revised approach to achieve its goal of a clean audit opinion by the end of 2028. DOD revised its approach after the DOD Office of Inspector General (OIG) issued a disclaimer of opinion on DOD’s financial statements for FY 2025, meaning that DOD was unable to provide sufficient evidence for DOD OIG to form an opinion. The revised approach includes centralizing coordination, placing increased emphasis on investing in technology (including artificial intelligence), and ensuring evidence supports material account balances, rather than relying on underlying internal controls for producing reliable data.

DOD’s Revised Approach to Achieving a Clean Audit Opinion by the End of 2028

|

Previous approach included |

Revised approach includes |

|

Decentralized response (bottom-up) |

Centralized coordination (top-down) |

|

Focus on correcting control deficiencies |

Focus on material line items |

|

Reliance on internal controls |

Manual testing of large samples and using artificial intelligence tools, as needed |

Source: GAO analysis of DOD documentation. | GAO-26-109115

DOD’s renewed focus on auditability is encouraging. However, questions remain about how the revised approach will address DOD’s other longstanding financial management issues and challenges. These include transparency and accountability in audit remediation (monitoring efforts to address overall audit findings); key IT and other material weaknesses; fraud risks; availability of trained financial management resources; and sustainability beyond 2028. These are important for DOD to consider in undertaking its revised approach.

Furthermore, this effort is likely to be labor and resource intensive and has important tradeoffs and risks. For example, under this approach, DOD would not prioritize remediating key internal control deficiencies for at least the next 2 years. Addressing these deficiencies is critical for producing reliable, useful, and timely financial information for decision-making. Stronger financial management could help DOD address critical issues such as unfunded priorities, ensuring it spends its funds appropriately, mitigating its fraud risks, and improving operations and readiness.

Why GAO Did This Study

DOD spends over $1 trillion annually to provide the military forces needed to deter war and to protect the security of the United States. DOD’s spending makes up almost half of the federal government’s total discretionary spending, and its physical assets make up about 82 percent of the federal government’s total physical assets. For FY 2027, the President has requested $1.5 trillion for DOD, a 44 percent increase from FY 2026.

DOD’s inability to achieve a clean audit opinion is one of three major impediments preventing GAO from expressing an audit opinion on the U.S. government’s consolidated financial statements. DOD obtaining a clean audit opinion is important for ensuring that its financial statements and underlying financial management information are reliable for decision-making. DOD’s financial management has been on GAO’s High-Risk List since 1995. In 2025, GAO expanded DOD’s financial management high-risk area to include fraud risk management.

This testimony discusses (1) DOD’s recent audit progress, realized benefits, and ongoing challenges; and (2) questions and important considerations as DOD implements its revised approach to achieving a clean audit opinion. This statement is primarily based on GAO’s related body of work from 2020 through 2026; details on GAO's methodology can be found in each of the reports cited in this statement.

Chairman Sessions, Ranking Member Mfume, and Members of the Subcommittee:

Thank you for the opportunity to discuss the Department of Defense’s (DOD) progress and challenges associated with its efforts to improve financial management, as well as questions and considerations associated with DOD’s recently announced revised approach to auditability.

DOD spends more than $1 trillion annually to provide the military forces needed to deter war and protect the security of the United States. DOD’s spending makes up almost half of the federal government’s total discretionary spending, and its physical assets make up about 82 percent of the federal government’s total physical assets. For fiscal year (FY) 2027, the President has requested $1.5 trillion for DOD, a 44 percent single-year increase in the department’s budget.

However, as of FY 2025, DOD is the only one of the 24 agencies subject to the Chief Financial Officers Act of 1990 (CFO Act) that has never obtained an unmodified (“clean”) audit opinion on its financial statements, primarily due to serious financial management and system weaknesses.[1]

Without having sound financial management practices and reliable, useful, and timely financial information routinely available, DOD risks being unable to effectively and efficiently manage its budgets and assets for the benefit of the warfighter and ensure accountability and stewardship over its extensive resources. DOD has established a goal for achieving a clean audit opinion by the end of 2028. This goal is consistent with a requirement in the National Defense Authorization Act for Fiscal Year 2024 that the department receive a clean audit opinion no later than December 31, 2028.[2]

In 1995, GAO designated DOD financial management as a high-risk area because of pervasive weaknesses in its financial management systems, business processes, internal controls, corrective action plans, acquisition management, and financial monitoring and reporting.[3] In 2025, we expanded DOD’s financial management high-risk area to include fraud risk management.[4] While DOD leadership over the years has demonstrated a commitment to improving its financial management, it has not yet demonstrated the same level of commitment to managing fraud risk.

Furthermore, the DOD Office of Inspector General (OIG) has reported that DOD’s efforts to improve and modernize its systems environment have not been complete or aggressive enough to ensure compliance in time to meet DOD’s 2028 deadline.[5] In addition, DOD business systems modernization, which includes financial and other systems that support business functions such as logistics and health care, has been on GAO’s High-Risk List since 1995.[6]

In early 2026, to help achieve its 2028 goal, DOD officials announced a revised approach to achieving a clean audit opinion. Officials stated that they will centralize coordination of the audit and remediation activities and align department-wide efforts to invest in technology and streamline financial reporting. This approach will prioritize supporting material line-item balances with evidence over resolving each material weakness and Notice of Findings and Recommendations (NFR).[7] While this approach may help DOD meet its goal of achieving a clean audit opinion by the end of 2028, it also raises questions about sustainability, transparency, and how and when DOD will address material weaknesses to ensure sound financial management. The department’s renewed focus on achieving a clean audit opinion is encouraging and could help it achieve a significant milestone. However, doing so without addressing these underlying control issues may leave DOD at continued risk of ineffective and inefficient use of its resources and limited in its ability to help the warfighter.

My testimony today provides information on this revised approach as well as DOD’s past and present efforts to improve its financial management and business practices and achieve auditability. Specifically, I will summarize our prior work addressing (1) DOD’s recent audit progress, realized benefits, and ongoing challenges; and (2) questions and important considerations as DOD implements its revised approach to achieving a clean audit opinion.

My remarks are primarily based on GAO work from 2020 through 2026, including several reports we have issued since April 2025, when we last testified before this committee on this issue.[8] This includes reports on the status of DOD audit remediation efforts, the auditability of DOD’s FY 2024 balance sheet, and the audit of the FY 2025 and FY 2024 U.S. government’s consolidated financial statements.[9] More detailed information on the scope and methodology of our prior work can be found within each specific report. This statement also includes information on our related ongoing work.

We conducted the work on which this testimony is based in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

Background

Congress Began Requiring Financial Statement Audits in 1994

We have long highlighted the importance of accurate financial information for the federal government. In February 1987, we stated that the accuracy and reliability of federal financial information was uncertain because most of the information was unaudited and agencies did not prepare financial statements.[10] We also noted that federal accounting systems were old, costly to operate and maintain, and did not produce the complete, consistent, reliable, and timely data needed for deciding policy or managing day-to-day operations. In addition, we noted that the federal government must develop a new financial management structure that encompasses strengthened accounting, auditing, and reporting and the comprehensive use of cost-based reporting.

In April 1994, we testified specifically on DOD’s efforts to improve accountability and controls over its operations.[11] We stated that expanding and making permanent the requirement for audited financial statements in DOD, as well as for agencies government-wide, is critical to ensuring basic accountability and making available the facts needed to run the government more efficiently.

Later that same year, Congress passed and the President signed the Government Management Reform Act of 1994 (GMRA), which required CFO Act agencies, including DOD, to prepare and submit audited financial statements, beginning with FY 1996.[12] It also included a provision for preparation and issuance of annual consolidated financial statements for the executive branch, which GAO must audit.[13]

As previously mentioned, as of FY 2025, DOD is the only one of the 24 agencies subject to the Chief Financial Officers Act of 1990 (CFO Act) that has never obtained a clean audit opinion on its financial statements. DOD’s inability to achieve a clean financial audit opinion is one of three major impediments that has continued to prevent GAO from expressing an audit opinion on the U.S. government’s consolidated financial statements since FY 1997.[14]

Federal Agencies Have Reported Benefits of Financial Statement Audits

Financial statement audits offer a disciplined approach to strengthening financial management and building public trust.[15] They often result in recommendations on how to improve the quality of day-to-day financial information. Reliable, useful, and timely financial and performance information is needed for managers to make sound decisions on the current results and future direction of vital federal programs and policies and effectively oversee taxpayer dollars.

In August 2020, we found that substantial benefits have been achieved as a result of agencies’ preparation and audit of financial statements, including:

· increased federal agency accountability to Congress and citizens, including independent assurance about the reliability of reported financial information;

· greater confidence to stakeholders (governance officials, taxpayers, consumers, or regulated entities) that federal funds are being properly accounted for and assets are properly safeguarded;

· an assessment of the reliability and effectiveness of systems and related internal controls, including identifying control deficiencies that could lead to fraud, waste, or abuse;

· a focus on information security; and

· early warnings of emerging financial management issues.[16]

Agencies across the federal government have reported examples of operational and other improvements as a result of financial statement audits, regardless of the resulting audit opinion. For example, as a result of our FY 2012 Internal Revenue Service (IRS) financial statement audit, we recommended that IRS, among other things, finalize implementation of an automated process for routinely updating date-of-death information and deceased status in its master files using Social Security Administration data.[17] IRS implemented these processes in 2013. The Treasury Inspector General for Tax Administration reported that as of October 2024, approximately 57 million deceased taxpayers had a lock on their account, preventing their personal information from being used to file a fraudulent tax return.[18] Additionally, the Department of Homeland Security, which achieved its first clean audit opinion on all its financial statements in FY 2013, reported in FY 2014 that it had made improvements in its program and payment procedures as well as its internal controls aimed at reducing improper payments.

Agencies Must Manage Fraud Risks

Ensuring the financial integrity of programs and expenditures requires effective fraud risk management. The federal government is a target for fraud. Fraud schemes are wide-ranging and occur when something of value is obtained through willful misrepresentation. For example, a DOD contracting company created another company that concealed the relationship and fraudulently marked up prices on items that were resold to the department, defrauding DOD of $48 million.[19] Fraud can have both financial and nonfinancial effects.

In July 2015, we issued A Framework for Managing Fraud Risks in Federal Programs (Fraud Risk Framework), which contains a comprehensive set of leading practices to guide agency managers in combating fraud in a strategic, risk-based way.[20] Specifically, the Fraud Risk Framework describes leading practices within four components: commit, assess, design and implement, and evaluate and adapt.

Ineffective fraud risk management compromises the financial integrity of DOD’s programs and trillion-dollar annual expenditures. We have highlighted the importance of managing fraud risks in ensuring the financial integrity of DOD programs and expenditures. For example, in 2025 we found that without robust fraud-risk management capacity, DOD cannot estimate the extent of fraud in its programs.[21] The lack of a robust fraud risk management program compounds DOD’s failure to establish a strong financial management internal control environment and increases opportunities for fraudulent actions against DOD’s vast resources.

DOD’s Efforts to Improve Its Financial Management and Undergo Its First Full Audit in 2018

DOD Has Undertaken Multiple Efforts to Improve Its Financial Management and Systems

For more than 30 years, DOD has made numerous organizational changes and initiated many efforts to modernize its business and financial systems. For example:

· In January 1991, DOD established the Defense Finance and Accounting Service to standardize, consolidate, modernize, and improve accounting and financial functions throughout the DOD.

· In November 1993, the National Defense Authorization Act for Fiscal Year 1994 established the DOD Comptroller (now the Under Secretary of Defense (Comptroller)) as the DOD Chief Financial Officer. Among other things, the Chief Financial Officer is responsible for developing and maintaining DOD financial systems that comply with applicable accounting principles, standards, and requirements.

· In 2005, DOD established the Financial Improvement and Audit Readiness Directorate to develop, manage, and implement a strategic approach for addressing the department’s financial management weaknesses, achieving auditability, and integrating those efforts with other improvement activities, such as its business system modernization efforts.

· In September 2021, DOD reorganized the roles and responsibilities associated with overseeing business and financial systems.[22]

Additionally, DOD has undertaken many improvements to its systems environment and oversight. For example, in July 2001, DOD initiated the Financial Management Modernization Program, which it intended to provide the department’s leaders with accurate and timely information through the development and implementation of a financial management enterprise architecture. More recently, in October 2021, the Marine Corps began using the Defense Agencies Initiative system as its core financial system, replacing the legacy Standard Accounting Budgeting and Reporting System.[23] As of November 2024, the Defense Agencies Initiative supported 30 components across DOD, including the Marine Corps.[24] Further, in January 2026, the Navy announced that it had successfully migrated all remaining commands to the Navy Enterprise Resource Planning system as part of its effort to streamline general ledger systems.

DOD Completed Its First Full Financial Statement Audit in 2018

Since FY 2018, DOD has been required by law to undergo annual, full-scope financial statement audits, which examine DOD’s reported financial information to determine whether DOD presents its financial statements fairly, in accordance with U.S. generally accepted accounting principles.[25] Prior to this requirement, the National Defense Authorization Act for FY 2010 mandated that DOD develop and maintain the Financial Improvement and Audit Readiness Plan.[26] This plan was required to include specific actions DOD planned to take to help correct deficiencies that impair DOD’s ability to prepare timely, reliable, and complete financial management information and ensure that its financial statements were validated and ready for audit by September 30, 2017. For the FY 2018 financial audit, the DOD OIG issued a disclaimer of opinion on the DOD consolidated financial statements, meaning DOD was unable to provide enough evidence (e.g., receipts, logs, or digital records) for auditors to validate information in its financial reports and form an opinion.

Across 24 stand-alone audits of DOD reporting entities in FY 2018, 16—including those associated with the military departments—received disclaimers of opinion.[27] In addition, six components received clean audit opinions and two received qualified opinions on their respective fiscal year 2018 financial statements.[28] The audits identified 20 DOD-wide material weaknesses and 2,595 NFRs, including for weak IT controls, insufficient controls to ensure the accuracy and completeness of property records, and incomplete universes of financial transactions.[29] Many of these previously identified deficiencies remain outstanding. For each fiscal year 2019 through 2025, the DOD OIG has issued a disclaimer of opinion on DOD’s financial statements.

DOD Has Made Progress in Improving Its Financial Management Practices, but Significant Challenges Remain

DOD’s Fiscal Year 2025 Audit Findings and Recent Audit Remediation Milestones

The DOD OIG issued a disclaimer of opinion on DOD’s financial statements in FY 2025 and identified 26 material weaknesses that have adversely affected DOD’s ability to prepare auditable financial statements. In doing so, the DOD OIG continued to highlight the role of financial systems in DOD’s annual audit findings. For example, in DOD’s FY 2025 Agency Financial Report (AFR), published in December 2025, the DOD OIG identified six IT-related material weaknesses.[30]

Additionally, according to DOD’s FY 2025 AFR, of the 28 DOD reporting entities, 11—including the Army and Air Force general funds and working capital funds and the Navy general fund—received disclaimers of opinion.[31] For both FY 2025 and 2024, 11 DOD reporting entities, including the Marine Corps, sustained a clean audit opinion.

Further, while DOD reduced its reported material weaknesses from 28 to 26 in FY 2025 by resolving the Security Assistance Accounts material weakness and consolidating the Beginning Balances material weakness, the department has made only limited progress in addressing its material weaknesses since 2021.[32]

Nevertheless, to DOD’s credit, the department and its components have achieved several recent remediation milestones on the path toward auditability. For example, in February 2026, the Marine Corps achieved its third consecutive clean audit opinion after receiving its first on its FY 2023 financial statements. In addition, the Defense Threat Reduction Agency and Defense Logistics Agency National Defense Stockpile Transaction Fund both achieved a clean opinion for the second consecutive year in FY 2025 after first achieving clean opinions in FY 2024.

In addition to the progress DOD has made in addressing the Security Assistance Accounts material weakness across the department, DOD has made improvements at the component level. For example, in FY 2025, the Army closed its component-level material weakness for Environmental and Disposal Liabilities-Asset Driven for its general fund and downgraded the Financial Reporting and Journal Entries material weakness for its working capital fund. Specifically, according to the Army’s FY 2025 AFR, the Army closed 23 of 24 auditor findings for the Environmental and Disposal Liabilities-Asset Driven material weakness in FY 2025 through the development of end-to-end business processes and controls and significantly improved policies and controls for manual journal entries.

However, according to the DOD OIG, the DOD reporting entities that received disclaimers of opinion on their FY 2025 financial statements, when combined, account for at least 43 percent of DOD’s total assets and at least 64 percent of DOD’s total budgetary resources and remain material to DOD-wide financial statements.

Benefits Associated with DOD Financial Statement Audits

The value of financial statement audits for DOD extends far beyond the audit opinion.

Cost savings and avoidances. DOD has identified cost savings and avoidances as a result of its financial statement audits and related remediation efforts, such as modernizing its financial systems.

For example, the Navy’s Operation Cattle Drive, which the Navy’s Financial Management Systems office and the office of the Navy Chief Information Officer lead, involves a multiphase approach to enable either the retirement or rationalization of obsolete, insecure, and unauditable IT systems.[33] Further, as part of each phase of Operation Cattle Drive, the Navy has identified and projected cost savings associated with decommissioning legacy systems. Over the first two phases, the Navy reported more than $100 million in potential savings from the shutdown of 11 legacy systems covering FY 2020 to 2026.

In addition, in 2023 and 2024, we estimated savings associated with DOD’s ability to identify and avoid making improper payments through its expanded use of its Advanced Data Analytics (Advana) system, a centralized data analytics platform used to link various DOD data sources. Specifically, we estimated that DOD saved at least $5.5 billion in avoided improper payments that it did not pay from 2020 through June 2023.

Visibility Over Assets and Inventory. DOD’s financial statement audits have identified billions of dollars’ worth of previously unaccounted for assets and inventory, including real property, equipment, and other materials. Based on our analysis of DOD information from fiscal years 2019 through 2023, DOD components reported identifying more than $16 billion worth of previously untracked assets and inventory during its financial statement audit inventory efforts.[34] The DOD OIG has also noted that accurate asset data enable informed decisions about maintenance, replacement, and disposal, leading to better resource allocation and long-term planning. This in turn improves operations and helps better ensure optimum use of resources to support warfighter priorities.

Additionally, in 2019, the DOD Under Secretary of Defense (Comptroller)/Chief Financial Officer and nominee for the position of Deputy Secretary of Defense described the benefits of the audit for inventory accuracy. For example, he reported that, in response to the agency-wide financial statement audit, the Defense Logistics Agency was able to fill approximately 59,000 backorders worth $287 million.[35]

Additional Operational Benefits. We have also identified additional operational benefits resulting from DOD’s financial statement audits, including improvements to policies and procedures and fraud risk management.[36] For example, in FY 2021, the Defense Contract Audit Agency reported that it improved internal controls relating to reviewing and handling potential travel card misuse issues to ensure appropriate actions are taken to address misuse or fraud and to prevent account delinquencies or suspension. Additionally, in FY 2021, the Navy reported that it provided guidance to and educated stakeholders on fraud awareness and fraud risk management leading practices. As a result, the Navy reported that participating organizations gained a better understanding of the Navy’s fraud risk management program, which promotes an antifraud culture aligned to Navy values.

Remaining DOD Audit Remediation Challenges

Despite demonstrated progress and realized benefits, DOD faces ongoing challenges in addressing longstanding issues impeding its auditability. These challenges include corrective action planning and addressing material weaknesses and associated NFRs. For example, in May 2023, we found that DOD plans, such as corrective action plans, lack details that are important to achieving a clean audit opinion.[37]

Material weaknesses have been a major obstacle to DOD achieving a clean audit opinion and limit the department’s ability to provide assurance of the effectiveness of the controls it has in place to support reliable financial reporting and compliance. For example, according to the DOD OIG, material weaknesses associated with IT continue to hinder audit progress for DOD and its component reporting entities. Specifically, the OIG reported that the lack of effective internal controls over financial management systems limits the auditor’s ability to rely on the information those systems produce and which support the DOD agencywide financial statements.[38] These weaknesses not only hinder audit progress but also increase the risk of DOD making ill-informed enterprise-wide business decisions, which could have a direct effect on DOD’s mission to ensure the security of our nation.

According to the House Committee on Oversight and Government Reform, Subcommittee on Government Operations’ DOD Financial Management Scorecard, the Army, Navy, Air Force, and Marine Corps each received an “F” in the Material Weakness category due to limited closure or downgrade of existing material weaknesses at the military service level in FY 2025. See Appendix I for the full scorecard.

Historically, DOD’s remediation of NFRs has played a significant role in its attempt to obtain a clean audit opinion and transform its financial management. Auditors provide direct, actionable feedback through NFRs that describe weaknesses in DOD’s business processes, IT systems, and financial reporting that require remediation. These NFRs include individual deficiencies or combinations of deficiencies making up material weaknesses.

Auditors closed 1,004 of the 2,972 NFRs open as of the end of FY 2024—including 596 associated with military service reporting entities—and issued or reissued 2,473 NFRs in FY 2025.[39] As the DOD OIG reported, each year auditors continue to identify new NFRs and reissue a significant number from prior years.[40] In the DOD Financial Management Scorecard, the four military services each received an “F” in the NFR category due to closing fewer than half of their FY 2024 NFRs during the FY 2025 audit (see app. I).

DOD has conferred with its auditors on the prioritization of NFRs to determine those DOD must remediate to get a material weakness downgrade or closure. To do so, it will be important for DOD to conduct and document root-cause analyses on identified deficiencies, then design and implement strategies to correct them.

DOD’s Revised Approach to Achieving a Clean Audit Opinion Raises Important Questions

DOD Has Outlined a Revised Approach to Achieving a Clean Audit Opinion

DOD officials have stated that the department is taking a revised approach to achieving a clean audit opinion on its financial statements by the end of 2028. DOD officials explained that its revised approach reflects a strategic shift away from resolving every material weakness and NFR and toward supporting material line items by focusing on validating account balances with documentation in an effort to accelerate DOD’s ability to achieve a clean audit opinion. DOD plans to rely on existing controls and systems to the extent feasible and then revert to manually supporting the balances in the financial statements while also using artificial intelligence tools where it can. Officials stated that the department is employing this approach with the goal of a clean audit opinion on the DOD Working Capital Fund in FY 2027, followed by a clean audit opinion on its DOD-wide financial statements in FY 2028.

This revised approach is characterized by several changes, including those highlighted in Table 1.

|

Previous approach included |

Revised approach includes |

|

Decentralized response (bottom-up) |

Centralized coordination (top-down) |

|

Focus on correcting control deficiencies |

Focus on material line items |

|

Reliance on internal controls |

Manual testing of large samples and using artificial intelligence tools, as needed |

Source: GAO analysis of DOD documentation. | GAO‑26‑109115

To centralize coordination, in March 2026, the Secretary of Defense directed the Under Secretary of Defense (Comptroller)/Chief Financial Officer to establish the Joint Task Force Audit to oversee audit preparation and response. The Secretary of Defense directed Joint Task Force Audit to:

1. obtain a clean audit opinion on the Consolidated Working Capital Fund and General Fund financial statements;

2. eliminate legacy financial systems; and

3. maximize use of artificial intelligence, automation, and data analytics/Advana to resolve audit issues.

The Secretary of Defense further directed military department secretaries and other heads of DOD components to partner closely with Joint Task Force Audit while designating assistant secretaries (financial management and comptroller) as audit leads. Relatedly, according to DOD officials, the department is planning for a unified, department-level approach to remediating audit findings rather than tracking audits at the component level.

Additionally, the department intends to invest in technology, such as artificial intelligence and robotic process automation tools, to automate matching and reconciliation of transactions and respond more quickly to document requests from auditors. The department hopes this approach will be faster and more efficient than, for example, searching manually for supporting documentation.

In March 2026, the department also announced plans to revise the presentation of its financial information to better align with its mission and streamline its financial reporting. For example, according to DOD officials, the department is planning to limit standalone financial statements to those required by statute or Office of Management and Budget guidance. For example, according to DOD officials, the department is planning FY 2027 standalone financial statements for the Air Force and Navy general funds and working capital funds, a consolidated Defense Working Capital Fund, and DOD’s agency-wide consolidated financial statements.[41] By comparison, in FY 2024, there were 28 DOD reporting entities that prepared and issued their own standalone financial statements.

In addition, the DOD OIG announced that it will contract with an independent public accountant firm to conduct the Defense Working Capital Fund and consolidated DOD-wide audits starting in FY 2027. In previous years, the DOD OIG performed an audit of agency-wide financial statements and oversaw independent public accountants’ audits of components’ financial statements. According to DOD OIG officials, the DOD OIG’s planned contracting approach is to also continue standalone financial statement audits of the Air Force, Navy, Marine Corps, Army Corps of Engineers – Civil Works, and Military Retirement Fund.

Questions to Consider for DOD’s Updated Audit Approach

DOD’s revised approach may help DOD meet its goal of achieving a clean audit opinion by the end of 2028, which would be a significant achievement. However, questions remain about this approach. We are raising these questions to highlight previously reported DOD financial management risks and present possible tradeoffs associated with the department’s revised approach toward a clean audit opinion. These questions should be addressed as DOD undertakes its revised approach toward achieving its goal of a clean audit opinion.

How will DOD’s revised approach contribute to transparency and accountability in audit remediation and financial reporting?

We have reported longstanding issues with transparency and accountability associated with DOD’s efforts to monitor progress and improve financial management. For instance, we have reported on DOD’s challenges in monitoring its financial management remediation activities. Specifically, in February 2025, we noted that DOD had previously prioritized financial statement audit remediation areas for addressing material weaknesses, including by developing roadmaps for how they can achieve clean audit opinions.[42] However, we found that these roadmaps have not contained sufficient details, such as interim milestone activities and dates to track progress, and that DOD has faced challenges meeting previously established target remediation dates.

The lack of sufficiently detailed roadmaps limits DOD’s transparency and accountability, as it limits the ability for DOD to track its detailed progress against actions that should be documented in its roadmaps. Additionally, the DOD OIG has reported on the department’s deficiencies in transparency and accountability. For example, in 2025, the DOD OIG reported that auditors found that the department did not maintain a complete population of transactions, preventing auditors from testing and verifying DOD’s reported dollar amounts.[43] In addition, with respect to access controls, the DOD OIG reported in 2025 that DOD had not fully implemented a uniform and reliable offboarding process, such as through an Identity, Credential, and Access Management (ICAM) solution, for terminated and separated employees. We have ongoing work in which we assess DOD’s efforts to develop a complete population of transactions and the status and implementation of the ICAM program across DOD.

DOD’s revised approach, which will result in the preparation and audit of fewer standalone financial statements, potentially risks limiting accountability and transparency. For example, DOD officials have stated that they plan to develop key performance indicators associated with the department’s revised approach. It will be important for the department to ensure that these indicators provide appropriate transparency and accountability for monitoring DOD’s efforts to achieve its auditability goal. In addition, DOD’s revised approach potentially risks limiting accountability and transparency for components that are planned for consolidation into the Defense Working Capital Fund in FY 2027. For example, the Army Working Capital Fund will no longer present standalone financial statements starting in FY 2027.

Further, as DOD shifts its focus to supporting material line items by focusing on validating balances with supporting documentation, it is undertaking an approach that may require substantive audit testing. This places DOD at risk of diverting resources away from addressing longstanding impediments, such as material weaknesses that impact transparency and accountability.

As a result, DOD may be at risk of continued limitations to the transparency and accountability of its financial management remediation efforts, even if DOD reaches its target audit opinion milestone.

How will DOD’s revised approach address key, longstanding impediments to auditability?

DOD’s financial auditors have identified material weaknesses that are major impediments to the department as it seeks to achieve a clean audit opinion and effective financial management. Specifically, in August 2024, the DOD OIG first identified 17 material weaknesses as scope-limiting (or pervasive), or weaknesses that do not allow auditors to perform sufficient procedures to draw a conclusion on the financial statements.[44]

The DOD OIG reported that these scope-limiting weaknesses are significant roadblocks to DOD’s auditability goals. For example, in August 2024, the DOD OIG identified information technology as a category of scope-limiting material weakness requiring collaboration between the Office of the Secretary of Defense, DOD components, and contractors. The DOD OIG reported that this was due to a complex systems environment that included outdated systems, 2,000 systems interfaces, and significant findings across most of its FY 2023 financial statement and performance audits.[45]

Additionally, the DOD OIG noted the Joint Strike Fighter program, the largest acquisition program ever undertaken by DOD, as a scope-limiting material weakness requiring collaboration. The DOD OIG reported that in FY 2023, DOD did not properly account for, manage, and report inventory for the Joint Strike Fighter program.

As of FY 2025, according to DOD, it has resolved just one of these 17 major impediments: the Security Assistance Accounts material weakness, as previously stated.[46]

DOD’s revised approach toward a clean audit opinion by the end of 2028 is likely to prioritize substantiating material line items at the expense of addressing the internal control deficiencies underlying these key material weaknesses. As a result, DOD would be deprioritizing remediating key internal control deficiencies for two or more years. This places DOD at increased risk of delaying its implementation of sustainable business processes, an effective internal control environment, and reliable information for its financial management operations.

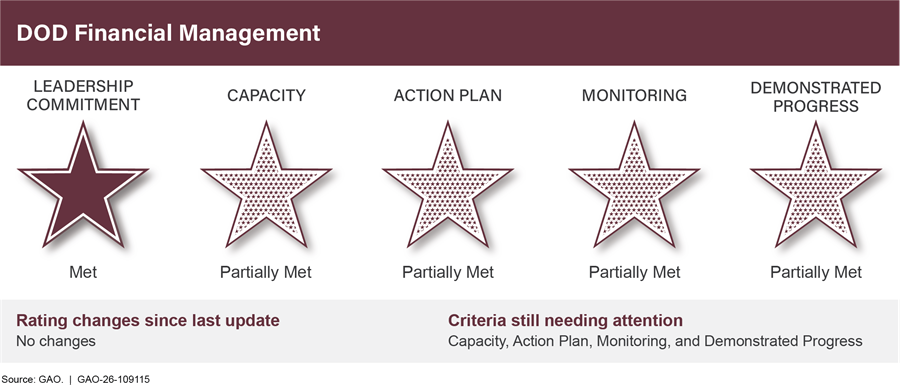

How will DOD’s revised actions contribute to DOD’s progress in addressing the DOD Financial Management High-Risk Area?

As discussed earlier in this statement, DOD financial management has been on our High-Risk List since 1995. This list highlights programs and operations across the federal government with serious vulnerabilities to fraud, waste, abuse, and mismanagement, or that are in need of transformation. We have reported that while DOD continues to take positive steps, it has not yet received a clean audit opinion on its annual department-wide financial statements because it has been unable to accurately account for and report on its spending or physical assets.[47] Figure 1 shows GAO’s February 2025 ratings for the DOD financial management high-risk area.

As discussed in our February 2025 report, DOD leadership continued its commitment to financial management improvements by, for example, adhering to the agency’s Financial Management Strategy, prioritizing audit remediation efforts, and continuing to phase out legacy systems while migrating to newer financial management systems.

However, we noted challenges DOD faces in managing its financial resources. For example, we found that DOD has not yet fully addressed key deficiencies we first identified in October 2020 pertaining to its corrective action plan process, such as ensuring the department performs and documents a root cause analysis. Under its planned revised approach, as noted, DOD plans to shift away from resolving every material weakness and NFR towards supporting material line items by focusing on validating account balances with supporting documentation. In doing so, DOD has indicated that its traditional approach of relying on internal controls for long-term success will not work in time to achieve a clean audit opinion in FY 2028. Nevertheless, DOD’s planned approach could continue to delay its development of root cause analyses and implementation of the corrective actions needed to achieve sound financial management practices and make progress on this high-risk area.

How will DOD’s revised approach affect its efforts to manage fraud risks?

An important component of the financial management high-risk area is fraud risk. DOD’s longstanding control weaknesses contribute to DOD’s susceptibility to fraud. The scope and scale of DOD’s financial activity make it inherently susceptible to fraud while the weak controls due to ineffective financial management processes and outdated financial systems make it easier for fraudsters to perpetrate fraud and conceal their fraudulent activities.

Among the agency-wide material weaknesses that the DOD OIG reported for FY 2025, access controls, segregation of duties, and accounts payable are examples of financial management weaknesses that also increase the risk of fraud, affecting DOD operations. Fraud risks in other areas of material weakness such as inventory and stockpile materials can affect warfighter readiness. For example, the DOD OIG reported that DOD could not substantiate the existence, completeness, and valuation of inventory and stockpile materials. Without the ability to confirm what inventory and stockpile materials it has—or should have—DOD is not in the position to readily detect if it had received such materials or if fraudsters had removed them from DOD possession.

In addition to these and other agency-wide material weaknesses the DOD OIG identified, we have also reported other challenges that could increase DOD’s fraud risk. For example, DOD lacks data on the number of and collective functions that contractors are performing.[48] This could allow for contractors to fraudulently bill or to not perform contracting functions.

While DOD has taken some actions to manage fraud risks, the lack of a robust fraud risk management program continues to pose challenges to the department’s internal control environment and the revised actions on auditability.

In June 2025, DOD issued the Fraud Risk Management Strategy and Guidance, which outlines roles and responsibilities and identifies actions for fraud risk assessments and related activities. However, it is unclear whether the organizational structure outlined in this strategy provides the necessary authority to design, oversee, and compel fraud risk management action across the department, including on data analytics. Such leadership to drive strategic fraud risk management actions is essential for the department to safeguard its vast resources while also acknowledging that DOD’s revised approach may pose additional fraud risks through pressure to cut corners or perverse incentives to comply with requirements to reach a clean audit opinion.

Both previously and under DOD’s revised approach to auditability, fraud risk management has not been on equal footing with financial management in terms of leadership attention to compel action across the department. Singular focus on auditability could pull attention further away from fraud risk management at a time of heightened risk.

In addition to fraud risks that may be exacerbated by the pressures of the revised audit approach, DOD’s increased budget also increases the risks for fraud. Significant funding increases from Public Law 119-21, commonly known as the One Big Beautiful Bill Act, as well as a requested budget increase for fiscal year 2027 provide further opportunities for fraud while pressures to expend funds quickly further compound already heightened procurement-related fraud risks. Such a fraud risk environment in the context of financial management material weaknesses strains support for the warfighter and increased military action around the world.

How will DOD acquire and organize the resources needed for this approach to achieve a clean audit opinion by the end of 2028?

The Marine Corps’ experience in working toward achieving a clean audit opinion suggests that DOD’s revised approach will need substantial resources. As previously noted, in February 2026, for the third consecutive year, the FY 2025 audit of the Marine Corps general fund financial statements resulted in a clean audit opinion. We have reported that the Marine Corps was able to obtain and sustain a clean audit opinion in FY 2023 and FY 2024 largely through a substantive-based audit approach and manual effort.[49] This resulted in an increase in detailed testing and required the Marine Corps to produce a large volume of information for auditors to test, which supported transactions, account balances, and other adjustments made while preparing financial statements. Specifically, the Marine Corps’ auditor noted that its substantive approach included more than 70 site visits. Additionally, auditors tested approximately 26 million assets, including extensive physical counts of military equipment, ammunition, and other property to obtain adequate audit evidence to support a clean opinion.

As stated, DOD intends to centralize the coordination of its audit plan and rely on existing controls and systems to the extent feasible. DOD also plans to use tools such as artificial intelligence to, for example, identify discrepancies and use substantive testing where necessary to validate balances. However, this revised approach places DOD and its auditors at risk of not being able to effectively scale and organize their resources to undergo substantive testing where necessary across the department. A key challenge facing the department is its size. According to Office of the Under Secretary of Defense (Comptroller) officials, the Marine Corps accounted for just over 1 percent of DOD’s total assets as of September 30, 2025. Additionally, high volumes of transactions for the Army, Navy, and Air Force could make it difficult to test transaction details and account balances at such a large scale. As a result, auditors risk not having sufficient trained financial management resources and not being able to obtain sufficient, appropriate evidence by testing assets and transactions when they are relying more on substantive procedures.

How will DOD ensure sustainability in its revised approach, including through remediation of internal control deficiencies, once it achieves a clean audit opinion?

We have previously noted that addressing financial statement audit findings has inherent benefits, including helping to identify vulnerabilities, improving operations and visibility over assets, producing cost savings, and enhancing DOD’s overall operational readiness and support for the warfighter. As such, it will be important for DOD to ensure the sustainability of its audit opinion through continued remediation efforts after it initially achieves a clean audit. Both the resources needed to sustain the opinion and the department’s ability to address its underlying internal control deficiencies will affect its sustainability. For example, in August 2024, the DOD OIG noted that longstanding IT challenges remain. These challenges prevent DOD from implementing efficient and effective financial management. They also inhibit progress toward receiving a clean audit opinion and implementing sustainable processes with effective internal controls.[50]

As it worked toward its first clean audit opinion, the Marine Corps underwent a single 2-year audit for its FY 2023 financial statements. According to DOD, this approach allowed the Marine Corps to invest significantly more time in executing corrective actions to address errors and inaccuracies in its financial data and records to allow the auditor to test transactions and balances. Nevertheless, this substantive audit approach was labor intensive for both the auditor and the Marine Corps, because the auditors were unable to rely on the Marine Corps’ internal controls over financial reporting. As previously noted, it is unclear whether or how successfully larger DOD entities could complete a successful financial audit while relying less on internal controls.

In addition, as noted, although the Marine Corps has achieved a clean audit opinion for three consecutive years, its auditors continue to report that the Marine Corps needs to address seven material weaknesses. These include three material weaknesses associated with its IT systems. It is important for the Marine Corps to address these material weaknesses to continue improving its financial management and operations.

According to DOD officials, FY 2026 is the beginning of a planned two-year cycle of regular auditor feedback and DOD remediation toward the department’s goal of a clean audit opinion on the new DOD-wide Working Capital Fund in FY 2027. Officials stated that this serves as a test run in advance of the department’s goal to achieve a clean audit opinion on its DOD-wide financial statements in FY 2028. Nevertheless, DOD’s planned approach presents the possible tradeoff that while the department works toward this goal, its efforts to implement sustainable processes with effective internal controls will be limited.

Like the Marine Corps, even after achieving a clean audit opinion, it will be important for DOD to continue taking steps to sustain a clean opinion and continue improving its financial management environment. However, without a demonstrated commitment to improving its internal controls and processes, DOD may be limited in its ability to realize important operational and other benefits.

DOD has acknowledged that achieving a clean audit opinion takes time, but also that a traditional approach of relying on internal controls for long-term success will not work in time to achieve a clean audit opinion by the end of 2028. Its proposed solution is one that, to DOD’s credit, could enable the department to achieve a significant milestone in its first clean audit opinion. However, the path to a clean audit opinion is likely to be labor and resource intensive for both the department and its auditors. This sets the stage for a sizable department-wide effort and potentially sizable associated risks if DOD is unable to leverage it to achieve its goal of a clean opinion.

In addition, as noted earlier, the President has requested about $1.5 trillion for DOD in FY 2027, a 44 percent single-year budget increase. DOD also expects to spend $1.7 billion in support of the department’s audit during FY 2027. The potential for rapid spending of these additional resources could stress already weak controls department-wide and exacerbate risks.

Addressing the previously noted questions is critical for producing reliable, useful, and timely financial information for decision making. Additionally, continuing remediation efforts can help increase the likelihood of DOD’s success in the short term and financial management sustainability in the long term while further assuring the public and Congress that DOD is an effective steward of taxpayer dollars. In addition, better oversight over the department’s resources could help it identify additional resources to address critical issues such as unfunded priorities.[51] We will continue to monitor the progress of DOD’s financial management improvement efforts.

Chairman Sessions, Ranking Member Mfume, and Members of the Subcommittee, this concludes my prepared statement. I would be pleased to respond to any questions you may have.

The Department of Defense (DOD) Financial Management Scorecard identifies grades for DOD’s efforts to improve financial and fraud risk management during fiscal year 2025. The Subcommittee on Government Operations, Committee on Oversight and Government Reform, House of Representatives, developed the scorecard with the assistance of GAO staff based on information that DOD and the DOD Office of Inspector General provided to GAO and publicly available DOD and DOD Office of Inspector General information.

In May 2026, Office of the Under Secretary of Defense (Comptroller) officials stated that the scorecard reflects legacy processes and does not reflect the department’s current priorities for achieving a clean audit opinion. This testimony statement discusses DOD’s revised approach to achieving a clean audit opinion.

May 13, 2026

|

|

|

Entity |

|||

|

Category |

Indicator |

Army |

Navy |

Air Force |

Marine Corps |

|

Financial Statement Reliability 20% |

Audit Resultsa |

D |

D |

D |

B |

|

Progress 40% |

NFR Closuresb 20% |

F |

F |

F |

F |

|

|

Material Weakness Downgrades 20% |

F |

F |

F |

F |

|

Planning 10% |

Financial Management Strategic Plansc |

A |

A |

A ⇧ |

A |

|

Oversight 10% |

Guidanced |

B ⇧ |

B |

B ⇧ |

B |

|

Financial Systems 20% |

Aging systemse 10% |

A |

B |

B ⇧ |

B ⇧ |

|

Systems compliance with financial management requirementsf 10% |

F |

F |

F |

F |

|

|

Overall Grade |

|

D |

D |

D |

C |

Source: Army, Navy, Air Force, and Marine Corps FY 2025 Agency Financial Reports and analysis of DOD information. | GAO‑26‑109115

aThis FY 2025 scorecard does not include a balance sheet auditability indicator or score. In April 2026, Office of the Under Secretary of Defense (Comptroller) officials stated that the Office of the Deputy Chief Financial Officer no longer applies the weighting and scoring methodology previously used to rank the auditability of DOD components, which included balance sheet auditability. As a result, the FY 2025 scorecard applies the additional 10% that was previously applied to balance sheet auditability to audit results.

bArmy, Navy, Air Force, and Marine Corps grades are based on February 2026 data from the DOD OIG Component Notice of Finding and Recommendation count.

cThe Marine Corps grade reflects the Department of the Navy’s Financial Management Strategic Plan.

dThe Marine Corps grade reflects the Department of the Navy’s guidance for initial approval and annual certification of business and financial systems.

eGrade is based on self-reported DOD data about systems relevant to internal controls over financial reporting.

fFinancial management requirements refer to the extent to which auditors report systems substantially comply with federal financial management system requirements, applicable federal accounting standards, and the United States Standard General Ledger at the transaction level.

Each entity was assigned an A-F grade for each indicator.

|

Category |

Weight |

Scoring Methodology |

|

Financial statement reliability: Audit results |

20% |

For all entities, the scoring methodology considers the annual financial statement audit results. Audit outcomes are converted to a letter grade using the following methodology: A = unmodified audit opinion with no material weaknesses and no instances of non-compliance with laws and regulations; B = unmodified audit opinion with material weaknesses and/or instances of non-compliance with laws and regulations; C = qualified audit opinion; D = disclaimer of opinion; and F = audit not conducted. Source: Military service agency financial reports. |

|

Progress: NFR closure rate |

20% |

For all entities, the scoring methodology considers the total count of notice of findings and recommendations (NFRs) from FY 2024 closed during the FY 2025 audit for both IT and financial NFRs. Closure percentages are converted to a letter grade using the following methodology: A = 80% and above; B = 70%-79%; C = 60-69%; D = 50-59%; F = 49% or less. Source: DOD Office of Inspector General component NFR count as of February 26, 2026. |

|

Material weakness |

20% |

For all entities, the scoring methodology considers the downgrade and/or the remediation of FY 2024 material weaknesses during the FY 2025 audit. A = 80% and above; B = 70%-79%; C = 60-69%; D = 50-59%; F = 49% or less. Source: Military service agency financial reports. |

|

Planning |

10% |

For all entities, the scoring methodology considers the contents of each entity’s financial management strategic plans. A baseline of 50 is awarded if the entity has a strategic plan, with additional points awarded if the plan and supporting documentation contain goals and objectives and examples of associated metrics, targets, and measures. A = 90% or greater, B = 80%-89%; C = 70-79%, D= 60-69%, F= 59% or below. The Navy and Marine Corps grades are the same because both entities fall under the Department of the Navy financial management strategic plan. Source: Military department financial management strategic plans and supporting documentation. |

|

Oversight |

10% |

For all entities, the scoring methodology considers the contents of each entity’s financial systems compliance guidance, based on the status of recommendations from GAO‑23‑104539. For the military services, a baseline of 50 is awarded if the entity has guidance, with additional points awarded if the guidance discusses the legislative requirements described in 10 U.S.C. § 2222. The Navy and Marine Corps grades are the same because both entities follow guidance issued by the Department of the Navy. A = 90% or greater, B = 80%-89%, C = 70%-79%, D = 60%-69%, F = 59% or below. No entity can receive higher than a B until the Department of Defense issues updated DOD level guidance that fully addresses the outstanding recommendations from GAO‑23‑104539 and updates its business enterprise architecture. Source: Military department guidance for 10 U.S.C. § 2222 compliance. |

|

Financial systems: Aging systems |

10% |

Each entity is assigned a grade based on the percentage of its existing systems that are less than 30 years old. A = 90% or greater, B = 80%-89%, C = 70%-79%, D = 60%-69%, F = 59% or below. In addition, the score considers changes in the total number of existing systems and changes in the ages of systems from year to year. Source: DOD provided data associated with systems relevant to the financial audit. |

|

System compliance with financial management requirements |

10% |

Each entity is assigned a grade based on the extent to which their agency financial reports state that their systems are substantially compliant with the three elements required by Section 803(a) of the Federal Financial Management Improvement Act of 1996. A baseline of 40 points is awarded if the entity has reported its compliance and 20 additional points awarded if the entity’s auditor reported compliance with each of the three elements. A = 90% or greater, B = 80%-89%, C = 70%-79%, D = 60%-69%, F = 59% or below. Source: Military service agency financial reports. |

|

Overall grade |

|

The overall letter grade for each entity is calculated using a weighted average of the above grades. Individual scores are initially assigned letter grades as described above. To assign overall grades, the letter grades are assigned numerical grades using the following methodology: A = 95; B = 85; C = 75; D = 65; and F = 55. The weighted average of these numerical grades are then used to develop the final overall letter grades. |

Source: Analysis of DOD information. | GAO‑26‑109115

Fraud Risk Management Component

|

Category |

Indicator |

DOD |

|

Fraud Risk Management |

Commit |

Da |

|

Assess |

Db ⇩ |

|

|

Design and Implement |

Dc |

|

|

Evaluate and Adapt |

Pendingd |

|

|

Overall Grade |

|

De |

Source: Analysis of DOD information. | GAO‑26‑109115

aIn June 2025, DOD issued an updated Fraud Risk Management Strategy and Guidance, which described main roles and responsibilities of DOD entities leading and implementing fraud risk management activities. This update is reflected in the numeric score supporting this letter grade, but does not change the grade overall.

bThis grade reflects deficiencies in the completeness and quality of fraud risk assessments provided to GAO as part of recommendation follow-up, including information from DOD stating that 15 reporting entities did not submit fraud risks in their assessments.

cAs the Design and Implement component of the Fraud Risk Framework is grounded in the actions under the Assess component, progress under this component is dependent on improvements in DOD fraud risk assessments, in terms of quality and number of entities participating. This grade is therefore consistent with Assess component scoring. Scoring methodology for this component changed from last year for more consistent alignment with the Fraud Risk Framework.

dThis is scored as pending because DOD has not yet significantly engaged in fraud risk management monitoring, evaluation, and adaptation activities. It will be scored when DOD begins to significantly execute these activities.

eThe overall grade does not include the evaluate and adapt indicator.

The categories outlined below in Table 4 are drawn from the GAO Fraud Risk Framework and align with the Framework’s four components and associated leading practices.

1. Commit to combating fraud by creating an organizational culture and structure conducive to fraud risk management (Commit)

2. Plan regular fraud risk assessments and assess risks to determine a fraud risk profile (Assess)

3. Design and implement a strategy with specific control activities to mitigate assessed fraud risks and collaborate to help ensure effective implementation (Design and Implement)

4. Evaluate outcomes using a risk-based approach and adapt activities to improve fraud risk management (Evaluate and Adapt)

Table 4: FY 2025 DOD Financial Management Scorecard Fraud Risk Management Component Scoring Methodology

DOD as an entity was assigned an A-F grade for each indicator.

|

Category |

Weight |

Scoring Methodology |

|

Commit |

⅓ |

The scoring methodology considers the actions of DOD leadership and DOD’s dedicated fraud risk management entity. A baseline of 50 is awarded if the component has a dedicated fraud risk management entity, with additional points awarded if the entity has defined responsibilities and the necessary authority to carry out fraud risk management activities, as well as if senior-level leadership demonstrates commitment to combating fraud and involves all levels of the agency in setting an antifraud tone, in alignment with GAO’s Fraud Risk Framework. A = 90% or greater, B = 80%-89%; C = 70%-79%, D=60%-69%, F=59% or below. |

|

Assess |

⅓ |

The scoring methodology considers the presence and quality of DOD’s fraud risk assessments and profiles. A baseline of 25 each is awarded if fraud risk assessments are conducted and fraud risk profiles are developed, respectively, with additional points awarded for higher quality assessments and profiles that align with GAO’s Fraud Risk Framework. A = 90% or greater, B = 80%-89%; C = 70%-79%, D=60%-69%, F=59% or below. |

|

Design and Implement |

⅓ |

The scoring methodology considers the contents of DOD’s antifraud strategy, the execution of its plan, and its collaboration with relevant stakeholders. A baseline of 25 is awarded if there is a developed and documented antifraud strategy (or strategies), grounded in a fraud risk assessment, with another 25 awarded if specific control practices have been designed and implemented to prevent, detect, and respond to fraud. Additional points are awarded for high-quality practices that align with GAO’s Fraud Risk Framework and for collaboration with internal and external stakeholders to prevent, detect, and respond to fraud. A = 90% or greater, B = 80%-89%; C = 70%-79%, D=60%-69%, F=59% or below. |

|

Evaluate and Adapt |

–a |

The scoring methodology considers how well DOD monitors and evaluates outcomes of its fraud risk management efforts and adapts as needed. A baseline of 25 is awarded if qualitative or quantitative data related to fraud risk management activities are collected where available, with another 25 points awarded if fraud risk management activities are adapted based on data evaluation. In the absence of sufficient data, points are awarded based on how well recommended leading practices for designing fraud risk management activities are followed. Additional points are awarded for high-quality practices that align with GAO’s Fraud Risk Framework and for communication of results to stakeholders. A = 90% or greater, B = 80%-89%; C = 70%-79%, D=60%-69%, F=59% or below. |

|

Overall grade |

|

The overall letter grade is calculated using an average of the above grades. Individual scores are initially assigned letter grades as described above. To assign the overall grade, the letter grades are assigned numerical grades using the following methodology: A = 95; B = 85; C = 75; D = 65; and F = 55. The average of these numerical grades is then used to develop the final overall letter grade. |

Source: Analysis of Fraud Risk Framework and DOD information. | GAO‑26‑109115

aDOD has not yet significantly engaged in fraud risk management monitoring, evaluation, and adaptation activities. This component will be scored when DOD begins to significantly execute these activities. Weights for all components will then become 25% each.

GAO Contacts

For further information on this testimony, please contact Asif A. Khan at

khana@gao.gov, Vijay A. D’Souza at dsouzav@gao.gov, or Seto

Bagdoyan at bagdoyans@gao.gov.

Staff Acknowledgments

Contact points for the individual reports are listed in the reports on GAO’s website. Contact points for our Offices of Congressional Relations and Media Relations may be found on the last page of this testimony. GAO staff who made key contributions to this testimony are Michael Holland (Assistant Director), Andrew Erickson (Analyst in Charge), Tulsi Bhojwani, Irina Carnevale, Heather Dunahoo, Benjamin Durfee, Scott Pettis, Edward Romesburg, and Andrew Weiss.

Financial Audit: FY 2025 and FY 2024 Consolidated Financial Statements of the U.S. Government. GAO‑26‑108073. (Washington, D.C.: Mar. 19, 2026).

DOD Financial Management: Insights into the Auditability of DOD’s Fiscal Year 2024 Balance Sheet. GAO‑25‑108052. (Washington, D.C.: Sept. 18, 2025).

DOD Financial Management: Status of Remediation Efforts to Meet Audit Mandate. GAO‑25‑107427. (Washington, D.C.: Sept. 16, 2025).

DOD Financial Management: Accelerated Timelines Needed to Address Longstanding Issues and Fraud Risk. GAO‑25‑108191. (Washington, D.C.: Apr. 29, 2025).

High-Risk Series: Heightened Attention Could Save Billions More and Improve Government Efficiency and Effectiveness. GAO‑25‑107743. (Washington, D.C.: Feb. 25, 2025).

DOD Financial Management: Action Needed to Enhance Workforce Planning. GAO‑25‑105286. (Washington, D.C.: Oct. 10, 2024).

DOD Financial Management: Benefits to Date of Financial Statements Audits and Need to Improve Financial Managements Systems. GAO‑24‑107593. (Washington, D.C.: Sept. 24, 2024).

DOD Fraud Risk Management: DOD Should Expeditiously and Effectively Implement Fraud Risk Management Leading Practices. GAO‑25‑108500. (Washington, D.C.: June 4, 2025).

Financial Management: DOD Has Identified Benefits of Financial Statement Audits and Could Expand Its Monitoring. GAO‑24‑106890. (Washington, D.C.: Sept. 24, 2024).

DOD Financial Management: Additional Steps Needed to Guide Future Systems Transitions. GAO‑24‑106313. (Washington, D.C., June 3, 2024).

DOD Fraud Risk Management: Enhanced Data Analytics Can Help Manage Fraud Risks. GAO‑24‑105358. (Washington, D.C.: Feb. 27, 2024).

DOD Financial Management: Efforts to Address Auditability and Systems Challenges Need to Continue. GAO‑23‑106941. (Washington, D.C.: July 13, 2023).

F-35 Program: DOD Needs Better Accountability for Global Spare Parts and Reporting of Losses Worth Millions. GAO‑23‑106098. (Washington, D.C.: May 23, 2023).

DOD Financial Management: Additional Actions Needed to Achieve a Clean Audit Opinion on DOD’s Financial Statements. GAO‑23‑105784. (Washington, D.C.: May 15, 2023).

Financial Management: DOD Needs to Improve System Oversight. GAO‑23‑104539. (Washington, D.C.: Mar. 7, 2023).

DOD Financial Management: Additional Actions Would Improve Reporting of Joint Strike Fighter Assets. GAO‑22‑105002. (Washington, D.C.: May 5, 2022).

DOD Fraud Risk Management: Actions Needed to Enhance Department-Wide Approach, Focusing on Procurement Fraud Risks. GAO‑21‑309. (Washington, D.C., Aug. 19, 2021).

Financial Management: DOD Needs to Implement Comprehensive Plans to Improve Its Systems Environment. GAO‑20‑252. (Washington, D.C.: Sept. 30, 2020).

Federal Financial Management: Substantial Progress Made since Enactment of the 1990 CFO Act; Refinements Would Yield Added Benefits. GAO‑20‑566. (Washington, D.C.: Aug. 6, 2020).

A Framework for Managing Fraud Risks in Federal Programs. GAO‑15‑593SP. (Washington, D.C.: July 28, 2015).

High-Risk Series: An Overview. GAO/HR‑95‑1. (Washington, D.C.: Feb. 1, 1995).

Financial Management: Financial Control and System Weaknesses Continue to Waste DOD Resources and Undermine Operations. GAO‑T‑AIMD/NSIAD‑94‑154. (Washington, DC.: Apr. 12, 1994).

Improving Government Management and Accountability. GAO/T‑AFMD‑87‑1. (Washington, D.C.: Feb. 18, 1987).

This is a work of the U.S. government and is not subject to copyright protection in the United States. The published product may be reproduced and distributed in its entirety without further permission from GAO. However, because this work may contain copyrighted images or other material, permission from the copyright holder may be necessary if you wish to reproduce this material separately.

The Government Accountability Office, the audit, evaluation, and investigative arm of Congress, exists to support Congress in meeting its constitutional responsibilities and to help improve the performance and accountability of the federal government for the American people. GAO examines the use of public funds; evaluates federal programs and policies; and provides analyses, recommendations, and other assistance to help Congress make informed oversight, policy, and funding decisions. GAO’s commitment to good government is reflected in its core values of accountability, integrity, and reliability.

Obtaining Copies of GAO Reports and Testimony

The fastest and easiest way to obtain copies of GAO documents at no cost is through our website. Each weekday afternoon, GAO posts on its website newly released reports, testimony, and correspondence. You can also subscribe to GAO’s email updates to receive notification of newly posted products.

Order by Phone

The price of each GAO publication reflects GAO’s actual cost of production and distribution and depends on the number of pages in the publication and whether the publication is printed in color or black and white. Pricing and ordering information is posted on GAO’s website, https://www.gao.gov/ordering.htm.

Place orders by calling (202) 512-6000, toll free (866) 801-7077,

or

TDD (202) 512-2537.

Orders may be paid for using American Express, Discover Card, MasterCard, Visa, check, or money order. Call for additional information.

Connect with GAO

Connect with GAO on X,

LinkedIn, Instagram, and YouTube.

Subscribe to our Email Updates. Listen to our Podcasts.

Visit GAO on the web at https://www.gao.gov.

To Report Fraud, Waste, and Abuse in Federal Programs

Contact FraudNet:

Website: https://www.gao.gov/about/what-gao-does/fraudnet

Automated answering system: (800) 424-5454

Media Relations

Sarah Kaczmarek, Managing Director, Media@gao.gov

Congressional Relations

David A. Powner, Acting Managing Director, CongRel@gao.gov

General Inquiries

[1]Pub. L. No. 101-576, 104 Stat. 2838. The list of agencies is codified at 31 U.S.C. § 901(b). These agencies are commonly referred to collectively as “CFO Act agencies.” An auditor expresses a clean opinion when the auditor concludes that the financial statements are presented fairly, in all material respects, in accordance with generally accepted accounting principles.

[2]National Defense Authorization Act for Fiscal Year 2024, Pub. L. No. 118-31, § 1005, 137 Stat. 136 379 (2023), reprinted at 10 U.S.C. § 240a note.

[3]GAO, High-Risk Series: An Overview, GAO/HR‑95‑1 (Washington, D.C.: Feb. 1, 1995). GAO’s High-Risk Series reporting identifies government operations that have serious vulnerabilities to fraud, waste, abuse, and mismanagement or that are in need of transformation.

[4]GAO, High-Risk Series: Heightened Attention Could Save Billions More and Improve Government Efficiency and Effectiveness, GAO‑25‑107743 (Washington, D.C.: Feb. 25, 2025).

[5]Department of Defense, Office of Inspector General, Audit of the DoD’s Plans to Address Longstanding Issues with Outdated Financial Management Systems, DODIG-2024-047 (Alexandria, Va.: Jan. 19, 2024).

[6]See GAO‑25‑107743 for the area’s current high-risk rating and GAO/HR‑95‑1 for when GAO first added it to the High-Risk List.

[7]An NFR includes one or more findings and discusses deficiencies that independent public accountants identified during their audit along with corresponding recommendations for addressing the deficiencies. DOD’s independent public accountants issue both financial and IT NFRs. A material weakness is a deficiency, or a combination of deficiencies, in internal control, such that there is a reasonable possibility that a material misstatement of the entity’s financial statements will not be prevented, or detected and corrected, on a timely basis. A line item describes an aggregation of account balances. See GAO, Financial Audit Manual Volume 1, GAO‑25‑107705 (Washington, D.C.: June 2025).

[8]GAO, DOD Financial Management: Accelerated Timelines Needed to Address Longstanding Issues and Fraud Risk, GAO‑25‑108191 (Washington, D.C.: Apr. 29, 2025).

[9]See, for example, GAO, DOD Financial Management: Status of Remediation Efforts to Meet Audit Mandate, GAO‑25‑107427 (Washington, D.C.: Sept. 16, 2025); DOD Financial Management: Insights into the Auditability of DOD’s Fiscal Year 2024 Balance Sheet, GAO‑25‑108052 (Washington, D.C.: Sept. 18, 2025); and Financial Audit: FY 2025 and FY 2024 Consolidated Financial Statements of the U.S. Government, GAO‑26‑108073 (Washington, D.C.: Mar. 19, 2026).

[10]GAO, Improving Government Management and Accountability, GAO/T‑AFMD‑87‑1 (Washington, D.C.: Feb. 18, 1987).

[11]GAO, Financial Management: Financial Control and System Weaknesses Continue to Waste DOD Resources and Undermine Operations, GAO/T-AIMD/NSIAD-94-154 (Washington, D.C.: Apr. 12, 1994).

[12]Pub. L. No. 103-356, § 405(a), 108 Stat. 3410, 3415, codified as amended at 31 U.S.C. § 3515.

[13]See provision codified at 31 U.S.C. § 331(e). The statements published by Treasury under this provision also include the legislative and judicial branches. See GAO, Financial Audit: FY 2025 and FY 2024 Consolidated Financial Statements of the U.S. Government, GAO‑26‑108073 (Washington, D.C.: Mar. 19, 2026).

[14]Since FY 1997, when the federal government began preparing consolidated financial statements, the other two primary impediments preventing us from rendering an audit opinion on the federal government’s consolidated financial statements have been (1) the federal government’s inability to adequately account for intragovernmental activity and balances between federal entities and (2) weaknesses in the federal government’s process for preparing the consolidated financial statements. See GAO‑26‑108073.

[15]See GAO‑26‑108073.

[16]GAO, Federal Financial Management: Substantial Progress Made since Enactment of the 1990 CFO Act; Refinements Would Yield Added Benefits, GAO‑20‑566 (Washington, D.C.: Aug. 6, 2020).

[17]GAO, Management Report: Improvements Are Needed to Enhance the Internal Revenue Service’s Internal Controls, GAO‑13‑420R (Washington, D.C.: May 13, 2013).

[18]Treasury Inspector General for Tax Administration, More Than 99 Percent of Deceased Taxpayers’ Accounts are Accurately Locked, 2026-400-004 (Washington, D.C.: Feb. 23, 2026).